Recession Fear, Volatility Drive Markets

The large-cap indices opened flat on Thursday while the QQQ gapped down about 0.40%. However, the bulls stepped in right away to rally all three major indices by 1.3% to 2% over the first hour, reaching the highs of the day at about 10:30 am. From there we saw a sideways grind for an hour before the bears stepped in to lead a long, steady selloff, reaching the lows of the day at 2:30 pm. The rest of the day saw a sideways rollercoaster ride not too far from the lows. This action gave us a black-bodied Inverted Hammer-type candle in the SPY and DIA. The QQQ formed a black-bodied Doji with a large upper wick. The SPY and QQQ both retested and slightly broke below their T-line (8ema).

On the day, seven of the ten sectors were in the red. Communications (+0.55%) was by far the biggest gaining sector while Utilities (-2.22%) and Industrials (-1.72%) led the way lower. The SPY lost 0.83%, DIA lost 0.34%, and QQQ lost 0.51%. The VXX fell 1.31% to 20.33 and T2122 fell but remains in the mid-range at 36.73. 10-year bond yields spiked again to 4.241% and Oil (WTI) was flat at $85.71/barrel. So, all-in-all, it was another indecisive day punctuated by intraday reversals.

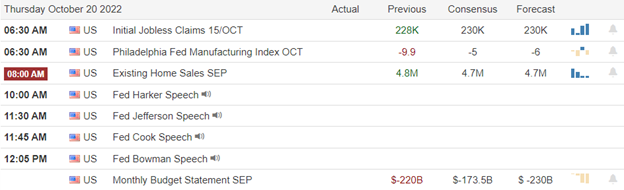

In economic news, Philly Fed Mfg. Index came in as -8.7, which was far worse than the -5.0 forecast, but also better than last month’s -9.9. At the same time, Weekly Initial Jobless Claims came in much better than was expected at 214k (versus the 230k forecast and last week’s 226k). Meanwhile, September Existing Home Sales fell 1.5% to a 10-year low of 4.71 million (which was essentially in line with the forecast of 4.70 million, but worse than the August number of 4.78 million) as mortgage rates continue to climb. In the afternoon, Philly Fed Pres. Harker said Thursday that rate hikes have done little to keep inflation in check. He went on to say “we are going to keep raising rates for a while” and “I expect we will be well above 4% by the end of the year.” This falls in line with the current rate being 3.25% and Fed Fund Futures now pricing in a 0.75% rate hike for November and December.

SNAP Case Study | Actual Trade

On the regulatory/legal front, the TX state AG has sued GOOGL for breaking the state’s law which prohibits companies from collecting user biometrics (facial recognition and voice data) without explicit user consent. This is very similar to the state’s lawsuit against META for Facebook doing the same thing. Meanwhile, AMZN is now facing a $1 billion lawsuit in the UK, claiming that the AMZN Marketplace abused its position and information to favor its own products over marketplace vendors. Elsewhere, the US Dept. of Justice has requested more details about the proposed $8 billion deal for CVS to buy SGFY. Finally, after the close, it was announced that WMT has agreed to pay the state of Florida $215 million to resolve claims related to its pharmacy’s part in opioid addiction in the state.

In other stock news, at the close, DB announced it has cut an unspecified number of staff from its investment banking unit as M&A activity (i.e., possible business) has dried up. Elsewhere, the IPO for PRME (Prime Medicine) opened 12% higher than the IPO price of $17 first trading at $18.97. Meanwhile, at the close, XOM announced it has agreed to sell its Montana refinery (which processes 63,000 barrels per day) to PARR for $310 million. Well after the close, PFE said they expect to hike the cost of US covid-19 vaccines by 300% (from $30/dose to $120/dose) in the first quarter of 2023, when the original government purchase contracts expire and the cost is shifted from government to private insurers. In addition, the Washington Post reported that Elon Musk told potential investors in his TWTR buyout that he plans to cut the TWTR staff by 75% (from 7,500 to under 2,000). Finally, Bloomberg reported this morning that the Biden Administration is now discussing whether some of Musk’s ventures should be subjected to national security reviews (TWTR was not mentioned specifically, but the stock is suffering in pre-market on this news).

In international news, UK PM was forced to resign Thursday after only 6 weeks in office. So, the UK is back in search of a leader. However, the Tory party is fast-tracking the system this time and they may have named a new PM by Monday. Whoever is selected will be pressured to renounce unfunded tax cuts (especially at the corporate and top-end brackets) as well as reaffirm the government commitments to cost of living increases in government programs. Meanwhile, the strong dollar continues to hurt most foreign economies as the Yen hit a 32-year low against the dollar (over 150 Yen per Dollar) and the Euro fell further below parity Thursday. Japan is back to saber rattling about intervention to strengthen the Yen, but there is little they can do when the US Fed is aggressively hiking rates and Japan’s economy is fragile enough that the Bank of Japan cannot match pace.

After the close, CSX, UFPI, SIVB, and SAM all reported beats on both revenue and earnings. Meanwhile, SNAP and THC missed on revenue while beating on earnings. On the other side, WAL beat on revenue while missing on earnings. However, both RHI and WHR missed on both the top and bottom lines. It should also be noted that WHR, RHI, and THC all lowered their forward guidance.

Overnight, Asian markets leaned heavily to the red side on mostly modest moves. It was Singapore (-1.75%) that was an outlier while Taiwan (-0.98%), Australia (-0.80%), Hong Kong and Shenzhen (both -0.42%) paced the losses. Malaysia (+0.61%) was by far the largest gainer. Meanwhile, in Europe, exchanges are down across the board at midday Friday. The FTSE (-0.72%), DAX (-1.34%), and CAC (-1.54%) are leading the region lower as markets react to the overnight collapse of the UK government (the 2nd in two months) and a plummeting British Pound. In the US, as of 7:30 am, US Futures are pointing toward a down start to the day. The DIA implies a -0.33% open, the SPY is implying a -0.35% open, and the QQQ implies a -0.67% open at this hour. 10-year bond yields are soaring again to 4.265% and Oil (WTI) is up a half of one percent to $84.92/barrel in early trading.

The major economic news events scheduled for Friday are limited to a Fed speaker (Williams at 9:10 am). The major earnings reports scheduled for the day include AXP, ALV, EEFT, HCA, HBAN, IPG, RF, SLB, and VZ before the open. There are no earnings reports scheduled for after the close.

So far this morning, VZ, AXP, SLB, IPG, HBAN, and EEFT have all reported beats on both the revenue and earnings lines. Meanwhile, HCA missed on revenue while beating on earnings. On the other side, RF beat on revenue while missing on earnings. However, ALV reported a miss on both the top and bottom lines.

With that backdrop, the bearish trend remains in place (both the short-term one from this week and the longer-term one since August). Again, all 3 major indices continue to flirt with printing an inverted head and shoulders (bottoming) pattern. Market extension is not a factor, either in terms of the T-line or T2122. However, intraday reversals and indecision remain the norm as we have seen a lot of gaps and wicks this week. So, continue to be cautious and show patience (wait for confirmation). With high volatility and less certainty at the moment, this may be the time to pursue more cautious trading strategies (options spreads for example), including remaining hedged, quick, and/or small. Beyond this, do not forget that it’s Friday. So, pay yourself and consider taking some money off the table ahead of the weekend’s new cycle.

Don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is not a hobby. It’s a job. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today (Rick is out). You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service