After a turbulent morning session dominated by bears, the bull won the day, triggering a relief rally to squeeze out short traders as they took profits. However, anything is possible with a jam-packed day of market-moving earnings and economic reports. So, keep a close eye on overhead resistance and support levels as the market react to all the data and prepare for possible gappy market opens the rest of the week as the tech giants report. Price action will likely be challenging as the drama unfolds with so much at stake. Plan your risk carefully!

Asian markets trading mixed during the night as many of the big banks downgraded the growth potential of China as the lockdown continues. However, European markets see green across the board this morning despite a Russian nuclear threat. U.S. futures point to a bearish open with the uncertainty of earnings and economic data ahead.

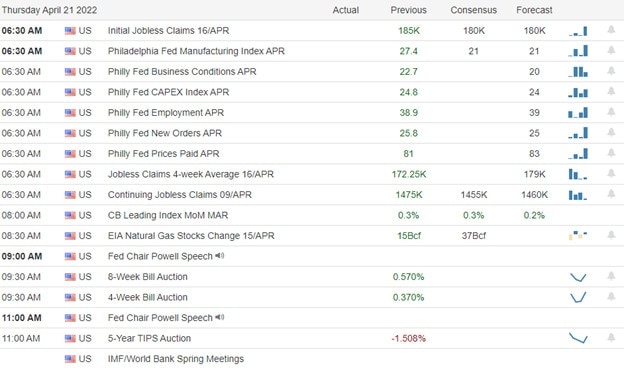

Economic Calendar

Earnings Calendar

Big Tech will highlight the earnings reports on Tuesday, with nearly 200 companies listed on the Tuesday calendar. Notable reports include GOOGL, MSFT, MMM, ADM, ARCC, AVY, BYD, CNI, CAI, COF, CNC, CMG, CB, GLW, DHI, ENPH, EQR, EXAS, FFIV, FANUY, GE, GM, HUBB, JBLU, JNPR, MDLZ, MSCI, NAVI, NTRS, NVS, PEP, RRC, RTX, SHW, SSTK, SKX, TER, TXN, TRU, TZOO, UBS, UPS, VLO, V, WM, & WH.

News & Technicals’

According to the top Russian official, “ the threat of nuclear war is real after the U.S. expressed the desire to see Moscow weakened. On Monday, the Twitter board agreed to a $44 billion buyout from Tesla CEO Elon Musk. However, few additional details are known, leaving users and employees uncertain about the future. In addition, the Tesla CEO has shared little about how he plans to improve Twitter, though he’s offered many criticisms. As a result, it’s unclear who will lead the company under Musk’s ownership or what is ahead for the company’s workforce. Twitter Chief Executive Parag Agrawal told employees on Monday that the future of the social media firm is uncertain after the deal to be taken private under billionaire Elon Musk closes. He was speaking at a town hall meeting that Reuters heard. “Once the deal closes, we don’t know which direction the platform will go,” Agrawal said. Donald Trump said he wouldn’t return to Twitter on Monday even if Elon Musk reversed the former president’s ban. “I was disappointed by the way Twitter treated me. I won’t be going back on Twitter,” the former president told CNBC’s, Joe Kernen. Twitter permanently suspended Trump from the platform in January 2021 following the attack by his supporters on the U.S. Capitol. Several economists at major investment banks have cut their China growth expectations in just about a week. The new median forecast among nine financial firms tracked by CNBC expects 4.5% China GDP growth for the full year. Nomura had the lowest forecast, while UBS cut its estimates the most. Treasury yields continued to dip slightly in early Tuesday trading, with the 5-year trading at 2.82%, inverted over the 10-year at 2.78%, and the 30-year pricing at 2.86%.

On Monday, the bears dominated the early trading session to test 2022 lows, but bulls won the day, triggering a nice relief rally as short traders took profits. We have a jam-packed economic calendar today coupled with the massive anticipation of the big tech earnings from MSFT and GOOGL after the bell. The tech giants will continue to report throughout the week, keeping traders guessing and the price action volatile. Significant point gap up or gap down opens could occur as a result, so plan your risk carefully as the drama unfolds. As we rally, respect overhead resistance levels and avoid the fear of missing and the desire to chase stocks that could gap substantially, vastly increasing the risk. Disappointing reports could also create huge point intraday whipsaws, so plan your risk carefully and be careful not to overtrade.

Markets gapped lower at the open Monday and then the bears gave us about half an hour’s worth of follow-through before bobbing along the bottom until noon. However, then the “intraday reversal” norm kicked in as the bulls stepped in and led a rally that lasted the rest of the day. This left us with white, large-bodied hammer-type candles in the SPY and DIA while the QQQ came up just short of printing a Bullish Piercing Candle. With that said, the SPY and QQQ are still a bit extended below their T-line with the DIA closer, but certainly not testing the 8ema yet. On the day, SPY gained 0.58%, DIA gained 0.68%, and QQQ gained 1.29%. The VXX fell more than 5% to 24.80 and T2122 rose but remains inside the oversold territory at 14.29. 10-year bond yields fell sharply to 2.822% and Oil (WTI) fell more than 2.9% to $99.07/barrel (which was well up off the lows of the day).

Following through on Sunday’s news, the board of TWTR reversed course and accepted Elon Musk’s offer of $54.20/share to take the company private. The stock closed up 5.64% to $51.69 after gapping up 4.25% at the open. The deal is still subject to the approval of a shareholder vote. Assuming the deal closes, this puts the TWTR platform in the hands of one of the company’s former most vocal critics (who happens to have used the platform to break the law, for which he was fined tens of millions of dollars by the SEC). While he is mainly just a PR man for all his companies, the key question for longer-term investors is how hands-on he will be and what this might mean for TSLA. Cryptocurrency (and Musk favorite) Dogecoin also jumped 20% on the news, pricing in the hope that he will continue to heavily promote Dogecoin through TWTR.

Also in the afternoon, F announced it expects to increase electric F-150 production by 3.5 times for 2022 over previously announced production numbers (150k units vs. 40k units announced last year). This would dwarf the production plans from RIVN and GM, which are expected to produce in the area of 10k units during the same period. The company said it was confident it would hit this production plan and is aiming to have produced over 2 million electric vehicles by 2026. TSLA, the leader in electric vehicles, has announced, but has not actually shipped any of its own “cyber trucks.”

Today another AMZN facility in NY will be voting on unionizing. Elsewhere, the Shanghai area reported a record After the close, CCK, WRB, PKG, OI, AXTA, CDNS, SBAC, and ARE all posted beats on both the top and bottom lines. Meanwhile, WHR, AMP, and ZION missed on revenues while beating on earnings. On the other side, UHS and CR beat on revenue while missing on the earnings line.

In economic news, after the close, the USDA updated its Food Price Outlook for 2022. The new forecast calls for 5%-6% overall food inflation in the US over the remainder of the year. Included in this number is a forecast 5.5%-6.5% increase in “away from home” food prices. Elsewhere, also after the close, a survey was released that showed 40% of US small businesses plan to raise prices by at least 10%. The survey was conducted by the National Federation of Independent Businesses (NFIB) between April 14 and 17 covering 540 of their small business members. The survey also found that nearly another half of the surveyed companies plan to increase prices between 4% and 9%.

Overnight, the Asian markets were mixed but leaned to the downside as China is again expanding testing and lockdowns for Covid. Australia (-2.08%), Shenzhen (-1.66%), and Shanghai (-1.44%) paced the losses while India (+1.46%) led gainers by more than a percent over South Korea (+0.42%) and Japan (+0.41%). In Europe, stocks are mostly green at mid-day. The FTSE (+0.82%), DAX (+0.89%), and CAC (+1.11%) lead the region higher while only Portugal and Greece show any red in early afternoon trading. As of 7:30 am, US Futures are pointing toward another down start to the day. The DIA implies a -0.44% open, the SPY is implying a -0.43% open, and the QQQ implies a -0.48% open at this hour. 10-year bond yields are dropping again to 2.799% and Oil (WTI) is up fractionally to $98.87/barrel in early trading.

The major economic news scheduled for release on Tuesday includes Mar. Durable Goods Orders (8:30 am), Conf. Board Consumer Confidence and Mar. New Home Sales (both at 10 am). Major earnings reports scheduled for the day include MMM, AAN, ALLE, ARCH, ADM, ARCC, AVY, CNC, GLW, CEQP, DHI, ECL, ENTG, GE, HUBB, NSP, IVZ, JBLU, MSCI, EDU, NTRS, NVS, NVR, PCAR, PEP, PII, BPOP, RTX, ROP, ST, SHW, SCL, TRU, UBS, UPS, VLO, and WM before the open. Then after the close, ACCO, GOOGL, ASH, AGR, BHE, BYD, CNI, COF, CHX, CHE, CMG, CB, CSGP, EW, EQR, EXAS, FFIV, GM, GOOG, HA, IEX, JPNR, MTDR, MSFT, MKSI, MDLZ, NCR, RRC, RHI, RUSHA, SKX, TER, TX, and V report.

So far this morning, CNC, UPS, VLO, ADM, GE, PEP, MMM, UBS, DHI, SHW, WM, GLW, ATLKY, AVY, GPK, ROPST, JBLU, ALLE, SCL, ENTG, and ARCH have all posted beats on both revenue and earnings. Meanwhile, RTX, NVS, CJPRY, and MSCI all missed on revenue while beating on earnings. On the other side, IVZ and ARCC have reported beating the estimates on revenue but missed on the bottom line. Finally, NMR, PII, FANUY, and AWI all reported missed on both lines.

A huge surge of mostly good earnings leads the day’s news. That is saying something, considering that Russian Foreign Sec. Lavrov threatened the West to stop supporting Ukraine by telling an interview that the threat of the war in Ukraine escalating into a nuclear war was “very, very real.” Another wave of those earnings will hit after the close, with MSFT and GOOGL headlining that list. Despite the positive earnings news and even PEP raising its forward guidance, the premarkets look to be taking back much of Monday’s gains. The fear of spreading covid impacts from China (but hitting the global economy) is also weighing on the minds of longer-term investors, which is a headwind for bullish traders. However, remember that both intraday reversals have been the norm for a while now. So, respect that fact and continue to be cautious. Don’t be in a hurry to chase gaps and early moves. It is better to give up a little of the move than to have to suffer through reversal pains after you jump early.

Focus on the process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Remember that the first rule of making big money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. If you are wrong, just admit it and take your loss. Trading is a marathon, not a sprint.

Ed

Swing Trade Ideas for your consideration and watchlist: VLO, SYY, TGT, JNJ, IBM, GPRO, PSTG, KSS, PEP. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Friday, the bears showed up with lots of reinforcements, and the carnage created significant technical damage to all four index charts. Asia and Europe have joined the selling as economies slow amid the punishing inflation and the soon to be aggressive FOMC rate increases. As the indexes test the low’s 2022, we have a big week of earnings and economic data that could save or sink the market into a complete bear condition. With so much at stake, expect very challenging price action in the days ahead that could easily cause substantial point whipsaws and overnight market reversals.

As we slept, Asian markets suffered significant selling, with Shanghai falling 5.13% as pandemic impacts extended. European markets trade decidedly bearish this morning as global sentiment declines. With U.S. futures suggesting a gap down open to test the market lows of 2022, there is a palpable uncertainty as we face a substantial week of earnings and economic data.

Economic Calendar

Earnings Calendar

We have a hectic week of earnings ahead, with more than 100 companies listed on the Monday calendar. Notable reports include ATVI, ARE, AXTA, BOH, CDNS, KO, CR, LII, OI, OTIS, PKG, PHC, SBAC, WRB, WHR, & ZION.

News & Technicals’

Twitter’s board met Sunday to discuss Elon Musk’s takeover bid after the billionaire disclosed he had secured $46.5 billion in the financing, a source close to the situation told CNBC. The person said the board is looking for other offers, and the company could provide an update by the time it reports its latest financial results Thursday, if not before. Centrist Macron obtained 58.54% of the votes on Sunday, whereas his nationalist and far-right rival Le Pen got 41.46%. Back in 2017, when the two politicians also disputed the second round of the French presidential vote, Macron won with 66.1% of the support, versus Le Pen’s 33.9%. Addressing her supporters in Paris Sunday night, Le Pen conceded defeat but said: “We have nevertheless been victorious.” China’s capital city of Beijing reported a spike in Covid cases over the weekend and warned more would be found since the virus had spread undetected in the city for a week. The city’s business district of Chaoyang began three days of mass testing on Monday for anyone living or working in the region. The increase in cases in Beijing comes as mainland China faces its worst Covid outbreak since early 2020, and most of Shanghai, China’s largest city, remains under prolonged lockdown. European stocks opened sharply lower on Monday as investors digested the projected result of the French presidential election and monitored the latest developments in Ukraine. France’s Emmanuel Macron has comfortably beaten his rival Marine Le Pen in Sunday’s election, securing a second term as president on his pro-business and pro-EU agenda. Treasury yields pulled back in early Monday trading, with the 5-year declining to 2.85%, the 10-year slipping to 2.82%, and the 30-year falling to 2.88%.

Friday’s selling created significant technical damage, with all four indexes closing below their 50-day averages. With the Asian and European markets joining in on the selling, U.S. markets look to open lower to begin a hectic week of earnings. With rising inflation and an aggressive Fed, will earnings be able to hold us at 2022 market lows, or will the results push into a complete bear market condition? On the hopeful side, the T2122 indicator suggests a short-term oversold condition that could bring about a relief rally anytime. However, if this week’s earnings disappoint, the path ahead might be filled with hungry bears. If that’s not enough drama, we have a big week of market-moving economic data to keep us guessing. Expect a challenging week of wild price action that could easily include huge point whipsaws and overnight market reversals as the drama unfolds.

The Bears remained in control all day long Friday as the 3 major indices sold off steadily the entire session. This gave us huge, ugly, black candles across the board. However, it also saw all 3 of those indices pull far away from their T-lines. So, they are extended. On the day, SPY lost 2.74%, DIA lost 2.71%, and QQQ lost 2.62%. The VXX rose more than 5% to 26.15 and T2122 dropped well into the oversold territory to 6.63. 10-year bond yields close down slightly to 2.904% and Oil (WTI) fell almost 2% to $101.75/barrel.

On the Fed watch, on Friday Cleveland Fed President Mester said that she is in favor of raising rates 50-basis-points in May and perhaps doing this a few times this year. She called her preferred approach “methodical.” However, she also said she would not go further than half a percent, saying she was not in favor of 75-basis-point moves to shock the economy as a way to slow inflation. Finally, she said she’d like to see the Fed Funds Rate reach 2.5% by year-end, which she felt would be neutral. This opinion splits the “year-end neutral rate” calls by Bullard (3.5%), Bostic (1.75%), and Evans (2.25%) from earlier last week.

On Sunday, the Wall Street Journal reported that the board of TWTR is taking another look at Elon Musk’s $43 billion takeover bid. The paper reported that the company is more likely to negotiate since he announced he had raised 3.5 billion more in funding than his initial bid. Since Musk made the bid, TWTR has risen more than one percent. TWTR is up 4.5% in premarket on the Sunday news. Probably, but not necessarily unrelated to this story, Musk received 25.3 million TSLA stock options last week (worth about $23 billion considering the exercise price) and will receive another TSLA 8.4 million options this week (as the last traunch of his 2018 compensation package). So, if he had the cash to pay the taxes, he could exercise and sell those options for enough to pay cash for 75% of his TWTR bid just from those proceeds, if he chose to do so.

Today another AMZN facility in NY will be voting on unionizing. Elsewhere, the Shanghai area reported a record number of Covid deaths on Sunday (still only 40). The local provincial government announced 9 new ways it plans to get to “zero covid” by adding more restrictions starting this week. However, AAPL’s largest iPhone production facility, which is located in the city (run by supplier Foxconn) remains open despite the region’s Covid lockdown. Foxconn received special permission to keep their employees living on-site by having their employees designated “key employees” for the region.

Major economic news later this week includes Mar. Durable Goods Orders, Conf. Board Consumer Confidence, Mar. New Home Sales on Tuesday. Then on Wednesday, we get Mar. Trade Balance, Retail Inventories, Mar. Pending Home Sales, and Crude Oil Inventories. On Thursday we see Q1 GDP and Weekly Initial Jobless Claims. Finally, on Friday we get Mar. PCE Price Index, Q1 Employment Cost, Mar. Personal Spending, Chicago PMI, and Mich. Consumer Sentiment.

Major Earnings coming later this week include MMM, GOOG, ADM, AVY, COF, CMG, GLW, FFIV, GE, GM, JNPR, MSFT, MDLZ, PEP, RTX, SHW, TXN, UPS, VLO, V, and WM on Tuesday. Then Wednesday we get ADP, AFL, AMGN, BA, BSX, DFS, F, GD, HES, HUM, KHC, LVS, FB, NSC, PYPL, QCOM, RJF, STX, TMUS, TDY, URI, and WAB. On Thursday, MO, AMZN, AEP, AAPL, BIDU, BAX, CAT, CE, CHD, CMCSA, DPZ, EMN, LLY, GILD, HIG, HSY, IP, IRM, KDP, KLAC, MA, MCD, NOC, PHM, SO, SWK, TROW, TXT, TMO, VRSN, and GWW report. Finally, on Friday we get reports from ABBV, AZN, BMY, CBOE, CHTR, CVX, CL, XOM, HON, LHX, LYB, NWL, PSX, and WY.

Overnight, the Asian markets were deeply red across the board. China in particular got crushed by the covid news as Shenzhen (-6.08%), Shanghai (-5.13%), Hong Kong (-3.73%), and Taiwan (-2.37%) led the region lower. In Europe, we see the same thing taking shape, with the lone outlier of Greece (+0.96%), at mid-day. The FTSE (-2.07%), DAX (-1.68%), and CAC (-2.16%) are leading the region lower in early afternoon trading despite the market-friendly win in the French Presidential election Sunday by Macron. As of 7:30 am, US Futures are pointing toward a gap lower at the start of the day. The DIA implies a -0.84% open, the SPY is implying a -0.97% open, and the QQQ implies a -1.06% open at this hour. 10-year bond yields are down sharply to 2.831% and Oil (WTI) is off more than 4% to $97.81/barrel in early trading.

There is no major economic news scheduled for release on Monday. Major earnings reports scheduled for the day include ATVI, KO, LII, and OTIS before the open. Then after the close, AMP, AXTA, BRO, CDNS, CR, CCK, OI, PKG, SBAC, UHS, WRB, WHR, and ZION report.

So far this morning, KO, LII, as well as a number of ADRs (RHHBY, HYMTF, HYMLY, CWQXY) have all reported beating the estimates on both the top and bottom lines. Meanwhile, OTIS has missed on revenue while beating on earnings.

The fear of spreading covid disease and restrictions hitting the global economy (as mentioned here last week) is rocking the boat for the bulls and giving the bears strength to follow through on a down month for markets. So, US Markets are looking like they will follow Asia and Europe lower at least early today. Remember that both intraday volatility and day-to-day chop have been the norm for a while now. So, respect that fact and continue to be cautious. Don’t be in a hurry to chase gaps lower in the first few minutes of the day. Swing trading is not about catching every cent of a move. It’s about taking your slice out of the middle of a swing.

Focus on the process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Remember that the first rule of making big money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. If you are wrong, just admit it and take your loss. Trading is a marathon, not a sprint.

Ed

Swing Trade Ideas for your consideration and watchlist: NXPI, C, LEN, ORCL, INTC, MSFT, LOW, EBAY, SHW, RWM, SDS, SQQQ, UVXY, TWTR. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Thursday, the index charts suffered some technical damage, producing a nasty intraday reversal at price resistance levels. The selloff extended into the close, leaving behind concerning candle patterns with the SPY, IWM, and QQQ closing below their 50-averages. With a lighter day of earings and economic data, will the bears find the inspiration to push on lower, or will the bulls step up to defend as we move toward the weekend? With a 5/10 and 5/30 bond inversion and a Fed signaling, aggressive rate increases expect the challenging price volatility to continue.

While we slept, Asian markets closed mostly lower, with the Nikkei leading the selling to close down 1.63%. European markets trade in the red across the board this morning due to the aggressive Fed comments. U.S. futures work to recover from overnight lows but still point to a slightly bearish open with a light day ahead of earnings and economic data. So, plan your risk carefully as we head into the uncertainty of the weekend.

Economic Calendar

Earnings Calendar

Friday, we get a little break with fewer companies expected to report. Notable reports include AXP, CLF, GNTX, HCA, KMB, NEM, RF, SAP, SLB, & VZ.

News & Technicals’

Fed Chairman Jerome Powell on Thursday said the central bank is committed to raising rates “expeditiously” to bring down inflation. That could mean an interest rate hike of 50 basis points in May as prices rise at their fastest pace in more than 40 years. “It’s absolutely essential to restore price stability,” he added. On Thursday, the Florida legislature passed a bill seeking to dissolve a special district that allows the Walt Disney Company to act as its own government within the outer limits of Orange and Osceola counties. If Gov. Ron DeSantis signs the bill into law, the Reedy Creek special district would be dissolved effective June 1, 2023. Dissolving the district would mean Reedy Creek employees and infrastructure would be absorbed by the counties, which would then become responsible for all municipal services. Warner Bros. Discovery has decided to shut down CNN+ just weeks after it launched. CNBC reported that fewer than 10,000 people were watching CNN+ each day last week. As a result, CNN+ head Andrew Morse is leaving the company. Warner Bros. Discovery leaders spoke to hundreds of CNN+ staffers Thursday to explain the decision to shut down the service. Snap missed Wall Street expectations for profit and sales when it reported first-quarter results on Thursday after the bell. Shanghai, China’s largest city, has struggled to contain a Covid outbreak and began large-scale lockdowns in late March. In the last week, authorities announced a whitelist of 666 companies that would get priority for resumption of work. Foreign business organizations said the list is a step in the right direction, but it’s challenging to get more than half of the workers to factories due to lockdown restrictions. Treasury yields continue to rise in early Friday trading, with the 5- year rising to 3.01%, inverting over the 10-year trading at 2.93%, and the 30-year pricing at 2.96%.

Thursday was a rough day for the indexes to produce a nasty intraday reversal at price resistance levels. Investors came to grips with aggressive rate increases likely coming from the FOMC next month. Unfortunately, the SPY and IWM fell below their 50-day averages again, while the QQQ failed at its 50-day, resulting in a bearish lower low. However, with defensive sector stocks finding favor in the turmoil, the DIA remained the sole index able to hold above its 50-day. The question for today is if the bears will have the energy to follow through to the downside or if the bulls will step up to defend as we slide into the weekend. With a lighter day of earnings and economic data, directional inspiration may be challenging to come by until the big tech earnings events next week. Another troubling factor investors will have to grapple with today is the 5-year Treasury yields inverting over the ten and thirty-year bonds that often signal a recession may be on the way. Expect price volatility to remain high and watch closely as we test recent lows for support.

The bears sprang a Bull Trap on Thursday morning. All 3 major indices gapped higher at the open, only to immediately begin a strong all-day selloff that took them out on the lows. This left us with large, ugly, black candles in all three indices, including a Bearish Engulfing candle in the DIA and something that approximates a Bearish Evening Star in the SPY. Both the SPY and QQQ failed their T-lines, while the DIA is now at that level and ready to retest. On the day, SPY lost 1.50%, DIA lost 1.09%, and QQQ lost 2.07%. The VXX rose almost 2% to 24.86 and T2122 fell back to just outside the oversold territory at 24.27. 10-year bond yields spiked back to 2.91% and Oil (WTI) rose almost 1.9% to $104.09/barrel. It is worth noting that the 5yr vs. 30yr bond yields have inverted again.

On the Fed watch, during the day Fed Chair Powell spoke twice. To nobody’s surprise, he said that taming inflation was absolutely essential as was restoring price stability (which I thought were the same thing). He committed to “raising rates expeditiously.” Then he went on to say that he thinks a 50-basis-point hike is on the table for May, which matches the Futures bets showing a 98% chance of a half-percent hike at that meeting.

In business news, the fight between Florida Republicans and DIS ratcheted up Thursday. The state dissolved the DIS special district as of June 1, 2023. This would eliminate certain special privileges DIS has had, such as having their own zoning authority and deciding their own infrastructure projects. However, the move would also transfer somewhere around $1 billion in debt to the two counties that would take over responsibility for the district area. This likely means a series of lawsuits will follow. Elsewhere, GPS announced that the CEO of their Old Navy division is leaving the company this week, fired over “execution challenges.” Finally, FB COO Sandberg is under investigation for pressuring a UK tabloid news outlet to bury a report about her boyfriend (ATVI CEO Kotnick) being under a restraining order filed by another woman. This pressure happened on two separate occasions, three years apart.

Elon Musk said he has lined up $46.5 billion to finance his takeover of Twitter. This does not affect his offer of $54.20/share. However, it is notable because just last week a judge ruled that he lied about the same thing (and was fined $20 million for stock manipulation by the SEC as well as paying TSLA stock owners $40 million over fraud claims) when he tweeted he had financing in place to take TSLA private in 2018. As far as the current bid for TWTR is concerned, as reported last weekend, the TWTR Board has already implemented a “poison pill” defense in case Musk was able to amass 15% or more of the shares of the company.

After the close, PPG, UFPI, WAL, and SIVB all reported beating on revenue and earnings. Meanwhile, FE and ISRG reported beats on revenue while coming up short on earnings. However, SNAP and SAM both missed on the top and bottom lines.

Overnight, the Asian markets were mixed, but leaned heavily to the downside as the Chinese Yuan hit a new one-year low. Japan (-1.63%), Australia (-1.57%), and India (-1.27%) paced the losses. Meanwhile, only Singapore (+0.38%), Shanghai (+0.23%), and Malaysia (+0.23%) managed any green. In Europe, stocks are red across the board at mid-day. The FTSE (-0.74%), DAX (-1.83%), and CAC (-1.55%) are typical of the continent in early afternoon trading. As of 7:30 am, US Futures are pointing toward a slightly lower start to the day. The DIA implies a -0.22% open, the SPY is implying a -0.14% open, and the QQQ implies a +0.01% open at this hour. 10-year bond yields are up again to 2.938% and Oil (WTI) is off 1.5% to $102.25/barrel in early trading.

The major economic news scheduled for release on Friday is limited to Mfg. PMI and Services PMI (both at 9:45 am). Major earnings reports scheduled for the day include AXP, ALV, CLF, HCA, KMB, NEM, RF, SAP, SLB, and VZ before the open. There are no major reports scheduled for after the close.

So far this morning, AXP, VZ, KMB, RF, SLB, and CLF have all reported beating the estimates on both the top and bottom lines. Meanwhile, SAP, HCA, and VLVLY (Volvo) have missed on earnings while beating on revenue. However, NEM and ALV have both reported misses on both lines.

Markets are limping toward the weekend and look to open lower as the SPY tries to avoid another down week. Remember that both intraday volatility and day-to-day chop have been the norm for a while now. So, respect that fact and continue to be cautious. Don’t be in a hurry to chase into a rally the first few minutes of the day. Swing trading is not about catching every cent of a move. It’s about taking your slice out of the middle of a swing. Finally, keep in mind that it is Friday and you need to prepare for the weekend news cycle.

Remember that the first rule of making big money in the market is to not lose big money in the market. Don’t be stubborn, and protect yourself from yourself. If you are wrong, just admit it and take your loss. Trading is a marathon, not a sprint. So, focus on the process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The QQQ struggled yesterday, with NFLX losing 50 billion in value in a single day, but earnings inspired the bulls to stretch the Dow index toward a test of recent highs. Today we will hear from Jerome Powell, followed by more comments from James Bullard as the 5-year bonds invert slightly over the 10-year with a 30-year inversion near. Finally, it will be a busy morning of earrings, Jobless Claims, and Philly Fed Mfg. numbers that consensus expects to decline. So, plan for an extra dose of volatility and watch for the potential of a pop and drop as the Dow tests the resistance of recent highs.

During the night, Asian markets traded mixed, with Shanghai leading the selling, falling 2.26% at the close as lockdowns continue amid surging infection rates. However, with the war in Ukraine intensifying European markets, trade decidedly bullish this morning. With a busy day of earnings, economic data, and Fed speeches, U.S. futures point to a substantial gap higher with earnings fueled speculation.

Economic Calendar

Earnings Calendar

We have our busiest day of the week, with about 120 companies listed on the earnings calendar today. Notable reports include ABB, ALK, AAL, T, AN, BJRI, BX, SAM, DHR, DOW, FCX, GPC, HBAN, ISRG, KEY, MMC, NEE, NEP, NUE, PM, POOL, PPG, DGX, SNAP, SIVB, TSCO, TPH, UNP, & WSO.

News & Technicals’

Melvin Capital, the embattled hedge fund run by its once high-flying founder Gabe Plotkin, has been discussing a novel plan with its investors under which the firm would return their capital while giving them the right to reinvest that capital in what would essentially be a new fund run by Plotkin. According to people familiar with his plans, Plotkin has committed to keeping his “new” fund at or below $5 billion in capital and returning to a focus on shorting stocks. Buy with Prime enables third-party retailers to take advantage of Amazon’s vast shipping and fulfillment network for orders placed on their site. Prime members can order items on other retailers’ websites using payment and shipping information stored in their Amazon accounts. The service is only available by invitation to some Amazon merchants, but the company plans to make it more widely available in the future. The rapid rise in the U.S. 10-year Treasury yield to three-year highs has erased its gap with its Chinese counterpart, which hasn’t happened for more than a decade. Analysts said that the narrowing gap reflects diverging monetary policy between the two countries. Investors are watching the implications of the narrowing yield gap for the Chinese yuan. Tesla beat analysts’ expectations on the top and bottom lines for Q1 2022. For the period ending March 31, 2022, Tesla reported $3.22 earnings per share and revenue of $18.76 billion. When Russia invaded Ukraine, no one knew how long the ensuing conflict would last or how deep the shockwaves sent through Europe or the rest of the world. As the war approaches its third month, however, the fallout from the conflict is becoming more apparent, and the outlook does not look good. Treasury yields climbed in early Thursday trading, with the 10-year rising to 2.871% and the 30-year moving to 2.909%.

Earnings inspired the bulls on Wednesday, with the Dow Surging 249 points while the Nasdaq struggled with NFLX losing 50 billion in value in a single day. With the strong report out of TSLA, futures are once again surging in the premarket, rapidly approaching signifiant price resistance levels. The T2122 indicator may also reach a short-term overbought condition this morning ahead of a Jerome Powell speech followed by more comments from James Bullard. Before the bell, we have a busy morning of earnings reports, Jobless Claims, and a Philly Fed Mfg. Reports that consensus expects to decline. Expect another day of volatility as data rolls out. Watch for the potential of a pop and drop as prices stretch to test index resistance levels with the 5-year bonds slightly inverted over the 10-year and near a 30-year inversion. Remember, as we stretch higher, pullback risk grows, so be careful not to chase stocks already extended away from support levels.

All three major indices gapped modestly higher at the open Wednesday. This was followed by an immediate 30-minute selloff in the QQQ. Then all 3 of those indices “roller-coastered” their way sideways in a volatile rest of the day. This left us with a gap-up Doji in the DIA, a gap-up black Spinning Top type candle in the SPY, and a Large black Dark Cloud Cover candle in the QQQ. On the day, SPY lost 0.10%, DIA gained 0.68% (largely on the earnings-related big gains from IBM +7.08% and PG +2.66%), and the QQQ lost 1.50%. The VXX fell 1.37% to 24.39 and T2122 rose to just outside the overbought territory at 76.55. 10-year bond yields fell to 2.846% and Oil (WTI) ended unchanged at $102.56/barrel.l.

During the day, Crude Oil inventories came in dramatically lower than expected (-8 million barrels vs + 2.5 million barrels set.). The Fed Beige Book also indicated that (surprise!) inflationary pressures remain strong. NFLX continued to be hammered for Tuesday night’s earnings miss, closing down 35% (which was actually up more than 4% from the lows of the day). AAPL has its Atlanta store employees file for a union election (jumping ahead of the New York City store that is also gathering signatures in order to trigger a union vote). San Francisco Fed President Daly (a dove) also voiced her thoughts. This included that she fears the coming series of rate hikes could tip the economy into recession, but that she also thought the dip would be mild.

After the close Wednesday, TSLA, EFX, KNX, LSTR, SCX, SEIC, KMI, VMI, and THC all reported beating on both the revenue and earnings lines. TSLA in particular blew away Wall Street’s expectations ($3.22 actual vs $2.26 est. and $18.76 billion vs $17.80 bill est.). Meanwhile, AA, and CCI both missed on revenue while beating on earnings. On the opposite side, CVNA and GL both beat on revenue while missing on earnings. However, LCRX and SNBR reported misses on both lines.

In business news this morning, AMZN announced that it plans to open up its Prime delivery service to other retailers. This will allow other merchants to sell their goods under the “Buy with Prime” without explicitly mentioning AMZN…for a fee of course. The service will also appeal to the 200 million existing AMZN Prime members. Elsewhere, AAL says that it expects a Q2 profit and is seeing very strong bookings. It has returned to 94% of its 2019 flight schedule, which is more than competitors DAL and UAL.

Overnight, the Asian markets were mixed again, with more exchanges in the green than red, but the losers moved more than the winners. Shenzhen (-2.70%), Shanghai (-2.26%), and Hong Kong (-1.25%) paced the losses. Meanwhile, India (+1.49%) and Japan (+1.23%) were by far the biggest gainers. In Europe, stocks are mostly green at mid-day. The FTSE (+0.17%) lags again while the DAX (+1.57%) and CAC (+1.82%) are leading the region higher in early afternoon trading. As of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.63% open, the SPY is implying a +0.79% open, and the QQQ implies a +1.08% open at this hour. 10-year bond yields are back up to 2.877% and Oil (WTI) is up three-quarters of a percent to $103.05 in early trading.

The major economic news scheduled for release on Thursday, we get Initial Weekly Jobless Claims and Philly Fed Mfg. Index (both at 8:30 am), and Fed Chair Powell speaks at both 11 am and 1 pm. Major earnings reports scheduled for the day include ABB, ALK, AAL, T, AN, BX, DHR, DQ, DOV, DOW, FCX, GPC, HRI, HBAN, KEY, MMC, NEE, NUE, PNR, PM, POOL, DGX, SNA, SON, SNV, TSCO, TPH, UNP, WSO, and XRX before the open. Then after the close, SAM, FE, ISRG, PPG, SNAP, SIVB, and UFPI report.

So far this morning, AN, PM, BX, DOW, DHR, MMC, AAL, TSCO, DGX, DOV, SON, HBAN, POOL, WSO, SNA, PNR, ALK, TPH, SNV, and DQ have all posted beats on both lines. Meanwhile, T missed on revenue while beating on earnings. On the other side, KEY, XRX, and HRI beat on revenue but missed on the earnings line. However, ABB missed on both lines.

Earnings will be a tailwind for the bulls today as a large majority of reports came in as beats on both lines last night and this morning. However, Jobless Claims have a chance to rock the boat in premarket while Fed Chair Powell is also speaking during the day. The mega-cap Dow Components look to be breaking free of the recent range while the broader SPY and QQQ seem to still be struggling with that resistance. This may indicate a rotation toward the names perceived to be safer in a rising-rate environment. However, remember that both intraday volatility and day-to-day chop have been the norm for a while now. So, respect that fact and continue to be cautious. Don’t be in a hurry to chase into a rally the first few minutes of the day. Swing trading is not about catching every cent of a move. It’s about taking your slice out of the middle of a swing.

Remember that the first rule of making big money in the market is to not lose big money in the market. Don’t be stubborn, and protect yourself from yourself. If you are wrong, just admit it and take your loss. Trading is a marathon, not a sprint. So, focus on the process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: MCK, CLX, TSLA, DVN, NKE, CCJ, MO, URA, IBM, ORCL, APD, UA, SWN, F, FSR, APA, GM, COP. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls defied the IMF global growth downgrade, the worsening situation in Ukraine squeezing out short traders as they rushed in stocks. However, one day does not make a trend, and it will be interesting to see if they have the energy to follow through today after the disappointing NFLX report. Next, we will turn our attention to mortgage data, existing-home sales, and a busy day of earnings and Fed speakers. Expect price volatility to remain high as the earnings drama continues.

Asian markets closed mixed overnight as China keeps its benchmark lending rate unchanged amid its struggling real estate sector. European markets had a shaky start to the day but have since turned positive as they watch Ukraine developments. U.S. futures trade modest and mixed this morning, with the Nasdaq under some pressure with NFLX indicated to open more than 25% lower.

Economic Calendar

Earnings Calendar

We have a busy day with more than 90 companies listed on the Wednesday earnings calendar, though several are unconfirmed. Notable reports include TSLA, ABT, AA, ANTM, ASML, BKR, BDN, CNS, CMA, CCI, CSX, EFX, GL, KMI, LRCX, LAD, MMLP, NDAQ, PG, SLG, STLD, THC & UAL.

News & Technicals’

Shares of Netflix cratered more than 25% on Tuesday after the company reported a loss of 200,000 subscribers during the first quarter. It’s the first time the streamer has reported a subscriber loss in more than a decade. Netflix blamed increased competition, password sharing, inflation, and the ongoing Russian invasion of Ukraine for the stagnant subscriber growth. Netflix said more than 100 million global households use a shared password, with more than 30 million in the U.S. and Canada. As a result, Netflix suggested it will begin to make accounts that share passwords pay up. Netflix has long ignored password sharing because it has been growing without cracking down on it, but it announced it lost subscribers in the first quarter for the first time in more than a decade. IBM beat consensus on the top and bottom lines. The technology services company offloaded Watson’s healthcare assets to a private-equity firm in the quarter. The stock has outperformed the S&P 500 so far this year. Russia’s war with Ukraine entered a new phase this week, with Moscow focusing its war machine on eastern Ukraine. The move is seen as a bid for Russia to cement its grip on the Donbas — an area that includes two breakaway, pro-Russian self-proclaimed “republics” — and try to annex it. Analysts warn how Russia’s latest offensive goes in the Donbas region could prove extraordinarily significant and decisive in the war against Ukraine. It could determine how Ukraine’s territorial boundaries look in weeks and years. Treasury yields dipped slightly early Wednesday, with the 10-year one basis point to 2.9034% and the 30-year down two basis points to trade at 2.9643%.

Bulls rushed into stocks yesterday, squeezing out short traders defying the IMF global growth downgrade and mixed earnings results. Now the question is can they follow through on that rally after the very disappointing results from NFLX after the bell. Surprisingly, the market seems to have chosen to ignore the rising commodities and inflation or that the Fed will begin to act more aggressively next month. Add to that list the war in Ukraine, the weakening economy in China, and lockdowns that will likley create supply chain challenges. Today, we will have another big round of earnings to supply price volatility, Mortage App data, Existing Home Sales, Petroleum Status, Fed Speakers, and a 20-year bond auction. Remember that one day does not make a trend that we still have significant resistance levels above in the index charts. So, plan your risk carefully and watch whipsaws and overnight reversals as earnings events continue to ramp up.

Markets opened basically flat on Tuesday but then proceeded to rally until 11 am before a sideways grind that lasted until 3 pm. Prices rallied the last hour of the day taking all 3 major indices out near their highs. This left use with large white candles and Morning Star patterns in all 3 of those indices. All 3 also climbed back above their T-line (8ema) before the close. On the day, SPY gained 1.63%, DIA gained 1.48%, and QQQ gained 2.22%. The VXX fell 2.3% to 24.73 and T2122 jumped up to the upper mid-range at 70.26. 10-year bond yields spiked again to 2.94% (highest since 2018) and Oil (WTI) fell 5.28% to $102.50/barrel.

Contrary to Monday’s call by the Fed’s Bullard (Hawk) for several half-point interest rate hikes (and potentially using three-quarters point rate hikes) targeting a “neutral rate of 3.5% by year-end, on Tuesday we heard from Atlanta Fed President Bostic. Bostic (usually considered a hawk) told CNBC he was concerned that raising rates too fast could hurt the economy and wants the FOMC to be “very measured” in rate hikes. He also said that the “neutral rate” could be as low as 1.75%, half of what Bullard (the most extreme hawk) felt would be neutral.

After the close Tuesday, IBM, OMC, and FHN all reported beats on both revenue and earnings. NFLX reported a significant beat on earnings ($3.53 actual vs $2.92 est.) but missed on revenue (as well as reporting it lost subscribers for the first time) and was absolutely hammered (down as much as 28%) in post-market trading on that miss. On the opposite side, IBKR missed on earnings, but beat on revenue.

As mentioned in yesterday’s blog, both the US and UK announced today that they will be sending new military assistance packages to Ukraine. This is in addition to last week’s $800 million package. The White House specifically mentioned that the new package would include more heavy artillery and shells. However, the Pentagon declined to outline the contents of this next package. The main US suppliers of artillery such systems are GD, RTX, NOC, and LMT.

News out of China may give us a chance to capitalize on future news. The largest and fourth-largest ports in the world are currently shut down due to covid lockdowns. There are over 300 container ships and over 500 bulk-carrier ships waiting offshore to be unloaded and reloaded with exports. This very likely means that once China opens and they surge to get the backlog out, the logjam will move back to the US ports of LA, Long Beach, and Oakland. All this means more supply chain problems for major importers. The five largest are WMT, TGT, HD, LOW, and DOLE.

Overnight, the Asian markets were mixed but leaned toward the green side. Shenzhen (-2.07%) and Shanghai (-1.35%) saw by far the biggest losses while New Zealand (+1.10%), India (+1.05%), and Taiwan (+0.91%) led the more numerous gainers. In Europe, stocks are nearly green across the board. The FTSE (+0.16%) lags, but the DAX (+1.03%) and CA (+1.13%) are typical of the region with even Russia (+2.47%) up strongly in early afternoon trading. As of 7:30 am, US Futures are pointing toward another flat start to the day. The DIA implies +0.14%, the SPY is implying +0.03%, and QQQ implies a -0.13% open to the day. 10-year bond yields are back down to 2.863% and Oil (WTI) is up just over 1% in early trading.

The major economic news scheduled for release on Wednesday includes March Existing Home Sales (10 am), Crude Oil Inventories (10:30 am), and Fed Beige Book (2 pm). There is also a Fed speaker scheduled (Daly at 10:30 am). Major earnings reports scheduled for the day include ABT, ANTM, ASML, BKR, CMA, LAD, MTB, NDAQ, PG, and before the open. Then after the close, AA, CVNA, CCI, CSX, EFX, KMI, KNX, LRCX, LSTR, LBRT, SEIC, SNBR, STLD, THC, TSLA, UAL, and VMI report.

So far this morning, ABT ANTM, PG, ASML, LAD, and NDAQ have all reported beating estimates on both revenue and earnings. At the same time, RCI and MTB both missed on revenue while beating on earnings. However, BKR and CMA missed on both the top and bottom lines.

Overnight it was announced that the largest public pension fund (CalPERS), which is a major holder of BRKB stock, will be voting in favor of a proposal to replace Warren Buffett as Chairman of Berkshire Hathaway. The “Oracle of Omaha” has been the public face and perceived leader of stock markets for at least 40 years and this move is notable, though not unexpected for a man who is 91 years old. No word is yet available on when the vote can be forced. However, in 2021 Buffett announced that his successor would be Greg Abel who is currently BRKB Vice-Chair for Non-Insurance Businesses.

Yesterday’s action took us back to the top of the recent trading range. However, it appears that the bulls may make at least an early bid to push up out of that range today. However, volatility and day-to-day chop have been the norm for a while now. So we have to respect the fact that we are right at a level of resistance in all 3 major indices. So, be cautious. Don’t be in a hurry to chase into a rally the first few minutes of the day. Swing trading is not about catching every cent of a move. It’s about taking your slice out of the middle of a swing.

Remember that the first rule of making big money in the market is to not lose big money in the market. Don’t be stubborn, and protect yourself from yourself. If you are wrong, just admit it and take your loss. Trading is a marathon, not a sprint. So, focus on the process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: CLVT, IT, HTZ, DISH, FIS, CMCSA, CLX, MA, NKE, XLB, MCD, APD, MRO, MNST, US, MMM. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service