U.S. stock futures climbed early Monday as investors geared up for a week packed with economic data and awaited potential new tariff announcements from President Donald Trump. In the premarket, steel and aluminum stocks surged, with U.S. Steel and Nucor both gaining 8%, Cleveland-Cliffs up 9%, and Alcoa trading 4% higher. The looming threat of additional tariffs came as investors prepared for several key economic reports, including January’s consumer price index on Wednesday, followed by initial weekly jobless claims and the producer price index on Thursday. Federal Reserve Chair Jerome Powell was also set to address Congress on Monday morning. Investors anticipated major corporate earnings reports from McDonald’s on Monday and Coca-Cola on Tuesday.

European stock markets kicked off the week positively, with the pan-European Stoxx 600 rising 0.35% at the open. Key regional indexes, including the U.K.’s FTSE 100, Germany’s DAX, France’s CAC 40, and Italy’s MIB, all saw a 0.3% increase at the start of trading. BP shares surged over 8% following news of an activist investor Elliott Management’s stake in the company. Thyssenkrupp, one of Europe’s leading steelmakers, stated it expects a “very limited impact” on its business if the U.S. imposes additional tariffs on steel and aluminum imports. The company emphasized that Europe remains its primary market, and it only exports high-quality niche products to the U.S., where it maintains a solid market position.

Asia-Pacific markets presented a mixed performance on Monday amid ongoing trade tensions, leaving investors cautious. Japan’s benchmark Nikkei 225 remained flat, while the Topix index saw a slight decline of 0.15%. The country reported a 3% year-on-year loan growth in January, down from December’s 3.1%. In South Korea, the Kospi closed unchanged, but the small-cap Kosdaq gained 0.91%. China’s CSI 300 Index edged up by 0.21%, with the Hang Seng index in Hong Kong rising significantly by 1.76%. China’s consumer inflation reached a five-month high in January. Conversely, in India, the Nifty 50 index dropped by 0.91%, and the BSE Sensex index fell by 0.87% following the Reserve Bank of India’s anticipated interest rate cut, marking the first reduction in five years.

Economic Calendar

Earnings Calendar

Notable reports for Monday before the bell include CNA, EPC, HAIN, INCY, MCD, MNDY, ON, ROK, ROIV, TSEM, & TGI.

After the bell reports include AMKR, ACGL, ARWR, ALB, ACLS, BTG, BRX, CINF, CMCO, CMP, CXW, COTY, FLNC, HLTI, INSP, KRC, LSCC, MEDP, MITK, SSD, SPSC, VRTX, VNO, & WTS.

News & Technicals’

The Consumer Financial Protection Bureau (CFPB) instructed its employees to work remotely until February 14th due to the closure of its Washington, D.C., headquarters, as per a memo from CFPB Chief Operating Officer Adam Martinez. This directive follows an email from the newly appointed acting director Russell Vought, who on Saturday ordered the suspension of almost all regulatory activities, including the supervision of financial firms. Additionally, Vought announced on social media that he was cutting off fresh funding to the agency, criticizing its past lack of accountability.

On Sunday, U.S. President Donald Trump announced plans to impose new 25% tariffs on steel and aluminum imports, adding to the existing duties, though no timeline for implementation was provided. These metals are essential in industries such as transportation, construction, and packaging. During his first term, Trump had already imposed tariffs on steel and aluminum imports from Canada, Mexico, and the EU, along with volume restrictions on imports from countries like South Korea, Argentina, and Australia. A Congressional Research Service report revealed that in the first five months of this policy, the Trump administration generated over $1.4 billion in revenue from these tariffs.

New projections for the federal Pell Grant program indicate a potential $2.7 billion funding shortfall later this year. Pell Grants, a crucial source of financial aid for low-income families, support approximately 40% of college students. Michele Zampini, senior director of College Affordability at The Institute for College Access & Success, warned that without additional funding, students might experience eligibility or funding cuts for the first time in over a decade.

Mega cap technology companies are set to significantly increase their investment in artificial intelligence and datacenter buildouts in 2025, with planned expenditures reaching $320 billion. Meta, Amazon, Alphabet, and Microsoft have all outlined ambitious spending initiatives based on recent comments from their CEOs. This figure marks a substantial rise from the $230 billion spent in 2024. Amazon has the most aggressive investment plan, with CEO Andy Jassy announcing the company aims to allocate over $100 billion, up from $83 billion the previous year. The funds will primarily support AI developments within Amazon Web Services, which Jassy describes as a “once-in-a-lifetime business opportunity.”

Monday gives us a data break but the rest of the we should expect price volatility with a week packed with economic data. Toss in the threat of new tariffs and we have a recipe for significant uncertainty. Bonds are already moving slightly higher with the worry of inflation so plan carefully and be prepared for some big point swing as we move through the week.

Markets opened slightly higher before the Bears stepped in. SPY gapped up 0.10%, DIA opened 0.07% higher, and QQQ opened 0.09% higher. All three major index ETFs then followed-through to the upside for 30 minutes. However, then President Trump announced he is planning reciprocal tariffs on US trading partners, which he will announce next week. (In other words, meaning we are likely to see across-the-board tariffs.) That caused the entire market to sell off fast at first and then just steadily the rest of the day. This action gave us large black-bodied candles with modest upper wicks, which crossed back below their T-line (8ema) in all three major index ETFs. SPY and QQQ printed Bearish Engulfing candles in the process. This happened on just below average volume in all three index ETF.

On the day, all 10 of the sectors were in the red with Consumer Cyclical (-1.40%), Basic Materials (-1.08%), and Healthcare (-1.01%) leading the market lower. On the other side, Energy (-0.21%) and Utilities (-0.28%) holding up better than other sectors. At the same time, SPY lost 0.90%, DIA lost 0.95%, and QQQ lost 1.26%. Meanwhile VXX popped 3.36% to close at 43.96 while T2122 dropped back into the lower half of its mid-range, closing at 36.78. On the bond side, 10-Year Bond yields rose to close at 4.487% and Oil (WTI) gained 0.51%, closing at $70.97 per barrel. So, Friday saw very modest gains on January Payroll data, which was then crushed by Trump talk and his proposed protectionism.

The major economic news on Friday included January Month-on-Month Avg. Hourly Earnings, which came in sharply higher at +0.5% (compared to a +0.3% forecast and December reading). On an annual basis, January Year-on-Year Avg. Hourly Earnings, stayed flat at +4.1% (versus a predicted lower +3.8% but in-line with December’s 4.1% value). For the headline number, Jan. Nonfarm Payrolls were down at +143k (versus a +169k forecast and far down from December’s +307k reading). On the private side, Jan. Private Nonfarm Payrolls were also sharply lower at +111k (compared to a +141k forecast and much lower than December’s +273k number). The January Participation Rate rose a tick to 62.6% (versus December’s 62.5%). Altogether, this gave us a Jan. Unemployment Rate which fell to 4.0% (versus a 4.1% forecast and December value). Later, Michigan Consumer Sentiment fell to 67.8 (compared to a 71.9 forecast and the January 71.1 reading). On the forward-looking side, Michigan Consumer Expectations were also down to 67.3 (versus a 70.0 forecast and 69.3 January value). In terms of inflation outlook, the Michigan 1-Year Inflation Expectations SKYROCKETED to +4.3% (up a full percent from the 3.3% forecast and January reading). Looking further out, the Michigan 5-Year Inflation Expectations increase was less, now at 3.3% (up a tick from the 3.2% forecast and January value). Later, December Consumer Credit spiked massively to $40.85 billion (dramatically higher than the $17.70 billion forecast and November’s -$5.37 billion number).

In Fed news, on Friday, Minneapolis Fed President Kashkari told CNBC he expects the Fed Funds rate to be “modestly lower” by the end of 2025. However, he said that for now the FOMC is in “wait and see” mode due to the uncertainty caused by the Trump administration policies (mainly tariffs since immigration arrests and deportations are on the same pace as the Obama administration). Kashkari said, “we’re in a very good place to just sit here until we get a lot more information on the tariff front, on the immigration front, on the tax front, etc.” He continued, “Barring something really surprising on the tariff front, immigration front, or fiscal policy front — so taking off some extreme outcomes there — I think inflation will continue to come down over this year.” At the same time, Fed Governor Kugler said she also feels there is “considerable uncertainty about the economic impact of new policy proposals.” She went on to say, “The prudent step is to hold the federal funds rate where it is for some time, given that combination of factors.”

Overnight, Asian markets were mixed with six in the red, five in the green, and one unchanged. Hong Kong (+1.84%) leading the gainers while Taiwan (-0.96%) and Thailand (-0.90%) paced the losses. In Europe, we see a brighter picture taking shape at midday with 11 of the 14 bourses in the green. The CAC (+0.23%), DAX (+0.22%), and FTSE (+0.60%) lead the region higher in early afternoon trade. Meanwhile, in the US, as of 7:15 a.m., Futures are pointing toward a green start to the day. DIA implies a +0.37% open, the SPY is implying a +0.44% open, and QQQ implies a +0.69% open at this hour. At the same time, 10-Year Bond Yields are up slightly to 4.497% and Oil (WTI) is up 1.31% to $71.93 per barrel in early trading.

There is no major economic news scheduled for Monday. The major earnings reports scheduled for before the open include CNA, INCY, NSP, MCD, ON, and ROK. Then after the close, AMKR, ACGL, CINF, CMP, COTY, BAP, MEDP, NGL, VRTX, and WTS report.

In economic news later this week, on Tuesday we get the API Weekly Crude Stocks report. Fed Chair Powell also testifies and Fed member Williams speaks. Then Wednesday, January Core CPI, January CPI, EIA Weekly Crude Oil Inventories and the January Federal Budget Balance are reported. Fed Chair Powell also testifies and Fed member Bostic reports. On Thursday, we get Weekly Initial jobless Claims, Weekly Continuing Jobless Claims, January Core PPI, January PPI, and the Fed’s Balance Sheet. Finally, on Friday, Jan. Core Retail Sales, Jan. Retail Sales, Jan. Export Price Index, Jan. Import Price Index, Jan. Industrial Production, Dec. Business Inventories, and Dec. Retail Inventories are reported.

In terms of earnings reports later this week, on Tuesday we hear from AN, BP, CG, CARR, KO, DD, ECL, FIS, GFS, HUM, LCII, LDOS, MAR, MAS, RPRX, SPGI, SHOP, SUN, WCC, KLG, ALSN, AMX, AIG, AIZ, BHF, BN, DASH, EW, ET, ES, ECG, EXEL, GILD, IAC, LYFT, MCY, PBI, PRI, ST, WELL, ZG, and Z. Then Wednesday, GOLD, BIIB, BAM, CHEF, CME, CNDT, CVS, DBD, D, EXC, GNRC, IPG, KHC, LAD, MLM, COOP, NI, QSR, R, SITE, SW, SAH, SPTN, TMHC, THC, VRT, WAB, WAT, ALB, AR, APP, CSCO, CPA, CRBG, CW, EIX, EQIX, FAF, GXO, HUBS, KGC, MTW, MGM, MKSI, MSA, NBR, PPC, QDEL, HOOD, ROL, RGLD, SCI, SLF, TTD, TSE, TROX, TYL, VTR, WCN, WFG, and WMB report. On Thursday, we hear from ALNY, ATUS, AEP, HOUS, AVNT, CBRE, CROX, DDOG, DE, DTE, DUK, GEHC, GPN, HBI, HRI, HTZ, HMC, HWM, H, IRM, KNF, LECO, TAP, MCO, DNOW, OGN, PBF, PAG, PCG, PHIN, PPL, SBH, SN, SONY, TU, TIXT, TRU, USFD, WEN, YETI, ZBRA, ZTS, AEM, AL, ABNB, AMAT, BIO, BFAM, CAE, COIN, DVA, DXCM, DLR, DKNG, GDDY, IR, LEG, MSI, PANW, RSG, ROKU, TWLO, and WYNN. Finally, on Friday, AMCX, AEE, AXL, BGC, ENB, FTS, MGA, MRNA, NMRK, POR, TRP, and THS report.

So far this morning, CAN, L, and ROK have reported beats on both the revenue and earnings lines. Meanwhile, INCY beat on revenue while missing on earnings. However, EPC and MCD missed on both the top and bottom lines.

With that background, it looks like the market is modestly positive in the early premarket. All three major index ETFs opened higher and have printed white-bodied candles since that point in the early session. SPY gapped back above its T-line (8ema), but retested it from above and has, so far, passed that test. However, it is printing a tiny hammer candle. QQQ similarly gapped back above its T-line, has retested from above and has passed that test. However, it has printed a long-handle (wide-range) Hammer in the early session. Meanwhile, DIA made the smallest gap up and remains just below its T-line. However, it has printed the strongest premarket candle a White Marubozu (Shaved Head) candle that has just not quite reached its T-line from below. So, the short-term trend is mixed but leans slightly bullish this morning. The mid-term downtrend (if you want to call it a trend) remains a choppy mess. In terms of extension, as mentioned, all three are back close to their T-line. Meanwhile, T2122 sits in the bottom half of its mid-range. So, both sides have room to work today if they can find momentum. In terms of the Big Dogs, nine of the 10 are in the green with META (+0.75%), NFLX (+0.73%), and GOOGL (+0.73%) leading a tightly bunched performance. TSLA (-1.53%) I by far the biggest loser and only Big Dog in the red. As far as liquidity goes, NVDA (+0.08%) leads with TSLA right on its heels and the next-heaviest trading Big Dogs having traded only about one-seventh as much dollar-volume as TSLA.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Thursday saw a modest start and then a divergence. SPY gapped up 0.29%, DIA gapped up 0.16%, and QQQ opened 0.03% higher. From there, SPY and QQQ chopped sideways all day with one modest “selloff about 2 p.m. and then a rally back that lasted the rest of the day. Meanwhile, DIA sold off steadily until after 2:30 p.m. before it too rallied modestly the rest of the day. This action gave us white candles in the SPY and QQQ and a black candle in DIA. SPY printed something like a Dragonfly Doji that retested and bounced up off its T-line (8ema). QQQ printed a white, mostly-body candle with a modest lower wick. At the same time, DIA gave us a black-bodied Hammer-type candle that also retested and bounced up off its T-line. This happened on well-below-average volume in all three major index ETFs.

On the day, seven of the 10 of the sectors were in the green with Financial Services (+0.82%) and Consumer Defensive (+0.79%) in front leading the market higher. On the other side, the Energy (-1.39%) and Healthcare (-1.17%) were by far the biggest losers and two of the only three red sectors. At the same time, SPY gained 0.35%, DIA lost 0.28%, and QQQ gained 0.52%. Meanwhile VXX lost two-thirds of a percent to close at 42.53 while T2122 dropped back out of the overbought territory, into the top half of its mid-range, closing at 69.48. On the bond side, 10-Year Bond yields rose to close at 4.44% and Oil (WTI) dropped 0.70%, closing at $70.53 per barrel. So, Thursday was a bit of a Bear trap with a move lower, followed by a sharp reversal and the Bulls not giving up the momentum the rest of the day.

The major economic news on Thursday includes Weekly Initial Jobless Claims, which came in a bit higher than expected at 219k (compares to a forecast of 214k and the prior week’s 208k value). On the ongoing side, Weekly Continuing Jobless Claims were also higher than expected at 1,886k (versus a 1,870k forecast and the previous week’s 1,850k reading). At the same time, Preliminary Q4 Qtr.-on-Qtr. Nonfarm Productivity was down sharply to +1.2% (versus at +1.5% forecast but down sharply from Q3’s +2.3% value). On the cost side, Preliminary Q4 Qtr.-on-Qtr. Unit Labor Costs was up sharply but lower than predicted at +3.0% (compared to a+3.4% forecast and Q3’s +0.5% reading). Then, after the close, the Fed Balance Sheet showed a $7 billion decline to $6.811 trillion.

In Fed news, on Thursday, Chicago Fed President Goolsbee clarified his remarks from earlier this week. He said, “We (economy) have kind of settled in at full employment. Inflation is looking better. If conditions keep like that (they are), rates will be lower (at the end of 2025) than they are today.” However, he continued to say that uncertainty brought by Trump administration proposals (and their lack of clarity or consistency) will mean a slower pace of cuts. “The more dust we (Trump administration) throw in the air…that makes it hard for us to calibrate what the conditions actually are (and) the more we have to wait and see. We (FOMC) just want to be confident we are not overheating and that the job (reducing inflation) is in fact done.” Later, the Boston Fed released a report that said “the full suite of tariffs sought by the Trump administration would create notable upward pressure on inflation.” The reports estimate that upward inflation due to the tariffs to be as much as 0.8% (based on the PCE Index). After the close, Dallas Fed President Logan indicated she was prepared to hold the Fed Funds Rate steady (no cuts) “for quite some time”…even if inflation continues to drop closer to the FOMC’s 2% target. She said that recent data “would strongly suggest that we’re already pretty close to the neutral rate, without much near-term room for further cuts.” She indicated that she was looking at the labor market as her signal for further rate cuts, saying, “if the labor market or demand cools further, that could be evidence it’s time to ease.”

After the close, AFRM, AMZN, BYD, CNO, EHC, EXPE, LION, FTNT, G, LGF.B, MTD, MHK, MPWR, OTEX, SENEA, and SSNC all reported beats on both the revenue and earnings lines. Meanwhile, AMRK, ILMN, PINS, PFG, and ULH beat on revenue while missing on earnings. On the other side, ATR, HUBG, MTX, POST, and TTWO missed on revenue while beating on earnings. However, FBIN, MCHP, NBIX, RGA, SKX, VSAT, and WERN missed on both the top and bottom lines.

Overnight, Asian markets were mixed but leaned toward the green side. Shenzhen (+1.75%), Thailand (+1.59%), Hong Kong (+1.16%), and Shanghai (+1.10%) led the region higher. At the same time, South Korea (-0.59%) was by far the worst loser on the day. In Europe, the bourses are mixed, but lean toward the red side at midday in modest trading. The CAC (-0.09%), DAX (+0.02%), and FTSE (-0.35%) lead a mixed region in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a mixed, flat open ahead of January Payroll data. The DIA implies a +0.08% open, the SPY is implying a dead-flat open, and the QQQ implies a -0.01% open at this hour. At the same time, 10-Year Bond Yields remain at 4.44% and Oil (WTI) is up 0.75% to $71.14 per barrel in early trading.

The major economic news scheduled for Friday includes Jan. Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Private Nonfarm Payrolls, Jan. Participations Rate, and Jan. Unemployment Rate (all at 8:30 a.m.), Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations (all at 10 a.m.), and Dec. Consumer Credit (at 3 p.m.). The major earnings reports scheduled for before the open include AVTR, CBOE, ROAD, FLO, FTV, ULCC, GPRE, KIM, NWL, PAA, and PAGP. Then after the close, there are no earnings reports scheduled.

So far this morning, ROAD, KIM, and UI have reported beats on both the revenue and earnings lines. Meanwhile, AVTR, FLO, and NWL missed on revenue while beating on earnings. However, GPRE, PAA, and PAGP missed on both the top and bottom lines.

With that background, it looks like the market is undecided again this morning ahead of the January Payrolls data. All three major index ETFs are little moved from Thursday’s close and have printed small-body, white-bodied candles in the premarket. All three are above their T-line (8ema), meaning the short-term trend is bullish. The mid-term downtrend (if you want to call it a trend) remains a mess. In terms of extension, as mentioned, all three are back close above their T-line. Meanwhile, T2122 in its mid-range. So, both sides have room to work today if they can find momentum. In terms of the Big Dogs, seven of the 10 are in the red with AMZN (-2.79%) far out front leading the losses (as it is being punished for a poor forecast in Thursday night’s report). On the other side, META (+0.31%) leads the three green Big Dogs. As far as liquidity goes, NVDA (+0.15%) leads with TSLA (-0.74%) and AMZAN having traded about one-third less and then the next closest being 12 times less dollar volume. However, bear in mind that it is light premarket in terms of liquidity. Also, remember that its Friday and we need to prepare for the weekend news cycle.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The morning was a Bear trap on Wednesday. SPY gapped down 0.19%, DIA opened just on the green side of flat, and QQQ gapped down 0.50%. From there, all three major index ETFs continued to sell, reaching the lows of the day just after 10 a.m. However, that was it for the Bears. From that point, all three rallied until 11:10 a.m. At that point, DIA continued higher at the same pace while SPY drifted higher and QQQ meandered sideways. Finally, all three rallied the last 10 minutes of the day, going out very near their highs. This action gave us white-bodied candles with lower wicks in all three. They all closed above their T-line after gapping down below that level at their open. This happened on well-below-average volume in SPY, DIA, and QQQ.

On the day, nine of the 10 of the sectors were in the green with Healthcare (+1.56%) well out in front leading the market higher. On the other side, the Consumer Cyclical (-0.47%) was the laggard and only sector in the red. At the same time, SPY gained 0.41%, DIA gained 0.71%, and QQQ gained 0.45%. Meanwhile VXX lost 2.04% to close at 42.80 while T2122 gained a little to climb back inside the edge of overbought territory, closing at 81.91. On the bond side, 10-Year Bond yields fell to close at 4.426% and Oil (WTI) dropped 2.13%, closing at $71.15 per barrel. So, Wednesday was a bit of a Bear trap with a move lower, followed by a sharp reversal and the Bulls not giving up the momentum the rest of the day.

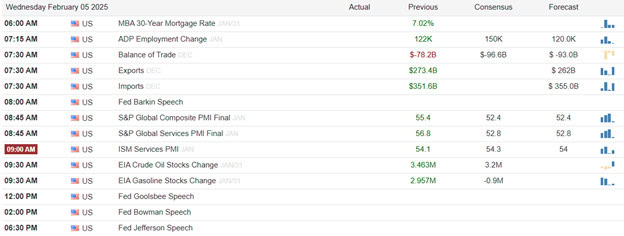

The major economic news on Wednesday included the ADP Nonfarm Employment Change, which came in much stronger than expected at +183k (compared to a +148k forecast, but not much above December’s +176k reading). At the same time, Dec. Exports were down to $266.50 billion (versus November’s $273.4 billion value). On the incoming side, Dec. Imports were up to $364.90 billion (compared to November’s $351.60 billion number). Together, this gave us a Dec. Trade Balance of -$98.40 billion (which was slightly above the -$96.50 billion forecast and well above November’s -$78.90 billion value). Later, S&P Global Services PMI was down to 52.7 (better than the 52.4 forecast but down from December’s 55.4 reading). This gave us a S&P Global Composite PMI of 52.9 (versus a 52.8 forecast but down from December’s 56.8 value). Later, ISM Non-Mfg. PMI was low at 52.8 (compared to a 54.2 forecast and December’s 54.0 reading). This came on an ISM Non-Mfg. Employment Index that was up to 52.3 (from December’s 51.3 number). On the cost side, the ISM Non-Mfg. Price Index were well down to 60.4 (versus the 64.4 December reading). Later, the EIA Weekly Crude Oil Inventories showed a MUCH larger-than-expected 8.664-million-barrel inventory build (compared to a 2.400-million-barrel forecasted increase and the prior week’s 3.463-million-barrel increase).

In Fed news, on Wednesday, Chicago Fed President Goolsbee warned about the potential inflationary impacts of tariffs. He said, “We now face a series of new challenges to the supply chain – natural and man-made disasters from fires and hurricanes to collisions with bridges that take out major ports, canal cloggings and threats of dockworker walkouts; geopolitical disruptions; immigration; and, of course, the threat of large tariffs and the potential for an escalating trade war.” He continued, “If we see inflation rising or progress stalling in 2025, the Fed will be in the difficult position of trying to figure out if the inflation is coming from overheating or if it’s coming from tariffs.” He went on, “If in 2018 companies shifted all the easiest things out of China, then what’s left might be the least substitutable goods… In that case, the impact on inflation might be much larger this time.” Meanwhile, Richmond Fed President Barkin also talked about the uncertainty brought by Trump tariff policy and flip-flopping. He said, “it remains impossible at this early stage to know where cost increases from any tariffs might be absorbed or passed along to consumers.”

After the close, ARM, CENT, CTSH, COHR, ENSG, NVST, F, HI, KMPR, NWSA, ORLY, PTC, QCOM, SNEX, TTMI, and WEX all reported beats on both the revenue and earnings lines. Meanwhile, AFL, CTVA, QGEN, and UHAL all beat on revenue while missing on earnings. On the other side, ALL, ASGN, CPAY, CCK, DLX, ENS, GL, HOLX, MUSA, SWKS, STE, UGI, and WFRD missed on revenue while beating on earnings. However, ALGN, AVB, BV, PLUS, MCK, MET, MAA, MOH, CNXN, RRX, and SYM missed on both the top and bottom lines.

Overnight, Asian markets were mostly green. Shenzhen (+2.26%), Shanghai (+1,27%), Australia (+1.23%), and South Korea (+1.10%) led the region higher. In Europe, we see green across the board at midday. The CAC (+0.88%), DAX (+0.90%), and FTSE (+1.52%) are leading that region higher in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a mixed, flat start to the day. The DIA implies a +0.05% open, the SPY is implying a +0.09% open, and the QQQ implies a -0.11% open at this hour. At the same time, 10-Year Bond Yields are up to 4.444% and Oil (WTI) is up two-thirds of a percent to $71.51 per barrel in early trading.

The major economic news scheduled for Thursday includes Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Preliminary Q4 Nonfarm Productivity, and Preliminary Q4 Unit Labor Costs (all at 8:30 a.m.), as well as Fed Balance Sheet (4:30 p.m.). We hear from Fed members Waller (2:30 p.m.) and Daly (3:30 p.m.). The major earnings reports scheduled for before the open include WMS, AGCO, APD, AB, APTV, MT, ARW, AZN, BCE, BDX, BDC, OWL, BWA, BMY, CX, CMS, CIGI, COP, DAR, LLY, ENTG, EFX, GTES, HP, HSY, HLT, HON, HII, NSIT, ICE, IQV, ITT, K, KVUE, LH, LEA, LNC, LIN, MKL, MMS, MDU, NVT, PATK, PTEN, BTU, PTON, PM, RL, RITM, RBLX, SNA, SPB, TPR, TEX, TRI, UAA, WMG, XEL, XPO, YUM, YUMC, and ZBH. Then after the close, AMRK, AFRM, AMZN, ATR, BYD, CNO, EHC, EXPE, LION, FTNT, FBIN, G, HUBG, ILMN, MTD, MCHP, MTX, MHK, MPWR, NBIX, OTEX, PINS, POST, PFG, RGA, SKX, SONO, SSNC, TTWO, VSAT, and WERN report.

In economic news later this week, on Friday, Jan. Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Private Nonfarm Payrolls, Jan. Participations Rate, Jan. Unemployment Rate, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and Dec. Consumer Credit are reported.

In terms of earnings reports later this week, on Friday, AVTR, CBOE, ROAD, FLO, FTV, ULCC, GPRE, KIM, NWL, PAA, PAGP report.

So far this morning, AGCO, AB, APTV, BCE, BDC, OWL, BMY, COP, CRARY, LLY, EMBC, ENTG, HSY, HLT, HON, IQV, LH, LEA, LNC, MMS, RITM, SNA, TPR, TEX, TRI, UA, UAA, WMG, XPO, YUM, and ZBH all reported beats on both the revenue and earnings lines. Meanwhile, WMS, AZN, CIGI, and PTON beat on revenue while missing on earnings. On the other side, AMG, APD, MT, BWA, CMS, DAR, ITT, KVUE, LIN, NVT, PM, SPB, and YUMC all missed on revenue while beating on the earnings line. However, HII and XEL missed on both the top and bottom lines.

With that background, it looks like the market is undecided so far this morning. All three major index ETFs are little moved from Wednesday’s close and have printed small-body, indecisive candles in the premarket. All three are above their T-line (8ema), so, the short-term trend is bullish. The mid-term downtrend (if you want to call it a trend) remains a mess. In terms of extension, as mentioned, all three are back close to their T-line. Meanwhile, T2122 sits just inside of its overbought territory. So, both sides have room to work today if they can find momentum, but the Bears may have just a little more slack to work with today. In terms of the Big Dogs, they are evenly split with five red and five green. NVDA (+1.14%) is way out front of the gainers while TSLA (-1.69%) is far ahead of the losers. As far as liquidity goes, it is a modestly liquid early session with TSLA leading with NVDA about 20% behind and the next closes ticker having traded six times less dollar-volume NVDA.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

U.S. stock futures trade flat following two consecutive winning sessions for major averages. However, semiconductor companies experienced declines in extended trading, with Qualcomm, Arm, and Skyworks Solutions losing approximately 5%, 4%, and 29%, respectively, after releasing their latest quarterly results. Ford Motor also saw a nearly 5% drop after projecting a challenging 2025. Despite initial concerns over tariffs announced by President Donald Trump—specifically a 10% levy on Chinese imports—investor sentiment improved as the president temporarily halted duties on Mexican and Canadian goods.

European markets experienced gains as investors analyzed earnings reports and awaited the Bank of England’s upcoming monetary policy decision. The Stoxx autos index managed to recover from early losses, trading 0.6% higher despite ongoing concerns about the impact of U.S. tariffs this year. Meanwhile, Sweden’s Volvo Cars saw a 9% drop after cautioning that 2025 would be a challenging year, with intensified competition from Chinese EV manufacturers and slower market growth. The Bank of England is anticipated to announce its first interest rate cut of the year during Thursday’s policy meeting.

Asia-Pacific markets showed positive momentum with most indexes trading higher. Australia’s S&P/ASX 200 climbed 1.23%, while Japan’s Nikkei 225 rose 0.61%, and the Topix added 0.25%. South Korea’s Kospi increased by 1.1%, and the small-cap Kosdaq advanced by 1.28%. Hong Kong’s Hang Seng Index gained 1.04%, with Mainland China’s CSI 300 up by 1.26%. In contrast, India’s benchmark Nifty 50 and BSE Sensex both saw declines of 0.48% and 0.43%, respectively. Investors are closely watching the Reserve Bank of India’s ongoing policy meeting, anticipating an interest rate cut aimed at stimulating the country’s struggling economy, with the decision expected on Friday.

Investors are eagerly anticipating the upcoming nonfarm payrolls report on Friday, which is expected to shed light on the U.S. employment landscape. Economists surveyed by Dow Jones predict that 175,000 jobs were added last month, with the unemployment rate remaining steady at 4.1%. Additionally, investors are awaiting the latest weekly jobless claims report on Thursday and are keen to hear speeches from Federal Reserve governor Christopher Waller and Fed Bank of San Francisco President Mary Daly. Notably, the ADP reported on Wednesday that private payrolls increased by 183,000 jobs in January, surpassing the 150,000 forecasted by economists and improving upon the 176,000 jobs added in December.

Shipping giant Maersk’s shares surged by over 10% after reporting fourth-quarter profits that exceeded expectations, despite ongoing trade uncertainties. The company’s earnings before interest, depreciation, taxes, and amortization (EBITDA) rose by 26% to $12.13 billion for the full year, with the fourth quarter alone reaching $3.6 billion, surpassing analysts’ forecasts1. CEO Vincent Clerc attributed this success to strong global trade and a robust price environment, although Maersk anticipates softer earnings for 2025 due to macroeconomic uncertainties

Strategy, formerly known as MicroStrategy, has rebranded and shifted its primary focus towards Bitcoin. The company introduced a new name, and logo, and adopted an orange brand color to reflect this change. In the fourth quarter of 2024, Strategy reported the acquisition of 218,887 bitcoins for $20.5 billion, bringing their total holdings to 471,107 bitcoins, which accounts for approximately 2% of the total supply. Despite recording a fourth-quarter net loss of $670.8 million from its legacy software operations, the company is progressing well on its $42 billion capital plan to acquire more bitcoins. CEO Phong Le highlighted the strong support from both institutional and retail investors for this strategic direction.

Qualcomm kicked off 2025 with a strong Q1 earnings report, posting record revenues of $11.67 billion, an 18% increase year-over-year, and adjusted earnings per share (EPS) of $3.41, up 24% from the previous year. The growth was driven by a 20% surge in chip sales, particularly in the smartphone sect or1. However, concerns over the company’s licensing business following the expiration of a key agreement with Huawei led to a nearly 5% drop in stock price during after-hours trading. Qualcomm remains optimistic about its future, with promising forecasts for Q2 and ongoing diversification into automotive and IoT chips

Shaking off tariff worries the bulls have rushed back in to test price resistance levels with two consecutive winning sessions after the Monday recovery. Volume, however, has been less than impressive and the market breadth has been on the decline. That said, keep an eye out for possible big point whipsaws if the bears find any reason to attack. As always focus on price action and plan your risk carefully as we test market highs.

Tuesday saw the markets start the day flat. SPY opened 0.06% higher, DIA opened dead flat, and QQQ opened up 0.07%. From there, SPY and QQQ rallied (QQQ’s rally being sharp). However, after that rally, those two chopped sideways all the way into the close. For its part, after the open, DIA sold off for 20 minutes before beginning a much slower rally that lasted the rest of the day. This action gave us white-bodied candles in all three. DIA printed a white, small-wick, Spinning Top candle that crossed back above its T-line. Meanwhile, SPY and QQQ printed large-body, white candles with tiny upper wicks that also crossed back above their T-lines as well. Both SPY and QQQ also crossed back above their 50sma. This happened on less-than-average volume in all three major index ETFs.

On the day, eight of the 10 of the sectors were in the green with Energy (+1.90%) well out in front leading the market higher. On the other side, the Utilities (-0.62%) and Consumer Defensive (-0.39%) sectors were the only ones in the red. At the same time, SPY gained 0.67%, DIA gained 0.28%, and QQQ gained 1.23%. (QQQ was led by AMD’s +4.58% gain.) Meanwhile VXX lost 3.06% to close at 43.69 while T2122 spiked all the way back up to just outside the edge of its overbought territory, closing at 79.37. On the bond side, 10-Year Bond yields fell to close at 4.513% and Oil (WTI) was flat, closing down a penny at $72.75 per barrel. So, Tuesday seemed to be a calming after the reaction and re-reaction to the Trump tariffs and then pushback of same.

The major economic news on Tuesday were limited to December Month-on-Month Factory Orders which were lower than expected at -0.9% (compared to a forecast of -0.7% and November’s -0.8% reading). At the same time, Dec. JOLTs Job Openings were also much lower than expected at 7.600 million (versus an 8.010 million forecast and November’s 8.156 million value). Then, after the close, the API Weekly Crude Stocks Report showed a larger-than-expected inventory build of 5.025 million barrels (compared to a +3.170-million-barrel forecast and the prior week’s 2.860-million-barrel number).

In Fed news, on Tuesday, Atlanta Fed President Bostic told an audience that since the FOMC has already slashed rates one percent and there was much greater economic uncertainty given the new administration’s volatile policies, there is no hurry to make any change to rates. Bostic specifically mentioned the ambiguous impact of US tariffs and potential retaliatory tariffs abroad. The bottom line of Bostic’s presentation was that the economy is now much more uncertain and will likely remain this way for quite a while. Therefore, the Fed must sit on its hands and wait to see how things shake out. Later, San Francisco Fed President Daly echoed Bostic’s point. She commented, “Growth is solid, the labor market is solid, and inflation is coming down, albeit gradually, but we’re heading toward our 2% target.” However, noting the uncertainty from the new administration, she continued, “In my time at the Fed, I’ve lived through a financial crisis and a pandemic, and those were extraordinarily uncertain times. Uncertainty is not a paralysis. It just means we have to watch and be careful and thoughtful as we navigate the information we have.” She went on to say, “The way we have to think about it (Trump’s immigration and tariff policies) as policy makers is to [focus on the] net effect of all of those, and we don’t know what it is yet.” She concluded that the Fed can’t be proactive given the volatility and uncertainty of Trump’s policy proposals. She said, “If you take preemptive action…you can end up making a policy mistake.”

After the close, AMD, ALGT, GOOGL, AMGN, CRUS, GOOG, LUMN, MOD, NOV, SPG, SKY, SNAP, and VOYA all reported beats on both the revenue and earnings lines. Meanwhile, DOX, AFG, COLM, MTCH, and WU beat on revenue while missing on earnings. On the other side, ATO, CMG, DXC, ENVA, FMC, THG, JKHY, JNPR, MAT, OI, and OMC missed on revenue while beating on earnings. However, CSL, EA, MDLZ, OSCR, PRU, and UNM missed on both the top and bottom lines.

Overnight, Asian markets were evenly split with six gaining exchanges and six losing ones. Taiwan (+1.61%), and South Korea (+1.11%) were way ahead leading the gainers while Thailand (-1.10%) and Hong Kong (-0.93% paced the losses. In Europe, we see a similar mixed picture taking shape on modest moves at midday. The CAC (-0.19%), DAX (-0.05%), and FTSE (+0.08%) lead the region in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a lower start to the day. The DIA implies a -0.10% open, the SPY is implying a -0.45% open, and the QQQ implies a -0.81% open at this hour. At the same time, 10-Year Bond Yields are down to 4.466% and Oil (WTI) is off one percent to $71.97 per barrel in early trading.

The major economic news scheduled for Wednesday includes the ADP Nonfarm Employment Change (8:15 a.m.), Dec. Exports, Dec. Imports, and Dec. Trade Balance (all at 8:30 a.m.), S&P Global Services PMI and S&P Global Composite PMI (both at 9:45 a.m.), ISM Non-Mfg. PMI, ISM Non-Mfg. Employment, and ISM Non-Mfg. Price Index (all at 10 a.m.), EIA Weekly Crude Oil Inventories (10:30 a.m.). We also hear from Fed member Bowman at 3 p.m. The major earnings reports scheduled for before the open include ARCC, ARES, BSX, BG, CPRI, CDW, COR, EMR, EQNR, EVR, FSV, FI, GSK, GFF, HOG, IEX, ITW, JCI, NYT, NVO, ODFL, PFGC, REYN, RXO, SR, SWK, TROW, TKR, TM, UBER, VSH, and DIS. Then after the close, AFL, ALGN, ALL, ARM, ASGN, AVB, EQH, BV, CENT, CTSH, COHR, CPAY, CTVA, CCK, DLX, ENS, ENSG, NVST, PLUS, F, GL, HI, HOLX, ITUB, KMPR, MCK, MET, MAA, MOH, MUSA, NWSA, ORLY, CNXN, PTC, QGEN, QCOM, RRX, SWKS, STE, SNEX, SU, TTMI, UHAL, UGI, VLTO, WFRD, and WEX report.

In economic news later this week, on Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Preliminary Q4 Nonfarm Productivity, Preliminary Q4 Unit Labor Costs, Fed Balance Sheet, and we hear from Fed members Waller and Daly. Finally, Friday, Jan. Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Private Nonfarm Payrolls, Jan. Participations Rate, Jan. Unemployment Rate, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and Dec. Consumer Credit are reported.

So far this morning, BSX, CDW, CMRE, COR, CRTO, EVR, FI, GSK, JCI, NYT, NVO, ODFL, REYN, RXO, SWK, TKR, TTE, TM, and UBER all reported beat on both the revenue and earnings lines. Meanwhile, ARES, BG, CPRI, HOG, and PFGC beat on revenue while missing on earnings. On the other side, EMR, KMT, and DIS missed on revenue while beating on earnings. However, ARCC, EQNR, SR, TROW, and VSH missed on both the top and bottom lines.

With that background, it looks like the market is modestly bearish this morning. All three major index ETFs gapped down a little to start the premarket. Since that point, they have printed indecisive (mostly wick) candles. SPY and QQQ are back below their T-line (8ema) while DIA is retesting that level in the early session. As a result, the short-term trend is bearish. The mid-term downtrend (if you want to call it a trend) remains a mess. In terms of extension, as mentioned, all three are back close to their T-line. Meanwhile, T2122 is just outside of its overbought territory. So, both sides have room to work today if they can find momentum, but the Bears may have a little more slack to work with today. In terms of the Big Dogs, nine of the 10 are in the red with AMD (-9.81%) out in front leading the pack lower. (Although AMD beat last night, it is being punished for lower-than-expected server revenue.) On the other side, NVDA (+0.94%) is holding up better than the others and is the only Big Dog in the green. As far as liquidity goes, it is a low-volume premarket but NVDA leads, followed by AMD with TSLA (-0.94%) not far behind.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stock futures fell on Wednesday after earnings from Alphabet and AMD as the tech giants disappointed investors, dragging the tech sector down. Apple’s decline further pressured futures, with the Technology Select Sector SPDR Fund dropping 0.7% in premarket trading. Apple’s 2.7% fall followed a Bloomberg News report that Chinese regulators were considering a formal investigation into the company’s App Store fees and policies. This situation unfolds amid escalating trade tensions between China and the U.S.; over the weekend, the U.S. imposed a 10% levy on Chinese imports, and China retaliated with tariffs of up to 15% on U.S. goods.

On Wednesday, European markets displayed mixed performance as investors continued to scrutinize regional corporate earnings. Spanish lender Santander announced a 14% year-on-year increase in annual profit, reaching €12.6 billion ($13.1 billion) for 2024, with full-year revenues in constant currency rising 10% to €62.2 billion. In contrast, French oil major TotalEnergies reported a significant drop in full-year earnings due to lower crude prices and weak fuel demand. The company posted an adjusted net income of $18.3 billion for 2024, a 21% decline from the previous year’s $23.2 billion.

Asia-Pacific markets exhibited mixed performance on Wednesday, following an overnight rise in Wall Street, as the region responded to Trump tariffs and China’s retaliatory measures. Mainland China’s CSI 300 Index initially gained but later reversed course, ending the day down 0.58%. China’s Caixin Services PMI for January registered at 51.0, down from December’s 52.2, indicating a slowdown in service sector activity. Hong Kong’s Hang Seng Index decreased by 0.97%. In Japan, the benchmark Nikkei 225 saw a modest rise of 0.09%, while the broader Topix index climbed 0.27%. South Korea’s Kospi increased by 1.11%, and the small-cap Kosdaq gained 1.54%. Australia’s S&P/ASX 200 rose 0.51%, whereas India’s benchmark Nifty 50 traded close to the flatline.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include ARCC, ARES, ATS, AZTA, TECH, BSX, BG, CPRI, CDW, COR, CTRI, CRTO, DAY, DIS, EMR, EVER, FSV, FI, GIL, GSK, GFF, HOG, ITW, JCI, KMT, KLC, NYT, ODFL, PFGC, REYN, RXO, SOBO, SR, SARO, SWK, TROW, TKR, UBER, VSH, & YUM.

The U.S. Postal Service announced on Tuesday that it is temporarily suspending all inbound packages from China and Hong Kong Posts, effective immediately and lasting “until further notice.” This suspension does not affect letters and large envelopes, also known as “flats,” sent from China and Hong Kong. The de minimis provision, which has been pivotal for Chinese e-commerce companies like Shein and PDD Holdings’ Temu to offer low-priced goods in the U.S., is under scrutiny. Lawmakers argue that de minimis imports give Chinese firms an unfair advantage by allowing them to bypass tariffs. Trade officials have also noted that these packages are subject to minimal documentation and inspection.

Apple shares declined on Wednesday following a Bloomberg report that Chinese regulators are contemplating a formal investigation into the company’s App Store fees and policies. The State Administration for Market Regulation (SAMR) is scrutinizing Apple’s practices, which involve taking up to a 30% commission on in-app purchases and restricting third-party payment services and app stores. This development coincides with China initiating an antitrust probe into Google earlier this week, though specific details about the latter investigation have not been disclosed by the market regulator. The prospect of heightened regulatory scrutiny in China has raised concerns among investors, impacting Apple’s stock performance.

Alphabet shares experienced a significant decline of over 9% in after-hours trading on Tuesday. This followed the company’s announcement of fourth-quarter results that fell short of revenue expectations, coupled with plans for increased artificial intelligence investments. Although Alphabet’s overall revenue grew by nearly 12% year over year, this was a slowdown compared to the more than 13% growth seen in the same quarter last year. Additionally, revenue growth for its search business, YouTube ads business, and services unit was slower compared to a year ago. The company revealed plans to invest $75 billion in capital expenditures in 2025, a figure surpassing Wall Street’s expectation of $58.84 billion, as per FactSet. For the first quarter, Alphabet anticipates capital expenditures to range between $16 billion and $18 billion, indicating its continued focus on expanding its AI strategy.

AMD reported a net income of $482 million, or 29 cents per share, for the fourth quarter, down from $667 million, or 41 cents per share, in the same period last year. The company’s adjusted earnings per share excluded costs related to acquisitions, inventory loss at contract manufacturers, and restructuring charges. AMD’s data center sales grew to $3.86 billion, marking a 69% increase year-over-year, driven by strong sales of its Instinct GPUs and EPYC CPUs, which compete with Intel’s processors. However, this fell short of the $4.14 billion that analysts polled by FactSet had anticipated. For the entire year, AMD’s data center division revenue surged 94% to $12.6 billion, with $5 billion attributed to sales of its Instinct GPUs for AI.

With huge spending plans for 2025, the some tech giants disappointed investors yesterday dragging the futures lower for Wednesday. Apple is also feeling some pressure this morning as China looks to probe the company for potential illegal practices. However, there is some good news this morning with the dollar moving lower we may be seeing worries of continued inflation beginning to subside. Plan carefully it could be another day of big price swings.