Bulls Look to Gap With Jobless Claims Up

Markets gapped down modestly (a half of a percent in the QQQ and a quarter percent in the large-cap indices) on Wednesday. Price then proceeded to meander sideways all day on low volume except for the DIA (which is looking like it will achieve average volume). This action is giving us black-bodied indecisive Doji candles in all three major indices. The QQQ managed to retest and fail resistance while the SPY and DIA did not get down to the level of testing support again.

On the day, nine of the ten sectors were in the red with Healthcare (+0.55%) by far the strongest and Energy (-0.65%) and Consumer Cyclical (-0.68%) the weakest sectors. In the meantime, the SPY was down 0.17%, the DIA was up 0.01%, and the QQQ was down 0.42%. The VXX was up by more than 1.45% to 15.29 and T2122 has climbed back out of the oversold territory to 20.52. 10-year bond yields were down a bit to 3.42% and Oil (WTI) was off 2.55% to $72.36 per barrel. So, Wednesday was an indecisive day that amounted to a fifth straight down day in the SPY and a fourth straight in the DIA.

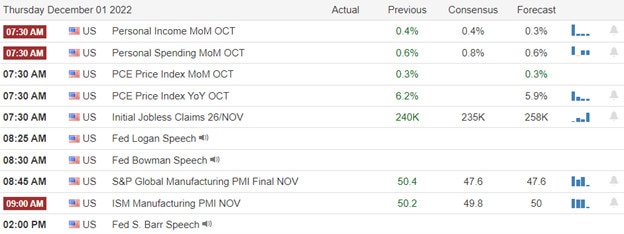

In economic news, Q3 Unit Labor Costs rose far less than expected at +2.4% (versus a forecast of +3.1% and the Q2 increase of 3.5%). Q3 Nonfarm Productivity was also up more than expected at +0.8% (compared to a forecast of +0.6% and the Q2 value of +0.3%). This caused a small gap lower as traders interpreted modestly good economic data as not pushing the Fed in either direction. Later in the morning, we saw EIA Weekly Oil Inventories fall more than expected at -5.187 million barrels (versus the forecast of -3.305 million barrels but still nowhere near as much of a drawdown as the prior week’s 12.580 million barrels).

SNAP Case Study | Actual Trade

In stock news, LUV reinstated its dividend Wednesday after a three-year suspension. The CEO of the company cited a strong return of travel demand as he announced the company will pay $0.18/share to shareholders of record on January 31. Later, Reuters reported that AMZN was offline mid-morning. No details on the cause of the outage were given. In other AMZN news, Washington DC has sued the company for diverting tips intended for delivery drivers to its own coffers. Elsewhere, the CEO of C said she expects trading revenue to rise 10% in the current quarter while investment banking fees will fall 60% (in line with industry norms this quarter). In “you don’t say” news, the CEO of COIN said he expects the revenue of their cryptocurrency trading platform to be down 50% for 2022 compared to 2021. This comes after their competitor FTX and Celsius Network both filed for bankruptcy as well as the massive crash of crypto prices. In legal news, CVNA is meeting with lawyers and bankers to discuss ways to restructure its debt load with the risk of bankruptcy rising.

In government news, US lawmakers declined to exempt BA from a looming deadline for a new safety standard related to its “737 Max” jets. This loss will mean BA will need to rework safety systems on new planes before they can be certified by the FAA. Meanwhile, after hours, GOOGL, ORCL, AMZN, and MSFT were awarded $9 billion in contracts by the Dept. of Defense related to “Cloud services.” This comes a year after an AMZN lawsuit killed the previous awarding of these contracts to MSFT (based on bias introduced into the procurement process by former-President Trump).

In energy news, crude oil (WTI) fell again Wednesday in volatile trading, reaching close to the lowest level in a year. The causes this time were the EIA report that showed an unexpected inventory build of 6.2 million barrels of distillates (like diesel fuel). This post-refining inventory glut more than outweighed the crude oil inventory drawdown of 5.2 million barrels and the fall came in spite of news that Chinese oil imports reached the highest level in 10 months in November. In other energy news, PSX announced that was one fatality and another contract employee injured in a crane accident at its Wood River IL refinery.

After the close, GEF and GME reported misses on both the revenue and earnings lines. So far this morning, GMS, CIEN, KFY, and MOMO all reported beats on both the top and bottom lines. (HOV reports at 9:15 am.)

Overnight, Asian markets were mixed but leaned bearish with Hong Kong (+3.38%) and outlier on the post-Covid China opening news. Australia (-0.75%), Taiwan (-0.53%), and South Korea (-0.49%) led the region lower. Meanwhile, in Europe, the exchanges are mostly in the red at midday. The FTSE (-0.05%), DAX (-0.34%), and CAC (-0.26%) are typical of the continent with only three smaller exchanges in the green in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modest green opening ahead of Jobless Claims. The DIA implies a +0.13% open, the SPY is implying a +0.20%) open, and the DIA implies a +0.20% open at this hour. 10-year bond yields are up to 3.447% and Oil (WTI) is up 2.19% to $73.55/barrel in early trading.

The major economic news events scheduled for Thursday are limited to Weekly Initial Jobless Claims (8:30 am). The major earnings reports scheduled for the day include Thursday, we hear from CIEN, GMS, HOV, and KFY before the open. Then after the close, AVGO, CHWY, COO, COST, DOCU, LULU, and RH report.

In economic news later this week, on Friday, November PPI and Michigan Consumer Sentiment are reported. In earnings later this week, on Friday, we hear from LI.

As stated above, Hong Kong skyrocketed overnight on the China opening story. Specifically, local Hong Kong media reported that the city is considering the outdoor mask requirement and reducing the isolation period for those who test positive for Covid-19. In addition, the Hong Kong government is considering replacing the need for two negative PCR tests with one rapid-antigen test for inbound travelers. Elsewhere, the Netherlands (home of ASML) appears to be falling in line with President Biden’s recently expanded chip sanctions for China (which restrict the sale of equipment used in the production of chip Fab facilities and which ASML is one of the world leaders in producing).

With that background, it looks like markets are setting up for a small gap higher, moving against the recent downtrend. Just remember Monday, when a similar gap-up turned into a slow all-day rout by the Bears. Over-extension is not yet a problem either in terms of the T-line (8ema) or the T2122 indicator. The short-term trend remains bearish within the mid-term bullish trend now broken. Only the large-caps indices still have support close below with the QQQ now not far below resistance (broken support). So, if the bulls cannot rally to hold those support levels we could see a bearish run for several percent in the near future.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: CLX, PUMP, BK, PAAS, ANF. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service