Member e-Learning 8-15-24 – John

Economic Data

US equity futures saw modest gains as traders anticipated a busy morning filled with economic data releases. Investors are particularly keen on the upcoming retail sales data, which will provide further insights into the economic trajectory. Additionally, Walmart’s earnings report, scheduled for release before the market opens, is expected to shed light on consumer spending patterns, making it a focal point for market watchers.

On Thursday, European stocks continued their upward trend, buoyed by cooler-than-expected inflation readings that bolstered investor confidence. This positive momentum was further supported by the latest U.K. GDP data, which revealed a 0.6% expansion in the second quarter, aligning with market expectations. The combination of these factors contributed to a generally optimistic outlook for European markets as the week progressed.

In the second quarter, Japan’s economy outperformed market expectations, with its gross domestic product (GDP) rising by 0.8% quarter-on-quarter, surpassing the 0.5% increase anticipated by economists polled by Reuters. Meanwhile, China’s retail sales experienced a year-on-year growth of 2.7%, slightly exceeding the forecasted 2.6% growth. However, the urban unemployment rate in China saw a minor uptick, climbing to 5.2% from 5% in June.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include WMT, BABA, AIT, CLBT, GRAB, NICE, SPTN, & TPR. After the bell include AMCR, AMAT, COUR, HRB, & ROST.

News & Technicals’

Cisco reported its third consecutive quarter of declining revenue, marking its first full fiscal year drop since 2020. Despite this, the company’s earnings and revenue exceeded analysts’ expectations. In response to the ongoing challenges, Cisco announced a 7% reduction in its global workforce. Prior to Wednesday’s close, Cisco’s stock had fallen by 10% this year, contrasting sharply with the Nasdaq’s approximately 15% gain.

More than a week into Ukraine’s unexpected incursion into Russia’s Kursk region, the gains have likely surpassed Kyiv’s highest expectations. Ukrainian forces now control over 1,000 square kilometers of Russian territory and have captured 74 settlements, according to Ukraine’s top military commander, Oleksandr Syrskyi. While Moscow has yet to mount a significant response, it has warned of a ‘worthy’ retaliation. Analysts suggest that Ukraine faces a critical decision: whether to reinforce its troops and hold or advance its position, or to withdraw before Russia launches what is expected to be a fierce and deadly counterattack.

Starbucks has announced a substantial compensation package for its incoming CEO, Brian Niccol, who is transitioning from Chipotle. Niccol will receive $10 million in cash and $75 million in equity awards upon joining the company. His annual base salary will be $1.6 million, with the potential to earn an additional $7.2 million in cash. As he steps into his new role, Niccol faces the significant challenge of revitalizing Starbucks’ struggling business.

Payments firm Airwallex has achieved an impressive annual revenue run rate of $500 million, driven by substantial growth in its North American and European operations, according to CEO Jack Zhang. Zhang aims to prepare Airwallex for an initial public offering (IPO) by 2026. The company, which was recently valued at $5.6 billion and is backed by Tencent, is considered a strong contender among major fintech IPO candidates.

With a very busy morning of potential market-moving economic data traders should prepare for just about anything. The relief rally is starting to get a little long in the tooth and perhaps today’s data can continue to inspire the bull higher. However, we should not be surprised to see a little profit-taking begin at any time. That said, avoid chasing with the fear of missing out.

Trade Wisely,

Doug

WMT Says Consumer Is Okay

Wednesday saw a mostly flat open after CPI data. SPY opened up 0.16%, DIA opened down just 0.03%, and QQQ “gapped” up 0.19%. From there, the whipsaw was on for the SPY and QQQ, both of which saw a selloff the first hour followed by a strong rally until noon and another selloff the hour after that. Meanwhile, DIA’s morning selloff was much smaller and its mid-morning rally was stronger and lasted longer. Then in the afternoon, things settled down as the wave got smaller in all three major index ETFs. This action gave us indecisive candles in the SPY and QQQ, but a more bullish candle in the DIA. All three remained well above their T-line (8ema). SPY printed a white-bodied Spinning Top, QQQ printed a black-bodied Spinning Top, and Dia printed a white-bodied candle with no lower wick and a modest upper wick. This all happened on above average volume in the DIA as well as below-average volume in the SPY and QQQ.

On the day, six of the 10 sectors were green with Financial Services (+0.98%) well out in front leading the gainers higher. Meanwhile, Basic Materials (-0.39%) and Consumer Cyclicals (-0.33%) leading the losers lower. At the same time, SPY gained 0.32%, DIA gained 0.57%, and QQQ gained 0.03%. VXX dropped another 6.51% to close at 47.14 and T2122 dropped back a bit more toward the center of its mid-range at 65.04. On the bond front, 10-year bond yields fell a bit to 3.839% and Oil (WTI) fell another 1.61% to close at $77.09 per barrel. So, Wednesday was a bullish, but fairly volatile day with the mega-cap DIA leading the rest of the market higher. This came after what analysts called “encouraging” CPI data that was the lowest since March of 2021. (It might be of interest to note that prior to the CPI release, 47.5% of Fed Fund Futures expected a quarter point rate cut in September. At the end of the day, 64.5% are now expecting a quarter-point rate cut. In both cases, the entire remainder expects a half percent cut.)

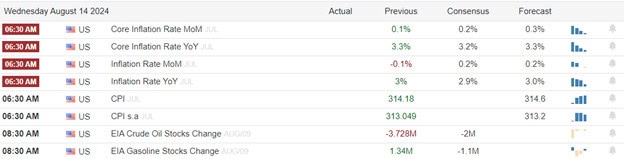

The major economic news scheduled for Wednesday were limited to July Core CPI (Year-on-Year) that was down a tick, as expected, at 3.2% (compared to a forecast of 3.2% and down slightly from June’s 3.3%). On the monthly basis, July Core CPI was actually up a tick as expected at +0.2% (versus a +0.2% forecast and June’s +0.1% reading). On the headline number, July CPI (Year-on-Year) was down more than was predicted at +2.9% (compared to a +3.0% forecast and prior month value). On the monthly basis, July CPI was up as predicted at +0.2% (versus a +0.2% forecast and the June -0.1% reading). Later, the EIA Weekly Crude Oil Inventories showed an unanticipated build of 1.357 million barrels (compared to a forecasted drawdown of 1.900 million barrels and the prior week’s 3.728-million-barrel drawdown).

After the close, CSCO reported beats on both the revenue and earnings lines. (CSCO also raised its forecasts and guidance, yet still announced cutting as many as 6,000 jobs.) Meanwhile, STNE beat on revenue while missing on earnings.

In stock news, on Wednesday, MU and Korea’s Samsung followed the third major computer memory manufacturer in raising prices by 15%-20%. At the same time private company Mars (of candy bar fame) announced they have agreed to buy K for $36 billion. Later, the CFO of UBS said the company would sell the CS mortgage servicing unit it acquired in the CS buyout. (No buyer or financial terms were mentioned.) At the same time, SHAK announced it has rolled out sidewalk robots to deliver orders in Los Angeles for those orders placed via the UBER Eats app. Later, SEC filings showed that INTC liquidated its stake in ARM during Q2, raising almost $147 million for the 1.18 million shares it sold. Meanwhile, as part of its earnings call, CSCO announced it will cut 7% of its global workforce. This is the company’s second round of cuts in 2024, having cut 5% (about 4,000 jobs) in February. At the same time, SEC filings showed that BRKB took new stakes un ULTA and HEI and increased its holdings of CB and SIRI during Q2. The same report stated that BRKB reduced its positions in COF and FND. Later, ALK flight attendants rejected the tentative contract deal the airline had struck with their union.

In stock legal and governmental news, on Wednesday, the state of TX added NWG to its list of “bad companies” that cannot do business with the state because they do not own oil and gas stocks. At the same time, LLY sent “cease and desist” letters to spas, telehealth companies, wellness centers, and doctors demanding that they stop selling unapproved “copycat” versions of LLY’s Zephound and Mounjaro weight loss and diabetes drugs. Later, D and EQNR were the winning bidders in the Dept. of Interior auction of offshore wind rights off DE, MD, and VA. At the same time, the FTC finalized its ban on companies buying or selling fake online reviews. The new rules give the agency the power to levy fines of up to $51,744 per violation. The rules were supported by AMZN, GOOGL, and YELP. (Surveys show the new rules are supported by 90% of online shoppers.)

Elsewhere, a federal judge in Kansas City has blocked a state of MO state rule barring financial professionals from considering so-called ESG factors in any investment advice. The rule had been supported by oil industry lobbyists. At the same time, the federal judge in the case brought by Epic Games (Fortnite maker) issued an order requiring the company to give Android phone users more ways to download apps. The judge expressed impatience with GOOGL’s stall tactics and protests about the cost and difficulty of implementing changes. He also said he will appoint a three-person “compliance committee” to determine GOOGL compliance with orders. Later, DIS filed “unique” (perhaps read that as preposterous) motion Wednesday, demanding that a wrongful death lawsuit be thrown out of court because the surviving spouse had signed up for a one-month trial of DIS+ years before the death. DIS claims the terms of that trial would bar a consumer from ever filing a lawsuit against the company. Later, the Committee on Foreign Investment fined TMUS $60 million for failing to prevent and report data breaches of sensitive data. (The agency scrutinizes national security risks of foreign investments and TMUS is majority owned by German DTEGY.)

Meanwhile, a DE judge upheld the $267 million legal fee request for legal firms that represented shareholders in the $1 billion settlement against DELL. (This was the largest-ever legal fee approved for a shareholder lawsuit.) After the close, the Dept. of Justice filed a motion urging the court to accept the BA revised plea deal including the company pleading guilty to a criminal conspiracy to commit charge and paying $243.6 million fine after breaching a 2021 deferred prosecution agreement. (Relatives of many of the 346 people killed in the two fatal 737 crashes that preceded the 2021 agreement have urged the plea be rejected.) Also after the close, the SEC and CFTC announced that another group of Wall Street firms have agreed to pay $470 million to settle charges they violated recordkeeping and communications rules (using off the record texting to communicate between firms). AMP, LPLA, RJF, BK, TD, LTSAP, and TFC were among the companies that settled.

Overnight, Asian markets were mostly green with just three of the 12 exchanges in the red. New Zealand (+1.10%), Shanghai (+0.94%), and Singapore (+0.90%) paced the gains while Taiwan (-0.60%) was by far the biggest loser. In Europe, the picture is even more green at midday with only one of 15 bourses in the red. The CAC (+0.02%), DAX (+0.32%), and FTSE (+0.06%) lead the region modestly higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a modest green start to the day here as well. The DIA implies a +0.21% open, the SPY is implying a +0.10% open, and the QQQ implies a +0.15% open at this hour. At the same time, 10-Year bond yields are up a bit to 3.845% and Oil (WTI) is up nine-tenths of a percent to $77.67 per barrel in early trading.

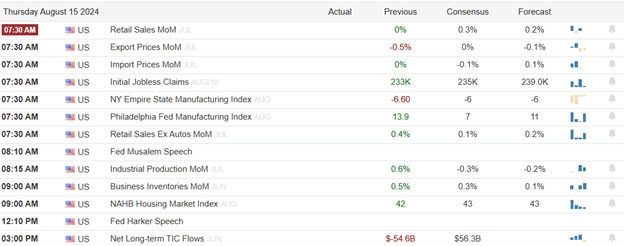

The major economic news scheduled for Thursday includes Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, July Core Retail Sales, July Export Price Index, July Import Price Index, NY Empire State Mfg. Index, Philly Fed Mfg. Index, Philly Fed Mfg. Employment Index, and July Retail Sales (all at 8:30 a.m.), July Industrial Production (9:15 a.m.), June Business Inventories and June Retail Inventories (10 a.m.), TIC Net Long-Term Transactions (4 p.m.), and the Fed Balance Sheet (4:30 p.m.). We also hear from Fed member Harker (1:10 p.m.). The major earnings reports scheduled for before the open include BABA, AIT, DE, GRAB, JD, NICE, SPTN, TPR, and WMT. Then, after the close, AMCR, AMAT, COHR, GLOB, and HRB report.

In economic news later this week, on Friday, July Building Permits, July Housing Starts, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations are reported.

In terms of earnings reports later this week, on Friday we hear from FLO.

So far this morning, DE, NICE, TPR, and WMT all reported beats on both the revenue and earnings lines. Meanwhile, BABA, AIT, GRAB, JD, and SPTN missed on revenue while beating on earnings. There were no tickers on the other side this morning. However, DDS missed on both the top and bottom lines.

In miscellaneous news, on Wednesday, Reuters reported that a potential seaport strike is looming in September that would impact East and Gulf Coast ports. The report cites a shipping industry expect saying the strike could back up and reroute cargo for weeks or potentially months. However, major importers such as WMT have been rushing their orders to get the shipments through the ports prior to the September 30 expiration of the current dockworkers contract. (Industry analysts say it takes about six days to clear the backlog caused by a one-day strike. So, a strike lasting weeks would delay both import and export shipments for months.) Elsewhere, Reuters reported that the US, which is one of the largest plastic producers in the world, will back a global treaty that calls for a reduction in plastic production.

In late-breaking news, WMT raised its guidance for the full year citing steady consumer health and the relative strength of the overall economy. WMT CFO Rainey said, “…our members and customers…remain choiceful, discerning, value-seeking, focusing on things like essentials rather than discretionary items, but importantly, we don’t see any additional fraying of consumer health.” Still, while raising its full-year 2024 forecast, the numbers do point to a second half that is not quite as strong as the first six months. They are just stronger than earlier predicted. Elsewhere, the Biden Administration released the prices for the first 10 drugs that resulted from the first-ever Medicare price negotiations. BMY, LLY, JNJ, MRK, AZN, NVS, AMGN, ABBV, and NVO are makers of those first 10 drugs subject to price negotiation and the White House says the lower prices will save Medicare $6 billion in the first year (based on 2023 drug demand data).

With that background, it looks as if markets are indecisively bullish again this morning. All three major index ETFs opened the premarket higher, but had all traded in an uncertain manner since then, producing more wick than body in all cases. All three are above their T-line (8ema) and the short-term trend is clearly bullish (or could be said to be in strong Bear Flag patterns). Meanwhile, the mid-term trend remains bearish, but with the downtrend line under pressure. In the long-term, while the bullish trend line is broken, the longer-term charts remain bullish. In terms of extension, the SPY and especially QQQ remain a little stretched above their T-line but the DIA is in better shape. At the same time, the T2122 indicator remains in its mid-range. So, the market has some room to run if either side can find the momentum (which has been on the Bulls side for a little over a week). However, the Bears have more slack to work with at this point. With regard to those 10 big dog tickers, eight of the 10 are in the green led by AMZN (+0.85%). However, the biggest dog, NVDA (-0.49%) paces the losers and is once again the dollar-volume trading leader. (This time only leading by a factor of 3.5.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Consumer Price Index

U.S. futures traded with a mix of anticipation and uncertainty, hovering around the flatline as investors awaited the release of the July Consumer Price Index (CPI) report. Scheduled for 8:30 a.m. ET, the CPI reading is expected by economists polled by Dow Jones to show a 0.2% increase from the previous month and a 3% year-over-year gain. This report follows a day after lighter-than-expected wholesale inflation figures provided a boost to stocks, adding to the market’s cautious optimism.

European stocks saw an uptick on Wednesday, driven by a mix of economic indicators and corporate performance. U.K. inflation rose to 2.2% in July, slightly below expectations but surpassing the Bank of England’s 2% target, signaling potential monetary policy adjustments. Swiss bank UBS experienced a notable increase of 2.95% after significantly exceeding net profit forecasts for the second quarter, boosting investor confidence. Sector-wise, auto stocks gained 1.2%, reflecting positive market sentiment, while mining stocks declined by 0.7%, indicating sector-specific challenges.

Asia-Pacific markets experienced a positive trend on Wednesday, buoyed by significant economic and political developments. The Reserve Bank of New Zealand’s decision to cut benchmark lending rates provided a boost to investor confidence, while Japan’s Prime Minister Fumio Kishida’s announcement of his impending resignation in September added a layer of political uncertainty. Despite these events, the Bank of Japan’s quarterly survey revealed a decline in business sentiment, with the sentiment index for manufacturers dropping to +10 in August and the non-manufacturers index falling to +24.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include ARCO, EAT, CAE, CAH, DOLE, GLBE, MRX, PFGC, RSKD, SFL, SDHC, UBS, & WKHS. After the bell include CSCO, DLO, LITE, PYCR, & STNE.

News & Technicals’

Japanese Prime Minister Fumio Kishida’s decision to not seek reelection as leader of the ruling Liberal Democratic Party paves the way for new leadership in Japan, the world’s fourth-largest economy. Kishida’s tenure has been marred by a scandal involving his party and persistent deflationary pressures on the economy. His resignation opens the door for a successor to address these challenges and steer Japan towards a more stable and prosperous future. This transition marks a significant moment in Japanese politics, with potential implications for both domestic and international economic policies.

Intel has divested its 1.18 million share stake in British chip company Arm Holdings, as revealed in a recent regulatory filing. This move comes amid Intel’s ongoing restructuring and cost-cutting initiatives, aimed at enhancing its competitive edge in the rapidly evolving semiconductor industry. The sale of its stake in Arm Holdings reflects Intel’s strategic efforts to streamline operations and reallocate resources as it navigates the challenges posed by fierce competition in the chip market.

General Motors is facing a lawsuit from the state of Texas, as announced by Attorney General Ken Paxton. The lawsuit stems from an investigation initiated in June, which is examining whether several automakers, including GM, collected and sold large amounts of data without drivers’ consent. The technology in question was reportedly installed in most GM vehicles starting with the 2015 model year. According to Paxton, insurers could potentially use this data to make decisions about raising premiums, canceling policies, or denying coverage. This legal action highlights significant concerns about data privacy and the ethical use of technology in the automotive industry.

In July, U.K. inflation rose to 2.2%, slightly below expectations but surpassing the Bank of England’s 2% target, according to data from the Office for National Statistics. The increase was primarily driven by housing and household services, with gas and electricity prices falling less than they did a year earlier. This uptick in inflation highlights ongoing cost pressures in essential services, reflecting broader economic challenges and potential implications for future monetary policy adjustments.

Up, down, sideways, and whipsaws are all possible today as the market reacts to the July Consumer Price Index report. Emotions are high and there is a lot at stake for the technical patterns in the index charts. Keep in mind Thursday is a huge day economic data as well so the wild price swings may not be finished just yet.

Trade Wisely,

Doug

PPI Better Than Expected – CPI On Deck

Markets gapped up to start the day Tuesday on better-than-expected PPI data. SPY gapped up 0.64%, DIA opened 0.31% higher, and QQQ gapped up 1.03%. From there QQQ started a steady rally that lasted right into the close. Meanwhile SPY and DIA took an hour to find their feet before following QQQ in steady rallies that lasted all day as well. This action gave us large, gap-up, white-bodied candles in the SPY and QQQ. At the same time, DIA had a large, gap-up white-body candle with wicks at both ends (particularly at the bottom). DIA also crossed back above its T-line (8ema). This all took place on average volume in DIA and below-average volume in the SPY and QQQ.

On the day, nine of the 10 sectors were green with Technology (+2.54%) out in front leading the gainers higher. Meanwhile, Energy (-0.49%) was by far, by 1.21%, the weakest sector. At the same time, SPY gained 1.63%, DIA gained 1.02%, and QQQ gained 2.48%. VXX dropped another 7.93% to close at 50.42 and T2122 spiked all the way up to the top end of its mid-range at 72.94. On the bond front, 10-year bond yields fell to 3.848% and Oil (WTI) fell 2.00% to close at $78.45 per barrel. So, Tuesday was all Bulls, all the time after better-than-expected Producer Prices. However, after an initial gap higher, price just steadily climbed as traders were generally happy, but also waiting on Wednesday’s CPI data.

The major economic news scheduled for Tuesday included July Core PPI (Month-on-Month) came in flat at 0.0% (compared to a forecast of +0.2% and well down from the June +0.3% reading). At the same time, July PPI (Month-on-Month) also came in down at +0.1% (versus a forecast and June value of +0.2%). Then, after the close, the API Weekly Crude Oil Stocks report showed a much larger drawdown than predicted at -5.205 million barrels (compared to a forecasted -2.000 million barrel and the prior week’s +0.180 million barrels).

In Fed news, on Tuesday, Atlanta Fed President Bostic reiterated that he expects the FOMC to cut rates by the end of the year, saying that recent economic data has made him “more confident” inflation is on the right path. However, he also said that he was worried about cutting too soon. So, he called for “a little more data” (before cutting) to lower the risk that the Fed might need to reverse course after starting cuts. Bostic said, “If economy evolves as I expect, there would be a rate cut by the end of the year.” He added that (the Fed needs to) “see a little more data” (to ensure that the inflation trend is real). He continued, “It would be really bad if we cut rates and then had to raise them again” (after starting to cut rates). Bostic concluded, “I am willing to wait, but it’s coming … It is coming.”

In stock news, on Tuesday, CG agreed to buy BAX’s kidney-care unit Vantive for $3.8 billion. Later, SBUX hired the now-former CEO of CMG Niccol as its new CEO. At the same time, LMT and GD announced they have signed an agreement to jointly build solid rocket motors for missiles starting in 2025. (NOC and LHX have been the main suppliers of such components to the defense industry in the past.) Later, BA said it had achieved plane deliveries that were in-line with expectations. In July, BA delivered 43 aircraft, in-line with analyst expectations and flat year-on-year, but slightly below the CFO’s previous guidance that deliveries would be “on par with June’s 44 aircraft.” (BA’s main rival Airbus, EADSY, delivered 77 aircraft in July.)

Meanwhile, Reuters reported that BX is exploring the sale of its Clarion Events unit for roughly $2.6 billion. Later, FIT, GOOGL, and PTON announced a partnership to produce and sell fitness content. At the same time, Reuters reported that PARA will begin laying off 15% of its workforce (about 2,000 people) as it looks to cut costs and leverage AI technologies. (90% of the job cuts are expected to be complete by September.) Later, GOOGL unveiled new Pixel smartphones and other devices with deeper AI integration. (This product announcement is several months ahead of GOOGL’s traditional October launches as the company attempts to keep up with AAPL’s AI-integrated product introductions.) At the same time, TLRY announced it will buy four craft breweries from TAP for an undisclosed sum. After the close, ALL said it has agreed to sell its employer voluntary benefits business to StanCorp for $2 billion.

In stock legal and governmental news, on Tuesday, Poland signed a contract to buy 96 AH-64E Apache attack helicopters and related maintenance equipment from BA for $12 billion. Later, the NHTSA announced that GM is recalling 21,000 electric SUVs over anti-lock brake issues. However, GM said it will solve the issue via an over-the-air update. At the same time, F and MZDAF (Mazda) warned customers to avoid driving certain models still impacted by faulty Takata airbag inflators. F said 374,300 vehicles had yet to have the previously-announced recall resolved while MZDAF estimated 83,000 of its US vehicles were still not fixed. Later, INTC was sued by a Jewish former employee (VP of Engineering) who alleges that he was fired after complaining about a senior executive he believed was openly celebrating antisemitism.

Elsewhere, the US Dept. of Defense announced the US had approved a $20 billion weapons package for Israel, including BA F-15 fighter jets worth $19 billion. After the close, Bloomberg reported that the US Dept. of justice is mulling plans to seek the breakup of GOOGL after the agency’s recent court victory declaring GOOGL a monopoly and in violation of US antitrust law. The report cited unnamed sources who say the DOJ is considering demanding GOOGL sell its Android phone operating system and Chrome browser businesses. Also after the close, the state of TX sued GM, alleging the car company installed technology on more than 14 million vehicles to collect data about drivers to be sold to insurance companies. Meanwhile, FE agreed to pay the SEC and state of OH $20 million to avoid prosecution in relation to a $60 million bribery scheme.

Overnight, Asian markets were mixed but leaned toward the green with eight of the 12 regional exchanges posting gains. New Zealand (+2.06%, Taiwan (+1.06%), and South Korea (+0.88%) led the gainers. On the other side, Shenzhen (-1.17%) was by far the biggest loser. Meanwhile, in Europe, we see a much greener picture with only Belgium (-0.52%) in the red as opposed to 14 green bourses at midday. The CAC (+0.43%), DAX (+0.46%), and FTSE (+0.35%) lead the region higher in early afternoon trade. As of 7 a.m., US Futures are pointing toward a start just on the green side of flat ahead of CPI data. The DIA implies a +0.02% open, the SPY is implying a +0.04% open, and the QQQ implies a +0.05% open at this hour. At the same time, 10-Year bond yields are down to 3.83% and Oil (WTI) is down 0.31% to $78.11 per barrel in early trading.

The major economic news scheduled for Wednesday are limited to July Core CPI and July CPI (both at 8:30 a.m.), and EIA Weekly Crude Oil Inventories (10:30 a.m.). The major earnings reports scheduled for before the open include ARCO, EAT, CAE, CAH, DOLE, ESLT, ICL, PFGC, and UBS. Then, after the close, CSCO, and STNE report.

In economic news later this week, on Thursday, we get Weekly Initials Jobless Claims, Weekly Continuing Jobless Claims, July Core Retail Sales, July Export Price Index, July Import Price Index, NY Empire State Mfg. Index, Philly Fed Mfg. Index, Philly Fed Mfg. Employment Index, July Retail Sales, July Industrial Production, Jun Business Inventories, June Retail Inventories, TIC Net Long-Term Transactions, and the Fed Balance Sheet. We also hear from Fed member Harker. Finally, on Friday, July Building Permits, July Housing Starts, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations are reported.

In terms of earnings reports later this week, on Thursday, we hear from BABA, AIT, DE, GRAB, JD, NICE, SPTN, TPR, WMT, AMCR, AMAT, COHR, GLOB, and HRB. Finally, on Friday, FLO reports.

So far this morning, CAH, DOLE, ESLT, and UBS all reported beats on both the revenue and earnings lines.

In mortgage news, interest rates fell to the lowest level in more than a year last week as the national average 30-year, fixed-rate, conforming loan rate fell to 6.54%. As a result, applications for refinance loans surged 35% compared to the prior week and were up a massive 118% versus the same week in 2023. On the new home front, new purchase applications rose just 3% for the week and were still down 8% from the same week in 2023. Even with the disparity in demand growth, refinance loan applications only made up 48.6% of all mortgage applications on the week.

In miscellaneous news, on Tuesday, the US Dept. Agriculture announced expanding the testing for bird flu among beef at slaughterhouses. 200 US herds have tested positive for the avian flu since March with one sample found in a slaughterhouse. At the same time, overseas, Chinese lending fell to a 15-year low in July as banks gave out just $36.28 billion in new loans according to the People’s Bank of China. This was down 88% from June and far below the average analyst estimate. (July is traditionally a slow loan demand month, but the miss was very large.) Back in the US, the National Federation of Independent Business said its Small Business Optimism Index (survey results) rose to 93.7. This was the highest reading, indicating the best small business sentiment in more than 2.5 years.

With that background, it looks as if markets are uncertain ahead of CPI data this morning. All three major index ETFs opened roughly flat and have printed indecisive (mostly wick) black-bodied candles since that point. (It is earlier than I normally report.) All three are above their T-line (8ema) and the short-term trend is clearly bullish (or could be said to be in strong Bear Flag patterns). Meanwhile, the mid-term trend remains bearish, but with the downtrend line under pressure in the QQQ. In the long-term, while the bullish trend line is broken, the longer-term charts remain bullish. In terms of extension, the SPY and especially QQQ are getting a little stretched above their T-line but the DIA remains in good shape. At the same time, the T2122 indicator is back toward the top end of its mid-range. So, the market has some room to run if either side can find momentum. However, the Bears have more slack to work with at this point. With regard to those 10 big dog tickers, six of the 10 are in the green led by the biggest dog, NVDA (+1.57%), once again also leads on the dollar-volume traded. (This time leading by a factor of five.) On the other side, GOOGL (-1.41%) is way out front pacing the losses after the overnight news that the DOJ is considering asking to have the monopoly company broken up.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Premarket Flatish With PPI Ahead

Monday started with a gap higher. SPY gapped up 0.24%, DIA gapped up 0.21%, and QQQ gapped up 0.19%. From there, all three major index ETFs rode the whipsaw in descending-magnitude waves and a slight bearish trend the rest of the day. This action gave us a gap-up black-bodied Spinning Top in the SPY, a gap-up, white-bodied Doji-type candle in the QQQ, and a gap-up, black-bodied Bearish Engulfing candle in the DIA. That meant that DIA retested and failed its T-line (8ema) while SPY and QQQ both retested and passed (stayed above) their own T-lines. This happened on lower-than-average volume in all three major index ETFs.

On the day, eight of the 10 sectors were red with Communication Services (-0.76%) leading the way lower. Meanwhile, the biggest mover was Energy (+0.95%) and by far the leader of the two sectors that held up best. At the same time, SPY gained 0.05%, DIA lost 0.34%, and QQQ gained 0.22%. VXX fell another 1.83% to close at 54.76 and T2122 fell back into the top of the oversold territory at 18.18. On the bond front, 10-year bond yields fell to 3.905% and Oil (WTI) spiked another 3.62% on Middle East war fears to close at $79.62 per barrel. So, Monday was a whipsaw day with violent whips the first two hours of the day and then continuingly decreasing waves the rest of the day. In general, it felt like a waiting day with traders wanting to see Tuesday’s PPI data.

The major economic news scheduled for Monday includes NY Fed 1-Year Consumer Inflation Expectations, which came in flat at 3.0% (the same as June’s 3.0% reading). In addition, the Fed report showed a big drop in the medium-term (3-Year) inflation expectations from 2.9% in June to 2.3% in July. However, the longer-term (5-Year) expectations stayed flat (the same way 1-Year expectations had) at 2.8%. Later, the Fed Budget Balance came in lower than expected at -$244.0 billion (versus the -$254.3 billion forecast but far above June’s -$66.0 billion).

After the close, AGRO and SLF missed on revenue while beating on earnings. On the other side, PACS beat on revenue while missing on earnings.

In stock news, on Monday, Canadian bank BNS announced it is buying a 14.9% stake in US regional bank KEY for $2.8 billion ($17.17 per share). Later, both S&P and MCO (Moody’s) downgraded JBLU credit rating after JBU announced plans to raise $3 billion in debt. (JBLU intends to use its flier rewards program as collateral for the new debt.) Meanwhile, BAC CEO Moynihan told CBS that he is urging the Fed to “consider lowering rates to prevent a potential economic downturn.” (He said he is basing that request on seeing BAC customers spending at a 3% growth rate in July and August, which is half as fast as the July-August spending increase in 2023.) On the other hand, UBS reported that their research indicates that the probability of a US recession fell from just a few months ago.

Elsewhere, CVX announced Monday that it has begun production in the world’s first “ultrahigh pressure” oil field. The field, located under US waters in the Gulf of Mexico is now set to open up many deep-sea oilfield projects that are only accessible using 20,000 pounds per square inch of pressure. The single well platform opened Monday will produce 75k barrels of oil and 28 million cubic feet of natural gas per day for the next 30 years. (However, the project did cost $5.7 billion and nobody has ever operated at those pressures, let alone over long periods of time.) BP hoped to match the CVX feet by 2029. Later, after the close, XOM laid off 59 employees as it begins the job cuts related to the acquisition of Pioneer Natural Resources.

In stock legal and governmental news, on Monday, GOOGL announced that it is deactivating Russian-based AdSense (advertising) accounts. The search giant said its decision was due to “the ongoing developments in Russia.” However, some analysts said this was a response to Russia slowing down YouTube service in that country. Later, Bloomberg reported JNJ now has the support of 75% of the tens of thousands of lawsuit plaintiffs to propose the $6.5 billion talc settlement for court approval. (75% is the US Bankruptcy Court approval standard.) If the story is true, the court could impose the settlement terms on all of the 61,000 claimants. Later, the TX Attorney General announced his office has formally launched an election year investigation into CNP (Houston electrical utility) related to “fraud and waste” in the wake of the Hurricane Beryl power outages.

Elsewhere, Bloomberg reported Monday that its own investigation has uncovered that store-brand versions of Mucinex Extended Release sold at WBA, CVS, TGT, and WMT contain cancer-causing agent Benzene. The report says the news agency information has been sent to the FDA. However, neither the agency nor any of the retailers would comment for the report. Meanwhile, the Biden Administration announced new proposed rules aimed at reducing consumer wait times, cumbersome forms, and hard-to-cancel subscriptions. The FTC has begun accepting comments on the proposed rules while the FCC is already moving toward a similar settlement with the major telecom providers. The Dept. of HHS said it will introduce similar rules for major healthcare and insurance providers in the near future as well.

Overnight, Asian markets were nearly green across the board. Only India (-0.85%) kept the Bulls from a clean sweep. Among the gainers, Japan (+3.45%) was far out front, followed by Singapore (+0.72%) and Shenzhen (+0.43%) leading markets higher. In Europe, the picture is much more dour at midday with only four of 15 exchanges in the green. The CAC (-0.19%), DAX (-0.03%), and FTSE (-0.08%) are typical of the modestly red trading in the region in the early afternoon. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a mixed and modest start to the morning. The DIA implies a -0.08% open, the SPY is implying a +0.18% open, and the QQQ implies a +0.28% open at this hour. At the same time, 10-Year bond yields are down to 3.904% and Oil (WTI) is off a quarter percent to $79.88 per barrel in early trading.

The major economic news scheduled for Tuesday includes July Core PPI and July PPI (both tat 8:30 a.m.) and API Weekly Crude Oil Stocks report (4:30 p.m.). In addition, Fed member Bostic speaks at 1:15 p.m. The major earnings reports scheduled for before the open include Tuesday, HD, JHX, MLCO, ONON, SE, and TME. Then, after the close, CIG, FNV, and NU report.

In economic news later this week, on Wednesday, July Core CPI, July CPI, and EIA Weekly Crude Oil Inventories report. On Thursday, we get Weekly Initials Jobless Claims, Weekly Continuing Jobless Claims, July Core Retail Sales, July Export Price Index, July Import Price Index, NY Empire State Mfg. Index, Philly Fed Mfg. Index, Philly Fed Mfg. Employment Index, July Retail Sales, July Industrial Production, Jun Business Inventories, June Retail Inventories, TIC Net Long-Term Transactions, and the Fed Balance Sheet. We also hear from Fed member Harker. Finally, on Friday, July Building Permits, July Housing Starts, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations are reported.

In terms of earnings reports later this week, on Wednesday, ARCO, EAT, CAE, CAH, DOLE, ESLT, ICL, PFGC, UBS, CSCO, and STNE report. On Thursday, we hear from BABA, AIT, DE, GRAB, JD, NICE, SPTN, TPR, WMT, AMCR, AMAT, COHR, GLOB, and HRB. Finally, on Friday, FLO reports.

So far this morning, HD, JHX, and TLN reported beats on both the revenue and earnings lines. Meanwhile, SE beat on revenue while missing on earnings. However, ONON and TME missed on both the top and bottom lines.

In miscellaneous news, on Monday afternoon there was a 4.4 magnitude earthquake in Los Angeles (centered about 7.5 miles Northeast of downtown LA). Fortunately, there were no immediate reports of structural or infrastructure damage. At the same time, Bloomberg reported foreign investment in China has fallen again this year, resulting in a net outflow. Elsewhere, in Russia, Putin replaced the Chief of his General Staff (head of military) Gerasimov with the head of the FSB (successor to KGB) Bortnikov. The move came after Ukrainian President Zelenskyy held a public staff meeting in which the Ukrainian military claimed they now control 1000 sq. km. of Russia’s Kursk region after seven days of their attack into the invader’s own country. Finally, in China, Bloomberg reports that Beijing has ordered rural banks to not settle recent bond purchase transactions as the central authorities attempt to control the country’s bond market rally. (In other words, Beijing is trying to force money into stocks.)

With that background, it looks as if markets are uncertain ahead of PMI data. All three major index ETFs gapped higher to start the premarket. However, all three have also sold off since then, printing black-bodied candles in the early session and taking price back to one or the other side of flat. DIA retested and has so far failed the retest of its T-line (8ema) while the SPY and QQ remain above their own T-line. The very short-term trend remains bullish while the mid-term trend is bearish. In the long term, while the bullish trend line is broken, the longer-term charts remain bullish. In terms of extension, all three major index ETFs are now back to being close to their T-line (8ema). At the same time, the T2122 indicator is back into the top of its oversold range. So, the market has some room to run if either side can find momentum. However, the bulls have slightly more slack to work. With regard to those 10 big dog tickers, nine of the 10 are in the green led by the biggest dog, NVDA (+1.61%), which also leads on the dollar-volume traded by a factor of six. TSLA (-0.28%), which is usually the second heaviest dollar-volume traded stock is the only red in the group, but is also working on very low dollar volume compared to the normal premarket.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Key Inflation Data

U.S. stock futures climbed early Tuesday as investors eagerly anticipated the release of key inflation data this morning. The focus is on the producer price index (PPI), a critical measure of wholesale prices, which is scheduled for release at 8:30 a.m. ET. According to Dow Jones consensus estimates, the PPI is expected to show a monthly increase of 0.2% in July, mirroring the previous month’s growth.

European stocks saw an uptick on Tuesday, maintaining a cautiously positive trend following last week’s volatility. The latest data from the U.K.’s Office for National Statistics revealed that wages, excluding bonuses, increased by 5.4% year-on-year between April and June, marking the slowest growth rate in two years. Additionally, the unemployment rate dropped to 4.2% from 4.4%, defying economists’ expectations of a rise to 4.5%, as per a Reuters poll.

Asia-Pacific markets experienced a general uptick, reflecting investor optimism despite a turbulent session in the U.S. overnight. This volatility in the U.S. was largely due to anticipation surrounding the upcoming release of the U.S. consumer price index (CPI) for July, a crucial metric for gauging the health of the U.S. economy. Meanwhile, in Asia, market participants were busy analyzing Japan’s producer price index data and Singapore’s second-quarter GDP growth figures, both of which are significant indicators of economic performance in the region.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include HD, HBM, HUT, HUYA, HIS, JHX, LOAR, MLCO, MRSN, MSGS, ONON, PSFE, SE, SLF, TLN, & TME. After the bell include DUOT, FNV, IBTA, INTA, KYTX, MRCY, NATL, NPCE, NU, USPH, & XP.

News & Technicals’

Share transactions in China have plummeted to their lowest level in over four years, driven by a fervent local bond rally amidst a weakening economy. The world’s second-largest stock market is on course for its fourth consecutive year of losses, exacerbated by an unprecedented housing crisis that has severely restricted investors’ options. This situation has led to a surge in demand for government bonds, raising concerns among regulators. Historically, similar episodes in China have triggered panic-driven selling, pushing the market to new lows, and the current scenario appears to be following this troubling pattern.

Shares of Home Depot dropped over 2% in premarket trading after the home improvement retailer issued a warning about weaker-than-expected sales for the second half of 2024. The company now anticipates full-year comparable sales to decline by 3% to 4%, a significant adjustment from its earlier forecast of a roughly 1% decrease. This revised outlook has raised concerns among investors about the company’s performance and the broader economic environment affecting consumer spending.

Carry trades, a popular foreign exchange strategy where investors borrow in low-interest currencies like the Japanese yen to invest in higher-yielding assets, have gained significant traction in recent years. This popularity stemmed from expectations that the yen would remain cheap and Japanese interest rates would stay low. However, this trend took a sharp turn last week when the Bank of Japan’s interest rate hikes strengthened the yen, triggering an aggressive unwinding of yen-funded carry trades. This sudden shift led to a dramatic sell-off in global markets, highlighting the volatility and risks associated with such strategies.

The Social Security Administration (SSA) is grappling with a “record-breaking backlog” of open cases, which has resulted in an estimated $1.1 billion in improper payments to beneficiaries, according to a recent report from the SSA Office of the Inspector General. This backlog has highlighted significant challenges within the SSA, with experts emphasizing the urgent need for increased budgetary funding to address what they describe as a “customer service crisis.” The situation underscores the critical importance of adequate resources to ensure timely and accurate service delivery to beneficiaries.

The wait for the key inflation data of the PPI report. The question now, will it inspire the bulls or bears? We should also consider the possibility of a sideways move as we wait for the more important CPI numbers on Wednesday. That said, be prepared for anything including gaps and big point whipsaws as the market reacts.

Trade Wisely,

Doug

Monday Starts Modestly Green

Markets opened modestly lower Friday. SPY opened down 0.16%, DIA opened down 0.09%, and QQQ opened down 0.34%. From there, all three of the major index ETFs meandered back-and-forth around the opening gap until 12:30 p.m. Then the market saw a sharp rally for a little over an hour, followed by a weaker selloff for an hour, with all three then drifting modestly bullishly the rest of the day. This action gave us small gap-down, white-bodied candles, with wicks at both ends in SPY, DIA, and QQQ. DIA was a prototypical Spinning Top candle. All three crossed back above their T-line (8ema), although DIA only did so by a dime. This happened on average volume in DIA and QQQ as well as less-than-average volume on the SPY.

On the day, nine of the 10 sectors were green with Technology (+0.57%) and Financial Services (+0.56%) out front leading the others higher. Meanwhile, Industrials (-0.10%) was the only sector in the red (barely). At the same time, SPY gained 0.44%, DIA gained 0.16%, and QQQ gained 0.52%. VXX plummeted 12.12% to close at 55.78 and T2122 fell but remained in its mid-range at 38.79. On the bond front, 10-year bond yields fell to 3.94% and Oil (WTI) popped another 1.04% to close at $76.98 per barrel. So, Friday was a meandering day with less energy that the other days in the week. As a result, the magnitude of the whipsaws Friday was muted.

This action ended a tumultuous week that started with a huge gap lower and featured heavy volatility, especially early in the week. That said, the week ended as “much ado about nothing” as stocks rallied back from the huge INTC-inspired gap lower Monday. SPY ended the week up 0.02% after trading in nearly a 5% range during that time. DIA did end the week 0.50% lower after having been down more than 3% at one point. And QQQ was the show-stealer, closing the week up 0.37% after having been down 5.59% at one point and trading in almost a 7% range for the 5-days.

There was no major economic news scheduled for Friday. In addition, there were no earnings reports after the close Friday.

In Fed speak news, on Saturday, Fed Governor Bowman softened her normal very hawkish tone. She noted “welcome” evidence of inflation reduction and seemed to indicate rate cuts will be needed if inflation stays on a downward trajectory. Bowman said, “Should the incoming data continue to show that inflation is moving sustainably toward our 2% goal, it will become appropriate to gradually lower the federal funds rate to prevent monetary policy from becoming overly restrictive on economic activity and employment.” The prepared remarks were delivered to a Kansas City Banking Assn.

In stock news, on Friday, STLA announced it is planning to lay off 2,450 US workers later this year as it plans to end production of the “Ram 1500 Classic” truck. (Layoffs may begin as soon as October 8.) Later, SBUX gained on a Wall Street Journal report that activist fund Starboard Value had taken a significant position in the company. At the same time, BA announced it had been awarded a $2.56 billion contract from the USAF for the development of two rapid prototypes of airborne warning and control aircraft. Later, after the close, C announced it has initiated a process to sell its Trust Services business unit. (No details were provided.) On Saturday. Reuters reported that CSCO will cut thousands of more jobs in a second round of layoffs this year. (CSCO laid off 4,000 employees in February.) Also on Saturday, TSLA stopped taking orders for the cheapest version of its Cybertruck ($61k) and not only has the $100k version available for sale.

In stock legal and governmental news, on Friday, the NHTSA announced it had opened an investigation into 330k HYMTF (Hyundai) vehicles over potentially faulty seatbelts. At the same time, the SEC announced it had reached settlements with the CEO of IDEX and two of the company’s former executives related to securities fraud and misleading financial reporting. Later, JPM asked a federal judge in Manhattan to dismiss its case against Russian VTB Bank, which was seeking to recover $439.5 million in accounts frozen after Russia’s invasion of Ukraine. JPM said it was being coerced to request the dismissal by a Russian injunction on JPM and fear of what retaliatory action would take place if the suit was not dropped. At the same time, META won an appeal by RFK Jr.’s anti-vax group which had been alleging censorship due to META’s policy against the spread of misinformation.

Overnight, Asian markets were mixed but leaned toward the green with eight of the 12 exchanges in positive territory. Taiwan (+1.42%) and South Korea (+1.15%) led the gainers while Singapore (-0.81%) paced the losses. In Europe, with the sold exception of Belgium (-0.18%) we see green across the board at midday. The CAC (+0.05%), DAX (+0.28%), and FTSE (+0.59%) lead the region higher in early afternoon trade. In the US, as of 7:45 a.m., Futures are pointing toward a modestly green start to the day. The DIA implies a +0.13% open, the SPY is implying a +0.20% open, and the QQQ implies a +0.22% open at this hour. At the same time, 10-Year bond yields are back up to 3.955% and Oil (WTI) is up another 1.09% to $77.68 per barrel in early trading.

There is no major economic news scheduled for Monday includes NY Fed 1-Year Consumer Inflation Expectations (11 a.m.), the WASDE Ag report (noon), and Fed Budget Balance (2 p.m.). The major earnings reports scheduled for before the open include GOLD, CEPU, FTRE, and BEKE. Then, after the close AGRO, PACS, AND SLF report.

In economic news later this week, on Tuesday we get July Core PPI, July PPI, and API Weekly Crude Oil Stocks report. In addition, Fed member Bostic speaks. Then Wednesday, July Core CPI, July CPI, and EIA Weekly Crude Oil Inventories report. On Thursday, we get Weekly Initials Jobless Claims, Weekly Continuing Jobless Claims, July Core Retail Sales, July Export Price Index, July Import Price Index, NY Empire State Mfg. Index, Philly Fed Mfg. Index, Philly Fed Mfg. Employment Index, July Retail Sales, July Industrial Production, Jun Business Inventories, June Retail Inventories, TIC Net Long-Term Transactions, and the Fed Balance Sheet. We also hear from Fed member Harker. Finally, on Friday, July Building Permits, July Housing Starts, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations are reported.

In terms of earnings reports later this week, on Tuesday, we hear from HD, JHX, MLCO, ONON, SE, TME, CIG, FNV, and NU. Then Wednesday, ARCO, EAT, CAE, CAH, DOLE, ESLT, ICL, PFGC, UBS, CSCO, and STNE report. On Thursday, we hear from BABA, AIT, DE, GRAB, JD, NICE, SPTN, TPR, WMT, AMCR, AMAT, COHR, GLOB, and HRB. Finally, on Friday, FLO reports.

So far this morning, GOLD and BEKE reported beats on both the revenue and earnings lines. However, FTRE missed on both the top and bottom lines.

In miscellaneous news, on Friday, the CFTC said that short bets on 5-Year Treasury Bond Futures were now the largest on record. The report stain almost 1.7 million contracts of short bets were in place as of the week ending Aug. 6. (Two-Year and 10-Year Bond Future short bets also increased during the week, but were not at record levels.) Elsewhere, the state of MI reported a human case of Swine Flu on Friday. (The source of exposure is still under investigation and no word on patient outcome was given.) Meanwhile, Sunday was the 900th day of Russia’s invasion of Ukraine (if you do not count the 2014 invasion that stole Crimea and parts of Eastern Ukraine) and the 6th day of the Ukrainian invasion of the Kursk oblast of Russia.

With that background, it looks as if markets are tepidly bullish again early today. All three major index ETFs made a modest gap higher to start the premarket. Since then, SPY and DIA have printed white-body, small-wick candles while QQQ had printed a black-body, mostly-wick candle. All three are back above their T-line (8ema) and the short-term trend remains bullish. However, the mid-term trend is bearish. Still, while the bullish trend line is broken, the longer-term charts remain bullish. In terms of extension, all three major index ETFs are now back to being close to their T-line (8ema). At the same time, the T2122 indicator is back into the mid-range. So, the market has some room to run if either side can find momentum. With regard to those 10 big dog tickers, eight of the 10 are in the green led by the biggest dog, NVDA (+0.79%), which also leads by far on the dollar-volume traded as usual, and AMZN (+0.78%). The second-largest dollar volume trader is TSLA (-0.30%), which is also the biggest loser in premarket.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Pending Inflation Data

U.S. equity futures remained nearly unchanged on Monday as investors prepare for pending inflation data following Friday’s relief rally. Callie Cox, chief market strategist at Ritholtz Wealth Management, noted that high emotions and clustered market swings could lead to another turbulent week. Investors are particularly focused on the upcoming July producer price index report, with the consumer price index set to follow on Wednesday, both of which are expected to significantly influence market sentiment and trading strategies.

European stocks began the new trading week on a positive note, initially rising before paring some of their earlier gains. Investors are closely watching for indications that the market turbulence from the previous week has subsided. The financial services and insurance sectors were among the top performers, each advancing by approximately 0.6%. This week, market participants are particularly focused on upcoming inflation data from the U.S. and U.K., which are expected to play a significant role in shaping market sentiment and investment decisions.

Asia-Pacific markets experienced a positive start to the week, with most indices showing gains on Monday. This comes after a tumultuous week marked by significant selloffs and a subsequent sharp recovery, particularly in Japanese stocks. Investors are now turning their attention to upcoming economic indicators from India, specifically inflation and industrial output data, which are expected to be released later in the day. These figures will likely influence market sentiment and trading strategies moving forward.

Economic Calendar

Earnings Calendar

Notable reports for Monday before the bell include BLDP, ESPR, FTRE, BEKE, & MNDY. After the bell include ALC, DHT, KGS, PACS, & RUM.

News & Technicals’

Veteran investor David Roche anticipates a bear market in 2025, driven by factors such as smaller-than-expected rate cuts, a decelerating U.S. economy, and an AI bubble. He predicts these elements could lead to a market decline of around 20%, potentially beginning at the end of this year. However, Roche also notes that the Federal Reserve will have the flexibility to adjust in response to these economic challenges.

The Pentagon has deployed a guided missile submarine, and a carrier strike group equipped with F-35C fighter jets to the Middle East, citing the need to bolster U.S. military presence and capabilities in response to rising regional tensions. This move follows a statement from Iran’s leadership vowing retaliation against Israel after the assassination of Hamas’ former political chief, Ismail Haniyeh, in Tehran on July 31. The Pentagon’s actions underscore the escalating conflict and the U.S.’s commitment to maintaining stability in the region.

The Biden Administration has launched a comprehensive, multi-agency regulatory initiative aimed at curbing corporate practices that are perceived to waste consumers’ time and impose unnecessary bureaucratic hurdles. White House domestic policy advisor Neera Tanden highlighted that these practices often involve companies delaying services or making it excessively difficult for consumers to cancel services, thereby retaining customers’ money for extended periods. Central to this new effort are a series of rulemakings by the Consumer Financial Protection Bureau, which aim to address and mitigate issues related to customer service “doom loops” and the use of chatbots.

U.S. short seller Hindenburg released a report on Saturday alleging that Madhabi Puri Buch, the chair of the Securities and Exchange Board of India, had previously invested in offshore funds also utilized by the Adani Group. In response, Buch dismissed the claims as baseless. According to the report, Adani Group companies experienced a significant market impact, losing approximately $2.4 billion in value on Monday.

There is a good chance of a choppy hurry up and day with the markets highly anticipating the Tuesday PPI and Wednesday CPI reports. Earnings numbers will decline sharply by mid-week removing a major source of inspiration and price volatility. However, the economic data this week could keep the wild whipsaws going as the market reacts to the results.

Trade Wisely,

Doug