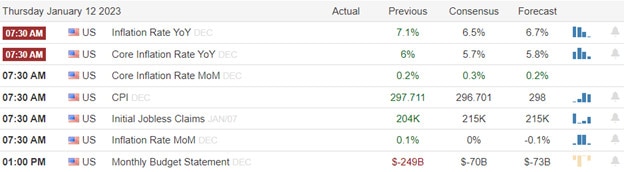

With investors anticipating better numbers in this morning’s pending CPI report, the bulls pushed higher with nervous energy as the VIX rose simultaneously. Jobless claims will be the next hurdle to cross this morning, and then Friday morning’s big bank reports will become the center of attention for the market. The coming 3-day weekend may be a welcome respite after the wild price volatility we will likely experience over the next 48 hours. But, of course, anything is possible, so be prepared for big point moves that may include quick whipsaws as the drama unfolds.

Asian markets mainly saw modest gains overnight with eyes on pending inflation data. European markets have stretched to their highest level since April 2022 on a report the eurozone may outperform the U.S. in 2023. With the highly anticipated CPI report pending, U.S. futures suggest a flat open, holding their breath, hopeful the numbers show the current FOMC rates are good enough.

Economic Calendar

Earnings Calendar

We have a few more small-cap companies reporting today, but the only notables are INFY and TSM.

News & Techncals’

Economists expect a slight decline in December’s consumer price index when it is released Thursday at 8:30 a.m. ET. The consensus forecast for CPI is for a decrease of 0.1% on a monthly basis but a 6.5% increase from the prior year, according to Dow Jones. Stocks rallied Wednesday ahead of the report on expectations the data will show a continued easing of inflation pressures and optimism that it could slow the Federal Reserve’s rate hiking.

Zeynep Ozturk-Unlu, Deutsche Bank’s chief investment officer for EMEA, said she could see Europe outperforming the U.S. in economic growth and capital markets in 2023. Other analysts also told CNBC they believe the U.S. had reached the end of a post-Global Financial Crisis rally. Moreover, some early data points look positive for the eurozone compared to the U.S.

Ubisoft shares slumped as low as 18.80 euros apiece Thursday morning, hitting their lowest level in more than seven years. Ubisoft said Wednesday it expects full-year net bookings will likely fall 10% after an earlier forecast called for a 10% increase. It’s the third gaming firm this week to issue a disappointing trading update. Devolver Digital and Frontier Developments issued separate profit warnings on Monday.

The bulls pushed higher on Wednesday, speculation that the pending CPI report will show a decline, but interestingly the VIX also rallied on another rather anemic volume day. Before the opening, we will get earnings from TSM and INFY, along with highly anticipated inflation and Jobless Claims numbers. Traders should prepare for some wild price gyrations as the market reacts. Will it be the bulls or bears inspired? We will soon find out! Though we have some Fed speakers and a 30-year bond auction, Treasury Statement, and Fed Balance Sheet later in the day, market attention will quickly shift to big bank reports happening Friday before the bell. Buckle up, it’s going to be a wild end to the trading week as we head into a 3-day weekend.

Tuesday’s anemic price action though bullish, recorded activity that was substantially lower than the pre-holiday volume of Christmas and the New Year. The pending CPI report Thursday and the big bank reports Friday, both happening before the bell, have raised the market uncertainty understandably high. We should expect big price moves by the end of the week, but the question is, in what direction will all this wound-tight emotion explode? Trade wisely because this is a dangerous market condition for retail traders!

Asian markets mostly rallied overnight, with only Shanghai seeing a modest decline while we slept. European markets are in rally mode this morning, looking to recover Tuesday’s weakness with uncertainty ahead. U.S. futures are once again pumping a bullish open, trying to put on a brave face with another day of low volume likely as we wait on the CPI and the official kickoff of earnings. Buckle up anything is possible by the end of the week.

Economic Calendar

Earnings Calendar

We have a very light day on the earnings calendar, with just one confirmed report coming from KBH after the bell.

News & Technicals’

Wells Fargo is stepping back from the housing market. Instead of its previous goal of reaching as many Americans as possible, the company will now focus on home loans for existing bank and wealth management customers and borrowers in minority communities. As part of its reduction, Wells Fargo is shuttering its correspondent business that buys loans made by third-party lenders and “significantly” shrinks its mortgage-servicing portfolio through asset sales. Altogether, the shift will result in a fresh round of layoffs for the bank’s mortgage operations, executives acknowledged, but they declined to quantify how many jobs will be lost.

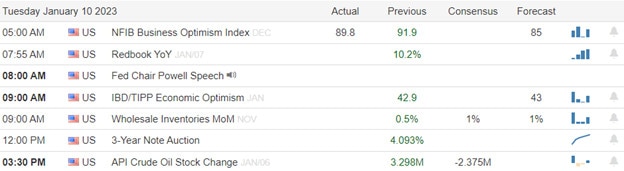

Fed Chairman Jerome Powell noted that stabilizing prices requires making tough decisions that can be unpopular politically. In other remarks, the central bank leader said the Fed is “not, and will not be, a ‘climate policymaker.’”

The World Bank slashed its 2023 global economic growth outlook to 1.7% 2023 from its earlier projection of 3%. It would mark “the third weakest pace of growth in nearly three decades, overshadowed only by the global recessions caused by the pandemic and the global financial crisis,” the World Bank said.

Although the indexes held the breakout support, the activity was lower than the pre-holiday volume of both Christmas and New Year trading. Unfortunately, there is a good chance we could see more of the same with the light earings and economic calendar on Wednesday. The uncertainty of the Thursday CPI report and the official beginning of 1st quarter earnings as the big banks begin to report on Friday is likely the reason for the anemic volume. The last couple of weeks of range-bound trading has wound the spring on the indexes very tight, and it’s likely to create some tremendous price volatility at the end of the week. The big question is, which way will it pop? Be careful not to overtrade out of boredom, and be prepared for the explosion of emotion just around the corner.

On Tuesday, after Fed Chair Powell’s morning speech, markets opened up just on the down side of flat. At that point, all three major indices chopped sideways until noon. Then a slow, steady bullish trend started that lasted into the close. This action gave us white-bodied, Bullish Engulfing signals in the SPY and QQQ. Meanwhile, the DIA bounced up off its 50sma on the day. All of this, once again, took place on lower-than-average volume.

On the day, all 10 sectors were in the green as Consumer Defensive (+0.09%) lagged behind and Consumer Cyclical (+1.46%) lead the other sectors higher. Meanwhile, the SPY was up 0.70%, the DIA was up 0.58%, and QQQ was up 0.85%. At the same time, the VXX was down 4.16% to 12.91 and T2122 remains in the overbought territory at 89.57. 10-year bond yields spiked to 3.606% and Oil (WTI) was up 0.31% at $74.86 per barrel. So, overall, it has been a bullish day that negated the potential bearish signal from Monday.

In economic news, as mentioned above, Fed Chair Powell spoke to Sweden’s central bank Tuesday. He made no reference to interest rate decisions other than to say that more increases are likely on the way this year. His remarks emphasized that fighting inflation requires measures that are politically unpopular and that the Fed must be independent of political control in order to take the hard actions that will bring inflation down. He also went on to address GOP criticisms by saying that “the Fed should stick to its knitting” (and not stray into using regulatory power to address climate change or social issues). He emphatically said, “We (the Fed) are not, and will not be a climate policymaker.” However, he also said asking big banks to examine their readiness for major climate-related events and other risks was fair game but that is as far as it should go. If the premarket is a judge, traders liked what they heard from Powell. Much later, after the close, the API delivered its Weekly Crude Oil Stocks report with a massive unexpected build in inventories. The data showed inventory up by 14.865 million barrels (compared to a forecasted drawdown of 2.375 million barrels).

In stock news, Airbus maintained its position as the world’s largest plane manufacturer when it reported that deliveries rose 8% in 2022. Airbus delivered 663 jets, compared to just 480 delivered by BA during the year. Elsewhere, GM, F, GOOGL, SPWR, and RUN announced they will work together to create standards and protocols that will allow for Virtual Power Plants to be used to ease loads on electricity grids. (The VPP idea is that thousands of decentralized energy sources like electric vehicles and batteries can be pooled together to create a source of power for an electric grid during high-demand periods.) Meanwhile, CNBC reported that the money AAPL app store developers have received this year suggests that AAPL app store growth has slowed and is likely in line with the 2021 revenue from that unit. At the same time, FDX said it was trimming Sunday deliveries starting in March, reducing the percentage of the US that is eligible for Sunday delivery down to 50% (from 80%). In other news, the Wall Street Journal reported that FRG is considering going private through a management buyout. Finally, WFC (long the leader in home lending) is scaling back its mortgage business and will now only offer home loans to existing banking customers.

In energy news, in addition to the crude oil stocks above, the Weekly API report also showed a 1.8-million-barrel increase in gasoline inventories and a 1.1-million-barrel build of distillate stocks (diesel fuel and heating oil). Compare these to a forecast of a 1.186-million-barrel build in gasoline inventory and an expected drawdown of 0.472-million-barrels of distillate. In other news, the US EIA released a forecast on Tuesday afternoon saying that global oil consumption will reach a new record of 102.2 million barrels per day in 2024. Finally, February Natural Gas futures fell another 7% on Tuesday (following Monday’s 5% rally), bringing the total drop to 52% over the last three weeks.

Early this morning, the FAA suffered a system outage that normally alerts pilots of in-air hazards and airport facility status changes (like closed airports and runways). That system has stopped processing new or updated information. This outage caused the FAA to order the delay or cancellation of all flights in US airspace (inbound or outbound) until the system is restored. As of 6:30 am, almost 800 flights had been delayed, canceled, or rerouted away from US airspace. Obviously, this will have a very minor, but real, impact on US businesses, especially airlines. (For reference, the storm just before Christmas caused the cancellation of many thousand flights each day for more than a week.)

Overnight, Asian markets were mixed but lean to the upside on modest moves with Japan (+1.03%) and Australia (+0.90%) leading the gainers while Shenzhen (-0.58%) and Taiwan (-0.35%) paced the losses. Meanwhile, in Europe, the exchanges are heavily weighted to the green at midday. The FTSE (+0.64%), DAX (+1.05%), and CAC (+0.98%) are leading the region higher in early afternoon trade with only Norway (-0.63%) and two other very minor spots of red on the board. As of 7:30 am, US Futures are pointing toward a start to the day just on the green side of flat. The DIA implies a +0.10% open, the SPY is implying a +0.15% open, and the QQQ implies a +0.10% open at this hour. At the same time, 10-year bond yields are back down to 3.578% and Oil (WTI) is up fractionally to $75.38%/barrel in early trading.

The major economic news events scheduled for Wednesday are limited to EIA Crude Oil Inventories (10:30 am). There are no major earnings reports scheduled for before the opening bell. However, after the close, KBH reports.

In economic news later in the week, on Thursday, December CPI, Weekly Initial Jobless Claims, the WASDE Ag Report, and the December Federal Budget Balance are reported. Finally, on Friday, we get December Import/Export Prices, Michigan Consumer Sentiment, and hear from Fed member Harker.

In terms of earnings, on Thursday, INFY and TSM report. However, on Friday, we hear from BAC, BK, BLK, C, DAL, FRC, JPM, UNH, WFC, and WIT report.

In mortgage news, after rising at the end of the year, interest rates dropped sharply last week from 6.58% to 6.42% for a 30-year, fixed-rate, conforming loan. That drop led to a 5% increase in refinance applications and an overall mortgage volume increase of 1.2% compared to the prior week according to the Mortgage Bankers Association. The mortgage volume was still 86% lower than the same week in 2022.

With that background, it looks like the large-cap indices are sitting just on top of their 50sma (also a resistance level for the SPY) after a very small bullish premarket move. Meanwhile, the QQQ is also positive in premarket, but has not yet reached its 50sma above. This is looking like a modest additional follow-through to Tuesday’s move. However, it is far from a definitive direction move in the bullish direction. Nonetheless, the premarket bias is bullish. Do not be surprised if price just drifts and chops around today as the market waits on that CPI report Thursday (not for its own sake, but as a read-through to what the Fed may do at month end). So, don’t count on average volumes, and be very careful trading thin tickers.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: BWA, DIS, CAT, PYPL, SBUX, ALLY, GILD, LUMN, and META. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls pushed hard, but overhead price resistance found bears waiting and willing to fight back, leaving some potential topping patterns behind. Jerome Powell’s comments this morning will likely cast the deciding vote on whether the bulls matain the Friday consolidation breakout or if the bears regain the upper hand. With a pending CPI report and big bank earnings just around the corner, speculation and uncertainty are high so brace for considerable volatility in the days ahead. Anything is possible!

During the night, Asian markets closed the day mixed with an eye on Jerome Powell. European markets trade modestly bearish across the board this morning, weighing inflation concerns and pending Fed comments. U.S. futures point to a gap as we wait to find out if the FOMC plans to stay on the hawkish path, bucking all the talking heads trying to promote the pivot narrative. Brace yourself for wild price action likely in the days ahead.

Economic Calendar

Earnings Calendar

We have just five confirmed reports this Tuesday, but only a couple of them are somewhat notable such as ACI and BBBY.

News & Technicals’

The global investment bank is letting go of as many as 3,200 employees starting Wednesday, according to a person with knowledge of the firm’s plans. That amounts to 6.5% of the 49,100 employees Goldman had in October, which is below the 8% reported last month as the upper end of possible cuts. However, other investment banks are adopting a “wait and see” attitude: If revenues are tracking below estimates in February and March, the industry could cut more workers, said a person familiar with a leading Wall Street firm’s processes.

According to an email obtained by CNBC, Disney CEO Bob Iger told hybrid employees on Monday they must return to corporate offices four days a week starting March 1. Iger’s four-day-per-week stipulation is relatively strict compared with other large companies, many of which have opted for two or three mandated in-office days for hybrid employees. Moreover, it comes less than two months after he returned to the company’s helm.

CNBC’s Jim Cramer told investors to stay away from tech stocks, even after their gains on Monday. “These short-term sector rotations like we saw today — they’re irrelevant because they can’t last. Think renters, not owners. The fundamentals, now they last,” he said.

The bulls followed through on Monday but faded into the afternoon, leaving behind some worrisome potential topping patterns at price resistance. Earnings uncertainty and worries about higher rates inspired the bears to push back as we wait on a Jerome Powell speech this morning. Will he continue to sound hawkish disappointing traders that talking heads continue to push the narrative of a Fed pivot? We will soon find out and should expect substantial price volatility as the market reacts to his comments. Past that, we won’t have much for the market to react to as we wait on the Thursday CPI and the start of big bank earnings. Nevertheless, speculation remains high, so plan your risk carefully.

Markets gapped higher at the open (by a half of a percent in the large-cap indices and by three-quarters of a percent in the QQQ), following the rest of the world higher. Then the bulls gave us a follow-through that lasted until we reached the highs of the day at about 11:30 am. At that point, the bears stepped in to lead an afternoon selloff that took us lower, all the way into the close. The large caps completely faded the gap, getting into negative territory by day end. However, while the QQQ sold off, it held up better than the large caps. This action saw the SPY retest and fail its 50sma and the coinciding resistance level. It has also brought the QQQ up near a retest of its own 50sma above before pulling back. We should also note that all three major indices printed Shooting Star-type candles.

On the day, six of the 10 sectors are in the green as Technology (+1.52%) led the way higher and Healthcare (-1.17%) lagged behind the other sectors. At the same time, the SPY was down 0.06%, the DIA was down 0.29%, and QQQ was up 0.65%. Volume was back below average again in all 3 indices. Meanwhile, the VXX was up 0.52% to 13.47, and T2122 fell but remains in the overbought territory at 85.33. 10-year bond yields plunged down to 3.53% and Oil (WTI) was up 1.53% at $74.90 per barrel. So, overall, it was a gap-up, Shooting Star type of day with the bulls happy early and the bears completely in control during the afternoon

In economic news, Atlanta Fed President Bostic spoke to an Atlanta business group, basically reiterating the recent comments made by Fed Chair Powell. Bostic said they (Fed) are prepared to take rates higher and stay higher for longer to tame inflation. (And, yes, even at the risk of tipping the economy into recession.) Meanwhile, San Francisco Fed President Daly told the Wall Street Journal that she expects rates to go “somewhere above 5%” and that “doing so in more gradual steps does give you the ability to respond to incoming information.” However, it did seem that both speakers were talking about whether the Fed will raise 0.25% or 0.50% on February 1. It is also worth noting that neither of these Fed Presidents have a vote in 2023 (both were voters in 2022).

In stock news, LMT announced a $14.2 billion sale of F-35 fighter jets to Canada (to be delivered in 2026). Elsewhere, two retailers increased their holiday sales forecasts as AEO and ANF both said Monday that consumers had been snapping up their winter gear during the holidays. However, on the other side, LULU lowered its Q4 guidance. In the healthcare space, MRNA is reportedly evaluating a $110-$130 price range for its Covid-19 vaccine once it moves from government contracts to commercial sales. This is a similar range to the one PFE revealed it is considering. (The original price for both was $15-$16 per dose and then rose to $26/dose in the July 2022 government contract.) After the close, Bloomberg reported that AAPL is preparing to stop using chips from AVGO and QCOM in its devices by the end of 2024 (replacing those chips with Wi-Fi chips built to internal designs). Finally, Bloomberg reported that MSFT is in discussions with OpenAI bout investing as much as $10 billion into the creator of the artificial intelligence chatbot named ChatGPT.

In energy news, the US Federal government has rejected the initial batch of bids to resupply 3 million barrels of crude into the Strategic Petroleum Reserve. No details on the bid prices were given, but the Dept. of Energy had previously said it is looking to refill the 180 million barrels recently released at a price of $70/barrel. Meanwhile, the price of the largest exported grade of Russian oil (Urals grade) was selling at well less than half of the international price. Urals was selling for $37.80/barrel (compared to $79.80/barrel for Brent) at the Baltic Sea port of Primorsk. This is far less than even the G-7 imposed price cap. All of which is proving that sanctions on Russia are having a serious economic impact. Finally, the German energy regulator said that a natural gas shortage is increasingly unlikely due to conservation efforts and a mild winter. The Federal Network Agency said Germany’s gas storage facilities are currently still 91% full.

After the close, JEF beat on both the revenue and earnings lines. However, both lines also showed negative growth (lowered targets) with earnings less than half of the same quarter in 2021. The company blamed a persistent slump in the number of M&A deals as the cause. So far this morning, BBBY reported misses on both lines (expected after very recent warnings that the company may file for bankruptcy). ACI and SNX report later in the premarket period.

Overnight, Asian markets were mixed but leaned to the downside. Singapore (-1.29%), India (-1.03%), and Malaysia (-0.56%) led the region lower while Japan (+0.78%), Shenzhen (+0.50%), and Taiwan (+0.34%) paced the gains. In Europe, with the sole exception of Portugal (+0.16%), we see red across the board at midday. The FTSE (-0.19%), DAX (-0.45%), and CAC (-0.73%) are leading the region lower in early afternoon trade. As of 7:30 am, US Futures are also pointing toward a down start to the day. The DIA implies a -0.36% open, the SPY is implying a -0.33% open, and the QQQ implies a -0.45% open at this hour. At the same time, 10-year bond yields are back up to 3.563% and Oil (WTI) is up a half of a percent to $75.04/barrel in early trading.

The major economic news events scheduled for Tuesday are limited to Fed Chair Powell speaking (9 am) and the API Weekly Crude Oil Stocks (4:30 pm). The major earnings reports scheduled for the day are limited to ACI, BBBY, and SNX before the opening bell. Then after the close, NOTV reports.

In economic news later in the week, on Wednesday, we get EIA Crude Oil Inventories. On Thursday, December CPI, Weekly Initial Jobless Claims, the WASDE Ag Report, and the December Federal Budget Balance are reported. Finally, on Friday, we get December Import/Export Prices, Michigan Consumer Sentiment, and hear from Fed member Harker.

In terms of earnings, on Wednesday, we hear from KBH. On Thursday, INFY and TSM report. However, on Friday, we hear from BAC, BK, BLK, C, DAL, FRC, JPM, UNH, WFC, and WIT.

In late-breaking news, COIN announced that it is cutting 20% of its workforce after having cut 18% back in June 2022. The cuts last June were attributed to “growing too fast” while the current cuts are blamed on “market conditions created by bad actors” (referring to FTX). Finally, the Dollar is trading up against the Yen and Pound while it is flat against the Euro this morning. The overall Dollar index is up 0.32% today, which will provide a headwind to commodity prices.

With that background, it looks like all three major indices look like they are headed for a retest of their T-line (8ema) in premarket action. This looks like at least an initial follow-through to Monday’s Shooting Star signal. However, this is far from a definitive direction change and none of the three major indices has even re-entered the three-week consolidation zone again. So, for the moment, this looks like volatility (chop) as markets wait on Fed speakers and CPI later in the week. Fed Chair Powell, may have an outsized impact this morning with no other economic data or major earnings news to offset his tone. So, be cautious in chasing the premarket move unless you are very nimble.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets gapped higher at the open (up 0.83% in the SPY, up 0.88% in the DIA, and up 0.66% in the QQQ). However, price then immediately reversed and faded the gap to trade back below Thursday’s close before reversing again. At about 9:50 am, a steady rally began that lasted all the way into 3:15 pm when a small pullback took us into the close. This action gave us large, white-bodied candles, with larger lower wicks and smaller upper wicks, that caused all three major indices to cross above their T-lines (8ema) and pop up out of the 3-week long consolidation range. DIA has also crossed back above its 50sma and SPY is about to retest its own 50sma from below.

On the day, all 10 sectors are in the green with the Basic Materials (+3.29%) leading the way higher as Healthcare (+0.99%) lagged way behind the other sectors. At the same time, the SPY was up 2.24%, the DIA was up 2.14%, and the QQQ up 2.76%. Volume was slightly above average (for the first time in a long time). Meanwhile, the VXX was down 2.33% to 13.40 and T2122 spiked back up into the overbought territory at 92.18. 10-year bond yields plunged down to 3.565% and Oil (WTI) was flat at $73.76 per barrel. So, overall, it was a bullish day that finally broke out of the long consolidation, oddly on economic data that may cause the Fed to stay Hawkish.

In economic news, December Nonfarms Payrolls came in above expectations at +223k (compared to +200k forecasted but less than November’s +256k number). This took the December Unemployment Rate down to 3.5% (versus the forecast of 3.7% and the November rate of 3.6%). The December Participation Rate also increased slightly to 62.3% (from the November value of 62.2%). However, the December Average Hourly Earnings came in lower than expected at +4.6% year-on-year (versus the forecast of +5.0% and less than the November reading of +4.8%). This might indicate lower inflationary pressure on wages. Later in the day, November Factory Orders showed a larger drop than forecast at -1.8% (compared to an expectation of -0.8% and an Oct. value of +0.4%). Then, finally, ISM Non-Mfg. PMI came in significantly lower than expected at 49.6 (versus a forecast of 55.0 and a November value of 56.5). So, most of this showed a stronger economy than was projected with less inflationary pressure than anticipated, but also a slightly contracting forward outlook in the Services sector.

In stock news, on Friday, TLSA announced it will cut prices on various Model 3 and Model Y cars. Elsewhere, LUV said that it expects to post a loss for Q4 after canceling 17,000 flights in December. Meanwhile, Reuters reported that China is in talks with PFE to secure licenses to allow its domestic drugmakers to produce a generic version of the antiviral drug Paxlovid. At the same time, the FDA approved a new Alzheimer’s drug that was co-developed by BIIB. In other FDA news, the agency announced that the AZN antibody cocktail Evusheld likely does not provide protection to the latest and most prevalent variant of covid. Later in the afternoon, Reuters reported that MCD is planning corporate layoffs and a shift in emphasis toward building more restaurants according to leaked internal memos.

In miscellaneous news, Congress finally elected Kevin McCarthy as Speaker of the House. It took 15 rounds of voting over 4 days (the longest Speaker election in 164 years) and nearly came to blows between Republicans after the 14th round as a single extremist held the rest of the GOP (and Congress) hostage. All the while, not a single Democrat crossed the aisle to resolve the matter. However, in the end, the holdouts were persuaded by major concessions which allow more debate, allow easier amendments, divide the government funding into 12 different bills, give the House ability to defund the salary of any/all government officials, prohibit voting on increasing the debt ceiling without also cutting domestic spending, and finally allow any member of the House to individually call a vote to remove the Speaker at any time. This sets the stage for what will almost certainly be a more contentious, obstructive, and drama-filled two years than has been the case in a long time. (And that’s saying something.) Elsewhere, (and in better news) Natural Gas fell 17.1% last week (February contract), making it the third weekly decline in a row. Meanwhile, Oil closed Friday flat, ending the week lower despite a healthy drop in the Dollar (which raises commodity prices). Across the pond, Euro-area inflation fell back to single digits in December for the first time since August.

Over the weekend, Bazil suffered an even worse attack than the US suffered on January 6, 2021, putting the current US political problems into perspective. Thousands of supporters of the Trump-esque defeated ex-President Bolsanaro attacked, ceased, and briefly occupied the Brazilian Congress, Presidential Palace, and Supreme Court. Interestingly, in Brazil, it did not take a lying leader with the megaphone of major mass-media organizations behind him to whip the ignorant masses into rioting. There, it was accomplished in a much lower-tech manner. At any rate, the Brazilian military eventually drove the mobs away, but the damage was done. Xenophoia, tribalism, and “kicking down” politics had assaulted democracy. Perhaps more importantly to us, Brazilian business, and grain exports were temporarily halted by the national turmoil.

Overnight, Asian markets were green across the board. Taiwan (+2.64%), South Korea (+2.63%), and Hong Kong (+1.89%) led the region higher. Meanwhile, in Europe, we see nearly the same picture at midday. Only the FTSE (-0.10%) is in the red, while the DAX (+0.50%), and CAC (+0.23%) lead that region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.30% open, the SPY is implying a +0.40% open, and the QQQ implies a +0.45% open at this hour. At the same time, 10-year bond yields are up a bit to 3.593% and Oil (WTI) has spiked 3.35% to $76.24/barrel in early trading.

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for the day are limited to AYI and CMC before the opening bell. Then after the close, JEF reports.

In economic news later in the week, on Tuesday, Fed Chair Powell speaks and the API Weekly Crude Oil Stocks are reported. Then Wednesday, we get EIA Crude Oil Inventories. On Thursday, December CPI, Weekly Initial Jobless Claims, the WASDE Ag Report, and the December Federal Budget Balance are reported. Finally, on Friday, we get December Import/Export Prices, Michigan Consumer Sentiment, and hear from Fed member Harker.

In terms of earnings, on Tuesday, ACI and SNX report. Then Wednesday, we hear from BSX and KBH. On Thursday, there are no major earnings reports. However, on Friday, earnings season kicks off again as we hear from BAC, BK, BLK, C, DAL, FRC, JPM, UNH, WFC, and WIT report.

Finally, GS announced early this morning that it will be cutting 3,200 jobs later this week after completing an internal cost-cutting review. Bloomberg reports that when GS reports Friday it will unveil a new unit (which will house all of the GS credit card and installment-lending business) and that new unit will show a $2 billion pretax loss. Elsewhere, the Dollar is trading near a seven-month low today. This gives a boost to all commodities in early trading.

With that background, it looks like all three major indices are looking to follow Asia and Europe higher (at least as of premarket). The follow-through on Friday’s strong candle has the SPY retesting its 50sma and resistance from previous price action. All three of the major indices are above their T-line (8ema), but over-extension is not yet a problem in any of them. With CPI and Fed speakers ahead later in the week, do not be surprised to see a move but hen a rest as the market then hopes for a clue as to how the Fed will act at the end of the month.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: TSLA, AAPL, AMZN, META. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls fueled by hope of declining inflation looked past economic data showing contracting economy to break the consolidation trigging the classic short squeeze. The DIA remains the strongest index and the only one above its 50 day morning average and long-term bearish downtrend. With worries of recession and the ramp up for 1st quarter earnings beginning this week traders should plan for considerable price volatility. There is no shortage of highly emotional speculation so expect big point moves and punishing whipsaw as well as full overnight reversals as drama unfolds.

While we slept Asian markets rallied with the tech heavy HSI leaning the way higher up 1.89% at the close. European markets also trade mostly bullish with the reopening of China providing the inspiration. U.S. point to bullish open trying to follow through on Friday’s but with so much overhead resistance in the SPY, QQQ and IWM we can’t rule out the possibility of a pop and drop, so be careful rushing in with a fear of missing out.

Economic Calendar

Earnings Calendar

We start to step up on the earnings this week and should expect considerable volatility with some big bank earnings at the end of the week. Notable for Monday include AYI, AZZ, JEF, CMC, PSMT, TLRY, WDFC.

News & Technicals’

Bolsonaro’s supporters stormed Brazil’s Congress, Supreme Court and presidential palace in Brasilia on Sunday. The demonstrators refused to accept Bolsonaro’s legitimate electoral defeat to leftist rival Luiz Ignacio Lula da Silva. “The coup plotters who promoted the destruction of public property in Brasilia are being identified and will be punished,” Lula said in a tweet, vowing to resume work in the palace on Monday.

At around 35,000 feet, the Virgin Orbit rocket will be deployed over the Atlantic, carrying nine small satellites into orbit in what is known as a horizontal launch. Crowds are expected to gather to watch the event, with Spaceport Cornwall having invited the general public to witness what they have described as a “historic moment.” The designated launch event will also include a “silent disco” tent.

The U.S. House of Representatives elected Kevin McCarthy of California as speaker in the 15th round of votes early Saturday. McCarthy made extraordinary concessions to win over a small bloc of far-right holdouts who blocked his speaker bid. McCarthy said the tense showdown on the House floor this week was proof that he is not someone who gives up easily.

Although Friday’s economic data continued to show a slowing economy the hope that inflation pressures are easing inspired the bulls to break the consolidation log jam trigging the classic short squeeze. Though we have a relatively light economic calendar this week Tuesday we will have to deal with a Jerome Powell speech and CPI reading on Thursday as earnings season ramps up. Emotion and uncertainty are high so traders should plan for considerable volatility as worries of recession continue to loom. The Dow remains the strongest of the indexes with the SPY, QQQ, and IWM remain under the long-term bearish trends and considerable resistance. Expect substantial point whipsaws and punishing overnight reversals in the days and weeks ahead.

For the first time in the new year, markets gapped down at the open Thursday (0.50% in the SPY, 0.50% in the DIA, and 0.68% in the QQQ). All three major indices then spend the rest of the day wobbling sideways in a three-quarters of a percent range below the open. This action gave us black-bodied, indecisive candles on the day. All three of the indices are now back just below their T-line (8ema) and remain in the recent consolidation. The DIA is also back below its 50sma with the QQQ looking like a “Dreaded-h pattern” setup.

On the day, eight of the 10 sectors were in the red with the Technology (-2.06%) and Utilities sector (-1.82%) leading the way lower as the Energy sector (+1.24%) held up best. Meanwhile, the SPY was down 1.14%, the DIA was down 1.00%, and the QQQ was down 1.57%. Yet again, this took place on lower-than-average volume. At the same time, the VXX was up 0.81% to 13.72 and T2122 dropped back down into the mid-range at 39.37. 10-year bond yields are up slightly to 3.72% and Oil (WTI) was up 1.37% to $73.84 per barrel. So, overall, it was a bearish day that remains in the choppy consolidation of the last 2+ weeks.

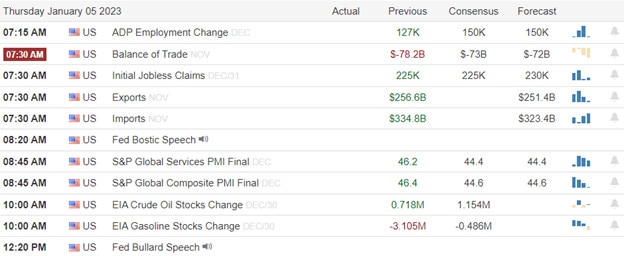

In economic news, December ADP Nonfarm Employment was up more than expected, adding 235k jobs (compared to a forecast of +150k and the Nov. reading of +182k). At the same time, both Imports and Exports were down in November, resulting in a Nov. Trade Balance that was better than expected at -$61.50 billion (versus a forecast of -$73.00 billion and the October value of -$77.80 billion). Later the Dec. S&P Global Composite PMI came in better than expected at 45.0 (compared to the forecast of 44.6 but still worse than the November reading of 46.4). Then the US December Services PMI came in at 44.7, which was better than expected (versus the forecast of 44.4 but again still worse than the Nov. reading of 46.2). Finally, EIA Crude Oil Inventories came in higher than expected at 1.694 million barrels (compared to a forecast of 1.154 million barrels and stronger than the prior week’s 0.718 million barrels).

In stock news, SFIX announced Thursday that its CEO will be stepping down effective immediately and also said it would be cutting about 20% of its workforce. Elsewhere, CAG raised its full-year sales forecast for 2023 by 7%-8% mostly on the impact of price hikes, and also increased its earnings forecast for the year. At nearly the same time, LW also raised its own 2023 revenue forecast to $4.8-$4.9 billion and significantly raised EPS guidance from $2.45-$2.85 all the way to $3.75-$4.00/share. Then BBBY announced that it was exploring options including bankruptcy to address its declining situation. Overseas, AAPL’s primary phone maker Foxconn said that production at its main plant in China had “basically returned to normal” after a 12% decrease in December. Meanwhile, LAZR announced that its Q4 production deals (orders) had exceeded the target for 60% year-on-year growth in its order book. Majority owner of WWE (former CEO) Vince McMahon elected himself and two allies to the board of directors (removing three others) with an eye on returning to a leading role one year after leaving over a sexual harassment scandal.

In government action news, a NY Judge has ordered that JPM does have to face a lawsuit from sunglasses maker Ray-Ban over a $272 million cyber theft from the French company’s New York bank account. Elsewhere, a US Bankruptcy judge has ruled that Celsius Networks actually owns most of its customers $4.2 billion crypto deposits. This means the customers will be last in line for payout from the lender’s bankruptcy case. Later in the day, PTON agreed to pay a $19 million fine for failing to promptly report a defect in their treadmills that could cause serious injury. Meanwhile, the FTC has proposed a rule that would forbid any company from requiring employees to sign non-compete or “training repayment” agreements. The rules are months from final passage, but if put into effect the FTC says it expects this would raise the wages of 30 million Americans by a total of $300 billion per year.

In miscellaneous news, for the second time in a week, natural gas futures (natty) plunged 11% in a day after Wednesday’s 5% increase. The very warm start to winter in the Northern Hemisphere (especially Europe) had hurt gas prices and put a large crimp in Russia’s efforts to squeeze Europe over its support of Ukraine. Elsewhere, Fed ultra-hawk Bullard said Thursday that he is optimistic the new year will bring relief from inflation. He also said “the probability of a soft landing has increased compared to where it was in the fall” adding that this is a great time to fight inflation because of the strong job market.

Overnight, Asian markets were mixed again. South Korea (+1.12%) was an outlier to the upside with Australia (+0.65%), Thailand (+0.60%), and Japan (+0.59%) leading the region higher. Meanwhile, India (-0.74%), Singapore (-0.48%), and Hong Kong (-0.29%) paced the losses. In Europe, the bourses are mostly green at midday. The FTSE (+0.27%) and CAC (+0.30%) lead the region higher while the DAX (-0.04%) is one of only two exchanges in the red in early afternoon trading. As of 7:30 am, US Futures are pointing toward a mixed and flat start to the day (ahead of December Payrolls data). The DIA implies a +0.12% open, the SPY is implying a -0.02% open, and the QQQ implies a -0.33% open at this hour. At the same time, 10-year bond yields are just slightly higher at 3.729% and Oil (WTI) is off fractionally to $73.38/barrel in early trading.

The major economic news events scheduled for Friday include Dec. Avg. Hourly Earnings, Dec. Nonfarm Payrolls, Dec. Participation Rate, and Dec. Unemployment Rate (all at 8:30 am), Nov. Factory Orders and Dec. ISM Non-Mfg. PMI (both at 10 am). The major earnings reports scheduled for the day are limited to GBX before the opening bell. There are no major earnings reports scheduled for after the close.

So far this morning, GBX has reported a beat on the revenue line while missing on the earnings line.

Unless you’ve been living under a rock, you know the other news of the day which is that the US House has yet to elect a Speaker as the GOP flounders to get its act together. The House adjourned again last night after an 11th attempt failed to reach the 218-vote majority required to elect a Speaker. The GOP is split with 6 “Never McCarthy” votes, 14 “Guarantee me more power” votes, and 202 “McCarthy” votes (of those 60 or so are said to be “McCarthy only” votes). The House will resume speech-making (nominations) and voting again at noon today as the fourth day of the Republican majority gets back underway. Again, if there is any good news, it is that without any real “GOP Platform Agenda” there is no real work that is being missed yet. The first real “must pass” legislation will be the US Debt Ceiling increase and that will not come for a few weeks. So far, markets do not seem to care and are just enjoying the distraction.

With that background, it looks like all three major indices are waiting to see what the December Payrolls data looks like before deciding what to do. Still, at this point in the premarket, all three major indices are close below their T-line (8ema) with the SPY retesting a support level and the QQQ seeming to work on a bearish Dreaded-h pattern. The consolidation range of the last 3 weeks continues to have a grip on the market. Regardless of the Payrolls data (where again, good news will likely be bad news for the market and visa-versa), be careful about chasing either direction on a Friday. No matter what it does today, this market can still break in either direction after reconsideration… especially a two-day reconsideration. If you do trade the post-announcement move, be very nimble or be prepared to wait out any reversal pressure your position might face. Volumes continue to be light as the big money has not decided on a direction yet.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

While encouraging to see a second day of gains, not much changed yesterday as the wide-range consolidation continues, unable to break through the upper resistance at the close. However, there seems to be a willingness to ignore the economic data pointing to a contraction of the U.S. economy. Today we get more job data along with international trade and energy figures as FOMC members resume their public conversations. Observe the substantial overhead resistance levels if they beak for a possible short squeeze to be triggered. On the other hand, if it fails to break, prepare for selling to resume pushing back into the consolidation range.

Asian markets saw gains overnight, and the European markets trade mixed as they came to terms with the continued hawkishness of the FOMC. U.S. futures have once again rebounded off overnight lows heading into the open ahead of earnings and potential market-moving economic reports amid some substantial layoff news in the tech sector.

Economic Calendar

Earnings Calendar

We have a bit more activity on the earnings calendar today. Notable reports include ANGO, BBY, CAG, STZ, HELE, LNN, NEOG, SCHN, & WBA.

News & Technicals’

Amazon, one of the largest employers in the U.S., is scaling back more than it had anticipated. Andy Jassy, Amazon’s CEO, said an employee leaked the plans, prompting him to make a public announcement. “Amazon has weathered uncertain and difficult economies in the past, and we will continue to do so,” Jassy wrote in a memo. However, they plan to cut over 18,000 positions from the reported number of 10,000. Salesforce is cutting 10% of its personnel (more than 7000 positions) and reducing some office space as part of a restructuring plan. Co-CEO Marc Benioff told employees that customers had been more “measured” in their buying decisions in the challenging macroeconomic environment. The cloud-based software company let go of hundreds of employees in November. CNBC’s Jim Cramer on Wednesday warned investors that the tech industry would likely see more layoffs due to continuing macroeconomic headwinds.

The U.S. House of Representatives adjourned for the night with no one being elected speaker, paralyzing Congress and deepening the longstanding schisms within the Republican Party. After six votes over two days, GOP leader Kevin McCarthy, R-Calif., failed to secure enough support to win the House speakership. The latest votes saw GOP holdouts nominate and vote for Florida Rep. Byron Donalds.

According to analyst estimates, Samsung’s profit could nosedive nearly 50% when it reports its fourth-quarter earnings guidance. The pessimism stems from a rapid fall in NAND and DRAM memory prices. Samsung is the global leader in memory chips. However, NAND and DRAM prices have fallen sharply in the fourth quarter due to a lack of demand for the products they eventually go into, such as PCs.

While it may have been refreshing to see a second day of gains, the wide-ranging consolidation continues, with the price action unable to breach upper resistance levels by the close of the day. The jobs data continues to roll in such a manner to keep the Fed engaged in continuing to raise rates, and according to the FOMC minutes released yesterday, their willingness to do so seems resolute. In addition, the ISM number indicated that the U.S. economy is still in contraction, adding worry to recessionary thoughts for the year ahead. Today we get more job data along with international trade and energy figures as Fed members resume public comments. Keep a close eye on the consolidation resistance as they continue to pump the premarket, trying to inspire enough buying to break through despite the poor economic numbers.

Markets gapped up again on Wednesday (0.60% in the SPY, 0.42% in the DIA, and 0.83% in the QQQ) and then looked to be following Tuesday’s example as we sold off to reach the lows by 10:15 am. However, then the dip-buyers stepped in to lead a steady rally that lasted until noon. After a 45-minute rest for lunch, the bears stepped in to drive us back near the lows by 2:30 pm, when another rally took over. This action gave us indecisive Doji or Spinning Top-like candles on the day. The large-cap indices managed to climb back just above while the QQQ remains just below its T-line (8ema). The DIA is also continuing to ride along its 50sma.

On the day, all ten of the sectors were in the green with the Consumer Cyclical sector (+3.11%) way out front leading the way higher as the Energy sector (+0.12%) lagged behind. Meanwhile, the SPY was up 0.75%, the DIA was up 0.40%, and the QQQ was up 0.47%. This took place on lower-than-average volume. At the same time, the VXX was down 2.72% to 13.61, and T2122 spiked back up to just outside of the overbought territory at 77.72. 10-year bond yields fell again to 3.679% and Oil (WTI) was down a whopping 4.85% to $73.21 per barrel. So, overall, it was a very indecisive back-and-forth day that remains in the consolidation of the last 2+ weeks.

In economic news, December ISM Mfg. PMI came in slightly below expectations at 48.4 (compared to a forecasted value of 48.5 and below the November value of 49.0). Meanwhile, November JOLTs Job Openings came in higher than expected at 10.458 million (versus the 10.000 million forecast and the October value of 10.512 million). Later, the December FOMC Minutes were released. In the minutes, it was clear that overall the group felt that restrictive policy was still in order until data indicated that inflation was clearly in a “sustained” downward trend toward 2 percent. The minutes also show that no voting members expect rate cuts during 2023. Finally, after the close, the API Weekly Crude Oil Stock Report came out showing a 3.298-million-barrel build (the first increase in three weeks), which was unexpected given the general consensus that the holiday week travel could cause a drawdown.

In stock news, CRM announced it is cutting 10% of its workforce (which should be roughly 7,900) and reducing office space in cost-cutting measures. CRM had already laid off hundreds of employees in November. Later, GM reclaimed its US sales crown from TM in 2022. GM sold 2.27 million vehicles (up 2.5% over 2021) compared to TM sales of 2.1 million (down 9.6% from 2021). Meanwhile, BLK is delaying redemptions from its UK property funds after a flood of investors have been seeking to exit Britain’s property market. During the afternoon, JEF surged following a Nikkei Asia report that SMFG is in the process of raising its stake in Jeffries. The CEO of SMFG told the outlet that he wants to increase the stake to between 20% and 50% of JEF as soon as discussions with US regulators and JEF management are concluded (SMFG already owns a 5% stake in JEF).

In government action news, CACC was sued by the US Consumer Finance Protection Bureau and the NY State Attorney General for predatory auto lending (misleading its customers and tricking them into taking high-cost loans on used cars). Elsewhere, COIN reached a $100 million settlement (which includes a $50 million penalty) with the NY State Dept. of Financial Services for failure to comply with laws regarding account creation. The FTC disclosed that it had forced OI to drop non-compete requirements that limited where its employees could seek work after leaving OI. (The agreements had covered about 1,700 workers.)

In energy news, Venezuela’s lack of dredging maintenance has caused a problem for CVX as it attempts to load and move four tanker ships. The joint ventures with the Venezuelan government intended to bring heavy crude to the US (Mississippi refineries). The channel to oil terminal in Venezuela is only deep enough to allow tankers to load up to half capacity. Small tankers are being used to shuttle the heavy oil to a ship-to-ship transfer at sea to fill the larger tankers. Elsewhere, as mentioned above, the API Weekly Crude Stock report also showed a 1.2-million-barrel build in gasoline (compared to an expected 486k barrel drawdown). However, there was also a 2.4-million-barrel drawdown in distillate (diesel and heating oil) stocks.

Overnight, Asian markets were mostly green. Shenzhen (+2.13%), Singapore (+1.55%), and Hong Kong (+1.25%) led the region higher while only a couple of exchanges were in the red. In Europe, we see a more mixed picture but still leaning to the upside at midday. The FTSE (+0.46%), DAX (-0.09%), and CAC (+0.05%) lead the region as usual with no clear direction chosen yet in early afternoon trade. As of 7:30 am, US Futures are pointing to a start to the day just on the green side of flat. The DIA implies a +0.05% open, the SPY is implying a +0.15% open, and the QQQ implies a +0.29% open at this hour. At the same time, 10-year bond yields are up a bit to 3.688% and Oil (WTI) is up 2.27% to $74.49/barrel in early trading.

The major economic news events scheduled for Thursday include Dec. ADP Nonfarm Employment Change (8:15 am), Weekly Initial Jobless Claims and Nov. Trade Balance (both at 8:30 am), Dec. Global Composite PMI and Dec. Services PMI (9:45 am), and EIA Weekly Crude Oil Inventories (11 am). The major earnings reports scheduled for the day include STZ, HELE, LW, MSM, RPM, SCHN, and WBA all before the opening bell. There are no major earnings reports scheduled for after the close.

In economic news later in the week, on Friday, we get Dec. Avg. Hourly Earnings, Dec. Nonfarm Payrolls, Dec. Participation Rate, Dec, Unemployment Rate, Nov. Factory Orders, and Dec. ISM Non-Mfg. PMI. And in terms of earnings, on Friday, GBX reports.

So far this morning, WBA, CAG, MSM, and HELE have all reported beats on both the revenue and earnings lines. Meanwhile, RPM missed on revenue while reporting in line on earnings. (STZ, LW, and SCHN report closer to the opening bell.)

In late-breaking news, AMZN has announced it will be laying off more than 18,000 employees. This is a much larger number than the 10,000 layoffs the tech giant had originally planned. We also have three previously unplanned Fed speakers today (Harker at 7:30 am, Bostic at 9:20 am, and Bullard 1:20 pm). And on the Congress front, after six failed votes, the Republicans are no closer to electing a new Speaker of the House as a group of 20 extreme conservatives are revolting in a combination of “give us even more power”, “let any one GOP Congressman call for a new Speaker vote at any time”, and “I’ll never vote for McCarthy” protests. A seventh vote will begin again at noon today. (The good news is that since the GOP has no real agenda, the first real piece of House business does not have to come for weeks, when the Debt Ceiling will need to be increased to avoid the US defaulting on its debt.)

With that background, it looks like all three major indices are trying to start the day slightly green. The SPY and DIA are holding on above their T-line and the QQQ is retesting its own T-line (8ema) from below this morning. The consolidation which has been holding for the last two weeks still seems to have a grip on the market. So, be careful about getting too bullish too soon. This market could still break in either direction. Sitting on your hands remains not the worst idea ever. However, if you trade, continue to either be very nimble or prepared to wait out any short-term pressure your position might face. The volumes are likely to pick up this week but the big money eases back into the market slowly and it hasn’t happened yet. (Remember, the big money does not chase. They buy strictly in a price band and will wait for the price to come back to them.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: EOSE, MASI, CLF, CAT, IAG, BBWI, BIDU, and AUY. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service