No Planned News and Bears On Top

Markets sold off in the morning Friday and then meandered sideways the rest of the day. SPY opened down 0.13%, DIA opened 0.23% lower, and QQQ opened down 0.18%. Then, all three major index ETFs ground sideways for 30 minutes. However, at 10 a.m., DIA sold off sharply for 15 minutes but the SPY and QQQ sold off hard until 11 a.m. and neither reached their low until 11:35 a.m. From there, all three drifted sideways with first a slight bullish trend until 1:20 p.m. and then sideways with a slight bearish trend the rest of the day. This action gave us black-bodied candles with modest upper wicks and very small, if any lower wicks. The SPY is at the breakout of a “Dreaded h” pattern and also crossed down through its 200sma. DIA is still in the downswing of its own Dreaded h and QQQ is sitting at the breakdown of a major support level. This happened with above-average volume in the SPY, average volume in the DIA, and a bit less-than-average volume in the QQQ.

On the day, all 10 sectors were in the red with Technology (-1.75%) out front leading the way lower. Meanwhile, Healthcare (-0.47%) held up better than other sectors. At the same time, the SPY was down 1.23%, the DIA lost 0.88%, and QQQ lost 1.49%. VXX gained 0.61% to close at 26.46 and T2122 dropped even further into the bottom of its oversold territory at 1.37. 10-year bond yields fell slightly to 4.914% while Oil (WTI) fell slightly to close at $89.02 per barrel. So, on Friday we had a very volatile market. There is no way to know for sure what the cause behind the morning volatility or the afternoon selloff was. However, Fed Chair Powell spoke at noon, and it was also midday when the latest stage of the House Republican fiasco began. There was also news out of the Middle East midday as the Israeli Defense Minister had reportedly green-lighted a ground invasion of Gaza and a US Destroyer intercepted drones/missiles launched by the Yemeni Houthi (backed by Iran).

The economic news reported Friday was limited to the September Federal Budget Balance which came in far, far worse than expected at a deficit of $171.0 billion (compared to a forecast of a $78.6 billion deficit and even the August number of an $89.0 billion deficit). Elsewhere, Bloomberg released its monthly survey of economists on Friday. The October survey indicates an increased average estimate for Q3 GDP of 3.5% (up from the 3.0% estimate in September).

In Fed speak news, Cleveland Fed President Mester indicated Friday that the Fed is at or at least very near its peak tightening. Mester said, “Regardless of the decision made at our next meeting, if the economy evolves as anticipated, in my view, we are likely near or at a holding point on the funds rate.” However, she said there is still plenty of room for the Fed to keep tightening by cutting its balance sheet, saying “There’s still more runway there” to lower the size of the Fed’s holdings and this process could play out over the next year and a half to two years.” Mester also made it clear that rate hikes and QT are separate issues, saying “we can have the balance sheet reduction continue independently of federal funds rate moves.”

In Autoworker contract talks and strike news, for the second time in a week, STLA has pulled out of a major auto show. The company cited an effort to reduce costs in the midst of the UAW strike. STLA also announced it would lay off an additional 100 workers due to the strike. Elsewhere, GM announced it increased its proposed wage increases to match the 23% increase offered by F, as well as the additional benefits enhancements. At the same time, UAW President Fain cited progress in his weekly update. He noted that he had received improved offers from GM and STLA. Fain said that a deal is close, but emphasized that the crucial part of any negotiation is the final push before the deal, which he means the need to remain on strike. He announced no new additions to the strike (facilities or workers). However, as usual, Fain threatened wider strikes if even better offers are not delivered by the companies. The strike is now 5-weeks old and some analysts wondered aloud whether Fain was hoping the upcoming earnings reports from GM and F might give those companies a reason to take one more step in order to report a tentative deal along with their earnings. (It would make the earnings call questions easier to address.)

In stock news, TM extended its temporary partial production shutdown until Monday following a fire at a major supplier in Japan. Elsewhere, SAVE canceled 11% of its flights Friday in order to do inspections for so-called “undocumented parts.” The outage is expected to last at least several days since many of the parts needing inspection are in the center of jet engines. Later, ADIL shares plummeted (closing down 24%) following its announcement of the sale of 1.4 million shares to raise cash. At the same time, BMY said its experimental renal cancer drug has achieved both primary and secondary targets in a Phase III study. In the auto industry, VLKAF (Volkswagen) cut its 2023 profit margin outlook, citing failures in its raw materials hedging. At the same time, a rail union (Brotherhood of Railroad Signalmen) initiated a safety program with NSC (following that railroad’s multiple safety failures this year) and also ratified a sick leave agreement with CSX. After the close, ORCL announced a strategic partnership with NVDA saying it has implemented the NVDA AI stack into its cloud marketplace. (ORCL sells AI processing via the cloud as a service to businesses.) At the same time, OKTA announced it had suffered a security breach via a stolen credential. (OKTA sells cloud software infrastructure intended to provide security authentication…so security breaches are not exactly good for business.) As a result of rumors and leaks of this news, OKTA was down 11.57% Friday (over 9% of the loss came after 2:40 p.m.).

In stock government, legal, and regulatory news, the Fed, FDIC, and Office of the Comptroller of the Currency extended the deadline for comments (from the big banks basically) about why banks should not face stricter capital rules and increased data collection on the banks’ financial stability. The new deadline for comment is Jan. 16. Later, a US District Judge gave final approval of a $75 million settlement reached by DB with various victims of Jeffrey Epstein who had accused the bank of facilitating the late financier’s sex trafficking. Later, Reuters reported that the EU antitrust regulators have resumed their investigation of ABDA (over its $20 billion bid to buy Figma) on Friday. This comes after the agency had halted its investigation while awaiting further data from ADBE. A decision on the deal is due by Feb 5. Later the US Supreme Court ruled in favor of the Biden Administration, throwing out lower court rulings that were intended to limit the administration’s ability to contact social media companies to have misinformation and disinformation moderated by META, GOOGL, AAPL, and Twitter (now X) as well as the non-mainstream platforms.

Overnight, Asian markets were red across the board again. Thailand (-1.66%), Shenzhen (-1.51%), and Shanghai (-1.47%) led the region lower but the move was broad-based. In Europe, we see a similar picture taking shape at midday with only Greece (+0.26%) in the green. The DAX (-0.80%), CAC (-0.21%), and FTSE (-0.54%) are leading the region lower in early afternoon trade. In the US, at 7:30 a.m., Futures are pointing to a move lower to start the week. The DIA implies a -0.54% open, the SPY is implying a -0.50% open, and the QQQ implies a -0.58% open at this hour. At the same time, 10-year bond yields are up again, teasing 5% at 4.999% while Oil (WTI) is down 0.77% to $87.40 per barrel.

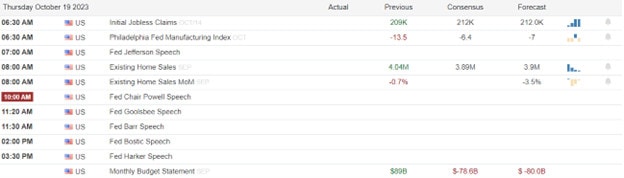

There is no major economic news scheduled for Monday. The major earnings reports scheduled for before the open include PHG and SDVKY. Then, after the close, AAN, ARE, BRO, CDNS, CLF, CR, CCK, LOGI, MEDP, PKG, SSD, TFII, TBI, and WRB report.

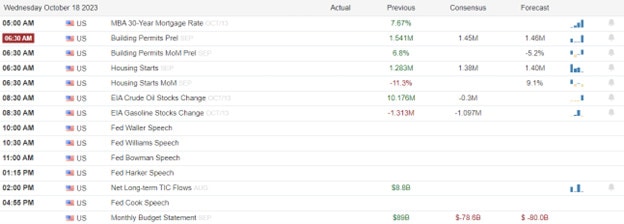

In economic news later this week, on Tuesday, we get S&P Global Manufacturing PMI, S&P Global Services PMI, S&P Global Composite PMI, and API Weekly Crude Oil Stocks. Then Wednesday, Building Permits, New Home Sales, and EIA Weekly Crude Oil Inventories are reported. We also hear from Fed Chair Powell. On Thursday, we get September Durable Goods Orders, Preliminary Q3 GDP, Preliminary Q3 GDP Price Index, September Goods Trade Balance, Weekly Initial Jobless Claims, Sept. Retail Inventories, Sept. Pending Home Sales, and we hear from Fed member Waller. Finally, on Friday, Sept. PCE Price Index, Sept. Personal Spending, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-year Inflation Expectations, and Michigan 5-year Inflation Expectations are reported.

In terms of earnings reports later this week, on Tuesday, MMM, HOUS, ADM, ARCC, ABG, BCS, CNC, KO, GLW, DHR, DOV, DOW, FI, FELE, GTX, GE, GM, HAL, HCA, HRI, ITW, IVZ, KMB, NEE, NHYDY, NVS, NUE, PCAR, PNR, PII, PHM, DGX, RTX, SHW, SPOT, SYF, TECK, TRU, VZ, XRX, GOOGL, BYD, CNI, CHX, CB, CSGP, ENVA, FFIV, GOOG, HA, MTDR, MSFT, RRC, RHI, RUSHA, SNAP, TDOC, TXN, V, WFRD, and WM report. Then Wednesday, we hear from ALFVY, APH, ATLKY, ADP, AVY, BA, BOKF, CME, CSTM, EVR, FTV, GD, GBX, GPI, HES, HLT, LTH, LAD, MHO, MCO, MSM, EDU, NSC, ODFL, OMF, OPCH, OTIS, OC, PAG, PRG, RDUS, ROP, R, SLGN, TMUS, TMHC, TDY, TMO, TNL, UMC, VRT, WNC, WAB, AEM, ALGN, ALSN, AMP, NLY, AR, ATR, ASGN, AVB, AGR, BKR, BHE, CACI, CP, CLS, CCS, CHE, CHDN, CMPR, CYH, EW, ESI, EQT, EQIX, EG, FLEX, FLS, FBIN, GL, GGG, ICLR, IEX, IBM, INVH, KALU, KLAC, LSTR, MAT, META, MAA, MOH, MYRG, NBR, NXT, ORLY, OII, PPC, PLXS, RJF, ROL, SEIC, NOW, STC, SUI, TER, TNET, TROX, URI, UHS, VMI, VICI, WCN, WFG, WU, and WHR. On Thursday, AOS, MO, AMT, AIT, ARCH, AMBP, BSX, BFH, BMY, BC, BG, CRS, CARR, CX, CNP, CMS, CMCSA, CFR, EXP, EME, FAF, FCNCA, FSV, ULCC, FCN, HOG, HAS, HSY, HTZ, HON, IP, KVUE, KDP, KEX, LH, LAZ, LEA, LII, LIN, LKQ, MDC, MAS, MA, MRK, NYCB, NEM, NOC, ORI, OSK, PATK, BTU, PCG, BPOP, RS, RCL, STX, SAH, LUV, STM, FTI, TXT, TTE, TSCO, TPH, UPS, VLO, VLY, VC, VMC, GWW, WST, WEX, WTW, AB, AMZN, AJG, BIO, SAM, COF, CSL, CC, CMG, CINF, COLM, DECK, DXCM, DLR, EMN, EHC, ENPH, ERIE, FE, F, HIG, HUBG, INTC, JNPR, LHX, LPLA, MTX, NOV, OLN, PFG, RSG, RMD, SKX, SKYW, SSNC, TEX, TXRH, X, VALE, WY, and WKC report. Finally, on Friday, we hear from ABBV, AER, ARLP, AON, ARCB, AN, AVTR, BAH, CBRE, GTLS, CHTR, CVX, CL, DAN, EQNR, XOM, FMX, FTS, GNTX, IMO, LECO, LYB, NWL, NVT, PSX, POR, SAIA, SNY, SWK, TROW, and XEL.

In US Congressional news, I’m sure you heard that Rep. Jordan failed in what was a surprise third vote in his try to become Speaker of the House on Friday. Just as had happened in the second vote, Jorden got less support, losing 4 more GOP votes than he had gotten in the second vote. Speaker Pro Tempore adjourned Congress for a long weekend immediately after the vote. Following adjournment, the GOP Caucus held a secret ballot to confirm their support of Jordan’s candidacy and Jordan got the backing of only 86 of the 221 Republicans. (So, in the space of an hour, Jordan had gone from 194 public votes to 86 private ones.) He was dropped as the GOP Speaker Nominee (and withdrew his candidacy). As of Sunday, there were nine sitting GOP Reps. that had filed officially to throw their hat into the ring for the job. The GOP plans to hear speeches from the nine on Monday and take their next GOP-only vote to choose one on Tuesday. Sadly, as of Sunday night, the Democrats had not shown enough leadership to publicly throw their support behind one of the nine either. Had they done so, they would have made it easier on moderate Republicans to elect a GOP Speaker with bipartisan support. That would have meant the Speaker was much less indebted to extremist minorities on either side. So, we continue down the partisan track, and assuming the GOP can choose their candidate Tuesday morning, the whole House will resume voting for the new Speaker later Tuesday. That will be exactly 24 calendar days and 9 scheduled House working days before another government shutdown ensues.

In miscellaneous news, the Biden Administration made a formal request for $105 billion of funding for Israel, Ukraine, Taiwan, and US border security. The packaging includes $61 billion for Ukraine ($50 billion of which will actually go to US defense contractors), $14.3 billion for Israel (some of which will also go for US-built missile systems), a bit more than $9 billion for humanitarian aid, $6.4 billion for border operations, $1.2 billion for fighting counterfeit fentanyl entering the country, and $2 billion for Taiwan.

In geopolitical news, two American hostages were released by Hamas on Friday after negotiations made through the UAE. In other Middle East news, a US Destroyer shot down missiles and drones launched by Iran-backed, Yemeni Houthi rebels that were headed toward Israel. Elsewhere, ship tracking data has identified one Russian and one Chinese ship that were in the locations of pipeline and telecom cable that were destroyed recently (running between Finland and Estonia). Sweden said the same two ships were at the location of a telecom cable running between Stockholm and Estonia that was damaged about a day prior to the Finnish damage. Meanwhile, flying under the radar last week, hours after Russia revoked its ban on nuclear testing, the Biden Administration showed its own ability to rattle sabers by conducting a large high-explosive (non-nuclear) test at US nuclear test site. The Dept. of Energy said the test was intended to validate new predictive models for the chemicals and radioisotopes used in the blast. (This will reportedly improve the US ability to detect atomic blasts in other countries.)

In late-breaking news, Japan announced it has launched an antitrust investigation of GOOGL related to mobile phone search monopoly. Third-party opinions on the topic are to be submitted by November 22. Elsewhere, CVX announced early today that it has agreed to buy HES for $53 billion in an all-stock deal. This comes not long after XOM bought PXD as huge consolidation in the US Oil space continues. (Don’t be surprised if the pair of deals draw antitrust scrutiny since the number 1 (XOM) and number 2 (CVX) oil producers gobbling up significant rivals. CVX said that after the deal closes, it intends to increase its share repurchase program by another $2.5 billion (on top of the existing $20 billion buyback plan).

With that background, it looks like the bears continue to have control in the premarket. However, all three of the major index ETFs are up off their lows of the early session. It is also worth noting that DIA and QQQ are printing indecisive premarket candles, with more wick than body and wick on both sides. Still, they are all black-bodied candles. So, the market leans bearish early with all three major index ETFs below their T-line (8ema). With no economic news on tap today and more earnings not really coming until after the close, we might get a true read on relative strength to start the week. Trading should be a little less volatile unless we get geopolitical news of some sort. In terms of extension, all three major index ETFs are starting to get stretched out below the T-line (8ema). The T2122 indicator is now also deep in the bottom of its oversold territory. So, we need a pause or bounce to relieve pressure even if the Bears maintain control. Just remember that the market can stay over-extended a lot longer than we can stay solvent being right too early. So, don’t go betting on “we’re due.”

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service