Though the Dow continued to pull back yesterday, the bulls held strong defending recent lows and prevented a lower low’s technical damage. Though the S&P is now suggesting that Evergrande is likely to default is suspect we will ignore the possible U.S. impacts in favor of new record highs in the Nasdaq and SP-500. However, this push higher seems to be struggling with momentum, so make sure you have a plan if the tide starts to go out.

Overnight Asian markets were mostly lower, led by tech shares and developer concerns, as Hong Kong fell 1.29%. European markets trade flat and mixed, worrying about the implications of the slipping consumer sentiment due to inflation impacts. However, U.S. futures don’t appear to have any concerns pointing to a bullish open and possible new record high.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have 35 companies listed with a few unconfirmed. Notable reports include BABA, AMAT, ATKR, AHM, BECN, BRBR, BJ, CAL, CSIQ, FTCH, HP, INTU, JD, KSS, M, NUAN, PANW, WOOF, POST, ROST, VIPS, WWD, & WDAY.

News & Technicals’

Saule Omarova, President Joe Biden’s choice to lead one of the nation’s top bank regulators, is set for a fiery nomination hearing. While Republicans have warned against recommending a candidate whose academic work calls to “end banking as we know it,” skepticism has also come from a Democrat, Sen. Jon Tester. Just one Democratic defection on a committee vote to recommend her to the broader Senate would likely end her nomination to head the Office of the Comptroller of the Currency. “I know that difference between the job of an academic … and the job of a regulator, which is very circumscribed,” Omarova said in an interview Tuesday. N26′s American customers will no longer be able to use its app from Jan. 11, 2022. The Berlin-based fintech said the move aimed at shifting focus to its core European business. It’s a reminder of how difficult it has been for European fintech to expand its services in the U.S. Evergrande default is highly likely, according to the S&P. “We still believe an Evergrande default is highly likely,” S&P Global Rating analysts said in a report Thursday. The firm has lost the capacity to sell new homes, which means its main business model is effectively defunct,” the report said. Treasury Yields pulled back slightly yesterday and continued to relax in early Thursday trading. The 10-year declined to 1.5838%, and the 30-year fell to 1.9713%.

Though we pulled back in Dow, creating lower high patterns, the bulls held strong preventing a lower low from occurring and avoiding technical damage. Unfortunately, the Russell was not so lucky with the price creating a lower low while holding substantial price support and the bullish trend. Though there may be some reason for uncertainty in the industrials, the tech sector continues to surge within striking distance of a new record high and lifting the SP-500 as well. That said, overall market momentum is slowing as inflation impacts curtail consumer activities. With jobless claims and manufacturing data on the horizon, the bulls are back on the job in the premarket.

Stocks opened flat Wednesday and then meandered sideways with a slight bearish lean the rest of the day. This left us with a Bearish Harami Spinning Top in the SPY, a black follow-through (from the prior day’s Gravestone Doji) candle in the DIA, and a Doji in the QQQ. On the day, SPY lost 0.25%, DIA lost 0.57%, and QQQ gained 0.05%. The VXX gained 1.63% to 20.52 and T2122 fell to 31.91. 10-year bond yields fell to 1.587% and Oil (WTI) dropped 3.37% to $78.04/barrel.

As noted, Oil dropped hard on Wednesday. The primary reasons for this were concerns about oversupply expressed in reports from the Intl. Energy Agency and OPEC. Both organizations cited concerns over the reemergence of Covid in Europe. Not cited, but certainly looming, was the major pressure President Biden has been placed under to release oil from the US strategic reserve. At any rate, contrary to the concerns about oversupply, US Oil inventories fell 2.1 million barrels last week versus an analyst consensus expectation of an increase of 1.4 million barrels.

After hours, NVDA crushed earnings, easily beating the consensus forecast on both lines. The company reported an unexpected 55% growth in data center sales as the advent of Artificial Intelligence (which uses specialty cards NVDA makes) grows across the business world. In earnings news from this morning, retail continues to post strong earnings as M, KSS, JD, and BJ all handily beat on both lines of their reports. However, BABA missed on both lines, a victim of the Chinese government crackdown on their domestic online industry.

Bloomberg reports that JPM economists are now predicting the Fed will make its first interest rate hike in September 2022. Their report says the economy has changed in fundamental ways since the last time the Fed said outright it did not expect a rate hike until at least 2023. The author (Michael Feroli) says that the FOMC’s goal of full employment will be reached by the middle of 2022 and the bond-buying taper should be complete by June. At that point, according to Feroli, the Fed will have no choice but to raise rates in order to fight inflation. Among the other big bank economists, GS recently said they expect the first rate hike in July, but MS economists still expect rates to remain unchanged throughout all of 2022.

Overnight, Asian markets were mostly red. Hong Kong (-1.29%), Shenzhen (-0.90%), and India (-0.75%) paced the losses. Taiwan (+0.44%) and Thailand (+0.39%) were the only appreciable winners in the region Thursday. In Europe, markets are also mostly in the red at mid-day. The FTSE (-0.18%), DAX (+0.06%), and CAC (+0.08%) are the big dogs in the region, but many of the smaller exchanges are further south (such as Portugal -0.86%, Norway -0.76%, and Finland -0.69%) in early afternoon trading. As of 7:30 am, US Futures are pointing toward a green open. The DIA is implying a +0.10% open, the SPY implies a +0.25% open, and the QQQ is implying a +0.51% open at this hour.

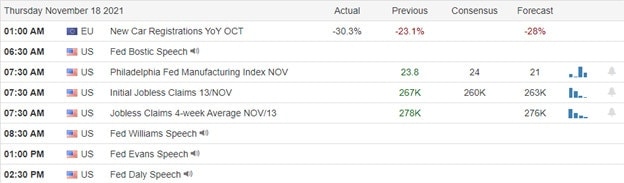

The major economic news scheduled for release Thursday is limited to Weekly Initial Jobless Claims and Philly Fed Mfg. Index (both at 8:30 am) as well as 3 Fed speakers (Bostic at 7:30 am, Williams at 9:30 am, and Daly at 3:30 pm). Major earnings reports scheduled for the day include BABA, BERY, BJ, CSIQ, PLCE, AVAL, JD, KSS, M, MMS, WOOF, and VIPS before the open. Then after the close, AMAT, BECN, CAL, FTCH, INTU, PANW, POST, ROST, UGI, WSM, WWD, and WDAY report.

With strong retail industry earnings continuing (signaling there is no let-up in spending by the consumer), the bulls have plenty of energy to help them run again this morning. Premarket prices are looking to challenge the all-time highs in the SPY and QQQ at the open, with the DIA lagging. Both the short and long-term trends are bullish in the SPY and QQQ and the short-term pullback continues in the DIA. However, that DIA longer-term trend remains bullish and even those mega-caps sit near all-time highs.

Watch your current positions before looking to add any new trades. Focus on your trade rules and on managing the things you can control. That should include consistently taking profits when you have them and moving your stops in your favor. Trade carefully and continue to think twice before holding through earnings…especially without a hedge.

Ed

Swing Trade Ideas for your consideration and watchlist: M, BBWI, AMD, LAC, MU. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although the tech enjoyed sustained buying yesterday, bullish momentum struggled with the Dow giving back most of its gains to leave behind an uncertain shooting star pattern. So the question for today can retail continue to inspire enough bullish momentum to keep the indexes rising? The rising dollar and increasing bond yields might signal a risk-off scenario, so keep a close eye on them if they continue marching higher.

Overnight Asian markets closed the day mostly lower, with only China posting a modest gain of 0.44%. European markets appear to have a more bullish outlook, but current gains hover near the flatline as they wait on earnings results. U.S. futures point to a flat to mixed open ahead of retail earnings and housing data.

Economic Calendar

Earnings Calendar

We have 44 companies listed on the earnings calendar with another day of focus on retail. Notable reports include TGT, NVDA, CRMT, BIDU, BBWI, BILI, CSCO, DSX, HI, IQ, LOW, MTOR, MBT, QUIK, SCVL, SONO, TTEK, TJX, UTI, VSCO, VINP, VTRU, XIM, ZTO.

News & Technicals’

Lowe’s beat expectations for fiscal third-quarter earnings, as it got a boost from online sales and business from home professionals. Despite analysts predicting a decline, the home improvement retailer’s same-store sales rose by 2.2% in the three months. In addition, CEO Marvin Ellison said sales to home pros, such as electricians and contractors, rose 16% in the third quarter. Amazon has told some customers that, from Jan. 19 onward, the company will no longer accept Visa credit cards issued in Britain. The e-commerce giant cited high fees charged by the payment processor. Visa said it was “very disappointed that Amazon is threatening to restrict consumer choice in the future.” The U.S. Justice Department will sell off $56 million worth of cryptocurrency it seized as part of a massive Ponzi scheme case against a man who promoted the crypto lending program BitConnect. The BitConnect scam has swindled thousands of people in the U.S. and abroad out of more than $2 billion worth of bitcoin. In September, the Securities and Exchange Commission sued BitConnect, its founder Satish Kumbhani and Glenn Arcaro, who was the lead promoter of BitConnect in the United States. Treasury yields dip just slightly in early Wednesday, with the 10-year trading at 1.625% and the 30-year edging lower to 2.0157%.

Substantial retail numbers brought out the bulls on Tuesday but curiously, the momentum struggled to stay on course into the close. While tech faired much better, the Dow gave up most of the day’s gains leaving behind the uncertainty of a shooting star pattern near price resistance. Perhaps the rising dollar with the ten, twenty, and thirty-year bonds rising are beginning to show signs of risk-off that I mentioned yesterday. However, with another round of retail with LOW and TGT this morning followed by results from NVDA after the bell, the bulls can reignite momentum. That said, I still believe it wise to wise to watch closely for a possible pullback to test support levels.

Markets opened flat Tuesday and rallied slowly until 2 pm on strong economic news. At that point, they slowly sold off into the close. This left us with Bullish Engulfing candles in the SPY and QQQ, both with upper wicks, and a Gravestone Doji-type candle in the DIA. On the day, SPY gained 0.39%, DIA gained 0.19%, and QQQ gained 0.73%. The VXX gained slightly to 20.19 and T2122 remains in the mid-range at 59.66. 10-year bond yields rose again to 1.644% and Oil (WTI) was flat at $80.78/barrel.

As mentioned, before the open, October Retail Sales and Exports came in much stronger than expected. Industrial Production also came in strong with only a slightly higher than expected increase in September Business Inventories. Socks rallied on this news. In related news, the retail sector got off to a good start on Q3 earnings as HD and WMT (both before the open) and then LZB (after close) all easily beat on both the revenue and earnings lines. The good news in retail reports has continued this morning with easy beats on both lines from BIDU, LOW, TGT, and TJX so far. (TGT beat revenue estimates by $2 billion for Q3.) LOW has also increased estimates for Q4 after posting 2.2% same-store sales growth (analysts had expected a 1.4% decline). The story seems to be that the consumer is in a “buy, buy, buy” mode.

During the day Tuesday, the electric vehicle industry made news as recent listing LCID passed F and GM in market capitalization. This resulted from a gain of almost 24% on the day. (LCID went public through a reverse merger and the stock has been parabolic since mid-October.) While not as ridiculously high as TSLA (over $1.2 trillion), the $89 billion market value tops rival NIO ($71 billion). LCID announced Monday evening a sizable increase in purchase reservations (17,000 now vs. 13,000 in Q3). They also announced it has a 20,000-vehicle production target for 2022, which would amount to approximately $2.2 billion in revenue.

Tuesday evening Treasury Sec. Yellen sent a letter to Speaker of the House Pelosi saying that she now estimates the US will hit its debt limit on Dec. 15. This is nearly two weeks later than the forecast made in October (Dec. 3), when the decision to suspend the debt ceiling was pushed back to December. The reason cited for the change of date is that the $1 trillion Infrastructure Law has funded some programs at a lower level than originally expected and slightly reduced spending. The increase in the debt limit has been tied to President Biden’s (and Democrats) Social Spending bill. The House is expected to vote on the Social Spending Bill this week and the Senate will take up the bill after returning from the Thanksgiving recess (about Nov. 29).

Overnight, Asian markets were mixed. South Korea (-1.16%) was an outlier as Australia (-0.68%), India (-0.56%), and Japan (-0.40%) were really the leaders to the downside. Meanwhile, Shenzhen (+0.67%), Shanghai (+0.44%), and Taiwan (+0.40%) led to the upside. In Europe, markets are also mixed, but on smaller moves as of mid-day. The FTSE (-0.33%), DAX (+0.12%), and CAC (+0.07%) are typical of the continent in early afternoon trading. As of 7:30 am, US Futures are pointing toward a mixed and flat open. The DIA is implying a -0.06% open, the SPY is implying an unchanged open, and the QQQ implies a +0.14% open at this hour. 10-year bond rates are unchanged and Oil (WTI) is down seven-tenths of a percent in early trading.

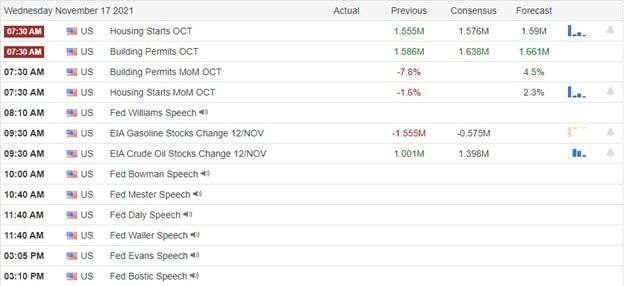

The major economic news scheduled for release Wednesday includes Oct. Building Permits and Oct. Housing Starts (both at 8:30 am), Crude Oil Inventories (10:30 am), and a slew of Fed speakers (Williams at 9:10 am, Bowman at 11 am, Waller at 12:40 pm, Daly at 12:40 pm, and Bostic at 4:10 pm). Major earnings reports scheduled for the day include BIDU, BILI, BV, IQ, LOW, MTOR, TGT, TJX, and ZIM before the open. Then after the close, BBWI, CSCO, CPRT, HI, YY, NVDA, TTEK, VSCO, and ZTO report.

Mortgage rates have continued to spike in the last week and as a result, refinance demand was down again, this time down 5% on the week. The less rate-sensitive new home purchase mortgage applications rose 2% week-on-week. Still, the great earnings out of the Retail Industry is likely to be the driver for markets early. Remember that the short-term trend is now bullish in the SPY and QQQ and the pullback trend is being challenged in the DIA. However, that longer-term strong bullish trend remains in place and we sit near all-time highs.

Watch your current positions before looking to add any new trades. Focus on your trade rules and on managing the things you can control. That should include consistently taking profits when you have them and moving your stops in your favor. Trade carefully and continue to think twice before holding through earnings…especially without a hedge.

Ed

Swing Trade Ideas for your consideration and watchlist: RMO, PLUG, NCTY, AEM, BA, CHPT. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With the uncertainty of retail sales numbers out this morning, the market struggled to find direction yesterday. The pop and drop pattern left behind would raise the possibility of a lower high at resistance if the bears were to happen to find some inspiration. However, with analysts suggesting a solid retail sales number is likely yesterday may prove only to be a rest before stretching to new highs. That said, anything is possible, and with earnings, inspiration to fuel the bulls market momentum could suffer.

Asian markets traded mixed during the night as the investors reacted to Biden-Xi talks with China selling slightly and Hong Kong surged higher. Across the pond, European markets sport modest gains across the board. U.S. futures began the morning in the red, but the bulls went to work pumping the premarket, which has become all too typical of late. Of course, anything is possible with the dollar showing strength, so buckle up the ride is about to begin.

Economic Calendar

Earnings Calendar

We have a much lighter day on the earnings calendar with just 44 companies listed, and several are unconfirmed. Notable reports include HD, ARMK, DLB, DAVA, AQUA, JMIA, LZB, NTES, SE, SBLK, STNE, TDG, VREX, WMT, ZENV, ZEPP.

News & Technicals’

October retail sales are expected to increase by 1.5%, boosted by early holiday shopping and higher gasoline prices. Economists say the report will be essential to examine whether consumers are willing to spend, even as sentiment has weakened. In addition, the report should show that the effects of the Covid delta variant are fading, as parts of the economy are rebounding. Home Depot topped Wall Street’s estimates for its third-quarter earnings and revenue. Consumers were spending more when they visited, raising the average ticket by 12.9% to $82.38. President Joe Biden signed the more than $1 trillion bipartisan infrastructure plan into law Monday. The plan will put $550 billion in new money into transportation, broadband, and utilities. In addition, Biden made a case for Democrats’ $1.75 trillion proposals to invest in the social safety net and climate policy. Finally, Tesla CEO Elon Musk faces a potential tax bill of more than $10 billion on stock options granted in 2012. Musk started exercising the options Monday, exercising $2.5 billion in shares and selling $1.1 billion of those exercised options to pay the taxes. But he continued to sell the additional stock, and it’s likely those sales were unrelated to the stock option exercises he must complete by August. This means future stock sales are likely. Treasury yield fell in early Tuesday trading, with the 10-year slipping to 1.6094% and the 30 pulling back to 1.9790%.

The indexes struggled for direction yesterday, challenged by overhead resistance and facing the uncertainty of retail sales figures coming out before the bell this morning. We will also hear from HD and WMT before the bell, the only likely market-moving earnings reports today. Yesterday’s pop and drop in all four indexes set up possible lower highs, but with economists suggesting a solid retail sales number, it could be nothing more than a rest before reaching out for more new records. However, with the decline in earnings inspiration and seeing a rising dollar, there is a concern of fading momentum and a possible risk-off scenario forming. As a result, a noticeable shift of energy into traditional defensive sector stocks, hinting at a possible rotation toward safety. Stay with the overall trend but never forget how elevated this market has become. A longer-term consolidation or a pullback is not out of the question, so have a plan to protect your capital because it can begin with breakneck speed!

The worst consumer sentiment reading in more than ten years didn’t dissuade the bulls at all as they worked a nice Friday rally. Retail will be in focus this week, with earnings from WMT, TGT, and HD, as well as last month’s retail sales figures coming our way Tuesday morning. It will be interesting to see if inflation and supply chain issues hampered the early holiday sales events. With consumer debt hitting record highs, my guess is no, but we will soon find out. Although the indexes remain very elevated, stay with the trend because the bulls seem to have no inflation concerns and want the party to continue.

Overnight Asian markets closed with modest gains through China fell slightly even as their retail sales topped expectations. European markets currently trade with modest gains and losses, as if searching for inspiration. However, U.S. futures point to a bullish open, with the Dow suggesting a 100 point gap. Nevertheless, with new price resistance above, don’t rule out the possibility of a lower high or even a pop and drop pattern to occur if the bears find a reason to fight.

Economic Calendar

Earnings Calendar

We have a busy day on the Monday earnings calendar with nearly 300 companies listed, but many of them unconfirmed. Notable reports include AAP, AND, AXON, SCPR, IBIO, JJSF, LCID, MGIC, OTLY, PLBY, RXT, STAF, COOK, TSN, WMG, STAF, COOK, TSN, WMG, XSPA.

News & Technicals’

Consumers will be a big focus for markets in the week ahead, with government retail sales data Tuesday and earnings from Walmart, Target, and Home Depot, among others. In addition, investors are watching the meeting between President Joe Biden and China President Xi Jinping Monday night for signs of any warming of relations on trade and other issues. According to contracts signed by four states, Apple requires states to maintain the systems needed to issue and service credentials at taxpayer expense. The agreement, obtained through public record requests from CNBC and other sources, mainly portrays Apple as having a high degree of control over the government agencies responsible for issuing identification cards. Apple has “sole discretion” for critical aspects of the program. Last week, the European Commission, the executive arm of the EU, projected a GDP rise of 5% for both the EU and the euro area this year. Some EU nations have started to see a high number of Covid-19 infections recently, mainly in countries where vaccination rates are still relatively low. Austria and the Netherlands have imposed new social restrictions in the last few days. Treasury yields look lower this morning, with the 10-year falling to 1.546% and the 30-year dipping to 1.9232% in early morning trading.

The indexes enjoyed a Friday rally choosing to ignore the worst consumer sentiment reading in more than ten years. However, the VIX declined, and big tech rallied strongly to end a volatile week of price action. This week we have a big focus on retail with earnings from WMT, TGT, and HD with a reading on Retail Sales figures Tuesday morning. The SP-500 P/E Ratio eased slightly with last week’s selling but remained strongly overvalued at 98% above the historical average. The Buffett Indicator is a whopping 215% market value ratio to GDP, holding 72% above the historical average. That said, the bulls seem to have no concern with the premarket activity working to inspire prices higher. So stay with the trend and enjoy the party as long as it lasts!

Markets made a modest gap higher at the open Friday and then waffled until mid-morning. At that point there a sharp rally for about 45 minutes before the market went dead-flat the rest of the day. This left us with strong white candles in the QQQ and SPY, but a Spinning Top in the DIA. On the day, SPY gained 0.75%, QQQ gained 1.06%, and DIA gained 0.51%. The VXX fell to 20.36 and T2122 rose, but remains in the mid-range at 71.00. 10-year bond yields rose to 1.578% and Oil fell a percent to $80.77/barrel.

During last week, Elon Musk ended up selling about $6.9 billion worth of TSLA stock. This included about $1.2 billion on Friday. Despite his having used a TWTR poll a week ago as justification, one of the main reasons behind his sale was to get the cash to pay taxes on a large pool of stock options he will be exercising this quarter. TSLA stock fell 15.4% on the week. However, in his apparent effort to remain in the news, this weekend, Musk taunted Senator Bernie Sanders and, in the process, suggested he may sell more shares of TSLA.

President Biden is scheduled to hold a several-hour “virtual summit” with Chinese President Xi today. The focus will be on Taiwan, its security, and rising tensions over what China calls a “renegade province” (or country, although we have never recognized them as a separate country). Trade, tariffs, and global supply chain issues are not scheduled to be on the agenda. However, the US-imposed tariffs are a major Chinese concern and on the US side, the Chinese commitment to reduce the use of coal (COP24 watered-down agreement) and the Chinese treatment of Uyghur minorities are priority issues.

Retail will take the earnings spotlight this week. WMT, HD, LOW, TGT, TGX, KSS, M, ROST, and FL all report later this week. In addition to Q3 reports, markets will be listening to how companies plan to cope with supply problems and spiking inflation in Q4. In related news, TSN beat on both lines and AAP beat on revenue, but missed on earnings in their reports this morning.

Overnight, Asian markets were mixed but mostly green. South Korea (+1.03%), Taiwan (+0.66%), and Japan (+0.56%) paced the gainers. Meanwhile, Malaysia (-0.58%), Indonesia (-0.53%), and Shenzhen (-0.47%) were the only appreciable losers. In Europe, markets are more mixed and lean to the red side on modest moves. The FTSE (-0.19%), DAX (+0.12%), and CAC (+0.42%) are typical of the spread across the continent at mid-day. As of 7:30 am, US Futures are pointing toward a green open. The SIA is implying a +0.29% open, the SPY is implying a +0.23% open, and the QQQ implies a +0.24% open at this hour.

The only major economic news scheduled for release Monday is limited to NY Empire State Mfg. Index (8:30 am). Major earnings reports scheduled for the day are limited to ACM, DDL, TSN, and WMG before the open. Then after the close, AAP, EDR, and RXT report.

With only the Empire State Mfg. Index report this morning and little earnings news, the path seems open for bulls to follow through on Friday and move prices higher (at least early). Remember that the short-term (pullback) downtrend has been broken in the SPY and QQQ and is being challenged in the DIA. However, that longer-term strong bullish trend remains in place and we sit near all-time highs.

Watch your current positions before looking to add any new trades. Focus on your trade rules and on managing the things you can control. That should include consistently taking profits when you have them and moving your stops in your favor. Trade carefully and continue to think twice before holding through earnings…especially without a hedge.

Ed

Swing Trade Ideas for your consideration and watchlist: GRWG, BX, SKLZ, BMY, CRSR, ROOT, AAPL, NKLA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although we saw modest selling yesterday, tech stocks remained the bright spot posting a gain while the industrials continued to slide lower. However, the moves showed no fear, with VIX pulling back during the choppy light day of price action. This morning, we will turn our attention to Consumer Sentiment and the JOLTS reports with a light day of notable earnings reports as the silly season begins to wind down. Will the data inspire the bulls to close the week positively, or will it bring out the bears, adding to the inflationary worries?

Asian markets closed Friday, trading green across the board during the night, inspired by record Singles Day shoppers. However, European markets trade mixed this morning with modest gains and losses. With a lighter day of earnings inspiration and economic data coming later this morning, the U.S. futures point to a positive as they try to shake off inflation concerns.

Economic Calendar

Earnings Calendar

We have a much lighter day on the earnings calendar with 85 companies, but many of them remain unconfirmed. Notable reports include AZN, DTEGY, VIVO, MFG, NGD, SPB, TOELY, & WRBY.

News & Technicals’

During a politically significant press conference Friday, a top Chinese official gave a rare criticism of the U.S. and Western democracy. The night before, Chinese President Xi Jinping joined the ranks of Mao Zedong and Deng Xiaoping in becoming the country’s third leader to oversee the adoption of a “historical resolution.” While criticizing Western political systems, Chinese officials promoted their country’s agenda and emphasized new development models under Xi. Alibaba and JD.com racked up around $139 billion of sales across their platforms on China’s Singles Day shopping event, setting a new record. The record sales come despite worries about the strength of the Chinese consumer and the impact of Beijing’s crackdown on technology companies. Singles Day was a slightly more muted affair as Chinese technology companies continue to face scrutiny from regulators and President Xi Jinping pushes for so-called “common prosperity.” Treasury yields traded mixed early Friday morning, with the 10-year rising slightly to 1.5716% while the 30-year moved slightly lower to 1.9183%.

Yesterday proved to be a choppy day, but tech stock remained the bright spot for the market with a modest gain while the Dow slowly ground lower. Worries of inflation elevated treasury bonds on Wednesday, and as of this morning, they continue to hold on to gains. However, the gains in gold and silver have softened overnight while still holding essential support levels. With earnings season beginning to wind down, we may turn more attention to economic data for inspiration. Today, we will test the Consumer Sentiment report’s temperature and see if we are making progress with the JOLTS numbers. Today could be interesting with the institutions wanting to close the week on a strong note, while the bears may still want to test price support levels in the index charts that remain below current prices.

Markets gapped higher at the open Thursday, but then drifted sideways back inside the gap the rest of the day on light holiday volume. DIA was the exception as it opened flat and traded down all day as traders punished DIS for their terrible report the night before. This left us with black candles in all 3 major indices. On the day, SPY gained 0.04%, DIA lost 0.45%, and QQQ gained 0.28%. The VXX fell 2% to 21.14 and T2122 rose a little but remains solidly in the mid-range at 63.51. 10-year bond yields rose to 1.57% and Oil (WTI) fell to $81.17/barrel.

This morning, JNJ announced plans to split into two companies, one focused on consumer healthcare products and the other being its pharmaceutical and medical device business units. (This is the second version of such a scheme in months.) The logic behind this plan is to move all liability from the Johnson’s Baby Powder cancer lawsuits into the consumer products business, insulating the larger business unit from liability. The move came just days after the company’s attempted “Texas two-step” (to split off just the talc business alone and choose its own bankruptcy court to limit company liability) failed and the courts ruled that the JNJ bankruptcy will be heard and litigated in the company’s home state of New Jersey. Hence the company is looking to divide to protect what parts of the company it can. JNJ stock is soaring in premarket on the news.

Continuing the conglomerate breakup theme started by GE and followed (for different reasons) by JNJ, Toshiba announced overnight that it is also breaking up. This one is a breakup into 3 companies. TOSYY will spin off its “device and storage” business which makes chips (now branded as Kioxia) as well as its “energy and infrastructure” units into their own companies. This split comes after a 5-month strategic review that was spawned by a governance scandal. The company hoped the reorganization is completed by the second half of 2023. Toshiba closed 1% lower on the news in Japan.

So far this morning, SPB reported a beat on both lines and AZN beat on revenue but missed on earnings. In other business news, Elon Musk took a back-handed shot at new rival RIVN. In a tweet last night, Musk said “I hope they (RIVN) are able to achieve high production and breakeven cash flow. That is the true test.” He went on to say TSLA is the only American carmaker to do so in the past 100 years. RIVN is up 58% from its IPO price in two days of trading (and up 4% in premarket). TSLA is up about 8% over the same time and is flat in premarket trading.

Overnight, Asian markets were mostly green. South Korea (+1.50%), India (+1.28%), and Japan (+1.13%) led the way. However, gains were widespread and only New Zealand (-0.91%), Indonesia (-0.60%), and Singapore (-0.30%) were in the red in the region. In Europe, markets are more mixed at mid-day. The FTSE (-0.39%), DAX (+0.16%), and CAC (+0.35%) are typical of the continent in early-afternoon trading. As of 7:30 am, US Futures are pointing toward a modestly green start to the day. The DIA is implying a +0.28% open, the SPY implies a +0.22% open, and the QQQ implies a +0.25% open at this hour. Bonds are up off overnight lows to 1.568% and Oil (WTI) is down almost 2% in early trading.

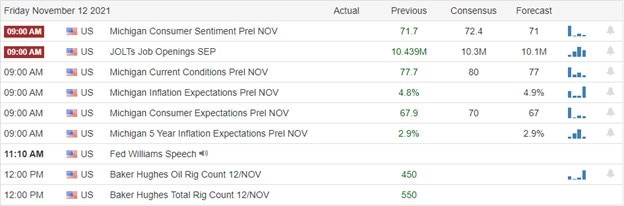

The major economic news scheduled for release Friday is limited to Sept. JOLTS and Michigan Consumer Sentiment (both at 10 am) as well as a Fed speaker (Williams at 12:10 pm). Major earnings reports scheduled for the day are limited to AZN and SPB before the open. There are no major earnings reports after the close.

With no economic news before the open and coming off a slow holiday session, markets are seeming to want to drift higher. While the trend of “rationalizing conglomerates” (breaking into actually related units) will get a lot of talk, that is not enough to move markets. Remember that the short-term trend is down, but the longer-term trend is very bullish and we sit near all-time highs.

Watch your current positions before looking to add any new trades. Focus on your trade rules and on managing the things you can control. That should include consistently taking profits when you have them and moving your stops in your favor. Trade carefully and think twice about holding through earnings.

Ed

Swing Trade Ideas for your consideration and watchlist: WISH, VUZI, CSIQ, CRSR, FAST, LUMN, ROOT, FCX, QS. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bears slowly react to inflation, hitting a 30-year high after an early attempt to rally the markets as if it didn’t matter at all. The wild speculative nature of this market is evident with the pricing of Rivian that has yet to produce 10,000 vehicles an expecting to lose more than 1.2 billion next quarter, now worth more than Ford and General Motors. Of course, that happens to be just another marker that is very reminiscent of the 1999 market bubble. Look for the possibility of light and choppy price action today due to the Federal Holiday of Veterans day.

Asian markets traded mixed with Hong Kong surging 1% as Evergrande makes another last-minute payment to avert default. European market trade mixed with modest gains and losses this morning. With government offices and banking shutdown, U.S. futures point to a bullish open with tech leading the way, trying to recover some of yesterday’s losses.

Economic Calendar

We have a very rare day with nothing on the economic calendar due to Veterans day.

Earnings Calendar

We have more than 160 companies listed on the Thursday calendar, but there are quite a few unconfirmed small caps. Notable reports include MARA, MT, ARRY, XAIR, BLNK, BRDCY, BHG, BAM, COUP, WATT, FRGI, FLO, GFI, RIDE, LAZR, OGN, SBH, SIEGY, TPR, UTZ, VPG, WB, WIX, & YETI.

News & Technicals’

Climate lawsuits will target banks and boards. “I think that the next step is to start also litigating against financial institutions who make these emissions and fossil fuel projects possible,” said Roger Cox, the lawyer for Milieudefensie, an environmental campaign group and the Dutch branch of Friends of the Earth. The Hague District Court on May. 26 ordered the Anglo-Dutch oil giant to reduce its global carbon emissions by 45% by the end of 2030, compared with 2019 levels. The ruling marked the first time in history that a company had been legally obliged to align its policies with the Paris Agreement and reflected a watershed moment in the climate battle. The congestion at U.S. ports, the trucker shortage, and the rise of e-commerce have created a unique opportunity for autonomous trucking, Embark Trucks CEO Alex Rodrigues told CNBC. Embark has completed its SPAC merger and will begin trading Thursday on the Nasdaq under ticker EMBK. Rodrigues will also become one of the youngest CEOs of a U.S. public company ever at 26 years old. Disney added just 2 million Disney+ subscribers after more than 12 million last quarter. However, Netflix bounced back in the third quarter with 4.4 million net adds after just 1 million in the second quarter. Disney, HBO Max, and AMC Networks were among the media companies affirming previously announced forecasts.

Although we saw the bears slowly react to the highest inflation reading in the 30 years, the selling appeared to be relatively controlled. The VIX closed below a 19 handle, and the index charts held well above price and technical support levels. Nevertheless, yesterday’s selling reminded us that bears still exist and that overextended conditions can produce some painful selloffs. I suspect today could be a very muted day with the observance of the Federal holiday of Veterans Day. Though there may be some local exceptions, banking and all government offices are closed. As a result, we could see light and choppy price action trading today.