Indexes closed mostly higher on Monday with a surge in the last minutes of the day climbing a wall of worry with key inflation data just ahead and big bank earnings looming on Friday. Volume was low with prices spending most of the day in a small chop zone with the tech giants enjoying the majority of the buyer’s attention. Today we will hear from several Fed speakers with little else to as we wait on the CPI data before the bell on Wednesday. Plan for another day of hurry-up and wait while keeping an eye out for whipsaws.

Asian markets mostly rallied during the night with the Bank of Korea holding rates steady. European markets see nothing but green this morning as they resume their holiday break with mining stocks leading the way. U.S. futures suggest a modestly bullish open with Fed speakers ahead and waiting on market-moving inflation data and the kick-off of earnings season.

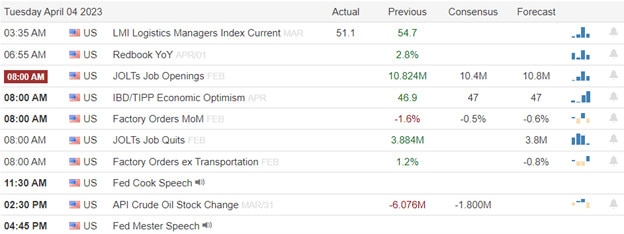

Economic Calendar

Earnings Calendar

We have a very light day as we build up to the big bank reports on Friday. Notable reports for Tuesday include ACI and KMX.

News & Technicals’

Warren Buffett recently told Nikkei that he is considering additional investment in Japan’s five major trading houses. Berkshire Hathaway has raised its stakes in all five trading houses to 7.4%. As a result, shares of Mitsubishi Corp. rose 2.1% in Japan’s afternoon trade, Mitsui & Co. gained 2.7%, and Itochu Corp climbed 3%. It seems that investors are optimistic about the future of these companies and their growth potential.

On Tuesday, Chinese regulators released draft rules designed to manage how companies develop generative artificial intelligence products like ChatGPT. The Cyberspace Administration of China’s draft measures lay out the ground rules that generative AI services have to follow, including the type of content these products are allowed to generate. For example, the content generated by AI needs to reflect the core values of socialism and should not subvert state power, according to the draft rules. It seems that China is taking steps to regulate AI development and ensure that it aligns with the country’s values and goals.

Yesterday, the stock market opened lower but then spent most of the day moving up and down around the same level climbing the wall of worry. The S&P 500 index ended up 0.1% higher and the Dow Jones Industrial Average increased by 100 points. It was a quiet start to the week as investors waited for this week’s inflation report. Short-term interest rates were slightly higher, which means that people expect the Federal Reserve to keep raising interest rates. Long-term interest rates didn’t change much because people are still unsure about how well the economy will do in the future. Plan for more of the same today as we hear from Fed members ahead of the CPI report Wednesday morning. There is little else no the earnings and economic calendars to inspire today so plan for another day of low-volume price action.

Markets gapped lower on Monday, in a divergent manner. The SPY opened down 0.62%, DIA gapped down 0.29%, and QQQ gapped down 0.90%. However, after that open, the bulls stepped in to lead a long, slow, rally that steadily took us higher until 3 pm. At that point, we saw a sideways grind in a very tight range for the last hour in all three major indices. This action gave us a white-bodied candle that bounced up off the T-line (8ema) in the SPY. DIA also printed a white-bodied candle with tiny wicks on each end. Meanwhile, the QQQ printed a white-bodied candle that started below the T-line, had a larger lower wick, and closed back above the 8ema on an overall inside day candle. With that said, you can definitely see that the DIA (and perhaps the other major indices) are in a Bull Flag pattern.

On the day, eight of the 10 sectors were in the green with the Industrials (+01.13%) leading the way higher while Healthcare (-0.07%) lagged and was the only sector more than a few ticks into the red. At the same time, the SPY gained 0.10%, DIA gained 0.32%, and QQQ lost 0.06%. VXX fell almost 1% to 43.06 and T2122 climbed back into the overbought territory at 87.79. 10-year bond yields climbed strongly all day to close at 3.421% while Oil (WTI) was down more than a percent to $79.80 per barrel. So, on Monday we saw a significant gap lower, met by all-day buying in what turned out to be a bear trap. All of this happened on well less-than-average volume in all three major indices.

In stock news, AMC reported all-time high US Easter weekend revenue, saying that 3.6 million people bought movie tickets over the three days. Meanwhile, Chinese (and Warren Buffett-backed) electric car maker BYD launched a new suspension system in an effort to take the brand upscale. The system will be similar to the Porsche and Mercedes Benz luxury ride control features. In M&A news, TECK again rejected the unsolicited $22.5 billion bid from GLNCY, telling its shareholders the offer was an illusion and management’s restructuring plan is the only viable option. However, PXD shares rose on reports that XOM has held preliminary talks about buying the company. (PXD is the third-largest Permian Basin oil producer after CVX and COP). Elsewhere, workers at a TSN poultry plant went on strike demanding better working conditions. (Since TSN announced it will close that plant in May, many employees have left, which leaves the remaining employees in tougher conditions and long hours.) Finally, it was reported Monday that global personal computer sales plunged in Q1. AAPL took the biggest hit with the sale of Macs dropping more than 40% during the quarter. This was far worse than the next-worst-hit Dell whose sales fell 31% in the first three months of 2023.

In stock legal and regulatory news, it didn’t take long for TSLA to be hit with a class-action lawsuit after reports surfaced at the end of last week that TSLA employees were sharing images and video recorded by TSLA cars from 2019 to 2022. No dollar amount has yet been assigned to the case. Elsewhere, BIDU sued AAPL (as well as relevant app developers) over fake copies of BIDU’s AI “Ernie bot” being sold through the AAPL App Store. Meanwhile, the US CFTC announced GS has agreed to pay $15 million to the US Commodity Futures Trading Commission over charges GS had failed to make proper disclosures and communicate fairly with swap customers. At the same time, the FTC opened a new front in its fight to stop ICE from buying BKI. This time the FTC has asked a federal court for a preliminary injunction to halt the deal while its internal administrative process moves forward. (ICE and BKI had planned to proceed with the deal after an April 28 vote, despite the FTC opposing it.)

In miscellaneous news, Reuters reports that solar panel installers like SPWR and RUN are bracing for an expected steep drop-off in demand in CA. The state has new solar reimbursement rules taking effect this week (April 15) which will reduce the electric reimbursement rates significantly. Meanwhile, in banking news, Bloomberg reported Monday that there are signs that the banking system issue is easing. Specifically, in the last week of March, the Federal Home Loan Bank system (known as the “lender of next-to-last resort”) had a sharp decline in home loans it issued. For that week, FHLB loaned $37 billion, a sharp decline from the record $304 billion it had loaned just two weeks earlier. This signals that the member banks had less of a need for liquidity. The report also noted that FHLBs had issued far fewer bonds that week, just $19.8 billion, well down from the $151 billion issued the week SIVB was put into receivership. Both of these are signs that loan-originating banks are not as strapped for cash and fell they have the liquidity to underwrite loans on their own.

Despite the improved bank liquidity situation reported above, the NY Fed came out with a lagging report from March on Monday. The survey found that more than 58% of those responding reported that it is harder to get credit than it was in March 2022. That level was the highest on record but it is critical to remember this survey has only existed since mid-2013. (So, less than 10 years.) The less useful part of the survey found that 53% of those responding expect credit to be even harder to get a year from now and expressed a possibility that they may miss a debt payment within the next three months.

Overnight, Asian markets were nearly green across the board. Only Shanghai (-0.05%) was in the red while South Korea (+1.42%), Australia (+1.26%), and Japan (+1.05%) led the rest of the region higher. In Europe, we see the same picture taking place at midday with no red on the board at all. The CAC (+0.86%), DAX (+0.49%), and FTSE (+0.26%) are typical and leading the region higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward another mixed and nearly flat start to the day. The DIA implies a +0.12% open, the SPY is implying a +0.09% open, and the QQQ implies a -0.10% open at this hour. Meanwhile, 10-year bond yields a down a bit to 3.402% and Oil (WTI) is just on the red side of flat at $79.67/barrel in early trading.

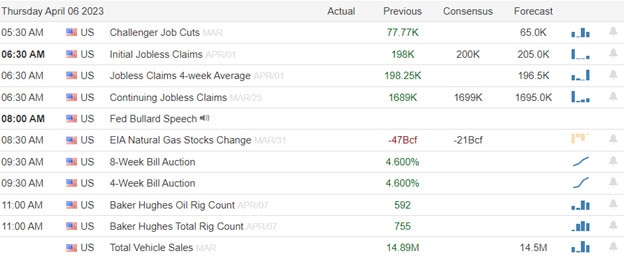

The major economic news events scheduled for Tuesday are limited to the WASDE Ag Report (noon) and API Crude Oil Stocks Report (4:30 pm). However, we do hear from two Fed more members (Harker at 4 pm and Kashkari at 7:30 pm). Major earnings reports scheduled for the day are limited to ACI and KMX before the open. Again, there are no earnings reports scheduled after the close.

In economic news later this week, on Wednesday, March CPI, EIA Crude Oil Inventories, March Federal Budget Balance, and the FOMC Meeting Minutes are released. On Thursday, March PPI and Weekly Initial Jobless Claims are reported. Finally, on Friday, March Retail Sales, March Import/Export Price Indexes, March Industrial Production, Feb. Business Inventories, Michigan Consumer Sentiment. Feb, and Retail Inventories are reported.

In terms of earnings reports later this week, on Wednesday, there are no major reports. Thursday, we hear from, DAL, FAST, INFY, and PGR. Finally, on Friday, BLK, C, JPM, PNC, UNH, and WFC report.

In mixed-bag news, Warren Buffett told Nikkei that he has raised his holdings of Japanese company stocks by almost 50% since 2020 (up 2.4% from 5% of his overall portfolio). Buffett also said he is looking to increase his exposure to Japan, although no specific target companies were named. Meanwhile, Bloomberg reports that in Switzerland, lawmakers are beginning to scrutinize the government’s move that agreed to provide up to $120 billion in taxpayer money to support the UBS takeover of CS. (Swiss lawmakers really can’t do anything to stop the deal at this point. However, they expect to make political hay and apparently hope to revamp the country’s “too big to fail” rules.)

So far this morning, KMX missed on revenue while absolutely blowing away the earnings line (a 100% upside surprise on earnings). ACI (KR acquisition target pending regulatory approval) reports at 8:30 am.

With that background, at least in the premarket, it looks like the consolidation continues in the major indices. Perhaps traders are waiting on CPI data or need to hear from the big banks as earnings season starts again on Friday. The SPY, DIA, and QQQ all sit just below their rising 3ema and just above their rising T-line (8ema), thus indicating that the short-term bullish trend remains in play. In turn, those 8emas are all sitting above a rising 17ema, which indicates a longer-term bullish trend. Longer-term, all three of the 34emas are rising and the 50sma of the SPY and QQQ are sloping upward as well. Only the DIA has a falling 50sma. So, putting fear and prediction aside, the chart is telling us it is bullish. It is also not over-extended in terms of the T-line. However, the T2122 indicator is back in the overbought territory. Make of that what you will. Personally, I’ve never been good enough to pick a top or bottom. So, all I can do is trade with the trend and cautiously watch for breaks of the trendline. That’s what I’ll do here too.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Traders and investors alike are in for a busy week with key inflation data, FOMC minutes, retail sales, and the big bank earnings that officially begin the 2nd quarter silly season. The index charts remain challenged by overhead resistance levels but the bulls keep knocking on the door despite the low volume and uncertainty that lies ahead. Emotions will likely be very high this week so plan for possible big point moves, whipsaws, and overnight reversals as the market tries to guess the path forward amid all the market-moving data.

Asian markets begin the week mixed with modest gains and losses across the indexes as investors ponder slowing economies. However, European markets trade higher this morning trying to build off the bullishness that closed the indexes higher last Thursday. U.S. futures on the other hand seem less certain trading modestly and mixed as they ponder pending inflation data and the earnings season beginning on Friday as jobs data indicate the economy is slowing.

Economic Calendar

Earnings Calendar

We start the week light and ramp up the official 2nd quarter earnings kick-off on Friday with big bank reports. Notable reports for Monday include GBX, PSMT & TLRY.

News & Technicals’

According to the Labor Department’s report, nonfarm payrolls grew by 236,000 in March which is about in line with the Dow Jones estimate of 238,000. The unemployment rate fell to 3.5% from the previous month’s 3.6%. The March jobs report showed a resilient economy and moderate inflation which pushed stock futures and Treasury yields higher. However, the New York Stock Exchange was closed for Good Friday. “As such, the odds of another quarter-point rate hike in May should go higher as the data does not appear to justify a Fed pause,” he added.

Last week’s data hinted at a slowdown in job growth which caused U.S. government debt prices to be higher on Monday. The yield on the benchmark 10-year Treasury note slipped to 3.363% while the yield on the 30-year Treasury bond dipped to 3.581%. The 2-year note yield fell 4 basis points to 3.931%. Remember that prices move inversely to yields.

The U.S. Defense Department is launching an interagency investigation into the source and the damage potential of a trove of classified documents that were leaked onto social media over the past few days. According to reports, the documents contained sensitive information on not just Ukraine but also China, the Middle East, and Africa. They also revealed the rate of expenditure of Ukraine’s S-300 air defense systems and a timeline suggesting when they would be depleted – and that they are running dangerously low.

Investors are in for a busy week of economic data. The latest consumer price index and producer price index data are due out Wednesday and Thursday, respectively. These will be key in determining if or when the Fed will pause or put an end to its rate-hiking campaign. The first batch of companies reporting first-quarter financial results will also be released this week. Tilray Brands kicks things off on Monday. The major banks – JPMorgan Chase, Wells Fargo, and Citigroup – will report on Friday. Plan for just about anything this week with so much uncertainty intraday whipsaws and big point overnight reversal is certainly possible.

Thursday saw a small gap lower at the open (down 0.17% in the SPY, down 0.09% in the DIA, and down 0.53% in the QQQ). After that open, all three major indices ground sideways to get their bearings for the first 30 minutes of the day. However, starting at 10 am in the SPY and QQQ as well as 11 am in the DIA, the bulls led a long, slow rally that lasted until 2:30 pm. From that point, the QQQ and SPY ground sideways in a fairly tight range. At the same time, DIA did a slow, shallow pullback. This action gave us a white Bullish Engulfing candle (that bounced up off its T-line) in the SPY, a white-bodied Spinning Top in the DIA, and a Bull Engulfing candle that crossed back up through its T-line in the QQQ.

On the day, seven of the 10 sectors were in the green with the Healthcare (+0.75%) group leading the way higher while Energy (-1.23%) lagged the other sectors. At the same time, the SPY gained 0.39%, DIA gained 0.02%, and QQQ lost 0.67%. VXX lost 1.76% to 43.48 and T2122 climbed but remains in the mid-range at 63.69. 10-year bond yields fell slightly again to 3.305% while Oil (WTI) was flat at $80.54 per barrel. So, on virtual Friday we saw a sideways to very modestly bullish session. All of this happened on well less-than-average volume in all three major indices.

In economic news Thursday, the Weekly Initial Jobless Claims came in much higher than expected at 228k (compared to a forecast of 200k but still far below the prior week’s 246k reading). Then on Friday, March Nonfarm Payrolls increased slightly less than was expected at +236K (compared to a forecast of +239k and far lower than the February reading of +326k). At the same time, March Private Nonfarm Payrolls increased far less than expected at +189k (versus the forecast of +215k and the February value of +266k). Meanwhile, the March Participation Rate came in a bit above expectation at 62.6% (compared to the forecast and previous reading of 62.5%). This all resulted in a better-than-expected March Unemployment Rate of 3.5% (versus the forecast and February value of 3.6%). (Of potential note, Black Unemployment fell to 5%, which is the lowest absolute level since 1972 and the narrowest gap to overall unemployment in over 50 years.) Finally, March Average Hourly Earnings also increased less than expected at +4.2% annualized (compared to a forecast of +4.3% and growing much slower than the Feb. increase of +4.6%). The bottom line is that the March Payrolls data came in about as well as the Fed could have hoped. Participation is up, but job increases are slowing and wage increases are slowing (without either falling off a cliff). This seems in line with the Fed’s stated path of one more quarter-point rate hike and then stable rates for the rest of the year. This should be good news for bulls and was followed by an increase in bond yields and the US dollar (which tend to indicate a move to a “risk on” stance).

In stock news Thursday, Reuters reported that between 2019 and 2022, TSLA employees shared private videos and images recorded by the cameras located in customer cars. (Many of these videos and images were reportedly highly invasive, showing customers in embarrassing situations and even naked.) TSLA responded by saying that customer car camera recordings remain anonymous. However, Reuters reported that several former employees said TSLA internal computer programs can and do routinely identify the locations and owners of the cars doing the recording. In other TSLA news, the company cut prices again over the weekend (this time by an average of 6%). This is TSLA’s fifth price cut in 2023. Elsewhere, WMT announced it has plans to launch a network of electric vehicle charging stations at many US stores by 2030. This will be in addition to 1,300 charging stations previously announced as part of the WMT partnership with VLKPY (Volkswagen). Meanwhile, Bloomberg reports that BA plans to increase the output of 737 jets to 38 per month by the middle of the year. (BA currently produces 31 of the 737 planes each month.) At the same time, HMC announced a recall of 563,000 CRV sport utility vehicles from 2007-2011 model years because rust may cause the frame to detach. In rumor news, the Wall Street Journal reported that NGG and D both are separately seeking to sell parts of their own natural gas pipeline networks, which combined could be worth $13 billion. Finally, in black eye news, Reuters reported that LUV CEO Jordan received a 75% compensation increase (mostly from bonus) even though he promised to cut executive bonuses after the 17,000 flight cancellations around Christmas and despite LUV stock falling more than 66% in the year preceding the raise.

In stock legal and regulatory news, the EPA proposed new rules on Thursday that would cause sweeping cuts in vehicle emissions. The rules will take effect starting in the 2027 model year with the last of the rules phased in by the 2032 model year. Later, HOOD agreed to pay $10.2 million in penalties to several individual states for platform outages in March 2020 as well as for deficient account review and approval processes prior to 2021. Meanwhile, a day after CMG sued SG for trademark infringement, SG has renamed its newest menu item (formerly known as the “Chipotle Chicken Burrito Bowl”). Elsewhere, the Treasury Dept. and MSFT reached a settlement over the tech firm’s violations of sanctions and export controls. MSFT agreed to pay a $3 million to settle 1,300 apparent sanction violations involving Cuba, Iran, Syria, and Russia. (The fine was so small because Treasury said the violations were not egregious and were self-reported.) At the same time, the US GAO denied LMT’s protest of the Army awarding a $7.1 billion helicopter contract (for a Blackhawk replacement) to TXT. On Friday, the Financial Times reported that the US Office of the Comptroller of Currency (Treasury Dept.) has scheduled an audit of JPM related to the company’s potential lack of “due diligence” performed as part of the bank’s acquisition of dozens of smaller companies in 2021 and 2022. This comes after the US Dept. of Justice filed fraud charges against the founder of financial aid company Frank for having defrauded JPM to the tune of $175 million. Finally, CNBC reported Friday that the Dept. of Labor (OSHA) has again found DG guilty of more than 180 serious workplace violations, including the blocking of fire exits. However, federal law only allowed OSHA to fine DG $245,544.

In money flow news, Fed data released Friday showed that bank deposit outflows have stabilized. Deposits at banks not among the 25 US largest banks were down just $1.1 billion the week ending March 22. That said, smaller bank deposits are still down $216 billion from their peak in December of 2022. Over the same period, deposits at the top 25 banks are down $96.2 billion. (Large bank deposits have fallen $519 billion from the high, which was $11.2 trillion dollars in February 2022.) A different way to look at this situation is that about $350 billion in new money poured into Money Market funds in the four weeks ending April 5. That took Money Market funds to a record total of $5.25 trillion. Over that same time, SPY is up 6%, DIA is up 4.77%, and QQQ is up 10.2%. So, money is flowing out of bank deposits and apparently into both stocks and money market funds at a significant clip. Big bank earnings reports starting at the end of this week may also give us better insight.

Overnight, Asian markets were mixed but leaned toward the green side. Shenzhen (-0.80%) was by far the biggest loser on the day. Meanwhile, Thailand (+1.02%) was the biggest winner in the region, followed by South Korea (+0.87%) and Japan (+0.42%). In Europe, the bourses are closed for holiday on Monday. In the US, as od 7:30 am, Futures are pointing toward another mixed, flat open. The DIA implies a +0.08% open, the SPY is implying a -0.07% open, and the QQQ implies a -0.36% open at this hour. At the same time, 10-year bond yields are up from Thursday’s close to 3.368% and Oil (WTI) also up very slightly to $80.69/barrel. (For its part, Natural Gas is making a strong move, desperately trying to hang on to the $2 level after a year-long decline.)

The only major economic news events scheduled for Monday is a speech from Fed member Williams (4:15 pm). The major earnings reports scheduled for the day are limited to GBX before the open. There are no earnings reports scheduled after the close.

In economic news later this week, on Tuesday, we get the WASDE report, API Crude Oil Stocks Report and hear from two Fed members (Harker and Kashkari). Then Wednesday, March CPI, EIA Crude Oil Inventories, March Federal Budget Balance, and the FOMC Meeting Minutes are released. On Thursday, March CPI and Weekly Initial Jobless Claims are reported. Finally, on Friday, March Retail Sales, March Import/Export Price Indexes, March Industrial Production, Feb. Business Inventories, Michigan Consumer Sentiment. Feb, and Retail Inventories are reported.

In terms of earnings reports later this week, on Tuesday, KMX and ACI report. Then, on Wednesday, there are no major reports. Thursday, we hear from, DAL, FAST, INFY, and PGR. Finally, on Friday, BLK, C, JPM, PNC, UNH, and WFC report..

In under-the-radar geopolitical news, last week, the Chinese response to Taiwan’s President Tsai meeting with US House Speaker McCarthy included announcing plans Friday to begin stopping and inspecting ships in the Taiwan Strait. Taiwan’s response was to say “No you won’t” and advised ships and shipping lines to call the Republic of China (Taiwan) Coast Guard or Navy should they be radioed or obstructed by China. Shortly afterward, China said that its operation was a three-day military drill intended to demonstrate its ability to control the Strait. (Thus, limiting the escalation.) For its part, the US Administration has de-escalated the situation by simply saying this Chinese move was another ratcheting up of tensions (the same thing China said before the US officials met the Taiwanese leader).

So far this morning, GBX beat on both the revenue and earnings lines. It is worth noting that GBX revenue included a 34% upside surprise.

With that background, at least in the premarket, it appears stocked have pulled back in the last 30 minutes, to give us a very modest but red across-the-board opening bell. QQQ is now retesting its T-Line (8ema), with the SPY and DIA not far above their own T-lines. It looks as if the consolidation of last week is trying to continue. Overall, the price action still looks like nothing more than a modest consolidation (or small pullback in QQQ) in a bullish trend. However, you’d still be hard-pressed to look at these charts and say the bears are in control in any meaningful way. Obviously, being this close to the T-lines, overextension is not an issue now, either in terms of the T-line (8ema) or the T2122 indicator. Be cautious, but the last indications we received were bullish candles Thursday and Payroll data that will likely be seen as bullish (unless you are one of the “I don’t know why the sky isn’t falling yet” crowd).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Declining private payrolls and the shrinking services sector created a chop fest on Wednesday and traders ponder the economic slowdown and if that means a recession is just around the corner. Volume was low and looking at the VIX suggests no fear even though there is a record outflow to money market funds as investors look to protect capital. We will hear Jobless Claims numbers before the bell and comments from James Bullard later this morning with pending Employment Situation numbers on Friday when the market is closed. Anything is possible by Monday morning so plan carefully.

Asian markets traded mixed overnight after a surprise move from India to hold rates steady. However, European markets want to shake off the slowing economic conditions this morning seeing green across the board. U.S. futures on the other hand suggest a mixed open ahead of potential market-moving economic data and the pending Good Friday holiday closure.

Economic Calendar

Earnings Calendar

Notable reports for Thursday include LW, LEVI, RPM, STZ, WDFC.

News & Technicals’

Dave Burt, CEO of investment research firm DeltaTerra Capital, was one of the few skeptics who recognized the housing market was on the brink of collapse in 2007. He believes that an overlooked and unpriced climate risk could see history repeating itself. Burt said that “We think of this repricing issue as maybe a quarter of the size and magnitude of the [global financial crisis] in the aggregate but of course very, very damaging within those exposed communities.”

According to the latest projections for Social Security and Medicare, two of the three major trust funds may be insolvent in the next decade. Lawmakers may consider a host of changes to resolve those issues, from raising taxes to cutting benefits or both. Experts weigh in on what changes would be on their wish lists. Social Security’s woes largely come down to demographics. Since 2010, the program has been spending more on benefits than it has been bringing in from payroll tax revenues. By 2030, all baby boomers will be age 65 or older, according to the U.S. Census Bureau.

According to the new CNBC Supply Chain Survey, only about one-third of supply chain managers think warehouse inventories will return to normal before 2024. A little over one-quarter (27%) say companies are selling excess inventory on the secondary market because high storage prices are hitting the bottom line, with impacts to materialize in upcoming quarterly results. As expectations rise that Wall Street will revise earnings estimates lower in a weaker economy, almost half of those surveyed said the biggest inflationary pressures they are paying are warehouse costs, followed by rent and labor, and many are continuing to pass those costs on to consumers.

Wednesday’s price action was a low-volume chop fest as the declining ADP numbers and shrinking services sector added to worries of a slowing economy and possible recession. Before the market opens we will get the Jobless Claims number and will hear from James Bullard at 10 AM Eastern. Will it be enough to inspire a bullish or bearish move or will traders take the day to reduce risk ahead of the Friday Employment Situation report with the market closed for Good Friday? That raises the risk of a substantial Monday morning gap but the direction of the move is anyone’s guess so plan your risk carefully.

Markets diverged, and yet, acted strangely similar most of the day. DIA opened dead flat, rallied the first 30 minutes, and then traded sideways in a tight range between the open and the 10 am highs the rest of the day. SPY, gapped down 0.21%, traded sideways for 30 minutes, and then sold off for an hour. However, from 11 am until the close it too traded sideways in a tight range. For its part, QQQ gapped down 0.33%, sold off hard until 11 am, and then it too traded sideways in a tight range the rest of the day. This action gave us a Bullish Harami candle in the DIA, an indecisive Doji in the SPY, and an indecisive (larger-bodied) Spinning Top in the QQQ. All of the major indices remained above their T-line (8ema) with only the QQQ even testing that level.

On the day, five of the 10 sectors were in the green with Utilities (+2.22%) leading the way higher while Consumer Cyclicals (-1.62%) lagged the other sectors. At the same time, the SPY lost 0.26%, DIA gained 0.26%, and QQQ lost 0.99%. VXX lost 0.92% to 44.26 and T2122 fell but remains in the mid-range at 56.00. 10-year bond yields fell again to 3.309% while Oil (WTI) was flat at $80.61 per barrel. So, on Wednesday we saw divergence as money sought safety. The mega-cap DIA gained ground while the tech-heavy QQQ lost a percent. SPY fell somewhere in the middle, hurt by the big tech names and helped by the mega-caps. All of this happened on less-than-average volume in the DIA and SPY but just above-average volume in the QQQ.

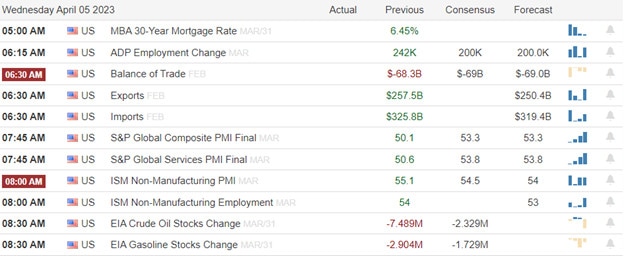

In economic news Wednesday, the March ADP Nonfarm Employment Change came in far below expectations at +145k (compared to a forecast of +200k and a Feb. reading of +261k). Later, the February Imports and Exports both came in above expectation but still below the January readings at $251.15 billion Exported and $321.70 billion Imported (versus forecasts of $250.40 billion for Exports and $319.40 billion for Imports but still down from the January Exports of $258.10 billion and Jan. Imports of $326.70 billion). This left the February Trade Balance at -$70.50 billion compared to a forecast of $69.00 billion and a January deficit of $68.70 billion. After the open, the March S&P Global Composite PMI came in one point below forecast at 52.3 but still better than the February reading at 50.1. The March US Services PMI also came in light at 52.6 (versus a forecast of 53.8 and a February value of 50.1). Meanwhile, the March ISM Non-Mfg. PMI reported below expectation at 51.2 (compared to a forecast of 54.5 and the Feb. reading of 55.1). Finally, the Weekly EIA Crude Oil Inventories fell 3.739 million barrels, which was more than the expected 2.329-million-barrel drawdown but still far below the prior week’s 7.489-million-barrel drawdown.

In stock news, WMT said Wednesday that it is seeing sustained pressure from inflation that is impacting its customers. As a result, it plans to slow its pace of hiring. (This is a day after WMT laid off 2,000 fulfillment center employees in an effort to reduce the cost of package processing by 20% via automation.) At midday, data from an engineering consortium (MLCommons) showed that flagship artificial chips from QCOM beat the best chips from NVDA in two out of three measures of power efficiency. (The cost of electricity is a major factor in AI technologies.) However, NVDA chips took the top spot in terms of absolute performance. Meanwhile, STLA joined the electric truck market by unveiling the Ram 1500 REV, which will debut in late 2024 as a 2025 model truck. This will be two years after the debut of F’s F-150 Lightning and a year after the GM electric Silverado (due out this fall). Later in the day, Reuters reported FDX will consolidate its FedEx Ground, outsourced package delivery unit and overnight Express air delivery businesses to cut costs and better compete with UPS and AMZN. After the close, COST reported that comparable store sales fell by 1.1% (led by a 1.5% decline in the US and a 2.4% decline in Canada) in March. Elsewhere, ABBV lowered its Q1 and full-year guidance a few weeks before it reports (4/27).

In stock legal and regulatory news, F and STLA both said that new rules from the US Treasury Dept. will cut EV tax credits on most of their electric and hybrid models. Later the US EEOC filed a “friend of the court” brief backing an appeal by a UBER driver that claims passenger ratings can be biased and were used by the company to kick out non-white drivers at a higher rate than whites. On the day, JNJ stock soared on what is still just a company-proposed $8.9 billion settlement of 40,000 lawsuits. (Approval of the JNJ proposal requires 75% of the 60,000 plaintiffs to accept.) At the close, GS was fined $3 million by FINRA for “mismarking” short orders for 14 billion shares when it reported its trades. This covered 12,335 trades. Elsewhere, the FDIC announced it has retained BLK to sell securities it holds in receivership after the collapse of SBNY. At the same time, CMG filed suit against SG for trademark infringement.

In miscellaneous news, Speaker of the House McCarthy and a bipartisan group of US Congressmen met with Taiwanese President Tsai on Wednesday during her “transit of the US.” (Called such because China would not like her “visiting” the US.) Regardless of the diplomatic labeling, China protested loudly and vowed a strong response. In other China news, AAPL has been secretly (and not so secretly) working to move the bulk of their production out of China and into India in the last six months or so. Even bringing their main manufacturer (Foxconn) with them. This is not just AAPL, but a major trend where the Chinese economy has grown enough that its people are a bit less desperate and beginning to demand better conditions and most importantly to corporations, pay. Vietnam and India seem to be “the winners” in that shift. However, according to Bloomberg today, EADSY (Airbus) is bucking that trend by opening a new jet manufacturing factory in China. Meanwhile, Mexico reported that its consumer inflation fell more than expected in March, reaching an 18-month low annual rate of 6.85%. This was down from a 7.62% annual rate in February. The question is whether this news bodes well for the US economy?

Overnight, Asian markets were mostly in the red. South Korea (-1.44%), Thailand (-1.44%), and Japan (-1.22%) led the region lower while Hong Kong (+0.28%) was the “big winner” on the day. However, in Europe, the bourses are leaning strongly to the green side at midday. Only, Norway (-0.48%) and Denmark (-0.33%) are in the red as the CAC (+0.31%), DAX (+0.35%), and the FTSE (+0.76%) lead the region higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing to another mixed and flat start to the day. The DIA implies a +0.04% open, the SPY is implying a +0.01% open, and the QQQ implies a -0.20% open at this hour. At the same time, 10-year bond yields are down to 3.285% and Oil (WTI) is just on the red side of flat at $80.49/barrel in early trading.

The major economic news events scheduled for Thursday are limited to Weekly Initial Jobless Claims (8:30 am), Fed Balance Sheet and Bank Reserve Balances with Federal Reserve Bank (both at 4:30 pm). The major earnings reports scheduled for the day include Wednesday, we hear from LW, STZ, RPM, and LEVI before the open. There are no earnings reports scheduled after the close.

In economic news later this week, on Friday, US markets are closed but March Avg. Hourly Earnings, March Nonfarm Payrolls, March Participation Rate, March Private Nonfarm Payrolls, and the March Unemployment Rate are reported.

There are no earnings reports scheduled for Friday.

So far this morning, RPM has reported beats on both the revenue and earnings lines., including a 23% upside surprise on the earnings line. However, RPM also lowered its forward guidance. Meanwhile, STZ reported 25 minutes late this morning for some reason, missing on revenue while beating on earnings. STZ also raised its guidance. LEVI is just scheduled for “before the open” and LW reports at 8 am.

With that background, at least in the premarket, the consolidation is continuing. It appears the QQQ will retest its T-Line (8ema) this morning. However, the two large-cap indices just seem to be hanging out at the moment. As I suggested yesterday, it could be that with March Payrolls data coming out while the market is closed Friday, traders want to just wait and see what Monday brings. Overall, the price action still looks like nothing more than a modest pullback and consolidation in a bullish trend. The most concerning of the major indices is QQQ which has pulled back the most and is testing its strong bullish uptrend line. However, you’d be hard-pressed to look at the chart and say the bears are in control in anything but the very short term. Obviously, being this close to the T-line, overextension is not an issue now, either in terms of T-line (8ema) or the T2122 indicator. Again, keep in mind that markets will be closed and you will not be able to react to March Payrolls data until Monday. So, be prepared for the 3-day weekend.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With the decline in the JOLTS report the market acknowledged the slowing economy and worries about a recession reliving some of the overbought conditions with some profit-taking. Though the indexes pulled back no substantial technical damage occurred except for the lower high at price resistance in the IWM. One day does not make a trend so it will be very important to see if the bears can follow through today or if the bulls have the energy to defend and recover. Prepare for just about anything as the market reacts to the economic reports and continue to watch out for the big point whipsaws plaguing the market of late.

While we slept Asian markets closed mixed as New Zealand hiked interest rates by 50 basis points. European markets trade mostly lower as slowing economies and recession worries resurface. At the time of writing this report, U.S. futures suggest a slightly bearish open that could easily improve or worsen as the pending economic data is revealed.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday include CAG, SCHN & SMPL.

News & Technicals’

Johnson & Johnson has agreed to pay $8.9 billion over the next 25 years to settle allegations that the company’s baby powder and other talc products caused cancer. The proposed settlement was announced in a securities filing and would require approval in bankruptcy court. J&J’s subsidiary LTL Management also refiled for Chapter 11 bankruptcy protection after its first attempt was thwarted. More than 60,000 claimants have committed to support the proposed resolution, according to the filing.

Virgin Orbit’s outgoing Chief Operating Officer Tony Gingiss sent a companywide email that appears to call out Virgin Orbit CEO Dan Hart, although not by name. Gingiss offered an apology to employees that they “have not heard from the person who should be saying it.” Virgin Orbit filed for Chapter 11 bankruptcy protection on Tuesday and noted in a securities filing that Gingiss was laid off as one of the 675 positions eliminated.

Federal Reserve Bank of Cleveland President Loretta Mester said on Tuesday that the U.S. central bank likely has more interest rate rises ahead amid signs that recent banking sector troubles have been contained. To keep inflation on a sustained downward path to 2% and keep inflation expectations anchored, Mester said she sees monetary policy moving “somewhat further into restrictive territory this year, with the fed funds rate moving above 5% and the real fed funds rate staying in positive territory for some time.”

Although the economic data has suggested we’ve had a slowing economy for some time the market decided yesterday with the decline in the JOLTS report to acknowledge the weakness. The Tuesday selling relieved some of the overbought condition as the dollar weakened and the precious metals surged as the worries of recession circulated. However, no significant technical damage occurred though the price patterns likely raised the level of uncertainty. Continue to watch for whipsaws as markets react to economic data with special attention to the oil numbers in light of the OPEC decision and its recent surge higher.

Tuesday started off flat in all three major indices. However, by 10 am, the bears had stepped in to sell off the whole market until 12:15 pm. At that point, we saw a sideways grind in a tight range near the lows in the SPY, DIA, and QQQ. This grind lasted the rest of the day. This action is giving us a Bearish Engulfing signal in the SPY (with a lower wick), a Bearish Harami in the DIA (again with a lower wick), and a black candle that qualifies as both a Bearish Dark Cloud Cover and an Indecisive Spinning Top in the QQQ. One additional piece of info is that the small-cap IWM printed a big, ugly Evening Star candle that crossed below its T-line (8ema). This all happened on far less-than-average volume in all three major indices, but the IWM had slightly greater-than-average volume.

On the day, seven of the 10 sectors were in the red with Industrials (-2.18%) leading the way lower while Communications Service (+0.37%) and Utilities (+0.33%) held up better than the other sectors. At the same time, the SPY lost 0.55%, DIA lost 0.58%, and QQQ lost 0.34%. VXX gained 1.73% to 44.67 and T2122 fell out of overbought territory to 64.79. 10-year bond yields fell again to 3.342% while Oil (WTI) was flat at $80.53 per barrel. So, Tuesday there was a little bit for both camps. We came into the day overextended to the upside. That means bulls would be perfectly justified if they characterized the day as a pause or consolidation of an uptrend. On the other hand, bears could also legitimately say it looks like the uptrend has lost steam and we could be at the start of a bearish reversal.

In economic news Tuesday, February Factory Orders came in below expectations at -0.7% (compared to the -0.5% forecasted but still much better than the -2.1% reading in January). Meanwhile, February JOLTs Job Openings came in better than expected at 9.931 million, which was the lowest level in two years, (versus the 10.400 million forecast and the January value of 10.563 million openings). Both of those will be seen as good news by the Fed as factory activity is slowing and there are notably fewer open jobs (so, less wage inflation pressure). Then, after the close, the API Weekly Crude Stocks Report showed a much bigger drawdown than expected at -4.346 million barrels (as compared to a forecast of -1.800 million barrels but still not as much as the prior week’s surprise drawdown of 6.076 million barrels).

In stock news, F reported a 10.7% increase in sales in Q1, selling 456,972 vehicles compared to 432,132 in Q1 of 2022. Of note is the fact that 95% of those Q1-2023 sales came from trucks and SUVs. Electric vehicle sales increased 41% year-over-year to 10,866 in the quarter. The company also announced adding a shift at their Kansas City plant and increasing production across the country to support strong demand. Meanwhile, F rival GM announced that about 5,000 salaried workers have taken buyouts which the company says puts them “well on their way” toward meeting a goal of cutting $2 billion in costs by the end of 2024. (The company CFO said the buyouts will contribute approximately $1 billion in savings. He also said GM will take a $1 billion charge in Q1 related to these contract buyouts.) Elsewhere, the US Army has awarded LMT a multi-year production contract for JAGM and Hellfire missiles that could run up to $4.5 billion (initial value $439 million in year one). At the same time, WMT announced that 65% of its stores will be serviced by automation by the end of fiscal 2026. (Meaning the distribution centers will be automated, eliminating warehouse workers.) The announcement also disclosed that the WMT will lay off more than 2,000 people at online order fulfillment centers related to this automation. Finally, after the close, TTE announced it has gotten a new (sweeter) deal from Iraq related to its $27 billion project to create 4 natural gas, oil, and renewables projects in the country. In the new deal, Iraq will take only a 30% ownership stake in the projects, compared to the original deal that gave Iraq 40% ownership in the projects.

In stock legal and regulatory news, the NHTSA announced a recall of 143,000 VLKPY (Volkswagen) 2018-2021 vehicles related to front passenger seat airbag systems. At the same time, a US Appeals Court has rejected a bid from AAPL, which was seeking to override its rejection for a trademark on “Apple Music.” (A jazz musician had been using the “Apple Music” term to brand his music in advertising since 1985.) Later in the day Tuesday, TPG agreed to buy a majority stake in the “Elite” software business of TRI for $500 million. Elsewhere, Reuters reported JNJ has refiled for bankruptcy of its talc subsidiary (created solely to limit JNJ liability from 40,000 lawsuits claiming the company’s tac powder contained cancer-causing agents). While JNJ had initially filed for bankruptcy and offered $2 billion to settle all lawsuits, the new filing is offering $8.9 billion (paid over 25 years) to resolve all current and future claims (there are more than 60,000 current claimants). Meanwhile, ABUS filed a patent infringement lawsuit against PFE and NNTX related to the latter pair’s COVID-19 mRNA vaccine. Later, a Reuters report says that a 3-judge panel of the 7th Circuit of the US Court of Appeals appears very skeptical of MMM’s attempt to do the same thing JNJ did above (move liability to a new subsidiary and then file bankruptcy for the subsidiary to avoid liability from lawsuits by the parent corporation. A bankruptcy judge had ordered lawsuits to continue against MMM even though the subsidiary (Aearo Technologies) is bankrupt. The suits are related to alleged defective military-issue earplugs that caused deafness.

In mortgage news, rates fell last week but demand for home loans dropped anyway. Analysts say a lack of home listings are outweighing lower rates as home buyers are not satisfied with the offering available. The average 30-year fixed-rate, conforming (20% down) loan rate was 6.40% (down from 6.45%) with origination points also falling from 0.62 to 0.59. Nonetheless, home purchase mortgage applications fell 4% week-on-week while refinance applications fell 5% on the week. The National Realtors Assn. says the main issue facing that market is a 20% drop in new listings and total “for sale” inventory (houses) less than half of what was on the market at this time in 2019. So, it appears Americans are staying put longer and not refinancing to do renovations.

Overnight, Asian markets were mixed but leaned (at least in broadness) to the upside. Japan (-1.68%), Thailand (-1.44%), and Hong Kong (-0.66%) paced the losses. At the same time, India (+0.91%), South Korea (+0.59%), and Shanghai (+0.49%) led the gainers. In Europe, we see the opposite picture taking shape at midday. The more plentiful red side of the market is led by CAC (-0.13%) and DAX (-0.20%), with eight smaller exchanges moving (some moving more) to the downside. Meanwhile, the FTSE (+0.44%) leads the gainers, with four smaller exchanges moving up less at least in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a start to the day just on the red side of flat. The DIA implies a -0.08% open, the SPY is implying a -0.12% open, and the QQQ implies a -0.13% open at this hour. 10-year bond yields are up a touch to 3.357% and Oil (WTI) is down four-tenths of a percent to $80.35/barrel in early trading.

The major economic news events scheduled for Wednesday include the ADP March Nonfarm Employment Change (8:15 am), Feb. Imports/Exports and Feb. Trade Balance (both at 8:30 am), March Service PMI and S&P March Global Composite PMI (both at 9:45 am), March ISM Non-Mfg. PMI (10 am), and EIA Weekly Crude Oil Inventories (10:30 am). The major earnings reports scheduled for the day include CAG and SCHN before the opening bell. There are no earnings reports scheduled after the close.

In economic news later this week, Thursday, we get Weekly Initial Jobless Claims and Bank Reserve Balances with Federal Reserve Bank. Finally, on Friday, US markets are closed but March Avg. Hourly Earnings, March Nonfarm Payrolls, March Participation Rate, March Private Nonfarm Payrolls, and the March Unemployment Rate are reported.

In terms of earnings, on Thursday, LW, STZ, RPM, and LEVI report. There are no reports scheduled for Friday..

So far this morning, CAG has reported a beat on both the revenue and earnings lines. The earnings beat was almost a 20% upside surprise versus the average analyst forecast. CAG also raised its forward guidance. (SCHN reports at 8 am.)

With that background, at least in the premarket, it looks like the consolidation continues. It could be that with March Payrolls data coming when the market is closed Friday that traders don’t want to get too far in front of their skis. Today’s ADP Payrolls number may give some of them the courage to change that stance. All-in-all, the bulls could not have hoped for a much better start (consolidation) to April after the surge the three-day surge that ended March. Overextension is not an issue now, either in terms of T-line (8ema) or the T2122 indicator. Stay cautious, but the trend is clearly bullish in all three major indices.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Despite the surging oil prices that could raise inflationary pressures the rally continued on Monday as the talking heads seem to sing in the chorus for a typical spring rally as if banking concerns no longer exist. The weak PMI, ISM, and construction spending numbers also did nothing to dissuade the bulls from running. Today we have Factory Orders and the JOLTS report for the bulls or bears to find inspiration. Like yesterday keep an eye on overhead resistance and watch out for those nasty big point whipsaws.

Asian markets mostly rallied overnight with modest gains and losses as Australia’s central bank held rates steady. European markets appear to have no concern over the rising energy prices as Finland joins NATO raising the ire of Russia seeing only green across the indexes. U.S. futures are also looking to extend the bullish run with the Nasdaq joining the party and brushing off the energy cost concerns of yesterday.

Economic Calendar

Earnings Calendar

If this looks like a repeat of yesterday it is because I accidentally used the Tuesday notables on the Monday blog. So here they are again AYI, LNN, MSM, RGP, SGH.

News & Technicals’

Jamie Dimon, the longtime CEO of JPMorgan Chase, recently commented on the latest financial shock in his annual letter. He stated that “The current crisis is not yet over, and even when it is behind us, there will be repercussions from it for years to come.” However, he added that “recent events are nothing like what occurred during the 2008 global financial crisis”. The recent banking issues in the U.S. began with the collapse of Silicon Valley Bank. Regulators closed it on March 10th as depositors pulled tens of billions of dollars from the bank.

Virgin Orbit has filed for Chapter 11 bankruptcy protection in the U.S. after failing to secure a funding lifeline. This comes days after the company’s CEO Dan Hart told employees during an all-hands meeting that the company was ceasing operations “for the foreseeable future”. The company’s last mission suffered a mid-flight failure, with an issue during the launch causing the rocket to not reach orbit and crash into the ocean.

The rally continued on Monday with talking heads talking up the typical spring rally despite the surge in oil prices that impact the consumer at the pump while increasing inflation pressures for the Fed. After rising 350 points the Dow whipsawed in a quick round of selling dropping more than 150 points before slowly grinding its way back to close at the high of the day. The QQQ was the only index in the red as it acknowledged the costs of rising oil but also found buyers in the afternoon to close it well off its intraday low. The stretch to the upside continues to present a short-term overbought condition so watch resistance levels and be prepared for a possible profit-taking pullback that could begin at any time.