Bears Owned Thursday, Bulls Look To Rebound

Mr. Market gave us a Bull trap on Thursday on all-day profit-taking after a strong two-week rally. The SPY gapped up 0.33%, DIA opened 0.18% higher, and QQQ gapped up 0.48%. However, that was pretty much it for the Bulls for the day. From there all three major index ETFs sold off the rest of the session. This action Black-bodied, Bearish Engulfing candles in all three. However, all three of them also remain above their T-line (8ema). It also gave us a higher high in the SPY, DIA, and QQQ. Still, once again this took place on below average volume in all three major index ETFs.

On the day, nine of the 10 sectors were in the red with Technology (-1.82%) way out front leading the others lower. On the other side, Financial Services (+0.09%) held up better than the others and was the only green sector. Meanwhile, SPY lost 0.78%, DIA lost 0.37%, and QQQ lost 1.59%. VXX popped 4.20% to close at 48.86% and T2122 dropped back out of its overbought territory and back into the top end of its mid-range to close at 73.58. On the bond front, 10-year bond yields popped to 3.865% and Oil (WTI) popped another 1.42% to close at $72.94 per barrel. So, Thursday we had reversal (or more likely a profit-taking day ahead of Fed Chair Powell’s presentation set for Friday at 10 a.m.

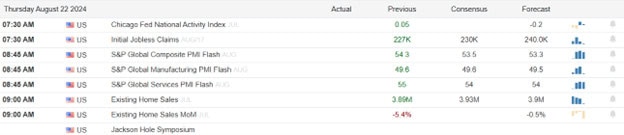

The major economic news scheduled for Thursday included Weekly Initial Jobless Claims, which were just as expected at 232k (compared to a 232k forecast and up just a bit from the prior week’s 228k). At the same time, Weekly Continuing Jobless Claims came in up but still below expectations at 1,863k (versus the 1,870k forecast and the prior week’s 1,859k). Later, S&P Global Mfg. PMI was a bit light at 48.0 (compared to a 49.5 forecast and the July 49.6 reading). At the same time, S&P Global Services PMI were a bit stronger than predicted at 55.2 (versus the 54.0 forecast and the July 55.0 value). This gave us an S&P Global Composite PMI that was also better than anticipated at 54.1 (compared to the 53.2 forecast and July’s 54.3 reading). Later, the July Existing Home Sales were slightly better than predicted at 3.95 million (versus a forecast of 3.94 million and up from June’s 3.90 million number). Then, after the close, the Fed Balance Sheet showed a $16 billion increase on the week, rising from $7.178 trillion to $7.194 trillion. (Note: The Fed balance sheet reduction or QT caused some market disruption when first started. The Fed then promised to stop QT prior to wider trouble taking shape. Since the ECB, Bank of Japan, and Bank of England have now all also started tightening, Bloomberg speculates the Fed is regulating its own balance sheet reduction to avoid trouble.)

In Fed news, the Jackson Hole Symposium began. Kansas City Fed President Schmid told CNBC that he has an open mind about rate cuts in September. Schmid said, “It bears looking harder at it (the unemployment rate). I’m going to let the data show where we lead (but) I would agree with several of my colleagues that you probably want to act maybe before (inflation) gets to two (percent) but that sustainability toward two I think is really important.” Later, Boston Fed President Collins indicated she feels it will soon be appropriate to cut interest rates. Collins said, “We’ve seen quite a lot of reduction in inflation. The reduction to me is consistent with more confidence that we are on that trajectory and with labor markets healthy overall, I do think that soon it is appropriate to begin easing.” She also seemed to signal that quarter-point rate cuts are the way to go, saying “I think a gradual, methodical pace once we are in a different policy stance is likely to be appropriate.” By mid-morning, Philly Fed President Harker told Reuters that as of now he is ready to cut rates in September. Harker said, “For me, barring any surprise in the data we’ll get between now and then, I think we need to start this (rate cut) process.”

After the close, BBAR, NDSN, SNOW, TBBB, URBN, and ZM all reported beats on both the revenue and earnings lines. Meanwhile, A, CAAP, and SNPS reported misses on revenue while beating on earnings. However, BMA missed massively on both the top and bottom line.

In stock news, on Thursday, Reuters reported that Japanese company Softbank is in serious talks to invest $684 million in SHCAY (Sharp electronics). At the same time, AMKAF announced it is evaluating but has not decided upon contingency strategies in Canada after the two top Canadian freight railroads (CP and CNI) locked out their employees and shut down operations Thursday. Later, research firm Jato Dynamics reported that BMWYY (BMW) overtook TSLA to become that largest-selling electric vehicle maker in Europe in July. At the same time, Bloomberg reported that CME and SPGI are in discussion about the sale of their OSTTRA joint venture. (Bloomberg says the joint venture is values between $2 billion and $4 billion.) Later, AAP announced it had struck a deal to sell its Worldpac unit to CG for $1.5 billion in cash. At the same time, WMT announced it has partnered with QSR (Burger King) to offer meal discounts to the retailers paying members. The move is designed to let WMT to better compete with AMZN Prime.

Meanwhile, F announced it had cancelled its planned 3-row electric SUV. (That vehicle had been scheduled to roll off assembly lines in 2025.) Later, the PARA buyout saga continued as private media veteran Bronfman raised his bid from $4.3 billion to $6 billion. At the same time, miners TECK and RIO joined the crowd of companies looking for alternatives after the Canadian rail shutdown. The two said they would need to truck some products and defer shipment on many commodities. (They mainly produce iron ore, aluminum ore, copper, and molybdenum in Canadian mines. The diamonds RIO mines there are not shipped by rail.) Later, Reuters reported that ELH is in talks with private equity firms TPG, KKR, and others over a potential sale. ELV (an insurer) is also among the suitors. At the same time, ACDVF (Air Canada) pilots voted to authorize a strike. (Any strike cannot take place prior to a 21-day “cooling off” period.) After the close, GM and UBER announced a multi-year partnership to deploy Cruise robotaxis on the UBER platform. (UBER already has a similar deal with GOOGL’s Waymo unit in Phoenix, AZ, which has been in operation since October.)

In stock legal and governmental news, on Thursday, the NHTSA announced that GM has agreed to recall 1,200 Cruise robotaxis over hard braking issues. Later, Reuters reported that AAPL will change how users choose browsers and other default apps (in the EU only) in response to European Digital Markets Act. (This will end the billions of dollars in fees GOOGL previously paid AAPL to have Chrome be the default browser on iPhones and iPads.) At the same time, a Washington DC Appeals Court ruled to revive an antitrust lawsuit against AMZN that had been brought by the district. The suit alleges that AMZN pricing policies (restrictions on third-party sellers and their own suppliers) illegally stifle competition. Later, GOOGL announced it has struck a “first in the nation” deal with the state of CA to fund newsrooms in the state in exchange for ending legislation that would have forced GOOGL and other tech giants to pay in order to distribute new content generated in the state. The plan calls for GOOGL to pay $15 million the first year, while the state will pay $30 million. During the next four years, CA’s contribution drops to $10 million per year while GOOGL’s increases to $20 million per year. (The deal was immediately criticized by journalists because it will help create AI tools to support journalists, which they feel will replace journalists with computers.)

Meanwhile, after the close, NASA said it expects to announce the decision on how the two-person BA Starliner crew will be brought back to earth on Saturday. The crew has been stranded at the International Space Station since the start of June after the glitchy Starliner leaked helium propellent before, during and after it travelled to the ISS. Also after the close, the Financial Times reported that AZN has warned it would seek to relocate its vaccine manufacturing site to the US (from the UK) amidst a negotiation deadlock with the UK over a planned cut in state aid. (The previous Conservative party administration had pledged $118 million in grants for the operation, but the new Labour government, which was left with a broken budget, has said it expects to cut the grants to $53 million under newly-required austerity measures.) Later, the NRLB determined that AMZN is a “joint employer” of subcontracted drivers who delivered packages for the company in CA. This ruling came after an unfair labor practices charge resulted in an investigation by the agency.

Overnight, Asian markets were mostly green on modest moves with just four of the 12 regional exchanges showing red. Thailand (+1.03%) was the outlier and leader of the gains while Malaysia (-0.36%) had the worst showing. In Europe, the picture is even brighter with just one bourse in the red against 14 in the green at midday. The CAC (+0.53%), DAX (+0.57%), and FTSE (+0.33%) lead the region higher in early afternoon trade. Meanwhile, in the US, at 7:30 a.m., Futures are pointing toward a gap higher to start the day. The DIA implies a +0.35% open, the SPY is implying a +0.51% open, and the QQQ implies a +0.75% open at this hour. At the same time, 10-Year bond yields have backed down to 3.848% and Oil (WTI) is up 1.3% to $73.96 per barrel in early trading.

The major economic news scheduled for Friday is limited to July Building Permits (8:30 a.m.), and July New Home Sales (10 a.m.). We also head from Fed Chair Powell at 10 a.m. as the Jackson Hole Symposium also continues. The major earnings reports scheduled for before the open include GFI. Then, after the close, there are no major earnings reports schedule.

So far this morning, UI missed on revenue while beating on earnings.

In miscellaneous news, on Thursday, the Equipment Leasing and Finance Assn. reported that US companies increased their borrowing to finance equipment in July. The report stated that July credit for equipment by US companies were up 11% from June’s $10 billion figure. Elsewhere, after the close, the Canadian government stepped in to end the freight rail shutdown in the country. The government ordered the railways and union to enter into binding arbitration. However, according to the AP, it’s uncertain how quickly the workers will return to work. Still, the Canadian Labour Minister said he expects the trains to be running again within days. CNI said they had ended their lockout within an hour of the government’s order. However, there was no word from CP as of 9 p.m. eastern.

With that background, all three major index ETFs gapped higher to start the premarket and have given us white body candles since then. QQQ is the most volatile of these, showing what looks like a fat-bodied Spinning Top at this point while the others have little wick. All three remain well above their T-line (8ema) and the short-term trend is still strongly bullish despite Thursday’s candle. Meanwhile, the mid-term bearish trend remains broken, though one could argue a new mid-term bullish trend has not formed yet (due to a lack of higher high to go with yesterday’s higher low). In the long-term, we are now clearly back in a Bull trend. In terms of extension, the pullback Thursday helped relieve much of the stretch above the index ETF T-lines. At the same time, the T2122 indicator has dropped back out of its overbought territory and is in the upper end of its mid-range. So, the market has room to run either direction. However, the Bears have more slack to play with Friday. Remember the mantra “follow, don’t lead, but also don’t chase” in mind. (In a volatile market, that may mean sitting on your hands.) With regard to those 10 big dog tickers, all 10 are in the green this morning, led by the biggest dog NVDA (+1.30%) and followed by the second-biggest dog TSLA (+1.067%). Meanwhile, NFLX (+0.43%) is the laggard. Finally, remember its Friday. So, prepare your account for the weekend news cycle and don’t forget to take profits. After all, Friday is payday.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service