Institutional program trading triggered a sudden and sharp end-of-day rally, leaving behind hopeful bullish engulfing candles in an otherwise frustratingly choppy day. However, the uncertainty is understandable, with a sharply declining housing market index number and the pending FOMC rate decision weighing on investors’ minds. Tuesday will likely see much of the same with the Fed meeting beginning today and a Housing Starts and Permits number out before the bell. Plan for lots of chop and quick intraday whipsaws inspired by institutional algorithmic trading.

Asian markets traded in a choppy session but ended the day higher as China kept the benchmark lending rate unchanged as core inflation in Japan grew at the fastest pace in eight years. European markets trade modestly red across the board this morning in a choppy session. U.S futures look to take back some of Monday’s gains at the open at the September FOMC meeting begins. Markets hate uncertainty, so plan for another choppy price action day as we wait.

Economic Calendar

Earnings Calendar

We have just three confirmed earnings reports today, and they are not particularly notable, but they are APOG, ACB, & SFIX.

News & Technicals’

The Riksbank said monetary policy would need to be tightened further to bring inflation back to its 2% target and forecast further rises in interest rates over the next six months. “The development of inflation going forward is still difficult to assess, and the Riksbank will adapt monetary policy as necessary to ensure that inflation is brought back to the target,” it said. Ether has fallen around 15%, while bitcoin has dropped 3% since the Ethereum network underwent a huge upgrade called the merge. Ahead of the network upgrade, the price of ether roughly doubled from the year’s lows in June, far outpacing bitcoin’s gains. Investors have taken profit as the merge was primarily priced in, while concerns about further interest rate rises from the U.S. Federal Reserve have hit risk assets across the board. Ford Motor on Monday warned investors that the company expects to incur an extra $1 billion in costs during the third quarter due to inflation and supply chain issues. Ford said supply problems have resulted in parts shortages affecting roughly 40,000 to 45,000 vehicles, primarily high-margin trucks, and SUVs that haven’t been able to reach dealers. However, the automaker reaffirmed its full-year guidance, saying it expects to deliver the vehicles to dealers in the fourth quarter.

A strengthening Hurricane Fiona barreled toward the Turks and Caicos Islands on Tuesday as it threatened to strengthen into a Category 3 storm, prompting the government to impose a curfew. Forecasters said Fiona could become a major hurricane late Monday or Tuesday when it was expected to pass near the British territory. The intensifying storm kept dropping copious rain over the Dominican Republic and Puerto Rico. The Bank of Japan reportedly conducted a foreign exchange check – a move seen as a precursor for formal intervention. However, HSBC says BOJ will prioritize maintaining its yield curve control policy instead. UBS says chances of shifting away from its current monetary stance are especially low under BOJ governor Kuroda. The 2-year treasury yield reached a 15-year high in early Tuesday trading at 3.97%, with the 5-year at 3.73%, the 10-year at 3.45%, and the 30-year at 3.55%.

Monday’s price action was a not-so-surprising choppy session until a sudden surge of institutional program trading triggered a sharp end-of-day rally, leaving behind some hopeful bullish engulfing candles. Unfortunately, the surge in buying could not breach overhead resistance levels, and the uncertainty of the pending FOMC rate decision weighs on investors. The Housing index numbers disappointed, coming in substantially under consensus estimates, and continue to show a dramatic slowdown in the industry. Today begins the FOMC meeting, and we will get a reading on Housing Starts and Permits before the bell with a 20-year bond auction later in the day. Treasury yields continue to rise, fanning the flames of recession, with the 2-year hitting a fifteen-year high earlier this morning. Expect price action to remain challenging as we wait on the rate decision amidst weakening economic conditions worldwide and right here in our backyard.

Markets gapped down (0.88% in the SPY, 0.89% in the DIA, and 1.10% in the QQQ) at the open Monday. However, this was a bear trap as bulls immediately stepped in and rallied all 3 major indices back up through the gap and into positive territory before 11 am. At that point, the market started a sideways grind with a slight bearish trend for a few hours. Then finally, the bulls stepped back in at 2:30 pm to drive us back to the highs of the day at 3 pm and take us out on the highs. This action left us with gap-down, white-bodied, Marubozu-type candles that engulfed the prior white candles.

Nine of the 10 sectors were green with Healthcare (-0.75%) by far the biggest loser and Basic Materials (+2.11%) by far the biggest gaining sector. Meanwhile, the SPY gained 0.76%, DIA gained 0.68%, and QQQ gained 0.60% on the day. At the same time, the VXX closed down over 9% to 17.99 and T2122 climbed out of the oversold territory to 27.34. 10-year bond yields pulled back from early highs to 3.49% and Oil (WTI) has recovered from early lows to $85.53/barrel. All-in-all, just a bear trap day that maybe held support and relieved some over-extension.

In stock news, AXP announced Monday that it will be hiring 1,500 technology workers before the end of 2022 (a 2.5% headcount increase) despite other financial institutions cutting jobs. Meanwhile, TSLA announced that it has completed its production capacity expansion project at its Shanghai facility. Elsewhere, at the end of the day Monday, Bloomberg reported that banks led by BARC and BAC are moving ahead with risky leveraged buyout financing projects that had 8-10% ahead of the Fed decision, citing several project examples. (The takeaway is that, despite interest rates rising, big banks are still willing to undertake risky projects in search of an additional 4% profit above their own projected terminal Fed Funds Rate…which would make risk-free bond yields in the area of only 2.5%-3% below their risky projects.) In other news, a group of 46 US states has now appealed a lower court dismissal of an anti-trust lawsuit against META. Finally, after the close, F warned investors of an additional $1 billion in unplanned supply chain costs during Q3.

In Economic news, on Monday, the National Assn. of Home Builders Housing Market Index dropped three points to 46. Any reading below 50 indicates that single-family homebuilders have a bearish sentiment toward the housing market. Elsewhere, Fed Funds futures have now priced in an 81% chance of a 0.75% rate hike along with a 19% probability of a 1.00% hike by the FOMC on Wednesday. The US Dollar rose on these expectations, nearing the 20-year high set on September 7th. Obviously, this inversely impacts all dollar-denominated commodities such as oil, gold, and grains. Finally, the second largest US Port (Port of Long Beach) reported a decline in inbound containers in August. The Port Executive Director attributes this to cooling consumer demand and the end of pandemic-related port backlogs. (Long Beach and Los Angeles together account for 40% of container traffic from China.)

In Energy news, Reuters reports that German utility companies (RWE and Uniper) are very close to signing a long-term LNG supply contract with Qatar as at least a partial replacement for Russian LNG. The Qatari fields that would supply this gas are partly owned and operated by RDS, XOM, and COP. In a related story, Bloomberg reports that European natural gas prices fell again (its longest losing streak since July) as EU countries unveiled plans to offset costs, avoid shortages, and help household users. Elsewhere, AAA reports that US vehicle traffic fell by 3.3% in July. This was the second consecutive monthly decline in travel that the group reported. However, year-to-date, the group says miles traveled is up 1.8% over 2021 levels.

In miscellaneous news, Turkey’s President Erdogan told PBS News that Russian President Putin has pressed him on the need for peace. Erdogan went on to say that the basis of any peace deal would have to be returning all Ukrainian land (including Crimea), but that no leader will ever admit military action was a mistake. Meanwhile, the battle to liberate Luhansk has Russian proxies worried and again threatening to hold a referendum to join Russia (implying Russia would then be free to nuke the rest of Ukraine to guarantee the Donbas then remains in Russian hands). Elsewhere, US Dollar strength continues as the Euro is back below parity, the British Pound is at its lowest level going back to 1980, and the Japanese Yen is again approaching a 24-year low versus the dollar. Finally, overnight Switzerland kicked off the week’s rate hikes by increasing its benchmark rate by 1.00%.

Overnight, Asian markets were green across the board. Australia (+1.29%), Hong Kong (+1.16%), and India (+1.10%) led the region higher as China kept its benchmark interest rate unchanged. Meanwhile, in Europe, at midday, we are seeing the opposite story taking shape. Russia’s -4.03% is an outlier in the region and the FTSE (-0.09%) is mostly flat in its first trading since before the Queen’s funeral. However, the DAX (-0.65%) and CAC (-0.74%) are more typical and lead the region lower. As of 7:30 am, US Futures are pointing toward another down start to the day. The DIA implies a -0.33% open, the SPY is implying a -0.40% open, and the QQQ implies a -0.47% open at this hour. 10-year bond yield continue to spike and are now at 3.539% while Oil (WTI) is off 0.4% to $85.39/barrel in early trading.

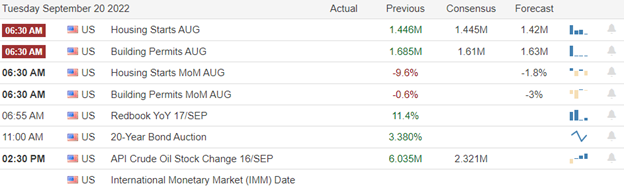

There major economic news events scheduled for Tuesday include August Building Permits and August Housing Starts (both at 8:30 am), and API Weekly Crude Oil Inventories (4:30 pm). The major earnings reports scheduled for Tuesday are limited to AJG before the open. Then after the close, SFIX reports.

In economic news later this week, Wednesday, August Existing Home Sales, EIA Weekly Crude Oil Inventories, Fed Interest Rate Projections, Fed Rate Decision, Fed Statement, Fed Economic Projections, and the Fed Chair Press Conference all are reported. On Thursday, we get Q2 Current Account and Weekly Initial Jobless Claims. Finally, on Friday, we see Mfg. PMI, Service PMI, and Fed Chair Powell speaks again.

In earnings reports later this week, Wednesday, GIS, FUL, KGH, LEN, SCS, and TCOM report. On Thursday, we hear from ACN, DRI, FDS, AIR, COST, and FDX report. Finally, on Friday there are no major earnings reports scheduled.

The downtrend remains in place but the market feels like it is pausing here, waiting on the Fed decision before making any significant moves. However, the vast majority of traders expect a 0.75% hike tomorrow (the futures say the probability is now 82%). You will have to judge for yourself whether the risk is more for a lesser or greater hike. With that said (and ahead of housing data), it looks like we will open with a gap down today. So, beware of the potential for “gap and reverse” like yesterday. Simply, just don’t get caught chasing.

The major indices all remain extended a bit to the downside at this point, at least relative to their T-line (8ema). As mentioned, the trend also remains bearish. However, there is support just below. This indecision is not a good environment for swing trading. This is a “get quick or get out” market where the intraday whip and the daily “gap and chop” could eat your account alive. So, don’t feel the need to trade. Be patient and remember that the first rule of making big money predict in the market is to not lose big money in the market.

Keep in mind that trading is our job. It’s not a hobby. So, treat it that way. Do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: BVN, NCLH, LVS, SQQQ, TZA, SPXS, MOS, WMT, NEM, NFLX, NVAX, ZS, PINS, KGC, MRNA, VALE, BAC, JPM, TSLA, FCX, CUK. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The market may struggle for energy and inspiration as we wait for Wednesday afternoon’s FOMC rate decision. We will have a few housing data points and very few notable earnings reports to inspire, so plan on some challenging price action in the next couple of days. The DIA, SPY, and QQQ have confirmed the current downtrend making new lows with the IWM lagging, trying to hold at the September lows. Unfortunately, the Friday bounce lacked the energy to test overhead resistance levels or improve the deteriorating technical conditions of the index charts.

Overnight Asian markets traded down across the board with China lowering rates and a pending Bank of Japan rate decision later this week. European markets are also seeing red this morning with all eyes on the Fed rate decision. The selling pressure continues this morning with the U.S. futures pointing to a gap down open, reversing the Friday bounce as the bear show their teeth ahead of the FOMC. Plan for challenging price action as we wait.

Economic Calendar

Earnings Calendar

Although we have a number of companies listed, we have just one confirmed, and it happens to be a notable AZO.

News & Technicals’

U.S. President Joe Biden said in an interview broadcast on Sunday that U.S. forces would defend Taiwan in the event of a Chinese invasion, his most explicit statement so far on the issue. Asked in a CBS “60 Minutes” interview whether U.S. forces would defend the self-ruled island claimed by China, he replied: “Yes, if there was an unprecedented attack.” Asked to comment, a White House spokesperson said U.S. policy towards Taiwan had not changed. Volkswagen targets a valuation of $70.1 billion to $75.1 billion for luxury sportscar maker Porsche. Volkswagen was expected to announce the pricing range of the Porsche IPO, planned for late September or early October, later in the evening. UBS downgraded its full-year growth forecasts from 3% to 2.7% for 2022 and from 5.4% to 4.6% for 2023. Their Zero-covid policy has essentially “stomped on human investor confidence in China,” said Mattie Bekink, China director for the Economist Intelligence Corporate Network. Goldman Sachs economists said the next key level to watch for the Chinese currency is 7.2 against the dollar.

In a bid to control domestic prices, the Indian government banned exports of broken rice and slapped a 20% export tax on several varieties of rice starting Sept. 9. The Philippines and Indonesia will be most vulnerable to the ban, according to Nomura. India accounts for approximately 40% of global rice shipments, exporting to more than 150 countries. Treasury yields held frim Monday morning with the 12-month at 3.95%, the 2-year at 3.93%, the 5-year at 3.69%, the 10-year at 3.49%, and the 30-year at 3.55%.

Friday began with a gap down, but the bulls went to work to rally back to resistance levels but lacked the energy or inspiration to get the job done. The DIA, SPY, and QQQ confirmed the current downtrend making lower lows, but the IWM stubbornly held firm at the September lows. Unfortunately, China’s weakening economy that cut rates during the night and the energy crisis in Europe combined with a pending FOMC rate increase has the bears active in the premarket this morning. Price action will likely remain challenging as we wait on the FOMC and several housing data points as the only inspiration.

FDX removing guidance and predicting a global recession had markets spooked on Friday. As a result, the 3 major indices gapped down (between 1.1% and 1.5%) at the open and has then oscillated sideways in a fairly tight range until 2:30 pm. At that point the bulls stepped to rally for the rest of the day, closing near the highs of the day. (However, still the lowest close in two months.) This action gave us gap-down, indecisive Spinning Top candles across all the major indices. This will put all 3 major indices in a large Bearish Engulfing signal on the Weekly chart.

On the day, all 10 sectors are firmly in the red. The Energy and Industrials sectors led the way lower while Comm. Services and Consumer Defensive held up the best. SPY fell 1.18%, DIA lost 0.76%, and QQQ fell 0.66%. The VXX gained 3.45% to 19.81 and T2122 dropped deep into the oversold territory at 5.87. 10-year bond yields are back down to 3.453% and Oil (WTI) is mostly flat at $85.28/barrel. So, overall, it has been a fearful and yet undecided day in the market as most eyes focus on the Fed decision coming this week.

In Economic news, on Friday, Michigan Consumer Expectations came in slightly above expectations (59.9 vs 59.7 forecast) while current Michigan Consumer Sentiment came in below estimates (59.5 versus 60.0 forecast). Bloomberg also reported interesting news about the housing markets that points toward the bifurcation of the economy. If seems that in July nearly one-third of home purchases came in all-cash deals (buyers who paid cash and did not need a mortgage). Records for such things are not kept, but this seems like a huge percentage. On Saturday, GS cut its US Economic Growth forecast for 2023 from 1.5% to 1.1% after it raised its terminal Fed Rate to 4.25% (Fed Funds have priced in 4.5% terminal). Finally, in what points toward a downturn, WBD has fired 100 television ad salesmen as NFLX also announced another round of 300 terminations in a cost containment move.

In stock news, Reuters reported that the details of SEC accounting guidance for any companies that hold cryptocurrency assets (announced on the last day of March) are now fleshed out. These additional costs and capital reserve holding requirements have caused major lenders (GS, JPM, BK, WFC, STT, etc.) to put cryptocurrency projects on hold (or outright canceled). After the close Friday, US Dept. of Justice officials have asked the court to take part in oral arguments in the Court of Appeals in the Epic Games vs. AAPL antitrust lawsuit. The DOJ is expected to be on the Epic side, but neither party objected to the DOJ request. Also, after the close, BMY and ABBV both announced minor job cuts (360 for both companies combined). On Saturday, the ECB asked AMZN and 4 European companies to submit proposals for the creation of a new Digital-Euro (cryptocurrency). This is part of a two-year prototyping and investigation phase of the project.

In Energy news, Germany took control of a major Russian-owned oil refinery Friday. (This was the Schwedt refinery owned by Rosneft. This refinery supplies 90% of the fuel used in Berlin.) Meanwhile, on Sunday, China’s August gasoline exports were reported as almost double (+97.4%), while its LNG imports for the month fell 28.1% from a year earlier. Overnight, Bloomberg reported that after a Russian Gazprom unit (seized by Germany earlier this year after the invasion) canceled shipments to India, GAIL India has been forced to buy 3 LNG tankers (for October to November delivery) on the open market, paying twice the price it had previously paid Russia.

In miscellaneous news, the Fed is not the only central bank looking at rate hikes this week. Japan, the UK, Norway, Sweden, Switzerland, Taiwan, and several other countries all have rate meetings set for this week. While the Fed is widely expected to continue the inflation-fighting theme with another 0.75% hike, much of the rest of the world (especially places like the Philippines, Indonesia, and even Turkey) is likely to take a softer approach. (Counting on the US and EU to do the heavy lifting on taming global inflation.) Speaking of Taiwan, overnight President Biden answered an interview question, stating that the US forces would defend Taiwan from “any unprecedented attack.” (That was the fifth time he has made a similar statement on Taiwan since the Russian invasion of Ukraine.) Finally, note that the UK markets are closed for the Queen’s funeral and Japan is also closed for a national holiday.

Overnight, Asian markets were nearly red across the board. Only India (+0.52%) and Thailand (+0.07%) were able to manage to hang onto the green. Meanwhile, South Korea (-1.14%), Malaysia (-1.08%), and Hong Kong (-1.04%) led the region lower. In Europe, we see a similar story taking shape at mid-day. Only Russia (+0.30%) is holding green. At the same time, the DAX (-0.69%), and CAC (-1.23%) are leading the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a gap lower to start the day. The DIA implies a -0.85% open, the SPY is implying a -0.87% open, and the QQQ implies a -0.92% open at this hour. 10-year bond yields are up to 3.506% (the highest level since 2011) and Oil (WT) is down almost 2% to $83.55/barrel in early trading.

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for Monday are limited to AZO before the open. (AZO reported a beat on both the top and bottom lines early today.)

In economic news later this week, Tuesday we get August Building Permits, August Housing Starts, and API Weekly Crude Oil Inventories. Then Wednesday, August Existing Home Sales, EIA Weekly Crude Oil Inventories, Fed Interest Rate Projections, Fed Rate Decision, Fed Statement, Fed Economic Projections, and the Fed Chair Press Conference all are reported. On Thursday, we get Q2 Current Account and Weekly Initial Jobless Claims. Finally, on Friday, we see Mfg. PMI, Service PMI, and Fed Chair Powell speaks again.

In earnings reports later this week, AJG and SFIX report Tuesday. Then Wednesday, GIS, FUL, KGH, LEN, SCS, and TCOM report. On Thursday, we hear from ACN, DRI, FDS, AIR, COST, and FDX report. Finally, on Friday there are no major earnings reports scheduled.

The downtrend continues with the gap lower looking to take at least the SPY and QQQ indices down near to a potential support level. With that said, and while there may be some movement today, many traders are going to be waiting to see whether the Fed gives us any surprises. (Talking heads are all over the place, calling for every scenario from +0.25% to +1.00% on Wednesday. However, traders have priced in +0.75% judging by the Fed Funds Futures.)

The major indices are extended to the downside at this point, far below their T-line and with T2122 deep into the oversold territory. However, we have seen indecision (more wick than candle body) the last 3 days (as well as in the premarket session today). So, expect some volatility after the gap lower…but also be prepared if the market goes dead while traders begin waiting on the FOMC. All we can do is trade the chart (the actual price action) and not what you predict will happen.

Remember that trading is our job, not a pastime or hobby. So, treat it that way. Do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No Tade Ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stocks gapped lower at the open Thursday (0.14% in DIA, 0.44% in SPY, and 0.89% in QQQ). Price then proceeded to meander sideways in a fairly tight range until 2 pm, when the bears took over to drive the market to new lows at about 3:30 pm. However, a slight rally in the last 30 minutes took us out not far up off the lows. This left us with black, Inverted Hammer type (maybe you’d call QQQ a spinning Top) candles in the 3 major indices. In addition, all 3 indices have either broken out of or are now right at the breakout level of, their “dreaded h” patterns. So, the bears will have the wind at their back on Friday.

On the day, eight of the 10 sectors were in the red. Healthcare (+0.20%) was really the only sector managing to stay green along with Financial Service (+0.01%) while Energy (-2.33%) and Utilities (-2.32%) were by far the weakest. The SPY closed down 1.14%, DIA lost 0.54%, and QQQ lost 1.67%. The VXX ended up 0.31% to 19.15 and T2122 remains in the oversold territory at 13.24. 10-year bond yields are climbing to 3.449% and Oil (WTI) is down just under 4% to $85.09/barrel. So, overall, it was an indecisive day until the bulls ran out of gas mid-afternoon and the bears took over to take us out near the lows.

In Economic news, August Retail Sales grew 0.3%, but some of that increase was in inflated prices rather than additional purchases. Weekly Jobless Claims came in a bit lower than expected at 213k (226k forecast). Meanwhile, both the Philly Fed Mfg. (at -9.9 vs. +2.8 forecast) and NY Empire State Mfg. Index (-1.50 vs -13.00 forecast) came in negative with Philly coming in lower than expected and NY coming in above the expectation. August Exports were down 1.6% while Imports were down 1.0%. July Business and Retail Inventories came in as expected. However, August Industrial Production came in below expectations (-0.2% vs. +0.1% forecast). So, overall, we had mixed results in terms of what the Fed may make of economic growth (if they were to just look at today’s data).

In stock news, after hours, FDX withdrew its 2023 forward guidance while saying it expects a global recession next year. The company also warned it will be adversely impacted by global softness in shipments in the current quarter, citing Asia and Europe in particular for economic weakness. FDX said it now estimates Q1 could come in at $3.44 EPS (far below the current consensus of $5.14). FDX stock was down 16% in past-market trade on the news. Elsewhere, 6 companies announced share repurchase plans today. (TXN announced a dividend increase as well as an additional $15 billion on top of the existing plan of $8.2 billion for share buybacks. KFRC announced an unspecified repurchase authorization during the period September 16 – November 2, 2022. MQ authorized $100 million in share buybacks. ARW added $600 million to its existing buyback program. OLP declared a $0.45 quarterly dividend and approved a small $5.2 million addition to its remaining $2.3 million repurchase program. And JG authorized $5 million of share buybacks over the next year.) Meanwhile, the Consumer Financial Protection Bureau announced it will start regulating “buy now, pay later” companies like AAPL, SQ, PYPL, and AFRM.

In Energy news, the deal to avert a rail strike hit oil hard on Thursday. This caused the “crack spread” (refiner profit margin) to close at its lowest level since March. Elsewhere, Germany is now in advanced takeover talks with the 3 major gas-importing companies in that country (Uniper SE, CNG AG, and Securing Energy…which was formerly Gazprom Germania). Finally, on Thursday the Biden Administration announced a plan to accelerate Off-Shore Floating Wind Electrical Generation, setting a new goal of 15 gigawatts of floating offshore capacity by 2035 as part of the broader (and nearer) goal of having 30 gigawatts of offshore wind capacity in production by 2030. (The latter goal includes floating as well as anchored wind farms.) Companies in that space include NEE, NEP, GE, WNDY, TPIC, and the etf FAN.

In China news, Asia woke up to a raft of Chinese Economic Reports. Among these were August Housing Prices (-1.3%), August Industrial Production (+4.2%, beating estimates of +3.8%), August Retail Sales (+5.4%, beating estimates of +3.5%), and August Unemployment (5.3%, down slightly). These reports did nothing to improve the hopes for a second-half recovery as the Chinese Property slump/debacle and new Covid-19 lockdowns continue to rock the second largest economy in the world. This came a day after Chinese President Xi Jinping met with Russian President Putin (and reportedly raised concerns over the Russian invasion and losses they have suffered). Finally, in a bid to bolster US competitive advantage, guarantee sources, and limit the transfer of technologies, President Biden issued an executive order that expanded the regulatory duties and power of the Committee on Foreign Investment in the US. The order requires them to block foreign acquisitions and investments by countries (especially China) with adversarial aims into US technology firms (especially AI, microelectronics, biotech, quantum computing, clean energy technologies, etc.). However, the order does not regulate “outbound investment” of American companies in China, which has been a major source of lost intellectual property in the past. (China requires foreign companies operating in China to turn over trade secrets and data.)

Overnight, Asian markets were nearly red across the board. The lone holdout was Singapore (+0.01%) which hung onto the green by its fingernails. Meanwhile, it was Shanghai (-2.30%), Shenzhen (-2.30%), and India (-1.52%) leading the region lower. In Europe, a similar picture is taking shape at mid-day. The FTSE (+0.12%) is the only real green in the region while the DAX (-1.45%) and CAC (-1.30%) are leading the region lower in early afternoon trading. As of 7:30 am, US Futures are pointing toward a gap down to start the day. The DIA implies a -0.72% open, the SPY is implying a -0.80% open, and the QQQ implies a -0.95% open at this hour. 10-year bond yields are up to 2.469% and Oil (WTI) is up two-thirds of a percent to $85.62/barrel in early trading.

The major economic news events scheduled for Friday are limited to the Michigan Consumer Sentiment (10 am). Friday is also Quadruple Witching, so watch for pinning action. There are no major earnings reports scheduled for the day.

Thursday’s action and the futures this morning suggest we are headed down to retest the July lows. However, most eyes are trained on the FOMC and traders are trying to prejudge what the Fed will do next week. Talking heads can’t make up their minds with some calling for a 1.00% increase while others say we need to ease off the increases and go 0.50% or even 0.25% this month. The Fed gets the only vote and all we know for sure is that they have been talking in such a way as to suggest 0.75% and that is what is baked into the Fed Funds Futures.

With that backdrop, we should note that the bears clearly have control. However, the gap lower implied by futures will put us pretty extended from both the T-line and in terms of the T2122 reading. So far, the potential support levels don’t seem to be helping the bulls hold the line and fight bearish momentum. All we can do is trade the chart (the actual price action) and not what you predict will happen. Still, keep in mind that it is Friday and that means it’s time to consider the weekend news cycle. Do you need to take profits, hedge, or reduce your position sizes? Think about it.

Remember that trading is our job, not a pastime or hobby. So, treat it that way. Do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: DXD, JDST, LABD, SPXS, FAZ, ERY, SPXU, DRIP, SQQQ, FNGD, DOG, SDOW, QID, RWM, SQXS, TZA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Most of Wednesday could be described as frustrating and choppy as the bulls and bears slept in waiting for all the economic reports before the bell today. The good news is by the end of the day, the bulls managed to hold September lows. But, unfortunately, they did so in not a very convincing way leaving more questions than answers. So, expect price volatility and be ready for just about anything at the open, with bond yields continuing to rise, with a hefty rate increase next week.

Asian market trade was relatively flat during the night as Chana kept mid-term rates steady as their currency weakened against the dollar. European markets also trade mixed this morning as they cautiously await U.S. economic data. U.S. futures had given up early gains at the time of writing this report with several potential market-moving reports before the open. Plan carefully as another day of wild price action is possible.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we only have seven confirmed earnings reports; the only notable one for the day is ADBE.

News & Technicals’

A tentative railroad agreement could avert a national rail strike that would have shut down a vital part of the U.S. transportation network. According to the Association of American Railroads, the new contracts provide 24% pay increases over 5 years from 2020 through 2024 and include immediate payouts averaging $11,000 upon ratification. More than three months after Elon Musk’s back-to-office edict, Tesla still doesn’t have the room or resources to bring all its employees back to the office. The company is now surveilling employees’ attendance, with Musk and other execs receiving detailed weekly reports on absenteeism. Some employees who were previously designated as remote workers but said they might be unable to relocate to meet the return-to-office requirements were dismissed in June. Ethereum’s biggest-ever upgrade just took effect, in what industry experts call a game changer for the entire crypto sector. Thus far, all signs suggest the so-called merge — which is designed to cut the cryptocurrency’s energy consumption by more than 99% — was a success.

Ford on Wednesday unveiled the redesigned 2024 Mustang hardtop and convertible with two gas-powered engines. The automaker said redesigning the iconic car without any electrification is part of its “Mustang family” strategy, including the all-electric Mustang Mach-E crossover. As a result, the Mustang could be the last gas-powered muscle car from the Detroit automakers — a narrowing of the segment that seemed far-fetched even a few years ago. In addition, Walmart is launching a virtual try-on tool to help shoppers see how a shirt, dress, or another clothing item would look on their bodies. It is the latest way the retailer uses technology from Zeekit, a startup it acquired last year. The discounter is launching the tool as some shoppers trim back purchases of discretionary purchases, such as clothing. Treasury yields rose early Thursday, with the 6-month at 3.75%, the 12-month at 3.92%, the 2-year at 3.83%, the 5-year at 3.64%, the 10-year at 3.45%, and the 30-year at 3.50%.

Both the bulls and bears slept in on Wednesday in a choppy session that finally got a little bullish attention as the dark pool trades consolidated to the market at the end of the day. Though the light volume session was frustrating, they did manage to hold the September lows as traders assessed the risk of all the potential market-moving reports on Thursday morning. Once again, premarket futures are trying to put on a bullish face, but with Jobless Claims, Philly Fed, Retail Sales, Import/Export prices, and Empire State numbers before the bell, anything is possible by the open. After that, we have Industrial production, business inventories, and a natural gas report. We should plan for another volatile session keeping a close eye on support and resistance levels keeping in mind the Fed will be rolling off their balance sheet today with rate increases planned for next week.

Stocks gapped very modestly higher at the open Wednesday following the extremely bearish gap and run Tuesday. However, all 3 major indices spent the rest of the day crossing back and forth that gap space. With that said, the bears picked up a little strength in the afternoon to take us back down to new lows…only for the bulls to step in and rally markets for the last 30 minutes of the day. This action left us with indecisive (Doji-like) candles in all 3 major indices.

On the day, seven of the 10 sectors were green. However, Energy (+2.64%) was far and away the most bullish sector while Basic Materials (-0.96%) was by far the most bearish sector. The SPY gained 0.38%, The DIA gained 0.11%, and the QQQ gained 0.79%. Meanwhile, the VXX was up less than half of a percent to 19.09 and T2122 climbed a bit, but remains oversold at 17.99. 10-year bond yields have pulled back after being up earlier to 3.41% and Oil (WTI) is up 1.58% to $88.69/barrel. All-in-all, the bears did not get any follow-through from Tuesday’s massacre. However, there was also nothing for bulls to really hang their hat on at all…the bears are clearly still in charge.

In Economic news, August wholesale prices (as measured by the PPI) fell 0.1% which is in contrast to Tuesday’s CPI increase. (The annual rate was 7.3%, down from the July reading of 7.7% annualized.) This was modestly encouraging to bulls during the premarket. Later in the morning, EIA Weekly US Crude Oil Inventories showed a 2.442-million-barrel build. Elsewhere, Amtrack has canceled all long-distance trains until after the railroad strike expected Friday is resolved. In related news, CSX, UNP, and NSF have stopped rail shipments of refrigerated and volatile or decay-sensitive products like food, chemicals, hazardous materials, etc. until the same potential strikes are resolved. (9 of 12 unions have reached a tentative deal with the railroads, 1 has rejected the management offer, and the other 2 are undecided as of Wednesday night.)

In stock legal news, TSLA was sued by owners over alleged false “Autopilot” and “Full Self-Driving” claims made by the automaker. Elsewhere, CA sued AMZN over violations of the state’s antitrust law for blocking price competition. Meanwhile, WFC reached a $94 million settlement to resolve a class-action lawsuit over impacting credit ratings by putting 213,000 mortgage borrowers in forbearance without the customer’s request or approval during the pandemic. Finally, the Wall Street Journal reported that Fed regulators are frustrated with the progress of C since it was reprimanded over its risk management system. Sources told the paper that C has been told it will face charges if it does not fix its risk management process very soon.

In miscellaneous news, 4 companies announced share repurchase plans Wednesday. These include JNJ (up to $5 billion), CHH (5 million shares, bringing the total to 6.7 million), CMCSA (increased to $20 billion), and NETI ($50 million). Elsewhere, GOOGL announced it will cut project funding and jobs in its “New Idea Incubator.” Meanwhile, the Ethereum merge (shifting from “proof of work” to “proof of stake”) is expected today. This merge will essentially kill Ethereum mining operations and dramatically limit the supply of the coin that is available.

In Energy news, oil was up Wednesday on talk of oil being used for heating in Europe if natural gas supplies remain cut by Russia. Meanwhile, in Congress, Senate Majority Leader Schumer announced that the stop-gap government funding bill (which must be passed and signed before Sept. 30 to avoid a shutdown) will include plans demanded by WV quasi-Democrat Manchin. Those riders will ease environmental protections and energy project permitting requirements. (This was part of the deal to get Manchin’s vote for the Inflation Reduction Act earlier this year.) However, progressive House Democrats (who must also pass any stop-gap bill) have not been consulted and are opposing the amendments on environmental grounds. Across the pond, the EU has now proposed a windfall profit tax for wind, solar, nuclear, and coal electricity generators by capping the price they could charge to $180/MWh (current prices are just below $500/MWh) in the region.

Overnight, Asian markets were mixed on mostly very modest moves. Shenzhen (-2.10%) and Shanghai (-1.16%) were the outliers with most exchanges moving only slightly in either direction. In Europe, we see the same picture taking shape (minus the Chinese outliers) at mid-day. The FTSE (+0.26%), DAX (-0.12%), and CAC (-0.28%) are typical and lead the region in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modestly red start to the day. The DIA implies a -0.14% open, the SPY is implying a -0.20% open, and the QQQ implies a -0.32% open at this hour. 10-year bond yields are back up to 3.449% and Oil (WTI) is off six-tenths of a percent to $87.95/barrel.

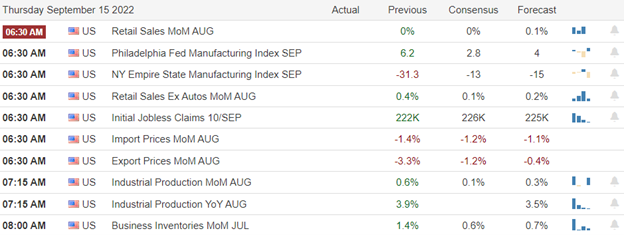

The major economic news events scheduled for Thursday include August Imports / Exports, Weekly Jobless Claims, NY Empire State Mfg. Index, Philly Fed Mfg. Index, and August Retail Sales, (all at 8:30 am), August Industrial Production (9:15 am), July Business Inventories and July Retail Inventories (both at 10 am). The major earnings reports scheduled for the day are limited to ADBE before the open. There are no major earnings reports after the close.

In economic news later this week, on Friday, we get Michigan Consumer Sentiment. Friday is also Quadruple Witching. In terms of earnings later this week, there are no earnings reports scheduled for Friday.

Wednesday was an indecisive, blah day in the market. Premarket futures are implying a similar start today, but we do have quite a bit of data coming before the opening bell. Overall, I would say it looks like traders are still trying to digest the surprise CPI number and prejudge what the Fed will do next week. Talking heads keep bringing up a 1.00% increase by the FOMC, but Fed Funds Futures have priced in 0.75%. In last-minute news, President Biden announced that a tentative deal has been reached between the Rail Worker Unions and the CSX, NSF, and UNP. This deal will avert a strike and avoid serious pain for US supply chains. This should be very good for the bulls (who had worried about impacts). However, I’m not sure many traders understand the real implications of a rail shutdown…so response could be muted.

With that backdrop, we should note that all 3 major indices remain below their downtrend lines and below their T-lines. The market bias is bearish. However, while the bears have control on the daily chart, the bulls have support just below to help them fight that momentum. So, keep an eye on that in the premarket news. Beyond that, trade the chart (the actual price action) and not what you predict will happen. We can’t be first or last over the hill if we want to succeed.

Remember that trading is our job, not a pastime or hobby. So, treat it that way. Do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: SQQQ, SPXU, DXD, EOG, TWTR, RCL, CCL, AMZN, AAPL. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

A CPI reading hotter than expected woke up angry bears Tuesday morning, with indexes failing their 50-day moving average supports once again. As a result, the U.S. dollar surged higher, and treasury yields spiked, adding pressure to an already hawkish FOMC. September lows held as support so far, but with another inflation number, this morning with the PPI, uncertainty abounds. So, prepare for another day of challenging price action as the battle to hold the Sept. lows begins.

Asian markets had a rough night in reaction to the U.S. inflation data, with the Nikkei leading the selling down 2.78%. European markets trade mostly lower this morning as they cautiously wait for the PPI number. However, U.S. futures try to put on a brave face ahead of the producer prices hoping for a hump day bounce after the Tuesday reversal. Once again, anything is possible by the open, and keep in mind the Fed balance sheet runoff ramps up with an FOMC decision next week.

Economic Calendar

Earnings Calendar

As we slide toward the end of the quarter, earnings report numbers continue to dwindle, with only eight confirmed reports today. Notable reports include DOOO & TNP.

News & Technicals’

Rather than fuel, food, shelter and medical services drove costs higher in August, slapping a costly tax on those least able to afford it. As a result, the food at home index, a good proxy for grocery prices, has increased 13.5% over the past year, the most significant rise since March 1979. For medical care services, the monthly increase of 0.8% was the fastest monthly gain since October 2019. Veterinary care was up 10% from a year ago. The consumer price index rose 9.9% annually, according to estimates published Wednesday by the Office for National Statistics. Last week, new British Prime Minister Liz Truss announced an emergency fiscal package capping annual household energy bills at £2,500 ($2,881.90) for the next two years. President Joe Biden and several Cabinet secretaries have been in talks with the railroad unions and the companies for months to try to avert the strike. However, two of the largest unions, representing half of railroad union workers, are still negotiating. That leaves about 60,000 workers ready to strike if a deal is not made. About 40% of the nation’s long-distance trade is moved by rail. If the unions strike, more than 7,000 trains would be idled.

About 40% of the nation’s long-distance trade is moved by rail. If the unions strike, more than 7,000 trains would be idled. As a result, JPMorgan can adjust its cost structure not only by cutting jobs but also by reducing the size of employee bonuses, he said. Trading has provided a welcome boost this year, however. JPMorgan said market revenue was headed for a 5% increase from a year earlier, as strong activity in fixed income offset lower equities trading revenue. Treasury yields continued to rise Wednesday, with the 6-month at 3.72%, the 12-month at 3.87%, the 2-year at 3.78, the 5-year at 3.61%, the 10-year at 3.43%, and the 30-year at 3.51%.

The CPI report woke up some angry bears Tuesday morning, reinforcing aggressive rate increases by the FOMC as food and medical cost increases stepped up to drive inflation. The selling created technical damage as the indexes once again failed their 50-day moving averages. However, September lows are held as price support as we face another inflation this morning with the PPI. The morning’s question is, can the Sept. lows continue to hold after the producer prices come out? We will soon find out, but traders should continue to expect challenging price action. The rising dollar and the sharp increases in bond yields also present a substantial stumbling block for the U.S. market and the global market conditions. Plan for more uncertainty with Fed balance sheet runoffs and rate increases around the corner.

The bulls were in a great mood early in the premarket Tuesday…too great of a mood. Then the August CPI came in hotter than forecast (and much hotter than the bulls had expected that it would come in well below forecast) and at that point, it was “Katy bar the door.” So, instead of gapping up two-thirds of a percent, all 3 major indices flipped in premarket and gapped down very significantly (between 2% and 3%) at the open. From that open, we saw follow-through by the bears until 11:30 am. Next came a two-hour mid-day pause with the bears finally stepping back in with gusto at 1:30 pm to steadily sell off the 3 major indices the rest of the day. This action left us with Bearish Kicker candles, which gapped down through the T-line (and downtrend line) and kept going south in the SPY, DIA, and QQQ.

On the day, all 10 sectors are down hard with Energy (-2.52%) and Utilities (-2.57%) as the laggards and Technology (-5.00%) leading the way lower. The SPY fell 4.31%, the DIA fell 3.96%, and the QQQ fell 5.48%. Meanwhile, the VXX is up 5% to 19.04 and T2122 dropped all the way from overbought to oversold at 13.21. After being down in the premarket, 10-year bond yields have spiked up to 3.423%, and Oil (WTI) is just on the red side of flat at $87.58/barrel. Overall, this was the worst day since 2020 across all 3 major indices.

In Economic news, as mentioned above, August CPI came in at an annual rate of 8.3% when 8.1% was forecast and there had been a lot of talk in the last few days expecting 8.0% based on the continued drop in gas prices. With that said, the August CPI Annual Rate was still better than the 8.5% in July. (As a result, Feds Fund Futures now show that traders give a 35% probability of a Fed hike of 1% next week.) Later in the afternoon, the August Federal Budget Balance also came in worse than expected at a $220 billion deficit versus a $213.5 billion deficit forecast and the July level at a $211 billion deficit. Elsewhere, the Dollar rallied 1.48%, bringing the Euro back below parity and gaining 1.2% against the Yen. Finally, after the close, API reported that US Oil Inventories rose just over 6 million barrels last week (compared to a 3.6 million barrel build the week before). However, the same group reported a gasoline drawdown of 3.23 million barrels for the same week.

In TWTR news, Republican Senator Lindsey Graham proposed Tuesday that TWTR, META and other major social media platforms should face increased regulation and be required to obtain a renewable license to operate. The Senator said he was working on legislation to do this along with other senators from both sides of the aisle. At the same hearing, the TWTR whistleblower (best known as “Mudge”) informed the Senate that the FBI previously told the company about Chinese government agents working for Twitter. However, the company was struggling internally to weigh the cost of protecting user data versus losing the Chinese advertising revenue if they were to take action against the Chinese. In the end, the company decided not to jeopardize the very lucrative revenue stream.

In other stock news, in contrast to GS (which announced coming job cuts on Monday), on Tuesday, both JPM and BAC both told media and investors that said they were more optimistic, would be cautious about doing any layoffs, and are fine with their current headcounts for now. Elsewhere, SBUX told investors that has plans to open 9,000 new stores in China by 2025. Meanwhile, the US Dept. of Commerce announced a deal with GOOGL to produce chips that researchers can then use to develop both nanotechnologies and other semiconductor chips. These chips will be produced by SKYT. (This is part of the spending from the recent Chips bill.) Finally, after the close, AAPL announced it is creating a new Ad division and will launch ads within the AAPL App Store before the holiday season.

In miscellaneous news, Bloomberg reported that the US will begin refilling its strategic petroleum reserves once oil falls below $80/barrel. So, that may put a floor under oil to some extent and for a while after oil prices reach that level. Elsewhere, President Biden’s National Security Advisor Sullivan told the press that they are preparing another aid package for Ukraine to help follow on to counteroffensive that country has used to liberate more than 2,300 sq. miles of Ukraine from Russian occupation in the last week. Meanwhile, European Commission President von der Leyen said they would raise an additional $140 billion (on top of the $225 billion of leftover Covid Relief funds that were approved by the EU) for use in cushioning consumer cost-of-living increases. On related news, Germany will increase its stake (and may fully nationalize) the country’s largest gas importer (Uniper SE). Finally, US mortgage demand fell again last week as interest rates rose. The national average 30-year fixed-rate mortgage for a conforming loan (20% down) went from 5.94% to 6.01%. At the same time, loan applications fell 4% for refinancing loans and were flat on the week for new purchase loans.

Overnight, Asian markets were down across the board. Japan (-2.78%), Australia (-2.58%), and Hong Kone (-2.48%) led the region lower. In Europe, with the exception of the FTSE-MIB (+0.57%), the same story is taking shape, just with less gusto. The FTSE (-0.96%), DAX (-0.48%), and the CAC (-0.32%) are leading the region lower on smaller moves in early afternoon trade. Even Russia (-1.62%) has not seen the bearish momentum we saw in the US yesterday. As of 7:30 am, US Futures are pointing toward a modestly green start to the day…ahead of data. The DIA implies a +0.28% open, the SPY is implying a +0.34% open, and the QQQ implies a +0.33% open at this hour. 10-year bond yields are up slightly to 3.442% and Oil (WTI) is flat at $87.24/barrel in early trading.

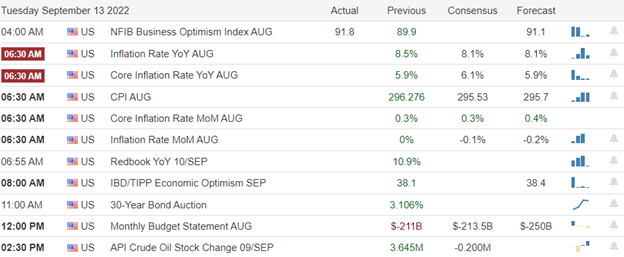

The major economic news events scheduled for Wednesday are limited to August PPI (8:30 am) and EIA Weekly Oil Inventories (10:30 am). The only major earnings report scheduled for the day is DOOO before the open.

In economic news later this week, on Thursday, we get August Import/Exports, Weekly Jobless Claims, NY Empire State Mfg. Index, Philly Fed Mfg. Index, August Retail Sales, August Industrial Production, July Business Inventories, and July Retail Inventories. Finally, on Friday, we get Michigan Consumer Sentiment. Friday is also Quadruple Witching.

In terms of earnings later this week, Thursday ADBE reports. However, there are no earnings reports scheduled for Friday.

Yesterday showed just how binary events can cause markets to react like a jilted lover. Small disappointments can sometimes lead to a face-ripping storm. Those of you who were very short the market had a glorious day (just don’t forget that event could have gone the other way) and those of you who were too long the market learned a valuable lesson about binary risk events. In either case, we’ve now had that zag I’ve been telling you was coming. The good news is that the market always overreacts, re-reacts, and reacts again. In other words, we know another zig is coming sometime soon.

With that backdrop, we should note that all 3 major indices are back below their downtrend lines and below their T-lines. The market bias is bearish. However, while the bears have control on the daily chart, the bulls have support just below to help them fight that momentum. The PPI news should not be such a binary risk as the CPI, but we may still see a reaction. So, keep an eye on that in the premarket. Beyond that, trade the chart (the actual price action) and not what you predict will happen. We can’t be first or last over the hill if we want to succeed.

Remember that trading is our job, not a pastime or hobby. So, treat it that way. Do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Analysts and talking head pontificators suggest a wide range of possibilities when the CPI number releases at 8:30 AM eastern. Some say prepare for a powerful rally, while others suggest new market lows are on the way. Still, others say the numbers will be confusing with contradictory results from the monthly to core numbers. So, although the entire world is waiting and watching, the only thing that matters is how the market reacts to the data! Plan for the price action to be initially volatile and dangerous except for the most experienced day traders. After that, anything is possible but keep in mind the bigger picture of a slowing global economy and an aggressive FOMC rate increase just around the corner.

While we slept, the Asian market rose slightly with cautious hope waiting on the U.S. economic numbers. European markets see modest gains across the board as they watch the U.S. inflation data report. But, with bold anticipation, U.S. futures point to a substantial gap up open ahead of the CPI report. However, anything is possible as the world reacts to the data. So, expect some wild and challenging price action that could include some big point whipsaws as investors digest the numbers.

Economic Calendar

Earnings Calendar

Tuesday is another very light day on the earnings calendar with just 12 confirmed reports, most of which are tiny small caps companies. So, the only marginally notable report will be from CNM today.

News and Technicals’

Peloton announced Monday that co-founder John Foley is resigning as executive chairman. Chief Legal Officer Hisao Kushi, another co-founder, is also departing. Uber veteran Tammy Albarrán will replace him. The changes come as CEO Barry McCarthy orchestrates a massive transformation plan for the fitness company. Nintendo said sales of Splatoon 3 in Japan surpassed 3.45 million units in the first three days since its Sept. 9 launch, marking a new record. Nintendo shares rose 5% on Tuesday after the announcement. Later Tuesday, the company will also hold its Nintendo Direct event, where it will reveal details of future games, which will help keep up the momentum for its aging Switch console. Oracle came up short on profit, but its revenue met expectations. The company closed its $28 billion acquisition of health data software maker Cerner in the quarter. According to a statement, revenue growth in the quarter ended Aug. 31 accelerated from the 5% it posted in the prior quarter.

Credit Suisse expects the Federal Reserve to pause interest rate hikes sooner than widely expected due to tumbling inflation. As a result, according to the firm’s chief U.S. equity strategist, it will launch a powerful market breakout. The August consumer price index will be released Tuesday at 8:30 AM. ET, and it is expected to show inflation is moderating. The report could be confusing because economists surveyed by Dow Jones expect headline CPI to decline by 0.1%, but it is expected to rise by 0.3%, excluding energy and fuel. The report is seen as key guidance for next week’s Federal Reserve rate decision. Still, economists say it is also critical for the longer-term view on interest rates since it could show whether some causes of inflation are receding. Treasury yields moved very little early Tuesday, with the 12-month at 3.60%, the 2-year at 3.52%, the 5-year at 3.40%, the 10-year at 3.32%, and the 30-year at 3.48%.

According to the vast amount of pontificators, the CPI number could plunge the market to new depths or send us into the stratosphere with a powerful rally! But, no matter the number, the most important thing is how the market reacts. One thing we can most likely count on is the reaction will likely create significant volatility rewarding some and punishing others at the open, which could be anything! But, despite how the market reacts, it’s unlikely to deter the Fed from raising rates aggressively in the coming FOMC meeting but may affect future decisions. In addition, the weakening global conditions and geopolitical issues will continue to be stumbling blocks we will have to deal with moving forward. So, fasten your seatbelt, plan carefully and get ready for the fireworks to begin.