Strong Reports, Lowered Guidance Today

Stocks gapped lower between 0.60% and 1.00% in the major indices Wednesday. Then after about an hour of sideways grind, they followed through to the downside to reach the lows of the day shortly after 11:45 am. However, once again the dip buyers stepped in and the bulls began a rally that took us back to the highs of the day closing the morning gap in the large-caps) by 2:40 pm. The Whipsaw took effect there and all 3 major indices started back down the rest of the day. This action left all 3 major indices giving us gap-down, Doji / Spinning Top candles which indicate indecision in the current pullback.

On the day, SPY lost 0.71%, DIA lost 0.45%, and QQQ lost 1.14%. Nine of the ten sectors were in the red with the Energy Sector managing green while Basic Materials, Technology, and Consumer Cyclicals led the way lower. The VXX fell just under 1% to 21.10 and T2122 fell out of the overbought territory to 71.31. 10-year bond yields were significantly higher to 2.889%, while Oil (WTI) was up 1.36% to $87.71/barrel on the day. Overall, a modestly red, indecisive day where all 3 major indices stayed above their respective T-lines (8ema).

In economic news, July Retail Sales came in dead flat, which was slightly below the +0.1% forecast and well below June’s +0.8%. Meanwhile, June Business inventories came in as forecast at 1.4% (down from May’s 1.6%) and June Retail Inventories came in better than expected a 1.5% (versus 1.6% forecast). The big surprise was EIA Oil inventories, which came in down 7.056mil barrels (versus -0.275mil forecast). With this said, the big news was the July FOMC Minutes, which indicated meeting participants are in favor of sustained action to bring down inflation and stated that they saw a “neutral rate” (neither supportive nor restrictive of growth) to be around 2.25% – 2.50%. Futures markets have now priced in a 50-basis-point hike for September (versus the last two meeting’s 0.75% hikes).

SNAP Case Study | Actual Trade

In earnings news, after the close, AMCR, BBWI, CSCO, KEYS, and SNPS all reported beating on both the revenue and earnings lines. Meanwhile, ZTO missed on revenue while beating on earnings. So far this morning, CLPBY, BJ, KSS, EL, NTES, SPTN, CSIQ, NICE, and FORTY all reported beats on both lines. Meanwhile, TPR missed on revenue while beating on earnings. However, it is worth noting that KSS, EL, and TPR all lowered forward guidance while reporting.

In stock news, HOG and union employees voted to ratify a 5-year contract that averts a potential strike. The BBY meme stock fell sharply when Ryan Cohen (CEO of GME) filed with the SEC that he is beginning to sell his 9.5 million shares (total holdings) which is roughly 10% of the outstanding shares. Then, after the close, Investing.com reported that DEN is exploring a potential sale after it escaped bankruptcy in 2020.

In Energy news, as mentioned above, US Oil Inventories fell sharply and unexpectedly this week. The EIA went on to report that the cause was not domestic consumption nor a lack of supply. The cause was a record amount of US oil exports of over 5 million barrels per day in the last week while WTI was selling at a steep discount to Brent. Earlier in the day, a US Appeals Court overruled a lower court ruling that had halted the Biden Administrations’ effort to pause and reevaluate oil and gas leasing on Federal land and waters

Bloomberg reports that following the visit of Speaker of the House Pelosi and a second Congressional delegation the following week, formal trade talks between the US and Taiwan will now start in a long-promised effort to deepen ties. This comes amidst strenuous opposition from China. Elsewhere abroad, UK inflation came in at over 10% yesterday, giving them the highest inflation rate among the G-10. Then early this morning (US time), Turkey cut its interest rates to spur growth…even as the country faces an 80% inflation rate.

Overnight, Asian markets were nearly red across the board. Only Singapore (+0.33%) showed any appreciable gains. Meanwhile, Japan (-0.96%), Hong Kong (-0.80%), and Shenzhen (-0.62%) led the rest of the region lower. In Europe, stocks are mixed at mid-day. The FTSE (-0.04%), DAX (+0.67%), and CAC (+0.45%) are leading a slight lean to the upside. However, 7 exchanges are showing red while 8 are showing green in early afternoon trading. As of 7:30 am, US Futures are pointing toward a flat start to the day. The DIA implies a +0.08% open, the SPY is implying a +0.08% open, and the QQQ implies a +0.03% open at this hour. 10-year bond yields are a bit lower to 2.868% and Oil (WTI) is up 1% to $88.98/barrel in early trading.

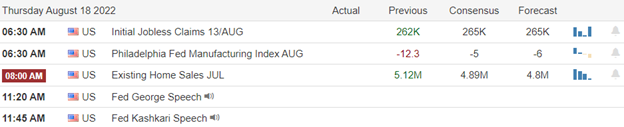

The major economic news events scheduled for Thursday include Weekly Initial Jobless Claims and Philly Fed Mfg. Index (both at 8:30 am), and July Existing Home Sales (10 am). There are also two Fed speakers (George at 1:20 pm and Kashari at 1:45 pm). The major earnings reports scheduled for the day include BJ, CSIQ, EL, KSS, NICE, SPTN, and TPR before the open. Then, after the close, AMAT and ROST report.

In economic news later this week, on Friday there is no major economic news. However, in earnings later this week, on Friday we get reports from DE, FL, and VIPS.

Earnings were surprisingly good (although some retail forward guidance was lowered) overnight and this morning. We still have Jobless Claims ahead, but at the moment it is looking like a modest (tentative?) bullish start to the day. That would make yesterday’s pullback exactly what the doctor ordered for a sustained rally. We can probably expect another low-volume, perhaps dead morning, as the rest continues. However, you can’t measure a river’s depth on average, meaning there will be pockets of extreme volatility in places like the meme stocks where BBBY is one to watch. The trend remains bullish, but remember the SPY and QQQ still have their 200sma overhead to deal with, and for that matter, DIA has not pulled away from its 200sma after breaking through.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: FUBO, VRM, C, GM, TOST, TTWO, GE, BAC, DM, WFC, WMT, UNP, TGT, RKT. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service