UAW Begins 3-Plant Strike and Data Ahead

On Thursday, markets gapped higher, opening up 0.57% in the SPY, up 0.59% in the DIA, and up 0.44% in the QQQ. However, the Bears said “Not so fast” as all three major index ETFs started immediately selling and didn’t stop until 10:25 a.m. The QQQ even recrossed its opening gap during that move. Still, that was the last we heard from the Bears as the Bulls stepped in to lead a rally that lasted the rest of the day (although to be fair, most of the afternoon was more of a sideways grind). This action gave us gap-up, white-bodied, Spinning Top candles in all three major index ETFs. All three are back above their T-line (8ema) and 50sma. QQQ even retested its T-line from above and passed the test while DIA did the same with its 50sma.

On the day, all 10 sectors were in the green with Basic Materials (+1.89%) out in front, leading the rest of the market higher, while Healthcare (+0.35%) lagged well behind the other sectors. At the same time, the SPY gained 0.86%, DIA gained 1.00%, and QQQ gained 0.82%. This all happened on just below-average volume in all three major index ETFs. (A bit better volume than we saw the three earlier days this week.) VXX dropped 2.93% to close at 19.91 and T2122 shot back up to just outside of overbought territory at 79.90. 10-year bond yields rose to close at 4.288% while Oil (WTI) spiked to end the day at $90.53 per barrel. So, with the exception of some “fade the gap” sentiment just after the open, it was the Bulls’ day and a pretty steady and boring one at that. Still, we closed just below potential resistance levels and that should not be ignored.

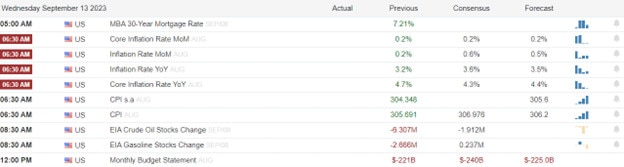

The major economic news reported Thursday included August Core PPI (month-on-month), which came in just as expected at +0.2% (right on the forecast but well down from the July +0.4% reading). However, August PPI (overall, not just core, month-on-month) came in hot at +0.7% (versus a forecast and July value of +0.4%). At the same time, August Core Retail Sales also came in above the predicted level at +0.6% (compared to a forecast of +0.4% but down from the July reading of +0.7%). Overall August Retail Sales (month-on-month) also came in well above anticipated at +0.6% (versus a forecast of +0.2% and even above the July +0.5% value). Later, July Retail Inventories were reported to have fallen, reported at flat +0.0% compared to the June +0.1% reading. At the same time, July Business Inventories also came in flat at +0.0% (below the forecast of +0.1% but up from the June -0.1% value). Finally, after the close, the Fed Balance Sheet Weekly report showed a continued decline but a much smaller one this week. This week it fell just $2 billion from $8.101 trillion to $8.099 trillion. This was the smallest decrease since March.

In new issue news, the much-hyped ARM IPO went live Thursday, opening at $56.21 after the stock had priced at $51. It traded as high as $66.25, as low as $55.55, and closed at $63.59. Elsewhere, a new ETF (QQQY) began trading Thursday that is aimed at taking advantage of the craze of zero and short-dated equity options. The new ETF aims to achieve a monthly yield for investors by selling 0DTE put options on the Nasdaq-100 index (hoping to capture the premium) in combination with buying Treasuries.

In stock news, UP appointed a member of the DAL board (George Mattson) as its new CEO. This came weeks after UP received a $500 million lifeline loan from a consortium of airlines (including DAL). Later, NVO announced it still intends to split its stock (ADR) 2-for-1 on September 20, despite its 23% surge since August 4 and 41% gain this year. Elsewhere, Reuters reported unnamed sources tell it that TSLA is very close to announcing new manufacturing technology that will allow the company to die-cast the entire underbody of its cars. (As opposed to making or buying and then assembling 400 underbody components now.) If/when implemented, a large amount of labor and cost would be removed from each car, allowing TSLA to achieve lower prices, higher margins, or more likely both. The technology would also allow TSLA to launch a new vehicle designed from the ground up in 18-24 months versus the current 3–4-year timeline. At the same time, TSM announced that it has acquired a 10% stake in the INTC Nanofabrication business unit for $430 million. This comes after INTC sold a 20% stake in the unit to Bain Capital. By midday, CZR disclosed that it had also suffered a cyber attack (and paid a $15 million ransom to the attackers) before MGM suffered a very similar attack Sunday. At the same time, the CFO of T said the company is optimistic it will reach its full-year free cash flow forecast of $16 billion. After the close, Reuters reported the new CEO of BAYRY plans to cut management jobs as a first step in his plan to overhaul the German industrial/chemical giant. (No number of jobs or timetable was provided.) Also after the close, Reuters reported that DIS has had preliminary talks with NXST over the sale of DIS subsidiary ABC. (NXST operates a regional network of TV stations.)

In stock government, legal, and regulatory news, the Indian state of Goa told ABT that it plans to suspend the company’s antacid manufacturing license. This comes after Goa authorities found contamination risks and sanitation issues in the plant. (ABT has a 7% share of the Indian market in that segment with annual sales of about $11 million.) Later, a day after France halted the sale, Belgium said Thursday it is reviewing the potential health risks of AAPL iPhone 12 models. However, there does not appear to be an EU-wide ban movement underway yet as the European Commission is waiting on feedback from its member countries before deciding on what, if any, action to take on the matter. By midday, the US Supreme Court froze an order by a lower court that had curbed the Biden Administration’s ability to engage with social media companies like META, GOOGL, and X (Twitter) in an effort to get them to remove misleading, false, or dangerous content. In stock legal news, GOOGL hinted at part of its antitrust defense. The search giant shared data it says shows that users are “happy to stick with Google search when pre-installed on their devices and quickly switch when competing search engines are pre-installed.” On the other side, the government introduced evidence showing that GOOGL spends $10 billion each year to keep Google as the default search engine in phones, tablets, and browsers. In the afternoon, a proposed class action lawsuit was filed against several companies, including JNJ, PG, WBA, GSK, and KVUE alleging these companies deceived consumers in advertising of over-the-counter cold medicines that contain an ingredient an FDA panel just recently unanimously ruled was ineffective (no more effective than placebo). No damage information is available yet, but that segment of products generates about $1.76 billion in annual sales in the US. After the close, GOOGL agreed to pay the state of CA $93 million to resolve a lawsuit claiming the company’s search engine misled consumers about its location tracking practices. (GOOGL continues to track and use people’s location data for advertising even after they have turned off the “Location History” setting.) Also after the close, UBER said it would appeal a $205 million fine from a Brazilian court over a ruling that the company used “irregular labor relations” for treating drivers as contractors and not as employees.

After the close, ADBE, CPRT, and LEN all reported beats on both the revenue and the earnings lines. (ADBE and CPRT both had actual quarter-on-quarter earnings growth while LEN beat a reduced number.) It is worth noting that both ADBE and LEN raised their forward guidance.

Overnight, Asian markets were mostly green again. Only Shenzhen (-0.52%), Shanghai (-0.28%), and Thailand (-0.20%) were in the red. The other nine Asian exchanges were led higher by Australia (+1.29%), Japan (+1.10%), and South Korea (+1.10%). In Europe, with the sole exception of Russia (-0.08%), the bourses are green across the board at midday. The CAC (+1.66%), DAX (+1.07%), and FTSE (+0.83%) are leading a broad and strong move higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mixed and modest start to the day. The DIA implies a +0.22% open, the SPY is implying a +0.09% open, and the QQQ implies a -0.08% open at this hour. At the same time, 10-year bond yields are popping higher at 4.324% and Oil (WTI) is up slightly to $90.66 per barrel in early trading.

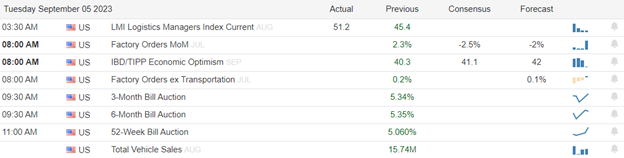

The major economic news scheduled for Friday includes August Export Price Index, August Import Price Index, and NY Empire State Mfg. Index (all at 8:30 a.m.), August Year-on-Year Industrial Production and August Month-on-Month Industrial Production (both at 9:15 a.m.), Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Consumer 12-month Inflation Expectation, and Michigan Consumer 5-Year Inflation Expectations (all at 10 a.m.). There are no major earnings reports scheduled for either before the open or after the close.

In Autoworker contract talks or strike news, GM sweetened its offer to include a 20% pay increase over 4 years as well as an unclear inflation-protection mechanism, and an increase to 5 weeks of vacation. For their part, F CEO Farley made no new offer but told reporters that the UAW’s 40% wage hike demand would put the company out of business (in bankruptcy). In addition, Farley said he has not received a counter-offer to the company’s 20% wage increase proposal. (To be fair, the union did lower its demand to a 36% increase over the new contract.) With just eight hours left until the current contract expired, the AP reported the sides remained far apart and the union’s targeted individual-plant strikes looked unavoidable. In the end, no deal was reached and at midnight, autoworkers went on strike at three key plants. The GM truck and van plant in MO, the F Ranger and Bronco pickup plant in MI, and the STLA Jeep plant in OH are the first plants to see pickets. The UAW says the 3 strikes so far cover just 12,700 union members (over more than 146,000). The three plants selected produce high-profit vehicles for the automakers. (UAW President Fain had previously announced that the strikes will rotate, move to different plants, and increase in number to cause maximum uncertainty and disruption if the strike continues. The idea is to force the Big 3 to live with the chaos of unpredictable operations and shortages, even as most union workers continue to draw normal paychecks. However, the Big 3 also have the option of locking all union employees out by closing all their plants. Neither option is good for the three largest automakers.)

In miscellaneous news, China struck back (rhetorically) at the EU Thursday after European Commission President von der Leyen had announced an investigation into China over electric vehicle subsidies that allowed Chinese carmakers to flood the world (Europe) with EVs at artificially low prices. China, predictably, blasted the European Commission move as protectionist, and anti-competitive and said it would harm economic relations. This last part caused concern among the German car industry which sells a lot of cars in China. Meanwhile, in the US, frustrated GOP House Speaker McCarthy provoked and taunted right-wing members of his caucus over their threats and pseudo-extortion. (The most extreme members of the small right-wing “Freedom Caucus” have publicly threatened to force McCarthy out of his Speakership unless their list of demands is met in recent days.) McCarthy told Republican Congressmen that if they wanted to remove him, they should file the…motion, but they should get out of the way of “everybody’s work.” Specifically, he told them nobody wins a government shutdown and he is set on not having that happen. However, there are only 9 “working days” (16 calendar days) left before a shutdown is forced by the House’s failure to pass the 12 different required appropriation bills. Elsewhere, China cut the reserve requirements for banks for the second time this year. However, this intended stimulus was minor to say the least, reducing the cash reserves requirement by a quarter percent to 7.4%. Still, the move is expected to free up just under $69 billion for loaning and investment into medium and long-term projects.

With that background, it looks like markets are undecided this morning. The three major index ETFs are little moved from the Thursday close and are printing small candles in the premarket session. All three remain above their T-line (8ema) but they are also close to that average and could easily recross it if the Bears find some strength. The SPY, DIA, and QQQ are all also above their 50sma again this morning. So, for now, they market remains in a bullish trend. However, we should also note that there is an obvious potential resistance level just above the SPY, QQQ, and DIA. The short, mid, and long-term trends remain bullish, but action has been choppy within those trends recently. In terms of extension, as mentioned, none of the major index ETFs are far from their T-line and the T2122 indicator is now at the top of its mid-range. So, there is plenty of slack for either the Bulls or the Bears to make a move. Finally, this is Friday. So, pay yourself and prepare your account for the weekend with whatever hedging or lightening up is appropriate for your risk tolerance.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service