Inflation Report

U.S. stock futures edged slightly lower early Thursday, with a cautious stance as traders as braced for the inflation report. The high anticipation centers around the June consumer price index and the ramifications it will have on future interest rate decisions. Economists polled by Dow Jones have set their expectations for a modest increase of 0.1% month-over-month. On an annual basis, the CPI is projected to rise by 3.1% compared to the same period last year.

European markets rallied Thursday morning, with indices across the region climbing as investors anticipate the forthcoming U.S. inflation data. The upbeat mood was bolstered by flash figures indicating that the U.K. economy expanded by 0.4% in May, a welcome recovery following a stagnant April and surpassing the modest 0.2% growth anticipated by analysts. This economic uptick was mirrored in the currency market, where the British pound appreciated by 0.21%, reaching its highest valuation against the U.S. dollar in the past four months.

The Japanese market saw significant gains, with the Nikkei 225 index climbing 0.94% to close at 42,224.02. This surge was largely attributed to a strong performance by technology stocks. Similarly, the broader Topix index also rallied, rising 0.69% to reach a new peak of 2,929.17. South Korea, the Kospi index increased by 0.75%, as the Bank of Korea maintained its interest rate at 3.5%. The tech-centric Kosdaq index modestly rose by 0.11%.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include DAL, & PEP. After the bell we have no notable reports.

News & Technicals’

PepsiCo’s financial performance in the second quarter presented a mixed picture, as the company fell short of Wall Street’s revenue expectations. This shortfall was primarily due to a decrease in volume across its three North American business units. In light of these results, PepsiCo has adopted a more conservative stance regarding its sales forecast for the entire year, signaling a cautious approach amid uncertain market conditions. Despite the revenue setback, the company managed to surpass earnings estimates for the quarter, indicating that while sales volume may have declined, profitability metrics and cost management strategies could have yielded better-than-expected outcomes. This divergence between revenue and earnings highlights the complex challenges and operational efficiencies within PepsiCo’s business operations.

The U.S. Treasury Department and the Internal Revenue Service (IRS) have reported a significant milestone in tax collection efforts, having recovered over $1 billion in tax debt from high-income individuals in the past year. This achievement underscores the government’s intensified focus on ensuring tax compliance among the wealthy. In a strategic move to bolster these efforts, the IRS announced in September its intention to heighten scrutiny on individuals earning in excess of $1 million per year who have substantial tax debts exceeding $250,000. This initiative represents a concerted push to enhance the integrity of the tax system and address the tax gap by targeting those with the highest earning brackets and significant outstanding tax obligations. The announcement serves as a reminder of the IRS’s commitment to fair tax enforcement and the importance of compliance with tax laws.

In a landmark decision, EU antitrust regulators have endorsed a set of commitments from Apple, marking a significant shift in the tech giant’s approach to its contactless payment technology. This development paves the way for competitors to access Apple’s tap and go payment system, potentially altering the landscape of digital payments in Europe. EU antitrust chief Margrethe Vestager highlighted the move as a pivotal change that promises to enhance competition and consumer choice. This announcement follows the European Commission’s initiation of an antitrust probe concerning Apple Pay back in 2020, reflecting the EU’s ongoing efforts to ensure fair competition in the digital market. The acceptance of these commitments by Apple indicates a willingness to comply with regulatory standards and could set a precedent for other tech companies operating within the EU.

The highly anticipated inflation report and the jobless claims with likely set the tenor for today’s trading. Will the reaction follow-though with the bullish surge the ended the Wednesday session or, will the bears find reason to whipsaw the indexes back down? Buckle up we will soon find out so plan your risk carefully.

Trade Wisely,

Doug

June CPI Today Following Another All-Time High

Wednesday was a bullish freight train and the Bears were tied to the track. The SPY gapped up 0.23%, DIA opened flat, and QQQ gapped up 0.42%. From there, all three major index ETFs ground sideways in a very tight range for 90 minutes. However, then the fuse was lit and all three rallied steadily for the rest of the day. They all went parabolic the last half hour with only five minutes of profit taking at the end keeping all three from ending on their highs. This action gave us large white-bodied candles with smaller wicks on both ends across the board. SPY and QQQ once again printed new all-time highs and gave us new all-time high closes (the 37th of the year). Meanwhile, after a successful retest of its T-line (8ema) the DIA rallied to break out of its trading range dating back to May and closed less than a percent from its own all-time high. This happened on below average volume in SPY and QQQ as well as above-average volume in DIA.

On the day, all 10 sectors were in the green with Basic Materials (+1.51%) way out front leading the rest of the market higher. Even the laggards, Consumer Cyclicals (+0.61%), Energy (+0.62%), and Consumer Defensive (+0.64%) were up significantly. At the same time, SPY gained 0.99%, DIA gained 1.08%, and QQQ gained 1.04%. VXX fell just a tad and remains extremely low at 10.27. Meanwhile, T2122 spiked up to the top half of its mid-range at 69.68. On the bond front, 10-year bond yields were down a bit to 4.281% and Oil (WTI) gained 1.24% to close at $82.42 per barrel. So, Wednesday was a bullish day in a strong bullish trend. SPY and QQQ have closed at a new all-time high close each of the last five sessions, led by the Tech Big Dogs like NVDA (+2.70%), AMD (+3.87%), and AAPL (+1.88%). In fact, the only one of the 10 Tech Big Dogs that was down was NFLX (-1.18%) and it only traded $1.8 billion in stock on the day. So, if traders were waiting on CPI data…they have a funny way of showing it.

The major economic news scheduled for Wednesday were limited to EIA Weekly Crude Oil Inventories, which showed a much larger drawdown than expected at -3.443 million barrels (compared to a forecasted build of 0.700-million-barrels but far less than the prior week’s -12.157 million barrels).

In economic speak news, on Wednesday, Fed Chair Powell testified again, this time in front of the House. Powell said the Fed does not need to reach the 2% target figure prior to cutting rates. In addition, he said the Fed will cut rates “when and as needed,” regardless of the election. Powell said, “Our undertaking is to make decisions when and as they need to be made, based on the data, the incoming data, the evolving outlook and the balance of risks, and not in consideration of other factors, and that would include political factors.” (For the second day in a row, GOP lawmakers pressed (begged?) Powell not to announce any rate cuts until after the November 5 election.) When asked about the path of inflation, Powell indicated he did have some confidence that inflation is headed back below 2%. However, when asked if the bar for a rate cut had been cleared, Powell said “”I am not ready to say that yet.” He continued, “There is a path to getting back to full price stability while keeping the unemployment rate low, … We’re on it. We’re very focused on staying on that path.”

After the close, PSMT and WDFC reported beats on both the revenue and earnings lines.

In stock news, on Wednesday, WBD announced its CNN unit will cut 100 jobs (2.8% of its workforce) and also launch a new CNN.com subscription service later this year. At the same time, INTU announced plans to layoff 1,800 employees (10% of workforce) in cost-cutting moves, citing that AI is transforming the company. Later, HON announced they have signed a deal to buy APD’s LNG pretreatment unit for $1.81 billion. At the same time, AMD announced they have agreed to buy Silo AI (private) for $665 million. Later, TLSA raised the prices of its Model 3 in Europe by about $1.622 after the EU imposed tariffs on EVs made in China. (The Model 3 is made in China.) Meanwhile, Bloomberg reported that GOOGL has walked away from its pursuit of purchasing HUBS. Later, Bloomberg reported that AAPL is expecting 10% growth in iPhone sales compared to 2023 according to internal sources it cited. (However, 2023 was a down year for iPhone shipments.) At the same time, the Athletic reported that AMZN. CMCSA, and DIS have finalized a $76 billion deal to broadcast NBA basketball games for 11 seasons. (However, the report said current NBA partner WBD still has the option to match the deal.) After the close, COST announced it will hike membership fees starting in the fall. Elsewhere, MSFT announced it will drop its “observer seat” on the OpenAI board to head off antitrust inquiries in the US and UK. AAPL followed MSFT’s lead giving up its own newly-acquired “board observer” seat.

In stock legal and governmental news, on Wednesday the NHTSA announced that STLA is recalling 332k 2017-2025 Alfa Romeo, Jeep, and Fiat vehicles in the US over faulty seatbelt sensors. At the same time, the same agency announced BMWYY was recalling 394k vehicles in the US due to faulty airbag inflators. Later, HE stock spiked on a report saying that a “massive settlement” related to the Maui wildfires could be unveiled as soon as next week. No other details were released, but 451 lawsuits (covering 1,800 individual plaintiffs as well as 425 business entity plaintiffs) related to those wildfires are in the courts now. At the same time, MSFT completed a $21.7 million deal to settle cloud licensing practices to avoid EU antitrust action. (The deal was with the main complainant to the EU about those practices.) GOOGL announced it will explore other options to fight MSFT cloud licensing practices after the settlement. Later, JBLU asked the Dept. of Transportation to disqualify the UAL proposal from winning one of the five new round-trip flight slots up for bid from Washington Reagan airport.

Elsewhere, a federal judge in CA dismissed most of the FCBN $1 billion lawsuit against HSBC for “poaching” 40 employees after the collapse of Silicon Valley Bank in March of 2023. Later, the CEO of BA was hauled before the NTSB and forced to apologize for violating its NTSB rules. After the apology, the BA CEO refused other comment. At the same time, NSC agreed to implement the series of safety recommendations made by the NTSB following the February 2023 train derailment in East Palestine OH. Later, the FTC announced plans to sue UNH, ESRX, and CVS over their negotiating practices (collusion) on drugs including insulin following a two-year investigation. After the close, the former CEO of WORX was convicted of securities fraud related to statements about the company becoming the major supplier of rapid COVID-19 tests, despite knowing the claims were untrue. At the same time, the Fed and Office of the Comptroller fined C $136 million after the bank was found to have made insufficient progress addressing data management issues. (The bank was fined $400 million in 2020 for the same deficiencies.)

Overnight, Asian markets were nearly green across the board. Only India (-0.03%) was below break-even. Meanwhile Hong Kong (+2.06%), Shenzhen (+1.99%), and Taiwan (+1.60%) led broad and strong gains in the region. In Europe, we see the same picture taking shape at midday with only Denmark (-0.03%) on the red side of flat. However, the CAC (+0.32%), DAX (+0.19%), and FTSE (+0.22%) lead modest gains ahead of US data. In the US, as of 7:30 a.m., Futures are pointing toward a start just below Wednesday’s close. The DIA implies a -0.17% open, SPY is implying a -0.11% open, and QQQ implies a -0.08% open at this hour. At the same time, 10-Year bond yields are up slightly to 4.281% and Oil (WTI) is up three-tenths of a percent to $82.35 per barrel in early trading.

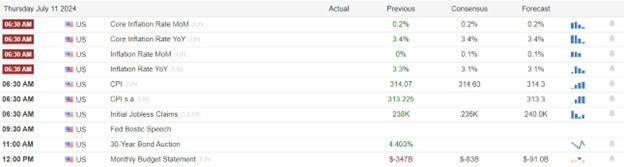

The major economic news scheduled for Thursday include June Core CPI, June CPI, Weekly Initial Jobless Claims, and Weekly Continuing Jobless Claims (all at 8:30 a.m.), June Federal Budget Balance (2 p.m.) and Weekly Fed Balance Sheet (4:30 p.m.). Fed member Bostic also speaks at 11:30 a.m. Earnings season begins again Thursday as Thursday, CAG, DAL, and PEP report before the open. However, there are no major reports scheduled for after the close.

In economic news later this week, on Friday, June Core PPI, June PPI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and the WASDE Ag report are delivered.

In terms of earnings reports later this week, Friday, BK, C, ERIC, FAST, JPM, and WFC report.

So far this morning, DAL beat on revenue while missing on earnings by a penny. On the other side, PEP missed on revenue while beating on earnings.

With that background, it looks as if markets are slightly, but undecidedly bearish in the premarket. All three major index ETFs started the early session flat, but have put in small, black-bodied candles since then. Still, regardless of your timeframe, the market trend (short-term, mid-term, or longer-term) remains very bullish. In terms of extension, QQQ is stretched above its T-line and SPY is also pushing its extension. The T2122 indicator is back up above the center of its mid-range. Therefore, the market still has room to run in either direction, but the Bears still have more slack to work with today. (We are in need of rest or pullback in the QQQ and SPY.) With regard to those 10 big dog tickers, eight of the 10 are in the red early this morning on modest moves. However, the biggest dog, NVDA (+0.36%) is also the best performer of that group on price move and volume.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Public e-Learning 7-9-24 – John

SPY Gave Us its 36th All-Time High of 2024

Market started out higher again Tuesday. SPY gapped up 0.17%, DIA opened just on the red side of flat, down 0.05%, and QQQ gapped up 0.30%. Fron there SPY ground sideways in a tight range all day. Meanwhile, QQQ traveled sideways for 45 minutes and then sold off slowly until 1:30 p.m., having crossed the gap in the process and then traded along the previous close level. Finally, DIA was most volatile, selling off half a percent in the first hour, then rallying 0.90% between 10:30 am and 1 p.m., and selling back off 0.60% in the afternoon. This action gave us indecisive candles in all three major index ETFs. SPY and QQQ gave us gap-up, black-body Spinning Top type candles. Both printed new all-time highs and new all-time high closes. However, DIA printed a black-bodied Doji type that retested (and passed the tests) both of its 17ema and T-line (8ema). This happened on well-below average volume in the SPY, just-below average volume in the QQQ, and just-above average volume in the DIA.

On the day, six of the 10 sectors were in the red again with Energy (-0.88%), Basic Materials (-0.68%), and Industrials (-0.66%) leading the way lower. On the other side, Financial Services (+0.51%) was by far the strongest sector. At the same time, SPY gained 0.10%, DIA lost 0.00%, and QQQ gained 0.09%. VXX gained just a tad, but it remains extremely low at 10.30 and T2122 fell down to just the edge of its oversold territory at 19.41. On the bond front, 10-year bond yields was up a bit t0 4.297% and Oil (WTI) fell 0.63% to close at $81.81 per barrel. So, Tuesday was another “much ado about nothing” day where the Bulls took SPY and QQQ to new all-time highs and all-time high close. Meanwhile, the Bears were unable to push the DIA lower. In the end, all three ended up little changed. It looks as if traders may be waiting on the CPI data on Thursday.

The major economic news scheduled for Tuesday were limited to the EAI Short-Term Energy Outlook, which forecasts record electric use in the US in 2024 and again in 2025. The EIA projects the percentage generated from natural gas to remain at 42%, while coal-based production continues to fall to 15% this year and 14% in 2025. On the oil front, EIA expects global oil demand to outstrip production by 0.900 million barrels per day in 2025. (Current OPEC+ production cuts are just about 6 million barrels per day. So, this could flip, if OPEC+ decides to discontinue their self-imposed restrictions.) US oil production is the largest in the world (13.25 million bpd) and will grow by 320k bpd in 2024 as well as climbing again in 2025. However, US natural gas production will decline in 2024 to 103.5 billion cubic feet per day (from a record 103.8 bcfd in 2023) as producers try to prop up prices. In addition, Natgas demand will grow from a record 89.1 bcfpd in 2023 to 89.4 bcfpd in 2024 before easing to 89.2 bcfpd in 2025. Later, after the close, the API Weekly Crude Oil Stocks showed a drawdown that was larger than expected at -1.923 million barrels (compared to a -0.250-million-barrel forecast but far less than the prior week’s -9.163 million barrels).

In economic speak news, on Tuesday, FOMC Vice Chair for Bank Supervision Barr said that the Fed is considering a rule change that could save the US’s eight largest banks billions of dollars in freed-up capital. (The bank is considering caving to global bank demands of a looser calculation of the capital they must keep on hand. Those banks held $230 billion in capital on hand in Q1 to offset systemic risks. The change could free up a half percent of capital at each bank, which can then be plowed into lending or trading operations…at the cost of slightly less cushion in the event of a crisis.) The banks affected include JPM, BAC, C, WFC, GS, MS, BNY, and STT. Later, Fed Chair Powell told Congress the US economy was no longer overheated. He continued, “We are well aware that we now face two-sided risks, … The labor market appears to be fully back in balance.” Powell said that he did not want to be seen to be sending any signals about the timing of future policy changes. This came in response to GOP Senator Cramer saying any move to lower rates prior to the election would be bad. However, Powell’s headline comment was that keeping rates too high for too long could jeopardize growth. He said, “Reducing policy restraint too late or too little could unduly weaken economic activity and employment.” He concluded by saying that more good inflation data would strengthen the case for a rate cut. At the same time Powell was testifying before the Senate, Treasury Sec. Yellen told a House Committee that the economy has made “tremendous progress” toward reducing inflation. She said, “I believe that it (inflation) will continue to come down over time. (However,) Rents and housing costs continue to leave it higher than we would ideally like.”

In stock news, on Tuesday, BA announced its plane deliveries fell 27% year-on-year in June. However, BA said the 44 jets delivered was the highest number it has delivered in any month so far in 2024. Later, a study published in JAMA showed that the LLY weight loss drug Mounjaro/Zepbound provides faster and greater weight reduction than competitor NVO’s Ozempic/Wegovy drugs. (Both drugs are in the same class, but used different active ingredients.) NVO stock fell 1.85% on the news while LLY gained 1.58%. At the same time, Reuters reported that ORCL ended talks on a $10 billion deal to provide Elon Musk’s xAI startup with servers. (This was a potential expansion of the existing deal where ORCL provides xAI cloud services access to NVDA AI chips.) After the close, IDC (research firm in tech space) announced that global PC shipments rose by 3% in Q2. This was the second-straight quarter of increase after two years of decline. According to IDC data, AAPL computer shipments jumped 20.8% on new product releases compared to Q2 of 2023. Meanwhile, while on the real PC side (about 85%-90% of the market) Taiwan-based Acer led the gains at 13.7% while DELL saw a 2.4% decline. Finally, PATH announced it will lay off 10% its workforce (420 jobs) in a restructuring. PATH stock fell 7% on the news.

In stock legal and governmental news, on Tuesday the US Consumer Financial Protection Bureau announced a $20 million fine of FITB for allegedly opening fake customer accounts and forcing customers to buy auto insurance even though they already had coverage. At the same time, the NHTSA opened a recall inquiry into 94k STLA Jeep hybrid SUVs over the loss of power while in operation. (STLA had a recall over the same issue with all-electric Jeep Wranglers in 2022.) Meanwhile, the NHTSA also announced the LCID is recalling 5,200 of its 2022-2023 Air luxury sedans over a software issue that could cause the same problem as STLA Jeeps face. Later, the state of MI reduced the incentive package (by almost $600 million) that F will receive for its battery plant in Marshall after the company announced expected production cuts.

Overnight, Asian markets leaned to the green side on modest trading with seven of the 12 exchanges above break-even. Thailand (+0.99%), New Zealand (+0.80%), and Japan (+0.61%) led the region modestly higher on the day. In Europe, with the lone exception of Greece (-0.51%) we see green across the board at midday. The CAC (+0.55%), DAX (+0.50%), and FTSE (+0.58%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mostly green start to the day. The DIA implies a flat open, the SPY is implying a +0.17% open, and the QQQ implies a +0.29% open at this hour. At the same time, 10-Year bond yields have fallen to 4.273% and Oil (WTI) is down 0.27% to $81.21 per barrel in early trading.

The major economic news scheduled for Wednesday are limited to EIA Weekly Crude Oil Inventories. However, Fed Chair Powell testifies again (10 a.m.) and Fed Governor Bowman speaks again at 2:30 p.m. There are no major earnings reports set for before the open. Nevertheless, after the close, PSMT and WDFC report.

In economic news later this week, on Thursday, we get June Core CPI, June CPI, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, and June Federal Budget Balance. Fed member Bostic also speaks. Finally, on Friday, June Core PPI, June PPI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and the WASDE Ag report are delivered.

In terms of earnings reports later this week, Thursday, earnings start again as we hear from CAG, DAL, and PEP. Finally, on Friday, BK, C, ERIC, FAST, JPM, and WFC report.

In miscellaneous news, more than 2 million residences and businesses in South Texas remain without power last night. This comes as the forecast is calling for a heat index of 106 degrees for Wednesday. Elsewhere, House GOP members introduced and passed bills to roll back Energy Dept. energy efficiency standards for both refrigerators and dishwashers. The obviously political stunt passed along party lines and will die in the Senate.

With that background, it looks as if markets are slightly bullish in the premarket. All three major index ETFs started the early session flat, but have put in white-bodied candles since then with QQQ leading the way as usual. QQQ and SPY are both testing Tuesday’s all-time high at this point. So, regardless of your timeframe, the market trend (short-term, mid-term, or longer-term) remains very bullish. In terms of extension, QQQ is stretched above its T-line. and SPY is pushing its extension. The T2122 indicator is just in the edge of its oversold range. Therefore, the market still has room to run in either direction, but the Bears have much more slack to work with today. (We are in need of rest or pullback in the QQQ and SPY.) With regard to those 10 big dog tickers, all 10 are in the green early this morning and the biggest dog, NVDA (+1.49%) leads the way on both price move and volume.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

BP Warns as Premarkets Look Green Tuesday

On Monday, SPY and QQQ essentially ground sideways while DIA did the same in more of a volatile way. SPY gapped up 0.13%, QQQ opened 0.07% higher, and DIA gapped up 0.20%. After that open, SPY and QQQ wobbled sideways never venturing more than 0.20% from the gap. However, DIA rallied almost 0.60% higher after the open before selling off 0.94% by noon and then ground sideways in a very tight range the rest of the day. This action gave us indecisive candles in all three major index ETFs. SPY printed a Doji, QQQ printed a white-bodied Spinning Top candle, and DIA gave us a black-bodied Spinning Top candle with the large upper wick. All three remain above their T-line (8ema). SPY and QQQ gave us well below-average volume while DIA printed just average volume.

On the day, seven of the 10 sectors were in the green again with Technology (+0.41%) leading the way higher. On the other side, Financial Services (-0.14%) was the worst-performing sector, just on the red side of flat. At the same time, SPY gained 0.12%, DIA lost 0.06%, and QQQ gained 0.24%. VXX fell 1.82% down to an extremely low 10.27 and T2122 climbed and is now in the center of its mid-range at 47.48. On the bond front, 10-year bond yields was flat at 4.277% and Oil (WTI) fell 1.11% to close at $82.24 per barrel. So, Monday was mostly a “much ado about nothing” day where the Bulls took SPY and QQQ to new all-time highs and all-time high close. Meanwhile, the Bulls tried to move DIA higher but were rejected by the Bears, ending up just on the red side of flat.

The major economic news scheduled for Monday was limited to the NY Fed 1-Year Consumer Inflation Expectation, which fell strongly to 3.0% from a June reading of 3.2%. Later, the May Consumer Credit showed significant increase to $11.35 billion (compared to a $10.70 forecast but up sharply from April’s $6.49 billion).

In stock news, on Monday, Bloomberg reported that MSFT has ordered its Chinese employees to only use iPhones for work as of September. The internal memo that Bloomberg cited said it was part MSFT’s global security push and a direct result of the GOOGL Play Store not being available in China. (GOOGL refused to comply with Chinese demands and as a result the Play Store was blocked from the country. On the other hand, AAPL plays ball with China and has been allowed to operate the AAPL App Store in that country.) At the same time, PARA and Skydance Media agreed to merge after Skydance acquired 70% of the PARA voting stock when it bought the Redstone family’s National Amusements. Later, Reuters reported that VSTO rejected the final $3.2 billion buyout offer from MNC Capital for its ammunition manufacturing unit. However, VSTO did accept an increased bid from a Prague-based Czechoslovak Group for that unit. At the same time, LLY agreed to buy MORF for $3.2 billion in cash ($57/share). Meanwhile, GLW raised its Q2 sales forecast and said it expects profits to come in at the top end or exceed the previously announced range. Later, Reuters reported that US airlines cancelled 1,479 flights and delayed 2,254 more Monday due to Hurricane Beryl. This included UAL cancelling 405 flights and LUV cancelling 268. At the same time, WSR Management told shareholders “it is likely there will be a change of control” in the REIT, even though the company had rejected a buyout offer from private MCB Real Estate. (MCB had offered $14/share, all cash.) Later, Reuters reported that BCSF is close to reaching a deal to buy ENV, near its current price of $63 per share.

In stock legal and governmental news, on Monday, the FIM-CISL union warned that STLA vehicle production in Italy could fall by a third if Italian government incentives to buy STLA cars do not work. (The union said the impact of incentives are not known yet, but output fell 25% in the first half of the year.) Later, the Dept. of Transportation announced it had screened 3.01 million passengers on Sunday, the most ever in a single day. Meanwhile, the UK antitrust regulator approved TMO’s $3.1 billion deal to buy OLK. After the close, the NTSB said it is investigating a UAL flight of a BA 757-200 jet that lost a wheel from its main landing gear after takeoff from Los Angeles. After the close, the Dept. of Defense said it is in discussions with the Dept. of Justice before determining the impact of BA’s guilty plea on existing government contracts. In unrelated news, the FAA ordered the inspection of 2,600 BA 737 jets because the planes passenger oxygen masks may fail during an emergency due to retention strap problems. (The agency had “requested” the inspections on June 17, but is ordering it now due to non-compliance.)

Overnight, Asian markets were nearly green across the board. Only Thailand (-0.20%) was lower as Japan (+1.96%), Shenzhen (+1.68%), and Shanghai (+1.26%) led a broad rally in the region. In Europe, markets are mixed at midday with six exchanges in the green while eight are down and one (Greece) is unchanged. The CAC (-0.87%), DAX (-0.44%), and FTSE (-0.13%) lead the region on volume as always. In the US, as of 7:30 a.m., Futures are pointing toward a modest green start to the day. The DIA implies a +0.08% open, the SPY is implying a +0.22% open, and the QQQ implies a +0.37% open at this hour. At the same time, 10-Year bond yields are up to 4.299% and Oil (WTI) is down half of a percent to $81.94 per barrel in early trading.

The major economic news scheduled for Tuesday are limited to EAI Short-Term Energy Outlook (noon) and API Weekly Crude Oil Stocks (4:30 p.m.). We also hear from Fed Vice Chair Barr (9:15 a.m.), Fed Chair Powell Testifies before Congress (10 a.m.), Treasury Sec. Yellen (10 a.m.), and Fed Governor Bowman (1:30 p.m.). The major earnings reports set for before the open are limited to HELE. After the close, there are no reports of note scheduled.

In economic news later this week, on Wednesday, EIA Weekly Crude Oil Inventories are reported. Fed Chair Powell also continues his testimony and Fed Governor Bowman speaks again. On Thursday, we get June Core CPI, June CPI, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, and June Federal Budget Balance. Fed member Bostic also speaks. Finally, on Friday, June Core PPI, June PPI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and the WASDE Ag report are delivered.

In terms of earnings reports later this week, Wednesday, PSMT and WDFC report. On Thursday, earnings start again as we hear from CAG, DAL, and PEP. Finally, on Friday, BK, C, ERIC, FAST, JPM, and WFC report.

So far this morning, HELE missed on both the top and bottom lines.

In miscellaneous news, early Tuesday BP warned of a $2 billion impairment related to a German refinery. It also cited weak refining margins and poor oil trading execution as reasons for concern. Elsewhere, CNBC reports that the office space vacancy rate in San Francisco proper has hit a record 34.5% in Q2. (San Fran has historically been some of the most expensive real estate in the country.) The report said that to adjust for that the “asking price” for office space has fallen back to 2015 levels. Meanwhile, the Sun Valley “Summer Camp for Billionaires” kicks off today with the CEOs of AAPL, AMZN, DIS, META, NFLX, PARA, WBD, and Bill Gates as well as Jeff Bezos meet with the CEO of OpenAI in the exclusive Idaho gathering.

With that background, it looks as if markets are set to open higher, but not in a decisive way. All three major index ETFs gapped up modestly to start the premarket. However, they have printed small, indecisive candles with the leader (QQQ) even giving us a black-body so far in the early session. Remember that all three are either at new all-time highs or not far away in the case of DIA. All three remain above their T-line (8ema). So, regardless of your timeframe, the market trend (short-term, mid-term, or longer-term) remains very bullish. In terms of extension, QQQ is stretched above its T-line. However, the T2122 indicator is in the center of its mid-range. Therefore, the market has room to run in either direction, but the Bears have more slack to work with today. With regard to those 10 big dog tickers, eight of them are in the green early this morning. For the second straight day it is INTC (+2.35%) leading that way joined by the biggest dog, NVDA (+1.52%). However, note that the two laggards are led by the second-biggest dog, TSLA (-1.04%) in the premarket.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

BA Pleads Guilty With Market At Record Highs

The markets on Friday started modestly higher and never looked back. SPY opened 0.06% higher, DIA opened 0.08% higher, and QQQ gapped up 0.19%. From that point, SPY and QQQ steadily rallied the rest of the day, closing near the highs. Meanwhile, DIA meandered sideways in waves until 12:45 p.m., when it rallied steadily the rest of the day. This action gave us large, white-bodied candles in the SPY and QQQ. Both printed new all-time highs and ended at new all-time high closes. At the same time, DIA retested its T-line (8ema) before printing a white-bodied Hammer-type candle that closed above its T-line. This happened on well below-average volume in all three.

On the day, seven of the 10 sectors were in the green again with Healthcare (+0.82%), Technology (+0.79%), and Consumer Defensive (+0.78%) leading the way higher. On the other side, Industrials (-0.60%) was by far the worst-performing sector. At the same time, SPY gained 0.58%, DIA gained 0.21%, and QQQ gained 1.04%. VXX actually gained slightly (+0.38%) to a still extremely low 10.46 and T2122 fell but remains in its mid-range at 30.88. On the bond front, 10-year bond yields dropped sharply to 4.277% and Oil (WTI) fell 0.72% to close at $83.28 per barrel. So, for the traders that showed up Friday (and there weren’t many), it was the Bull’s day from the start. On a steadily rallying day, the Bears simply never came back, instead opting for a four-day weekend.

The major economic news scheduled for Friday included, June Avg. Hourly Earnings, which came in down as expected at +3.9% Year-on-Year (compared to forecast of +3.9% and down from May’s +4.1% reading). On a Month-on-Month basis, June Avg. Hourly Earnings were also down as expected at +0.3% (versus the +0.3% forecast and down from May’s +0.4% value). At the same time, June Nonfarm Payrolls were also down but higher than predicted at +206k (compared to a forecast of +191k but down from May’s +218k number). On the private side, June Private Nonfarm Payrolls were far lower than anticipated at +136k (versus a forecast of +160k and particularly lower than May’s +193k reading). Note that the prior two months values on Nonfarm Payrolls were revised downward 100k jobs. At any rate, this gave us a June Unemployment Rate that came at 4.1% (versus a forecast and May value of 4.0%). This all came on a June Participation Rate of 62.6% (which was in-line with the 62.6% forecast and up a tick from May’s 62.5% reading).

In Fed speak news, on Friday, NY Fed President Williams (well before the employment data release) told an Indian central bank audience that the Fed still has “a ways” to go before reaching their 2% inflation goal. Williams said, “We have seen significant progress in bringing it down, … But we still have a way to go to reach our 2 percent target on a sustained basis. We are committed to getting the job done.” He continued, “We must accept that uncertainty will continue to define the future.” (This last remark was in reference to the fact that economists and analysts simply aren’t able to deliver accurate forecasts of exactly how much time at a given Fed Funds rate or how much quantitative tightening will deliver exactly how much improvement in each of many different inflation and employment metrics. In other words, Williams was saying its not math, there is a lot of art to central banking.

In stock news, on Friday, SHEL announced it will take a charge of $2 billion related to the sale of a Singapore refinery and halting the construction of a biofuel plant in the Netherlands. At the same time, Epic Games announced that AAPL has again (for the second time) rejected applications to create a European store for use with Epic iPhone apps. (European courts and regulators had ordered AAPL to allow this.) Later, the Wall Street Journal reported that JPM has begun warning customers that they need to prepare to pay for checking accounts. At the same time, CG announced they are in exclusive talks to acquire BAX’s kidney care spinoff unit (Vantive) for more than $4 billion, which includes unspecified debt takeover. Meanwhile, Reuters reported that VYX (NCR) is exploring the sale of its digital banking business, hoping to raise $3 billion. After the close (and after the reports noted above), AAPL reversed course and approved Epic Games marketplace app for iPhones and iPads. Elsewhere, KOSS has become the latest meme stock, spiking more than 205% just on Wednesday and Friday. This comes after social media posters decided that a “Roaring Kitty” post of a picture of a microphone with a US Flag background. Meme traders took this to mean that Roaring Kitty was leading a short-squeeze play on KOSS around the July 4 holiday. (The thing that makes this scary is that KOSS doesn’t make microphones, it sells headphones.)

In stock legal and governmental news, on Friday, the European Commission (acting as Europe’s antitrust regulator) announced that V and MA agreed to extend the caps on their fees on tourist card use through 2029. (The caps are a 0.2% fee on non-EU debit card use and 0.3% fee limit on non-EU credit card settlements. For “card not present” or online commerce, the fee limits will remain 1.15% for debit cards and 1.5% for credit cards.) Later, the PSWR announced it had received a subpoena from SEC back in February related to company accounting practices. At the same time, NVO was given a reprimand from UK regulators for failing to disclose the fees and expenses paid to individual and organizations in the British healthcare sector (who could either use or prescribe NVO products). Later, a court in Australia fount that PYPL used unfair contracts with small businesses. At the same time, the European Commission said it had “requested: more information from AMZN on the measures the company has taken to comply with the European Digital Services Act. (In the past, such requests have led to rulings and might lead to significant fines.) Later, Reuters reported that a trade group representing miners has been strongly lobbying for the revival of the Bureau of Mining (which was closed in 1996). Perhaps oddly, the business group is claiming that adding a dedicated agency would speed up and streamline mining policy and approvals (at the cost of additional federal jobs). Meanwhile, a federal judge threw out a central claim of the FTC in the agency’s lawsuit against WMT. The suit alleges that WMT turned a blind eye to scam artists using its money transfer services to swindle customers out of millions of dollars. (The ruling rejects the claim that WMT owes monetary damages for violating the federal Telemarketing Sales Rule.) In later-breaking news, early Monday BA decided to plead guilty to fraud related to the two crashes of 737 MAX jets in 2018 and 2019 after violating the 2021 consent decree settlement that had allowed the company from facing prosecution then.

Overnight, Asian markets were mostly in the red. Only Taiwan (+1.37%) and Thailand (+0.80%) were green. Meanwhile, Hong Kong (-1.55%) and Shenzhen (-1.54%) led 10 of the regions 12 exchanges lower. In Europe, the outlook is much rosier are midday with 11 of the 15 bourses in the region green. The CAC (+0.215), DAX (+0.34%), and FTSE (+0.21%) lead the region higher in early afternoon trade. In the US, as of 7:00 a.m., futures point toward a start just on the red side of flat. The DIA implies a -0.04% open, the SPY is implying a -0.05% open, and the QQQ implies a -0.03% open at this hour. At the same time, 10-Year bond yields are up to 4.299% and Oil (WTI) is down more than one percent to $82.29 per barrel in early trading.

The major economic news scheduled for Monday is limited to NY Fed 1-Year Consumer Inflation Expectations (11 a.m.) and May Consumer Credit (3 p.m.). There are no major earnings reports set for before the open. However, after the close, HELE reports (the only report of note).

In economic news later this week, on Tuesday we get the EAI Short-Term Energy Outlook and API Weekly Crude Oil Stocks report. We also hear from Fed Vice Chair Barr, Fed Chair Powell Testifies before Congress, and Fed Governor Bowman. Then on Wednesday, EIA Weekly Crude Oil Inventories are reported. Fed Chair Powell also continues his testimony and Fed Governor Bowman speaks again. On Thursday, we get June Core CPI, June CPI, Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, and June Federal Budget Balance. Fed member Bostic also speaks. Finally, on Friday, June Core PPI, June PPI, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, and the WASDE Ag report are delivered.

In terms of earnings reports later this week, there are no earnings reports scheduled for Tuesday. Then Wednesday, PSMT and WDFC report. On Thursday, earnings start again as we hear from CAG, DAL, and PEP. Finally, on Friday, BK, C, ERIC, FAST, JPM, and WFC report.

In miscellaneous news, on Friday, the UK seated its new Labour Prime Minister and ministers (cabinet) after that party’s landslide victory in Thursday’s election. (Labor won 63%, or 412, of the 650 seats in UK House of Commons. That gives them the biggest majority since Tony Blair’s win in 1997. Meanwhile, the Conservatives, aka Tories, won just 121, a dramatic fall from their previous 365 seats.) In France, on Sunday, voters rallied to reverse the first round of voting and keep the far-right out of power. A record turnout (not seen since 1978), gave a significant majority of seats in the parliament to a grand alliance against the far-right in the second, final round. Contrary to the first round of voting, the left-wing New Popular Front took 182 seats (plus another 13 left-wing seats from other parties), President Macron’s centrist Ensemble party took 168 seats, (the alliance of those parties two having well more than the 289 needed to have a majority and elect a leader). At the same time, the right-wing extremist National Rally was limited to 143 seats (after having been projected at more than twice that number after the first round of voting). Other parties fill out the remaining 71seats.

In other overseas news, on Friday, reports came out that Hamas had finally agreed to the conditions of the cease fire plan for Gaza that President Biden outlined at the end of May. However, Israel immediately came back with new conditions and Israeli PM Netanyahu told the press “It should be emphasized that there are still gaps between the sides.” Then on Sunday, Netanyahu doubled down by saying he won’t agree to a cease fire until “Israel has achieved all its military objectives. Further North, on Friday Russian flunky and Hungarian autocrat Victor Orban visited Moscow and Putin while “uninviting” German Chancellor Scholz from a state visit to Hungary. In other news, on Saturday, the Wall Street Journal reported that Chinese ecommerce websites Shein and Temu (AMZN and BABA competitors) appear to be growing fast outside of Asian. They quoted the CEO of DHL (a major airfreight shipper owned by DHLGY) as saying the two companies have grown to take up 30% of cargo space on many shipping routes. (This is significant because neither company sells perishable or high-value goods typical of air freight.) In June, this caused Chinese shipping rates to increase 40% as e-commerce bid up airfreight rates and is now causing manufacturers and retailers to buy up space early for upcoming holiday shipments.

With that background, it looks as if markets are undecided, sitting here at the all-time highs in SPY and QQQ as well as DIA being less than 2% from its own all-time high. All three major index ETFs opened flat and (at least early) have printed small, indecisive candles so far in the premarket. All three remain above their T-line (8ema). So, regardless of your timeframe, the market trend (short-term, mid-term, or longer-term) remains very bullish. In terms of extension, QQQ is a bit stretched above its T-line. However, the T2122 indicator remains in the lower end of its mid-range. Therefore, the market has room to run in either direction, but the Bears have more slack to work with today. With regard to those 10 big dog tickers, they are evenly split between gainers and losers in the premarket. INTC (+3.44%) is by far the biggest mover, but TSLA (-0.94%) and NVDA (+0.64%) have traded nine and eight time (respectively) the dollar-volume of stock as INTC in the premarket.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Sitting at All-Time High Closes in SPY and QQQ

Tuesday started off with a Bear trap. SPY gapped down 0.30%, DIA opened 0.16% lower, and QQQ gapped down 0.32%. However, at that point, SPY and QQQ began a steady all-day rally. Meanwhile, DIA chopped sideways in the gap until 1 p.m. when it followed the other major index ETFs higher. All three posted a strong rally into the close. This action gave us large white-bodied, Marubozu candles in the SPY, DIA, and QQQ. SPY and DIA also printed Bullish Engulfing signals. All three crossed back above their T-line after a retest and SPY and QQQ both gave us new all-time high closes. This happened on well below-average volume across the board.

On the day, nine of the 10 sectors were in the green again with Financial Services (+0.92%) out in front leading the way higher. Communications Services (-0.38%) was the only sector in the red. At the same time, SPY gained 0.67%, DIA gained 0.47%, and QQQ gained 1.05%. VXX dropped another 1.14% to a very low 10.37 and T2122 climbed back into the center of its mid-range at 43.09. On the bond front, 10-year bond yields fell to 4.431% and Oil (WTI) fell 0.41% to close at $83.04 per barrel. So, what we saw on Tuesday seemed like a very low volume pre-holiday rally after a gap down.

The major economic news scheduled for Tuesday was limited to May JOLTs Job Openings, which came in higher than expected at 8.140 million (compared to a 7.960 million forecast and an April value of 7.919 million). Then, after the close, the API Weekly Crude Oil Stocks report showed a huge, unexpected drawdown of 9.163 million barrels (versus a forecasted 0.150-million-barrel drawdown and the previous week’s 0.914 million inventory build).

In Fed speak news, Fed Chair Powell told a conference that US inflation is now falling again. Powell said, “I think the last reading … and the one before it to a lesser suggest that we are getting back on the disinflationary path.” However, Powell indicated the Fed still needs to see more before cutting rates, saying, “We want to be more confident that inflation is moving sustainably down toward 2% … before we start … loosening policy.” He went on to say that, while there is two-sided risk, there is still no need to rush into rate cuts. Powell said, “Given the strength we see in the economy we can approach the question carefully.” Finally, he concluded with the point that the Fed does not want to wait too long, saying “we don’t want to lose the expansion.” Elsewhere, Chicago Fed President Goolsbee told CNBC that he sees some “warning signs” of weakening in the economy. Goolsbee said, “You only want to stay this restrictive for as long as you have to.”

In stock news, on Tuesday, AAL agreed to a deal to purchase 100 hydrogen-electric engines for its regional jets (made by BDRBF). (It is unclear how new “green” engines would be fitted onto or approved for use on those regional jets.) At the same time, Reuters reported that major Japanese insurance companies are planning to sell $3.1 billion of HMC stock. Later, RIVN shares popped as it reported vehicle deliveries that modestly beat analyst estimates for Q2. At the same time, TSLA stock gapped up more than 4% after it reported deliveries that exceeded expectation, 443,956 actual versus 439,302 (consensus estimate). Those deliveries were still down 5%, but better than expected. At the same time, CONN stock plunged on a Bloomberg report that the company is preparing to file bankruptcy. Meanwhile, Bloomberg also reported that HOOD is considering offering “crypto futures” to the US and European markets. (HOOD is hoping to use futures licenses from Bitstamp, a cryptocurrency exchange the company agreed to purchase last month.) Elsewhere, GM reported slower sales growth in Q2, up just 0.6% from the same quarter in 2023. However, TM posted strong 9.2% Q2 sales growth in North America.

In stock legal and governmental news, on Tuesday, President Biden called out NVO and LLY, specifically related to their blockbuster GLP-1 weight loss drugs, in an op-ed article. Later, interestingly given all of its recent rulings, the US Supreme Court refused to hear a challenge to OSHA regulatory authority from an OH company that had claimed OSHA had exceeded its authority to regulate. Two of the extreme right justices indicated they wanted to hear the case, but they could not find enough support (4 justices must indicate they want to hear a case for it to be taken up). Later, the FTC announced it would sue to block the merger between TPX and retailer Mattress Firm as being detrimental to competition. At the same time, a US Appeals Court threw out a dismissal of an antitrust lawsuit against 10 big banks due to a financial conflict of interest. (The judge’s wife owned stock in at least one of the banks.) So, the case against BAC, C, JPM, CS, DB, GS, MS, WFC, NWG, and BCS will proceed. Later, PGR agreed to pay $48 million to settle a class-action lawsuit alleging it systematically undervalued wrecked cars to reduce claims paid. Meanwhile, after the close, the FDA approved LLY’s early Alzheimer’s drug donanemab. (Donanemab is priced at $32k per year, slightly higher than the only approved competitor.) Also after the close, both SLB and CHX disclosed they have received a second set of requests for information from the US Dept. of Justice in connection with their $7.75 billion acquisition deal.

Overnight, Asian markets leaned heavily to the green side. Only Shenzhen (-0.59% and Shanghai (-0.49%) were in the red. Meanwhile, Singapore (+1.41%), Taiwan (+1.28%), and Japan (+1.26%) led the majority of the region higher. In Europe, with the lone exception of Norway (-0.19%) we see green across the board at midday. The CAC (+1.63%), DAX (+1.01%), and FTSE (+0.59%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing to mixed, flat start to the day. The DIA implies a +0.06% open, the SPY is implying a -0.01% open, and the QQQ implies a -0.02% open at this hour. At the same time, 10-Year bond yields are at 4.433% and Oil (WTI) is flat at $82.78 per barrel in early trading.

The major economic news scheduled for Wednesday includes that MARKETS CLOSE AT 1 P.M. In addition, JUNE ADP Nonfarm Employment (8:15 a.m.), Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, and May Trade Balance (all at 8:30 a.m.), S&P Global Services PMI and S&P Global Composite PMI (9:45 a.m.), May Factory Orders, June ISM Non-Mfg. Employment, and June ISM Non-Mfg. Prices (10 a.m.), EIA Weekly Crude Oil Inventories (10:30 a.m.), and FOMC Meeting Minutes (2 p.m.). NY Fed President Williams also speaks at 7 a.m. The major earnings reports set for Tuesday are limited to STZ before the open. There are no major reports set for after the close.

In economic news later this week, on Thursday, MARKETS ARE CLOSED. However, we still get the Fed Balance Sheet. Then on Friday, June Avg. Hourly Earnings, June Nonfarm Payrolls, June Private Nonfarm Payrolls, June Participation Rate, and June Unemployment Rate are reported. NY Fed President Williams also speaks.

In terms of earnings reports later this week, there are no earnings reports Thursday or on Friday.

So far this morning, STZ missed slightly on revenue while beating handily on earnings.

In miscellaneous news, on Wednesday morning LUV announced it has adopted a “poison pill” policy to fend off activist investor Elliott Management. IF Elliott were to acquire 12.5% of the LUV stock, all existing shareholders would be allowed to buy an additional share for every share they own…at a 50% discount to the market price. At the same time, PARA is back in the deal arena as Skydance and Shari Redstone’s National Amusements (which owns 70% of the voting shares of PARA) have reached another “preliminary deal” for Skydance to acquire it. (They had a preliminary deal in June that fell through and then the two sides walked away.) The new deal reduces Redstone’s take to $1.75 billion with Skydance acquiring half of PARA voting stock at $15/share ($4.5 billion) and contributing another $1.5 billion toward PARA balance sheet debt.

With that background, it looks as if markets are undecided, sitting here at the all-time highs. All three major index ETFs opened flat and have printed small, indecisive candles so far in the premarket. DIA, the laggard, is showing the strongest candle in the early session, but that is hardly a big bull candle. All three remain above their T-line (8ema). So, the short-term trend is now bullish again and both the mid-term and especially the longer-term trend in all three major index ETFs remains very bullish. In terms of extension, none of those three are extended above their T-line and while the T2122 indicator is in the center of its mid-range. Therefore, the market has room to run in either direction. With regard to those 10 big dog tickers, they are evenly split between gainers and losers in the premarket. NVDA (-0.98%), the biggest dog, is the worst performer but TSLA (+2.10%), the second biggest trader is the strongest performer of the 10.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Volatile Price Action

U.S. stock futures took a downward turn on Tuesday morning in yesterday’s volatile price action where the bulls were once again unable to hold early gains. Federal Reserve Chair Jerome Powell is scheduled to address a policy panel at the European Central Bank Forum at 9:30 a.m. ET. Additionally, the release of the May job openings and labor turnover report will provide further clarity on the state of the U.S. labor market. Investors are also looking ahead to Friday, when the June jobs report.

The European markets trade red this morning, with the Stoxx 600 index declining by 0.57% as of 11 a.m. in London. Inflation data from the euro area provided a mixed picture; while headline inflation experienced a decrease to 2.5% in June, as reported by the European Union’s statistics agency, core and services inflation figures remained elevated at 2.9% and 4.1% respectively.

Asian markets, the Nikkei 225 surged past the 40,000 thresholds, a peak it hadn’t reached in the previous three months. Conversely, the Topix index narrowly missed setting a record for its all-time closing high. The Japanese yen experienced a significant dip, sliding down to 161.67 against the US dollar, marking its weakest position in nearly four decades. Meanwhile, in South Korea, the Kospi index closed 0.84% lower. Across the waters, Hong Kong’s Hang Seng index saw a modest rise of 0.33, and the Australian market witnessed a slight downturn, with the S&P/ASX 200 dropping by 0.42%.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include MSM, & RDUS. After the bell include SLP.

News & Technicals’

The U.S. stock market has witnessed a significant shift in its composition over the past decade, with the 10 largest companies now representing more than a third of the S&P 500 stock index, compared to just 14% a decade ago. This change has been largely fueled by the meteoric rise of technology giants, often referred to as the “Magnificent Seven”: Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia, and Tesla. Their combined market capitalization has soared, driven by widespread tech enthusiasm and their increasing influence on consumers and businesses alike.

This concentration has sparked a debate among market observers. Some experts express concern that such a heavy weighting towards a handful of tech behemoths could expose investors to heightened risks, particularly if these companies face regulatory challenges, shifts in technology, or changes in consumer behavior. On the other hand, some analysts argue that this concentration is not worrisome, pointing to the companies’ robust earnings, solid growth prospects, and the fact that they are at the forefront of innovation and market trends.

The divergence in opinion highlights the complexity of market dynamics and the challenges in predicting the impact of market concentration. While the dominance of these tech giants is clear, the long-term implications for the market and investors continue to be a subject of intense scrutiny and debate. Whether this concentration is a harbinger of risk, or a non-issue will likely depend on future market conditions, regulatory environments, and the companies’ continued ability to innovate and adapt.

The political landscape in the UK has been dominated by a singular narrative since Conservative Prime Minister Rishi Sunak announced a general election in May — the forecast of a sweeping victory for the Labour Party. Voter polls have consistently shown a significant advantage for the Labour Party, suggesting a lead of approximately 20 points over the Conservative Party. Despite this, the Labour Party has maintained a cautious stance, refraining from commenting on these projections. Their reluctance is rooted in the understanding that polls can be volatile, with results that can “vary and fluctuate.” This measured approach reflects a broader awareness of the unpredictability inherent in political campaigns and the potential for last-minute shifts in public opinion. As the election draws nearer, all eyes will be on whether the Labour Party can convert their lead in the polls into actual votes and possibly reshape the UK’s governing body.

Iran’s political arena is set for a pivotal moment with a runoff election scheduled for Friday, July 5. This election features a stark contrast between a right wing hardliner and a reformist candidate, reflecting the nation’s deep divisions amidst severe economic, social, and geopolitical pressures. The initial round of voting saw a historically low turnout, with only about 40% of eligible voters casting their ballots. Despite the low participation, the results were telling reformist Masoud Pezeshkian emerged as the frontrunner, securing 10.4 million votes out of the 24.5 million total votes. Close on his heels was the hardline candidate, Saeed Jalili, a former nuclear negotiator, who garnered 9.4 million votes. The outcome of this runoff has the potential to significantly influence Iran’s future direction, as the two candidates offer vastly different visions for addressing the nation’s challenges.

In another day of volatile price action, the bulls were unable to hold early gains. Although the DIA, SPY and QQQ remain in bullish patterns there are hints the bears could be waking up from a very long slumber. However, the low volume of a holiday week adds to a lot of uncertainty on the path forward. Plan your risk carefully and have a plan to protect yourself if the bears do suddenly decide to attack.

Trade Wisely,

Doug

Market Nervous and Down Overnight

Monday gave us a modestly sideways day with little more gain from QQQ than the SPY and DIA. SPY gapped up 0.28%, DIA gapped up 0.23%, and QQQ opened just 0.17% higher. From there, all three major index ETFs faded the open, reaching the lows of the day mid-morning. This was followed by a rally that took SPY and DIA back into the morning gap and QQQ across the gap to new highs in early afternoon. However, all three spend the afternoon grinding sideways. This action gave us indecisive candles across the board. QQQ printed a white-bodied, Hammer, Bullish Harami candle which retested its T-line (8ema) and bounced up off the successful test. At the same time, SPY printed a black-bodied Dragonfly Doji type candle that also retested and remains above its T-line. DIA gave us a black-bodied, Spinning Top-type candle with a high wick. However, DIA also retested and passed the test of its T-line from above.

On the day, six of the 10 sectors were in the red again with Basic Materials (-0.95%) out in front leading the way lower. Meanwhile, Technology (+0.35%) led the four green sectors. At the same time, SPY gained 0.21%, DIA gained 0.09%, and QQQ gained 0.58%. VXX dropped 3.94% to a very low 10.49 and T2122 fell, but again remains in the mid-range, this time just above the oversold territory at 22.15. On the bond front, 10-year bond yields spiked to 4.269% and Oil (WTI) spiked 2.35% to close at $83.46 per barrel. This all happened on below-average volume in the SPY, DIA, and QQQ. So, Monday really was a was a “much ado about nothing” day for the market. If you look very closely you can see a 4-5 day very modest rally (particularly in the QQQ). However, you really have to look to see it.

The major economic news scheduled for Monday included S&P Global Mfg. PMI, which came in a tick shy of expectations at 51.6 (compared to a 51.7 forecast but up modestly from the May 51.3 reading). Later, May Construction Spending was down 0.1% (versus a forecast of +0.3% which was also the April value). At the same time, the June ISM Mfg. Employment Index was lower than anticipated at 49.3 (compared to a forecast of 50.0 and a May reading of 51.1). The headline June ISM Mfg. PMI was also lower than predicted at 48.5 (versus a 49.2 forecast and May’s 48.7 number). The June ISM Mfg. Price Index was lower than expected at 52.1 (compared to a 55.8 estimate and the May 57.0 reading).

In Fed speak news, NY Fed President Williams told a conference Sunday (those comments were not made public until Monday), “I’m confident that we at the Fed are on a path to achieving our 2% inflation goal on a sustained basis.”

In stock news, on Monday, BA agreed to buy SPR for $4.7 billion (all stock) with parts of the supplier going to EADSY (Airbus). As part of the deal, SPR will pay EADSY $559 million. At the same time, RACE announced two warranty extension plans that will allow owners of their hybrid models to get battery replacements at particular times (the 8th and 16th year of battery life). Later, UBS announced it had completed it merger (acquisition) of CS in Switzerland. Meanwhile, DE announced 590 layoffs (280 at an IL plant and 310 at an IA plant), citing declining demand. At the same time, Reuters reported that AMZN has become the first company to “sidestep” a global standard for verifying carbon offsets. (This is particularly interesting since AMZN founder Bezos was the founder and Chair of the group that created the standard.) AMZN claims they still support the standard for verification as a model, but want a new, higher standard. Later, EADSY announced its plane deliveries rose 2% in the first half of 2024 to 323, including 67 planes in June. At the same time, BLK announced it will buy British company UK Data Group for $3.23 billion in cash. Later, GS reported that, during June, global hedge funds sold shares of technology, media and telecom companies at the fastest pace since 2016. However, GS said this trend (three straight months of such selling) was almost entirely driven by short sellers targeting the all-time highs. After the close, shareholders of CRM voted to reject the CEO (and other executive’s) compensation plans. However, the vote is not binding on board action.

In stock legal and governmental news, on Monday, BMY agreed to pay $2.7 million to settle an Israeli anti-trust case over blocking a generic version of its cancer drug Imnovid. At the same time, the US Supreme Court ruled in favor of a ND convenience store, reinstating its lawsuit against the Fed over a 2011 regulation allowing credit card companies (V and MA) to charge “swipe fees” per transaction up to a maximum $0.21 each. Following the court throwing out the Chevron Deference, this will be one of the new suits that will challenge agency’s authority to regulate. Later, Reuters reported that anti-trust regulators in France are set to charge NVDA over anti-competitive practices. At the same time, Keith Gill (known as “Roaring Kitty”) was sued by GME investors who allege they lost money due to him running a “pump-and-dump” scheme on the stock. Later, a US Appeals Court ruled that part of the new Biden Administration student debt relief plan may resume, reversing an injunction issued by a judge in KS.

Elsewhere, the US Supreme Court punted on cases involving GOP-led states ability to regulate social media. The court unanimously held that the lower courts had not adequately assessed the impact of the laws in question impact on the social media company’s first amendment rights. The ruling cast doubt on the TX law (which a lower court had upheld) prohibiting moderation by META, GOOGL, and SNAP among others. Later, the SEC sued SICP for securities fraud, alleging the crypto-focused company misleads investors about bank secrecy and anti-money laundering compliance programs. Separately, SICP agreed to pay $63 million to settle probes of the company’s compliance lapses. At the same time, a federal judge blocked a MS law that required users of social media platforms to verify ages and restricted access by minors without parental consent.

Overnight, Asian markets were mixed but mostly in the red. Japan (+1.12%) and Singapore (+0.88%) were by far the biggest gainers while Shenzhen (-0.97%) and South Korea (-0.84%) led the more numerous losers. In Europe, the bourses are mostly red with Russia (+1.39%) the only noteworthy gainer12 of the 15 bourses in the red. The CAC (-0.83%), DAX (-0.99%), and FTSE (-0.32%) lead the region lower in early afternoon trade. In the US, as of 7:00 a.m., Futures are pointing toward a move lower to start the day. The DIA implies a -0.31% open, the SPY is implying a -0.36% open, and the QQQ implies a -0.46% open at this hour. At the same time, 10-Year bond yields are up to 4.45% and Oil (WTI) is up another 0.73% to $83.99 per barrel in early trading.

The major economic news scheduled for Tuesday is limited to May JOLTs Job Openings (10 a.m.) and the API Weekly Crude Oil Stocks report (4:30 p.m.). However, Fed Chair Powell speaks at 9:30 a.m. The major earnings reports set for Tuesday are limited to Tuesday MSM, PSNY, and RDUS before the open. There are no major reports set for after the close.