As the second half of 2024 commences, investors are gearing up for a holiday shortened week. The week could be eventful, with the anticipation building towards Friday’s release of the June jobs report, which is expected to provide significant insights into the current state of the labor market. Preceding this, the S&P PMI manufacturing and ISM manufacturing data for June will be disclosed on Monday. Additionally, May’s construction spending figures are also slated for release, potentially impacting market movements.

Europe’s Stoxx 600 index experienced a modest recovery, climbing 0.45% by mid-morning and breaking a streak of four consecutive losses. This uptick was largely fueled by a surge in France’s CAC 40 index, which saw an initial spike of over 2.5%, later stabilizing to a 1.3% increase.

China’s (PMI) for manufacturing held steady at 49.5 over the weekend, mirroring the figure from May and signaling a continuation in the sector’s contraction for the second consecutive month. Meanwhile, Japan’s economic outlook has been adjusted to reflect a deeper downturn than initially reported. The country’s Gross Domestic Product (GDP) for the first quarter was revised downward, showing a contraction of 2.9% year-on-year.

Economic Calendar

Earnings Calendar

There are no notable reports on this Monday.

News & Technicals’

Google is set to make a significant leap in renewable energy investment by partnering with BlackRock to develop a 1 gigawatt solar capacity pipeline in Taiwan. This initiative, announced on Monday, is part of Google’s broader strategy to enhance energy capacity and reduce carbon emissions, particularly in light of the growing demands of the artificial intelligence industry. The collaboration involves a capital investment in Taiwanese solar developer New Green Power, pending regulatory approval, which aims to expedite the construction of a substantial solar infrastructure. A segment of this new solar capacity is designated to supply power to Google’s data centers and cloud region within Taiwan, aligning with the company’s commitment to sustainable operations and its goal of achieving net-zero emissions by 2030. This move not only underscores Google’s dedication to environmental stewardship but also reflects the tech giant’s recognition of the critical role that green energy plays in supporting the technological advancements of the future.

In a strategic move to consolidate its manufacturing process and address ongoing safety concerns, Boeing has announced its intention to acquire fuselage manufacturer Spirit AeroSystems. This decision follows a significant leadership overhaul at Boeing, which was prompted by a serious incident where a door panel detached midflight from a nearly new Boeing 737 Max 9 jet. The acquisition, valued at approximately $4.7 billion, is seen as a step towards improving the quality and safety of Boeing’s aircraft, as both companies have faced challenges in eliminating manufacturing defects on the 737 Max, Boeing’s best-selling aircraft.

Meta, the parent company of Facebook, has come under scrutiny from European Union regulators. On Monday, it was accused of not adhering to the EU’s stringent antitrust regulations concerning its new ad-supported social networking service. This accusation marks a significant challenge for Meta, as it navigates the complex regulatory environment of the EU. The bloc’s antitrust rules are designed to ensure fair competition and prevent any single company from dominating the market to the detriment of consumers and competitors. Meta’s alleged non-compliance could have serious implications, including the possibility of hefty fines and mandatory changes to its business practices. The situation underscores the increasing tension between large tech companies and regulatory bodies, as governments seek to rein in the influence of these digital giants.

As the premarket bulls try to shake off Friday’s whipsaw to kick-off this holiday shortened week, we should expect volume to decline with the early close on Wednesday. However, expect bursts of price volatility with a Powell speech, FOMC minutes and of course the Friday employment situation report.

Friday gave us a modestly higher open. SPY and QQQ both gapped up 0.15%, while DIA opened 0.05% lower. At that point, all three major index ETFs rallied hard for 45 minutes (SPY and QQQ) or 75 minutes in DIA. This took the SPY and QQQ to new all-time highs. However, this was a Bull trap as the rug was pulled out from under the market and we saw a strong and steady selloff all the way until 3:35 p.m. Only a modest bounce during the last 30 minutes kept them from closing on the lows. This action gave us large, indecisive, black-bodied Spinning Top type candles in SPY, QQQ, and DIA. SPY and QQQ were also Bearish Engulfing of the prior candle while DIA was a Bearish Harami compared to the prior candle body. All three retested their T-line (8ema) with QQQ and DIA remaining just above while SPY crossed just below following the test.

On the day, six of the 10 sectors were in the red with Consumer Cyclical (-0.58%) out in front leading the way lower. Meanwhile, Communications Services (+0.89%) led the four gaining sectors. At the same time, SPY lost 0.39%, DIA lost 0.08%, and QQQ lost 0.52%. VXX climbed just over one percent to close at a still very low 10.92 and T2122 climbed again, but remains in the center of its mid-range at 61.69. On the bond front, 10-year bond yields spiked to 4.384% and Oil (WTI) fell slightly to close at $81.52 per barrel. So, Friday was a volatile day that saw a strong early run met with a sustained selling that only ended with some short-covering. This all took place on a bit below-average volume in SPY, average volume in QQQ, and slightly above-average volume in DIA.

Friday was also month and quarter end. For June, SPY gained 3.20%, DIA gained 0.93%, and QQQ gained 6.30%. Over Q2, SPY gained 4.04%, DIA lost 1.67%, and QQQ 7.91%. So, as has been the case all year, QQQ and SPY lead (mostly on the strength of the AI trade led by NVDA), while the much less techie DIA followed.

The major economic news scheduled for Friday included May Core PCE Price Index, which was down as expected at +0.1% (month-on-month) compared to a +0.1% forecast and April’s +0.3%. On the Year-on-Year basis, the May Core PCE Price Index was +2.6% (right on the 2.6% forecast and down from April’s +2.8% reading). The headline on a Month-on-Month basis the May PCE Price Index was also down as predicted at +0.0% (versus a 0.0% forecast and down from April’s +0.3% number). On the Year-on-Year basis, May PCE Price Index was +2.6%, right on the +2.6% forecast and down a tick from April’s +2.7%. At the same time, May Personal Spending was up a tick, but below what was anticipated at +0.2% (compared to a +0.3% forecast and April’s +0.1% value). Later, the June Chicago PMI was significantly stronger than was expected at 47.4 (versus a 39.7 forecast and May’s 35.4 reading). Then, Michigan Consumer Sentiment was down but a bit higher than predicted at 68.2 (compared to a 65.6 forecast and May’s 69.1 value). On the future prospects side, Michigan Consumer Expectations were up slightly to 69.6 (versus a 67.6 forecast and May’s 68.8 reading). Further out, the Michigan 1-Year Inflation Expectations were down strongly to 3.0%, versus the 3.3% forecast and prior reading. On the longer-term, the Michigan 5-Year Inflation Expectations were also 3.0% (better than the 3.1% forecast and the same as the prior month’s 3.0%).

The most important thing that happened Friday was another (terrible) Supreme Court ruling that was a massive win for corporations and big money in the aptly named case “Relentless v. Dept. of Commerce.” The decision wiped out the 40-year-old “Chevron Deference,” which had held that Congress is incapable of writing perfectly detailed and crystal-clear laws. In addition, Courts are not subject experts and are likewise unable to devine either the intent or understand and decide the nuances and issues that are involved. So, under the previous Chevron Deference, if there was a question of nuance or implementation of an aspect of the law, the courts would defer to the interpretation of the experts at the Federal agency in charge of applying that law. This new ruling throws that out, saying the courts will decide all such issues (or, theoretically, Congress could revisit every law and repass new revisions every time somebody tries to challenge an aspect of the law). On one hand, this decision is a huge, full-employment jobs program for lawyers. More importantly, it is a license to challenge any and every aspect of regulation that is not clearly and explicitly set out in law. (If there is any possible way to interpret a law differently than federal agencies have interpreted it in the past, it is now up to a court to decide how it should be construed.) This drastically reduces the power of the Federal government and means that the courts will decide vastly more of the issues regulating business and personal behavior at the expense of real expertise or speed. So, a ton of guardrails just got removed from food and drug safety, environmental protection, labor protection, etc. and the world just got much slower. Meanwhile, money got more powerful and the courts just got much, much busier. This was a huge win for those who want less (or no) regulation. It was also a huge defeat for anyone who does not trust businesses to ALWAYS do the right thing and act in the best interest of society. Another outcome is that a lot more of the federal budget will be spent on litigation.

In stock news, on Friday BA (and NASA) again delayed the possible return trip of the company’s Starliner spacecraft. The announcement said the problems with the BA spacecraft will require at least a “couple more weeks” of testing by engineers before it can be determined if it is safe to attempt the return trip. In another classic “own goal” the BA executive on the conference call announcing the decision to reporters criticized the press for reports saying the two astronauts in the Starliner crew were stuck in space. This led to NASA confirming that if worse comes to worse, they can launch a SpaceX (BA rival) mission to retrieve the crew. Elsewhere, CNBC reported that F now expects to sell a $30k electric vehicle that is profitable within 2.5 years. On Saturday, AMZN announced it is doubling the free cloud service credits (to $200k) that is gives to startups. The move comes in an effort to better compete with MSFT, which is making gains in cloud computing market share. Elsewhere, on Sunday US prosecutors met with BA and families of BA crash victims from 2018 and 2019. The topic of discussion was on whether the US will prosecute BA for violating their consent decree that allowed them to avoid prosecution over those two crashes. The contention is that the company did not change and improve quality after the consent decree given the many revelations of the last year or so. On Sunday evening, CNBC reported that the Dept. of Justice is now seeking a guilty plea from BA over the matter. There was no reply from BA when asked for comment.

In stock legal and governmental news, on Friday, the NTSB and FAA announced they are investigating a LUV flight that took off from a closed airport in ME. At the same time, EU antitrust regulators announced they will release their decision on the HPS $14 billion acquisition of JNPR by August 1. Later, the US Dept. of Energy said they are bidding to buy $2.7 billion of domestically-supplied uranium to boost the US nuclear energy supply chain. This will benefit LEU and a British/Dutch company (Urenco) with uranium mining operations in NM. At the same time, the NHTSA announced it has opened a recall inquiry into more than 120k HMC Ridgeline trucks over failures of the rearview cameras.

Overnight, Asian markets were mostly green. Only Australia (-0.22%) and Thailand (-0.12%) fell below break-even while Shanghai (+0.92%), Shenzhen (+0.57%), and India (+0.55%) led the region higher. In Europe, we see green across the board at midday. The CAC (+1.46%) seems to love first round election results while the DAX (+0.27%), and FTSE (+0.27%) are also leading the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a modestly green start as well. The DIA implies a +0.18% open, the SPY is implying a +0.19% open, and the QQQ implies a +0.18% open at this hour. At the same time, 10-Year bond yields are spiking again up to 4.412% and Oil (WTI) is up another two-thirds of a percent to $82.05 per barrel in early trading.

The major economic news scheduled for Monday includes S&P Global Mfg. PMI (9:45 a.m.), May Construction Spending, June ISM Mfg. Employment, June ISM Mfg. PMI, and June ISM Mfg. Prices (all at 10 a.m.). There are no major earnings reports set for Monday either before the open or after the close.

In economic news later this week, on Tuesday we get May JOLTs Job Openings, API Weekly Crude Oil Stocks, and Fed Chair Powell speaks (9:30 a.m.). Then Wednesday, MARKETS CLOSE AT 1 P.M. In addition, JUNE ADP Nonfarm Employment, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, May Trade Balance, S&P Global Services PMI, S&P Global Composite PMI, May Factory Orders, June ISM Non-Mfg. Employment, June ISM Non-Mfg. Prices, EIA Weekly Crude Oil Inventories, and FOMC Meeting Minutes are reported. NY Fed President Williams also speaks. On Thursday, MARKETS ARE CLOSED. However, we still get the Fed Balance Sheet. Then on Friday, June Avg. Hourly Earnings, June Nonfarm Payrolls, June Private Nonfarm Payrolls, June Participation Rate, and June Unemployment Rate are reported. NY Fed President Williams also speaks.

In terms of earnings reports later this week, on Tuesday we hear from MSM, PSNY, and RDUS. Then Wednesday, STZ reports. There are no earnings reports Thursday or on Friday.

In miscellaneous news, on Friday, Bloomberg reported it has seen an unpublished government report that claims the lithium market is about to change. Even with huge deposits and despite massive investment from outside the country, Argentina has only had one lithium mine come online in the last 10 years. However, the report cited by Bloomberg claims that four new lithium mines will come online in Argentina in the next few weeks to months. This will nearly double the production capacity of that fourth-largest lithium producing country. Elsewhere, early Monday an SEC filing showed that social media poster (leader of the meme stock movement) has taken a 6.6% ownership position in CHWY. (This confirms the huge volatility caused by his cryptic posting of a dog picture Thursday.)

In foreign election news, polls released Saturday show the UK is headed for its first Labor government since 2010. With the election set for July 4, the Labor Party is at 40%, the current-government Conservatives are at 20% (and falling), and the Reform Party is at 17%. Across the English Channel, the first round of the French election took place Sunday. The far-right National Rally party won 34%, the left-wing New Popular Front won 28.1%, and President Macron’s centrist Ensemble party came in third at 20.3%. All other parties will be eliminated in next Sunday’s second and final round of voting. So, between now and next week, the fight will be on to capture the 17%-18% of votes that were cast for parties eliminated yesterday. (It is worth noting that in just-dissolved Parliament, Macron’s party only had 43% of the seats. So, he was a coalition President even in the last Parliament.)

With that background, it looks as if markets are starting the premarket modestly stronger. All three major index ETFs retested their T-line in the early session but have made modest moves up off that retest. It is worth noting that SPY and QQQ have printed indecisive Spinning Top-type candles so far this morning. All three major index ETFs remain above their T-line (8ema). Again, remember that despite intraday movement, all three major index ETFs are still quite near their all-time highs. So, the short-term trend is modestly bullish. However, the mid-term and especially the longer-term trend in all three major index ETFs remains very bullish. In terms of extension, none of those three are extended above their T-line and the T2122 indicator is in its mid-range. Therefore, the market has plenty of room to run in either direction. With regard to those 10 big dog tickers, eight of the 10 are in the green this morning. However, the biggest dog of all, NVDA (-1.10%) is one of the two laggards.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Thursday, markets started out just on the red side of flat. SPY opened 0.03% lower, DIA opened 0.15% lower, and QQQ opened 0.04% lower. From there, all three major index ETFs meandered sideways in waves ranging from up half a percent to down a third of a percent. The most notable move of the day was the late-day rally on the final up wave. This action gave us white-bodied, indecisive candles (some form of a Spinning Top) in all three. SPY and DIA both retested their T-line (8ema) from above and passed by bouncing up off that line. However, it should be noted that all three of the major index ETFs traded at far less than half of their 50-day average volume.

On the day, nine of the 10 sectors were in the green with Energy (+0.49%) leading the market higher. Meanwhile, Consumer Defensive (-0.38%) was the laggard and only sector in the red. At the same time, SPY gained 0.16%, DIA gained 0.08%, and QQQ gained 0.26%. VXX fell another 0.64% to close at 10.81 and T2122 climbed again, this time closing right in the center of its mid-range at 52.54. On the bond front, 10-year bond yields fell to 4.286% and Oil (WTI) gained 1.19% to close at $81.86 per barrel. So, Thursday was a very low volume and just on the bullishly indecisive day where it looks like traders were either holding off until after the Presidential Debate or PCE data release. (Or maybe traders have already left for a very long holiday break.)

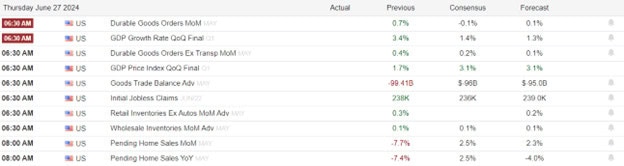

The major economic news scheduled for Thursday included Weekly Initial Jobless Claims, which came in slightly lower than expected at 233k (compared to a forecast of 236k and a previous week value of 239k). In terms of ongoing claims, the Weekly Continuing Jobless Claims were higher than predicted at 1,839k (versus a 1,820k forecast and the prior week’s 1,821k reading). At the same time, May Core Durable Goods Orders were down at -0.1% month-on-month, compared to a forecast of +0.2% and the April +0.4% reading. For the headline number, May Durable Goods Orders (again, month-on-month) were down but higher than anticipated at +0.1% (versus the -0.5% forecast but down from April’s +0.2% value). Meanwhile, Q1 Core PCE Prices were higher than expected at +3.70% (compared to the +3.60% forecast and sharply higher than April’s +2.00% value). At the same time, Q1 GDP was stronger than was predicted at +1.4% (versus a +1.3% forecast but down as expected from Q4’s +3.4%). In terms of Q1 GDP Price Index, it came in exactly as predicted at +3.1% (compared to a +3.1% forecast and the Q4 +1.7%). Elsewhere, the Preliminary May Goods Trade Balance was a bit worse than anticipated at -$100.62 billion (versus the -$96.00 billion forecast and -$99.41 billion April reading). At the same time, Preliminary May Retail Inventories were lower than April at +0.0% (compared to April’s +0.2% number). In the housing market, May Pending Home Sales well lower than predicted at -2.1% (versus a forecast of +0.6% but far, far better than April’s -7.7%). Then after the close, the Fed Balance Sheet fell significantly, down $22 billion for the week, to $7.231 trillion from the prior week’s $7.253 trillion.

In terms of Fed speak, Atlanta Fed President Bostic said Thursday that he expects one rate cut in 2024 and as many as four cuts in 2025. As all Fed speakers, Bostic hedged, saying, “There are plausible scenarios in which more cuts, no cuts, or even a raise could be appropriate. I will let the data and conditions on the ground be my guide.” At the same time, Fed Governor Bowman spoke again, continuing her recent statements that she is not ready to cut rates until data more clearly shows inflation is falling. She said, “we are still not yet at the point where it is appropriate to lower the policy rate, and I continue to see a number of upside risks to inflation.” Bowman added, “Should the incoming data indicate that inflation is moving sustainably toward our 2% goal, it will eventually become appropriate to gradually lower the federal funds rate to prevent monetary policy from becoming overly restrictive.”

After the close, NKE missed on the revenue line while beating on earnings. Both were significant with a 3% miss on revenue and a 18.8% beat on earnings. It is also worth noting that NKE also lowered forward guidance.

In stock news, on Thursday BP announced they have halted hiring and is slowing the rollout of renewable energy (offshore wind) projects in a bid to win over investors. At the same time, NYCB said it expects to do a one-for-three reverse stock split in mid-to-late July. (No specific date was announced.) Later, WMT announced it has added NKLA hydrogen fuel-celled semi-trucks to its Canadian fleet. (This comes less than two months after reported that WMT was not receiving the TSLA semi-trucks it had ordered due to production delays.) After the close, NOK announced it will acquire INFN in a $2.3 billion deal ($6.65 per share, a 26.4% premium on INFN’s Thursday close price). Meanwhile, ILMN announced it will take a $1.47 billion “goodwill” charge related to its forced spinoff of Grail. At the same time, Bloomberg reported that MSFT has begun informing its customers that a Russian state-sponsored hacking group had breached their internal systems, including emails.

In stock legal and governmental news, on Thursday the US Center for Disease Control and Prevention narrowed the recommendation for the use of RSV vaccines. GSK, PFE, and MRNA are the drug companies in that market. GSK got crushing in its home British market, falling 7%. Meanwhile, UBER and LYFT agreed to pay $175 million to settle a lawsuit over classifying drivers as contractors. (The news came shortly after the MA Supreme Court ruled that a fall vote will let voters decide whether drivers are contractors or employees.) At the same time, the FCC Chair (Rosenworcel) demanded that T, VZ, CMCCSA and other cable and telecom companies report their efforts to stop fraudulent political robocalls and other AI-generated political mis-information. Later, Federal regulators FERC voted 2-to-1 to approve a new LNG plant in LA state. The move clears the way for the private “Venture Global” to become the second largest LNG exporter in the US behind LNG (Cheniere). At the same time, the NTSB once again had to sanction BA (and said it would refer the matter to the Dept. of Justice) this time over the company’s misrepresentations and illegal release of partial undisclosed investigative information (which had tried to attribute the January 5 ALK mid-air door blowout to “lost paperwork” in an attempt to downplay company quality issues). Once again, BA responded with a meaningless public apology.

Elsewhere, the ultra-Republican Supreme Court blocked the EPA from regulating ozone emissions that may worsen air pollution in neighboring states. The ruling in favor of KMI and three GOP-led states will prohibit the EPA from regulating smog-producing ozone emissions from power plants and steel furnace operations. Later, a US Appeals Court ruled that META must face a class-action lawsuit alleging it prefers foreign workers over American citizens (because it can pay lower wages and have more docile employees when the threat of losing US residency is tied up in the employment agreement. At the same time, in a quite surprising 5-4 decision, the US Supreme Court threw out the opioid settlement with Purdue Pharmaceuticals that had been meant to resolve the bankruptcy of the company. Without specifically attacking the practice, this decision will make it harder for companies to use the “Texas Two-Step” process to avoid liability by declaring bankruptcy and making the waiver of liability part of the settlement agreement with creditors (plaintiffs). (MMM and JNJ are major companies trying to use that process now to avoid liabilities.) After the close, BAC, GS, JPM, C, MS, UBS, DB, BCS, BNPQY, and NWG settled a long-running antitrust lawsuit for rigging the $465.9 trillion interest rate swaps market. As usual, the ten banks were not forced to admit wrongdoing and will pay only $46 to $71 million.

Overnight, Asian markets were mixed with seven of the region’s 12 exchanges in the green. Shanghai (+0.73%), Japan (+0.61%), and Taiwan (+0.55%) paced the larger gainer group. Meanwhile, New Zealand (-0.99%) and Thailand (-0.65%) led the losing exchanges. In Europe, markets are much greener at midday with 11 of 15 bourses above break-even. The CAC (-0.31%), DAX (+0.62%), and FTSE (+0.59%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a modestly green start to the day. The DIA implies a +0.07% open, the SPY is implying a +0.35% open, and the QQQ implies a +0.42% open at this hour. At the same time, 10-Year bond yields are up to 4.304% and Oil (WTI) is up almost a percent to $82.51 per barrel in early trade.

The major economic news scheduled for Friday includes May Core PCE Price Index, May PCE Price Index, and May Personal Spending (all at 8:30 a.m.), June Chicago PMI (9:45 a.m.), Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations (all at 10 a.m.). We also hear from Fed Governor Bowman at noon. There are no major earnings reports scheduled for either before the open or after the close Friday.

In miscellaneous news, on Thursday it was announced that North Korea will send troops to Ukraine to support Russia within a month. Reportedly, Russia claims these troops will be engineering units that will free up more Russian troops (for their typical “meat wave” assault tactics). However, Pentagon spokesman told the press that the US expects the troops to be “cannon fodder,” meaning they expect the North Koreans to be part of combat operations. Most analysts expect this announcement to be yet another Putin gambit to get the West to self-restrict by not sending troops to train AFU (Ukraine military) troops and take over border patrol duties from Ukrainian troops.

In other news, most snap analysis of last night’s Presidential debate indicate that Biden performed poorly, reinforcing his “age problem” by not coming across as strong (in the sense of physical vigor as potentially indicated by a forceful voice). On the other side, as usual ex-President Trump lied non-stop. Fact-checkers found 30 lies or misleading statements by Trump during his share of the 90-minute event. Still, most see it as a victory for Trump.

With that background, it looks as if markets (or at least the broader indices) are starting the premarket stronger. SPY and QQQ gapped up to start the premarket and had printed small white-body candles since that start. For its part, DIA has reacted much more modestly with a slight open higher in the early session and giving us a small, indecisive, white-bodied candle since then. lower. All three major index ETFs remain above their T-line (8ema). Again, remember that despite intraday movement, all three major index ETFs are still quite near their all-time highs. So, the short-term trend is modestly bullish. However, the mid-term and especially the longer-term trend in all three major index ETFs remains very bullish. In terms of extension, none of those three are extended above their T-line and the T2122 indicator is in the center of its mid-range. Therefore, the market has plenty of room to run in either direction. With regard to those 10 big dog tickers, nine of the 10 are in the green this morning. Only GOOGL (-0.16%) is in the red early. You should also be aware that the biggest dog, NVDA (+0.91%) and the second-biggest, TSLA (+1.12%) are leading the rest of the market higher early.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Thursday’s trading session began on a subdued note as stock futures as the market’s reacted earnings reports and market-moving data anticipation. Today investors face a busy morning of earnings and economic reports. Traders are poised to assess the latest data on weekly jobless claims, durable goods orders, pending home sales figures and the latest reading on GDP.

European markets exhibited a cautious stance on Thursday. The pan-European Stoxx 600 index saw a modest decline, edging down by 0.2% as of 11:15 a.m. London time. Media stocks managed to buck the trend, gaining 0.44%, which could suggest a shift in investor focus towards more defensive sectors. On the other hand, the retail sector faced a significant pullback, dropping 1.78%, possibly due to the impact of inflationary pressures on consumer spending and sentiment.

In a significant shift in the currency market, the Japanese yen experienced a substantial depreciation, reaching a nearly 38-year low. Late Wednesday, it plummeted to 160.82 against the U.S. dollar, marking a notable milestone as reported by FactSet. Despite the yen’s weakening, Japan’s domestic economic indicators painted a more robust picture. Retail sales in May outperformed expectations, registering a 3% year-on-year growth, surpassing the anticipated 2% forecasted by a Reuters poll of economists. Meanwhile, China’s economic landscape also showed signs of strength, with industrial profits witnessing a 3.4% increase from January to May.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include AYI, APOG, LNN, MCK, SMPL, & WBA. After the bell include NKE, & ACCD.

News & Technicals’

Micron Technology, a leading chipmaker, experienced a surprising 7% drop in its share value on Wednesday, despite reporting quarterly results that surpassed expectations. This decline occurred even though the company’s revenue guidance met analysts’ estimates, suggesting that other factors may be influencing investor behavior. Over the past year, Micron’s stock has seen a remarkable surge, more than doubling in value, largely attributed to the burgeoning demand for chips in the artificial intelligence sector. This sector’s rapid growth has been a significant driver for the semiconductor industry, with Micron being one of the beneficiaries of this trend. However, the recent dip in share price indicates that even companies at the forefront of technological advancements are not immune to market volatility.

Levi Strauss, the iconic denim brand, encountered a slight setback as it narrowly missed Wall Street’s sales expectations, despite denim’s growing popularity. The company’s Chief Financial Officer expressed concerns, noting that consumers are exercising caution with their spending, particularly regarding discretionary items. This cautious consumer behavior could reflect broader economic trends or a shift in spending priorities. In response to the evolving retail landscape, Levi Strauss has been strategically reducing its dependence on department stores. The brand is expanding its direct-to-consumer channels, including enhancing its own website and brick-and-mortar stores. While this move aims to establish a more direct relationship with customers, it also presents its own set of challenges, such as increased competition in the digital space and the need for strong online user experience.

Wall Street is poised with anticipation for the release of May’s personal consumption expenditures (PCE) price index on Friday, a key indicator of inflation. Investors are hopeful that the report will reveal a softening of inflationary pressures, which could reinforce the possibility of the Federal Reserve reducing interest rates later in the year. Amidst this backdrop, there is an ongoing debate among investors regarding the sustainability of the artificial intelligence (AI) sector’s influence on market performance. As the year progresses, questions arise about whether the AI-driven market rally can maintain its momentum or if a broader range of sectors will need to contribute to market growth. According to strategists surveyed by CNBC Pro, there is a tempered expectation that the S&P 500 will conclude the year with a marginal increase, potentially less than 1% above the current levels. This forecast reflects a cautious outlook on the market’s trajectory in the face of various economic uncertainties.

As we wait with massive data anticipation, remember it doesn’t really matter what the data is, it’s the market reaction that matters. Unfortunately, being unable to see the future we must be prepared for the possibility of big point gaps and whipsaws as the market tries to price in the new information. Keep in mind we’re facing the Core PCE number Friday morning so plan for the price volatility and uncertainty to continue.

Markets started the day modestly lower. SPY gapped down 0.20%, DIA gapped down 0.23%, and QQQ started off 0.20% lower at the open. From that point, all three major index ETFs spent the rest of the day meandering sideways. Only SPY ended on a short spurt to close bear the highs. This action gave us white-bodied candles in all three as DIA printed a Spinning Top that retested and stayed above its T-line (8ema). Meanwhile, SPY and QQQ printed larger-body white candles with small upper wicks. Both of them retested their T-line from above and bounced up off to close above. This all happened on well-below average volume in all three, especially the DIA.

On the day, five of the 10 sectors were in the green with Consumer Cyclicals (+0.63%) leading the gainers higher. Meanwhile, Utilities (-0.43%) and Financial Services (-0.41%) led the laggard sectors lower. At the same time, SPY gained 0.12%, DIA gained 0.06%, and QQQ gained 0.21%. VXX fell another 1.09% to close at 10.88 and T2122 gained a bit but remains in the lower half of its mid-range at 34.04. On the bond front, 10-year bond yields spiked to 4.325% and Oil (WTI) fell slightly (-0.21%) to close at $80.66 per barrel. So, Wednesday was another “wait and see” day where markets basically treaded water while waiting on GDP or the Presidential Debate (or more likely PCE data on Friday).

The major economic news scheduled for Wednesday included Building Permits, which came in a bit higher than expected at 1.399 million (compared to a forecast of 1.386 million but below the last 1.440 million reading). Later, May New Home Sales were lower than predicted at 619k (versus the 636k forecast and well down from the April 698k value). Then the EIA Weekly Crude Oil Inventories showed an unexpected large inventory build of 3.591 million barrels (compared to a forecasted drawdown of 2.600 million barrels and the prior week’s 2.547-million-barrel drawdown).

Then after the close, the results of the Annual Fed Bank Stress Tests were announced. The Fed said that all 31 banks passed the tests, even withstanding a hypothetical severe economic downturn. However, the banks tested this year showed that they would have larger (but still sustainable) losses under this year’s scenarios than the very similar 2023 scenarios. The Fed announcement said the largest banks would see 9.9% dips in “high-quality capital” at the worst point of this year’s harshest scenario.

Also after the close, CNXC, FUL, JEF, MU, and WS all reported beats on both the revenue and earnings lines. Meanwhile, LEVI and MLKN both missed on revenue while beating on earnings. BB is of special note. BB had a massive miss on revenue but still beat (by 175%) on the earnings line.

In stock news, on Wednesday, AIG sold its travel insurance unit to ZURVY (Zurich Insurance) for $600 million. Later, Reuters reported (exclusively) that German firm Robert Bosch is considering a takeover bid for WHR according to three sources. (WHR was up 17.10% on the day on this report.) Meanwhile, Bloomberg reported that B is exploring “strategic alternatives” including a sale of the company. (B stocks was up 7.63% on the news.) During the day, AMZN passed the $2 trillion valuation mark, becoming just the fifth company to do so. (Analysts attribute the climb to AI mania, but that does not really explain Wednesday’s 3.91% gain to a level not far above the May and April highs.) After the close, Reuters reported that CG and KKR have won the auction to acquire the $10 billion student loan portfolio from DFS.

In stock legal and governmental news, on Wednesday, the NYSE denied the claims of IBKR, which resulted in the brokerage losing $48 million. (IBKR had tried to get NYSE to pay for trade executions IBKR made when BRKA dropped from $622k/share to $185/share on June 3, prior to the BRKA stock being halted due to erroneous data. At the same time, the NHTSA announced that TM is recalling 145k vehicles over side curtain air bad issues. Later, the US Dept. of Commerce awarded a $75 million grant to ENTG as part of the Chips Act program. (The money will go toward development of a new ENTG facility in CO. At the same time, the NHTSA announced that VLKAF (Volkswagen) is recalling 307k vehicles in North America over an airbag sensor wiring problem. Later, Bloomberg reported that VLVLY (Volvo) will delay shipments of its EX30 electric vehicle due to the higher tariffs the US has imposed on Chinese imports. As a result, VLVLY won’t deliver these cars until 2025 (previously scheduled for late summer to early fall). Eventually, Volvo will begin producing the cars in Belgium during 2025, which will allow it to avoid the higher tariffs by shipping to the US from that location instead of the China plant. After the close, MO filed a request to the FDA to authorize it to sell nicotine pouch products in the US. Also after the close, Republican state AGs refused to accept any increase in NHTSA CAFÉ (mileage) standards on car makers. The Biden administration’s watered-down 2% per year increase (only starting in 2026) has “forced” those state AGs to file suit against the NHTSA for exceeding its regulatory authority.

Overnight, Asian markets leaned heavily to the red side. Hong Kong (-2.06%) and Shenzhen (-1.53%) were way out in front pacing the losses. Meanwhile only India (+0.74%) and Singapore (+0.35%) were in the green in the region. In Europe, the picture is more mixed but still leans to the red side at midday. The CAC (-0.67%), DAX (+0.07%), and FTSE (-0.31%) lead the region on volume. However, Russia (+1.39%) is the biggest European mover in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a down start to the day. The DIA implies a -0.21% open, the SPY is implying a -0.18% open, and the QQQ implies a -0.22% open at this hour. At the same time, 10-Year bond yields are up to 4.329% and Oil (WTI) is up a third of a percent to $81.19 per barrel in early trade.

The major economic news scheduled for Thursday include Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, May Core Durable Goods, May Durable Goods, Q1 Core PCE Prices, Q1 GDP, Q1 GDP Price Index, May Goods Trade Balance, and May Retail Inventories (all at 8:30 a.m.), and May Pending Home Sales (10 a.m.). The major earnings reports scheduled for before the open include AYI, MKC, and WBA. Then after the close, NKE reports.

In economic news later this week, on Friday, May Core PCE Price Index, May PCE Price Index, May Personal Spending, Jun Chicago PMI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations are reported. We also hear from Fed Governor Bowman.

In terms of earnings reports later this week, on Friday, there are no earnings reports scheduled.

In miscellaneous news, on Wednesday, the US Dollar hit a 38-year high against the Yen. (Speculation continued to ramp that the Bank of Japan will intervene to make the Yen stronger soon as BoJ currency chief Kanda said they were “seriously concerned and on high alert”.) Elsewhere, Reuters reported that the SEC could well approve ETFs based on the spot price of ether cryptocurrency to begin trading as soon as after the July 4 holiday.

So far this morning, MKC reported beats on both the revenue and earnings lines. At the same time, AYI missed on revenue while beating on earnings. On the other side, WBA beat on revenue while missing on earnings. IT is worth noting that WBA also lowered its forward guidance.

With that background, it looks as if markets are starting the premarket modestly lower. All three major index ETFs have retested their T-lines again in the early session and so far all have remains above that 8ema on small white-bodied candles. However, those candles are indecisive and did start off from a modest gap down in the early session. Again, remember that despite intraday movement, all three major index ETFs are still quite near their all-time highs. So, the short-term trend is mixed. However, the mid-term and especially the longer-term trend in all three major index ETFs remains very bullish. In terms of extension, none of those three are extended above their T-line and the T2122 indicator is still in its mid-range. Therefore, the market still has room to run in either direction. With regard to those 10 big dog tickers, eight of the 10 are in the red this morning. Only AAPL (+0.37%) and AMZN (+0.30%) are in the green early. You should also be aware that the biggest dog, NVDA (-1.65%) is the biggest mover and biggest loser of the group this morning, acting as an anchor on the rest of the market.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The stock market displays some optimism on Wednesday morning, with futures pointing upwards, after the tech giants reverse and the AI hype returns. Investors and analysts alike are now turning their gaze towards the upcoming release of May’s personal consumption expenditures price index on Friday, a key indicator of inflationary trends. Additionally, the traders anticipate earnings from General Mills and Paychex, scheduled for Wednesday morning, while Micron Technology is set to report its earnings later in the day. These events are poised to provide further insights into the economic landscape and potentially influence market trajectories.

European markets experienced a rebound on Wednesday, with stocks climbing and shaking off the pessimism from the previous session’s downturn. However, economic indicators suggest caution; German consumer sentiment is projected to decline in July, halting a four-month streak of gains. Concurrently, French consumer confidence dipped to 89 in June, as reported by the country’s national statistics office.

Australia was lower on the day as the headline inflation rate increased, reaching 4%, a notable rise from April’s 3.6%. However, industry giants like Taiwan Semiconductor Manufacturing Company, SK Hynix, and MediaTek also saw their shares climb by 1.38%, 4%, and 3.25% respectively. These gains underscore the robust demand for semiconductor technology, which is a critical component in a wide array of consumer and industrial products, amidst a challenging inflationary environment.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include GIS, PAYX & UNF. After the bell include MU, AVAV, CNXC, FUL, LEVI, MLKN, & WD.

News & Technicals’

FedEx’s stock experienced a remarkable surge, climbing over 15% after the market closed on Tuesday, following the announcement of their fiscal fourth-quarter results. The company not only exceeded analysts’ expectations in terms of earnings and revenue but also highlighted its ongoing $4 billion cost-cutting initiative, which includes merging its air and ground operations. This strategic move is aimed at streamlining processes and improving efficiency. The positive financial report, coupled with a reduction in capital expenditure, reflects FedEx’s commitment to optimizing its business model and strengthening its market position amidst challenging economic conditions. The after-hours leap in share price is a testament to investor confidence in FedEx’s restructuring efforts and future prospects.

Volkswagen’s strategic move to invest up to $5 billion in the electric vehicle startup Rivian marks a significant shift in the automotive industry’s transition towards sustainable transportation. The initial commitment of $1 billion underscores the confidence Volkswagen has in Rivian’s potential to disrupt the market. The subsequent investment of $4 billion, contingent upon the successful formation of a joint venture, reflects a long-term vision for collaboration and innovation. However, despite this substantial financial backing, Rivian’s stock performance has been underwhelming, with a decline of approximately 49% in 2024. This juxtaposition of robust corporate support against market skepticism highlights the volatile nature of the EV sector and the challenges that new entrants like Rivian face in a rapidly evolving market landscape.

Ooredoo’s recent partnership with Nvidia represents a landmark development for technology in the Middle East. This collaboration, Nvidia’s first significant foray into the region, involves the deployment of thousands of Nvidia’s GPUs across 26 data centers spanning Qatar and five other countries: Kuwait, Oman, Algeria, Tunisia, and the Maldives. While the financial details remain undisclosed, the strategic implications are clear. These powerful GPUs will be instrumental in processing vast quantities of data, fueling AI chatbots and various tools that are crucial to the AI infrastructure of these nations. This move not only enhances Ooredoo’s data capabilities but also signifies the growing importance of AI technology in global telecommunications and the pivotal role of the Middle East in the tech industry’s future.

The QQQ celebrated on Tuesday as the tech giants reverse lead by the AI darling NVDA. Unfortunately, the DIA and IWM also reversed as the rush back into tech reversed taking way the nice gains of Monday. I suspect the price volatility will continue as the market focus will soon turn to the looming market-moving data coming Thursday and Friday. Plan your risk accordingly.

Tuesday saw SPY and QQQ open higher and DIA opened down slightly. SPY gapped up 0.23%, QQQ gapped up 0.446%, and DIA opened 0.12% lower. From that point, the three major index ETFs diverged. SPY spent the day grinding sideways. At the same time, QQQ rallied modestly all day, closing near the highs. However, DIA sold off with more vigor than the other two until 12:50 p.m. before grinding sideways near the lows the rest of the day. This action gave us a white-bodied Spinning Top that retested and crossed above its T-line (8ema) again. The QQQ gave us a gap-up, white-bodied candle the crossed back up above its T-line. Meanwhile, DIA printed a gap-down, black-bodied candle that retested (from above) and closed still just above its T-line.

On the day, nine of the 10 sectors were in the red with Industrials (-0.84%) and Utilities (-0.83%) out front leading the red sectors lower. Meanwhile, Technology (+1.30%) was the biggest mover and only gainer. At the same time, SPY gained 0.37%, DIA lost 0.75%, and QQQ gained 1.14%. VXX fell another 1.79% to close at 11.00 and T2122 dropped back to the bottom of its mid-range, just outside oversold territory at 22.50. On the bond front, 10-year bond yields fell to 4.224% and Oil (WTI) fell 1.02% to close at $80.80 per barrel. So, Tuesday saw the long-time leading index ETFs perhaps putting in a bottom to their pullback while the DIA might have started its own pullback after a six-day rally. It is also worth noting that NVDA (+6.76%) broke its 3-day selloff to again lead tech names and the second most-traded name, TSLA, also gained 2.61%. This put us back in the pattern the market has seen for months.

The major economic news scheduled for Tuesday was limited. It included the June Conference Board Consumer Confidence Index, which came in above expectation at 100.4 (compared to a 100.0 forecast but down from May’s 101.3). Then, after the close, the API Weekly Crude Oil Stocks, which showed an unexpected inventory build of 0.914 million barrels (versus a forecasted drawdown of 3.000 million barrels but lower than the prior week’s 2.264-million-barrel inventory build).

In terms of Fed speak, Fed Governor Bowman indicated she felt it is appropriate to hold rate policy steady (no hike or cut) for some time. Very early Tuesday she did this by outlining scenarios or threats for both a hike or cut. She said, “I have not written in further rate cuts in my statement of economic projections for the bulk of this year.” She went on to say that she is open to a rate hike if inflation does not pull back further, but that is inflation is moving toward the 2% goal “it will eventually become appropriate to lower the federal funds rate.” Later, Fed Governor Cook told the Economic Club of NY that the Fed is back on track for a rate cut…when the economy meets her expectation. Specifically, Cook said, “With significant progress on inflation and the labor market cooling gradually, at some point it will be appropriate to reduce the level of policy restriction to maintain a healthy balance in the economy.” (This seemed to be a bit more dovish than Bowman, although both Governors hedge their statements.)

After the close, FDX missed slightly on the revenue line while beating on the earnings line. At the same time, WOR missed by quite a bit on both the top and bottom lines. However, FDX raised forward guidance and post-market trading reacted positively.

In stock news, on Tuesday Reuters reported that BA and EADSY (Airbus) are near a deal to carve up their supplier SPR. Reportedly, EADSY will take the SPR plant in Kinston, NC as well as the plant in Northern Ireland. The remainder of the company would go to BA. Later, XOM told Reuters it may need to suspend operations at its refinery in Northern France if strikers continue to block access to the plant. (That plant produces 20% of the refining capacity for all of France.) In fighting the union demands, XOM said that refinery has lost more than $535 million over the last 5.5 years. At the same time, Bloomberg reported that takeover talks between DASH and its London-based rival Deliveroo have stalled. (The two sides had far different valuations for the Deliveroo company.) After the close, RIVN shares spiked more than 60% after VLKAF (Volkswagen) announced a $5 billion investment (by 2026) in RIVN as well as a joint venture with the EV carmaker.

In stock legal and governmental news, on Tuesday, the NHTSA announced that F will recall 668k F-150 pickup trucks over a transmission issue. At the same time, TSLA announced another recall of its Cybertrucks, this time requiring physical (not software) updates. The cause of this recall is wiper and trim defects in 11,000 vehicles. Later, VZ agreed to pay a $1 million fine over repeated 911 outages in six states during 2022. At the same time, a US District Judge rejected a $30 billion antitrust settlement where V and MA agreed to limit the fees they charge merchants. (The objecting majority of merchants who had opposed the settlement allege that the fees remain too high for the service being provided by V and MA.) After the close, the NTSB charged NSC for its venting and burning of hazardous materials after the February 2023 train derailment in East Palestine OH. (Last month NSC agreed to a $15 million penalty and $57.1 million in reimbursement for government cleanup costs to resolve a US lawsuit on the event.) Also after the close, firefighters in the state of CT sued DD, MMM, and HON over protective “turnout gear” that was contaminated with forever chemicals (PFAS). (Last year the three companies reached an $11 billion settlement over the same chemicals being in firefighting foam and other products that then polluted drinking water supplies.)

Overnight, Asian markets were green across the board with the lone exception of Australia (-0.71%). Meanwhile, Shenzhen (+1.55%), Japan (+1.26%), and New Zealand (+1.01%) led the region higher. In Europe, markets are mixed but lean toward the red side at midday. The CAC (-0.56%), DAX (+0.11%), and FTSE (+0.01%) lead the region lower while Russia (+1.39%) is an outlier to the upside in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mixed, flat start to the day. The DIA implies a -0.21% open, the SPY is implying a -0.03% open, but the QQQ implies a +0.12% open at this hour. At the same time, 10-Year Bond yields are up to 4.283% and Oil (WTI) is up two-thirds of a percent to $81.36 per barrel in early trading.

The major economic news scheduled for Wednesday includes Building Permits (8:30 a.m.), May New Home Sales (10 a.m.), EIA Crude Oil Inventories (10:30 a.m.), and the Fed Bank Stress Test Results (4:30 p.m.). The major earnings reports scheduled for before the open include GIS, PAYX, and UNF. Then after the close, BB, CNXC, FUL, JEF, LEVI, MU, MLKN, and WS report.

In economic news later this week, on Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, May Core Durable Goods, May Durable Goods, Q1 Core PCE Prices, Q1 GDP, Q! GDP Price Index, May Goods Trade Balance, May Retail Inventories, and May Pending Home Sales. Finally, on Friday, May Core PCE Price Index, May PCE Price Index, May Personal Spending, Jun Chicago PMI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations are reported. We also hear from Fed Governor Bowman.

In terms of earnings reports later this week, on Thursday, AYI, MKC, WBA, and NKE report. Finally, on Friday, there are no earnings reports scheduled.

In miscellaneous news, on Tuesday, Reuters reported that the state of DE is close to approving a new law that will drastically change corporate governance for companies incorporated in that state. The law would allow corporations to enter into contracts giving specific shareholders outsized power over board decisions. For example, in February a DE Court invalidated an agreement that had given one shareholder (the founder) veto power over all board decisions of MC. Under the new law, that contract would stand. Elsewhere, after the close, Reuters reported an internal memo obtained from CDK Global (software) indicates the company does not expect to recover from the outage caused by hacker attacks before the end of the month. (That CDK software powers the internal operations of 15,000 car dealers and service centers in the US and Canada. As a result of the outage, those businesses are operating on paper without visibility into parts inventories, online ordering of parts, insurance pricing, or buyer vetting.) Finally, the Equipment Leasing and Finance Assn. (ELFA) announced that May business equipment financing borrowing increased 11% in May versus the same month in 2023. However, this was down 7% from April 2024. ELFA speculated that businesses are holding off on equipment spending until interest rates drop.

So far this morning, GIS reported a miss on the revenue line while beating on earnings.

With that background, it looks as if markets are indecisive this morning, perhaps waiting on data later in the week. All three major index ETFs opened the premarket slightly higher, but have printed small, black-bodied candles since then with varying degrees of pullback. SPY and QQQ both remain above their T-line (8ema) while DIA is retesting its own T-line from above in the early session. Before you get caught up in the tick-level movements, just bear in mind that all three major index ETFs are still quite near their all-time highs. So, the short-term trend is mixed. However, the mid-term and especially the longer-term trend in all three major index ETFs remains very bullish. In terms of extension, none of those three are extended above their T-line and the T2122 indicator is still in its mid-range (albeit the very bottom of that mid-range). Therefore, the market still has room to run in either direction. With regard to those 10 big dog tickers, six of the 10 are in the red this morning. However, that biggest dog, NVDA (+2.48%) continues its Tuesday bounce-back and will do much to pull other indexes (and the whole market) higher.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets diverged Monday, even on broadly sideways action. The SPY opened 0.06% higher, DIA gapped up 0.30%, and QQQ gapped down 0.39%. From there, SPY and QQQ put in slow selloffs (QQQ faster than SPY) that both hit a crescendo the last 30 minutes of the day and closed on their lows. For its part, DIA rallied sharply after the open until 11 a.m. From that point, DIA followed the slow selloff (even slower than SPY) until 1:30 p.m. and then moved sideways the rest of the day. This action gave us a black-bodied Inverted Hammer that crossed below its T-line (8ema) in the SPY. QQQ printed a large-bodied, black candle with upper wick that also crossed below its T-line. However, DIA gave us a gap-up, white-bodied candle with an upper wick. This all happened on slightly less-than-average volume in the QQQ and DIA with SPY having volume that was well-below-average.

On the day, nine of the 10 sectors were in the green with Energy (+2.42%) way out in front (by 1.1%) leading the other eight green sectors higher. Meanwhile, Technology (-1.24%) was the worst-performing sector by more than 1.25%. At the same time, SPY lost 0.34%, DIA gained 0.66%, and QQQ lost 1.30% as money rotated out of the tech names. VXX fell 0.80% to close at 11.20 and T2122 moved up to the high-end of its mid-range at 69.59. On the bond front, 10-year bond yields fell to 4.23% and Oil (WTI) popped 1.16% to close at $81.67 per barrel. So, Monday was a rotation day with money fleeing technology (NVDA was down 6.68% on $54 billion in stock traded) and seeking safety in the big oil (XOM +2.97%, CVX +2.60%, and COP +3.44%) and financial names (JPM +1.21%, BRKB +1.06%, BAC +1.34%). It is worth noting that NVDA, which has been the driving engine of the market for months, has been down almost 13% over the last three trading sessions.

There was no major economic news scheduled for Monday.

In terms of Fed speak, Cleveland Fed President Mester (retires next week) said she believe the Fed needs to remain open to selling more of its mortgage-backed securities as part of reducing the Fed Balance Sheet. However, she said that she doesn’t think this will happen soon. Mester said, “I don’t think it’s immediate that we should be selling MBS.” Later, Chicago Fed President Goolsbee told CNBC that while inflation is (slightly) cooling, he is looking for more confirmation before a rate cut. Goolsbee said he is a closet optimist but that the Fed need to get “a little bit more confidence on the inflation side.” He said, “If unemployment claims are going up (the unemployment rate is inching up) many of the other measures have cooled down to something like what they were before the pandemic and you start to see weakness on consumer spending.” If this comes to pass Goolsbee said the Fed will need to start thinking about balancing both sides (inflation and employment) rather than focusing on just inflation. Meanwhile, San Francisco Fed President Daly told an audience that inflation is not the only risk. She said, “We must continue the work of fully restoring price stability without a painful disruption to the economy.” She continued, saying the Fed must “exhibit care” … (while there is still) “more work to do” (on bringing inflation down) … “inflation is not the only risk we face.”

After the close, there were no noteworthy earnings reports.

In stock news, on Monday, UPS sold its Coyote Logistics unit to RXO for $1.025 billion (UPS bought the company for $1.8 billion in 2015). Later, NVO announced it will spend $4.1 billion to build a new manufacturing plant in NC to boost production of its highly-profitable weight loss drug Wegovy. At the same time, PARA announced it will raise the price of its streaming services in late summer. Later, BA announced its troubled Starliner has again delayed its return to earth. The first manned flight of Starliner is stuck, docked to the International Space Station after having rescheduled its undocking three times now. (Current plans are for a July 6 attempt to return to earth, which, if hit, would mean the 8-day mission had been forced to last a month.) After the close, Bloomberg reported that contrary to earlier rumors, AAPL and META are not in talks about forming an AI partnership.

In stock legal and governmental news, on Monday the 9th Circuit Court of Appeals threw out a proposed class-action suit against UBER which alleged the company process for terminating low-rated drivers was racially discriminatory. (Evidence had not been presented showing the company terminated a higher percentage of non-white drivers. However, without discovery, the plaintiffs argued they could not get such data.) Later, the CEO Stankey of T, asked that Congress give the FCC power (and a mandate) to require big tech firms like META and GOOGL to pay into a fund to be used to subsidize access to broadband services. At the same time, family members of BA 737 MAX crash victims asked a US District Judge to appoint a corporate monitor to examine BA safety and corporate compliance procedures. The request comes after the group had accused BA of reneging on the promises the company gave in 2021 to avoid prosecution related to the two crashes in 2018 and 2019. Later, PacifiCorp (owned by BRKB) settled with 378 plaintiffs for $150 million related to the 2020 fires caused by the utility’s electric equipment. This settlement resolves nearly all individual claims, but many corporate and government claims remain unsolved. The US has also threatened to sue PacifiCorp for failure to pay $356 million in costs and damages for the single “Slater” fire. (This brings the company’s total settlements to over $1 billion for those fires.)

Overnight, Asian markets were mostly green. Australia (+1/36%), Japan (+0.95%), and India (+0.78%) led the region higher. In Europe, stocks are mostly lower at midday. The CAC (-0.66%), DAX (-0.88%), and FTSE (-0.19%) lead the region lower in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a mixed but positive start to the day. The DIA implies a -0.12% open, the SPY is implying a +0.17% open, and the QQQ implies a +0.41% open at this hour. At the same time, 10-year bond yields are down to 4.224% and Oil (WTI) is off 0.65% to $81.10 per barrel in early trading.

The major economic news scheduled for Tuesday is limited to Conference Board Consumer Confidence and API Weekly Crude Oil Stocks. We also hear from Fed Governor Bowman twice. The major earnings reports scheduled for before the open include CCL and SNX. Then after the close, FDX and WOR report.

In terms of earnings reports later this week, on Wednesday, we hear from GIS, PAYX, UNF, BB, CNXC, FUL, JEF, LEVI, MU, MLKN, and WS. On Thursday, AYI, MKC, WBA, and NKE report. Finally, on Friday, there are no earnings reports scheduled.

In miscellaneous news, on Monday Bloomberg reported 2023 saw record contributions to 401(k) accounts again as in 2022. The average percent of salary deposited into the 4012(k)s stayed the same at 11.7%, but average salaries increased more than had been seen in quite a while. Elsewhere, the San Jose Mercury News reported Monday that for the first time, utilities (especially electric companies) across CA and broader in the West, enter peak summer wildfire season without insurance. Similar to the ways that hurricanes have made insurance companies stop serving FL, TX, and other disaster-prone regions, wildfires have caused insurance companies to raise rates to untenable levels or abandon insuring major utilities altogether. As a result, the utilities are self-insuring this fire season in what amounts to a gamble of tens or hundreds of millions of dollars. Finally, Reuters reported that the TSA screened an all-time record of 2.99 million passengers Sunday. This was the highest number of passengers ever screened on a single day.

In late-breaking news, the EU Antitrust Commission charged MSFT with “abusive bundling” of its Office and Teams applications. (Teams is just a business version of Skype.) In 2023, MSFT unbundled the two from their subscription “365” service in a bid to head off these charges. However, the EU called the move “insufficient” due to the already accomplished integration and Office’s massive market share. Elsewhere, Fed Governor Bowman (a long-time Hawk) told a London audience that she was open to raising rates if inflation does not pull back further. However, she also hedged her bets by saying, “Should the incoming data indicate that inflation is moving sustainably toward our 2 percent goal, it will eventually become appropriate to gradually lower the federal funds rate…”

With that background, it looks as if markets are indecisive but leaning bullish so far this morning. SPY and QQQ are both retesting their T-line (8ema) from below. Meanwhile, DIA is printing a gap-up, black-bodied candle in the premarket such that it is back below Monday’s close. Just continue to bear in mind that all three major index ETFs are still close to their all-time highs. So, the short-term trend is mixed. At the same time, the mid-term remains bullish in all three major index ETFs and the longer-term market remains very Bullish in trend. In terms of extension, none of those three are extended above their T-line and the T2122 indicator is in the upper-end of its mid-range. Therefore, the market still has room to run in either direction. With regard to those 10 big dog tickers, eight of the 10 are in the green again this morning. Only META (-0.16%) and MSFT (-0.10%) are in the red so far in the early session.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Tuesday, stock futures suggested a mixed open, after a sharp NVDA selloff that blead over to other technology stocks. The result was the most substantial single-day decline of the Nasdaq Composite’s since April. However, shares of Nvidia rebounded, climbing over 3% in overnight price action. This uptick comes on the heels of a previous session where Nvidia’s stock tumbled more than 6%, marking its sharpest drop since April 19, when it plummeted by 10%. The broader semiconductor sector also felt the heat, with companies like Super Micro Computer, Qualcomm, and Broadcom experiencing downward pressure on their stock prices.

European markets faced a downturn on Tuesday, mirroring the negative shift in U.S. market sentiment that marked the beginning of the week. The pan-European Stoxx 600 index, a key benchmark for regional equity performance, was particularly impacted during morning trading hours. The decline was led by the tech and industrial sectors, which saw significant selloffs

In the recent trading session, Japan’s Topix index surged, hitting its highest point in three weeks. Meanwhile, South Korea’s Kosdaq, primarily composed of small-cap stocks, rebounded, ending a three-day losing streak. Contrasting these gains, Mainland China’s CSI 300 experienced a decline, dropping by 0.54% to 3,457.90, marking its lowest level in four months. This downturn for the CSI 300 represents its weakest close since February 28. Despite this, the broader Asia-Pacific markets exhibited an upward trend.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include SNX. After the bell include FDX, PRGS, & WOR.

News & Technicals’