Weekend News Lead by Yellen Deal – Talk

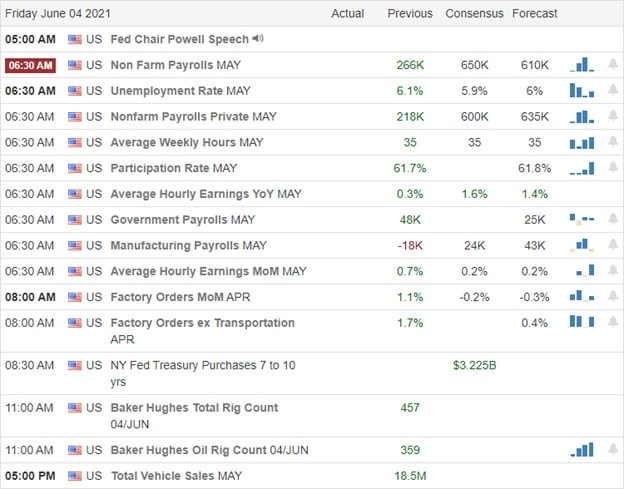

Markets gapped-up Friday as the May Payroll numbers seemed to hit the sweet spot. After that, stocks did a very slow, but steady climb into the last few minutes of the day. This left us with strong white candles in all 3 major indices. On the day, SPY gained 0.91%, DIA gained 0.54%, and QQQ gained 1.70%. The VXX fell over 5% to 33.39 and T2122 climbed back into the overbought territory at 87.62. 10-year bond yields fell to 1.557% and Oil (WTI) rose eight-tenths of a percent to $69.37/barrel.

The big weekend news was the G-7 (US, Canada, France, Germany, Italy, Japan, and the UK) agreeing to back a proposal for corporations to pay a minimum of “at least 15%” tax rate. In addition, the agreement included rules forcing companies with at least a 10% profit margin to pay taxes on at least 20% of the profits earned, in the country where the sale was made. This is a step toward preventing corporate shell games to avoid taxes by moving profits to low-tax haven countries. While these are major steps in the negotiations around digital economy taxation, these measures are still a long way from implementation, perhaps years. Getting sign-off by the G-20 (which includes China, India, Brazil, and Russia among others) is the next step. Key opponents of such digital tax rules include AAPL, GOOG, FB, etc. as well as countries whose business model is “low tax rates to draw in major companies.”

Sunday, Treasury Sec. Yellen told Bloomberg that the US has been fighting inflation and interest rates that are “too low” for a decade. So, she said that slightly higher interest rates would be a good thing, not a bad thing. She (former Fed Chair) said this is also the Fed’s point of view. So, she concluded that President Biden’s $4 trillion spending proposals (which would increase spending $400 billion per year) would be a positive for the economy and society in general.

Related to the virus, new US infections continue to fall. The totals rose to 34,210,782 confirmed cases and deaths are now at 612,366. However, the number of new cases is falling again and are back down to an average of 13,185 new cases per day (the lowest number since March 2020). Deaths are also falling, just more slowly, but are now down to 375 per day (again, the lowest number since March 2020).

Globally, the numbers rose to 1724,092,834 confirmed cases and the confirmed deaths are now at 3,745,093 deaths. The trends are better again as we have seen a slowing in the rate of increase now that India has passed its peaked. The world’s average new cases are falling quickly now, but remain at 418,913 new cases per day. Mortality, which lags, is also falling, but remains at 9,741 new deaths per day.

Overnight, Asian markets were mixed on very modest moves. Singapore (+0.79%), New Zealand (+0.53%), and India (+0.52%) led the gainers. Meanwhile, Malaysia (-0.76%), Hong Kong (-0.45%), and Taiwan (-0.37%) paced the losers. In Europe, markets are mostly green on modest moves so far today. The FTSE (+0.26%), DAX (+0.15%), and CAC (+0.31%) are typical of most of the continent’s exchanges. As of 7:30 am, US Futures are also pointing to a flat open. The DIA is implying a +0.09% open, the SPY implying a -0.04% open, and the QQQ implying a -0.13% open.

There is no major economic news scheduled for Monday. There are no major earnings reports on the day. The only major earnings reports on the day come after the closing bell when MRVL, REVG, SFIX, and MTN report

It seems that markets want to start the week off slow at the open Monday as the bulls chase the record highs, just points away. A lower than expected May Payrolls number Friday helped alleviate inflation fears, but only time will tell if that feeds over into Monday trading. The global tax news, while impactful on major multi-national tax dodgers, is still months or years away. So that proves Yellen’s chops on deal-making, but should not move markets in the short-term. So, just remember we are at the all-time highs, an area that has proved to be resistant before. However, the mid-term and short-term trends are bullish.

Follow the trend (the one appropriate for your trading horizon) and respect support and resistance levels (but don’t just assume they will hold). Beyond that, keep locking in profits as soon as you achieve your trade goals and maintain discipline by following your trading rules. Consistency is the key to long-term trading success. So, keep hitting those singles and doubles rather than swinging for the fence.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service