Earnings Stay Red Hot Despite Inflation

Thursday was another win for the bulls as we saw a small gap higher in the SPY and QQQ followed by the bulls controlling action. Large-cap indices were more undecided, both closing as Doji-type candles, but the QQQ was strong closing as a Marubozu (shaved head) candle at a new all-time high close. On the day, QQQ gained 0.66%, SPY gained 0.23%, and DIA gained 0.08%. The VXX rose slightly to 30.47 and T2122 fell back to the mid-range at 56.60. 10-year bond yields fell to 1.263% and Oil (WTI) gained almost 2% to $71.69/barrel.

During the day, major Internet outages (caused by AKAM equipment running in the AMZN AWS services) took many brokers and major business websites offline for over an hour. Interestingly, it was the big tech names, led by AMZN, that buoyed markets all day long. This was the third major Internet outage in the last few months.

After the close, INTC, TWTR, COFO, CE, and RHI all posted beats on both lines. VRSN beat on revenue but missed on earnings. And FE beat on earnings but missed on revenue. Overall, another very strong day of earnings reports. However, INTC also guided much lower for Q3 (forecasting 55% margins vs. 59.2% in Q2), citing supply constraints.

So far this morning, AXP, HON, RF, ROP, and SLB all reported beats on both lines. NEE beat on earnings but came up just short on revenue. However, KMB stood out as missing estimates on both lines. The bottom line is that earnings remain very strong this quarter. Despite all the talk of inflation, strong profit margins indicate that most of the major companies retain are able to pass along more than the cost increases they are experiencing.

Overnight, Asian markets were mixed. China paced the losses with Shenzhen down 1.53% and Hong Kong down 1.45%. Gains were modest with Japan (+0.58%) leading the way. In Europe, Markets are green across the board with the lone exception of Russia (-0.29%). The FTSE (+0.74%), DAX (+0.86%), and CAC (+0.95%) are typical for the continent, but a few of the smaller exchanges show gains over 1%. As of 7:30 am, US Futures are pointing to a green open. The DIA is implying a +0.48% open, the SPY implying a +0.42% open, and the QQQ implying a +0.39% open. The dollar is up this morning while 10-year bond yields are unchanged and commodities are generally lower early.

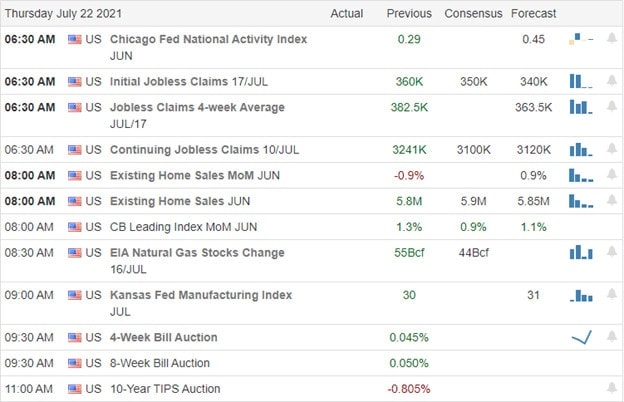

The major economic news scheduled for release on Friday is limited to Mfg. PMI and Services PMI (both at 9:45 am). The major earnings reports scheduled for the day include AIMC, AXP, GNTX, HON, KMB, NEE, RF. ROP, and SLB before the open. Then after the close, there are no scheduled reports.

Even with a brutal day to start the week, the bulls have clearly been in charge for the rest of the week. And it looks like we’ll see yet another green gap at the open today. So the momentum remains to the upside. However, we seem to be feeling undecided at least in the large-caps as the tech-led, lockdown-type market conditions are back in force. Be wary of “gap and fade” volatility. We are at or near all-time highs and there should be no hurry to chase the gap.

Manage your current positions first and take your time early. The first few minutes of the day is very likely not the key to your success, but it is the time of maximum volatility as overnight orders clear and the big boys start putting down their real bets. So, do not chase, stick with your trading rules, and maintain discipline. Success comes from your consistency. This means focusing on the process and repeatedly taking those singles and doubles. Limiting losses and taking profits when we get them is the key. Also, remember this is Friday. Don’t forget to pay yourself and prepare for the 2-day new cycle when markets are closed.

Ed

Swing Trade Ideas for your consideration and watchlist: TBIO, VLRS, AAP, BRKR, LSI, EW, SPLK. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service