SIVB Dominates Market Mindshare

Markets started out basically flat on Friday (down 0.15% on the SPY, down 0.18% in the DIA, and up 0.11% in the QQQ). All three major indices then meandered sideways in the morning, with an up wave reaching the highs of the day at about 11:30 am. At that point, the SPY, DIA, and QQQ all sold off strongly until 2 pm. The rest of the day was spent in a relief bounce and then heading back down to the lows of the day at 3:50 pm before ending on a modest 10-minute bounce. This action gave us larger-bodied, black candles with wicks on both ends. The QQQ (which has been the leader for some time) took out its most recent swing-low (completing a Dreaded-h pattern) as well as breaking down through and closing just below both its converging 50sma (rising) and 200sma (falling). At the same time, the SPY closed at a potential support level.

On the day, all 10 sectors were in the red with Financial Services (-2.75%) once again leading the way lower while Communications Services (-0.32%) held up best. At the same time, the SPY lost 1.44%, the DIA lost 1.04%, and QQQ lost 1.40%. The VXX spiked more than 11.4% to 52.93 and T2122 dropped even more deeply into the oversold territory at 2.08. 10-year bond yields plummeted to 3.704% (a massive 0.219% move for bond yields) and Oil (WTI) climbed 1.27% to $76.68 per barrel. So, Friday saw the bears react to February Payrolls by anticipating that the Fed will not like stronger-than-expected jobs growth and will hike rates more than traders had already baked in. This all happened on huge volume (at least in terms of recent months), the highest in the last four months…which begs the question as to whether this was capitulation?

In economic news, February Nonfarm Payrolls came in above expectation at +311k (compared to a forecast of +205k but well below the blowout January reading of +504k). At the same time, Feb. Private Nonfarm Payrolls also beat expectations at +265k (versus the forecast of +210k and again, below the blowout January number of +386k). Meanwhile, the February Participation Rate crept up to 62.5% (up from 62.4% in January). However, the February Unemployment Rate unexpectedly rose to 3.6% (above the forecasted 3.4% and the January value of 3.4%). On top of all this, the February Average Hourly Earnings (year-on-year) increased less than expected at +4.6% (as compared to the forecast of +4.7% but still well above the January reading of +4.4%). So, overall, the bulls could hang their hat on the increase in payrolls showing good growth while also decreasing in pace as the Fed wants at the same time the wage growth is easing slightly. However, the bears could see still much stronger job growth than anticipated and wage growth still far above the Fed’s target rate. Finally, at 2 pm, the February Federal Budget Balance showed a larger deficit than was expected at -$262.0 billion (versus a forecast of -$256.0 billion).

SNAP Case Study | Actual Trade

In stock news, after widespread rumors, FRC and WAL both calmed markets Friday saying their liquidity and deposits remain strong and neither expects spill-over effects from the SIVB implosion. Elsewhere, MRNA said Friday that it is planning to hire 2,000 employees by the end of 2023 as well as setting up new West Coast offices as it plans to scale up RNA vaccine research. (For comparison, MRNA had 3,900 employees at the end of 2022.) Meanwhile, Reuters reported that GM is exploring the use of ChatGPT in a collaboration with MSFT. In M&A news, a majority of RBA shareholders have voted in favor of the company buying IAA for about $7 billion (cash and stock). At the same time, AAPL shareholders rejected two proposals from politically conservative groups related to diversity and business done with China. In other news, seeking some good press (and/or avoiding negative) NSF agreed to give members of two unions up to seven paid sick days per year. In addition, F announced they will resume the production of F-150 Lightning trucks today after solving battery cell manufacturing defects. Finally, a rash of companies (especially silicon valley startups) are being forced to address how much of their assets are now tied up (and potentially lost) due to the failure of SIVB. Among these are RBLX (who said 5% of its cash is tied up at SIVB) and ROKU (who said 26% of its cash is tied up at that bank). It is worth noting that the FDIC only insures $250k in deposits. However, capitalism never misses an opportunity as, on Saturday, several hedge funds began offering to buy the deposits of companies with stranded capital at a price of 60 cents on the dollar or less.

In stock legal and regulatory news, on Friday, SIVB was halted before the opening bell by the SEC and the bank itself was shut down by State of CA regulators who turned it over to the FDIC after the company failed to raise enough capital in its last-ditch stock offering Thursday. Elsewhere, Reuters reported an exclusive on Friday saying that the OCC (Options Clearing Corporation, the largest options clearing house) and the FIA (Futures Industry Assn.) have begun investigating the risk of 0DTE (Zero Days to Expiration) options contracts in a project that began on March 1. This comes after analysts at JPM publicly said they fear 0DTE options could supercharge volatility, turning a 5% intraday loss into a 25% or greater rout. (0DTE volume on the S&P500 have tripled since January.) The leaning seems to be toward continuing to allow 0DTE options, but industry members are nervous (or perhaps are not making as much or in as much control of that new market yet). Meanwhile, after the close Friday, the FAA approved BA restarting the deliveries of 787 Dreamliners following the company resubmitting previous erroneous data analysis.

In bank fear news, the shocking speed behind the collapse of SIVB (the 16th largest US bank) has made many think back on how quickly Lehman Brothers and Bear Sterns went under. Speaking of speed, on Sunday, the FDIC completed the auction for buyers of SIVB assets after being unable to find a bank to acquire the entirety of SIVB. Sunday morning, Treas. Sec. Yellen told CBS reporters that the government will not bail out SIVB, but is already working with its depositors on ways to secure their uninsured funds beyond what the FDIC insures. Later that same day, Sec. Yellen ordered the FDIC to allow SIVB depositors to have access to all their money Monday. (So, the FDIC has been ordered to bail out the depositors, if not the bank, by increasing the amount of deposits covered.) Meanwhile, CNN reports that other US banks are now sitting on more than $620 billion in unrealized losses. Since the banking system is all built on confidence, any fear of bank runs could cause a vicious cycle of fear causing runs and runs causing more fear. By Sunday night, the Treasury Dept., Fed, and FDIC made a joint decision to close SBNY due to this systemic risk. However, Reuters reported that several sources told them there will be some major government action (involving the Fed, Treasury Dept., and FDIC) to shore up the system. Most likely, this will be announced before the open today.

Overnight, Asian markets were mixed. Hong Kong (+1.95%), Shanghai (+1.20%), and South Korea (+0.67%) led the gainers. Meanwhile, Thailand (-1.66%), India (-1.49%), and Singapore (-1.42%) paced the losers. In Europe, with the lone exception of Russia (+0.26%), the regions are in the red across the board at midday. The FTSE (-1.69%), DAX (-2.10%), and CAC (-1.92%) are leading the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing to a mixed but green open. The DIA implies a flat +0.05% open, the SPY is implying a +0.36% open, and the QQQ implies a +0.89% open at this hour. At the same time, 10-year bond yields are plummeting again (as traders seek safe havens) to 3.549% and Oil (WTI) is down 1.54% to $75.50/barrel in early trading.

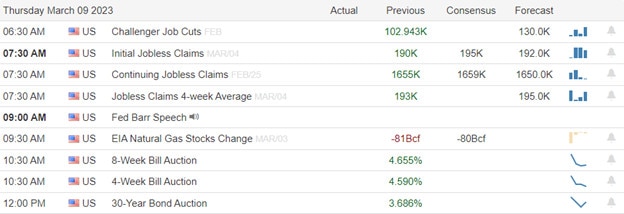

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for the day are limited to LU and ZIM before the opening bell. There are no reports scheduled for after the close.

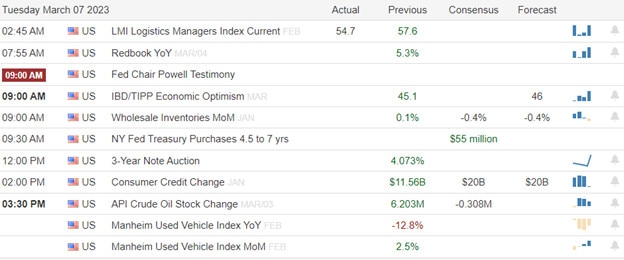

In economic news later this week, on Tuesday, we get February CPI, API Weekly Crude Oil Stocks, and hear from Fed member Bowman. Then Wednesday, February PPI. Feb. Retail Sales, NY Empire State Mfg. Index, Jan. Business Inventories, Jan. Retail Inventories, and EIA Weekly Crude Oil Inventories are reported. On Thursday, we get Feb. Building Permits, Feb. Housing Starts, Feb. Export Price Index, Feb. Import Price Index, Weekly Initial Jobless Claims, and Philly Fed Mfg. Index. Finally, on Friday, Feb. Industrial Production, and Michigan Consumer Sentiment are reported.

In earnings later this week, on Tuesday, we hear from CAL, IHS, GES, LEN, and STNE. Then Wednesday, ARCO, CLMT, ADBE, FIVE, HSAI, YY, TPC, and ZTO report. On Thursday, we hear from ASO, DG, GIII, MOMO, JBL, BEKE, LE, SIG, TITN, WSM, and FDX. Finally, Friday, AQN and XPEV report.

So far this morning, ZIM reported beats on both the revenue and earnings lines. At the same time, LU missed on revenue and reported in-line with analyst expectations on the earnings line. Neither company has changed guidance as of this point.

In late-breaking news, HSBC bought the entirety of SIVB’s UK operations for the princely sum of $1.21 (1 pound sterling). So, UK customers of SIVB will continue life as normal while HSBC absorbs SIVB in that country. Elsewhere, GS has changed its call for the Fed next week. GS now expects no rate hike (pause), down from its earlier call of a quarter-percent hike this time around. Obviously, the reason for the change is an expectation the Fed will not want to change liquidity or make any more changes until the SIVB shock works its way out of the financial system. Traders have also shifted their bets with Fed Fund futures now showing a 66% probability of a quarter percent hike and a 34% of no hike at all.

With that background, it looks like futures are pulling back in the last 15-20 minutes. We are now looking at more of a flat (large-cap indices) to modestly up (QQQ) open to the day. Extention is not a problem in terms of the T-line (8ema). However, the T2122 indicator is very stretched. As I see it, SPY has no real support below til it reaches the 378-379 area. Meanwhile, the DIA has very, very modest support right here and then none until it reaches the 311 area. As for QQQ, I see no support until it reaches the 284 area. Expect volatility today. There will likely be unscheduled news and soothing words from the FDIC, Fed, Treasury Sec. Yellen, and maybe the President. However, it is hard to say whether the market will take those as a good thing or a reason to panic.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service