The FOMC disappointed the market as indexes turned negative after raising rates with a unanimous vote from the committee. Unfortunately, the news adds more pressure to the regional banking sector with PACW now looking for a solution for the rapid selloff. We have a jampacked day of earnings and economic data to keep traders guessing and investors on edge culminating with a highly anticipated AAPL report after the bell. Don’t be surprised to see a substantial gap up or gap down, as a result, Friday morning.

Asian markets traded mixed with Hong Kong’s tech-heavy index gaining 1.27% by the close. However, with an ECB rate decision pending European markets see only red this morning as they wait. U.S. futures suggest a mixed open ahead of a massive day of earnings data with worrisome jobs, trade, and productivity data pending. Keep an eye on the regional banking sector with several names under attack.

Microsoft is rolling out a new version of its Bing search engine that will let anyone with a Microsoft account chat with a bot that uses an OpenAI artificial intelligence model. The bot can answer questions, provide suggestions and generate content based on the user’s queries. The new Bing also offers chat history, export options, and visual enhancements to improve the user experience. Microsoft plans to add third-party integrations to Bing in the future. The company hopes that the new Bing will help it gain more share in the search advertising market, where it still lags behind its competitors, according to Bernstein analysts.

PacWest, a California-based bank, is looking for ways to survive after the collapse of First Republic, another regional bank. PacWest’s stock has plunged since First Republic’s failure, which raised concerns about the health of smaller banks. PacWest said it is negotiating with several potential partners and investors who could help it weather the storm. The bank also said it had not seen any unusual deposit withdrawals after First Republic’s demise.

With a unanimous vote, the Federal Reserve increased rates by 0.25%, making its overnight policy rate 5% – 5.25%. The statement did not include a line that said, “some additional policy firming may be appropriate,” which may mean a pause at this level is possible The 2-year Treasury yield and the U.S. dollar declined but stocks also fell, as the decision disappointed investors, and the struggling regional banks. Today is a massive day of earnings data with the highly anticipated Apple report coming after the bell. Traders will also have to deal with Challenger Job-Cut, International Trade, Jobless Claims, Productivity, and Natural Gas numbers while keeping an eye on regional bank pressures.

On Tuesday, markets opened just on the red side of flat again (down 0.18% in the SPY, down 0.15% in the DIA, and down 0.01% in the QQQ). However, after the tepid open, the bears stepped in to drive a strong selloff that reached the lows of the day at about 11:30 am in all three major indices. From that point, the rest of the day was a sideways meander with a modest bullish trend. This action gave us black-bodied candles with large lower wicks in the SPY, DIA, and QQQ. The QQQ retested and held above its T-line (8ema) while the two large-cap indices closed just below their 8emas. It also does not take too much imagination to see all three major indices as an Evening Star-type candle.

On the day, all 10 sectors were in the red with Energy (-4.17%) leading the way lower while Basic Materials (-0.40%) held up better than the other sectors. At the same time, the SPY lost 1.12%, DIA lost 1.02%, and QQQ lost 0.87%. VXX climbed 4.43% to 38.89 and T2122 dropped down well into the oversold territory to 11.11. 10-year bond yields plummeted again to 3.435% while Oil (WTI) plunged 5.34% to $71.62 per barrel. So, to summarize, Tuesday was the bears’ day ahead of today’s Fed decision. This all happened on a little shy of the average volume in all three major indices.

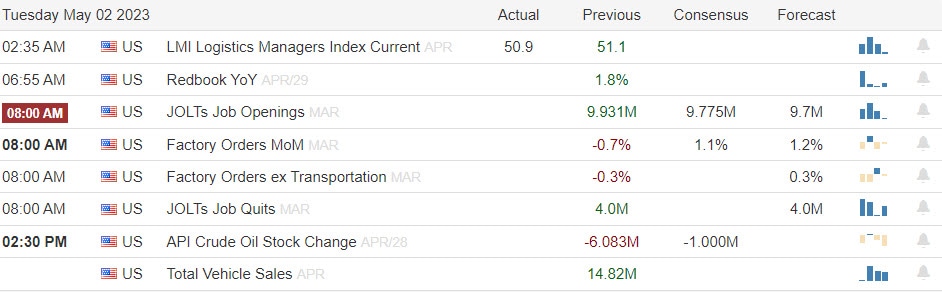

In economic news, March Factory Orders came in below expectation at +0.9% (versus a forecast of +1.1% but much better than the February reading of -1.1%). At the same time, the labor market remained strong as March JOLTs Job Openings came in lower than anticipated at 9.590 million (compared to a forecast of 9.775 million and a February value of 9.974 million). So, Factory activity continues to grow but at a slow pace, while the labor market is slowly tightening, with 400k fewer openings in March than in Feb. After the close, the API Weekly Crude Oil Stock Report showed a much larger than expected oil inventory drawdown of 3.939-million-barrels (versus a forecast of a 1.000-million-barrel drawdown but still much less than the prior week’s 6.083-million-barrel drawdown.

In stock news, regional banks took a beating again Tuesday with PACW closing down 27.78%, WAL down 15.12%, and even much larger USB down 7.01% and TFC down 7.61%. Elsewhere, electric vehicle maker MULN announced that has received a 1,000-truck order ($63 million) with first deliveries scheduled to begin in August. At the same time, Reuters reported the US will announce another $300 million military aid package for Ukraine as soon as today. The new package will include air-launched rockets, 155mm shells (both made by GD), HIMARS missiles (from LMT), TOW missiles (from RTX) as well as other miscellaneous munitions. After the close, PNC bank said it can offer $15 billion of its short-term commercial paper (very liquid and generally secure) to calm market worries over liquidity. This announcement was made even after the bank reported a rise in deposits and profits during Q1. Finally, despite a blowout success in its quarterly report Tuesday night, F announced it is cutting the price of the Mustang Mach-E again as the price war with TSLA continues.

In stock legal and regulatory news, VMW lost the retrial of its patent infringement case filed by Densify and will pay $84.5 million in the verdict. (This is much less than the original verdict of $237 million from 2020 which was thrown out on appeal.) Elsewhere, the US SEC will vote today on whether to adopt new rules increasing transparency from the advisors to hedge and private-equity funds. Meanwhile, after the close, AMGN sued NVS for patent infringement over drugs AMGN has sold $5.6 billion of and NVS has now proposed launching generic versions. At the same time, the White House has summoned the CEOs of GOOGL and MSFT (as well as others) to a Thursday meeting to discuss AI issues and potential regulation. In bankruptcy news, CNNWQ received court approval to raise $2.26 billion as part of its exit from bankruptcy. Finally, the US Dept. of Transportation announced Tuesday that it will not extend the July 1 deadline for plane 5G retrofits as had been requested by airlines. And Airline industry group said this may cause airline operational disruptions during the peak summer travel season.

After the close, F, SBUX, AMD, MUSA, AIZ, CZR, CLX, CWH, AFG, WELL, THG, AXTA, WU, CHK, RNR, LFUS, CRK, JKHY, BFAM, MTW, HY, and UIS all reported beats on both the revenue and earnings lines. Meanwhile, OKE, ANDE, EIX, AMCR, UNM, YUMC, UFPI, ENLC, EXPI, MTCH, and CLW missed on revenue while beating on the earnings line. On the other side, PRU, LUMN, VOYA, HLF, SPG, MCY, EXR, and GPOR beat on revenue while missing on earnings. Unfortunately, ET, SMCI, BXC, and ASH missed on both the top and bottom lines. It is worth noting that AMCR, MTCH, and ASH lowered their forward guidance. However, CLX, SMCI, LFUS, JKHY, and PAYC all raised their forward guidance. (It is also worth noting that F had 62% upside surprise, YUMC had a 61% upside surprise, AIZ had a 55% upside surprise, CZR had a 50% upside surprise, SWH had a whopping 169% upside surprise, THG had an 86% upside surprise, and BFAM had a 44% upside surprise on earnings.)

Overnight, Asian markets were mixed but mostly red. Hong Kong (-1.18%), New Zealand (-1.08%), and Australia (-0.96%) led the region lower. Meanwhile, in Europe, the bourses lean heavily to the green side with only three spots of red on the board at midday. The CAC (+0.68%), DAX (+0.82%), and FTSE (+0.22%) are leading the region higher in early afternoon trade. In the US, as of 7:30 am, the Futures are pointing toward a modestly green start to the day. The DIA implies a +0.11% open, the SPY is implying a +0.15% open, and the QQQ implies a +0.24% open at this hour. At the same time, 10-year bond yields are down to 3.407% and Oil (WTI) is plummeting again (by 3.07% this time) to $69.47/barrel in early trading.

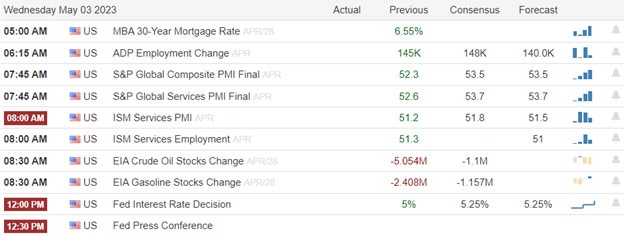

The major economic news events scheduled for Wednesday include the ADP Nonfarm Employment Change (8:15 am), Services PMI (9:45 am), April ISM Non-Mfg. PMI (10 am), EIA Crude Oil Inventories (10:30 am), FOMC Rate Decision and Fed Statement (both at 2 pm), and Fed Chair Press Conference (2:30 pm). The major earnings reports scheduled for the day include ADNT, ALGT, AVNT, AVA, GOLD, BDC, BGCP, EAT, BIP, BLDR, BG, CDW, CHEF, CLH, SID, CVS, XRAY, DBD, DRVN, EMR, EL, EEFT, EXC, FTS, GRMN, GNRC, GFF, HBI, HZNP, INGR, JHG, KHC, LPX, MUR, NI, PSN, PSX, RXO, SMG, SBGI, SITE, SR, SPR, STLA, TKR, TT, TRMB, UTHR, VRSK, and YUM before the open. Then, after the close, ALB, ALL, ATUS, AMED, ANSS, HOUS, APA, ATO, AVT, EQH, BHE, BKH, CPE, CENT, CENTA, CDAY, CHRD, CIVI, COKE, CTSH, CODI, CTVA, CCRN, CW, NVST, EQIX, ETSY, FG, FLT, FNF, ULCC, GIL, GL, HST, IR, IOSP, MRO, VAC, MMS, MELI, MET, MKSI, MOS, NFG, OPAD, PARR, PDCE, PSA, QGEN, QRVO, QCOM, QDEL, O, REZI, SIGI, SEDG, RUN, TWI, TTEC, TTMI, UGI, VSTO, WERN, WES, WMB, XPO, YELL, and Z report.

In economic news later this week, on Thursday, we get March Imports, March Exports, March Trade Balance, Weekly Initial Jobless Claims, Preliminary Q1 Nonfarm Productivity, Preliminary Q1 Unit Labor Cost, the Fed Balance Sheet, and Bank Reserves with the Federal Reserve. Finally, on Friday, April Average Hourly Earnings, April Nonfarm Payrolls, April Private Nonfarm Payrolls, April Participation Rate, and the April Unemployment Rate.

In miscellaneous news, fear of another potential pandemic (and potential threat to the poultry supply) is taking shape in the UK. Thousands of dead wild birds litter England. The problem is so bad the British government has warned dog walkers to keep their animals on leashes at all times to keep the dogs from eating birds or bird droppings. The avian flu isn’t contained to the UK either as the USDA has reported at least 170 confirmed cases of mammals (mostly cats and dogs) picking up the disease in the US from this latest wave. This comes after more than 60 million chickens and turkeys died or were culled to prevent the spread of the last wave in 2022. The good news is that dating back to 1997, there are less than 900 confirmed cases of humans contracting the earlier variants of the avian flu.

So far this morning, CVS, PSX, KHC, BLDR, EXC, EMR, TT, GOLD, FTS, NI, AVNT, GRMN, CLH, GNRC, TKR, EAT, XRAY, PSN, SR, VRSK, JHG, BDC, MUR, CHEF, DRVN, HSC, FDP, and QUAD have all reported beats on both the revenue and earnings lines. Meanwhile, CDW, BIP, INGR, SMG, LPX, TRMB, and UTHR all missed on revenue while beating on earnings. On the other side, BG, EL, YUM, BLCO, SITE, EEFT, and ALE beat on revenue while missing on the earning line. Unfortunately, SPR, HZNP, DBD, and AVA missed on both the top and bottom lines. It is worth noting that CVS, BLDR, and TRMB lowered their forward guidance. However, KHC, EMR, INGR, TKR, CHEF, and HSC all raised their forward guidance.

With that background, it looks like the large-cap indices are retesting their T-lines (8ema) in the premarket and the tech-heavy QQQ is pushing up away (a bit) from its own. We all know that today will be all about the Fed. So, don’t be surprised with either a dead market or chop going back and forth in an indecisive way right up to 2 pm. Over-extension from the T-lines is not a problem and while T2122 is well into the oversold territory, it is not extremely extended. Don’t get caught predicting the reaction to the FOMC. And, also remember that there tends to be a knee-jerk, followed by a re-reaction…and then an “on second thought” move the next morning when there is a Fed announcement. Be prepared.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bears feasted on Tuesday as the renewed banking weakness sparked a sharp selloff hoping to send a message to the FOMC on the pending rate decision this afternoon. Big tech held its ground while IWM suffered the most technical damage with many regional banking names included in the average. Today we face a big round of earnings events so plan whipsaws and uncertain chop as we wait for the Fed decision at 2 PM Eastern with Powell’s presser thirty minutes later that may well create some wild price swings.

Asian market traded mix overnight as worries about the huge banking outflows and the next Fed decision. However, European markets seem much more upbeat with gains across the board. The U.S. is also trying to shake off the pending Fed decision and banking worries with futures suggesting modest gains at the time of writing this report.

The global economy is facing a dilemma as inflation continues to soar despite the efforts of central banks to tame it. By raising interest rates, central banks hope to cool down the demand for goods and services and reduce the cost of living. However, higher interest rates also make borrowing more expensive and can hurt economic growth and financial stability. According to a survey by the World Economic Forum, most economists believe that central banks have to choose between fighting inflation and supporting the financial sector. This could pose a serious challenge for policymakers as they try to balance the needs of the economy and society.

The clock is ticking for the U.S. government on its debt ceiling, which could trigger financial complications for the economy as worries of stagflation grow. While Democrats have publicly blamed Republicans for refusing to cooperate on raising the debt ceiling, they have also quietly taken some steps to open the door for a possible compromise. President Joe Biden has signaled his willingness to negotiate with Republicans on his spending plans, while Democratic leaders in Congress have explored ways to use their slim majority to raise the debt limit without GOP support. These moves suggest that both parties are aware of the high stakes of the debt ceiling standoff and may be willing to make concessions to avert economic consequences.

Renewed banking weakness brought out the bears on Tuesday adding pressure to the pending FOMC rate decision. As investors worry about possible recession or stagflation the earnings season excitement is struggling to overcome. Some people are buying bonds instead of stocks because they think bonds are safer or moving cash into money market funds to protect capital from massive uncertainty. Plan for a choppy session as we wait on the FOMC decision with a big round of earnings data and economic reports to keep the whipsaw and the price action volatile.

Markets opened on the red side of flat, mostly gapping very mildly lower (down 0.13% in the SPY, up 0.02% in the DIA, and down 0.18% in the QQQ). From that point, it was a whipsaw day that saw the bulls marginally in control in the morning and the bears marginally in control in the afternoon. This action left us with indecisive candles in all the major indices. The QQQ printed a DOJI Harami, the SPY printed a Gravestone Doji Harami, and the DIA printed a black-bodied Inverted Hammer-type candle. All three remain above their T-lines (8ema) and nothing appreciable has changed in any of those charts. This all happened on less-than-average volume across the market.

On the day, five of the 10 sectors were in the red with Energy (-0.84%) leading the way lower while Healthcare (+0.71%) held up better than the other sectors. At the same time, the SPY lost 0.10%, DIA lost 0.18%, and QQQ lost 0.11%. VXX fell 1.64% to 37.24 and T2122 dropped back a little further into the mid-range at 65.55. 10-year bond yields spiked up to 3.57% while Oil (WTI) fell 1.41% to $75.70 per barrel. So, to summarize, Monday was a nothing-burger of indecision as markets showed no ill effect from the failure of FRC (acquired by JPM) and seem to be waiting on the Fed or more earnings to move the needle.

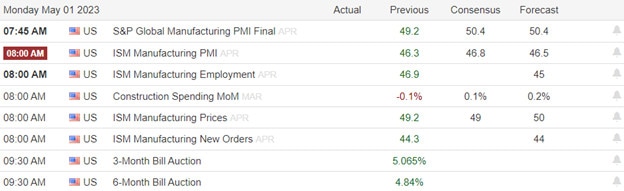

In economic news, April Manufacturing PMI came in below expectation at 50.2 (versus a forecast of 50.4 but still above the March reading of 49.2). (Anything above 50 indicates economic expansion.) Later, April ISM Manufacturing PMI came in above expectation at 47.1 (compared to a forecast of 46.8 and a March value of 46.3). April ISM Manufacturing Employment was well above the anticipated level at 50.2 (versus a forecast of 47.9 and a March level of 46.9). Finally, April ISM Manufacturing Prices came in well above what was expected at 53.2 (compared to a forecast of 49.0 and a March reading of 49.2).

In stock news, RIDE warned of potential bankruptcy after Foxconn (one of the electric automaker’s largest investors) alleged RIDE has breached the agreement between the two companies. This puts $170 million in funding for RIDE at jeopardy. Elsewhere, AAL pilots have authorized the union to call a strike (96% of pilots voted and 99% of those voted in favor of a strike authorization). No strike date is set as this is negotiation leverage, not imminent action. Later, after the close, Bloomberg reported that IBM has paused hiring with plans to replace up to 7,800 jobs (30% of its non-customer-facing jobs) with AI in coming years. At the same time, Reuters reports that MS will cut 3,000 jobs in Q2. Meanwhile, Reuters reported that META is looking to raise $8.5 billion in a 5-part bond offering. (META raised $10 billion using the same mechanism in 2022.) Finally, overnight, TSLA hiked prices on Model 3 and Model Y cars (in the US, China, Canada, and Japan only) in what seems to be a plea for help by either the CEO or senior management. This minuscule $250 hike in price (on a $40k to $47k original price) and coming after price cuts earlier in the year make it seem like they are flailing around looking for a pricing strategy.

In stock legal and regulatory news, Reuters reported Monday that the EPA may delay a decision on giving eRIN credits to Electric Vehicle makers under a renewable fuel program. The reason for the delay is that the House GOP wants to file a legal challenge on behalf of the fossil-based Energy industry, as they claim those credits were intended only for biofuel (ethanol and biodiesel) manufacturers. This delay will impact TSLA most heavily, but all other electric vehicle makers as well, who will not get the credits they were expecting since the fall. In other EV news, FSR received certification from EU regulators and will begin delivering its “Ocean” electric SUVs on Friday. Meanwhile, a US federal judge gave F a win. He ruled that while Versata Software had proven that F stole their trade secrets in breach of their agreement, the defendant had not provided enough evidence of the damages suffered to justify a lower court jury award of $105 million. Instead, the judge ordered F to pay a massively-reduced $3 million.

LEG, TEX, ANET, FLS, SBAC, AL, SGRY, WWD, INVH, KMT, and VICI all reported beats on both the revenue and earnings lines. Meanwhile, SON, FMC, and SCI all missed on revenue while beating on earnings. On the other side, CYH, RE, OGS, CNO, and RIG all beat on revenue while missing on earnings. Unfortunately, FANG missed on both the top and bottom lines. It is worth noting that SYK, NXPI, SFM, TEX, SBAC, SGRY, and WWD all raised their forward guidance. However, AMKR lowered its forward guidance.

Overnight, Asian markets leaned heavily toward the green side. Shanghai (+1.14%), Shenzhen (+1.09%), and South Korea (+0.91%) led the region higher with Australia (-0.92%) showing any appreciable loss. In Europe, the bourses are mostly in the red on moderate moves at midday. The CAC (-0.41%), DAX (-0.19%), and FTSE (-0.01%) lead the region lower with three minor bourses modestly in the green in early afternoon trade. As of 7 am, US Futures are pointing toward a slightly red start to the day. The DIA implies a -0.22% open, the SPY is implying a -0.19% open, and the QQQ implies a flat -0.03% open at this hour. Meanwhile, 10-year bond yields are back down to 3.536% and Oil (WTI) is off another seven-tenths of a percent to $75.16/barrel in early trading.

The major economic news events scheduled for Tuesday are limited to March Factory Orders and March JOLTs Job Openings (both at 10 am), and API Weekly Crude Oil Stocks (4:30 pm). The major earnings reports scheduled for the day include ADT, AER, AGCO, ARLP, ABC, AME, BP, BR, CX, CQP, LNG, CIGI, CEIX, CEQP, CMI, DORM, DD, ETN, ECL, EPD, ESAB, EXPD, FELE, IT, GVA, GPK, HWM, HSBC, IDXX, IHRT, ITW, INCY, NSIT, LDOS, MDC, MPC, MAR, TAP, MLPX, MD, PFE, PEG, QSR, SEE, SUN, SYY, TROW, TRI, TRN, UBER, ZBRA, and ZBH before the open. Then, after the close, AMD, AMCR, AFG, ANDE, ASH, AIZ, AXTA, BXC, BFAM, CZR, CRC, CWH, CHK, CLW, CLX, EIX, ET, ENLC, EQX, EXPI, F, THG, HLF, JKHYLFUS, LUMN, MTW, MTCH, MCY, MUSA, OKE, PGR, PRU, RNR, SPG, SBUX, SMCI, UNM, VOYA, WELL, WU, and YUM report.

In economic news later this week, on Wednesday, the ADP Nonfarm Employment Change, Services PMI, April ISM Non-Mfg. PMI, EIA Crude Oil Inventories, FOMC Rate Decision, FOMC Statement, and Fed Chair Press Conference all happen. Thursday, we get March Imports, March Exports, March Trade Balance, Weekly Initial Jobless Claims, Preliminary Q1 Nonfarm Productivity, Preliminary Q1 Unit Labor Cost, the Fed Balance Sheet, and Bank Reserves with the Federal Reserve. Finally, on Friday, April Average Hourly Earnings, April Nonfarm Payrolls, April Private Nonfarm Payrolls, April Participation Rate, and the April Unemployment Rate.

In miscellaneous news, on Monday the US Treasury Department warned that the government could run out of cash by June 1 without a debt limit increase. In response, the President called the Majority and Minority leaders of both Houses of Congress, inviting them to a May 9 meeting to talk about the debt ceiling and federal spending. In other news, after JPM acquired FRC on Sunday night, CEO Jamie Dimon reversed his recent warnings and said the “banking crisis” may be over for now. He went on to point out that many regional banks have posted good first-quarter results. Dimon’s rival, CEO of C, Jane Fraser agreed saying the US banking system is “the envy of the world” (which, to be fair, is not the same thing as saying it is in great shape).

So far this morning, ABC, PFE, ETN, DD, UBER, GPK, ZBH, AME, QSR, ZBRA, MDC, IDXX, MAR, MPLX, TROW, TRI, MD, and IT have all reported beats on both the revenue and earnings lines. At the same time, BP, MPC, and EPD missed on revenue while beating on earnings. On the other side, LDOS, and TRN both beat on revenue while missing on earnings. Unfortunately, GVA missed on both the top and bottom lines. (There are many others reporting later this morning.) It is worth noting that ABC, ETN, and IT have raised their forward guidance. Meanwhile, DD and ZBRA have both lowered guidance.

With that background and with the possible exception of DIA, it looks like the market is looking to open flat again today as we wait on the Fed decision and the digestion of a flood of earnings. All three major indices are above their 3ema, T-line (8ema), and 17ema…all of which are also trending higher. SPY and DIA continue to face a resistance level right near the Friday close. However, immediate resistance for QQQ is less than obvious. Over-extension is not a problem in any of the major indices. With so much in the air, it is quite possible that a good part of at least today and Wednesday will be spent in “wait and see” mode. The Fedwatch tool tells us that confidence in a 0.25% rate hike by the Fed is even stronger than yesterday, up to 91% probability. The other 9% probability is for “no hike.” Beyond this week, futures still currently see little (32% on the largest probability and that for a quarter-point hike in June) chance of an additional increase this year and most are actually still betting on rate decreases sometime in the Fall. (That would be against what the Fed has repeatedly said, but that is what the Fed Fund Futures tell us.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The wait on the Fed began Monday producing a choppy session with little to no concern from investors about the ongoing regional banking declines. We also learned that due to declining tax receipts, the Federal default deadline may be sooner than originally projected. Today we investors will have a lot of earnings data to digest as well as Factory Orders and the JOLTS report. However, don’t be surprised if we see another light volume choppy day as we wait to hear from Jerome Powell on Wednesday afternoon.

Asian markets mostly rallied while we slept with the ASX the only decliner after raising rates by 25 basis points. European markets trade mixed with the FOMC rate decision in focus. U.S. futures point to a slightly lower open ahead of a slew of earnings and economic data with worries about the debt ceiling, regional banks and the pending Fed action swirling.

The US government is facing a looming deadline to raise its debt ceiling or the maximum amount of money it can borrow to pay its bills. The debt ceiling, which is set by Congress, currently stands at $31.4 If the debt ceiling is not raised or suspended by June 1, Treasury Secretary Janet Yellen warned that the US could default on its debt obligations for the first time in history. This could have disastrous consequences for the US economy and global financial stability, as investors would lose confidence in the US dollar and the government would have to cut spending on essential services. President Joe Biden has invited the top four congressional leaders to a meeting at the White House on May 9 to discuss the debt limit issue. However, Republicans and Democrats have different views on how to address the debt problem, and a compromise may be hard to reach.

Shein is a company that sells cheap clothes online. It started in China. Some people in the US government are worried that Shein uses workers who are not paid or treated well. These workers are from a group of people called Uyghurs who live in China. The US government does not like how China treats Uyghurs. The US government wants to stop Shein from selling its shares to the public in the US. They want Shein to prove that it does not use bad workers. Shein says it does not use bad workers and it follows the rules.

Stocks did not change much on Monday chopping in a range as wait on the FOMC began. Talking heads seem to make light of 3rd bank’s failure as the pressures on regional banks continue and the market appears willing to ignore the situation. The federal default deadline is back in the news today due to declining tax revenues further complicating the Fed rate decision Wednesday afternoon. Today we investors have big wave earnings data to react to as well as Factory orders and the JOLTS report. Don’t be surprised if we see another choppy day with Jerome Powell’s comments pending.

After a small gap lower to get the session started (gapping down 0.23% in the SPY, down 0.33% in the DIA, and down just 0.07% in the QQQ at the open) the Bulls had another day in charge on Friday. From that open, with the sole exception of a 30-minute pullback at 10:30, all three major indices saw a slow, steady rally all day long and went out on their highs. This took the SPY and DIA to just above (still in a retest) the mid-April highs and left the QQQ a new high not seen since August 2022. This action gave us large, white Marubozu (Shaved Head) candles in the SPY and DIA. The QQQ had a small lower wick and not quite as large candle, but still a strong showing for the Bulls.

On the day, eight of the 10 sectors were in the green with Energy (+1.79%) by far out in front of the rest and Communications Services (-0.24%) lagging behind the other sectors. At the same time, the SPY gained 0.85%, DIA gained 0.84%, and QQQ gained 0.69%. VXX fell 4% to 37.82 and T2122 climbed up to the top of the mid-range, just outside of the overbought territory at 78.77. 10-year bond yields fell to 3.433% while Oil (WTI) gain 2.50% to $76.63 per barrel. So, slowing inflation and generally good earnings trumped everything else on the last trading day of April despite fears for the future of FRC (a regional bank). This all happened on average volume in all three major indices.

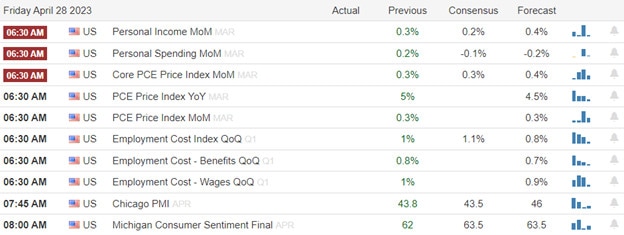

In economic news, March PCE Price Index (the Fed’s preferred measure of inflation) showed a slower-than-expected increase in prices at +0.1% month-on-month (compared to a forecast of +0.3% and the February reading of +0.3%). On an annualized basis, that brought the reading down to 4.2% from a 5.0% reading just one month earlier and a 5.3% reading at the end of February. While you could say the glass is half empty by noting inflation is still far above 2%, it is undeniable that there has been a strong and steady decline in this inflation metric since July 2022. And it’s quite likely that the trend is what all but the Fed ultra-hawks will latch onto. However, in other inflation-relation economic news, the Q1 Employment Cost Index came in above expectation at 1.2% (versus a forecast and previous value of 1.1%). (This may be a preliminary reading, it was not marked and I am unsure.) Later in the day, Chicago PMI came in above the anticipated level at 48.6 (compared to a forecast of 43.5 and the March reading of 43.8). Finally, the Michigan Consumer Sentiment remained where it was expected at 63.5 (versus the forecast and prior value which were both also 63.5).

In stock news, on Friday, MBGAF (Daimler) announced a $650 million joint venture with NEE and BLK to develop and operate a nationwide network of public charging stations and hydrogen fueling stations in the US. Elsewhere, the US Dept. of Defense awarded a $7.8 billion contract modification to LMT for building 126 F-35 aircraft. In the oil business, the big names are rolling in cash with XOM having $32.6 billion on hand and CVX having more than $15 billion of cash. The two differ on what to do, as the CEO of XOM said Friday he is happy to hold a large surplus for the next downturn although he is not averse to a particularly good acquisition. On the other side, the CEO of CVX said he did not intend to sit on $15 billion in cash because it is economically inefficient. Wall Street is pushing both to again increase buybacks and dividends rather than spend cash on acquisitions.

In stock legal and regulatory news, an Inspector General report released Friday said that FAA Engineers recommended the grounding of 737 MAX planes (BA’s best-selling jet at the time) very soon after the second major crash in March 2019. However, FAA officials in Washington delayed the grounding despite analysis that told them there was a 25% chance of another crash within 60 days. The grounding was eventually forced and lasted 20 months. On Saturday, the Wall Street Journal reported US regulators had asked big banks for their “best and final bid” to acquire FRC. The report said that JPM and PNC have expressed interest and BAC and a few others are also considering making a bid. Bids are due Sunday and immediate action is expected. So, by the time this blog comes out, the FDIC seizure, receivership, and transfer of ownership may well have already happened. Meanwhile, the US FDA voted to allow the restricted use of an experimental prostate cancer drug from AZN. Elsewhere, ENR and WMT were sued by consumers and other retailers in three proposed class action lawsuits. The suits allege the two companies conspired to raise disposable battery prices and keep WMT as the cheapest battery offering. (If any retailer offered a lower price than WMT, the company would be cut off from ENR battery supply.) Finally, on Friday, the state of CA approved new rules that will require all new medium and heavy-duty trucks in the state to be zero emission in 2036. The rules also require existing fleets of semis, buses, garbage trucks, government fleets, etc. to be transitioned by 2039.

In banking news, as expected, late Sunday the FDIC seized FRC and then immediately sold the company to JPM. JPM beat out bids from PNC and CFG (BAC and USB were invited but did not bid). The process will cost the FDIC $13 billion (compared to $20 billion from the SIVB failure) and JPM has paid $10.6 billion. In the purchase, JPM acquired $92 billion in deposits, is taking on $173 billion in loans, and about $30 billion in securities. JPM also gains 84 branches (which will be open today).

Overnight, Asian markets were mostly in the green. Shanghai (+1.14%), Shenzhen (+1.09%), and Taiwan (+1.09%) led the gainers. Meanwhile, in Europe, we see a similar picture taking shape at midday. Six of the bourses are in the red while nine are in the green. The DAX (+0.77%), CAC (+0.10%), and FTSE (+0.50%) are leading the region higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a flat start to the day. The DIA implies a +0.01% open, the SPY is implying a -0.02% open, and the QQQ implies a -0.05% open at this hour. Meanwhile, 10-year bond yields at up to 3.458% and Oil (WTI) is down 2% to $75.25/barrel in early trading.

The major economic news events scheduled for Monday are limited to April Mfg. PMI (9:45 am) and April ISM Manufacturing PMI (10 am). Major earnings reports scheduled for the day include AMG, CHKP, CAN, BEN, GPN, KBR, NCLH, ON, PK, and WEC before the open. Then, after the close, AMKR, ANET, CAR, CF, CNO, CYH, CVI, FANG, RE, FLS, FMC, HOLX, INVH, KMT, LEG, MGM, NXPI, OGS, RYI, SBAC, SCI, SON, SFM, SYK, SGRY, TEX, RIG, VRTX, VIVI, and WWD report.

In economic news later this week, on Tuesday we get March Factory Orders, March JOLTs Job Openings, and API Weekly Crude Oil Stocks. Then Wednesday, the ADP Nonfarm Employment Change, Services PMI, April ISM Non-Mfg. PMI, EIA Crude Oil Inventories, FOMC Rate Decision, FOMC Statement, and Fed Chair Press Conference all happen. Thursday, we get March Imports, March Exports, March Trade Balance, Weekly Initial Jobless Claims, Preliminary Q1 Nonfarm Productivity, Preliminary Q1 Unit Labor Cost, the Fed Balance Sheet, and Bank Reserves with the Federal Reserve. Finally, on Friday, April Average Hourly Earnings, April Nonfarm Payrolls, April Private Nonfarm Payrolls, April Participation Rate, and the April Unemployment Rate.

So far this morning, WEC, GPN, KBR, CHKP, NCLH, PK, SOFI, L, and LKNCY all reported beats to both the revenue and earnings lines. Meanwhile, AMG missed on revenue while beating on earnings. Unfortunately, CAN missed on both the top and bottom lines. It is worth noting that GPN raised its forward guidance.

With that background, it looks like the market is looking to open just on the red side of flat. All three major indices are above their 3ema, T-line (8ema), and 17ema…all of which are also trending higher. SPY and DIA are dealing with a resistance level right near the Friday close. However, immediate resistance for QQQ is less than obvious. Over-extension is not yet a problem in any of the major indices. Moreover, with the Fed decision on its way Wednesday and a ton of earnings this week, it is quite possible that a good part of the next five days will be in “wait and see” mode. The Fedwatch tool tells us that confidence in a 0.25% rate hike by the Fed remains high at an 86+% probability. The other 14% probability is for “no hike.” Beyond next week, futures currently see little (28% on the largest probability month) chance of an additional increase this year and most are actually still betting on rate decreases sometime in the Fall. (That would be against what the Fed has repeatedly said, but that is what the Fed Fund Futures tell us.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Friday was another big tech-buying party as the sharp rally pushed the SP-500 up 0.9% in just two trading days. With the FRC takeover by JPM as regional bank worries continue, an FOMC rate decision Wednesday, and Apple’s earnings slated for Thursday afternoon expect another week of emotionally charged price swings. Goldman is warning that the CTA’s could be ready to sell off as much as 200 billion of stock holdings. If that occurs expect some big point moves as fear can trigger a rush for the door to protect gains. Buckle up it could be a wild week ahead!

With some Asian markets closed for Labor Day the Nikkei lead the buying by 0.92% with Australia also in a bullish mood. European markets trade mixed but mostly higher this morning with modest gains and losses as banking worries continue. With manufacturing data pending and a slew of earnings U.S. futures trade mixed and flat this morning perhaps suffering from buying hangover after the buying party last week as we wait on the FOMC decision.

JPMorgan Chase, the largest bank in the US, has acquired First Republic Bank, the fourth bank to fail this year, in a deal brokered by the Federal Deposit Insurance Corporation (FDIC). The deal will allow JPMorgan to assume all the deposits and most of the assets of First Republic, which had about $229 billion in total assets and $104 billion in total deposits as of April 13, 2023. First Republic’s 84 offices in eight states will reopen as branches of JPMorgan today. The FDIC said the deal avoids the agency having to use its emergency powers and minimizes disruptions for customers and loan borrowers. The takeover follows the collapse of Silicon Valley Bank and Signature Bank in March, which sparked fears of a wider banking crisis.

Charlie Munger, the vice chairman of Berkshire Hathaway and a legendary investor, has sounded a warning on the U.S. commercial property market, which he said is facing trouble due to bad loans and falling prices. Munger told the Financial Times that U.S. banks have made many risky loans to commercial property owners, such as office buildings and shopping centers, that may not be able to repay them as the demand for such properties declines amid the pandemic and changing consumer habits. Munger said that while the situation is not as bad as the 2008 financial crisis, it still poses a threat to the stability of the banking system and the economy. He also said that Berkshire Hathaway has been cautious about investing in banks because of these uncertainties.

The indexes continued their sharp rally on Friday, with the SP-500 adding 0.8% to its 2.0% surge on Thursday and ending the week with a 0.9% gain. Amazon’s warning of slowing growth in its cloud-computing segment was no match for hungry bulls willing to buy up the tech giants seemly at any cost. First Republic Bank, which plunged 49% on Friday and 95% for the week was taken over by JPM in a deal late Sunday yet more regional banks suffering massive outflows are still in question. Today trades face a possible hangover from Friday’s buying party as well as PMI, ISM, Construction Spending, and a slew of earnings reports. The FED’s May rate decision comes Wednesday afternoon and next tech giant Apple will report Thursday afternoon this week so plan on price volatility as we wait.

Thursday belonged to the Bulls as we opened higher (gapping up 0.57% in the SPY, up 0.37% in the DIA, and up 1.27% in the QQQ). After that, a long, steady rally kicked in, carrying all three major indices to new highs all day long. This action gave us gap-up, large white-bodied candles in the DIA, SPY, and QQQ. In fact, all three indices printed their largest gains in months as all three major indices also crossed back above their T-line (8ema). In fact, if you were a little loose with the definitions, you could even say the SPY and DIA printed Morning Star signals while the QQQ printed a Bull Kicker signal. However, again this happened on less-than-average volume.

On the day, all 10 sectors were in the green with Consumer Cyclical (+2.27%) leading the way higher and Energy (+0.28%) lagging behind the other sectors. At the same time, the SPY gained 1.99%, DIA gained 1.58%, and QQQ gained 2.72%. VXX fell 4.34% to 39.43 and T2122 popped out of the oversold territory and into the mid-range at 59.12. 10-year bond yields rose to 3.526 while Oil (WTI) gain 0.61% to $74.77 per barrel. So, the cumulative effect of strong earnings, especially in the big tech names, overcame fear over regional banks and recession…at least for a day.

In economic news, Preliminary Q1 GDP came in far short of expectations at +1.1% (compared to a forecast of +2.0% and a Q4 GDP of +2.6%). In addition, the GDP Price Index (Preliminary) came in hotter than expected at +4.0% (versus a forecast of +3.7% and a Q4 value of +3.9%). This tells us that the +1.1% GDP number is actually artificially high due to inflation. If you are a “glass half empty” kind of person, you’d say that means we’re heading into stagflation…inflation is higher than expected and growth is smaller than expected. However, personally, I choose to look at this as the Fed is going to see GDP growth slowing quickly and believe that they have done enough to ease inflation with the rest just being a matter of time. At the same time, Weekly Initial Jobless Claims came in below expectations at 230k (compared to a forecast of 248k and the prior week’s 246k reading). Then after the close, the Fed reported its Balance Sheet had shrunk slightly from $8.593 trillion to $8.563 trillion. The Reserve Balances of Banks with the Fed also shrunk from $3.165 trillion to $3.132 trillion.

In stock news, LYFT said Thursday that it will lay off “about” 1,072 employees (26% of its workforce) in the first step of new CEO Risher’s cost-cutting program. At midday, JNJ announced it will indemnify its newly-formed consumer health unit Kenvue of all costs and liability related to talc litigation in the US and Canada. (As reported here in previous days, JNJ intends to IPO Kenvue while retaining vast majority ownership.) Elsewhere, HMC announced it is investing about $3 billion in a partnership formed with another Japanese company to produce batteries for electric vehicles and homes. In an unrelated announcement, HMC announced $2.7 million in funding for environmental and conservation education initiatives in the US. Meanwhile, Reuters reports that META has merged its advertising, business messaging, and commerce departments into one division as part of the broader cost-cutting program. There was no word on any related staff reductions yet. Executives at large drugmakers told Reuters Thursday that they are searching for acquisition and ramping up research spending as their future profit pipelines are drying up (current drugs will face patent sundown). The companies cited are MRK, AZN, ABBV, LLY, and BMY. Finally, the USDA reported that flooding in the upper Midwest (due to record winter snowfalls that are now melting) will wreak havoc on the Mississippi River. This will halt barge traffic for weeks to come. (60% of US grain exports and a similar percentage of US fertilizer shipments normally use that waterway in their supply chain. This will cause shippers to find alternate, more costly transportation such as rail and trucking.

In stock legal and regulatory news, MA reported that it is under investigation by the US Dept. of Justice related to its practices on US debit cards and its competition against other payment networks for those accounts. (V revealed a similar probe in January.) Meanwhile, a US Appeals Court ruled in favor of META, rejecting the appeal of states Attorneys General who had sought to revive an antitrust case against the social media giant. The court stated the reason for the ruling was that the states had waited too long to file suit. Finally, when pushed on the matter of FRC, both the White House and Treasury Sec. Yellen told reporters that they, the FDIC, Fed, and state bank regulators in several states are keeping a close eye on the bank’s finances. Even after repeated questions, both the White House Press Sec. and Treasury Sec. Yellen did not offer an opinion on whether FRC depositors of amounts greater than $250,000 should be covered in the event of a bank run. However, they did say they have a track record of acting swiftly and decisively on such matters.

After the close, AMZN, HTHIY, MDLZ, X, WY, MHK, RSG, AJG, SKX, CC, GFL, RMD, ATR, SKYW, ALSN, DXCM, PINS, ACA, BZH, PEAK, MTX, EHC, ERIE, and AEM reported beats on both the revenue and earnings lines. Meanwhile, TMUS, INT, HIG, AMGN, EMN, LPLA, HUBG, CINF, DLR, SM, and SNAP missed on revenue while beating on earnings. On the other side, INTC, DNZOY, COF, GILD, LHX, PFG, FE, ATVI, SSNC, COLM, SAM, SGEN, and SSB all beat on revenue while missing on earnings. Unfortunately, OLN, CSL, and FLSR missed on both the top and bottom lines. It is worth noting that MDLZ, SKX, ATR, and ALSN all raised their forward guidance. However, INTC and HUBG both lowered their forward guidance. Finally, it is worth noting that INTC reported the largest quarterly loss in company history.

Overnight, Asian markets leaned heavily to the green side. Japan (+1.40%), Shanghai (+1.14%), Taiwan (+1.09%), and Shenzhen (+1.09%) led the region higher. In Europe, the bourses are mostly in the red in late-morning trade. The CAC (-0.62%), DAX (-0.19%), and FTSE (-0.22%) are leading the region modestly lower going into lunch. In the US, as of 6:45 am, Futures are pointing toward a modestly red start to the day. The DIA implies a -0.29% open, the SPY is implying a -0.31% open, and the QQQ implies a -0.26% open at this hour. At the same time, 10-year bond yields are back down to 3.481% as money seeks safe harbor and Oil (WTI) is up just less than four-tenths of a percent to $75.02/barrel in very early trading.

The major economic news events scheduled for Q1 Employment Cost Index, March PCE Price Index, and March Personal Spending (all at 8:30 am), Chicago PMI (9:45 am), and Michigan Consumer Sentiment (10 am). Major earnings reports scheduled for the day include AON, ARCB, ARES, AVTR, BLMN, CCJ, GTLS, CHTR, CVX, CL, DAN, XOM, FMX, GNTX, IMO, JKS, LAZ, LYB, NYCB, NWL, NHYDY, NVT, POR, SAIA, and TRP before the open. There are no reports scheduled for after the close.

So far this morning, XOM, CVX, SONY, MBGAF (Daimler), KMTUY (Komatsu), ELUXY (Electrolux), CRI, BBVA, CL, TRP, BLMN, POR, and NVT all reported beats on the revenue and earnings lines. Meanwhile, LYB, GTLS, and CCJ missed on revenue while beating on earnings. On the other side, AON, NWL, ARES, CHTR, and APELY beat on revenue while missing on earnings. Unfortunately, ARCB and LAZ missed on both the top and bottom lines.

With that background, it looks like the large caps are going back to test their T-lines (8ema) as support early this morning. If the Bulls are going to follow through on Thursday’s strong candles, they’ll need to work for it after AMZN reported a blowout quarter but then put a damper on the party by warning about cloud services growth. That combined with INTC getting slaughtered (worst quarterly loss ever) has the big tech names (long the market leaders) feeling a little blu (make that red) this morning. However, that is tempered a bit by yet another record quarterly profit from XOM. Over-extension is not a problem based on either the T-line or the T2122 indicator. Interestingly, the Fedwatch tool tells us that confidence in a 0.25% rate hike by the Fed next week has resurged since yesterday morning. We are now back up to an 85% probability of that, with the other 15% probability being “no hike.” Beyond next week, markets see very little (21%) chance of an additional increase this year and most are actually betting on rate decreases sometime in the Fall. (That would be against what the Fed has repeatedly said, but that is what the Fed Fund Futures tell us.) Right now, the Bulls have work to do (resistance to overcome) but the ball is in their court. Finally, don’t forget it’s Friday. Get your account ready for the weekend news cycle.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With earnings as the focal point indexes surged on Thursday as investors averted their eyes from the regional banking crisis. Unfortunately, the situation seems to have worsened for FRC over the last 24 hours and some suggest an action by the Fed may be required as soon as this weekend. The very bullish reaction to the initial AMZN and INTC earnings seems to have tempered after the conference calls. Today we have fewer earnings events but have several potential market-moving economic reports highlighting the Feds favored core PCE number before the bell. Buckle up it could be a wild Friday session.

Asian market surged higher in overnight trading as Japan keeps monetary policy unchanged weakening the Yen. However, European indexes see only red this morning after a 0.1% GPD number with sinking bank prices raising concerns. With bank worries back in focus this morning and tempered excitement from after-the-bell earnings reports U.S. futures point to bearish open.

Amazon, the e-commerce giant and cloud leader, reported its first quarter earnings for 2023 on Thursday, April 28. The company beat analyst expectations on both revenue and profit, posting $127.4 billion in revenue and $3.2 billion in profit, or 31 cents per share. However, the company also warned of a slowdown in its cloud segment AWS, which grew 16% year-over-year, compared to 37% in the same period last year. Amazon’s online retail business also saw no growth in the first quarter, as shoppers became more cautious and less reliant on e-commerce amid the pandemic. Amazon’s stock rose 9% in after-hours trading following the earnings release.

Intel, the semiconductor giant, and PC chip leader, reported its first-quarter earnings for 2023 on Wednesday, April 27. The company reported the largest quarterly loss in its history, losing $2.8 billion, or 66 cents per share, compared to a profit of $8.1 billion, or $1.98 per share, a year ago. Revenue fell nearly 36% year over year to $11.7 billion, as the company faced fierce competition from rivals like AMD and Nvidia, as well as supply chain challenges and a global chip shortage. Intel also lowered its full-year guidance, expecting to lose $2.30 per share on revenue of $65 billion to $68 billion. Intel’s stock dropped 5% in after-hours trading following the earnings release.

The U.S. stock market earnings as the focal point, and tech companies have been delivering strong results that have boosted investor confidence and key indexes. Microsoft and Alphabet surprised the market with their earnings yesterday, and META followed suit today with a beat that sent its shares up 14%. The earnings season is not over yet, and Amazon could be the next big mover when it reports later today. The U.S. economy, however, is slowing down, according to the GDP report released this morning. This suggests that the Fed will not raise rates much more, but also that it will not cut them soon either, as inflation remains high.

Markets diverged at the open on Wednesday, as SPY gapped up 0.15%, DIA opened 0.07% higher but QQQ gapped up 1.13% on the strong tech earnings from Tuesday night. All three major indices then ground sideways for 30 minutes. Then the whipsaw began. All three made a 15-minute selloff followed by a rally for an hour and 40 minutes, reaching the highs of the day at about 12:10 and then a protracted selloff that took us to the lows of the day at 3:50 pm before bouncing the last 10 minutes. This action gave us large, black-bodied candles again but this time with larger upper wicks and smaller lower wicks. And, once again, this happened on less-than-average volume in the SPY, DIA, and QQQ.

On the day, eight of the 10 sectors were in the red with Utilities (-2.06%) leading the way lower and Technology (+0.40%) holding up better than the other sectors. This is very odd on a down day in the market. At the same time, the SPY lost 0.42%, DIA lost 0.71%, and QQQ gained 0.58%. VXX fell 2.5% to 41.22 and T2122 dropped further into the oversold territory at 7.96. 10-year bond yields rose to 3.441% (again, odd for a day when the large-cap indices fell) while Oil (WTI) plummeted another 3.62% to $74.30 per barrel. So, fear over regional banks (based apparently exclusively on FRC Q1 deposit withdrawals) overrode generally strong earnings by major companies. The market just seems skittish, perhaps waiting on the Fed’s favorite inflation index PCE Price Index on Friday (ahead of the FOMC meeting next week).

In economic news, March Durable Goods orders increased far more than expected at +3.2% month-on-month (compared to a forecast of +0.7% and the February reading of -1.2%). At the same time, the Preliminary March Goods Trade Balance showed a lower-than-expected deficit at -$84.60 billion (versus the forecast of -$89.00 billion and well better than the February value of -$91.99 billion). In addition, the Preliminary March Retail Inventories grew more than expected at +0.4% (compared to a forecast of +0.1% and a February reading of -0.1%). Later in the day, the EIA Weekly Crude Oil Inventories reported a much greater-than-expected drawdown of 5.054-million-barrels (versus a forecast for a 1.486-million-barrel drawdown and even more than the prior week’s 4.581-million-barrel inventory reduction). As with the API report numbers on Tuesday evening, this was the fourth drawdown in the last five weeks.

In stock news, early Wednesday, the UK officially blocked the MSFT purchase of ATVI. This caused ATVI to gap down 9% and end the day down 11.45%. Later, STLA offered 33,500 US employees (2,500 salaried and 31,000 hourly) voluntary buyout packages. At the same time, a Jefferies analyst reported that LOW is revamping its stores in an attempt to focus on rural America. The refresh is apparently aimed at imitating TSCO. Elsewhere, Reuters reported that TSN told employees Wednesday it is planning to eliminate 10% of corporate jobs (about 600) and 15% of executive roles. Just before the close, it was reported that US bank regulators are considering downgrading their assessment of FRC. This would potentially limit FRC’s ability to borrow from the Fed. This comes after the FDIC has given the bank weeks to reach private deals to shore up its finances but FRC has been unable to reach such deals. Meanwhile, after the close, the CEO of BMY stepped down and it was announced he will be replaced with current COO Boerner on November 1. (BMY reports Thursday.)

In stock legal and regulatory news, an NRLB Administrative Judge ruled Wednesday that TSLA supervisors had broken US Labor Law by ordering employees at a Florida TSLA Service Center not to discuss pay, working conditions, or other complaints with higher-level management. A “cease and desist” order was immediately filed with any fines to be determined later in the process. Elsewhere, DIS filed a federal lawsuit against Florida Governor DeSantis over his effort to exert control over DIS theme parks in that state. (DeSantis had his hand-picked board vote to throw out a long-term legal contract DIS signed with the prior board, outsmarting the Governor’s effort to take control of the board and punish DIS for speaking out against his cultural agenda.) Later, UBER won when a panel of US Circuit Court of Appeals judges ruled that UBER drivers are not exempt from a law requiring them to take legal disputes to private arbitration rather than join class-action lawsuits. (This means UBER drivers around the country cannot join a class-action suit brought charging that they were misclassified as contractors and are due overtime pay and work-related expense reimbursement.)

After the close, META, PXD, AFL, WM, PPC, ORLY, MKL, EBAY, KLAC, LSTR, RHI, NOW, WCN, CACI, CLS, NOV, EW, MTH, TNET, MEOH, AB, MAT, CCS, ALGN, NLY, TROX, PLXS, FIX, TER, IEX, ROKU, ENSG, CMPR, NLY, MYRG, ACHC, AVB, ROL, HELE, EQT, TDOC, SUI, BMRN, WSC, PTC, GGG, SLM, MAA, TYL, CHDN, COLB, FBIN, KALU, MORN, and NEU all reported beats on both the revenue and earnings lines. Meanwhile, MOH, ACGL, ICLR, AXS, SAVE, STC, ESI, and SNBR all missed on revenue while beating on earnings. On the other side, RJF, URI, AR, CHE, OII, and AWK all beat on revenue while missing on earnings. Unfortunately, CHRW, TA, CP, and ASGN all missed on both the top and bottom lines. It is worth noting that CACI, ALGN, and TER raised their forward guidance. However, IEX lowered its guidance.

Overnight, Asian markets were mixed. Thailand (-0.82%), Singapore (-0.36%), and Australia (-0.32%) paced the losses while Shanghai (+0.67%), India (+0.57%), and Hong Kong (+0.42%) led the gainers. Meanwhile, in Europe, we see a similar picture taking shape at midday. The CAC (+0.30%), DAX (+0.09%), and FTSE (-0.02%) lead the region on volume and market cap while the smaller exchanges have made larger moves. In the US, as of 7:30 am, Futures are pointing toward a gap higher to start the day. The DIA implies a +0.47% open, the SPY is implying a +0.61% open, and the QQQ implies a +0.93% open at this hour. At the same time, 10-year bond yields are up slightly to 3.454% and Oil (WTI) is flat at $74.25/barrel in early trading.

The major economic news events scheduled for Thursday include Preliminary Q1 GDP and Weekly Jobless Claims (both at 8:30 am), and March Pending Home Sales (10 am). The major earnings reports scheduled for the day include AOS, ABBV, MO, AAL, AIT, ARCH, AMBP, AZN, BAX, BFH, BMY, BC, CRS, CARR, CAT, CBRE, CNP, CHD, CMS, CNX, CMCSA, CROX, CRF, DQ, DPZ, DTE, LLY, EME, FIS, FAF, FCFS, FCN, GOL, HOG, HAS, HP, HSY, HTZ, HGV, HON, IP, IPG, IQV, KDP, KEX, LEA, LII, LECO, LIN, LKQ, HZO, MA, MRK, NEM, NOC, ORI, OSK, PATK, PTEN, BTU, PNR, DGX, RS, ROK, ROP, SPGI, SNY, SNDR, SIRI, SAH, SO, LUV, SAVE, SRCL, STM, FTI, TXT, TTE, TSCO, TPH, VLO, VLY, VC, GWW, WST, WEX, WTW, WIT, and XEL before the open. Then, after the close, ATVI, AEM, ALSN, AMZN, AMGN, ATR, ACA, AJG, BZH, COF, CSL, SS, SINF, COLM, DXCM, DLR, EMN, EHC, ERIE, FLSR, FE, GFL, GILD, HIG, PEAK, HUBG, INTC, LHX, LPLA, MTX, MHK, MDLZ, OLN, PINS, PFG, RSG, RMD, SGEN, SKX, SKYW, SM, SNAP, AWN, SSNC, TMUS, X, WY, and INT report.

In economic news later this week, on Friday, Q1 Employment Cost Index, March PCE Price Index, March Personal Spending, Chicago PMI, and Michigan Consumer Sentiment.

In terms of earnings reports later this week, on Friday, AON, ARCB, ARES, AVTR, BLMN, CCJ, GTLS, CHTR, CVX, CL, DAN, XOM, FMX, GNTX, IMO, JKS, LAZ, LYB, NYCB, NWL, NHYDY, NVT, POR, SAIA, and TRP report.

So far this morning, CAT, VLO, MRK, HON, OSTK, HSY, KEX, NOC, AZN, CMCSA, KDP, TAL, OSK, PTEN, SO, AOS, LIN, STM, TXT, IP, CNP, ROP, LII, PNR, CHD, DGX, FCFSCNX, RS, ROK, XEL, CBRE, BC, AIT, TPH, LEA, WEX, LKQ, BFH, CBZ, FIS, WST, TTE, WTW, SRCL, CROX, HOG, SPGI, and BAX all reported beats on both the revenue and earnings lines. Meanwhile, AAL, BMY, SNY, CMS, FAF, ASX, BCS, NEM, DTE, and MBLY all missed on revenue while beating on earnings. On the other side, LLY, HAS, IQV, ARCH, VC, FTI, and VLY all beat on revenue while missing on earnings. Unfortunately, LUV, DQ, TSCO, SAH, and HZO missed on both the top and bottom lines. It is worth noting that LLY HSY, BAX, ROP, PNR, and WST raised their forward guidance. However, HZO lowered its forward guidance.

With that background, it looks like the Bulls are going to make a run to start the day. The QQQ seems set to gap up to retest its T-line (8ema) and the DIA is not far behind at this point in the premarket. Over-extension is not a problem based on T-line but we are well oversold according to the T2122 indicator. Interestingly, the Fedwatch tool tells us that confidence in a 0.25% rate hike by the Fed next week continues to fade a bit. We are now down to a 76% probability of that, with the other 24% probability being “no hike.” Right now, the chart tells us the bias has flipped bearish after uptrends were broken. However, we aren’t far from the consolidation range, and with good earnings to give them energy, the bulls are not likely to give in easily.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service