Powell Giveth and Yellen Taketh Away

Markets opened flat on Wednesday as traders waited on the Fed decision. The three major indices then wandered around the opening level before a midday selloff. The bulls then stepped in at about 1:15 pm and rallied markets into the Fed announcement. At that point, all three showed major volatility, first spiking up, selling off hard, and reversing again and again. All three reached the highs of the day at 2:50 pm before then putting in the strongest downtrend of the day. This move saw a 3:15 pm bounce but resumed and took all three major indices out on their lows. This action gave us large, black-bodied candles with large upper wicks in the SPY, DIA, and QQQ. The DIA also printed an Evening Star signal and crossed back below its T-line and 200sma. SPY crossed down its 200sma while remaining above its T-line. And, continuing to be the strongest of the major indices, QQQ remains well above its T-line.

On the day, all 10 sectors were in the red with Financial Services (-2.39%) leading the way lower while Consumer Defensive (-0.80%) held up better than the other sectors. At the same time, the SPY lost 1.70%, the DIA lost 1.67%, and QQQ lost 1.36%. VXX climbed 4% to 50.43 and T2122 dropped back into the oversold territory at 8.06. 10-year bond yields plummeted again to 3.451% while Oil (WTI) gained half of a percent to $70.02 per barrel. So, Wednesday saw huge volatility following the Fed statement, Dot Plots, and press conference the bulls seemed to like but Treasury Sec. Yellen said the FDIC will not cover all deposits, which gave the bears firm control at the end of the day (on fears of more regional bank runs). This all happened on average volume.

In economic news, the EIA Weekly Crude Oil Inventories came in much higher than expected at +1.117 million barrels (compared to a forecast that called for a drawdown of 1.565 million barrels and the prior week’s build of 1.550 million barrels). Later, the Fed Future Interest Rate Projections (aka Dot Plots) showed a forecast of 5.1% (the terminal rate) for 2023 (up from the prior forecast of 4.4%), 4.3% interest rate in 2024 (down from the prior forecast of 5.1%), and 3.1% in 2025 (down from the prior forecast of 4.1%). The FOMC also raised the Fed Funds Rate by 25 basis points to the 4.75%-5.00% range. The Fed statement continued to predict one more rate hike and no rate cuts in 2023. However, they also stated that the future hike is not a sure thing and will depend on data. During his press conference, Fed Chair Powell said “the US banking system is sound and resilient.” He also said disinflation is happening, that the Fed had considered a rate hike pause due to the banking issue, and that this current situation with regional banks is likely to tighten credit conditions for households and businesses (which will help the Fed to curb inflation by weighing on the economy). At the same time, Treasury Sec. Yellen told the Senate Banking Committee that banks have been shoring up their liquidity the last two weeks and that the government was taking steps to protect depositors. However, she said the FDIC was not considering providing “blanket insurance” (insuring all deposits regardless of size) at this time. She said it was worthwhile to look at changes, but increasing above the current $250,000 limit is not being considered. Still, she said when a bank fails and is believed to pose a systemic risk (i.e., pose a risk of contagion of bank runs) “we are likely to invoke a risk exception” that allows the FDIC to cover all deposits. So, basically, Yellen said they won’t insure all deposits but if a bank gets run and they think it will prevent panic, they will cover all deposits for that specific bank. (Here’s to hope that your bank is likely to cause a panic if it goes under.)

SNAP Case Study | Actual Trade

In stock news, the CFO of BA said Wednesday that the company will be taking more charges due to supplier quality issues on the KC-46 Tanker jet program, but added that the charges would not impact BA annual cash flow. Elsewhere, the surprise GME profit on Tuesday night triggered a massive short-squeeze resulting in a 35% gain after a very volatile day that saw the stock up 53% at one point. Meanwhile, BIDU’s smart car business unit received approval to be the first company to test autonomous vehicles on the road in Shanghai (population 26 million). At the same time, Reuters reported that the MSFT search engine Bing has received a 15.8% boost in usage (compared to a 1% decline in the use of the GOOGL search engine) since the February 7 release of Bing’s AI-powered (ChatGPT) engine. However, please be aware that Bing’s share of searches was so small to start with that this seemingly big move is really tiny overall. In other news, ALB announced it will be opening a $1.3 billion lithium processing plant in South Carolina. After the close, COIN said it has been issued a Wells Notice (notice the SEC intends to bring enforcement action). Finally, F announced on Thursday it will be re-releasing 2021 and 2022 results to reflect a finer level of detail by business unit. This is the first major car company to do so and will give much more insight into the company (and industry). Industry analysts expect to see massive losses from the electric vehicle unit but time will tell.

In stock legal and regulatory news, the CEO of MRNA defended the new, dramatically higher $130/dose price (versus $18/dose) for the COVID-19 vaccine before the US Senate Wednesday. He was pushed by Senator Sanders but responded by pointing out it will be in single-dose syringes rather than in the 10-dose vials sold to the US government in 2021-2022. In other drug news, the NIH announced it will not be using its “march-in” rights to grant production licenses to other manufacturers for the PFE prostate cancer drug Xtandi. The agency said their analysis shows the drug is widely available (despite it selling for $170,000/year/patient). At the same time, the US FDA has declined to approve ABBV’s Parkinson’s disease therapy. This was a significant hit to ABBV, as the treatment was meant to be one of the company’s biggest drug introductions in the next one to two years. Elsewhere, Reuters reported that GOOGL will gain unconditional EU antitrust approval for the acquisition of math app Photomath. The European Commission will rule on the deal on March 28, but sources tell Reuters the deal is approved. Meanwhile, on this side of the pond, JNJ has appealed to the US Supreme Court to revive its effort to use bankruptcy law to avoid liability in more than 38,000 cases alleging JNJ’s Baby Powder (contaminated with asbestos) caused damages. In other news, House GOP members are lining up behind business interests as they summoned NRLB officials while alleging the NRLB had been unfair to SBUX in ruling that the company broke labor law hundreds of times in its effort to fight unions. In transportation, the FAA agreed to a request from DAL to reduce the “minimum flights requirement” and New York and Washington DC airports. The change will allow DAL and UAL to operate fewer flights (during congestion, staff outages, or whatever) without losing their landing slots at those airports.

After the close, CHWY, KBH, WOR, and SCS all reported beats on both the revenue and earnings lines. Meanwhile, MLKN missed on revenue while beating (significantly) on earnings. It is worth noting that MLKN lowered forward guidance and SCS raised guidance at the time of the report. It is also worth noting that in addition to MLKN, CHWY, and WOR earnings were significant upside surprises versus the average analyst forecast.

Overnight, Asian markets were mixed but leaned toward the green side. Australia (-0.67%), India (-0.44%), and Japan (-0.17%) led the losses. Meanwhile, Hong Kong (+2.34%), Shenzhen (+0.94%), and Taiwan (+0.66%) paced the gainers. In Europe, markets are red across the board at midday. The CAC (-0.55%), FTSE (-0.97%), and DAX (-0.63%) are typical and are leading the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.20% open, the SPY is implying a +0.47% open, and the QQQ implies a +0.90% open at this hour. At the same time, 10-year bond yields are back up to 3.50% and Oil (WTI) is down three-quarters of a percent to $70.43/barrel in early trading.

The major economic news events scheduled for Thursday include Building Permits (8 am), Q4 Current Account and Weekly Initial Jobless Claims (8:30 am), and February New Home Sales (10 am). The major earnings reports scheduled for the day include ACN, DOOO, CMC, DRI, FDS, and GIS before the opening bell. Then after the close, JOAN reports.

In economic news later this week, on Friday, Feb. Durable Goods, Mfg. PMI, S&P Global Composite PMI, and Services PMI are reported. In earnings later this week, on Friday, EXPR reports.

So far this morning, ACN, GIS, DRI, and DOOO all reported beats on the revenue and earnings lines. Meanwhile, FDS missed on revenue while beating on earnings. On the other side, CMC beat on revenue while missing on earnings. It is worth noting that GIS has raised its forward guidance.

In late-breaking news, Bloomberg reports that the big Wall Street banks have eased off of their previously announced hiring freezes as they attempt to snap up the best talent available from CS. Elsewhere, F began releasing its prior results broken out by business unit. It seems the EV unit lost $2.1 billion in 2022, which was offset by $10 billion in operating profits from the internal combustion and fleet sales units. Finally, the CEO of C (Jane Fraser) said that the SIVB collapse demonstrates we are in a new world where bank customers can move millions of dollars with just a couple clicks from any location. She implied there need to be new or changed regulations to protect banks from “digital runs” because remote access to money electronically has removed banks’ ability to forecast the need for liquid assets.

With that background, it looks like the bulls are looking to make a move against yesterday’s late-day selloff. This is especially true in the QQQ. SPY has recrossed its T-line (8ema) and 200sma to the upside in premarket. Overextension from the T-line is not an issue in any of the big indices. However, T2122 is back in the oversold zone. While there is some economic news (including Weekly Jobless Claims) today, I suspect that talk and fears related to regional banks may be a big driver of direction. Until the regional banks stocks calm down, it will be hard for the big banks to hold up. And without the big banks, it’s hard for the DIA and SPY to hold ground either. So, be cautious and don’t let FOMO put you in a position where this daily chop eats you alive.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yellen Says US Could Cover More Deposits

On Monday, markets started the day essentially flat (opening up 0.15% in the SPY, up 0.27% in the DIA, and down 0.33% in the QQQ). After that open, the SPY rallied slowly until 11:30 am. Meanwhile, the DIA rallied more strongly but only for 30 minutes. The QQQ sold off during the first 30 minutes but then rallied until 11:30 am. From that point, all three major indices had a midday slump before rallying right back to where they were at 11:30 am. This action gave us a white-bodied inside day candle in the SPY (crossing above its T-line in the process). QQQ printed a white-bodies Hammer candle. For its part, DIA printed a white, large-bodied candle with only a tiny upper wick (also crossing back above its own T-line by pennies). This happened on average volumes (down from the last week and a half) as traders wait on the Wednesday Fed move.

On the day, all 10 sectors were in the green with Energy (+1.68%) leading the way higher while Consumer Cyclical (+0.38%) lagged behind the other sectors. At the same time, the SPY gained 0.94%, the DIA gained 1.19%, and the QQQ gained 0.20%. VXX fell 5% to 53.16 and T2122 rose back out of the oversold area to 24.82. 10-year bond yields climbed (significantly from premarket open) to 3.492% while Oil (WTI) fell 1.15% to $67.51 per barrel. So, Monday saw markets calm down after the Friday bank worries. This came even though FRC got hammered (-47.11% after several trading halts during the day) and a few other regionals were also big losers. However, NYCB, PACW, FCNCA, and other regional banks also were big winners on the day.

In stock news, AMZN announced Monday that it will lay off 9,000 more employees in the coming weeks. (The company laid off 18,000 in November – January.) In leadership news, the CEO of NCLH announced Monday that he is retiring in June and will be succeeded by insider Frank Del Rio. At the same time, SBUX CEO Shultz left two weeks early with new CEO Narasimham taking over Monday. Elsewhere, MULN announced it has acquired both the North and South American distribution rights for the DragonFLY K50 electric supercar (capable of 0-60mph in 2 seconds and a top speed of more than 200mph). At the same time, PSNY officially launched an electric SUV in China and clashed its starting price by $29,000 in doing so. It is unclear if PSNY intends to offer the reduced prices in the US as well. Meanwhile, JPM CEO Dimon is heading up talks with other major bank CEOs in an effort to rescue and stabilize FRC. The Wall Street Journal reports sources to the talks tell them that some or all of last week’s $30 billion in deposits the big banks made at FRC may be converted to a capital injection. However, the same sources told WSJ that a complete buyout is also on the table. In other banking news, COIN has stopped support for the SBNY digital payment platform (more than a week after regulators took control of the bank and a day after NYCB entered into an agreement to buy the deposits and loans of SBNY). In M&A news, RBA completed its acquisition of IAA on Monday. In M&A rumors, Reuters reports the TMO and South Korean firm Celltrion are competing to acquire the BAX Biopharma Solutions unit. Sources told Reuters the sale could net BAX $4 billion.

SNAP Case Study | Actual Trade

In stock legal and regulatory news, European Commission Vice President Vestager said Monday that tax deals between multinationals and EU countries amount to illegal tax breaks. She indicated new investigations into many multinational companies are likely to happen. Europe’s top court has not yet ruled on her ruling (thrown out by lower courts) against AAPL, AMZN, and SBUX. However, the same court did uphold her ruling against ENGIY and her actions have forced Luxembourg, the Netherlands, and Belgium to change their practices of giving breaks to corporations. Elsewhere, the NHTSA said Monday that F has recalled 1.5 million (2013-2018 Fusion and Lincoln MKZ) vehicles over faulty brakes and wipers. Meanwhile, GOOGL has denied charges from the US DOJ (and 30 states) that the company intentionally destroyed records of internal chat communications related to the search business as part of an antitrust case. GOOGL said it made “reasonable efforts” to preserve those records since the case was filed in 2020 but unfortunately those records have now been permanently deleted. In other potential news, IATA (an airline industry lobbying group) told Reuters Monday that increased airline travel may trigger UN-based global emission caps on the major airlines (AAL, DAL, UAL, JBLU, etc.) as soon as 2024.

In energy news, Reuters reported that US crude oil exports to Europe have hit another record this month, at an average of 2.1 million barrels per day so far in March. The report cited lower demand from US refineries and the broad discounts in the WTI benchmark price. Meanwhile, over in the Natural Gas space, the front-month April Natty contract continued falling Monday. The price closed at $2.24/mmBtu, the lowest closing price since February (which was itself the low since July 2020).

In miscellaneous news, President Biden used his first veto to slap down the anti-ESG bill (which forbade federal employee retirement funds from considering ESG issues for any reason when choosing investments, regardless of the implications of such or customer preferences). The bill had passed both houses of Congress with small majorities. So, it is unlikely supporters can overcome the veto. On the other side of the political aisle, a few GOP lawmakers have already requested all documents and personnel records from the Fed and FDIC relating to the failures of SIVB and SBNY banks. Their letter to the agencies seems to state a conclusion (before beginning) with the letter demanding the records, citing what “appears to be glaring bank mismanagement and regulators lack of basic supervision and enforcement of…rules.” There is no word on when the investigation will begin or when hearings will be held.

Overnight, Asian markets leaned heavily to the green side. Japan (-1.42%) and New Zealand (-0.29%) were the only red in the region. Meanwhile, Shenzhen (+1.60%), Thailand (+1.40%), and Hong Kong (+1.36%) led the area markets higher. In Europe, we see green across the board at midday. The FTSE (+1.37%), DAX (+1.64%), and CAC (+1.50%) are leading the continent higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a move higher to start the day. The DIA implies a +0.88% open, the SPY is implying a +0.80% open, and the QQQ implies a +0.54% open at this hour. At the same time, 10-year bond yields are climbing fast to 3.549% and Oil (WTI) is up fractionally to $67.79/barrel in early trading.

The major economic news events scheduled for Tuesday are limited to Feb. Existing Home Sales (10 am) and API Crude Oil Stocks Report (4:30 pm). The major earnings reports scheduled for the day include CSIQ and TME before the opening bell. Then after the close, AIR, GME, and NKE report.

In economic news later this week, on Wednesday, EIA Crude Oil Inventories, Q1 Interest Rate Projections, the Fed Rate Decision, and the Fed Statement, are all reported and Fed Chair Press Conference takes place. On Thursday, we get Building Permits, Q4 Current Account, Weekly Initial Jobless Claims, and New Home Sales. Finally, on Friday, Feb. Durable Goods, Mfg. PMI, S&P Global Composite PMI, and Services PMI are reported.

In earnings later this week, on Wednesday, OLLI, WOOF, WGO, CHWY, KBH, MLKN, SCS and WOR report. On Thursday, we hear from CAN, DOOO, CMC, DRI, FDS, and GIS. Finally, on Friday, EXPR reports.

So far this morning, CSIQ and TME reported beats on both the revenue and earnings lines. It is worth noting that CSIQ also lowered its forward guidance.

In late-breaking news, this morning Treasury Sec. Yellen told an American Bankers Association audience that the government is ready to guarantee more deposits if the banking crisis were to worsen. In an apparent attempt to stave off criticism (mostly from GOP lawmakers but also the most progressive Democrats), she said the actions taken so far were not aimed at any specific banks or classes of banks but instead were to protect the broader US Banking system. She went on to say “And similar actions could be warranted if smaller institutions suffer deposit runs that pose a risk of contagion.” FRC (currently the most troubled bank) jumped 15% in premarket after her remarks were published. Finally, as of this morning, the Fed Funds Futures are saying that there is an 86.4% probability of a quarter-point hike by the Fed tomorrow and a 13.6% chance we see no hike.

With that background, it looks like the bulls are making another charge this morning (at least in the premarket). SPY is challenging Thursday’s high and DIA is well above its recent high. However, while QQQ is moving up, it remains below the recent highs from Thursday and Friday. Overextension is still not an issue in any of the big indices and T2122 is up out of the oversold territory at this point. While the regional banking issue may cause more turbulence, I suspect we may be in the “wait and see” area ahead of Fed actions on Wednesday. So, the bulls may make a run this morning and we should be prepared for bank-caused volatility. However, much like Monday afternoon, I think we may drift until there is certainty on the Fed’s move.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Welcome to Spring – UBS Buys CS

On Friday, markets gapped lower in the large-cap indices (down 0.74% in the SPY and down 0.82% in the DIA) while the QQQ opened flat. This came after markets had rethought the Thursday lifelines that had been thrown the CS ($50 billion loan) and FRC ($30 billion in deposits from the US mega banks). After a half hour of waffling to the side, all three major indices sold off sharply until 11:45 am. From there, the rest of the day saw a sideways grind inside of a tight range. This action gave us Bearish Harami candles in the two large-cap indices and a black Spinning Top in the QQQ. It is worth noting that the SPY crossed back down through its T-line (8ema) and 200sma after having crossed above Thursday.

On the day, all 10 sectors were in the red with Financial Services (-3.09%) leading the way lower while Communications Services (-0.64%) held up better than other sectors. At the same time, the SPY lost 1.55%, the DIA lost 1.47%, and the QQQ lost 0.47%. VXX spiked by 10.90% to 55.96 and T2122 dropped back inside of the oversold area at 8.54. 10-year bond yields plunged to 3.429% on a risk-off day while Oil (WTI) fell another 2.96% to $66.34 per barrel. So, Friday saw a gap lower on more fear of bank collapses. However, the QQQ bulls did not really give much back and remained the strongest of the major indices. Once again, this happened on heavier-than-average volume across the board, particularly in the QQQ. This pattern of increasing volumes has been noticeable the entire last week.

In economic news, February Industrial Production came in far below expectation on a year-on-year basis at -0.25% (compared to a forecast of +3.00% and the January reading of +0.49%). On a month-on-month basis, Feb. Industrial Production was flat but still below the expectation of +0.2% and far below the January monthly +0.3% value. So, bottom line, for the third day in a row we had data suggesting industrial manufacturing is not in great shape. Then, later in the day, Michigan Consumer Sentiment also came in below expectation at 63.4 (versus a forecast of 66.9 and well below the February reading of 67.0). With all of that said, fear of spreading liquidity problems for regional banks (which have plowed massive amounts of money in long-dated bonds for years and now would lose their shirts if forced to sell in order to fulfill deposit redemption requests) and the entire CS solvency problem, made the health of the US and Global banking system the primary economic topic Friday.

SNAP Case Study | Actual Trade

In stock news, META launched a verification subscription service like the one Elon Musk did at Twitter and later SNAP launched. The META service is available on both Facebook and Instagram. Elsewhere, Bill Ackman tweeted Friday that BAC is buying recently closed SBNY as of today (Monday). He didn’t cite a source of his information. However, Reuters then reported that sources tell it that Ackman’s rumor is false. In unrelated news, the Financial Times reported Friday that the GS trading desk has lost around $200 million in the market turmoil following the collapse of SIVB. Meanwhile, after the close Friday, BRKB urged its shareholders to reject proposals that company management avoids discussing hot-button social and political issues. They also asked shareholders to reject a proposal that the company discloses more about its climate change and diversity efforts. At the same time, but unrelated, BBBY announced it will do a reverse stock split and a special meeting on March 27 to determine the ratio (between 1-for-5 and 1-for-10). The BBBY stock was down 23% in after-hours trading on the news. Finally, the Wall Street Journal reported that DIS kept 94% of its subscribers despite raising prices 38% on its Disney+ streaming service.

In stock legal and regulatory news, the SEC will vote Wednesday on new regulations first proposed in January 2022 that would require funds to report within one business day any events indicating “significant stress.” (The idea, introduced after the Archegos Capital Management collapse, is that even the collapse of private funds could pose a systemic threat to other financial institutions.) Elsewhere, ASTR has asked Nasdaq for more time to get its stock price back above $1 to avoid being delisted. The company has not been in compliance since October. ASTR said it expects to hear back from the exchanges by April 5, which follows its March 30 earnings report. If an extension is not granted, ASTR will face being dropped by the exchange. After the close Friday, a US Appeals Court revived a lawsuit by UBER challenging the CA law that would require them to provide proof that workers are independent contractors in order to avoid having to treat them as employees. Meanwhile, days after being sued by the state of Ohio, NSC shareholders sued the railroad for defrauding them by prioritizing profit over safety. (Being too risk-seeking instead of capital preservationist.) Finally, on Sunday, the FDIC said that a subsidiary of NYCB will take over the vast majority of SBNY (including the branches and $60 billion in outstanding loans), leaving about $4 billion in receivership.

Regarding the CS saga, Friday afternoon, Reuters reported that CS would be holding internal talks over the weekend on “the scenarios facing the bank.” That came as other major European banks had already “curbed dealing with CS” until after events play out. Those banks included DB and SCGLY, and HSBC according to Reuters. Friday night, the Financial Times reported that UBS was in talks to buy CS or at least some of the assets of CS. By Sunday, Bloomberg reported that UBS had offered to buy CS for (a paltry) $1 billion and that CS was pushing back against that offer. Meanwhile, the Financial Times said multiple sources told it that the Swiss government was seriously considering either a partial or full nationalization of the troubled bank. Finally, on Sunday evening, CS agreed to terms with UBS acquiring them for $3.2 billion (CS shareholders get 1 UBS share for every 22.48 CS shares they hold). The Swiss National Bank also pledged a $108 billion loan to support the takeover project.

Overnight, Asian markets were red across the board. Hong Kong (-2.65%) was by far the biggest loser with Japan (-1.42%). Australia (-1.38%), Singapore (-1.37%) and New Zealand (-1.37%) leading the region lower. Meanwhile, in Europe, the bourses lean heavily toward the green side at midday. The FTSE (+0.22%), DAX (+0.65%), and CAC (+0.73%) are leading the region higher in early afternoon trade. As of 7:30 am, US Futures are Pointing toward a start to the day just on the green side of flat. The DIA implies a dead flat open, the SPY is implying a +0.02% open, and the QQQ implies a +0.03% open at this hour. At the same time, 10-year bond yields continue to fall, now at 3.376% and Oil (WTI) is off 1.5% to $65.74/barrel in early trading.

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for the day include FL and PDD before the opening bell. Then after the close, ACDC reports.

In economic news later this week, on Tuesday we get Feb. Existing Home Sales and EIA Crude Oil Inventories. Then Wednesday, Q1 Interest Rate Projections, the Fed Rate Decision, and Fed Statement are all reported and the Fed Chair Press Conference takes place. On Thursday, we get Building Permits, Q4 Current Account, Weekly Initial Jobless Claims, and New Home Sales. Finally, on Friday, Feb. Durable Goods, Mfg. PMI, S&P Global Composite PMI, and Services PMI are reported.

In earnings later this week, on Tuesday, we hear from CSIQ, TME, AIR, GME, and NKE. Then Wednesday, OLLI, WOOF, WGO, CHWY, KBH, MLKN, SCS and WOR report. On Thursday, we hear from CAN, DOOO, CMC, DRI, FDS, and GIS. Finally, on Friday, EXPR reports.

So far this morning, FL posted beats on both the revenue and earnings lines. (FL posted a massive beat on revenue…at 86.5% positive surprise.) However, PDD missed on revenue while beating on earnings. It is worth noting that FL also lowered its forward guidance.

With that background, it looks like the SPY is remaining in its range from the previous seven days. At the same time, DIA was below its own seven-day range but has climbed back up into that area now. Meanwhile, the QQQ (which has been the market leader for some time) seems to be continuing its pullback inside Thursday’s big bullish candle…at least in premarket action. Overextension is not an issue in any of the indices at this point. However, T2122 is well into the Bullish Reversal Zone (extended). Another issue we have to deal with today is that the banking situation in the US (mainly regionals) is not settled. FRC is down more than 20% in premarket action (which is actually a 26% recovery from the premarket lows). On the other hand, NYCB and PACW are up 30% and 18% respectively. So be prepared for volatility swings as the explosiveness of regional banks spills over into other areas of the market on what would normally be a “wait and see” a couple of days ahead of the Fed Meeting Wednesday.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

CS and FRC Down Again On Rethink

Markets opened weak on Thursday with SPY gapping down 0.62%, DIA gapping down 0.59%, and QQQ gapping down 0.29%. However, bulls immediately started a strong rally in the QQQ and the two large-cap indices followed after an hour of wandering around near the open. Shortly after 1 pm, all three major indices rallies began a very mild consolidation pullback that lasted until 2:40 pm. At that point, a more modest rally got underway again and drove into the close with the SPY, DIA, and QQQ all closing very near the highs of the day. This action gave us large, white-bodied candles with very little wick. Again, the QQQ led, bouncing up off its T-line (8ema) and pulling away during the day to break the downtrend line that had held since the start of February. For its part, the SPY crossed up through its T-line and 200sma. Meanwhile, the DIA came up and is sitting just below both its T-line and 200sma.

On the day, nine of the 10 sectors were in the green with Technology (+2.77%) leading the way higher while Communications Services (-0.27%) was the only red sector. At the same time, the SPY gained 1.73%, the DIA gained 1.17%, and the QQQ gained 2.64%. VXX plummeted 8.19% to 50.46 and T2122 surged back up out of oversold territory at 31.93. 10-year bond yields surged to 3.587% on a risk-on day while Oil (WTI) climbed 1.12% to $68.32 per barrel. So, Thursday, saw a gap lower on lasting fear of bank contagion. However, the bulls led by tech (particularly semiconductors) rallied markets out of the recent choppy consolidation range. Again, this happened on heavier-than-average volumes across the board, particularly in the QQQ.

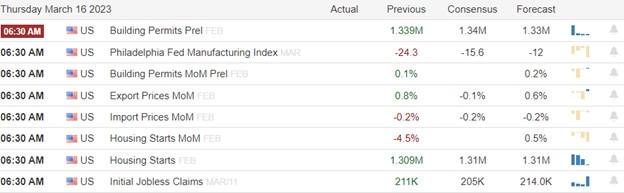

In economic news, February Building Permits came in notably stronger than expected at 1.524 million (versus a forecast of 1.340 million and much stronger than the January reading of 1.339 million). Likewise, the February Housing Starts came in above expectations at 1.450 million (compared to the forecast of 1.310 million and the Jan. value of 1.321 million). This meant Building Permits were up 13.8% for February and Housing Starts were up 9.8%. Both seem to show the housing market remains strong. Meanwhile, the February Export Price Index was well above expectation at +0.2% (compared to a forecast of -0.1% but down significantly from the January +0.5% value). At the same time, the February Import Price Index fell but not as much as expected at -0.1% (versus a forecast of -0.2% and a January reading of -0.4%). This means the average value of the goods the US exported rose while the average value of goods imported fell in February. Elsewhere, Weekly Initial Jobless Claims came in lower than expected at 192k (compared to a forecast of 205k and well below the prior week’s 212k). All of the above tends to show a robust economy. On the other side of the ledger, like the Empire State report Wednesday, the Philly Fed Mfg. Index came in well below the reading expected at -23.2 (versus a forecast of -15.6 but slightly better than the Feb. reading of -24.3). So, currently (March), Manufacturing seems to have slowed greatly while the rest of the economy appears to still be in good shape.

SNAP Case Study | Actual Trade

In stock news, the Financial Times reported that HOOD made a policy exception (policy banning short positions) for their customers who had Puts on SBNY. The exception will allow HOOD customers holding profitable Puts in SBNY to keep those positions open into the expiration date (today). Elsewhere, STLA has launched the first tranche of its nearly $1.6 billion buyback program starting today and going through June. Meanwhile, BLNK announced Thursday that it has won a contract from the US Postal Service to sell the agency 41,500 electric vehicle charging units. (No dollar amount was given for the contract.) Mid-afternoon, Reuters reported that PACW was well into talks about receiving a liquidity boost from ATCO. In other regional bank news, FRC received $30 billion from JPM, C, BAC, WFC, GS, and MS as part of a rescue package. Later, to calm investor fears, the CEO of MULN released a statement telling investors that the automaker was on track to fulfill its deliveries schedule, including beginning delivery for a 6,000-unit order before the end of March. After the close, MSFT announced and made a demo of a new “AI Copilot” for its Office 365 programs (Word, Excel, PowerPoint, and Outlook). The AI product will first be released to 20 of MSFT’s enterprise customers but will be rolled out wider soon. Finally, DUK announced after the close, that its unit in Central Florida (Polk County) will begin construction this month on its first water-based (lake) solar array of 1,800 floating solar panels (generating 1 megawatt) covering 2 acres of water.

In stock legal and regulatory news, AAL lost an appeal to the European Union Court of Justice which had sought to get the EU to nullify an agreement between AAL and DAL (where AAL gave up two airport landing slots to DAL for the Heathrow and Philadelphia airports) due to DAL not using the slots they were given. At nearly the same time, London’s High Court ruled LNVGY (Lenovo) must pay IDCC $138.7 million for a license for use of a portfolio of IDCC’s telecom patents. Elsewhere, CS was sued by US investors claiming the bank defrauded them by concealing problems and for having material weaknesses in internal controls that contributed to those shareholders having the wrong impression of the bank’s finances. Meanwhile, after the close, the FDA Advisory Board voted 16-1 in favor of full approval of the PFE oral COVID-19 antiviral treatment for adults at high risk of progression to severe disease. (The FDA very seldom rules against the Advisory Board’s recommendation.) Also, after the close, Dept. of Labor investigators reported that BP safety rules and poor training contributed to the death of two Ohio refinery workers last year. OSHA has proposed that BP pay $156,250 in penalties (the amount is limited by federal statute) for eleven violations at the facility, which BP has since sold to CVE.

In miscellaneous news, the Fed reported data Thursday evening saying that banks had borrowed a record $153 billion from its Discount window over the last week. This was a massive jump over the prior week’s borrowing of $4.58 billion. In addition, it was a huge increase in the record borrowing from the Fed. Prior to this week, the previous record was $111 billion borrowed in one week during the 2008 financial crisis. Elsewhere, there are a few troubling signs (in terms of economic strength) coming out of how companies treat their employees when times get tough. BBBY announced Thursday that it will not pay severance to the employees let go from stores the retailer closes. (Presumably, those people would still be eligible to draw state unemployment insurance benefits, meaning presumably the company paid unemployment premiums for those employees.) Then, last night, GOOGL decided it will not honor previously approved (and started) medical or maternity leave of those employees it has laid off. However, regardless of the employee’s status at the time of layoff, those people will get standard severance as of their termination date. There was no word on how much this move will save the tech giant.

After the close, FDX missed on the revenue line but crushed estimates on earnings ($3.41 versus the analyst-expected $2.76 per share). FDX also raised its forward guidance for 2023.

Overnight, Asian markets ended the week green across the board. Hong Kong (+1.64%), Taiwan (+1.52%), Malaysia (+1.46%), and Japan (+1.20%) led the region higher. Meanwhile, in Europe, the bourses lean heavily to the green side at midday. Only Portugal (-1.05%) and Switzerland (-0.25%) are in the red. At the same time, the FTSE (+0.45%), DAX (+0.33%), and CAC (+0.19%) lead the rest of the region higher in early afternoon trading. As of 7:30 am, US Futures are modestly down. The DIA implies a -0.44% open, the SPY is implying a -0.30% open, and the QQQ implies a -0.03% open. 10-year bond yields are falling significantly again (implying a move to safety) at 3.50% and Oil (WTI) is up 0.35% to $68.59/barrel in early trading.

The major economic news events scheduled for Friday are limited to Feb. Industrial Production (9:15 am), and Michigan Consumer Sentiment (10 am). The major earnings reports scheduled for the day include AQN and XPEV before the opening bell. There are no major earnings reports scheduled for after the close. Also, be aware that today is Triple-Witching Friday.

So far this morning, AQN beat on both the revenue and earnings lines. However, XPEV missed on both lines. It is also worth noting that XPEV has lowered its forward guidance. Unrelated, but also of note is that CS, FRC, PACW, and probably other banks are getting hammered by bears again early this morning. There seems to have been a rethink about whether the huge bailout loans/deposits of CS and FRC are bullish or bearish. Beware any spread of that sentiment across the other banks.

In central banks news, despite the EU raising rates 0.50% Thursday, Fed Funds Futures indicate there is an 80.5% probability of a quarter-point hike by the FOMC next week. The remaining 19.5% of probability is on “there will be no hike at all.” Interestingly, one of the reasons cited by European Central Bank President Lagarde for staying with a half percent rate hike was that the ECB feared a change in course would spook markets. As one would expect, she went on to say the European banking system is strong, there is no liquidity crisis, and there is no tradeoff between price stability (inflation) and financial stability. On the other side of the Pacific, China loosened its reserve requirement ratio (the key tool the People’s Bank of China uses to regulate monetary policy). The move reduces that requirement to 7.6%, the lowest level since 2007. So, China is easing, Europe is tightening, and the US appears to be on path to slowing its tightening.

With that background, it looks like markets are reassessing yesterday’s bullish move, despite the FRC bailout taking shape (which was just a rumor yesterday afternoon). The SPY looks to be coming back down to retest its T-line and 200sma. Meanwhile, the DIA looks to be failing or pushing down off those averages in premarket action. However, QQQ remains strong and QQQ bulls are not giving an inch this morning. Overextension is not an issue in large-cap indices. However, QQQ is a bit extended above its T-line. Another issue we have to deal with today is that today is Triple-Witching Friday. So be prepared for volatility swings as the big institutions roll positions (on top of banking sector concerns and news). And, triple witching or not, it is Friday. So, take some profit, pay yourself, and get your positions ready for the weekend news cycle and Fed meeting next week.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Banking Contagion Subsiding?

The painful overnight reversal on Wednesday on the spreading banking contagion subsided by the end of the day as Credit Suisse found another benefactor to backstop the embattled bank, sparking an end-of-day rally. However, if a relief rally can begin, we must first get past Housing, Jobless, Pilly Fed, and Import/Export economic reports before the bell. Once again, anything is possible as investors try to digest all the data to predict what the FOMC will do next week. So expect the challenging price action to persist as the bulls and bears slug it out for directional control.

Asian markets saw declines across the board as we slept with investors grappling over what comes next in the pending FOMC decision. However, European markets feel much better this morning as Credit Suisse recovers after burrowing 54 billion from Swiss National. With market-moving economic reports just around the corner, U.S. futures suggest a mixed open, but everything could quickly change after the data release. Plan for another volatile morning with significant price swings possible before the opening.

Economic Calendar

Earnings Calendar

Notable reports for Thursday include ASO, AUY, DBI, DG, COOK, FDX, GIII, MOMO, HNST, JBL, SIG, TITN & WSM.

News & Technicals’

Wall Street has been debating whether the economy is heading into a recession for months. However, the rapid market moves after the regional bank failures in the U.S. has some strategists now expecting a contraction in the economy to come sooner. Economists are also ratcheting down their growth forecasts on the assumption there will be a pullback in bank lending.

Credit Suisse will borrow up to 50 billion Swiss francs ($53.68 billion) from the Swiss National Bank under a covered loan facility and a short-term liquidity facility. The measures come after the lender’s shares saw sharp declines on Wednesday after its top investor Saudi National Bank said it could not provide further assistance.

Snap shares surged nearly 8% to $11.15, while Meta shares rose slightly over 3% to $203.49 after The Wall Street Journal reported that TikTok faces a possible ban in the U.S. if ByteDance fails to comply with the Biden Administration’s proposition. Investors believe that if TikTok were to be banned in the U.S., social media companies like Snapchat and Meta would regain users lost to the short-form video platform. However, ByteDance said, “If protecting national security is the objective, divestment doesn’t solve the problem: a change in ownership would not impose any new restrictions on data flows or access.”

Wednesday’s significant overnight reversal saw the Dow sink 700 points before whipsawing and recovering nearly 400 points by the close as worries over the spreading banking contagion subsided. While the DIA, SPY, and IWM saw a rough day, the QQQ, led by the big tech giants, traded like nothing was happening, retesting its downtrend. The T2122 suggests we are overdue for a relief rally. Perhaps with the Swiss National Bank providing a backstop for Credit Suisse, the banking fears will subside slightly, encouraging the bulls to defend recent support levels. Of course, to do that, we will need to get past the Housing, Jobless, Pilly Fed, and Import/Export reports that could encourage the bulls or the bears. Plan for another wild day ahead.

Trade Wisely,

Doug

Swiss Loan Shores Up CS but FRC In Need

On Wednesday, US markets opened significantly lower, following Europe, in the wake of news that troubled major bank CS would not get any more financial support from its largest holder (Saudi National Bank). The SPY gapped 1.5% lower, the DIA gapped down 1.64%, and QQQ gapped 0.91% lower at the open. The QQQ then rode a roller coaster sideways until 1 pm, when a strong rally started that recrossed the opening gap and took it to the highs of the day at 3 pm. Meanwhile, the two large-cap indices then meandered above and below their opening level until just before 2 pm. At that point, they followed the QQQ higher in a rally that lasted until 3 pm but never recrossed their opening gap lower. From 3 pm into the close, all three major indices chopped sideways. This action gave us gap-down, white-bodied, candles with large lower wicks and very little upper wick in the SPY, DIA, and QQQ. QQQ also closed above its T-line after a morning retest.

On the day, nine of the 10 sectors were in the red with Energy (-5.04%) leading the way lower while Utilities (+0.63%) was the only green sector. At the same time, the SPY lost 0.62%, the DIA lost 0.83%, and QQQ gained 0.52%. VXX spiked 6.39% to 54.96 and T2122 fell back deep into the oversold territory at 4.20. 10-year bond yields plummeted again to 3.47% as traders sought shelter in bonds and Oil (WTI) plunged 4.23% to $68.31 per barrel (the lowest in more than a year). So, Wednesday, saw a large gap lower on fear of bank contagion from CS in Europe. However, the bulls finally got things going in the afternoon to rally back, led by the tech-heavy QQQ. Once again, this happened on heavier-than-average volume, particularly in the SPY and DIA.

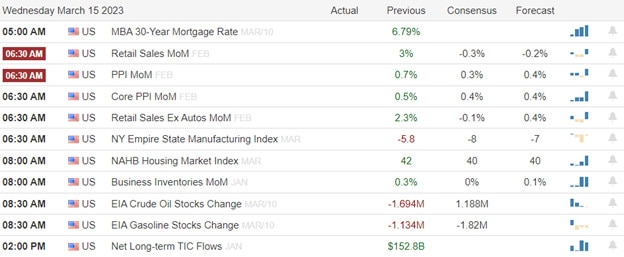

In economic news, the February PPI came in much better than expected at -0.1% (compared to a forecast of +0.3% and the January reading of +0.3%). The Feb. Core PPI number also thumped expectations a 0.0% (versus the forecast of +0.4% and even better than the January value of +0.1%). So, markets got good news in the “reasons the Fed might slow down hikes” front. However, the NY Fed Empire State Mfg. Index was a bad miss, coming in at -24.60 (compared to a forecast of -8.00 and a January reading of -5.80). February Retail Sales fared better but also missed coming in at -0.4% (versus a forecast of -0.3% and far worse than the January reading of +3.2%). Later in the morning, January Business Inventories beat estimates by coming in at -0.1% (compared to a forecast of +0.1% and a December value of +0.3%). This was the first fall in business inventories in almost two years. January Retail Inventories also beat expectations at +0.1% (versus the forecast of +0.2% and the Dec. reading of +0.2%). Finally, the EIA Weekly Crude Oil Inventories showed a build of 1.550 million barrels (versus a forecasted build of 1.188 million barrels and far worse than the previous week’s drawdown of 1.694 million barrels).

SNAP Case Study | Actual Trade

In stock news, TMUS announced it has agreed to buy budget mobile service Mint Mobile (owned by celebrity Ryan Reynolds) for $1.35 billion. Elsewhere, the FDIC has contracted with PIPR to relaunch an auction for failed lender SIVB. (Rumored bidders include RY and PNC.) Late in the day, Bloomberg reported that the Swiss government was in talks with CS on options to stabilize the bank. At the same time, the Swiss National Bank had pledged financial support for the company (the second largest Swiss bank behind UBS). At the same time, the US Senate Banking Committee said Wednesday it will hold hearings on banking sector risks which are likely to include questioning of C, JPM, BAC, WFC, USB, PNC, and perhaps some of the most volatile regional banks. However, Republicans also want answers from regulators as to why SIVB was not caught before its collapse. (However, SIVB was not subject to stress tests or other risk management rules since the 2018 regulation rollbacks.) No reintroduction of old or introduction of new regulations is expected for political reasons. Meanwhile, K announced it will change its name (of the remaining global snack unit) to “Kellanova” once its North American cereal unit is spun off. Kellanova will continue to trade under ticker K. Late in the afternoon, Reuters reported that XOM is strongly considering selling its majority stake in the Rovigo LNG terminal located offshore Italy.

In stock legal and regulatory news, the US Consumer Financial Protection Bureau has opened an investigation into data broker companies that collect and track personal data. No specific targets were mentioned, but among the largest brokers of that data are EFX, ORCL, and EXPGY (as well as several unlisted companies). Meanwhile, Medicare announced Wednesday that it will impose “inflation fines” on 27 drugs for having had their prices raised faster than the inflation rate. These include drugs from ABBV, GILD, PFE, KMDA, JNJ, and SGEN. The fines vary from $2 to $390 per dose. In the auto industry, TSLA has been hit with a class action lawsuit over the company preventing TSLA car owners from exercising “the right to repair.” In legal news BUD lost its case, in which BUD had accused STZ of violating a US distribution agreement related to selling hard seltzers. Elsewhere, the COP Willow project has been hit with a lawsuit filed by a coalition of environmental groups hoping to reverse President Biden’s recent approval of the project. (COP is not the defendant as the suit is against the Bureau of Land Management, but they are the one impacted by the suit.) After the close, a federal appeals court upheld the $5.6 billion antitrust class-action settlement against V and MC (filed on behalf of 12 million retailers).

After the close, ADBE, ZTO, and FIVE reported beats on both the revenue and the earnings line. Meanwhile, AE and TPC missed on revenue while reporting in-line on earnings (although both were losses). It is worth noting that TPC reduced its forward guidance.

Overnight, Asian markets leaned heavily to the red side, with only New Zealand (+0.70%) and India (+0.08%) managing to stay green. Meanwhile, Hong Kong (-1.72%), Shenzhen (-1.54%), and Australia (-1.46%) led the region lower. In Europe, we see the opposite picture taking shape at midday. Only Denmark (-0.53%) and Russia (-0.05%) are in the red, while the FTSE (+0.77%), DAX (+0.35%), and CAC (+0.56%) are leading the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a mixed but generally down start to the day. The DIA implies a -0.48% open, the SPY is implying a -0.38% open, and the QQQ implies a +0.09% open at this hour. At the same time, 10-year bond yields are lower again to 3.468% and Oil (WTI) is off fractionally to $67.38/barrel in early trading.

The major economic news events scheduled for Thursday include February Building Permits, Feb. Housing Starts, Feb. Export Price Index, Feb. Import Price Index, Weekly Initial Jobless Claims, and Philly Fed Mfg. Index (all at 8:30 am). The major earnings reports scheduled for the day include ASO, DG, GIII, MOMO, JBL, BEKE, LE, SIG, TITN, and WSM before the opening bell. Then after the close, FDX reports.

In economic news later this week, on Friday, Feb. Industrial Production, and Michigan Consumer Sentiment are reported. Meanwhile, in earnings later this week, on Friday, AQN and XPEV report.

So far this morning, SIG, BEKE, MOMO, OEZVY, and PLCE all reported beats on the revenue and earnings lines. Meanwhile, DG and DBI missed on the revenue line while beating on earnings. On the other side, GIII and LE both beat on revenue while missing on the earnings line. (JBL, WSM, and ASO report later in the morning.) It is worth noting that BEKE raised its forward guidance while DBI, GIII, MOMO, and PLCE lowered forward guidance.

In late-breaking bank news, CS soared overnight on more details. The Swiss bank regulators announced that CS meets all capital and liquidity requirements and the Swiss National Bank said it has loaned CS $54 billion. CS stock was up as much as 24% in the US premarket session before fading to up 5.5% after soaring 30% at the European open. Meanwhile, regional bank FRC was cut to “junk credit status” by two rating agencies (S&P and Fitch) Wednesday and overnight announced it is seeking “strategic alternatives” including the sale of the company. Elsewhere, it was announced last night that GS received $100 million for its part in trying to broker the sale of SIVB and for buying SIVB bonds as part of last-ditch efforts to save the bank. (At least one US Senator is demanding investigation and potential clawbacks since GS was on both sides of the sale of those bonds.) In other GS news, they raised their odds of a US recession to 35% based on the banking crisis.

With that background, premarkets have faded from early apparent moves higher (following Europe). Ahead of the morning data, it looks like we are in a flat, wait-and-see, mood. The most that can be said of the action this week might be that the large-cap indices are in a choppy consolidation for the last 4-5 days. Meanwhile, the QQQ is trying to pull the market a bit higher. Overextension is not an issue this morning. However, choosing a direction and getting some follow-through is an issue. Expect more volatility as the banking saga plays out with ever more shoes dropping and corresponding “all is well” signs. Be careful and either quick or slow and able to take short-term pressure in your trading.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Banking Uncertainty

Though filled with big point whipsaws the Tuesday relief rally was a welcomed sight but the banking uncertainty continues to cloud the path forward. However, hopes for further recovery are in question this morning with the indexes pointing to a full reversal of yesterday’s gains in the premarket. With potential market-moving economic data pending anything is possible so traders should plan for substantial price swings as the market reacts. The huge global bank of Credit Suisse dropping 20% and suggesting a sub two dollar open only adds to the uncertainty ahead.

During the night Asian markets rebound with modest gains despite posting as slow start for there post pandemic recovery. However, European indexes see only red this morning as they reverse the Tuesday relief rally. U.S. futures also suggest a full reversal at the open as we wait on several market moving reports that have the potential to add to the selling pain or completely reverse the open depending on the data revealed. Buckle up for another wild ride.

Economic Calendar

Economic Calendar

Notable reports for Wednesday include ADBE, ARRY, EBIX, FIVE, FNV, PTRA, PLCE, PATH & ZTO.

News & Technicals’

Diamond Sport Group, an unconsolidated and independently run subsidiary of Sinclair Broadcast Group, filed for bankruptcy protection on Tuesday. The company, which airs local NBA, NHL and MLB games across the country, said it plans to restructure its more than $8 billion debt load. Diamond said it was still finalizing the restructuring support agreement with creditors. The plan could see Diamond separate from Sinclair to become a standalone operation, Diamond said.

Democratic Sens. Elizabeth Warren and Richard Blumenthal asked the DOJ and SEC to open a probe of executives at Silicon Valley Bank. The letter came on the heels of a joint announcement by the Justice Department and the SEC about a pending investigation into the SVB failure. The inquiry will take place in separate and preliminary phases and look into stock sales that SVB executives conducted ahead of the bank’s collapse.

“The challenging adjustment to the exit from zero-COVID, for both borrowers and lenders, will weigh on banks’ asset quality and profitability over the next 12-18 months,” said Moody’s analysts in a note Wednesday. Moody’s had changed its outlook on China’s banks to “negative” from “stable” in November due to “deteriorating operating environment, asset quality and profitability.”

Tuesday’s relief rally was needed but proved challenging as it whipped in big point swings as the banking uncertainty keeps investors on edge hoping the contagion is now contained. Unfortunately, we wake this morning to see a full overnight reversal a the global bank of Credit Suisse tumbles 20% after the Saudi backer says no more assistance as outflows surge. If that were not enough we also face a big day of economic data that has the potential to move the market dramatically. Traders should prepare for substantial price swings that could easily test the wide range between support and resistance levels. The QQQ has held better than the other indexes but also indicates in the premarket a possible full reversal from yesterday’s close. If the DIA, SPY and IWM make news lows it will become difficult for the QQQ to continue to buck the trend.

Trade Wisely,

Doug

CS Fears Across Europe and US This AM

Markets gapped higher Tuesday as trader fear over regional banks faded over Monday night. The SPY opened up 1.33% higher, the DIA up 1.04% higher, and the QQQ up 1.21% higher. All three of those major indices then led a slow, steady rally until 11:30 am. From that point, we saw a slow, steady pullback until 1 pm. At 1 pm, that selloff picked up steam, reaching the lows of the day at about 3:20 pm. However, the day ended with a rally in the last 40 minutes. This action gave us gap-up, white-body candles. The QQQ had the least wick on each end and crossed back above its T-line (8ema), 50sma, and 200sma. However, the DIA printed a gap-up Doji that remained below its T-line and could be said to have failed a test of its 200sma overhead during the day. Lastly, the SPY printed a gap-up, Spinning Top candle that failed a retest of its T-line and 200sma.

On the day, all 10 sectors were in the green with Technology (+2.30%) leading the way higher while Energy (+0.40%) lagged behind the other sectors. At the same time, the SPY gained 1.65%, the DIA gained 1.07%, and QQQ gained 2.30%. VXX fell more than 5% to 51.66 and T2122 climbed but remains inside the oversold territory at 17.81. 10-year bond yields climbed to 3.691% and Oil (WTI) fell 4.4% to $71.52 per barrel. So, Tuesday saw a reversal of sentiment, particularly in the regional banks, during the premarket and then a whipsaw day. This was led by extremely volatile regional banks, which gapped very strongly higher but then got hit midday when Moody’s announced it has placed five regional banks on “review for downgrade” in terms of creditworthiness. (I don’t know how much to put into this, but Bloomberg reported that more than 100 top executives of regional banks bought shares of their own company Tuesday.) Once again, this happened on heavier-than-average volume, particularly in the SPY.

In economic news, interestingly, the February CPI numbers were a non-event for the market. The year-over-year number came in at 6% which was exactly as expected (and much better than the January surprise 6.4%). Meanwhile, the month-on-month number came in at 0.4% (again exactly as forecast but 0.1% better than the 0.5% reading last month). At the same time, the February Core CPI reading was right on forecast year-over-year (and had fallen a tenth of a percent from January) while the month-over-month reading came in 0.1% high at 0.5% (versus a forecast and previous reading of 0.4%). The bottom line is that this indicated that inflation is coming down but remains far above the Fed’s 2% target. After hours, the API Weekly Crude Oil Stocks report was released. The report said that US crude inventories rose 1.155 million barrels last week. However, the report also saw sharp weekly declines in gasoline and distillates (diesel and heating oil) inventories.

SNAP Case Study | Actual Trade

In stock news, NKE announced it will stop using kangaroo skin for shoes later this year. This move comes weeks after German rival Puma made the same move. In aerospace news, BA said its plane deliveries fell to 28 in February (down from 38 in January). The company cites supply chain problems. Over in the semiconductor space, Reuters reported that INFN (chips for telecom) is exploring strategic options including the sale of the company. Elsewhere, RCAT announced it has made an unspecified “significant” investment in Firestorm (an American company that is developing a completely modular 3D-printed UAV. Meanwhile, AMC investors approved issuing more shares and implementing a 1-for-10 reverse split while also converting APE shares into AMC common stock. The move will allow AMC to raise money while diluting the position of existing AMC holders. APE shares jumped 22% on the news while AMC fell 12%. In Cupertino, AAPL stalled bonuses and promotions (and said they will reduce the frequency of future bonuses) while also expanding the company hiring freeze. In other big tech news, META said on Tuesday that it will cut 10,000 jobs sometime this year. This follows the company’s first round of layoffs last fall where 11,000 jobs (13% of the workforce) were eliminated. In food news, TSN said after the close Tuesday that it will be closing two chicken processing plants in the US on May 12, resulting in the termination of 1,700 employees. At the same time, DLTR announced it is at least temporarily stopped selling eggs amidst skyrocketing egg prices from last year. The company says it hopes to bring back eggs in the fall.

In stock legal and regulatory news, a CA judge ruled that a California Civil Rights Agency must provide details of its investigation that resulted in the agency suing TSLA over “widespread race discrimination” at its main assembly plant. (TSLA is claiming the agency did not investigate the discrimination cases before suing the company.) In medical news, the FDA said data from PFE’s oral COVID-19 drug trials support its use in adults with a high risk of progressing to severe disease. This brings the drug (pill) closer to approval. At the same time, NVO said it will follow the lead of LLY and slash the list price for its insulin by up to 75%, bowing to pressure from President Biden and the 2022 Inflation Reduction Act (which capped Medicare recipients insulin price at $35 per month). In the tech space, EBAY asked a US judge to block META’s bid to get an EBAY executive to testify as part of its defense of an FTC antitrust lawsuit. EBAY claimed the META subpoena would allow META (whose marketplace is a competitor to EBAY) to get proprietary information. Elsewhere, the US Surface Transportation Board is set to announce its decision on whether to approve or reject the CP $31 billion bid to acquire KSU today. In other railroad news, the state of Ohio sued NSC on Tuesday over the February 3 derailment that released over one million gallons of hazardous materials into the environment around East Palestine OH. No dollar amount is yet listed, but the suit seeks compensation for the cleanup as well as the death of tens of thousands of animals and fish.

In energy news, oil fell to a three-month low on Tuesday, purportedly on worries that inflation will cause the Fed to increase rates higher than expected. This is a bit odd since the stock market seems to have had a completely different read on the CPI data. Elsewhere, the US Senate reintroduced a bill at the urging of the American Petroleum Institute (big oil) that would allow the nationwide sale, year-round, of a higher percentage blend of ethanol. The bipartisan bill would allow a 15% blend (10% is the current maximum) and would increase US corn demand and perhaps food input prices at the margin. The stated purposes of the bill are reducing fuel costs and dependence on foreign oil. For what it is worth, it should be noted that this bill is opposed by many environmental groups (ethanol causes more smog than gasoline) and the US is an oil exporter, not an importer (3.6 million barrels per day exported). However, there is broad backing from midwestern (corn-producing) states and the oil industry. Finally, after the close, the US Interior Dept. withdrew a land exchange deal that had been approved by the Trump administration. The deal would have allowed a road to be built through a national wildlife refuge to allow oil companies to more easily reach the North Slope drilling facilities.

After the close, GES, LEN, and CTOS all reported beats on the revenue and earnings lines. Meanwhile, STNE missed on revenue while beating on earnings. It is worth noting that GES lowered its forward guidance. (LEN specifically cited high property prices as having helped offset supply problems during the quarter.)

Overnight, Asian markets leaned heavily to the green side. Thailand (+2.70%), Hong Kong (+1.52%), and Singapore (+1.38%) led the region higher while India (-0.42%) was the only appreciable red in the area. Meanwhile, in Europe, at midday, we see deep red across the board after the top holder of CS ruled out investing more in the company. The FTSE (-2.32%), DAX (-2.81%), and CAC (-3.42%) are leading the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a big move lower to start the day. The DIA implies a -1.54% open, the SPY is implying a -1.55% open, and the QQQ implies a -1.38% open at this hour. At the same time, 10-year bond yields are plunging to 3.526% and Oil (WTI) is down another 1.78% to $70.09/barrel in early trading.

The major economic news events scheduled for Wednesday include February PPI, Feb. Retail Sales, and NY Empire State Mfg. Index (all at 8:30 am), Jan. Business Inventories and Jan. Retail Inventories (both at 10 am), and EIA Weekly Crude Oil Inventories (10:30 am). The major earnings reports scheduled for the day include ARCO and CLMT before the opening bell. Then after the close, ADBE, FIVE, HSAI, YY, TPC, and ZTO report.

In economic news later this week, on Thursday, we get Feb. Building Permits, Feb. Housing Starts, Feb. Export Price Index, Feb. Import Price Index, Weekly Initial Jobless Claims, and Philly Fed Mfg. Index. Finally, on Friday, Feb. Industrial Production, and Michigan Consumer Sentiment are reported.

In earnings later this week, on Thursday, we hear from ASO, DG, GIII, MOMO, JBL, BEKE, LE, SIG, TITN, WSM, and FDX. Finally, Friday, AQN and XPEV report.

So far this morning, ARCO reported beats on both the revenue and earnings lines. Meanwhile, CLMT beat on revenue while missing on earnings. On the other side, EONGY missed on revenue while coming in in-line on earnings.

In late-breaking news, the Saudi National Bank, the largest holder of CS, ruled out providing any more assistance to the troubled Swiss bank. This caused CS shares to plummet 24% before rebounding slightly and led to a spread of fear throughout Europe similar to what US markets suffered under the SIVB collapse last Friday. Elsewhere, US mortgage demand rose 6.5% for the week (a 7% increase for home purchase loan applications and a 5% increase in refinance applications). This came after rates plummeted on the SIVB news and came despite extremely volatile US interest rates. Meanwhile, it was announced the federal prosecutors were investigating SBNY over their business with crypto clients prior to the bank being shut down. However, NY state banking regulators said the closure had nothing to do with crypto.