Over-Extended Markets Look For Relief

Friday saw another serious gap down in the SPY (-1.20%) and DIA (-1.08%) but only a 0.34% gap down in the QQQ. However, after a half hour of volatility, all three major indices got in lock step to sell off until 10:30 am and then slowly drift sideways with a very modest bearish trend that reached the lows of the day at about 2:30 pm. At that point, the bulls stepped in to rally us up off the lows this last hour as volatility kicked in for expiration gyrations. This action is giving us gap-down, black-bodied, indecisive, Spinning Top type candles in all the major indices. The SPY and QQQ have both now dropped down through their 50sma while the DIA bounced up off its own 50sm after a test of that level as a support. Volume has been above average in the DIA, but much less so in the SPY and QQQ.

On the day, all ten of the sectors are in the red with Utilities (-1.50%) leading the way lower while the Healthcare (-0.30%) and Basic Materials (-0.43%) sectors held up best. At the same time, the SPY was down 1.63%, the DIA was down 1.15%, and the QQQ was down 0.95%. The VXX is flat at 15.01 and T2122 dropped deep inside of the oversold territory at 7.25. 10-year bond yields were down from the open to 3.484% and Oil (WTI) was down 2.36% to $74.31 per barrel. So, overall, it was a bearish and volatile day where we only the DIA was able to stay above its 50sma.

In economic news, the Manufacturing PMI came in below expectation at 46.2 (versus a 47.7 forecast and 47.7 previous reading). The same was true for Services PMI which came in at 44.4 (compared to the 46.8 forecasted and 46.2 prior reading). In addition, the S&P Global Composite PMI was also below expectations at 44.6 (versus 47.0 which was forecasted and the prior reading of 46.4).

SNAP Case Study | Actual Trade

In stock news, BAYRY and the state of OR finalized a $698 million settlement resolving chemical environmental pollution claims dating all the way back to 1977. The root cause was PCBs manufactured by MON (which BAYRY acquired). Elsewhere, the NHTSA has opened an investigation into GM Cruise robotaxis after 242 reports of the vehicles unexpectedly stopping in the middle of the street, snarling San Francisco traffic and stranding passengers. At the same time, BMO reported that it has raised $1.9 billion of capital by issuing new shares in an effort to increase its capital cushion with a turbulent economy ahead. In other news, FFIE fell more than 26% on Friday after the company revealed that production plans for its long-delayed luxury electric vehicle will depend on the company getting additional financing. In layoff news, it was reported by Bloomberg that internal sources tell them GS is preparing to fire 8% of its workforce (4,000 people). Finally, the US Dept. of Labor announced after the close that AMZN had failed to record work-related injuries at six different warehouses located in five states. This included 14 separate OSHA safety violations, each with a fine of a paltry $14,500.

In energy news, US gasoline prices hit a 15-month low on Friday as the AAA reported that the national average price dropped to $3.18/gallon. Meanwhile, the EU Energy Ministers are meeting in Brussels in furious negotiations to agree on a price cap for Natural Gas prices as their national leaders agreed should happen last week.

In miscellaneous news, LHX announced Sunday that it has agreed to buy AJRD for $58/share. (It is worth noting that LHX competitor LMT was forced to drop its own deal to buy AJRD earlier this year when antitrust regulators sued to block a deal.) Then this morning (US time) META was warned by the EU that it is breaching EU Antitrust Laws by abusing its position to corner the online classified advertising market. In Elon Musk news, he launched a poll asking Twitter users whether he should step down as CEO and 57.5% of respondents (17.5 million votes cast) said “yes.” This comes one day after the third-largest TSLA shareholder told Musk he should resign as CEO of TSLA.

Overnight, Asian markets leaned heavily to the downside. Shanghai (-1.92%), Shenzhen (-1.51%), and Japan (-1.05%) led the region lower with only India (+0.83%) and Singapore (+0.49%) in the green. However, in Europe, with the sole exception of Russia (-0.82%), exchanges are green across the board at midday. The FTSE (+0.54%), DAX (+0.53%), and CAC (+0.62%) lead the region higher although the gains are broad and similar across the continent in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modestly higher start to the day. The DIA implies a +0.20% open, the SPY is implying a +0.28% open, and the QQQ implies a +0.37% open at this hour. 10-year bond yield have jumped up to 3.535% and Oil (WTI) is up nearly a half of a percent to $74.60/barrel in early trading.

There are no major economic news events scheduled for Monday. There are no major earnings reports scheduled for before the open. However, after the close, HEI and SCS report.

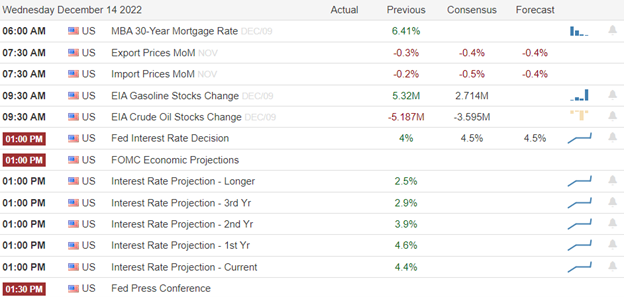

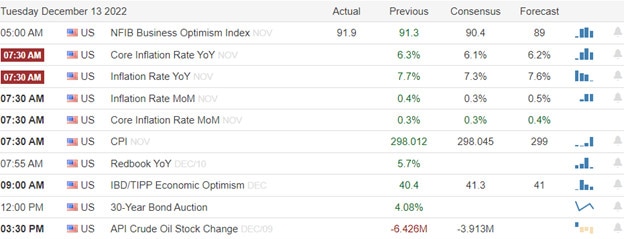

In economic news later this week, on Tuesday, we get Nov. Building Permits, Nov. Housing Starts, and API Weekly Crude Oil Stocks Report. Then, on Wednesday, Q3 Current Accounts, Conf. Board Consumer Confidence, Nov. Existing Home Sales, and EIA Weekly Crude Oil Inventories are reported. Thursday, we get Q3 GDP, Q3 GDP Price Index, and Weekly Initial Jobless Claims. Finally, on Friday, Nov. Durable Goods, Nov. PCE Price Index, Nov. Personal Spending, Michigan Consumer Sentiment, and Nov. New Home Sales are reported. Also, remember that Friday is a half-day as markets close early for virtual Christmas Eve.

Meanwhile, in earnings later this week, on Tuesday we hear from FDS, GIS, FDX, NKE, and WOR. Then Wednesday, CCL, RAD, TTC, MU, and MLKN report. On Thursday, we hear from KMX and PAYX. Finally, on Friday, there are no reports scheduled.

With that background, it looks like markets will start the week in a modestly bullish mood. (Up, but still inside of Friday’s candles.) The DIA and SPY may have closed last week sitting on minor support levels. In either case, the bears have the short-term trend in their favor. However, we are over-extended to the downside in terms of the T-line and also the T2122 (4-week new high/low ratio) indicator. So, some relief is in order. Be cautious and aware of the recent volatility (gaps and intraday reversals).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas Today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service