Member e-Learning 1-18-24 – Doug

QQQ and SPY Looking to Rally Early

Markets followed Asia and Europe down by gapping lower at the open again. The SPY opened 0.65% lower, DIA gapped down 0.49%, and QQQ opened 0.80% lower. At that point, SPY meandered sideways following the opening level the entire day. Meanwhile, DIA roamed back and forth across its gap the entire day. For its part, QQQ sold off after the open but from 10 a.m. until the close it traded in a bullish trend the rest of the day, closing very near the high of the day and inside its morning gap. This action gave us white-bodied candles in all three major index ETFs. The SPY printed a gap-down Spinning Top with most of its wick below the body. DIA printed a larger, white-bodied Spinning Top with most of its wick above the body. QQQ split the difference, printing a larger white-bodied Spinning Top with most of its wick below the body and retested its T-line (8ema) from below after the gap down. It did close just above that T-line.

On the day, all 10 sectors were in the red with Utilities (-1.36%) out in front leading the way lower. At the same time, Consumer Defensive (-0.40%) and Financial Services (-0.46%) held up better than the other sectors. At the same time, the SPY lost 0.56%, DIA lost 0.25%, and QQQ lost just 0.56%. Meanwhile, VXX gained 3.65% to close at 15.92 and T2122 dropped even further into the oversold territory at 6.25. 10-year bond yields climbed to 4.102% and Oil (WTI) rose 0.60% to close at $72.83 per barrel. So, after a significant gap lower, Mr. Market was indecisive with a very modest bias toward the bullish side. This happened on less-than-average volume in the SPY, and average volume in both the QQQ and DIA.

The major economic news on Wednesday included December Core Retail Sales, which came in much stronger than expected at +0.4% (compared to a forecast and Nov. readings of +0.2%). For the broader, Dec. Retail Sales things also came in above what was anticipated at +0.6% (versus a forecast of +0.4% and the Nov. value of +0.3%). At the same time, the December Import Price Index was flat at 0.0% (versus a forecast and November of -0.5%). In addition, the Dec. Export Price Index fell more than predicted at -0.9% (compared to a -0.6% forecast but in line with November’s -0.9% reading). Later, Dec. Industrial Production (year-on-year) increased at +0.98% (versus a 2023 reading of -0.62%). On a month-on-month basis, the Dec. Industrial Production grew more than expected at +0.1% (compared to a 0.0% forecast down also down from November’s +0.2%). After that, Nov. Business Inventories came in as predicted at -0.1% (versus the -0.1% forecast and October reading). At the same time, Nov. Retail Inventories were down more than anticipated at -0.9% (compared to a -0.8% forecast but in line with the October -0.9% value). Then, after the close, the API Weekly Crude Oil Stocks report showed a modest inventory build of 0.483 million barrels (versus a forecast calling for a 2.400-million-barrel drawdown and the prior week’s 5.215-million-barrel drawdown.

In Fed news, the Fed Beige Book showed steady to slightly improved economic activity and employment levels. This included stable or declining input costs, more than half of the Fed districts having steady employment levels, and retailers adjusting profit margins in response to the changing costs. Earlier, Fed Governor Bowman said the proposed plan to increase bank capital requirements has some shortcomings. Still, she was optimistic policymakers and the banking industry advocates could compromise. (It is worth noting that Bowman had voted against the rules which passed anyway back in July.)

After the close, AA and FUL missed on revenue while beating on earnings. (It is worth noting that AA’s beat was just less of a loss than expected.) At the same time, DFS, SNV, and WTFC all beat on revenue while missing on earnings. However, KMI missed on both the top and bottom lines.

In stock news, after settling the lawsuit related to how majority owner BRKB was doing valuation accounting, BRKB bought out the remaining 20% of the Pilot Truck Stop business from the Haslam family. (Terms were not disclosed.) At the same time, DOOR announced it had ended its bid to acquire PGTI. Later, ALSN employees voted to ratify the previously tentative contract the UAW had negotiated with the company. (82% voted in favor of the deal, which offers a $20/hour starting wage and a 6%-8% increase in company contributions to 401k accounts.) At the same time, AMD said it has cut the price of its Radeon RX 7900 XT graphics card by $40 (originally $809, then $749 and now sold at $709) to better compete with NVDA products. Elsewhere, ALB (the world’s largest lithium producer) announced Wednesday that it will cut jobs, and push off one new project as part of cost-cutting it said was driven by falling lithium prices. At the same time, VZ announced that it will take a $5.8 billion write-down of its wire-based unit amidst increased competition from wireless services. Later, TSLA slashed the price of its Model Y cars in Europe (between 8% and 9%). At the same time, Reuters reported that AAPL topped Korea’s Samsung as the top seller of smartphones. AAPL had a 20.0% market share in 2023 compared to Samsung’s 19.4%. (Interestingly, QCOM and Samsung jointly announced a new S24 line of phones that include a QCOM chip and will come with GOOGL generative AI built-in.)

In stock government, legal, and regulatory news, the FAA announced Wednesday that it had completed inspection of the first 40 (of 171 total) BA 737 MAX 9 jets. (This was just data collection. The data from the inspection still needs to be reviewed.) In the UK, British antitrust regulators won a court appeal over data requests to BMWYY (BMW motors) and VLKAF (Volkswagen), which the companies had sought to block. At the same time, GOOGL announced it will tweak search results in Europe to comply with EU rules to treat rival services and products the same as its own listings. Later, the NTSB announced that if a partial government shutdown takes effect on Friday, it will be forced to suspend the probe into the ALK airline BA 737 MAX 9 jet losing a portion of its fuselage in flight. Elsewhere, the US Court of Appeals rejected AAPL’s appeal and ordered the ban on importation of AAPL watches effective at 5 p.m. ET on Thursday. (Lower courts found that AAPL violated the patent rights of MASI by putting MASI-designed oxygen sensors in their watches without paying MASI.) Later, a unit of SBGI signed a deal with creditors to emerge from bankruptcy by getting funding from AMZN as part of a streaming sports content deal. The deal must still be approved by the bankruptcy court, but this is expected since creditors are now on board. After the close, ARAV announced it will delist from the NASDAQ and dissolve the company by selling company assets to satisfy creditors.

Overnight, Asian markets were mixed. Shenzhen (+1.00%), Hong Kong (+0.75%), Shanghai (+0.43%), and Taiwan (+0.38%) led the rebound from a tough Wednesday while Malaysia (-0.81%) and Australia (-0.63%) dragged on the rally. In Europe, with the sole exception of Russia (-0.01%) we see green across the board at midday. The CAC (+0.94%), DAX (+0.73%), and FTSE (+0.23%) led a broad-based rally in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a much better start than earlier in the week. The DIA implies a flat open at -0.01%, the SPY is implying a +0.42% open, and the QQQ implies a +0.76% open at this hour. At the same time, 10-year bond yields are down to 4.088% and Oil (WTI) is flat at $72.50 per barrel in early trading.

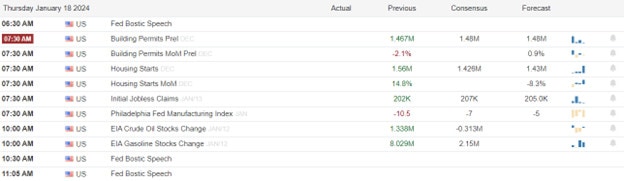

The major economic news scheduled for Thursday includes Dec. Building Permits, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. Housing Starts, and Philly Fed Mfg. Index (all at 8:30 a.m.), EIA Weekly Crude Oil Inventories (11 a.m.), and the Fed Balance Sheet (4:30 p.m.). We also hear from Fed member Bostic (7:30 a.m. and 11:30 a.m.). The major earnings reports scheduled for before the open include FAST, FHN, KEY, MTB, NTRS, TSM, and TFC. Then, after the close, JBHT, and PPG report.

In economic news later this week, on Friday, we get Dec. Existing Home Sales, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations as well a Fed member Daly speaking.

In terms of earnings reports later this week, on Friday, ALLY, CMA, FITB, HBAN, RF, SLB, STT, and TRV report.

In miscellaneous news, the National Assoc. of Builders reported Wednesday that the confidence of Builders jumped 7 points this month to 44 on its index as optimism flowed from falling mortgage rates and signs of an improving economy. However, 31% of the surveyed group still reported cutting prices to boost sales. (That is down from 36% who were cutting price in both December and November.) Meanwhile, China reported that its population fell in 2023, making it the second consecutive population decline. The Chinese population now stands at 1.4 billion after a spike to 11.1 million deaths following the lifting of COVID restrictions in that country. Meanwhile, Chinese births fell 5.6% to 9 million. (2023 was China’s seventh-straight year of decline in births.) This leads to concerns over the potential growth of the world’s second-largest economy as faltering demographics point to higher costs for retirement benefits and increasing competition for a shrinking labor pool could also mean higher labor costs.

In Government-related news, on Wednesday, President Biden hosted a negotiation session over the $110 billion package that will include aid to Ukraine, and Israel, as well as funds for the US border. It was a large meeting with the leadership of both parties in both houses of Congress as well as all the key committee leaders in attendance. After the meeting, attendees were upbeat and hoped for an agreement soon. However, House Speaker Johnson made a point of saying there will be no compromise on immigration. Elsewhere, the Consumer Financial Protection Bureau proposed cutting credit card overdraft fees to a maximum of $3.00. This is much lower than the current average of $26.00. Banks immediately responded that they have already cut other fees and there is no reason to cut overdraft fees. (The bankers did not mention the potential impact on bank profits.) Meanwhile, the US Supreme Court heard arguments Wednesday on what is called the “Chevron deference.” This is a long-standing (since 1984) position of the courts that when there is a dispute over the interpretation of a regulation, the deference goes to the regulators (executive agencies) that wrote those regulations. The case at hand challenges the executive branch’s ability to regulate fishing. (Specifically, whether fishermen must pay for tracking devices that make sure they were not fishing in protected areas that had been set as off limits to protect fish populations.) The plaintiff seeks to overturn the “Chevron deference” to make it such that only laws and rules explicitly passed by Congress could be enforced by the executive branch. This would have massive implications, overturning a huge part of government regulation and forcing Congress to visit every single issue and interpretation of every law. Even with that said, the questioning by justices led many observers to feel that the court is split with many of the conservative-packed court members strongly in favor of stripping all federal agencies of the power to regulate anything not explicitly laid out by Congress. While it is possible to argue the issue on both sides, the idea of Congress getting into every detail would likely lead to a practical problem of nothing being regulated for a long time. (Think environment, labor, health, education, energy policy, etc.) After all, it’s been years since Congress could pass even broad department-level budgets, let alone dictating every rule and regulation as well as how each will be interpreted. That would leave litigation and federal courts to decide on the interpretation of every rule and regulation. In other words, who should write and interpret federal regulation details? Congress? The Courts? Or the Agencies that are experts in and are charged with carrying out those regulations? This could be a massive societal change.

So far this morning, FAST, FHN, KEY, NTRS, and TSM all reported beats on both the revenue and earnings lines. (Some of the banks, in particular, had big beats on revenue, such as NTRS beating revenue by 51% and FHN beating that line by 23%.) At the same time, MTB, TBCI, and TFC all beat on revenue while missing on earnings.

With that background, all three major index ETFs gapped lower to start the premarket session. SPY gapped down through its T-line, but QQQ again is holding on to that level after an early test. Both SPY and QQQ are giving us white-bodied candles in the early session while DIA is indecisive after the gap down. So, the short-term trend is being challenged and is indeterminate except for DIA which has turned down in the short-term. (If you take a broader look at DIA, it has just chopped sideways for a month.) However, the Bulls remain slightly in control of the short-term trend in at least the QQQ and SPY (market leaders). In the longer term, we are near all-time highs (potential resistance) in the SPY, QQQ, and DIA. In terms of extension, none of the three major index ETFs are far from their T-line (8ema). However, the T2122 indicator is now sitting well inside of its oversold range. So, both sides have room to run if they can gather the momentum to do it. However, the Bulls have more slack to work with. As I’ve been saying, keep watching those Tech Big Dogs. If they make a move as a group, it is almost impossible for the rest of the market to do anything but follow given their trading volumes.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Rate Uncertainty

The bears were a bit more active on Wednesday as rate uncertainty grew with hotter-than-expected retail numbers and Fed speeches continuing to suggest higher for longer than the market has anticipated. However, the SPY and QQQ left behind some hopeful candle patterns that a relief rally may be close at hand as long as earnings and economic data cooperate. Investors will look for inspiration in the housing, jobless, manufacturing, oil and gas reports along with more Fed speeches and earnings. Big point swings remain possible so plan your risk carefully.

While we slept Asian market ended mixed but mostly higher as Hong Kong relieved some of yesterday’s sharp selloff while China continued to linger near five-year lows. European markets are also taking a break from the recent selling showing green across the board this morning. U.S. futures suggest a substantial gap in the Nasdaq though the Dow and SP-500 trade flat ahead of earnings and economic data.

Economic Calendar

Earnings Calendar

Notable reports for Thursday include OZK, FNB, FAST, FHN, HOMB, JBHT, KEY, MTB, NTRS, PPG, TCBI, & WNS.

News & Technicals’

Google’s CEO Sundar Pichai announced in a memo to employees on Wednesday that the company will reduce its workforce this year. Pichai said that the company has big plans in fields such as artificial intelligence and that it needs to invest more in these areas. He also said that to make room for this investment, the company has to make difficult decisions and cut some jobs. He did not specify how many jobs will be affected or which divisions will be impacted.

Apple has decided to scrap the blood oxygen feature from its newest Apple Watches, the company announced on Wednesday. The feature, which measures the oxygen level in the blood, was challenged by Masimo, a medical device maker, who claimed that Apple infringed on its patents. Apple said that by removing the feature, it will be able to keep importing the devices to the U.S. while the legal dispute is ongoing. The revised versions of the Apple Watch Series 9 and Ultra 2, which were launched in September, will be available for purchase on Thursday.

TSMC, the world’s largest contract chipmaker, saw its revenue and net income decline in the fourth quarter of 2023, compared to the same period a year ago. The company reported revenue of NT$625.53 billion, down 1.5% year-on-year, and net income of NT$238.71 billion, down 19.3% year-on-year. The company attributed the lower results to the global chip shortage, which affected its production and delivery. TSMC’s main customers include Apple and Nvidia, who rely on TSMC to make the most advanced processors for their products, such as the iPhones.

Rate uncertainty inspired the bears to be a bit more active as the markets ended the day in the red on Wednesday, extending Tuesday’s losses, but leaving behind some hope clues that a relief rally is possible soon. Investors seem to be adopting a more cautious stance on 2024 rate cuts and the geopolitical tensions that continue to grow. Rates rose on the day, following Fed Governor Waller’s speech which seemed to counter the market’s anticipation of imminent rate cuts. The 10-year yield has risen to 4.1% after beginning the year below 4%. Across the globe, stocks fell after data revealed weak growth in China and higher inflation in the U.K., while oil prices edged up and gold fell on the day. Today investors will look for inspiration in Housing Starts and Permits, Jobless Claims, Philly Fed Mfg., Natural Gas, and Petrolem figures. We also have several notable earnings and more Fed member speeches to keep traders guessing.

Trade Wisely,

Doug

Public e-Learning 1-16-24 – John

Tough Day

The indexes had a tough day on Tuesday as financial reports, rising bond yields, Fed remarks, and the huge miss on the Empire State numbers weighed heavily on investor sentiment. Only the tech sector managed a positive close with just a small list of tech giants doing all the lifting. Wednesday is chalked full of earnings and economic reports but with the China CPI miss slowing economic concerns look to start the day with some bearish uncertainty. Watch for whipsaws with big point moves possible as investors react.

During the night Asian markets closed the day lower across the board with Hong Kong declining a whopping 3.71% and the Shanghai exchange falling near a 5-year low. European markets are also decidedly bearish this morning with U.K. inflation rising. U.S. futures suggest a bearish open but are already well off the overnight lows as we wait on retail sales data. Buckle up, the morning session could prove quite volatile.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday include AA, SCHW, CFG, DFS, FUL, KMI, PLD, SNV, USB, & WTFC.

News & Technicals’

China’s economic growth slowed down slightly in the fourth quarter of 2023, falling short of analysts’ forecasts. The GDP increased by 5.2% year-on-year, compared to 5.3% expected in a Reuters survey. The annual GDP growth rate was also 5.2%, the lowest since 1990. Retail sales, a key indicator of consumer spending, also disappointed, rising by 7.4% in December from a year earlier, below the 8% projection. China also resumed publishing the unemployment rate for young people, which stood at 13.1% in December, up from 12.9% in November.

Iran’s foreign minister issued a stern warning to the U.S. over its alliance with Israel, saying that it would be a mistake to link their future to that of Prime Minister Benjamin Netanyahu, who is facing corruption charges and political turmoil. He also blamed Washington’s unconditional backing of Israel for the instability and violence in the region, especially in Gaza, where Israeli airstrikes have killed hundreds of Palestinians. He urged the U.S. to “stop the war in Gaza” and respect the rights of the Palestinian people. He also emphasized that Iran was concerned about the security of the Red Sea, where it has a strategic interest and presence.

Tesla has lowered the prices of its Model Y electric SUVs in several European markets, following a similar move in China earlier this month. The company’s website shows that the Model Y prices in Germany have been reduced by up to 8.1%, while in France, the Netherlands, and Norway the prices have also been cut by varying amounts. The price cuts come as Tesla faces increasing competition from other automakers in the fast-growing electric vehicle market. Tesla’s stock price fell by 1.6% in the U.S. premarket trading on Tuesday.

The European Central Bank (ECB) is facing a dilemma as inflation in the eurozone hits a record high of 5% in December. While markets are pricing in aggressive interest rate cuts starting in the spring, some ECB officials are resisting such a move, arguing that it could be premature and counterproductive. One of them is Robert Holzmann, the governor of the Austrian central bank and a known hawk, who told CNBC on Monday that there were downside risks to the inflation outlook that could prevent any rate cuts this year.

Tuesday proved to be a tough day for the indexes, as earnings reports from financial firms and Fed remarks weighed on investor sentiment. The huge miss on Empire State numbers added a bit of uncertainty about a sharply slowing economy. Cyclical sectors, such as energy, industrials, and materials, underperformed, while tech was the only sector to end the day in the green all due to a very select few giant tech names. Global markets also declined, with Asian and European stocks closing lower. In Canada, CPI inflation increased by 3.4% year-on-year in December, matching expectations but exceeding the 3.1% rate in November. Bond yields rose, with the 10-year reaching around 4.05%, and the 2-year climbing to over 4.2%. The higher bond yields followed Fed Governor Christopher Waller’s statement where he said he did not see any need for the Fed to hurry into rate cuts. Today we have a few more notable earnings with Mortgage Apps, Retail Sales, Import/Export Prices, Industrial Production, Business Inventories, Housing Market Index, Beige Book, and three Fed speakers to provide bullish or bearish inspiration.

Trade Wisely,

Doug

Asia and Europe Leading Us Lower Early

The Bears had control of the ball pretty much all day Tuesday. The SPY gapped down 0.30%, DIA gapped down 0.23%, and QQQ gapped down 0.29%. From there, all three major index ETFs saw 30 minutes of follow-through to the downside followed by an hour of rally that showed the divergence in the three. The rally in DIA only made it back up to the open level while SPY recrossed the opening gap and QQQ rallied to more of a gain than the open gapped lower. All three then sold off slowly until 2:30 p.m. and then rallied very slowly for the last 90 minutes. This action gave us indecisive candles in all three, with SPY printing a Doji that retested and held above its T-line (8ema). The QQQ printed a small-body, white-bodied Spinning Top that also retested and bounced up off its T-line. Meanwhile, DIA was the weak sister again, giving us a black-bodied Spinning Top that retested its T-line from below and failed that test.

On the day, nine of the 10 sectors were in the red with Energy (-2.18%) out in front leading the way lower. At the same time, Communications Services (+0.15%) was the only sector able to hang onto green territory. At the same time, the SPY lost 0.37%, DIA lost 0.60%, and QQQ lost just 0.01%. Meanwhile, VXX gained 3.50% to close at 15.36 and T2122 dropped sharply, down well into the oversold territory at 10.39. 10-year bond yields climbed to 4.054% and Oil (WTI) fell 1.06% to close at $71.91 per barrel. So, after the opening gap lower (mostly on the weekend tit-for-tat strikes in and off of Yemen), it was basically an indecisive day. This happened on less-than-average volume in the SPY and QQQ as well as average volume in the DIA.

The only economic news on Tuesday was the NY Fed Empire State Manufacturing Index, which came in far below expectations at -43.70 (compared to a forecast of -5.00 and even down significantly from December’s -14.50 reading). This low value led to speculation that the Fed may indeed cut rates in March as expected. (More than 97% of Fed Funds Futures bets expect no change at the end of January. However, 65.9% of futures bets are expecting a quarter point rate cut in March with just 34.1% thinking there will be no change in March.)

In FOMC news, Fed Governor Waller said Tuesday that the US “is now within striking distance” of its 2% inflation target. However, he also said the FOMC should not rush to cut its benchmark rate until it is clear lower inflation will be sustained. (Markets did not like the idea of not rushing cuts.) Waller said “The key thing is the economy is doing well. It is giving us the flexibility to move carefully and methodically. We can see how the data comes in, see if progress is being sustained.” He continued, “The worst thing we’d have is it all reverses after we’ve already started to cut. We really want to see evidence that this progress in the real data and the inflation data continues. I believe it will.” Waller also said, “Recent data is almost as good as it gets for the central bank with economic growth gradually slowing, the unemployment rate remaining low, and important measures of inflation now hitting the 2% target for the past six months.”

After the close, IBKR beat on revenue while missing on earnings. Interestingly, it was a massive beat on revenue (+38.2%) but still missed on earnings by 1.3%.

In stock news, STLA announced Tuesday that it has signed a deal to sell 250k vehicles over three years to German-based rental firm SIXT. (Deliveries will start this quarter and will cover both Europe and North America.) In other auto news, TSLA CEO Musk tweeted that he would be uncomfortable growing the company into a leader in AI and robotics without having 25% of the voting stock. (Musk only owns 13% of that stock now, after his sales to support his purchase of Twitter. So, Musk is demanding twice as much voting power as his ownership provides.) At the same time, SNPS announced it had agreed to buy ANSS for $35 billion. Later, QSR (Burger King) bought out its largest franchisee, TAST, for about $1 billion ($9.55 per share). QSR will get 1,000 Burger King and 60 Popeye’s Chicken restaurants in the deal. QSR also said it will invest $500 million to remodel 600 of the restaurants at twice the pace TAST was doing so. At the same time, AAPL announced it is offering discounts of up to $70 on iPhones sold in China and cut the price on other products by as much as $110. This is part of a push by AAPL to compete with Chinese phone giant Hauwei. Later, XOM said it would buy an additional 1.2 million tons of LNG per year from Mexico Pacific over a 20-year contract. Elsewhere, TSN announced more closures and temporary scaled-back meatpacking operations due to winter weather. At the same time, SHEL announced it is exiting Nigerian on-shore oil production after more than a century. The company said it will sell its operations to a consortium of five mostly local companies for $2.4 billion. Later, BA named an “independent quality advisor” to lead a review of its quality management practices. At the same time, LEG issued a business update, saying it plans to consolidate 15-20 of its 50 production and distribution facilities. The move will gradually cut between 900 and 1,100 jobs although this will not be accomplished until late 2025.

In stock government, legal, and regulatory news, France’s highest court rejected a request from HCMLF that it rule the company cannot be charged with complicity in “crimes against humanity” charges levied against the Syrian government. (HCMLF kept its factory running throughout the Syrian civil war and lower courts ruled the company was complicit in the regime’s actions due to company support of the regime.) Later, KR and ACI both announced they are pushing the closure of the $24.6 billion acquisition until “first half 2024” from “early 2024” after discussions with the FTC who (along with lawmakers) has questioned and pushed back on the deal. At the same time, JPM agreed to pay an $18 million civil penalty to settle charges it violated laws on whistleblower protection. Later, the US Supreme Court on Tuesday declined to hear the appeal by AAPL on the portion of the lower court’s decision that the company had lost in the lawsuit brought by Epic Games related to App Store billing requirements and rules. Elsewhere, the FAA-ordered grounding of 171 BA 737 MAX 9 jets entered its 11th day while inspections over loose bolts and other structural defects continue. At the same time, a US District Judge ruled in favor of the FTC and blocked the acquisition of SAVE by JBLU. Meanwhile, QMCO said Tuesday that it had offered voluntary retirement to more than 1,500 employees at its Panama mine. (This is continued fallout from the Panamanian government’s December decision to shut the company’s Cobre Panama mine in the public interest.) Meanwhile, the US banking industry and its main lobbying groups all peppered the Fed with criticism Tuesday all aimed at forcing the Fed to completely redo its rules which increase in bank capitalization requirements.

Overnight, Asian markets were red across the board. China led a huge push down in the region with Hong Kong (-3.71%), Shenzhen (-2.58%), and South Korea (-2.47%) leading the charge lower. In Europe, we see a similar (if not yet as bad) picture taking shape at midday. The CAC (-1.15%), DAX (-1.01%), and FTSE (-1.81%) are leading the move lower with only Greece (+0.20%) and Russia (+0.14%) in the green in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward another gap lower to start the day. The DIA implies a -0.33% open, the SPY is implying a -0.34% open, and the QQQ implies a -0.44% open at this hour. At the same time, 10-year bond yields are up slightly to 4.068% and Oil (WTI) is down 1.71% to $71.16 per barrel in early trading.

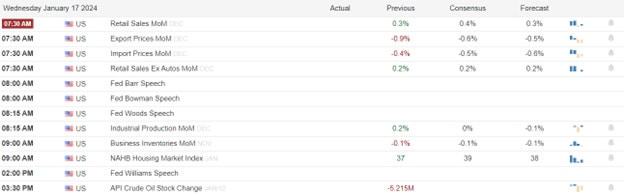

The major economic news scheduled for Wednesday includes Dec. Core Retail Sales, Dec. Retail Sales, Dec. Imports, and Dec. Exports (all at 8:30 a.m.), Dec. Industrial Production (9:15 a.m.), Nov. Business Inventories and Nov. Retail Inventories (both at 10 a.m.), Fed Beige Book (2 p.m.), and API Weekly Crude Oil Stocks (4:30 p.m.). We also have two fed speakers, Bowman at 9 a.m. and Williams (3 p.m.). The major earnings reports scheduled for before the open include SCHW, CFG, PLD, and USB. Then, after the close, AA, DFS, FUL, KMI, SNV, and WTFC report.

In economic news later this week, on Thursday, Dec. Building Permits, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. Housing Starts, Philly Fed Mfg. Index, EIA Weekly Crude Oil Inventories, and Fed Balance Sheet are reported as well as Fed member Bostic speaks. Finally, on Friday, we get Dec. Existing Home Sales, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations as well as Fed member Daly speaking.

In terms of earnings reports later this week, on Thursday, we hear from FAST, FHN, KEY, MTB, NTRS, TSM, TFC, JBHT, and PPG. Finally, on Friday, ALLY, CMA, FITB, HBAN, RF, SLB, STT, and TRV report.

In miscellaneous news, on Tuesday night (US time) the US Navy carried out more strikes on Yemeni Houthi anti-ship missiles. This came after a Houthi missile hit a Greek-owned vessel in the Red Sea. Elsewhere, a meteorological study out of Canada said that Western Canada’s abnormally dry winter (so far) likely points to the worsening of a severe drought in the region. (In turn, these will impact US grain, oil, gas, and timber prices.) That region produces most of the country’s grain, oil, gas, and forest products. It was also the site of many wide-ranging fires in 2023 that were bad enough to severely impact US city air quality last summer. Meanwhile, the EIA said that Wind and Solar are going to lead the growth in US power generation over the next two years. The agency said it expects Solar generation to increase 75% over that period from its 2023 level of 163 billion kWh. Over the same time, the EIA expects wind farm production to grow a much more modest 11% from its current 429 billion kWh. (EIA expects coal generation to fall 18% and natural gas production to remain level over the same two years.)

In mortgage news, loan demand surged last week by 10.4% compared to the prior week. This came as the national average loan rate fell again from 6.81% to 6.75% for a 30-year, fixed-rate, conforming loan. However, loan closing points did increase from 0.61 to 0.62 on the week. New home purchase loan applications were up 9% on the week while refinance loan applications jumped 11%.

So far this morning, USB reported a significant beat on the revenue line (29.5% growth) but only came in in line on earnings. At the same time, CFG also beat handily on revenue (+15.2% over forecast) but missed significantly (-43.3% versus estimates). PLD and SCHW both report at 8 a.m.

With that background, all three major index ETFs gapped lower to start the premarket session. SPY gapped down through its T-line, but QQQ again is holding on to that level after an early test. Both SPY and QQQ are giving us white-bodied candles in the early session while DIA is indecisive after the gap down. So, the short-term trend is being challenged and is indeterminate except for DIA which has turned down in the short-term. (If you take a broader look at DIA, it has just chopped sideways for a month.) However, the Bulls remain slightly in control of the short-term trend in at least the QQQ and SPY (market leaders). In the longer term, we are near all-time highs (potential resistance) in the SPY, QQQ, and DIA. In terms of extension, none of the three major index ETFs are far from their T-line (8ema). However, the T2122 indicator is now sitting well inside of its oversold range. So, both sides have room to run if they can gather the momentum to do it. However, the Bulls have more slack to work with. As I’ve been saying, keep watching those Tech Big Dogs. If they make a move as a group, it is almost impossible for the rest of the market to do anything but follow given their trading volumes.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Mag7 Stocks

Friday closed with the Mag7 stocks working their magic to hold indexes while internally more stocks were declining rather than advancing. Friday’s big bank reports produced mixed results but they will have another chance today to inspire the bull or bears with reports from the likes of GS and MS before today’s bell. We will also get figures from Empire State Mfg., have some Fed speak as well as short-term bond auctions to inspire. The geopolitical tensions in the Red Sea add considerable uncertainty looking forward so plan carefully.

Overnight Asian market closed mostly lower with only the Shanghai exchange eking out a small gain of just 0,27%. European markets trade lower across the board this morning as they monitor ECB members talking about rate cuts at Davos. U.S. futures point to a lower open though we have rallied significantly off the overnight lows as earnings results roll in.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday include CVGW, FULT, GS, HWC, IBKR, MS, PNFP, PNC, & PRGS.

News & Technicals’

Vodafone and Microsoft have announced a 10-year strategic alliance to deliver cutting-edge AI, digital, enterprise, and cloud solutions to millions of customers in Europe and Africa. Vodafone will leverage Microsoft’s Azure OpenAI and Copilot technologies to create customer-centric AI applications and will migrate its data centers to the Azure cloud platform to reduce costs and increase efficiency. Microsoft will also take a stake in Vodafone’s IoT business, which will be spun off as a separate entity by 2024, and will support Vodafone’s expansion of its mobile money service in Africa.

Elon Musk, the CEO of Tesla and SpaceX, wants to increase his voting power over Tesla to 25%. He currently holds about 13% of the electric car maker’s shares. In a post on Monday, Musk said he felt uneasy about Tesla’s future as a leader in AI and robotics without having more say in the company’s decisions. Musk’s move comes after he and Tesla faced a lawsuit from shareholders in Delaware, who claimed that Musk’s 2018 compensation package was too generous and that the board that approved it violated its duty to the company.

The Allianz Risk Barometer, a report that assesses the most pressing risks facing businesses and societies, revealed that political risk reached its highest level in five years in 2023. According to the report, about 100 countries faced a high or extreme likelihood of civil unrest, such as protests, riots, or violence, due to social and economic grievances. The CEO of Allianz, Oliver Bäte, attributed this situation to the growing gap between the political elite and the working class, which he regarded as the biggest threat to social stability.

Chinese Premier Li Qiang urged the world to avoid using tech innovations as tools of geopolitical rivalry and containment. Speaking at the World Economic Forum in Davos, Switzerland, on Tuesday, Li said that the only way to foster healthy competition and unleash the potential of innovation was to enhance cooperation among countries. Li did not single out any country in his speech, but his remarks came amid the ongoing tensions between Beijing and Washington over technology issues. China has repeatedly called on the U.S. to lift its sanctions on Chinese firms that block their access to advanced technology from American suppliers. The U.S. has imposed these measures in the past two years, citing national security concerns and accusing China of using high-end semiconductors for artificial intelligence to boost its military power.

The week ended on a positive note though more stocks were declining than advancing, the effect of the Mag7 stocks. The S&P 500 gained 0.1% and the Dow lost 118 points with UnitedHealth’s leading the selling, as we slide into the uncertainty of a three-day weekend. In the commodities markets, gold and oil prices increased, as geopolitical tensions escalated and bond yields moved higher. The big bank reports produced mixed results on Friday but with several more coming our way this morning be prepared for just about anything. We will also have to keep an eye on reports coming out of Daovs as the so-called political elite pontificates the future rest of us, underlings. Along with earnings we have Empire State numbers, Fed speaks, and bond auctions for the bulls or bears to find inspiration as we begin this holiday-shortened week.

Trade Wisely,

Doug

PNC Crushes, GS Beats, and Empire State Ahead

Friday was another flat and indecisive day in the market. Spy gapped up 0.32%, DIA opened 0.07% higher, and QQQ gapped up 0.26%. At that point, DIA diverged from the other two major index ETFs. DIA sold off the first 90 minutes and then followed the SPY and QQQ, which traded sideways in a tight range. Both QQQ and SPY spent the day bouncing around in the lower end of the opening gap. This action gave us black-bodied Spinning Top candles in all three index ETFs with the DIA having the largest body. DIA retested its T-line (8ema) closing just pennies below it. This all happened on below-average volume in the QQQ and SPY. For its part, DIA had just shy of average volume.

On the day, eight of the 10 sectors were in the green with Energy (+1.09%) out in front leading the way higher on the Yemeni strife. At the same time, Consumer Cyclical (-0.93%) was by far the biggest loser on the board. At the same time, the SPY gained 0.07%, DIA lost 0.33%, and QQQ gained 0.05%. Meanwhile, VXX gained 1.64% to close at 14.84 and T2122 rose but remained firmly in the center of its mid-range at 52.59. 10-year bond yields fell 3.939% and Oil (WTI) gained 1.03% to close at $72.76 per barrel.

The economic news on Friday, December Core PPI came in dead flat and lower than was expected at 0.0% (compared to a forecast of +0.2% and in line with November’s 0.0% value). At the same time, December PPI also came in lower than anticipated at -0.1% (versus a forecast of +0.1% and in line with the November -0.1% reading).

In stock news, before the open Friday, C announced it was cutting 20k jobs over the next two years as part of its massive restructuring effort. At the same time, CNC completed the sale of its Circle Health Group to private firm Pure Health. Later, STLA announced Friday that due to the recent attacks on ships in the Red Sea, the company will temporarily prioritize airfreight to address supply disruptions (at a much higher cost, obviously). At the same time, DAL announced it is shifting toward EADSY (Airbus) A350-1000 aircraft instead of BA jets (which it has used for decades). This included the order for 40 of the A350-1000 planes with the first half to be delivered in 2026. Later, UNP said it expects continued delays in shipments in midwestern states due to heavy snow, severe thunderstorms, and road closures which impact its ability to move crews to trains. Elsewhere, TSCO and TGT were among the retailers saying Friday that they expect product outages of up to 20 days due to the Red Sea attacks, which are causing ships to be rerouted around the horn of Africa. At the same time, WFC, C, and JPM all said they expect industry Net Interest Income (spread between borrowing and lending costs) peaked in Q4 2023. (This is in line with their expectation that rates will fall in 2024.) Later, SUM finalized its $3.2 billion merger with Argos North America. Meanwhile, MSFT edged out AAPL as the company with the largest market cap in the world. (MSFT was at $2.887 trillion as AAPL was “only” $2.875 trillion.) This is the first time since 2021 that AAPL was not the largest capitalized company in the world.

In stock government, legal, and regulatory news, a bipartisan group of 15 US Senators urged the SEC to closely scrutinize the bid of JBSAY to list on the NYSE. The group echoed the concerns of British Parliamentarians from earlier in the week. However, the group’s public letter to the SEC failed to directly call on the SEC to deny the listing, but the letter clearly implied that was their wish. At the same time, the FDA classified the recall of RMD respiratory masks as extremely serious since the use of those products could lead to major injuries or death. (It seems the devices cause magnetic interference with other medical devices and implants.) Later, a US Appeals Court upheld two earlier decisions by a patent tribunal reaffirming the ruling that AAPL stole the intellectual property of MASI related to medial sensor technologies that AAPL then put into their watches. Elsewhere, the FAA said Friday that the agency is planning to perform “closer monitoring” of BA 737 MAX 9 jets when they do reenter service. The agency chief told Reuters it was “pretty clear” the mid-air blowout was a manufacturing problem and not a design defect. As such, BA deserves more scrutiny, including an increase in production line and supplier inspections, which have not been standard in the past. At the same time, MS agreed to pay $249.5 million to the US Dept. of Justice and SEC to end criminal and civil investigations into the company’s handling of large block trades for its customers. Later, the US Supreme Court agreed to hear a challenge by SBUX to lower court decisions that required the company to rehire seven employees it was found to have fired due to their support of unionization. In the afternoon, the FDA announced a major recall by PEP of many Quaker Oats products over the risk of salmonella contamination. At the same time, WH told Reuters it had received a second request for information from the FTC related to a $7.8 billion hostile takeover bid from CHH.

Overnight, Asian markets leaned heavily to the red side. Hong Kong (-2.16%) was way out in front leading Taiwan (-1.14%), and South Korea (-1.12%) as well as the rest of the region lower. Only Shenzhen (+0.31%) and Shanghai (+0.27%) were in the green in that region. In Europe, we see a similar picture taking shape at midday. Only Oslo (+0.22%) is in the green while the CAC (-0.34%), DAX (-0.39%), and FTSE (-0.33%) lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a lower open to start the day. The DIA implies a -0.34% open, the SPY is implying a -0.40% open, and the QQQ implies a -0.46% open at this hour. At the same time, 10-year bond yields have moved back above four percent to 4.014% and Oil (WTI) is up a half of a percent to $73.08 per barrel in early trading.

The major economic news scheduled for Tuesday is limited to NY Fed Empire State Mfg. Index (8:30 a.m.) and Fed Governor Waller speaks (11 a.m.). The major earnings reports scheduled for before the open are limited to GS, MS, and PNC. Then, after the close, IBKR reports.

In economic news later this week, on Wednesday we get Dec. Core Retail Sales, Dec. Retail Sales, Dec Imports, Dec. Exports, Dec. Industrial Production, Nov. Business Inventories, Nov. Retail Inventories, Fed Beige Book, API Weekly Crude Oil Stocks, and Fed member Williams speaks. Then Thursday, Dec. Building Permits, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. Housing Starts, Philly Fed Mfg. Index, EIA Weekly Crude Oil Inventories, and Fed Balance Sheet are reported as well as Fed member Bostic speaks. Finally, on Friday, we get Dec. Existing Home Sales, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations as well as Fed member Daly speaking.

In terms of earnings reports later this week, on Wednesday, SCHW, CFG, PLD, USB, AA, DFS, FUL, KMI, SNV, and WTFC reports. Then Thursday, we hear from FAST, FHN, KEY, MTB, NTRS, TSM, TFC, JBHT, and PPG. Finally, on Friday, ALLY, CMA, FITB, HBAN, RF, SLB, STT, and TRV report.

In miscellaneous news, on Friday, the Biden Administration put out another bid for 3 million additional barrels of oil to continue refilling the US Strategic Petroleum Reserve. Elsewhere, if you’ve ever doubted whether the saying “it’s not the news, it’s how the market reacts to the news” than Friday was a day for you. JPM reported a record $49.6 billion in profit for 2023 on Friday, a 32% increase over 2022. This caused more than a 2% gap higher and JPM stock was up more than 3.5% in the first five minutes of the day. This was a bear trap as hard selling started at 9:35 a.m. and lasted all the way into the close. On the day, JPM sold off more than 4.12% from the high and ended the day down 0.73% compared to Thursday’s close. For its part, WFC profits rose 9% for Q4, but the market did not like that its costs rose although less than the revenue. WFC was punished with a 2.38% gap lower and ended the day down 3.34%. Part of this big bank angst was due to the forecast by big banks that they truly believe rate cuts are real and will start “soon” cutting into their interest income.

In geopolitical weekend news, Taiwan thumbed its nose at Beijing by electing the “status quo” candidate, which was not Xi’s preferred contender because he is not pro-reunification, William Lai. Almost immediately, President Biden moved to calm the situation by announcing that the US does not support Taiwanese independence and that US policy is still “one China, two systems.” However, the Chinese still did not like the fact that a lesser official, US Sec. of State Blinken, congratulated Lai on his election victory. Meanwhile, in the Red Sea, Saturday the Houthi rebels fired on a US destroyer with rockets and drones. All drones were shot down and no damage was reported. Then on Sunday, the Pentagon reported two Navy Seals had been lost overboard during a ship boarding operation in rough seas off the coast of Yemen. (That seems quite odd given the timing and other happenings in that area, but it was the story disseminated.) At the same time, the US led a second wave of air attacks on the Houthi rebels. In retaliation, on Monday the Houthi hit a US-owned container ship (which was stupid enough to ignore the events in that shipping lane during the last month as well as the US Navy’s explicit warning to all ships to avoid the area for at least three days). No major damage was reported, but a fire was caused in one hold.

So far this morning, GS and PNC reported beats on both the revenue and earnings lines. (PNC destroyed market expectations by reporting $3.16/share in earnings against the consensus forecast of $2.14/share on only modestly higher than expected revenue.) At the same time, MS beat on revenue while missing on earnings. GS cited better-than-expected “asset management profits” during its report.

With that background, markets look to be recovering a bit from a gap lower to start the premarket. All three major index ETFs are showing significant white-bodied candles at this point in the early session. SPY and QQQ both crossed back above their T-line (8ema) and DIA is close to retesting the level that all three gapped below early this morning. So, the Bulls remain in control of the short-term trend in at least the QQQ and SPY (market leaders) although the news out of Yemen had traders very nervous at the beginning of the premarket. In the longer term, we are near all-time highs (potential resistance) in the SPY, QQQ, and DIA. In terms of extension, none of the three major index ETFs are far from their T-line (8ema). At the same time, the T2122 indicator is now sitting in the middle of its mid-range. So, both the Bulls and Bears do have room to run if they can gather the momentum to do it. Continue to keep an eye on the Tech Big Dogs. If they make a move as a group, it is almost impossible for the rest of the market to do anything but follow given their trading volumes.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Member e-Learning 1-11-24 – Rick