When I hear the word engulfing, I imagine a wave washing over a shore or a building being consumed by flames. To engulf means to sweep over something, to surround it, or to cover it completely. Thus, it should come as no surprise that a Bullish Engulfing pattern features one candlestick covering (or engulfing) another. This two candlestick pattern occurs after a downtrend and is formed by one bearish candlestick (which is covered) and one bullish candlestick (which does the covering). It occurs frequently, so it is important that you learn to identify and interpret it. Ready for a quick lesson? To learn more about the Bullish Engulfing pattern’s formation and meaning, simply scroll down.

Markets started the day flat Thursday, down 0.02% in the SPY, down 0.03% in the QQQ, and down 0.05% in the DIA. However, the SPY and QQQ immediately sold off, reaching the low of the day shortly after 11 a.m. Then both began a slower rally that took them back to their highs (high of the day in SPY) about 2:45 p.m. From there, the pair of index ETFs traded sideways with a very modest bearish trend for the last 75 minutes. Meanwhile, DIA traded sideways in a very tight range for an hour after the open. Then it followed the other major index ETFs lower, finding its lows at about 11:50 a.m. At that point, DIA traded sideways until 1:15 p.m. before following the SPY and QQQ higher until 2:45 p.m. From there, DIA traded sideways in a tight range for the rest of the day.

On the day, six of the 10 sectors were in the red with Consumer Defensive (-1.67%) way out in front (by almost a full percent) leading the way lower. Meanwhile, Financial Services (+0.76%) held up better than the other sectors. At the same time, the SPY lost 0.04%, DIA gained 0.06%, and the tech-heavy QQQ lost 0.29%. VXX fell 1.28% to close at 23.97 and T2122 climbed but still remained well into the oversold territory at 9.09. 10-year bond yields basically bobbed along sideways after Wednesday’s “fall” to close at 4.714% while Oil (WTI) dropped another 2.10% to end the day at $82.45 per barrel.

This action gave us very indecisive candles in all three major index ETFs. The DIA and SPY printed Dojis that remain below their T-line all day. At the same time, QQQ printed more of a black-bodied Spinning Top which retested its T-line before closing just below it again. This all happened on below-average volume in all three major index ETFs. So, we saw a flat open followed by a selloff, a rebound, and finally a lack of conviction in the last hour. That probably tells us Mr. Market is just waiting on the next shoe to drop this morning (September Payrolls and Unemployment data in the premarket).

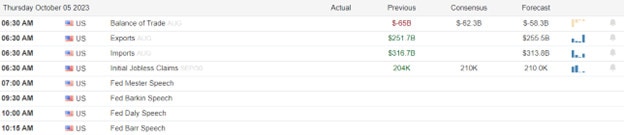

The major economic news reported Thursday included August Exports, which came in higher than the previous month at $256 billion (compared with $251.9 billion in July). At the same time, August Imports were down slightly to $314.3 billion (versus July’s $316.6 billion). Together this gave us an August Trade Balance (Deficit) of $58.3 billion which was better than expected (compared to a forecast of -$62.3 billion and July’s -$64.7 billion. After the close, the Fed’s Balance Sheet came in below $8 trillion for the first time in over two years at $7.956 trillion (down $46 billion on the week). Much of the drop was attributed to a big drop in the credit being given to deal with bank failures.

In Fed speak, Chicago Fed President Goolsbee told Bloomberg he doesn’t see treasury yields threatening a soft landing. (To be fair, the interview was recorded before rates hit 7.5%.) Goolsbee said “On the real side I feel like nothing has happened so far that is convincing evidence that we are off the golden path.” (Goolsbee has been referring to the Fed path to a soft landing as “the golden path.”) Later San Francisco Fed President Daly hinted at keeping rates steady at the next Fed meeting. Daly said, “If we continue to see a cooling labor market and inflation heading back to our target, we can hold interest rates steady and let the effects of policy continue to work.” Finally, Richmond Fed President Barkin said that surging Treasury yields reflect the strong economic data we’ve seen lately along with a heavy supply of bonds in the market. (More bonds available drive down bond prices, which automatically drives up the bond yields.)

In Autoworker contract talks and strike news, GM revealed Thursday that it has made a counter-offer to the UAW. (No details were released.) Elsewhere, Reuters reported details of the tentative deal between the UAW and VLVLY (Volvo Mack Trucks). The report showed a 19% hike over 5 years (10% immediately) plus a $3,500 “ratification bonus,” improved benefits (including a $1,000 annual addition to each 401K plan), additional vacation days, and a reduction in the tier-structure (the time it takes to get to top pay scale). The deal must still be ratified by 4,000 hourly UAW workers. Meanwhile, UAW President Fain announced he will hold another 2 p.m. Eastern streaming event to update workers on the progress of the talks. In his post-scheduling the event, he hinted there might be an expansion of the strike but that all three of the automakers may not be hit.

In stock news, BHP told Reuters Thursday that it intends to focus on cost-cutting rather than M&A to improve results over the next year. Without setting a goal or forecast, the CEO said “If we can cut our cost base by 10%, that’s $20 billion in value…the last time someone created $20 billion with an M&A – I’d like them to tell me when it was.” At the same time, XOM raised its Q3 profit forecast by $1 billion, citing escalated oil prices. Elsewhere, a study published in the JAMA Medical Journal showed a link to increased stomach paralysis and other rare gastrointestinal issues for NVO’s wildly popular diabetes drugs Ozempic, Wegovy, and Saxenda which are all widely used for significant weight loss. Bloomberg said the study found patients on one of those drugs are nine times more likely to develop swelling of the pancreas than a competing diabetes drug. At the same time, C outlined its layoff process for eliminating layers of management in a brief internal meeting on Thursday. No specifics were given, but Reuters reports the next layoffs will hit in November. A bit later, CLX announced that its sales took a hard hit from a cyber-attack but also acknowledged a “challenging consumer environment.” In the early afternoon, GSK announced it had raised $1.1 billion by selling 270 million shares of Haleon Plc in the UK. The funds will reportedly be rolled back into its Pharma business unit (Haleon is just an investment). Meanwhile, STLA announced a $90 million investment in Argentina Lithium & Energy. STLA will hold 19.9% ownership as a result of the deal. Late in the day, MRTX shares jumped after Bloomberg reported rumors that French Pharma giant SNY is exploring an acquisition of MRTX. After the close, MGM announced it expects operational disruptions from its September cyber-attack to negatively impact Q3 results.

In stock government, legal, and regulatory news, the UK announced Thursday morning that it will investigate the AMZN and MSFT dominance of the cloud computing market. (The two combined have 80% market share with GOOGL being the closest competitor with 5%-10% of the market.) Later, the Commerce Dept. said it is examining TSM, whose $40 billion AZ plant is a crucial planned recipient of US CHIPS Act funds. Recent information indicates that nearly half of the project’s workforce comes from Taiwan. This is, of course, contrary to the act’s goal of increasing US employment and chip manufacturing capability. (TSM has had a very hard time filling jobs with qualified, i.e., experienced, US workers and has found it most expedient to bring in staff from the Taiwanese facility, of which the AZ fab is designed to be a mirror image.) Elsewhere, GIFI announced a settlement of a lawsuit with Hornbeck Offshore Services. After the settlement, the court dismissed the suit. (No terms were released.) At the same time, principally INTC, NVDA, and QCOM (but including others) launched a large-scale lobbying campaign in Washington in a bid to defeat semiconductor sales to China. (NVDA was particularly vocal with the trio above claiming the restrictions could cost their firms $50 billion in lost sales per year from China.) The three companies also testified before a House committee hearing Thursday. Later, TSLA asked the Mexican government to build new infrastructure in the Northern Mexican state where the company intends to construct a new car plant. (These improvements included upgrades to the region’s electric grid and railway system.) In the afternoon, the NHTSA held a public hearing and recommended the government mandate a recall of 52 million air bag inflators (11 million of those produced under license by ALV). These inflators were used between 200 and 2018 by 12 different car makers. At the close, the SEC sued TSLA CEO Musk related to his X (Twitter) purchase. The SEC is attempting to force Musk to testify in the agency’s probe of his purchase of the company. (Musk defied a subpoena to appear on Sept. 15 from the agency.)

After the close, LEVI missed on revenue while beating on earnings. The company also cut its full-year guidance again. (It cut forward guidance just 3 months ago as well.)

Overnight, Asian markets were mostly green. Thailand (-0.97%) was the only major outlier to the downside while Hong Kong (+1.58%) was an outlier to the upside. Singapore (+0.61%) and India (+0.55%) were the more typical leaders to the upside. In Europe, we see the same picture taking shape at midday with only two of the 15 bourses showing red. The CAC (+0.69%), DAX (+0.83%), and FTSE (+0.40%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., markets are now looking to start the day on the upside. (Of course, this is pre-Payrolls data.) The DIA implies a +0.20% open, the SPY is implying a +0.21% open, and the QQQ implies a +0.27% open at this hour. At the same time, 10-year bond yields are higher at 4.744% and Oil (WTI) is just on the green side of flat at $82.43 per barrel in early trading.

The major economic news scheduled for Friday includes Sept. Avg. Hourly Earnings, Sept. Nonfarm Payrolls, Sept. Private Nonfarm Payrolls, Sept. Participation Rate, Sept. Unemployment Rate (all at 8:30 a.m.). We also hear from a Fed speaker (Waller at noon). The major earnings reports scheduled for before the open are limited to. There are no major earnings reports scheduled for Friday (either before the bell or after the close).

In miscellaneous news, Nat Gas hit a price not seen since January as the commodity broke $3 to close at $3.184. After hours, AMC announced that cultural phenom Taylor Swift is helping it rake in money. A film of Swift’s recent Eras tour will open on Oct. 13 and has already surpassed $100 million in advance ticket sales. Meanwhile, Politico reports that in the wake of the GOP mess in Congress, the Biden Administration is now looking at using State Dept. grants as a way to send more weapons to Ukraine. The idea seems to be grating the money to Ukraine who would use the funds to buy arms from US weapons manufacturers such as GD, NOC, and RTX. (The same mechanism has been used to transfer weapons to Taiwan in the past.) At the same time, the National Assn. of Realtors said the average US mortgage rate has now hit a 22-year peak of 7.49% for a 30-year, fixed-rate loan.

In late-breaking news, TSLA announced it will cut its US prices again on its Model 3 and Model Y cars. (A 3%-4% cut in Model 3 prices and a 3.7% cut in Model Y.) The move comes after TSLA vehicle deliveries for Q3 missed the market expectations. At the same time, PHG (Philips) took a hit overnight as the FDA said it does not believe the data shared by the medical device maker is sufficient to evaluate the risks posed by the company’s recalled sleep apnea ventilators. (More than 10 million of those devices were recalled after a number of deaths were attributed to breathing toxic materials produced by the breakdown of some silicone components of the device.) Elsewhere, Bloomberg reports this morning that XOM is in “advanced talks” on buying PXD in a $60 billion deal. It would be the oil giant’s biggest acquisition since Mobil back in 1999. (The CEO of PXD had previously announced his retirement at year end.) Finally, a meeting between President Biden and Chinese President Xi next month is looking more likely. The meeting would take place on the sidelines of an APEC (Asia-Pacific Economic Cooperation) summit in San Francisco in Mid-November.

With that background, it looks like the Bulls are tentatively and indecisively in charge prior to today’s data drop. All three major index ETFs are easing closer to their T-line (8ema) from below. All three are also printing very small, white-body, Spinning Top type candles very early. In terms of extension, none of the three major index ETFs are far below their T-line (8ema) but the T2122 indicator is now in the middle of its oversold range. So, we are not extremely oversold and have some slack to run with if either the Bulls or Bears can find energy. Expect some volatility at 8:30 a.m. and again at the open (and possibly when the UAW streams its news mid-afternoon). Also remember that this is Friday, payday, and time to get your account ready for the weekend news cycle. Just remember, the first rule of making big money in the market is to not lose big money in the market.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The price action Wednesday produced a sputtering relief rally that provided some hope through the lack of momentum kept uncertainty high. The sharp decline in the ADP signaled a weakening jobs market while at the same time suggesting the rising rate increases may be coming to an end. Big tech names enjoyed the majority of the bullish energy while the energy sector sector pulled back sharply on worries of consumer demand declines. Today we face data from International Trade, Jobless Claims, Natural Gas figures, as well as several Fed speakers to find bullish or bearish inspiration. Plan your carefully with the likely market-moving Employment Situation report before the bell on Friday.

Overnight Asian markets closed mixed but mostly higher inspired by the pullback in treasury yields. European markets are also showing some relief with modest gains across the board this morning despite the plunge in Metro Bank. Though U.S. Future has recovered some of its overnight lows they still suggest a modestly lower open ahead of trade and jobless numbers. Buckle up for another day of uncertainty as we wait on the big Friday jobs report.

Economic Calendar

Earnings Calendar

Notable reports for Thursday include CAG, LW, STZ, LEVI.

News & Technicals’

Metro Bank, a British retail bank, saw its shares plunge by more than 29% on Thursday before trading was suspended by the London Stock Exchange. The reason for the sharp drop was the news that the bank was trying to raise £600 million ($727 million) in debt and equity, amid its financial troubles. The bank has been struggling since 2019 when it revealed a major accounting error that damaged its reputation and profitability. The bank has been trying to improve its balance sheet and reduce its costs, but it has faced challenges from the pandemic, the low-interest rate environment, and the intense competition in the UK banking sector. The bank said that it was in talks with existing and new investors to raise the funds, but it did not provide any details or confirmations. The London Stock Exchange, which lists the stock, confirmed to CNBC that the trading was briefly suspended due to its circuit breaker mechanisms, which are designed to prevent excessive volatility.

Ofcom, the UK’s communications regulator, has expressed its concern that the cloud computing market is dominated by a few large players, known as “hyperscalers”. These are companies like Amazon Web Services (AWS) and Microsoft Azure, which provide cloud services such as storage, computing, and networking to other businesses. According to Ofcom’s estimate, AWS and Microsoft Azure together account for about 60% to 70% of the total cloud spending, leaving little room for other competitors. Ofcom said that this could limit the choice, innovation, and quality of cloud services for consumers and businesses in the UK. Ofcom also said that it is monitoring the cloud market and exploring potential regulatory interventions to promote competition and protect consumers.

LG Energy Solution, a South Korean company that makes batteries for electric vehicles (EVs), has announced that it will supply EV batteries to Toyota, the Japanese automaker, for its cars that will be produced in the U.S. LG Energy Solution’s CEO, Youngsoo Kwon, said in an exclusive interview that the company will invest about $3 billion to build new factories for battery cells and modules exclusively for Toyota and that the factories will be completed by 2025. He also said that the company decided to invest in the U.S. market because of the high inflation, labor costs, and tax incentives in the country. He said that the IRA tax credit, which is a federal tax credit for EV buyers, is a big factor that offsets the costs and boosts the demand for EVs in the U.S. He said that LG Energy Solution is aiming to become a global leader in the EV battery market by partnering with Toyota and other automakers.

Indexes Wednesday began a sputtering relief rally after finding some encouragement in the ADP payroll data showed some signs of a slowing labor market, which could ease the inflation pressure. The bond yields helped ease rate pressures declining modestly giving stocks a little breathing room The sectors that have been lagging, such as consumer discretionary and technology, performed better on Wednesday. However, the energy sector was a big loser, as the oil prices dropped by more than 5%, their worst daily decline in a year. Today we have a few notable earnings, International Trade, Jobless Claims, Natural Gas figures as well as several more Fed speakers to inspire the bulls or bears. Keep in mind the next big market-moving report is Friday before the bell with the release of the Employment Situation numbers so plan your risk carefully because the sputtering relief could continue as we wait.

Surging bond yields and the sharply rising dollar kept the bears engaged Tuesday in a painful selloff that added to the technical damage of the index charts. The T2122 indicator is in an extreme short-term oversold condition suggesting a relief rally could begin at any time. However, bond yields are still rising this morning with a parade of Fed speakers today, adding to the uncertainty. Investors will look for inspiration in Mortgage, ADP, PMI, Factory Orders, ISM Services, and Petroleum Status figures as well as a handful of notable earnings reports today. Expect the price action to remain challenging as we head toward the Friday, Employment Situation report.

Asian markets were mostly lower overnight as Australia kept interest rates unchanged with China closed for a holiday. European markets are however working to relieve the recent selling pressure with modest gains this morning in a cautious session. U.S. futures recovered from overnight lows pointing to a modestly bullish open ahead of earnings and economic data that could provide fuel to the bulls or bears so plan your risk carefully.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday include ANGO, HELE, RGP, RPM, & TLRY.

News & Technicals’

The U.S. bond yields surged higher on Wednesday, as investors were worried about the possibility of the Fed keeping the interest rates high for a longer period than expected. The Fed’s interest rate policy affects the bond yields, which are the returns that investors get from buying bonds. The higher the interest rates, the lower the bond prices and the higher the bond yields. The Fed has been raising the interest rates since 2015, to control inflation and support economic growth. The Fed’s latest meeting in September signaled that it may raise the interest rates one more time this year and three more times next year. This has caused the bond yields to rise to their highest levels in more than a decade. The 10-year Treasury yield, which is the most widely watched indicator of the bond market, was slightly up at 4.81% on Wednesday. It had reached a high of 4.884% earlier in the day, after crossing the 4.8% mark on Tuesday for the first time since 2007. The 30-year Treasury yield, which is another important indicator of the bond market, was slightly down at 4.934% on Wednesday. It had briefly traded above 5% earlier in the session, also reaching levels last seen in 2007.

The United Nations Conference on Trade and Development (UNCTAD) has released a new forecast for global economic growth in 2024. The forecast predicts that the world economy will grow by 2.5% in 2024, slightly higher than the 2.4% growth in 2023. However, the forecast is based on several assumptions and uncertainties, and UNCTAD warns that the growth outlook is fragile and uneven. UNCTAD is particularly cautious about the U.S. economy, which is expected to slow down from 3.1% in 2023 to 2.1% in 2024, due to the fading effects of the fiscal stimulus and the rising interest rates. A UN director told CNBC that the forecast is “optimistic” given the “pretty weak” state of the global economy. He said that the main risk for global growth is the eurozone, which is on the verge of a recession. The eurozone is expected to grow by only 0.9% in 2024, after a meager 0.7% in 2023. UNCTAD urges the eurozone to adopt more expansionary fiscal and monetary policies and to address the structural problems of its banking sector and its trade surplus.

ntel, the world’s largest chipmaker, announced that it will spin off its Programmable Solutions Group (PSG) as a separate business, with the intention of taking it public in the next two to three years. PSG is the division that makes programmable chips, also known as field-programmable gate arrays (FPGAs), which can be customized for specific applications. Intel acquired PSG in 2015 when it bought Altera for $16.7 billion. Intel said that it will continue to support PSG and will retain a majority stake in the business, but it will give PSG more autonomy and flexibility to pursue its growth strategy. Intel’s stock price rose by 2.3% in after-hours trading following the announcement.

The stock market dropped sharply on Tuesday, as the bond yields and dollar kept rising as investors now seem to be aware that rates will be higher longer as the Fed has been saying. The S&P 500 fell by more than 1% and the Dow lost over 400 points. The sectors that did better were the ones that provided essential goods and services, such as utilities and consumer staples. The sectors that did worse were the ones that depended on innovation and spending, such as technology and consumer discretionary. Today we have ADP, PMI, Factory Orders, ISM Services, Petroleum Status, and a slew of Fed speakers to provide inspiration and volatility in the extreme short-term oversold condition. Although we have a few notable earnings it’s unlikely they will market-moving so instead keep an eye on those bond yields that are continuing to rise this morning. A relief could begin at any time but if bad data continues to pile on be prepared for more selling, whipsaws, and challenging price volatility.

Monday kicked off the fourth quarter with an uncertain mixed start as the so-called magnificent seven tech giants rallied while small caps moved sharply lower. Bond yields were once again higher across the board as the dollar continued to surge higher adding selling pressure to commodities such as gold, silver, and oil. Unfortunately, we have another light day of earnings and economic reports for the bulls or bears to find inspiration likely making for another challenging day of choppy price action and whipsaws. The JOTLS report could be market-moving as the start to a big week of employment figures.

Asian markets traded mixed but mostly lower overnight with Hong Kong leading the way selling off 2.69%. European markets also trade mostly lower this morning as world sentiment continues to decline even as data shows U.K. food prices declined slightly. The U.S. futures fluctuated during the night but currently point to a bearish open ahead of light-day data.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday include CALM & MKC.

News & Technicals’

Satya Nadella, the CEO of Microsoft, testified in the federal antitrust trial against Google in Washington, D.C. He told the court that Google has an unfair advantage in online search, as it controls more than 90% of the market share. He said that this means that publishers and advertisers have to follow Google’s rules and standards, which makes it difficult for other search engines, such as Microsoft’s Bing, to compete and attract users. He also revealed that Microsoft offered to pay billions of dollars to Apple to make Bing the default search engine on its devices, such as iPhones and iPads. However, Apple rejected the offer and chose to stick with Google, which pays Apple an estimated $15 billion a year for the same deal. Nadella argued that Google’s payments to Apple are another way of maintaining its dominance and excluding its rivals.

The Russian ruble has been facing a severe depreciation against the U.S. dollar, as the country’s economy suffers from the impact of Western sanctions, falling oil prices, and the Covid-19 pandemic. The ruble reached its lowest level in more than six years in August when it traded at more than 100 rubles per dollar. The Bank of Russia, the country’s central bank, reacted by raising its key interest rate, which is the rate at which it lends to commercial banks, by 3.5 percentage points to 12% in an emergency meeting. The central bank hoped that this would stabilize the ruble and curb inflation, which is the increase in the prices of goods and services. However, the measure did not have the desired effect, as the ruble continued to weaken and inflation remained high. In September, the central bank increased its key rate again by another percentage point to 13%, citing the persistent inflationary pressure in the economy. The central bank said that it would continue to monitor the situation and take further actions if necessary.

The U.S. stock market has been showing signs of divergence, as the Russell 2000 index, which tracks the performance of small-cap stocks, turned negative for the year on Monday. The index fell by 1.6% on Monday, bringing its year-to-date return to a loss of 0.2%. It is also down by 12.5% from its highest level in the past 52 weeks. This contrasts with the performance of the S&P 500 and the Nasdaq Composite, which track the performance of large-cap stocks, especially in the technology sector. The S&P 500 and the Nasdaq Composite are up by 11% and 26%, respectively, for the year. The gap between the small-cap and large-cap stocks reflects the concerns that the 2023 market rally has been driven by a few big tech companies, such as Apple, Microsoft, and Amazon while ignoring the rest of the market. The Russell 2000 index is often seen as a better indicator of the health of the U.S. economy, as it represents smaller businesses that are more sensitive to economic conditions, such as consumer spending, inflation, and interest rates.

The stock market had a mixed start to the fourth quarter on Monday. The small-cap stocks, lagged, losing almost 2%, and the NASDAQ, gained about 0.7%. The ISM manufacturing report showed that the factory activity was stronger than expected in September while still indicating the sector is in contraction. The construction-spending data came in flat from last month as higher rates restrict home sales. The bond yields rose across the board, with the 10-year Treasury yield ending around 4.7% and the 2-year yield around 5.1%. The rest of this week will be focused on the labor-market reports, which could have a significant impact on monetary policy decisions. We begin with the JOLTS report today with a bit more Fed speak and just a couple of notable earnings for the bulls and bears to try and find inspiration.

Markets opened close to flat Monday (down 0.20% in the SPY, down 0.15% in the DIA, and up 0.04% in the QQQ). At that point, the SPY chopped sideways until 11:30 a.m. while the DIA chopped but slightly to the downside and QQQ chopped slightly to the upside during the same timeframe. Then all three sold off until 12:50 p.m. before closing out the day in a sideways chop channel that lasted until 3 p.m. Finally, all three rallied in the last hour of the day. This action gave us Doji candles in the SPY (white-bodied) and DIA (black-bodied) as well as a Bullish Harami, white-bodied, Spinning Top type candle in the QQQ. This all happened with above-average volume in the DIA, average volume in the SPY, and a bit below-average volume in the QQQ.

On the day, nine of the 10 sectors were in the red. However, Utilities (-4.25%) was a MASSIVE outlier, by 2%. Other than that, Energy (-2.35%) led the rest lower. Only Technology (+0.53%) held onto the green area. At the same time, the SPY lost 0.04%, DIA lost 0.26%, and the tech-heavy QQQ gained 0.83%. VXX gained slightly to close at 23.36 and T2122 dropped deep into the oversold territory at 6.21. 10-year bond yields spiked to 4.683% while Oil (WTI) plummeted 2.34% to end the day at $88.66 per barrel. So, we saw a flat open followed by chop, a selloff, more chop, and finally a rally. That all left us little changed overall with only NVDA, GOOGL, ADBE, META, MSFT, AMZN, PDD, and APPL dragging the QQQ back up above its T-line (8ema) to perform better than the large-cap index ETFs.

The major economic news reported Monday included September Global Mfg. PMI, which came in slightly above expectations at 49.8 (compared to a forecast of 48.9 and a previous reading of 47.9). A few minutes later, September ISM Mfg. Employment was reported above anticipated at 51.2 (versus a forecast of 48.3 and an August value of 48.5). At the same time, September ISM Mfg. PMI also came in above expectation at 49.0 (compared to a forecast of 47.7 and an August reading of 47.6). September ISM Mfg. Price Index came in well below predicted at 43.8 (versus a forecast of 48.6 and an August value of 48.4). So, according to S&P and ISM manufacturing is holding up. At the same time, the manufacturing price drivers (ISM PMI Price factors) are coming down compared to predicted levels.

In Fed speak news, Fed Governor Bowman told a banking conference that she thinks further rate hikes will be needed. She said, “…my own expectation that progress on inflation is likely to be slow given the current level of monetary policy restraint, suggests that further policy tightening will be needed to bring inflation down in a sustainable and timely manner.” Later, Fed Vice Chair for Bank Supervision Barr told a New York economic forecaster conference that he is much less concerned about how much more to raise rates than how long to keep them high. He said, “In my view, the most important question at this point is not whether an additional rate increase is needed this year or not, but rather how long we will need to hold rates at a sufficiently restrictive level to achieve our goals.” Barr went on to say “I expect it will take some time.” Finally, Fed Chair Powell spoke to a business group in PA. He did not address monetary policy, but said the economy was still dealing with the aftermath of the COVID-19 Pandemic. Finally, last night Cleveland Fed President Mester told a group that she still thinks the FOMC may need to raise rates one more time. She added the obvious and often repeated stated Fed position that inflation remains too high and the terminal Fed Funds rate, as well as how long it is held at that level, will depend on how the economy evolves.

In Autoworker contract talks and strike news, GM and F announced they will furlough another 500 workers across four plants because of the impact of the UAW strikes. At the same time, F announced it was laying off 330 workers due to the strike. Meanwhile, the UAW confirmed to Reuters that it had presented a new contract proposal to GM on Monday and also held another round of talks with STLA.

In stock news, TSLA reported disappointing Q3 delivery numbers, saying that it had delivered 435,059 vehicles in Q3 (short of the average analyst estimate of 456,722). At the same time, TSLA manufactured 430,488 cars in Q3 well below the average estimate of 461,992. (It should be noted that this failure brings China’s BYD within 3,456 cars of becoming the world’s largest EV maker.) Shortly after the TSLA report, RIVN reported higher-than-expected Q3 vehicle deliveries of 15,564 (compared to an analyst estimate of 14,470), which was a 23% increase from Q2. At the same time, KKR announced it has sold $560 million worth of industrial real estate (about 5 million square feet) across 50 buildings in Atlanta, Dallas, Chicago, and Central PA. (The buyer was not disclosed.) Elsewhere, the CEO of troubled BA supplier SPR resigned and was immediately replaced on an interim basis by a former BA executive. At the same time, NSC faced its second service outage in the last month (both caused by IT issues). NSC was downgraded by some analysts on this news. Later, MSFT CEO Nadella said Monday that major players were competing to lock up content creators for their data (needed to train AI models). He said the whole atmosphere reminded him of the early days of search engines where the big players started paying tens of billions to lock up publishers with exclusive deals. After the close on Monday, BF.A announced a $400 million share buyback program beginning immediately and lasting until Oct. 1, 2024. Also after the close, a coalition of hedge funds increased its offer for SCU to $13/share (up from $12.76/share). SCU closed at $11.38/share. Meanwhile, WE announced it was delaying a $95 million interest payment. This raised speculation of bankruptcy but was leaked to be a negotiation tactic with creditors and landlords.

In stock government, legal, and regulatory news, CI announced it reached a settlement over the weekend to pay $172 million for overcharging the government for Medicare Advantage claims. (It was actually fraud because false claims were submitted to get tens of millions in unearned money.) Later, MCD and WEN defeated a lawsuit that had alleged the restaurants deceived consumers about the size of their burgers. At the same time, the NHTSA expanded its investigation into F sport utility and trucks over catastrophic engine failures due to faulty valves. The investigation now covers 708k 2021-2022 vehicles. Later, in the early afternoon, the FDIC issued a consent order without fines for DFS, who had been under investigation since an Oct. 2022 audit found incorrect credit card classifications. However, DFS responded quickly and strongly and was rewarded for its treatment by FDIC. Elsewhere, Reuters reported Monday that all 10 of the drugmakers subject to negotiations over Medicare drug pricing signed up for the negotiations with the US HHS Dept. prior to the October 1 deadline. Most of them are suing HHS, wanting to prevent negotiations, but a federal court ruled against a suit on behalf of the 10 from the US Chamber of Commerce on Friday. In the afternoon, AAPL announced it would appeal a Netherlands Consumer and Markets Authority ruling related to App Store policies. At the same time, a US District judge in CA ruled in TSLA’s favor by ruling that TSLA owners must pursue any fraud claims (that the company misled them about Autopilot features) in individual arbitration rather than in courts, throwing out a proposed class-action lawsuit in the process. Meanwhile, the FCC announced the first ever “space debris” fine of just $150k against DISH for waiting until there was not enough fuel left to send an end-of-life satellite into re-entry which would burn up the satellite. After the close, the US Patent Office tribunal rejected a request from VTRS for the agency to review two patents held by NVO related to two weight-loss drugs. VTRS claimed the two patents obviously were based on existing patents for the underlying diabetes drug and should be invalidated.

Overnight, Asian markets leaned heavily to the red side. Hong Kong (-2.69%), Thailand (-1.51%), and Australia (-1.28%) led the region lower. In Europe, we nearly see red across the board at midday. Only the FTSE (+0.19%) remains in the green while the CAC (-0.41%) and DAX (-.51%) lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a start to the day just on the red side of flat. The DIA implies a -0.07% open, the SPY is implying a -0.09% open, and the QQQ implies a -0.16% open at this time. Meanwhile, 10-year bond yields are spiking again to 4.727% and Oil (WTI) is down another two-thirds of a percent to $88.27 per barrel in early trading.

The major economic news scheduled for Tuesday is limited to JOLTs Job Openings (10 a.m.) and API Weekly Crude Oil Stocks (4:30 p.m.). The major earnings reports scheduled for before the open are limited to MKC. Then after the close, CLM, and NG report.

In economic news later this week, on Wednesday we get Sept. ADP Nonfarm Employment Change, Sept. S&P Global Services PMI, Sept. S&P Global Composite PMI, Aug. Factory Orders, Sept. ISM Non-Mfg. PMI, Sept. ISM Non-Mfg. Price Index, EIA Crude Oil Inventories, and Fed member Bowman speak. On Thursday, we get August Imports, August Exports, Weekly Initial Jobless Claims, the Fed Balance Sheet, and two Fed Speakers (Mester at 9 a.m. and Daly at noon). Finally, Friday, Sept. Avg. Hourly Earnings, Sept. Nonfarm Payrolls, Sept. Private Nonfarm Payrolls, Sept. Participation Rate, Sept. Unemployment Rate, and a Fed speaker (Waller at noon).

In terms of earnings reports later this week, on Wednesday, we hear from AYI, HELE, and RPM. On Thursday, CAG, STZ, LW, and LEVI report. Finally, on Friday, there are no major earnings reports scheduled.

So far this morning, MKC missed on revenue while reporting in-line on earnings. Even so, this was a 5.6% quarter-on-quarter increase for MKC.

In late-breaking news, late last night Florida Rep. Gaetz followed through on his threats by filing a “motion to vacate the chair” in hopes of removing House Speaker McCarthy. Gaetz has vowed that even if he loses this time, he will refile the motion every time Speaker McCarthy reaches across the aisle to court Democratic votes on any legislation. On that note, it will very likely be Democrats who decide whether McCarthy keeps his post. So, the matter will come down to whether McCarthy and the less-fringe Republicans can reach a compromise (actual governing solution) or whether the parties are too far into the “us good vs. them evil” mindset to govern. Oddly, Gaetz has at least said he backs House Majority Leader (#2 House Republican) as McCarthy’s replacement. The issue is that that person, Steve Scalise, is currently incapacitated while being treated for a rare blood cancer and in the past has been a staunch supporter of McCarthy. The point of the whole story is that Congress now has yet another hurdle to get past before it can accomplish anything. Remember the 15 rounds of votes over a number of days it took the GOP to elect McCarthy? Here’s to hoping that doesn’t become “the good old days of a semi-functional Congress.”

With that background, it looks like the Bears are in control this morning in the premarket. All three major index ETFs are printing black-bodied candles with upper wicks and sitting at their early session lows. The QQQ has (as of now) given up its T-line again and it appears we are headed for a modest gap lower at the open. So, for now, the short-term trend clearly remains headed lower. In terms of extension, none of the three major index ETFs are far below their T-line (8ema) but the T2122 indicator is now well into the lower half of its oversold range. So, over-extension is an open question. This tells us either side has at least some slack if they can find the momentum to run.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service