Member e-Learning 6-21-24 – Member Joe F

Member e-Learning 6-20-24 – Doug

Member e-Learning 6-20-24 – John

One Stock That Rules Them All

S&P 500 futures point upwards on Thursday morning as the bulls look to extend the one stock that rules them all, NVDA. In addition to monitoring the stock market’s movements, investors are gearing up to dissect a slew of new economic data slated for release in the latter half of the week. Key among these are the initial jobless claims figures and housing starts data, both due this morning.

European stock markets opened on an optimistic note on Thursday morning, buoyed by a series of key monetary policy announcements. The Swiss National Bank (SNB) contributed to the positive sentiment by reducing its policy rate by 0.25 percentage points to 1.25%, marking a cautious yet significant move in its monetary stance. Meanwhile, Norway’s central bank has opted for stability, maintaining its policy interest rate at 4.5%. All eyes in the United Kingdom are now turned towards the Bank of England’s rate decision, which is due later today.

In a day marked by a general downturn in the Asia-Pacific markets, China stood out by maintaining stability in its monetary policy, holding its one- and five-year loan prime rates steady at 3.45% and 3.95%, respectively. On a brighter note, New Zealand’s economy showed signs of resilience, emerging from a technical recession with a 0.2% growth quarter-on-quarter in the initial three months of the year.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include ACN, CMC, DRI, GMS, JBL, KR, & WGO. After the bell include SWBI.

News & Technicals’

Amid escalating tensions in the Middle East, Hezbollah has issued a stark warning, indicating a stance of no restraint or “no red lines” should a comprehensive conflict break out between Lebanon and Israel. The militant group’s Secretary General, Sayyed Hassan Nasrallah, has publicly claimed that Hezbollah possesses intelligence suggesting Israel is actively engaging in military exercises within Cyprus as a precursor to war with Lebanon. In response to these allegations, Cyprus’ President Nikos Christodoulides has firmly denied any involvement in such hostilities. On Wednesday, he emphasized Cyprus’ neutral position, asserting that the nation is not a participant in the conflict but rather a contributor to the peace process. This statement from the Cypriot leader seeks to clarify the island nation’s role and dispel any misconceptions about its stance amidst the growing regional unrest.

The Swiss National Bank (SNB) has reduced its key interest rate by 25 basis points, bringing it down to 1.25%. This marks the institution’s second rate cut within the year, aligning with the predictions of two-thirds of the economists surveyed by Reuters. The consensus had been leaning towards this exact quarter-percentage-point reduction. Meanwhile, Switzerland’s inflation rate has stabilized at 1.4% in May, following a transient increase the previous month. The SNB forecasts that this inflation rate will maintain a steady average throughout the entirety of 2024. This proactive approach by the SNB reflects its commitment to balancing economic growth with price stability, amidst a landscape of fluctuating global financial conditions.

The mortgage landscape has seen a slight easing this week, as the average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances (up to $766,550) experienced a dip to 6.94% from the previous 7.02%. This marginal decrease comes amidst a broader context where mortgage applications for home purchases have shown a modest uptick of 2% over the week. However, this figure still trails by 12% compared to the same period last year, underscoring a year-over-year slowdown in the housing market. Initially, mortgage rates inched higher at the start of the week, but the trend reversed following Tuesday’s announcement of weaker-than-anticipated retail sales data, which prompted a pullback in rates. This fluctuation reflects the ongoing responsiveness of mortgage rates to economic indicators and market dynamics.

Despite its already extended condition NVDA looks to gap higher as the once stock that rules them all becoming the most valuable company in the world last Tuesday. Leadership in the market is however extremely thin so watch these tech titans careful as a turn lower could a trigger a painful pullback for those chasing in a fear of missing out.

Trade Wisely,

Doug

Public e-Learning 6-18-24 – John

Retail Sales Data

S&P 500 futures remained relatively unchanged on Tuesday morning, with investors bracing for the release of May’s retail sales data. Consensus suggests a modest increase of 0.2% from April anticipated by economists surveyed by Dow Jones. The day is also set to bring a suite of economic reports, shedding light on industrial production and business inventories. Adding to the uncertainty is, several Federal Reserve officials, including Boston Fed President Susan Collins and Richmond Fed President Tom Barkin, are slated to deliver speeches at various events nationwide.

European stock markets experienced an uptick in Tuesday’s trading session, shaking off the uncertainty that began the week. Investors’ attention is now focused on the upcoming policy rate decision from the Bank of England, scheduled for Thursday. The consensus among economists suggests that the Bank will maintain the current interest rate at 5.25%. This expectation is bolstered by a Reuters poll, where a majority of economists predict that the Bank of England might opt for a rate cut in August.

Asia-Pacific stock markets experienced a significant rebound on Tuesday, buoyed by a positive overnight performance on Wall Street. The upswing came as investors digested the latest interest rate decision from the Reserve Bank of Australia. In response to the central bank’s move, the Australian S&P/ASX 200 index saw a notable increase of 1.01%. Meanwhile, Japan’s Nikkei 225 index recovered from Monday’s nearly 2% drop, rising by 1%. The broader Topix index also enjoyed gains, albeit more modest, finishing 0.58% higher. In South Korea, the Kospi index ascended by 0.72%.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include CRMT, CGNT, & PDCO. After the bell include KBH.

News & Technicals’

Apple is currently under significant scrutiny by the European Union due to several “very serious” concerns related to the Digital Markets Act (DMA), as stated by the EU’s competition chief, Margrethe Vestager, in a CNBC interview on Tuesday. The DMA represents a comprehensive legislative effort to curb the influence of major technology companies. In March, the European Commission, which is the executive branch of the EU, initiated an investigation into Apple’s practices under this new regulation. This probe is part of a broader initiative to ensure that tech giants operate within a framework that promotes fair competition. Vestager has indicated that the findings of this investigation are expected to be disclosed “hopefully soon,” which could have significant implications for Apple’s operations within the European market.

Fisker, the American electric vehicle (EV) manufacturer, has sought bankruptcy protection, a move announced late Monday. The company has been grappling with a swift depletion of funds, primarily due to the costs associated with rolling out its “Ocean” SUVs in both the United States and Europe. In a strategic pivot aimed at addressing its financial woes, Fisker is now looking to sell its assets and restructure its debt under Chapter 11. The decision comes after a thorough review of potential avenues for the business, with the company stating, “After evaluating all options for our business, we determined that proceeding with a sale of our assets under Chapter 11 is the most viable path forward for the company.” This development marks a significant turn for Fisker, as it seeks to navigate through its current challenges and find a sustainable path forward in the competitive EV market.

The Kremlin has confirmed that President Vladimir Putin is set to embark on a ‘friendly state visit’ to the Democratic People’s Republic of Korea (DPRK), accepting an invitation from North Korea’s leader, Kim Jong Un. This announcement, made on Monday, has sparked considerable attention on social media platform X, where videos and images depict the streets of Pyongyang adorned with Russian flags and portraits of Putin, signaling preparations for his anticipated arrival. The visit is drawing scrutiny from geopolitical analysts, with one commenting that the burgeoning relationship between Moscow and Pyongyang represents “a threat like no other” to Western interests. This visit underscores the deepening ties between the two nations and could have far-reaching implications for international relations and security dynamics.

Boeing’s CEO, Dave Calhoun, is set to confront a Senate panel amid escalating concerns over safety and quality control issues plaguing the aircraft manufacturer. The hearing, convened by the Senate Homeland Security Committee’s Permanent Subcommittee on Investigations, is scheduled to commence at 2 p.m. ET on Tuesday. This comes in the wake of a recent incident where a door plug was ejected from a Boeing 737 Max plane mid-flight, an event that has intensified scrutiny on the company. The nearly new aircraft’s mishap in January has put Boeing squarely in the hot seat, as it grapples with the fallout and faces tough questions from lawmakers about its commitment to safety standards.

After Monday’s surge higher it’s likely the retail sales data will determine if the bulls can follow though for another winning day. Expect price volatility Fed members pontificate interest rates with speaking engagements around the county today. Remember the market is closed on Wednesday so plan your trading risk accordingly.

Trade Wisely,

Doug

Contrasting Performance

The stock market presented a contrasting performance last week, with the Dow Jones Industrial Average facing a downturn for the third time in four weeks. In contrast, both the S&P 500 and the Nasdaq Composite soared, achieving record highs and marking their seventh week of gains in the recent eight. The upcoming week, however, will see a truncated trading schedule as markets close on Wednesday in observance of the Juneteenth holiday. This pause in trading may offer a moment for investors to reflect on the market’s recent volatility and prepare for the second half of the month.

European markets experienced a downturn on Monday, retracting from initial advances as a wave of pessimism swept through the trading floors. Investors’ focus was largely drawn towards the impending interest rate verdict from the Bank of England, which cast a shadow of uncertainty. By mid-morning, at 11:15 a.m. London time, the Stoxx 600 index had declined by 0.33. The French CAC 40 also succumbed to the negative trend, edging down by 0.14%.

In a recent economic update, the People’s Bank of China maintained its medium-term lending facility rate steady at 2.5% on a substantial 182 billion yuan, aligning with market predictions. Meanwhile, China’s retail sector outperformed analyst forecasts, registering a 3.7% year-on-year increase in May, surpassing the anticipated 3% rise based on a Reuters survey. However, Asian markets closed red across the board.

Economic Calendar

Earnings Calendar

Notable reports for Monday there are no reports before the bell. After the bell include LEN, & LZB.

News & Technicals’

In an effort to de-escalate mounting tensions along the Lebanon border, a senior U.S. adviser is set to visit Israel. The region has seen an uptick in hostilities, with a recent barrage of missiles intensifying concerns over the possibility of a larger conflict. The Israeli military has cited Hezbollah’s increasing aggression as a critical factor pushing the situation toward a potential escalation. Amos Hochstein, serving as a senior diplomatic adviser to U.S. President Joe Biden’s administration, is scheduled to arrive in Israel on Monday. This visit, reported by an Israeli official to NBC News, is a strategic move to mediate and hopefully reduce the strains that have been building in the volatile border area.

TDK, the renowned Japanese electronic parts manufacturer, announced a significant breakthrough on Monday with the development of a new material designed for solid-state batteries. This Tokyo-based company, also known for supplying components to Apple, highlighted the potential of this innovation to revolutionize personal electronics. The material is particularly suited for devices that are worn close to the body, such as wireless earphones, hearing aids, and smartwatches. A key aspect of TDK’s solid-state battery technology is the incorporation of oxide-based solid electrolytes. This choice of material is not just a technical decision; it’s a commitment to safety, as the company asserts these batteries are “extremely safe.” This advancement could pave the way for more reliable and durable consumer electronics that integrate seamlessly into our daily lives.

In a landmark decision, a judge has sanctioned a $4.5 billion settlement involving Do Kwon, Terraform Labs, and the U.S. Securities and Exchange Commission (SEC). This settlement comes in the wake of Binance’s earlier agreement with the U.S. authorities in November, which amounted to $4.3 billion. These legal resolutions are part of a broader crackdown on illicit activities that shook the foundations of the cryptocurrency sector in 2022. The recent series of criminal convictions and financial penalties signify a turning point, bringing closure to the tumultuous events and holding accountable the individuals whose actions significantly disrupted the crypto industry. This marks a concerted effort by regulatory bodies to restore integrity and stability in the digital asset space.

The future of Social Security benefits hangs in the balance, with projections suggesting a potential across-the-board cut for beneficiaries within the next decade unless Congress intervenes. The legislative body currently appears immobilized, unable to reach a consensus on the path forward. Amidst this deadlock, the proposal of a bipartisan commission has emerged as a possible solution, garnering a polarized response. Advocates argue that such a commission could bridge political divides and forge a sustainable future for Social Security. Conversely, critics fear that it may lead to compromises that could undermine the program’s integrity. This dichotomy of views underscores the complexity of reforming a system that millions of Americans rely on for financial security in retirement.

The contrasting performance with new record highs in the SPY and QQQ with the DIA and IWM show bearish trend makes for considerable uncertainty in this holiday shortened week. Keep an eye on the dollar breaking recent highs but showing considerable volatility in the overnight session. With retail sales figures in focus before the bell Tuesday after Friday’s disappointing Consumer Sentiment, plan your risk carefully.

Trade Wisely,

Doug

Bears Looking to Roar This Morning

TSLA and AVGO led broader market ETFs to open higher (again) Thursday while DIA started lower. SPY gapped up 0.34%, QQQ gapped up 0.74%, and DIA gapped down 0.20%. From that opening level, SPY and QQQ slowly sold off, reaching the lows at 12:35 p.m. At that point, both of the broader index ETFs reversed course and slowly rallied the rest of the day. Meanwhile, after the open, DIA sold off a bit more sharply, reaching its lows at 10:40 a.m. Then it ground sideways until 12:35 p.m. when it started its own slow, steady rally lasting 3 p.m. when it had recrossed the opening gap. From there, DIA slowly sold back down toward the opening level by day end. This action gave us a gap-up, black-bodied, Hanging Man type candle in the SPY. The QQQ gave us a gap-up, black-bodied, Spinning Top candle. Finally, DIA printed a gap-down Doji candle that did not quite retest its T-line (8ema) from below. It is worth noting that this was the fourth-straight new record high close in both the SPY and QQQ.

On the day, all 10 sectors were in the red with Energy (-1.27%) way out in front (by half a percent) leading the rest of the market lower. Meanwhile, Technology (-0.06%) and Utilities (-0.06%) holding up better than other sectors. At the same time, SPY gained 0.20%, DIA lost 0.21%, and QQQ gained 0.54%. VXX was down 0.28%, closing at a very low 10.86 and T2122 dropped back down into its oversold territory at 12.70. On the bond front, 10-year bond yields fell sharply again to 4.246% and Oil (WTI) fell 0.49% to close at $78.01 per barrel. So, on Thursday we saw divergence in the market as NVDA, TSLA, AAPL, and AVGO nearly alone dragging the broader index ETFs higher (perhaps with the help of good PPI data), while 70% of the market was down. It is also worth noting that SPY had only half of its average volume while DIA and QQQ had less-than-average volume.

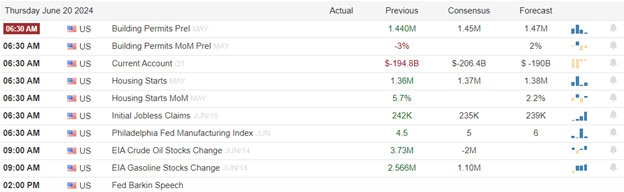

The major economic news scheduled for Thursday included Weekly Initial Jobless Claims, which came in higher than expected at 242k (compared to a forecast of 225k and the prior week’s 229k value). On the ongoing front, Weekly Continuing Jobless Claims, were also above expectations at 1,820k (versus a forecast of 1,800k, and the prior week’s 1,790k reading). At the same time, May Core PPI (month-on-month) was down at +/-0.0% (compared to a forecast of +0.3% and well below the April +0.5% value). On the headline side, May PPI (month-on-month) was also down significantly at -0.2% (versus the +0.1% forecast and far below April’s +0.5% reading). Then, after the close, the Fed Balance Sheet actually grew slightly on the week, now standing at $7.259 trillion (compared to last week’s $7.256 trillion) for a $3 billion increase.

In economic speak news, Treasury Sec. Yellen told the Economics Club of NY that US public sector investments are crucial to sustainable growth because it attracts private capital investments. However, she warned that China’s model of huge state subsidies of industrial projects was unacceptable to the world. (Expanding on this, in more of an economic or economic-political philosophy clarification, Yellen said that supply-side economics relies too heavily on tax cuts and has been proven to fail to benefit workers, causing disparity.) She said “We have learned through experience that heavy-handed central planning through government dictates is not a sustainable economic strategy … But neither is traditional supply-side economics, which ignores the importance of public infrastructure, education and workforce training and government-supported basic research.” She concluded, by saying tax cuts for the wealthy and deregulation have not fueled “growth and prosperity for the nation at large.” Elsewhere, NY Fed Pres. Williams pushed back against the idea of rate cuts anytime soon in his noon speech. Williams said, “we aren’t really talking about rate cuts right now (at the Fed) … and it’s premature to speculate about them.”

After the close, ADBE reported beats on both the revenue and earnings lines. At the same time, RH beat on revenue while missing on earnings. It is worth noting that ADBE also raised forward guidance. (ADBE was up 17% in post-market trading.)

In stock news, on Thursday, Reuters reported that BA is investigating new quality issues with 787 Dreamliner jets that have not been delivered yet. This comes after the company discovered hundreds of fasteners were incorrectly installed in fuselages. (It was found than many were incorrectly torqued, or tightened, while some were in the wrong place altogether.) At the same time, INSM announced that its negotiations with AZN over commercialization of its brewnsocatib drug have ended with no deal. Later, Bloomberg reported that WFC had fired more than a dozen employees from its wealth mgmt. and investment unit for faking work by using simulation of keyboard activity. At the same time, WMT announced it will re-launch a private label fashion line focused on attracting Gen Z customers.

Elsewhere, TSN suspended its CFO (the great-grandson of company founder) after his second arrest for driving under the influence in two years. At the same time, F announced it will soon reverse its decision and allow all of its dealerships to sell electric vehicles. (Previously, F had required dealers to spend between $500k and $1 million on equipment, training, and “programs” before they were allowed to sell F electric vehicles.) Later, GME stock prices were boosted on the day after Keith Gill (Roaring Kitty) exercised 40,000 call options, taking possession of 4 million new shares and making him the fourth-largest shareholder with over 9 million shares. (Gill also took profits on 80,000 call options, meaning he liquidated all 120k call options he held going into the day.) GME was up 14.28% on the day. At the same time, Elon Musk claimed victory early Thursday, but the shareholder vote did not begin until after the close. By 7 p.m. Eastern, it was announced that shareholders had in fact approved Musk’s $56 billion pay package. The package had originally been based on the value of TSLA rising to more than $650 billion between 2018 and 2028. (As of now, TSLA has a $582 billion market cap, but in 2021 it was worth $1.2 trillion at its peak.)

In stock legal and governmental news, on Thursday, the largest oil industry trade group (representing the likes of XOM and CVX) sued the EPA, seeking to block the Biden Administration’s efforts to reduce car emissions. (The EPA tightened, slightly…by 2% per year after 2026, to encouraging electric vehicle adoption.) The suit alleges the EPA exceeded it authority in setting emissions standards that would require a change in fuel type for the auto industry to meet. Later, the state of FL and DIS ended the long feud (based on the Gov. retaliating against the Mouse House for its opinion on his “Don’t Say Gay” law), by signing a 15-year deal allowing DIS to develop additional portions of the oversight district. (The board of that district was the method the Gov. used to attack DIS for its criticism.) At the same time, the FAA Administrator Whitaker admitted the agency had been “too hands off” with BA by focusing on analysis of the faked or wrong paperwork BA submitted rather than in-person audits of production line work (prior to the paperwork being created). Whitaker said that approach had been corrected and will not revert (in what was an unstated claim that BA could not be trusted).

Meanwhile, JPM won a court battle with a Greek fintech firm who created an app called Viva Wallet. The court ruled JPM had no incentive to depress Viva Wallets value because the bank owned 48.5% of the app-creating company. Under the ruling, the Greek firm loses the right to refuse JPM’s offer to buy them out and valued the company at $5.4 billion. At the same time, a lawsuit was filed against AAPL in CA, accusing the company of 12,000 female employees less than men for comparable jobs. Later, the US Supreme Court ruled in favor of SBUX, throwing out a lower court ruling that the company had to abide by an NRLB injunction requiring the company to rehire employees fired when they sought to unionize. (The ruling was actually that the lower court had used the wrong legal standard for siding with the NLRB and the case must be reheard at the lower court level.) At the same time, GOOGL was hit with a complaint to the EU antitrust regulators over alleged user tracking by its Chrome web browser.

Overnight, Asian markets were evenly split with six exchanges in the green and six in the red. Taiwan (+0.86%) led the gainers while Hong Kong (-0.94%) paced the losses. In Europe, the picture is much weaker with 14 of the 15 bourses in the red and only Russia (+0.43%) in the green. The CAC (-2.58%), DAX (-1.51%), and FTSE (-0.53%) are a good representation of the spread and lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a gap lower to start the day. The DIA implies a -0.88% open, the SPY is implying a -0.60% open, and QQQ is implying a -0.33% open at this hour. At the same time, 10-year bond yields are down to 4.207% and Oil (WTI) is just on the green side of flat at $78.67 per barrel in early trading.

The major economic news scheduled for Friday include May Import Price Index and May Export Price Index (both at 8:30 a.m.), Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations (all at 10 a.m.), and the Fed Monetary Policy Report (11 a.m.). There are no major earnings reports scheduled for either before the open or after the close.

In miscellaneous news, on Thursday, cocoa traded back above $10k per ton as the supply outlook worsens. (The world’s top producer Ivory Coast halted exports for June and forward sales of next season’s crop on Thursday.) Elsewhere, twice-impeached, convicted felon ex-President Trump said Thursday that, if elected, he would reduce corporate tax rates again, as well as considering cuts to other income tax rates (in addition to extending the tax cuts from his administration scheduled to sunset in 2025). This was part of his campaign to buy corporate donors and PAC support. (The statement was made to a group of CEOs including JPM’s Dimon and AAPL’s Cook.) Meanwhile, Bloomberg reported some surprising data out of NY. The report said average Manhattan apartment rents unexpectedly slipped in May, with new leases showing a 3.5% decline in price from a year earlier.

In geopolitical news, Russian “President” Putin made a propaganda announcement of his preconditions that Ukraine would need to meet before he would even begin peace negotiations (following 2.5 years of his unprovoked invasion and genocidal war against Ukraine). Those preconditions include Ukraine ceding their provinces of Donetsk, Lugansk, Zaporizhzhia, and Kherson to Russia. (Russia illegally annexed those four oblasts after its invasion. In addition, he demanded that Ukraine denounce and give up its long-standing ambition to join NATO. (The latter would leave Ukraine as a target he can invade again without NATO retaliation, should they ever do anything he does not like or he just feels more prepared.) These are all obvious non-starter conditions, but are intended as PR ahead of the global peace conference to be attended by 80-90 countries (Russia not invited).

In other news, interestingly, Elon Musk’s big $56 billion pay package win in the shareholder vote Thursday DOES NOT override the court ruling from five months ago, when Musk’s pay package was thrown out as egregious as part of a shareholder lawsuit. However, the post-verdict vote could help his (technically TSLA’s) appeals of the verdict in the future. Not one to let things alone, Musk told the board that “his Optimus humanoid robots” could make TSLA worth $25 trillion (which would be 55% the S&P 500’s combined value at today’s prices). That figure should be weighed against TSLA’s current $580 billion value.

With that background, the Bears have control in the premarket this morning. The SPY and QQQ opened a bit higher but have put in large black-body candles since then. (However we should note they are both well up off the early session lows.) Meanwhile, DIA gapped lower to start the premarket and has also sold off since then. but again us up off the early session lows.) Again, SPY and QQQ sit at all-time highs as they wait for the open while DIA is 4.3% below its all-time high. So, Bears are in control this morning, but are coming from different starting places. Again, the short-term is mixed with DIA definitely bearish and SPY and QQQ clearly bullish. At the same time, the mid-term remains bullish in all three major index ETFs and the longer-term market remains very Bullish in trend. In terms of extension, QQQ is now extended far above its T-line and is badly in need of rest or pullback. Neither of the others are extended from their T-line. However, the T2122 indicator is back in the center of its oversold range. So, the bottom line is that outside of the QQQ, the market has room to run in either direction. With regard to those 10 big dog tickers, eight of the 10 are in the red this morning. However, it is again the two biggest TSLA (+1.35%) and NVDA (+0.03%) that are the ones holding onto green territory. Remember, its Friday, Pay Day, and that next Wednesday is a market holiday.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

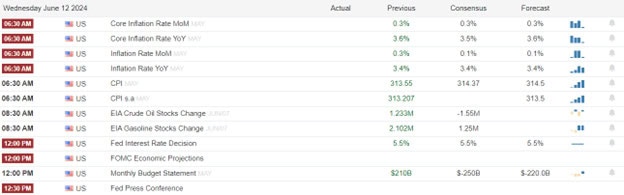

PPI in Focus

The S&P 500 futures Thursday, with PPI in focus with a side order of jobs data before the bell. This followed closely on the heels of the Federal Reserve’s latest interest rate decision, which, along with a May consumer inflation report that was more subdued than anticipated. Broadcom stood out with its shares leaping 14% in premarket trading, announcing an enticing 10-for-1 stock split.

European markets faced a downturn on Thursday, with the Stoxx 600 index falling 0.6% by 9:45 a.m. in London, a stark contrast to the robust gains it had secured the previous day. The volatility was particularly pronounced in the case of the French IT giant Atos, whose shares experienced a dramatic 14% drop following the announcement of the divestiture of its consultancy arm, Worldgrid.

Asian markets traded mixed but mostly higher. Leading the charge was South Korea’s Kospi, increased of 0.98%, closing at 2,754.89. Over in Hong Kong, the Hang Seng index also participated in the rally, climbing 0.87%.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include KFY, SIG, MDRX, & WLY. After the bell includes ADBE.

News & Technicals’

Elon Musk, CEO of Tesla, has indicated that the company’s shareholders are poised to endorse his contentious $56 billion pay package, alongside a resolution to relocate Tesla’s corporate domicile to Texas. This substantial compensation plan, which was initially ratified in 2018, set forth ambitious benchmarks for Tesla’s financial metrics and valuation. While some detractors have voiced concerns over the enormity of the package and Musk’s potential diversion of focus due to his involvement with other ventures, including a social media platform, proponents maintain that Musk’s leadership and innovative drive are indispensable for Tesla’s continued prosperity and pioneering role in the electric vehicle industry. The debate encapsulates the broader discourse on executive remuneration and the impact of dynamic leadership on corporate success.

The trading landscape for GameStop shares took a dramatic turn on Wednesday afternoon as a significant sell-off ensued. Amidst this market activity, attention was drawn to “Roaring Kitty,” also known as Keith Gill, a prominent figure in the GameStop trading frenzy. The latest disclosure of his investment portfolio revealed on Monday night that he retained ownership of 120,000 call options contracts. These contracts are characterized by a strike price of $20 and are set to expire on June 21. In a remarkable display of market movement, GameStop call options matching Gill’s strike price and expiration date saw a staggering 93,266 contracts being traded on Wednesday, highlighting the volatile nature of the stock and the keen interest of traders in these specific options.

Digital wallets have become a cornerstone in the global payment landscape, as evidenced by their substantial share in both e-commerce and brick-and-mortar transactions. In 2023, digital wallets were responsible for 50% of all e-commerce purchases and 30% of in-store purchases, amassing a staggering $14 trillion in transaction value. This trend is expected to continue its upward trajectory, with projections estimating that digital wallet transactions will reach an impressive $25 trillion by 2027. The Asia-Pacific region, in particular, has embraced this payment method with open arms; 70% of online payments and 50% of in-store payments were conducted through digital wallets last year, the highest adoption rate globally. China is at the forefront of this digital revolution, leading the world with 82% of e-commerce and 66% of in-store purchases made via digital cards, contributing to approximately $7.6 trillion in transactions. This data not only highlights the growing consumer preference for digital wallets but also underscores the significant role they play in shaping the future of financial transactions worldwide.

The wild price volatility and whipsaws could continue this morning with the PPI in focus along with Initial Claims to keep traders guessing. However, big tech continues to surge after the Broadcom reports expecting another new record high in the Nasdaq at the open.

Trade Wisely,

Doug