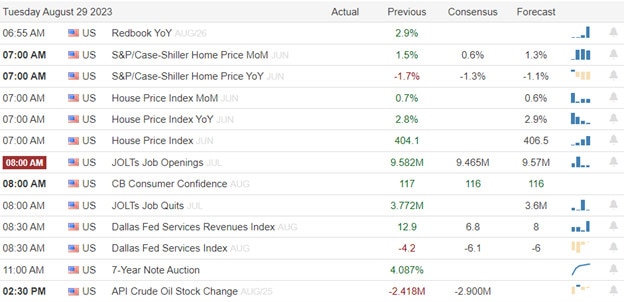

Markets around the world enjoyed a relief rally with choppy price action in the U.S. with overhead resistance levels holding with bond yields adding worries to future rate increases. Today traders will have much more earnings and economic data to inspire with Case-Shiller, Consumer Confidence, and JOLTS figures pending. Light choppy price action could be possible as we wait for the Wednesday release of the GDP providing the uncertainty.

Overnight Asian markets continued their relief rally led by Hong Kong up 1.95% at the close as Japan reported higher than expected unemployment. European markets also advance building on the bullish momentum. Ahead of earnings and economic data, U.S. futures point to a bullish open with the uncertainty of the GDP report looming Wednesday.

Lithium is a metal that is used in various applications, such as batteries, electric vehicles, aerospace, and medicine. It is considered a critical mineral for the transition to a low-carbon economy. However, the supply of lithium may not be able to keep up with the growing demand, as a research unit of Fitch Solutions warned. According to BMI, “Global lithium supply is expected to enter a deficit relative to demand by 2025”. This means that there could be a worldwide shortage of lithium soon, which could affect the prices and availability of lithium products. The main factors that contribute to the supply-demand imbalance are the limited production capacity, the environmental and social challenges, and the geopolitical risks of lithium mining and processing. Therefore, it is important to find alternative sources of lithium, such as recycling, seawater extraction, and geothermal brines.

Toyota Motor, the world’s largest automaker by sales, has faced a major disruption in its production system due to a technical glitch. The company announced on Tuesday that it has halted operations at all 14 of its assembly plants in Japan, affecting its domestic output of about 30,000 vehicles per day. The company said that the malfunction occurred in its information system that connects the production lines and the parts suppliers, causing delays and errors in the delivery of components. The company apologized for the inconvenience and said that it is working to restore the system as soon as possible. The suspension of operations could have a significant impact on Toyota’s sales and profits, as well as on its global supply chain and customers.

Artificial intelligence (AI) is a powerful technology that can have both positive and negative impacts on humanity. Brad Smith, president and vice-chairman of Microsoft, one of the leading companies in AI development, said that AI has “the potential to become both a tool and a weapon”. He stressed the need for human control over AI to “slow things down or turn things off” in case of any harmful or unethical outcomes. His statement came amid the growing popularity and controversy of ChatGPT, a generative AI-powered chatbot that can produce humanlike responses to any input. ChatGPT has been praised for its creativity and versatility, but also criticized for its potential risks of spreading misinformation, manipulation, and violence. Some tech leaders have warned that AI poses a human extinction risk on par with nuclear war if it becomes too intelligent and autonomous. Therefore, it is important to establish ethical principles and regulations for AI to ensure its safe and beneficial use for humanity.

Indeses enjoyed a relief rally in the U.S. on light choppy price action with bond yields rising during government auctions. Today investors have more data on the earnings and economic calendars for the bulls or bears to find inspiration. Asian and European relief rallies are helping to lift premarket bullish spirits despite their weakening economic figures. Keep a close on overhead resistance levels in price and technicals such as the 50-moving averages that could harbor entrenched bears. Don’t be too surprised by light volumes and choppy price action with the uncertainty of the GDP report coming Wednesday morning.

Markets whipsawed as investors tried to interpret Fed Chair Powell’s comments. Although the indexes enjoyed a late day relief rally from the short-term oversold conditions bond yields on the short end of the curve continued to rise. This week’s plan for the price action instability continue with a slew of jobs data, GDP, PMI and manufacturing data for the bulls and bears to find inspiration.

Asian markets followed the U.S. markets overnight reliving recent selling pressure even as real estate issues in China expanded with Evergrande shares plunging. European markets are also trading higher this morning in a modest relief rally as China uncertainty expands. Ahead of a light day of earnings and economic data U.S. futures point to bullish open hoping to continue the relief rally started Friday afternoon to test overhead resistance levels.

Economic Calendar

Earnings Calendar

Notable reports for Monday include HEI.

News & Technicals’

China Evergrande Group, one of the largest real estate developers in China, has been facing a severe liquidity crisis that has shaken the confidence of its investors and creditors. The company’s shares have been suspended from trading on the Hong Kong exchange since March 21, 2023, after closing at a record low of 1.65 Hong Kong dollars ($0.13) per share on March 18. The suspension came as the company reported a massive loss of 39.25 billion yuan ($5.38 billion) for the first half of 2023, with total liabilities reaching a staggering 2.39 trillion yuan. The company has been struggling to repay its debts and avoid default, as it faces regulatory pressure, legal challenges, and public protests from its customers and suppliers.

The labor market in the United States has witnessed a surge of strikes and protests by workers who demand better pay and working conditions from their employers. According to data from the Cornell University School of Industrial and Labor Relations, more than 320,000 workers have participated in at least 230 strikes so far this year, affecting various industries such as health care, education, hospitality, and manufacturing. Some of the workers have successfully negotiated favorable labor deals, such as UPS workers and airline pilots, while others are still in the process of bargaining or threatening to walk out, such as Hollywood writers and actors and auto workers. The wave of labor unrest reflects the growing dissatisfaction and frustration of workers who feel underpaid, overworked, and unsafe amid the pandemic and the economic recovery.

Microsoft, the tech giant and the owner of Xbox, has made a renewed bid to acquire Activision Blizzard, the American game publisher behind popular titles such as Call of Duty, World of Warcraft, and Candy Crush. The company has submitted a fresh takeover proposal of $69 billion to the U.K. regulators, who rejected its initial offer on the grounds of anti-competitive concerns in the nascent cloud gaming market. Brad Smith, Microsoft’s vice-chairman and president, told CNBC that the company “really tried to take concerns to heart” and addressed the issues raised by the regulators in its new proposal. He also said that the deal would benefit both gamers and developers by creating more diverse and innovative games. However, he acknowledged that the final decision rests with the regulators and that “it will be up to them to decide whether that path is clear”.

On Friday, stock markets rose as they tried to interpret Fed Chair Powell’s speech at the Jackson Hole symposium for any hints about future interest-rate moves. Chair Powell struck a balanced tone, saying that the Fed would base its decisions on the data but said rate increases may not be over. Global markets had mixed results, and Treasury yields as shorter-term rates went up. Today we have a light day on both economic and earnings calendar, however, later this week will be filled with jobs data and a key GDP report. Plan for price volatility to remain high with investors hoping for a relief rally with the uncertainty of the weaking China economy as there real estate crisis expands and the consumer in the U.S. consumer shows signs of inflation impacts with record credit card and household debt burdens.

On Friday, stocks gapped a bit higher with SPY gapping up 0.43%, DIA gapping up 0.46%, and QQQ gapping up 0.25%. Markets then ground sideways until 10 am, when volatility kicked in as Fed Chair Powell’s Jackson Hole prepared remarks led to some knee-jerking and then a 45-minute selloff that reached the lows of the day in all three major index ETFs about 5 minutes after 11 am. However, the Bulls stepped in at that point, giving us a long, wavy rally that lasted until 3:30 pm when the SPY, IDA, and QQQ all hit their high of the day. Then we saw modest profit-taking the last 30 minutes across the board. This action gave us indecisive, white-bodied, Bullish Harami Spinning Top candles in all three of the major index ETFs. QQQ managed to close just above its T-line (8ema), while SPY closed just below its T-line, and DIA did not quite reach its T-line, even at the high of the day.

On the day, nine of the 10 sectors were in the green with Technology (+0.81%) and Energy (+0.78%) leading the way higher Communications Services (-0.10%) being the only sector left in the red. At the same time, the SPY gained 0.70%, DIA gained 0.72%, and QQQ gained 0.78%. VXX dropped 4.35% to 24.20 and T2122 climbed back up to the edge of oversold territory at 19.47. 10-year bond yields pulled back slightly to close at 4.231% while Oil (WTI) gained 1.27% to close at $80.05 per barrel. This happened on slightly above-average volume in all three of the major index ETFs. So, the volatility and bearish sentiment lasted about 45 minutes and then the day belonged to the Bulls heading into the weekend. DIA has now taken out its uptrend (stretching back to October 2022). QQQ is right at (and retesting) its uptrend line stretching back to January. SPY remains the only one of the major index ETFs still above and not yet retesting its bullish trend stretching back to mid-October 2022.

The major economic news reported Friday included August Michigan Consumer Sentiment, which came in a bit below expectations at 69.5 (compared to a forecast of 71.2 and the July reading of 71.6). At the same time, August Michigan Consumer Expectations were also a bit low at 65.5 (versus the 67.3 forecast and the July 68.3 value). In terms of forward-looking survey results, the August Michigan Inflation Expectations (over the next 12 months) were high at 3.5% (compared to the forecast of 3.3% and the July reading of 3.4%). Finally, the August Michigan 5-year Inflation Expectation was 3.0% (versus the 2.9% forecast but in line with the July 3.0% value).

In Fed Speaker News, Fed Chair Powell’s Jackson Hole speech was the big news. In his prepared remarks (released minutes prior to his speech, Powell said “It is the Fed’s job to bring inflation down to our 2% goal, and we will do so.” His remarks continued, “We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.” Still, he also left room for a continued pause in hikes in September by saying, “We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.” Elsewhere, on the sidelines of the conference, Cleveland Fed President Mester also bolstered the hawk message, saying “We’ve come a long way, but you know, we don’t want to be satisfied because inflation remains too high.” She continued, “We need to see more evidence to be assured that [inflation is] coming down in a sustainable way and in a timely way.”

The other major central banker speaking Friday was European Central Bank President Lagarde. She called for EU rates to be “higher for longer.” The ECB President said, “In the current environment, this means – for the ECB – setting interest rates at sufficiently restrictive levels for as long as necessary to achieve a timely return of inflation to our 2% medium-term target.” Lagarde also went on to warn central bankers to fear wage increases “That could make inflation more persistent if expected wage increases are then incorporated into the pricing decisions of firms, giving rise to what I have called ‘tit-for-tat’ inflation.” Interestingly, that argument seems to run contrary to both research and common sense. In the US, by far the largest component of inflation in recent months has been the rise in the cost of shelter (rent and house prices), followed by the rise in energy prices, both of which are not driven by wages according to BLS data. Finally, recent reports from economic researchers have said the main culprit behind inflation since 2019 has been the backlog of orders caused by the pandemic and the resulting cascade of supply chain issues. In short, supplies fell much more sharply than demand around the world and stayed that way for two years. So, Lagarde seems to be arguing that workers should accept stagnant wages and whatever inflation that comes every year, in order to avoid giving companies an excuse to raise prices even more than the wage increases they might demand.

In stock news, on Friday ERIC announced that it forecasts $1 billion in patent cross-licensing revenue from its licensing agreements with Chinese phone maker Huawei. At the same time, C reported that net outflows from its equity funds have continued. C says there were $6.1 billion in outflows from equity funds during the week that ended August 23. Elsewhere, RAD shares plunged Friday when the Wall Street Journal reported that it is getting ready to file for Chapter 11 bankruptcy. (RAD closed down 51.04%.) Later, Bloomberg reported that BA is close to restarting the delivery of 737 MAX jets to China after a four-year pause following the deadly crashes in 2019 and 2020. By late afternoon, Reuters reported that BB had received an acquisition offer from private equity firm Veritas Capital. (BB closed up more than 18% on the day.) Meanwhile, UAW workers voted overwhelmingly (97% in favor) to authorize a strike against GM, F, and STLA any time after the current contract expires on September 14. (As of now, the negotiations between the union and “Big 3” are contentious and not making much progress according to media reports. Some economists say a strike on all three would cost the economy $500 million per day.) Late in the day, Reuters reported that TWNK is exploring a sale after receiving takeover interest from major snack food makers. This news caused a massive spike in the price of TWNK at 2:40 pm. On the day, TWNK pulled back to close up 21.73%.

In stock legal and regulatory news, on Friday the MA Supreme Court reversed a lower court ruling in a blow to HOOD. The decision gives MA state regulators a significant victory in their enforcement action against the online broker, by ruling that the broker does have fiduciary responsibility. (This was central to the MA case, which claims that HOOD breached its fiduciary responsibility by encouraging inexperienced investors to place risky trades via gamification.) Elsewhere, AZN joined the other major pharma companies by filing suit against the US over Medicare drug price negotiation plans. At the same time, the SEC reported that MMM has agreed to pay $6.5 million to settle the charges that it had violated the Foreign Corrupt Practices Act by bribing Chinese officials to curry favor. Later the SEC also reported that WFC has agreed to pay $35 million in penalties to settle charges that the company overcharged its customers for advisory fees. Late Friday evening, the FTC suspended its challenge of AMGN’s $27.8 billion acquisition of HZNP. This pause is effective until September 18 and will give the agency time to consider whether it should settle the case rather than continue a lengthy court fight. (AMGN may have offered some compromise since it announced “it would be pleased if its commitment were honored.”) Finally, on Sunday, MMM tentatively agreed to pay $5.5 billion to settle 300,000 lawsuits claiming defective MMM earplugs caused permanent hearing loss among US military veterans. The settlement would stop the need for MMM’s once-court-blocked attempt to avoid liability by shifting it to a subsidiary that was then declared bankrupt.

Overnight, Asian markets were nearly green across the board. Only Malaysia (-0.02%) remained in the red while Japan (+1.73%), Shanghai (+1.13%), and Shenzhen (+1.01%) led the region strongly higher. In Europe, we do see green across the board at midday. The CAC (+0.69%), DAX (+0.51%), and lagging FTSE (+0.07%) lead the region higher on volume in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a modestly green start to the day. The DIA implies a +0.25% open, the SPY is implying a +0.18% open, and the QQQ implies a +0.29% open at this hour. At the same time, 10-year bond yields are up slightly to 4.239% and Oil (WTI) is off fractionally to $79.72 per barrel in early trading.

There is no major economic news scheduled for Monday. There are no major earnings reports scheduled for before the opening bell. Then, after the close, HEI reports.

In economic news later this week, on Tuesday we get Conference Board Consumer Confidence, JOLTs Job Openings, and API Weekly Crude Oil Stocks Report. Then Wednesday, ADP Nonfarm Employment Change, Q2 GDP, Q2 GDP Price Index, July Goods Trade Balance, July Retail Inventories, July Pending Home Sales, and EIA Crude Oil Inventories are reported. On Thursday, we get Weekly Initial Jobless Claims, July PCE Price Index (year-on-year), July PCE Price Index (month-on-month), July Personal Spending, August Chicago PMI, and the Fed Balance Sheet. Finally, on Friday, August Average Hourly Earnings (month-on-month), August Average Hourly Earnings (year-on-year), August Nonfarm Payrolls, August Private Nonfarm Payrolls, August Participation Rate, August Unemployment Rate, August S&P US Mfg. PMI, August ISM Mfg. Employment, August ISM Mfg. PMI, and August ISM Mfg. Prices are reported.

In terms of earnings reports later this week, on Tuesday, BMO, BNS, BBY, BIG, CTLT, CHS, DCI, SJM, NIO, PDD, AMWD, HPE, HPQ, YY, and PVH report. Wednesday, we hear from PDCO, CHWY, COO, CRWD, FIVE, GEF, OKTA, PSTG, CRM, VEEV, and VSCO. On Thursday, ASO, CAL, CPB, CM, CIEN, DG, GCO, GMS, HRL, BEKE, OLLI, PSNY, SIG, TITN, UBS, ARMK, AVGO, DELL, LULU, NTNX, and VMW. On Friday, DDL reports.

In miscellaneous news, CNBC reported Saturday that with 9 million open jobs (in June) and only 5.8 million unemployed workers, a serious imbalance exists. Economists have suggested easing immigration policy to help address the problem, which an economist from the Cato Institute (Libertarian) estimates is costing the US “something like $1 trillion a year” in lost GDP. (The current immigration process takes about 5 years for a person to legally enter the US and join the workforce.) However, a survey taken by that same institute found Americans are split on easing immigration restrictions. As you probably expected, that split is largely along political lines. Elsewhere, CNBC also reported Saturday that AMZN is expanding its biometric authorization process. The company already has 200 Whole Foods Market stores that allow customers to have cards on file and then authorize payments by scanning their palms. AMZN says it will expand that number to 500 stores by year-end. Finally, it seems a primary driver of Asian (and probably European) markets are Chinese measures announced Sunday. China reduced the tax on stock trades, eased restrictions on executives selling shares, and lowered deposit ratios for margin trading. All the moves were to encourage more trading in Shanghai, Hong Kong, and Shenzhen. However, while there was a pop, many investors were looking for stronger action to actually stimulate the Chinese economy.

With that background, it looks like the Bulls are retesting the T-line (8ema) in all three major index ETFs in the early session. The QQQ candle is showing some bullishness (not just a modest gap higher) while the two large-cap index ETFs are much smaller premarket candles. The bulls still have a lot of work ahead of them since in addition to the 8ema, the 50sma remains overhead (we are still looking at a Blue Ice Failure pattern in all three). There is also a number of levels created by previous swing points to overcome. In other words, the Bears have the momentum. As far as extension goes, none of the major index ETFs are too far extended from their T-line and the T2122 indicator is sitting right at the upper edge of the oversold territory. So, both sides have room to run but the Bulls obviously have more slack if they could manage a rally.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets diverged a bit at the open following NVDA’s blowout results the night before. SPY gapped up 0.38%, DIA gapped down 0.11%, and QQQ gapped up 0.94%. DIA did its best to catch up by rallying sharply the first 30 minutes of the day. However, QQQ was already throwing the mega-caps a curve by reversing and selling off hard at that same time. Things got back in sync at 10 am as all three major index ETFs then went on to sell off the rest of the day, closing very near the low of the day. This action gave us large, black, Bearish Engulfing candles in the SPY and QQQ. Both of those index ETFs also crossed back below their T-line (8ema) in the process. For its part, DIA failed a retest of its own T-line on a large, black-bodied candle with a large upper wick. DIA also fell down out of its four-day consolidation. All three also retested and failed their 50sma, thus giving us a Blue Ice Failure pattern (with the exception that only QQQ has enough space left down to its 200sma to qualify as a Blue Ice Failure).

On the day, all 10 sectors were in the red with Technology (-2.17%) and Consumer Cyclical (-1.92%) way out front leading the way lower with Financial Services (-0.32%) and Communications Services (-0.35%) holding up better than the other sectors. At the same time, the SPY lost 1.39%, DIA lost 1.10%, and QQQ lost 2.14%. VXX popped up 4.12% to 25.30 and T2122 dropped back down into the oversold territory to 10.06. 10-year bond yields jumped back up to close at 4.241% while Oil (WTI) was flat to close at $78.88 per barrel. This happened on slightly above-average volume in the QQQ and average volume in the SPY and DIA. So, the profit-taking off the opening pop was dramatic and lasted all day Thursday. DIA has now taken out its uptrend (stretching back to October of 2022). QQQ is right at (and retesting) its uptrend line stretching back to January. And SPY remains the only one of the major index ETFs still above and not yet retesting its bullish trend stretching back to mid-October 2022.

The major economic news reported Thursday included July Durable Good Orders, which came in lower than expected at -5.2% (compared to a forecast of -4.0% and even worse than the June reading of -4.4%). This included July Core Durable Goods Orders that were reported better than expected at +0.5% (versus a forecast of +0.2% which was also the June value). At the same time, Weekly Initial Jobless Claims were reported at 230k (versus a forecast of 240k and the previous week’s 240k number). Later, after the close, the Fed Balance Sheet continued to show its slow reduction as it shrank from $8.146 trillion to $8.139 trillion. In related news, it is also worth noting that the St. Louis Fed said Thursday that the Fed may need to stop shrinking its balance sheet at least temporarily. Since the government has issued $1 trillion in bonds since June, money market funds have been holding back on their purchases of bonds. That leaves the Fed as the other major potential buyer.

In Fed Speak news, Philly Fed President Harker told CNBC Thursday morning that he doubts the FOMC will need to raise rates again. Harker said, “Right now I think that we’ve probably done enough.” He went on to say, “I’m in the camp of let the restrictive stance work for a while, let’s just let this play out for a while, and that should bring inflation down.” However, Harker was not ready to predict when the Fed might start cutting rates. Just a bit later, Boston Fed President Collins said something very similar when she told Yahoo Finance, “We may be near, we could even be at a place where we would hold and not raise rates further … But certainly, additional increments are possible, and we need to look holistically and be really patient right now and not try to get ahead of what the data will tell us as it unfolds.” (Both did their interviews on the sidelines of the Jackson Hole Central Banker Conference.) Both of them also seemed to embrace the recent bond yield rate spikes as something that could help the Fed by increasing longer-term borrowing costs and therefore cooling the economy.

In stock news, TMUS said Thursday that it will be cutting 5,000 jobs (about 7% of its workforce). The company cited rising costs, cheaper phone plan offerings, and the competitive phone market. Elsewhere, MA will end its partnership with crypto exchange Binance (which had covered four countries). In other finance news, the Wall Street Journal reported that a group of funds (led by BLK) that have lent money to WE are exploring the possibility of a Chapter 11 bankruptcy filing. At the same time, RY announced it would be cutting 1,800 jobs as a cost-cutting measure. In auto industry news, STLA announced it is expanding its “manufacturer-approved pre-owned vehicle” sales program to the US. (The program started in Europe in 2019.) Meanwhile, GOOGL said Thursday that it will provide more information on targeted ads and give researchers more access to data in order to come into compliance with new EU online content rules. After the close, HE plummeted as much as 24% after announcing it was suspending its dividend after subsidiaries were forced to draw $370 million from their revolving credit lines in the wake of the massive Maui fires. Also after the close, LMT was awarded a $2.7 billion contract by the US Navy to build 35 additional CH-53K helicopters. At the same time, GM announced it has agreed to increase the pay of workers at its OH battery plant by an average of 25%. In addition, Reuters reports that AMZN is in talks with DIA over a potential streaming deal with DIS’s ESPN unit.

In stock legal and regulatory news, late Wednesday night, the SEC made a court filing saying that investors who lost money (victims) when Elon Musk tweeted about taking TSLA private will soon begin receiving payouts, recouping 51.7% of their losses. At the same time, the TX Public Utilities Commission announced that TSLA will provide the state with two “virtual power plants” (drawing power from people who have TSLA Powerwall batteries and compensating them for the electricity). Elsewhere, Reuters reported that SAVE has agreed to pay up to $8.25 million to settle a class action suit over hidden carry-on baggage fees. At the same time, WHR agreed to pay $11.5 million to the US Consumer Protection Product Safety Commission over failure to report glass cooktops that could turn themselves on posing burn and fire hazards. Later, the NHTSA told Reuters that it would resolve its two-year investigation into TSLA Autopilot in a public announcement soon. The spokesman declined to describe what that resolution will be or exactly when “soon” will come. Meanwhile, starting today, the big tech names will be forced to comply with the new EU Digital Service Act which imposes stricter rules on content moderation, user privacy, and transparency. These include META, AAPL, and GOOGL. (AMZN is fighting its inclusion on the list of companies covered in court.) Failure to comply could result in fines of up to 10% of total global sales per infraction. After the close, a US District Court judge dismissed a lawsuit against GOOGL that had been brought by the Republican National Committee which had claimed the tech giant had maliciously marked RNC mass emails as spam. Also after the close, TD said it expects to be fined and other non-monetary penalties from US authorities over a money laundering investigation.

After the close, AFRM, INTU, MRVL, JWN, ULTA, and WDAY all reported beats on both the revenue and earnings lines. Meanwhile, GPS missed on revenue while beating on earnings. It is worth noting that AFRM, INTU, and WDAY raised their forward guidance.

Overnight, Asian markets were mostly red. Japan (-2.06%) and Taiwan (-1.72%) were way out front leading 10 of the region’s 12 exchanges lower. In Europe, the opposite picture is taking shape at midday. 14 of the 15 bourses in the region are squarely in the green while the CAC (+0.74%), DAX (+0.56%), and FTSE (+0.49%) lead the region higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing to a green start to the day here as well. The DIA implies a +0.34% open, the SPY is implying a +0.26% open, and the QQQ implies a +0.10% open at this hour. At the same time, 10-year bond yields are up slightly to 4.249% and Oil (WTI) is up just over one percent to $79.86 per barrel in early trading.

The major economic news scheduled for Friday includes Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Inflation Expectation, and Michigan Consumer 5-year Inflation Expectations all at 10 am. Fed Chair Powell also speaks at 10:05 am as the Jackson Hole Conference continues. There are no major earnings reports scheduled for the day (either before the open or after the close).

In miscellaneous news, both the TX and Central State electric grids warned customers of potential power outages as the brutal heatwave continues to pound much of the US. Both grid operators urged voluntary power conservation to avoid rolling outages. In other news, the BRICS group invited some more oil to the party as they formally asked Saudi Arabia, Iran, and UAE to join. Rounding out the new countries invited were Argentina, Egypt, and Ethiopia.

As mentioned above, Fed Chair Powell speaks just after 10 am Eastern this morning. Markets are very likely to parse through every word and facial gesture he delivers looking for a clue to the path for interest rates. (This is especially true after two dovish statements from Fed members delivered in interviews on the sideline of the conference Thursday.) If you want to get a little wonky, see if Powell addresses an abstract metric known as “R*” (R-star). This is not the target interest rate, but instead, it is the rate at which Fed policy is theoretically neutral (neither restricts or stimulates the economy). Since 2019 that rate has been 2.5% and prior to that the R* was 3.5% going back until 2015. While Powell will be the main show on Friday, EC President Lagarde also speaks at 3 pm Eastern. (This will be her first public remarks since the EC’s July rate hike.)

With that background, it looks like the premarket is modestly bullish after Thursday’s big bearish candles. None of the major index ETFs have done enough premarket work to be retesting their T-lines (8ema) or 50sma. So we are still looking at a Blue Ice Failure pattern in all three with huge Bearish Engulfing candles in the SPY and QQQ (which could both also be working on Dreaded-h patterns (the opposite of a J-hook). In other words, the Bears have all the chart patterns in their favor this morning. So, the short-term downtrend break is back in question for the SPY and QQQ, while DIA has resumed its own move lower. As far as extension goes, none of the major index ETFs are too far extended from their T-line but the T2122 indicator is back down well into the oversold territory. So, both sides have some room to run but the Bulls obviously have more slack if they could manage a rally. Finally, don’t forget it is Friday with the Jackson Hole Conference continuing Saturday (although we do not EXPECT much news then). We also have the long weekend news cycle. So, prepare your account for the weekend by taking some money off the table (it is Payday after all) and moving stops, hedging, or lightening up your positions.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

It was the Bulls Day on Wednesday. SPY opened 0.24% higher, DIA opened 0.15% higher and QQQ gapped up 0.32%. At that point, all three major index ETFs followed through with a steady rally until almost 2 pm. Then all three traded sideways the rest of the day with a slight profit-taking trend. This action gave us gap-up, large-body, white candles in all three. The SPY crossed back above its T-line (8ema) and with a tiny tick on top is now just below its 50sma. The QQQ also crossed back up through its T-line but had a slightly larger upper wick than the SPY. QQQ is also just below its 50sma and you might even say it tested the 50 at the high of the day. DIA is still in more of a sideways consolidation than a rebound rally like the other two majors.

On the day, all 10 sectors were in the green with Technology (+1.08%) way out front leading the way higher followed by Financial Services (+1.20%) while the lagging sector was Energy (+0.11%). At the same time, the SPY gained 1.08%, DIA gained 0.52%, and QQQ gained 1.58%. VXX was down 3.34% to close at 24.30 and T2122 climbed back out of the oversold territory into the lower half of the mid-range at 39.42. 10-year bond yields plummeted lower to close at 4.194% while Oil (WTI) fell 1.48% to close at $78.46 per barrel. This happened on well-below-average volume in all three of the major index ETFs. So, the rally relationship has resumed, with QQQ and SPY leading the market higher while DIA lags again. The question is whether or not this is just a relief rally in the month-long pullback. Either way, Wednesday belonged to the Bulls.

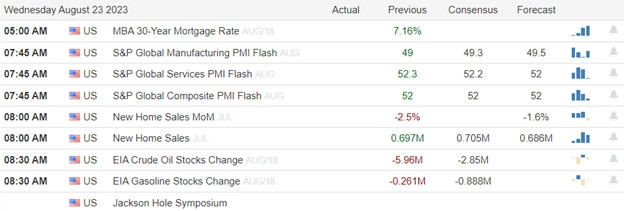

The major economic news reported Wednesday included Building Permits, which came in slightly above expectation at 1.443 million (compared to a forecast of 1.442 million and a July reading of 1.441 million). This amounted to a 0.1% month-on-month increase versus the July value which itself was down 3.7% from June. Later, the Preliminary August S&P US Mfg. PMI came in light at 47.0 (compared to a forecast calling for 49.3 and a July reading of 49.0). At the same time, the Preliminary August Services PMI was reported at 51.0 (versus a forecast of 52.3 and a July value of 52.3). In addition, the Preliminary S&P Global Composite PMI was 50.4 (compared to a 52.0 forecast and a 52.0 July value). After that, the July New Home Sales came in higher than expected at 714k (versus a 705k forecast and a 684k June reading). This amounted to a 4.4% increase in July, which was better than the +0.2% increase anticipated and far better than June’s decline of 2.8%. Later, the EIA Weekly Crude Oil Inventories followed the API report from Tuesday night, showing a 6.135-million-barrel drawdown (compared to a predicted 2.850-million-barrel draw and even the prior week’s 5.960-million-barrel drawdown of inventory.

In Russian news, Putin’s unofficial warlord Yevgeny Prigozhen was killed along with the other co-founder of Wagner Private Military Company (Dmitry Utkin). Most saw this plane crash coming as the inevitable result of Wagner’s June uprising against Putin. Still, it is notable. Elsewhere, Reuters reported Wednesday that Russian central bank authorities are working on a presidential decree that may give that country’s retail investors a way to unblock their frozen assets held in overseas accounts. The scheme would allow foreign investors to buy the assets held abroad (3.5 million Russians hold almost $16 billion in foreign accounts that are now frozen). The idea is that non-Russian investors would buy the frozen Russian account assets (presumably at a discount) in exchange for assets held in non-frozen accounts that can be repatriated to Russia. It’s unclear whether Western sanctions would now (or could be made to) block this move. (One would think this to be the case, otherwise, the Russian oligarchs surely would have done this 18 months ago.) It is also unclear if there is some sort of unmentioned reciprocal agreement at play allowing Western business assets frozen in Russia to be released.

In stock news, research firm Antenna reported that NFLX continued its strong growth in new subscribers in July (not as strong as June’s record increase, but still 2.6 million is a significant gain in subscribers for a month). NFLX was up 3.48% on the day of that news. At the same time, a Business Insider report said TSLA cut its production targets in Germany by 13% (with plans to cut it more later). The current rate of output is now 4,350 per week from the TSLA Berlin plant. Simultaneously, Reuters reported that NVO has chosen TMO as a second contract manufacturer for its hit weight loss drug Wegovy. In the early afternoon, JNJ announced its Janssen division would be closing down much of its vaccine research and development operations. (The JNJ COVID-19 vaccine did not perform as well as competitors from PFE and MRNA.) Later, the UAW announced workers at the major F Louisville plant have voted to authorize a strike with three weeks left before the current labor contract expires. In other auto industry news, GM said they are halting production at their Ft. Wayne assembly plant for a week as they continue to wrestle with part supply issues. (GM blamed the shortage on a lack of railcars and truck drivers which led to a massive buildup of partially completed vehicles at the plant.) In M&A news, private company Esmark announced it has rescinded its offer to buy X for $35/share. In a statement, Esmark said it will respect the USW Steel Workers Union position (the union is supporting CLF buying X for a lower $7.3 billion total price). After the close, GM announced it was cutting 940 jobs in AZ and would cease its IT operations in that state to reduce costs. (80-90 of these layoffs come from the self-driving software team.) At the same time, Reuters reported that a new supplier quality problem has been identified related to 737 MAX production. The new problem will delay near-term deliveries of those planes and is likely to impact annual production goals. AAPL announced after the close that it supports the CA state “Right to Repair” bill as currently written, specifically citing that the bill “protects consumer safety, device security, and manufacturers intellectual property rights.” (This almost assuredly means the bill has been transformed into something worthless to consumers and non-AAPL repair businesses.)

In stock legal and regulatory news, OSHA said Wednesday that it’s investigating a chemical spill at a lithium battery plant owned by GM and South Korea’s LG Energy. This is one of six open OSHA investigations into that plant’s operations. (In a possibly related case, after the close, Bloomberg reported that the joint venture is working on a deal to give employees at that plant a 33% raise plus back pay.) At mid-morning, drugmaker Mallinckrodt (MNKKQ) told Reuters it expects to file for a second bankruptcy in the next few days. This comes after the drugmaker reached a deal with victims who had agreed to accept $1 billion less in their settlement with the company over opioid distribution practices. Later, a court in Kenya ordered META into mediation in the company’s dispute with 184 content moderator employees and two contractors who were suing the company for unfair dismissal (because they were organizing a union). The court ruled META has 21 days to reach an agreement to resolve the dispute with the plaintiffs. In the afternoon, Reuters reported that UAL has agreed to a $30 million settlement after one day of trial in a case related to their treatment of a quadriplegic man in a vegetative state. Late in the day, a coalition of environmental activist groups sent a letter to the SEC, pushing to stop Brazilian meatpacker JBSAY from being listed (issuing an IPO) on the NYSE. After the close, GS, JPM, MS, and UBS agreed to pay $499 million to settle an antitrust lawsuit from investors, which had accused them of conspiring to stifle competition through their stock lending practices. Also after the close, the FCC announced it would be releasing the public comments made in a bid to deny the broadcast license renewal of the FOX TV station in Philadelphia. Comments made by the grassroots group “The Media and Democracy Project” have asked for denial based on FOX’s false and harmful information (lies) about the 2020 election. FOX dismissed the petition as frivolous and without merit, but the petitioners mentioned FOX’s $787.5 million defamation case settlement brought by Dominion Voting System and FOX internal communications released related to that case that proved the company knew the results of the election were valid but repeatedly lied about it anyway and knew that could lead to something like the January 6 riot attempting to stop official vote counting. At the same time, an FDA panel of independent experts voted against the approval of an MDT blood pressure treatment device.

After the close, ADSK, GES, NTAP, NVDA, SNOW, and SPLK all beat on both the revenue and earnings lines. It is worth noting that ADSK, GES, NVDA, and SPLK all also raised their forward guidance. It is also worth noting that there were some major surprise beats on earnings with NVDA surprising by 29.2%, SPLK surprising by 57.8%, GES surprising by 84.6%, and SNOW surprising by 120%. However, the most notable beat of the day was NVDA’s 170% jump in sales (year-on-year) resulting in a 27% beat on revenue…driven by AI processing demand (whose division sales more than doubled). NVDA also expects AI-related demand to continue increasing, more than doubling again in 2024. That is likely to drive markets (especially QQQ and SPY) this morning.

Overnight, Asian markets were mostly green on the back of the AI rally. Hong Kong (+2.05%), South Korea (+1.28%), and Taiwan (+1.17%) led the region higher. Only New Zealand (-0.60%) and India (-0.29%) were in the red. In Europe, we see a very similar picture taking shape at midday. Only Russia (-0.76%) and Finland (-0.05%) are in the red, while the CAC (+0.46%), DAX (+0.36%), and FTSE (+0.35%) lead the region higher. In the US, as of 7:30 am, Futures are pointing toward a mixed open. The DIA implies a flat open of -0.02%, the SPY is implying a +0.64% open, and the QQQ implies a +1.27% open at this hour. At the same time, bonds are back up a bit to 4.214% and Oil (WTI) is up fractionally to $79.04 per barrel in early trading.

The major economic news scheduled for Thursday includes July Durable Goods Orders and Weekly Initial Jobless Claims (both at 8:30 am), Fed Balance Sheet and Bank Reserve Balances with the Fed (both at 4:30 pm). The Central Bankers Jackson Hole Conference also starts at 8 am. The major earnings reports scheduled for before the opening bell include BURL, DLTR, NTES, WOOF, RY, TD, and WB. Then, after the close, GPS, INTU, MRVL, JWN, ULTA, and WDAY report.

In economic news later this week, on Friday, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Consumer Inflation Expectation, and Michigan Consumer 5-year Inflation Expectations are reported. Fed Chair Powell also speaks as the Jackson Hole Conference continues.

In terms of earnings reports, there are no earnings reports scheduled for Friday.

In miscellaneous news, retail industry analyst Susquehanna reported that big retailers have already returned to a cost-cutting focus by going back to a just-in-time inventory model. Susquehanna analyzed the last 20 years of ocean container ship imports into the US looking for trends. They found that the “big 4” big box retailers (WMT, TGT, HD, and LOW) all reduced their inventories by more than 4% in Q2, which was the largest reduction since 2015. The analyst is predicting (based on discussions with retailer management) Q3 pre-holiday inventory builds will be larger than last year’s 6% quarter-on-quarter increase but far less than the 14% average from pre-COVID years.

In late-breaking news, Turkey surprised markets this morning with an unexpectedly large rate hike of 7.5%, bringing that country’s main rate to 25%. The Dollar fell against the Turkish Lira almost immediately. Elsewhere, privately-held Subway (sandwich shops) sold itself to privately-held Roark Capitol. Roark already owned Dunkin Donuts, Baskin-Robbins, Sonic, Arby’s, Buffalo Wild Wings, and a host of other restaurant industry brands. Finally, Bloomberg reported that China has a major $9 trillion “off the books” debt problem. It seems that this is the amount of debt held by Chinese local governments through state-owned companies set up to borrow on behalf of province and local government entities. The problem is that the local governments have not been able to raise enough income (tax revenue) to pay the interest on that $9 trillion in hidden debt. So, banks are unwilling to lend to those entities and investors are not buying bonds issued by those financing companies. If there were a default by any of those shadow funding agencies, China’s entire $60 trillion financial system would be at risk of collapse.

So far this morning, BURL, DLTR, FRO, RY, and SN all reported beats on both the top and bottom lines. Meanwhile, NTES and WB missed on revenue while beating on earnings. On the other side, WOOF and TD beat on revenue while missing on the earnings line. It is worth noting that WOOF lowered its forward guidance.

With that background, it looks like the premarket is giving us a similar feel as the Wednesday normal session. SPY and especially QQQ gapped higher and will open with significant gains. Meanwhile, DIA is stuck in the mud and not participating. It is interesting that all three of their premarket candles are indecisive candles (after the gaps from the two broader ETFs). SPY and QQQ are above their T-line (8ema) while DIA remains just below its own T-line. The morning gap will also see the QQQ well up above its 50sma and the SPY retesting its 50sma from below. So, the short-term downtrend has been broken in the SPY and QQQ, but the DIA remains in just a consolidation. Of course, the much longer-term trend is still bullish since last year but that has been pushed hard recently by the Bears. As far as extension goes, the morning gap may have QQQ a little extended above its T-line but the other two are not far from that average. The T2122 indicator is also back in its mid-range, so there is plenty of room to move in either direction, say it with me, if we can find the momentum.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Mixed results from the retail sector suggest that consumers are inflation worry and beginning to make different choices in their spending fading premarket gains and ending the day lower. The T2122 indicator continues to signal a short-term oversold condition on a light volume day as investors dealt with more banking downgrades and higher bond yields adding to the pressure. However, the highly anticipated NVDA earnings and the talking head marketeering from Jackson Hole could quickly shift sentiment for a relief rally. Of course, the results from today’s earnings and economic reports will have something to say about direction and could keep volatility high.

Asian market traded mixed after business activity reports from Australia and Japan. European markets look to extend yesterday days gains with gains across the board this morning despite lower PMI numbers. U.S. futures once again push for a bullish open but have already faded slightly after early retail earnings results.

The eurozone economy showed signs of recovery in the second quarter of 2021, despite the impact of the Covid-19 pandemic. According to the latest data, the region’s gross domestic product (GDP) grew by 0.3% in the April-June period, compared to 0.1% in the previous quarter. However, this growth rate was still lower than the pre-pandemic level, as the data excluded the months when most countries imposed lockdowns and restrictions to contain the virus. If the pandemic months are excluded, the latest numbers point to the lowest reading since April 2013. The European Central Bank (ECB) is expected to maintain its accommodative monetary policy stance, as analysts predict that it will leave its main interest rate unchanged at 3.75%. The ECB has been providing stimulus to the eurozone economy through its quantitative easing program and its pandemic emergency purchase program. The bank will announce its next policy decision on September 7, 2021.

FedEx pilots are facing uncertainty about their future as the company struggles with a sharp decline in package volume. According to the latest statistics, FedEx Express delivered 3.19 million packages a day within the US during its fiscal year 2022, down from 3.283 million in fiscal 2021. This drop in demand is partly due to the impact of the Covid-19 pandemic, which disrupted global trade and travel, as well as the loss of some major customers, such as Amazon and Walmart. FedEx has been trying to cut costs and improve efficiency by consolidating its operations and offering voluntary buyouts to some employees. However, some pilots fear that these measures may not be enough to avoid layoffs or furloughs in the near future.

Japan is preparing to release more than a million tons of treated radioactive water from the Fukushima Daiichi nuclear power plant into the Pacific Ocean, a controversial decision that has sparked protests and criticism from its neighbors. The water release, which is expected to start in 2023 and take decades to complete, comes more than 10 years after a massive earthquake and tsunami triggered the second-worst nuclear disaster in history, causing meltdowns at three reactors and forcing the evacuation of thousands of people. Japan’s government has argued that the discharge of the water, which has been filtered to remove most of the radioactive elements except for tritium, is safe and necessary to make room for more contaminated water accumulating at the site. The U.N.’s nuclear watchdog, the International Atomic Energy Agency (IAEA), has endorsed the move, saying Tokyo’s plans are consistent with international standards and will have a “negligible” impact on people and the environment. However, neighboring countries such as China, South Korea, and Taiwan are far from happy, as they fear the water release will harm their marine ecosystems, fisheries, and public health.

U.S. stocks ended the day in the red after retail earnings showed mixed results and consumers changing spending habits. Macy’s, a major retailer, reported that it had more credit card defaults than expected in the second quarter, which made investors worry about the U.S. consumer’s spending power. The financials sector also suffered a hit, as S&P Global lowered the ratings of five U.S. regional banks on Monday and bond yields continued to rise adding additional pressure. Today we have a busier earnings calendar with the highly anticipated report from NVDA after the bell with PMI, New Home Sales, and Petroleum Status data pending on the economic calendar.

On Tuesday, the SPY and QQQ gapped up while the DIA opened flat. SPY opened 0.39% higher, QQQ opened 0.70% higher and DIA opened up only 0.01%. However, at that point, all three major index ETFs spent the rest of the day in a slow downtrend. (It is worth noting that QQQ’s downtrend was more volatile and roller-coaster-like than the large caps, but all three made the same slow trip lower.) This action gave us large-body, black candles in all three. The SPY printed a Dark Cloud Cover candle that failed a retest of its T-line (8ema). QQQ also failed a retest of its 8ema but failed to did not print a candle signal. For its part, the DIA did not even get close enough to test its T-line again but did print an Evening Star signal.

On the day, seven of the 10 sectors were in the red with Financial Services (-0.92%) out front leading the way lower while Utilities (+0.30%) held up better than the other sectors. At the same time, the SPY lost 0.27%, DIA lost 0.50%, and QQQ lost 0.14%. VXX was basically flat to close at 25.14 and T2122 climbed slightly gain but remained well into the oversold area at 10.00. 10-year bond yields rebounded after they opened lower to close at 4.332% while Oil (WTI) fell 0.58% to close at $80.25 per barrel. This happened on a well-below-average volume in all three of the major index ETFs. So, volatility reigned in the morning, but the Bulls took over for the second half of the day.

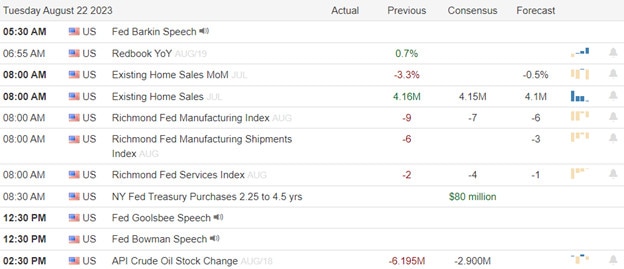

The major economic news reported Tuesday was limited to July Existing Home Sales which came in a bit below expectation at 4.07 million (compared to a forecast of 4.15 million and a June reading of 4.16 million). That corresponded to a 2.2% decrease month-on-month coming after a 3.3% month-on-month decline in June. (Curiously, at the same time, the median home price rose 1.9% to $406,700, just the fourth time the average has topped $400,000.) Then, after the close, the API Weekly Crude Oil Stocks Report showed a smaller-than-expected draw on inventories at 2.418 million barrels (versus a forecast calling for a drawdown of 2.900 million barrels but much less than the prior week’s 6.195-million-barrel drawdown).

In Fed speak, Richmond Fed President Barkin told Reuters Tuesday that the Fed needs to be aware of the possibility that the US economy may accelerate rather than slow in the coming months. If it does, that would have implications for the FOMC’s fight against inflation. He noted that US Retail Sales were stronger than expected in July and Consumer Confidence is also rising. Barkin said, “The reacceleration scenario has come onto the table in a way that it really wasn’t three or four months ago.” He went on to say, “If I got convinced that inflation was remaining high and demand was giving no signal that inflation was going to come down, that would make the case (for further tightening of monetary policy).” Related to bond rates, Barkin told Reuters, “It doesn’t strike me that having a 10-year (bond) rate over 4 percent is somehow wildly inappropriate.”

In stock news, META announced a new AI model that can transcribe and translate 100 languages on Tuesday morning. The model (SeamlessM4T) offers speech recognition as well as all the speech-to-text, text-to-speech, text-to-text, and speech-to-speech translation modes. In other META news, the company rolled out a web-based version (pre-announced a day earlier) of Instagram Threads. Later, IBM announced it had agreed to sell its weather business to private equity firm Francisco Partners for an undisclosed amount. (The Wall Street Journal previously reported IBM was seeking to sell the unit at a $1 billion valuation.) Elsewhere, VMW (in the process of being bought by AVGO) announced it has partnered with NVDA to launch a set of tools that will allow customers to create their own AI applications on NVDA hardware running in their own data centers (as opposed to buying AI processing from cloud vendors like MSFT and AMZN). In the afternoon, industry watchers said that TSLA’s 13,900 new insurance registrations in China last week added to the 14,000 from the week prior and 12,800 the week before suggests a strong August sales pace for TSLA, at least in China. In M&A drama news, CLF demanded Tuesday afternoon that X reveal all of its buyout offers. X has previously rejected CLF’s $7.3 billion cash-and-stock offer and has also received offers (that we know of) from MT and private firm Esmark. Just after the close, the Teamsters announced their 340,000 UPS workers had approved the new 5-year contract recently agreed between the union and company.

In stock legal and regulatory news, some AAL Pilots are fighting their union in the hope of extending their flying careers. The union opposed the bill in Congress (championed by airlines) that would raise the retirement age from 65 to 67. However, some pilots are going around their union (with the help of airlines) to lobby Congress on behalf of the bill. (An airline industry group says the law could “save” the industry 5,000 pilots over the next two years. Critical amidst an industry-wide pilot shortage.) At midday, the US Dept. of Justice announced that NMR had agreed to pay a $35 million fine, pay $808k in restitution, and take responsibility in written form in order to avoid prosecution for lying to customers about bond prices. (NMR had previously been fined $1.5 million and paid $20.1 million in restitution in a civil settlement with the SEC for the same fraud.) At the same time, the US Consumer Finance Protection Bureau filed suit against CURO, alleging the lender had pushed 10,000 struggling borrowers to simply refinance their short-term loans to increase their fees. Later, a “reverse discrimination” lawsuit was filed against GCI, but five current and former employees who claim the newspaper publisher discriminates against white staff in order to fulfill diversity goals. (No damage figure was provided.) At the same time, Bloomberg reported that FORG will be acquired by private equity firm Thoma Bravo after the US Dept. of Justice declined to challenge the deal. Later in the afternoon, MO filed a complaint with the US International Trade Commission seeking to ban the import of rival Juul products, which MO claims infringe on two of its patents. Then, the US Interior Dept. approved a 704-megawatt wind farm off Rhode Island to be owned and operated jointly by DOGEF and ES. At the close, the US Dept. of Health and Human Services awarded $1.4 billion in grants, including $326 million for REGN to develop next-generation therapies and vaccines for future COVID-19 variants.

In volatility news, Vietnamese electric vehicle maker VFS (VinFast) continued its massively volatile ride in the six days since its IPO. On Tuesday, VFS closed up almost 109%after having been up more than 167% at one point in the session. At the same time, SRE fell almost 50% Tuesday while FN climbed 31.58% by the close.

After the close, LZB, TOL, and URBN all reported beats on both the revenue and earnings lines. It is also worth noting that TOL raised its forward guidance.

Overnight, Asian markets were mixed but leaned toward the green side. Taiwan (+0.85%), New Zealand (+0.75%), and Japan (+0.48%) led the more plentiful gaining exchanges. Meanwhile, China is still on the struggle bus with Shenzhen (-2.14%) and Shanghai (-1.34%) pacing the losers. In Europe, stocks are mixed with more of the bourses in the red than in the green at midday. The CAC (-0.14%), DAX (-0.03%), and FTSE (+0.64%) are typical of the spread with only Switzerland (+1.00%) moving more than a percent in early afternoon trade. In the US, as of 7:30 am, markets are looking to open just on the green side of flat so far. The DIA implies a +0.13% open, the SPY is implying a +0.13% open, and the QQQ implies a +0.06% open at this hour. At the same time, 10-year bond yields have backed down strongly again to 4.259%, and Oil (WTI) is down 1.52% to $78.42 per barrel in early trading.

The major economic news scheduled for Wednesday includes Building Permits (8 am), Preliminary August S&P US Mfg. PMI and Preliminary August S&P Global Composite PMI (both at 9:45 am), July New Home Sales (10 am), and EIA Crude Oil Inventories (10:30 am). The major earnings reports scheduled for before the opening bell include ANF, AAP, ADI, BBWI, DY, FL, GRAB, KSS, LANC, PTON, and WSM. Then, after the close, ADSK, GES, NTAP, NVDA, SNOW, and SPLK report.

In economic news later this week, on Thursday, we get July Durable Goods Orders, Weekly Initial Jobless Claims, Fed Balance Sheet, and Bank Reserve Balance with the Fed. The Central Bankers Jackson Hole Conference also starts. Finally, on Friday, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Consumer Inflation Expectation, and Michigan Consumer 5-year Inflation Expectations are reported. Fed Chair Powell also speaks as the Jackson Hole Conference continues.

In terms of earnings reports, on Thursday, BURL, DLTR, NTES, WOOF, RY, TD, WB, GPS, INTU, MRVL, JWN, ULTA, and WDAY report. Finally, on Friday, there are no earnings reports scheduled.

In miscellaneous news, accounting firm Ernst & Young reported that in 2022, for the first time ever, US oil and gas companies paid out more in earnings to shareholders than they spent on exploration and field development. The E&Y report said the top 50 US oil and gas producers spent $58.8 billion on buybacks and dividends while only spending $55.1 billion on exploration and development. The report predicted the trend will continue as well as seeing more money plowed into acquisitions rather than actual finding and producing oil and gas. Elsewhere, Bloomberg reported Tuesday evening that bond sales by US financial institutions topped $2 trillion so far this year, reaching that milestone in the fastest time ever. This comes the same day that S&P downgraded 10 US regional banks, including KEY and CMA. Finally, mortgage demand dropped to a 28-year low as interest rates spiked last week. The national average rate for a 30-year, fixed-rate, conforming loan spiked to 7.31%. This caused new purchase loan applications to fall 5% for the week while refinance applications dropped 3%.

So far this morning, ANF, DY, GRAB, and KSS all beat on both the earnings and the revenue line. Meanwhile, BBWI missed on revenue while beating on earnings. On the other side, AAP and PTON both beat on revenue while missing on earnings. However, ADI and FL missed on both the top and bottom lines. It is worth noting that ADI, FL, and PTON all lowered their forward guidance.

With that background, it looks like the market is tepid at this hour. While the premarket session opened higher, all three major indices are printing black candles in the early session and have fallen back near Tuesday’s closing level. The SPY and QQQ are failing another retest of their T-lines (8ema) on the early move. The short-term trend remains bearish. Also, on top of the normal resistance levels, all three major index ETFs have to climb through their T-lines AND their 50sma (where they are all flirting with a Blue Ice Failure pattern) to make a push. In other words, the Bulls have their work cut out for them at this point. With that said, the SPY and especially the QQQ are trying to reverse to break the downtrend. Of course, the much longer-term trend is still bullish since last year but that has been pushed hard recently by the Bears. As far as extension goes, there is no issue with extension below the T-line (8ema). However, the T2122 indicator remains oversold, although it isn’t pegged to the bottom of its range. So, once again we have room to move in either direction, but the relief pause or bounce may be here. Just remember the market can remain too extended a lot longer than we can remain solvent betting on a reversal that has not happened yet.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The highly anticipated earnings from NVDA on Wednesday brought out the speculators surging the stock price that drove a Nasdaq rebound on Monday. However, the DIA and IWM struggled to find footing making for a choppy day even as the short-term oversold condition suggests a relief rally to at least test overhead resistance levels. With a bit more potential inspiration on the earnings and economic calendar perhaps the relief can continue to gain strength today but keep an eye on the rising bond yields that hint the Fed may not be done with rate increases.

Asian markets enjoyed a relief rally overnight shaking off the rising bond yields and worries over the Chinese economy. European markets look to extend the relief started yesterday with the tech sector leading the way. U.S. futures also point to a bullish open ahead of earnings and economic reports as bond yields push to levels not seen since 2007.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday include BJ, SCIQ, COTY, DKS, LZB, LOW, M, MDT, TOL, and URBN.

News & Technicals’

The U.S. banking sector is facing increased pressure from the global rating agency S&P Global, which downgraded the credit ratings and outlooks of several major banks on Monday. The agency cited the challenges posed by the ongoing pandemic, low-interest rates, and heightened competition as the main factors that could erode the banks’ profitability and credit quality. S&P Global followed the footsteps of Moody’s, which also lowered its ratings and outlooks for some U.S. banks last week. Both agencies warned that the banks could face higher funding costs and lower earnings in the near future.

Lowe’s announced its second-quarter results, showing a solid performance amid the high demand for home improvement products and services. The company reported a net income of $3.02 billion, or $4.25 per share, up from $2.83 billion, or $3.74 per share, a year earlier. This beat the consensus estimate of $4.01 per share. However, the company’s revenue fell slightly short of expectations, as it recorded total sales of $27.57 billion, compared to the forecast of $27.75 billion. Lowe’s attributed the revenue miss to the supply chain disruptions and labor shortages that affected its ability to meet customer demand. Despite the challenges, the company reaffirmed its full-year guidance, expecting a sales growth of 4.5% and an operating margin of 12.2%.

Zoom continued to enjoy strong growth in the second quarter, as more people and businesses relied on its services for remote work and communication. The company reported a revenue of $1.02 billion, up 54% year-over-year, and surpassing the analysts’ estimate of $991 million. The company also posted a net income of $317 million, or $1.08 per share, compared to $186 million, or $0.63 per share, a year ago. This exceeded the consensus forecast of $0.99 per share. Zoom also raised its full-year guidance, expecting revenue of $4.01 billion to $4.02 billion, and earnings per share of $4.75 to $4.79. Zoom also introduced a new feature that allows customers to start free trials for automated meeting summaries without recording calls, enhancing its product offerings and customer experience.

The S&P 500 and the Nasdaq rebounded from a three-week slump, led by a surge in NVDA heading into its highly anticipated earnings report on Wednesday. European stocks also rose, while Asian markets were mixed amid ongoing worries about China. Government bond yields climbed to multiyear highs ahead of the Fed’s annual Jackson Hole meeting. The 10-year Treasury yield reached 4.33%, the highest since 2007, and the 30-year yield hit 4.45%, the highest since 2011 putting more pressure on the banking sector and consumers. Today we face reports on Existing Home Sales, Richmond Fed Mfg. along with a couple of Fed speakers. We also have several notable earnings reports for the bulls or bears to find inspiration with a retail theme. Plan for volatility to continue with higher rates worries about the Chinese economy and banking downgrades.

Monday gave us a morning roller-coaster. The SPY gapped 0.24% higher, DIA opened just 0.04% higher, and QQQ gapped up 0.40%. The SPY and QQQ then rallied until 10:10 am. Meanwhile, DIA only managed to grind sideways until 9:45 am. Then, all three major index ETFs sold off steadily until 12 pm. At that point, QQQ was back at the opening level, SPY had crossed back below Friday’s close, and DIA had fallen significantly below Friday’s close. However, at noon, the Bulls stepped in to drive a strong, steady rally that lasted until a modest pullback in the last 15 minutes. This action gave us a large, white-bodied candle in the QQQ which barely failed a retest of its T-line on the last-minute profit-taking. For its part, SPY gave us a white Spinning Top candle. Finally, the DIA printed a black Spinning Top candle.

On the day, six of the 10 sectors were in the red with Utilities (-0.66%) leading the way lower while Technology (+1.42%) was far out front, holding up better than the other sectors. At the same time, the SPY gained 0.65%, DIA lost 0.13%, and QQQ gained 1.61%. VXX fell 2.64% to close at 25.03 and T2122 climbed slightly but remains deep into the oversold area at 8.66. 10-year bond yields spiked higher to close at 4.342% while Oil (WTI) fell 0.43% to close at $80.90 per barrel. This happened in average volume in the QQQ and below-average volume in the SPY and DIA. So, volatility reigned in the morning, but the Bulls took over for the second half of the day.

There was no major economic news reported Monday. However, Reuters did report that a “feud” between centrist and hardline Republicans in the US House has raised the risk of a government shutdown. The “Freedom Caucus” are pushing for spending $120 billion less than the deal agreed in June between the President and House (taking another bite of the apple). That group also announced its opposition to any stopgap measures to keep the government open. Other Republicans are looking for spending on top of the June level for defense, veteran benefits, and border security. If those two ideas were taken together, it would result in a 25% budget cut in the rest of the budget (including the infrastructure spending the President and Congress have been actively taking credit for recently). The centrist group (who now call themselves the “Governing Republicans”) say the hardliners ignore the reality that Senate Democrats are not going to go along with their priorities. As a result of this schism, GS reported Monday they now feel a shutdown is more likely than not. Current funding ends on September 30 for all 12 appropriations bills and Congress does not return from recess until September 12. At the same time, the National Federation of Independent Business released the results of its quarterly small business owner survey. The survey found 52% believe the US is already in recession, which is actually down slightly from 55% in April. However, 80% said the economy was “okay” or better, and most said their own business financial situation was “strong.” More than half also said they were less concerned about the health of their own bank, which is a dramatic increase from 31% which had that opinion in April.