As the corporate earnings season accelerates, stock futures fell in premarket trading on Tuesday. Investors are closely watching third-quarter earnings, with about 20% of the S&P 500 companies set to report their results this week. So far, approximately 14% of the companies in the index have shared their earnings. Despite being early in the season, there are concerns on Wall Street that expectations for corporate America might be too high. Megan Horneman, Chief Investment Officer at Verdence Capital Advisors, believes that 2025 estimates are overly optimistic, even after recent adjustments. She also noted that investors will be paying close attention to discussions on interest rates, inflation, and the overall economic outlook during this earnings season.

On Tuesday, European markets saw a decline as investors evaluated earnings reports from key companies across the region. Despite the overall downturn, technology stocks managed to rise by 0.8%, driven by a notable performance from SAP. The software giant’s shares surged over 5% to a record high following an upward revision of its revenue guidance, fueled by robust growth in its cloud business. Conversely, the utilities and telecom sectors were the day’s laggards, falling by 2.05% and 1.43%, respectively. Shipping giant Maersk initially saw its shares climb 3.3% after upgrading its full-year earnings forecast due to strong container demand, but the gains were short-lived as the stock reversed to close 1% lower.

On Tuesday, Asia-Pacific markets experienced a general downturn, with most indices closing in the red amid a light day for economic data from the region. Australia’s S&P/ASX 200 dropped 1.66% to 8,205.7, marking its lowest point in nearly two weeks. South Korea’s Kospi fell 1.31% to 2,570.7, and the small-cap Kosdaq saw a significant decline of 2.84%, reaching its lowest level in over a month. Japan’s Nikkei 225 decreased by 1.39% to 38,411.96, while the broader Topix index fell 1.06% to 2,651.47. In contrast, Hong Kong’s Hang Seng index edged up 0.12% in its final hour of trading, and mainland China’s CSI 300 rose 0.57% to close at 3,957.78.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include GE, VZ, MMM, AOS, AUB, BANC, CMCSA, CBU, DHR, DENN, FL, GATX, GPC, HRI, IVZ, KMB, MCO, ONB, PCAC, PNR, PM, PII, PHM, DGX, RTX, & SHW. After the bell reports include ADC, BKR, BDN, CNI, CSGP, EWBC, ENVA, ENPH, HIW, JBT, MANH, MTDR, NBR, NBHC, PKG, PFSI, RRC, ROIC, RHI, STX, LRN, TXN, TRMK, VMI, VBTX, & VICR.

News & Technicals’

On Tuesday, Russia is hosting the latest BRICS summit, welcoming its allies in a display of strength aimed at the West. Originally formed as a coalition of rapidly developing economies, the BRICS group—comprising Brazil, Russia, India, China, and South Africa—has evolved into a significant geopolitical forum. The group’s influence has further expanded with the addition of Egypt, Ethiopia, Iran, and the United Arab Emirates in January. Russian President Vladimir Putin often speaks of his vision for a “new world order” designed to challenge and potentially surpass the geopolitical and economic dominance of the U.S.-led Western world.

HSBC has announced a significant restructuring, introducing a new geographic setup, streamlined operations, and appointing its first female Chief Financial Officer. This marks the second major leadership change for the bank in recent months, following the appointment of former finance chief Georges Elhedery as CEO in July. The reorganization will see HSBC divided into four key divisions: Hong Kong, U.K., international wealth and premier banking, and corporate and institutional banking. This overhaul aims to enhance the bank’s operational efficiency and strategic focus across its global markets.

The U.S. government is in the final stages of reviewing measures aimed at restricting investments into China, particularly in sensitive technologies such as artificial intelligence. According to a recent update, the Treasury Department will soon require notifications for outbound investments into these areas. The final rules are expected to be released within the next week. The Treasury Department highlighted the potential risks to U.S. national security posed by the military, intelligence, surveillance, and cyber applications of these technologies, especially when developed by countries of concern like China.

The U.S. government is in the final stages of reviewing measures aimed at restricting investments into China, particularly in sensitive technologies such as artificial intelligence. According to a recent update, the Treasury Department will soon require notifications for outbound investments into these areas. The final rules are expected to be released within the next week. The Treasury Department highlighted the potential risks to U.S. national security posed by the military, intelligence, surveillance, and cyber applications of these technologies, especially when developed by countries of concern like China.

Gold has entered a new bullish phase, according to Paul Wong, market strategist at Sprott Asset Management. This surge is driven by factors such as increased central bank buying, rising U.S. debt, and a potential peak in the U.S. dollar. Wong’s comments follow gold’s recent climb to a record high of $2,700 per ounce. Many analysts are optimistic that this upward trend will continue, with some forecasting that gold prices could surpass $2,800 within the next three months.

The price volatility is likely to expand as the earnings season accelerates with about 15% of the SP-500 expected to report throughout the remainder of the week. Before establishing any new trade, it would be wise to check the earnings date before pulling the trigger. There is a growing concern that earnings estimates are to high so plan carefully and be prepared if reports happen to disappoint.

Markets opened lower on Monday prior to DIA diverging to the downside. SPY opened down 0.11%, DIA opened 0.05% lower, and QQQ gapped down 0.22%. At that point, QQQ rallied sharply to recross the opening gap and reach the high of the day at 10:20 a.m. before selling off sharply again, finding the low of the day at 11:30 a.m. From there, QQQ slowly rallied slowly back up across the gap before meandering sideways around Friday’s closing level and closing on the plus side. Meanwhile, after its open, SPY slowly meandered back up across the opening gap to find its high of the day at 10:20 a.m. Then it traded in-sync with QQQ, selling off hard to reach the low of the day at 11:35 a.m. and then slowly drifting higher but never quite getting back to its opening level. For its part, after the open, DIA immediately sold off sharply until 11:30 a.m. and then traded sideways along the lows the rest of the day. This action gave us divergent daily candles. SPY printed a black-body Doji that retested its T-line (8ema) and passed that test. DIA gave us a large, black-bodied candle that also retested its T-line and closed just barely above. Finally, QQQ printed a white-bodied candle (that retested and passed the test of its T-line) that was about half lower wick. This happened on below average volume in all three major index ETFs.

On the day, nine of the 10 sectors were in the red with Communication Services (-1.25%) out in front, leading the market lower. On the other side, Technology (+0.16%) was the only sector in the green. Meanwhile, SPY lost 0.16%, DIA lost 0.76%, and QQQ gained 0.19%. VXX was just on the plus-side of flat to close at 51.35 and T2122 dropped all the way back into the bottom third of its mid-range to close at 33.14. At the same time, 10-Year bond yields fell to close at 4.192% while Oil (WTI) climbed 1.68% to close at $70.38 per barrel. So, the Bulls were in-charge pretty much all day on what was also an indecisive day. NFLX (+11.09%) was among the leaders of this charge after its blowout earnings Thursday evening. (For the week, SPY gained 0.86%, DIA gain 0.91%, and QQQ gained 0.22%. This was the sixth-straight week of gains for all three major index ETFs.)

The major economic news scheduled for Monday was limited to the September US Leading Economic Indicators Index, which came in lower than expected at -0.5% (compared to a -0.3% forecast and a -0.3% August reading).

In Fed news, on Monday, Dallas Fed President Logan indicated she sees both more rate cuts and Balance Sheet shrinkage ahead. She said, “The economy is strong and stable, but, meaningful uncertainties remain in the outlook.” Logan continued, “If the economy evolves as I currently expect, a strategy of gradually lowering the policy rate toward a more normal or neutral level can help manage the risks and achieve our goals.” Regarding Quantitative Tightening, she said, “At present, liquidity appears to be more than ample” … “one sign liquidity remains in abundant supply, and not merely ample, is that money market rates continue to generally run well below the Fed’s interest on reserve balances rate.” She went on to say that the FOMC should be able to tolerate normal, temporary volatility in the money markets. However, she went on to say that, “reducing the (reverse repo) interest rate could incentivize participants to return funds to private markets.” However, Logan concluded by saying that getting mortgage bonds off the Fed Balance Sheet is “not a near-term issue in my view.” (i.e. not a massive priority).

Later, Minneapolis Fed President Kashkari said he also expects modest rate cuts ahead. Kashkari said, “Right now I see modest cuts over the next several quarters.” However, he also indicated that a weakening of the labor market might need to be met with stronger cuts. He said, “If we saw a weakening, like real evidence that the labor market is weakening quickly, then that would tell me, as one policymaker, ‘Hey, maybe we ought to bring down our interest rate more quickly than I currently expect,’” Kashkari continued, “We want to keep the labor market strong and we want to get inflation back down to our 2% target.” He then concluded with the normal Fed boiler plate statement that “interest rates will depend on the data.” Elsewhere, Kansas City Fed President Schmid said that he supports “a cautious and deliberate” approach to rate cuts. Schmid said, “While I support dialing back the restrictiveness of policy, my preference would be to avoid outsized moves, especially given uncertainty over the eventual destination of policy and my desire to avoid contributing to financial market volatility.” He continued, “Lowering rates in a gradual fashion would provide time to observe the economy’s reaction to our interest rate adjustments and give us the space to assess at what level interest rates are neither restricting nor boosting the economy.” Finally, San Francisco Fed President Daly said Monday that she has not seen anything to suggest the FOMC would stop cutting interest rates. She said interest rates are “absolutely still high enough that they are restraining the economy.”

After the close, BOKF, CADE, NUE, SAP, and ZION all reported beats on both the revenue and earnings lines. Meanwhile, AGNC, ARE, SIGI, and WTFC beat on the revenue line while missing on earnings. On the other side, MEDP and WRB missed on revenue while beating on earnings. However, TFII missed on both the top and bottom lines.

In stock news, on Monday, RCDOF announced it plans to divest its Defense business in order to focus on Environmental Consulting. (No details were announced, but they recently got a $385 million US Army contract extension that runs through 2027.) Later, XLMDF announced it has a conditional agreement to sell its North American business to SRAD for $30 million in cash ($20 million up front and up to $10 million based on unit performance). At the same time, SNY said it has entered exclusive talks to sell a 50% controlling stake in its consumer health unit to private equity firm Clayton Dubilier & Rice. (The unit had been valued at $17 billion earlier this year.)

Meanwhile, UBS announced it agreed to a deal to sell a 50% stake in the Swisscard business acquired in the CS acquisition to AXP. (The terms of the deal were not disclosed.) At the same time, DIS announced it will appoint former MS CEO Gorman as the new DIS Chairman in as of January. Later, SAN announced it has launched a digital bank in the US to help it fund over $30 billion in auto lending and broaden its retail banking reach in the US market. At the same time, shipping giant AMKAF (Maersk Moeller) raised its profit outlook on what it called a “strong shipping market.” Later, according to the Wall Street Journal, activist investor JCP Investment Mgmt., which has a 2% stake in the company, has issued a letter urging CAKE to spinoff three of its smaller brands (North Italia, Flower Child, and Culinary Dropouts).

In AI news, LUMN announced a strategic partnership with META aimed at increasing network capacity to support the META AI infrastructure. Later, HON announce it had signed a deal with GOOGL to bring the latter’s AI technology to the industrial data market. At the same time, IBM announced it launched a new AI model called Granite 3.0. (The model is open source, but IBM sells a paid version to be run on enterprise data centers.) Later, MSFT announced they will allow customers to build autonomous artificial intelligence agents using its Copilot Studio application starting in November. (This is a move to compete with CRM, which is already offering such AI agents for particular business tasks.) At the same time, QCOM announced that it is bringing chips designed for laptop CPUs to its mobile phone offerings. (The idea is to make phone processing more powerful to support AI.) Meanwhile, MEAT announced a batch of AI models, including one specifically created to check the quality of other AI models.

In stock legal and governmental news, on Monday, Nigeria blocked the SHEL sale of its entire Nigerian onshore and shallow-water operations for $2.4 billion. However, at the same time, Nigeria approved a similar deal for the sale of XOM’s operations for $1.28 billion. At the same time, the High Court of London ruled that BHP is “cynically trying to avoid responsibility” for Brazil’s worst environmental disaster (which came after a dam holding BHP mining waste collapsed). This came as the $47 billion lawsuit began its final phase with 600k Brazilians, 46 local governments, and about 2k Brazilian companies as the plaintiffs. (BHP had argued the case should be thrown out because it had paid almost $8 billion to everyone effected in Brazil.)

Elsewhere, LLY filed suit against three more medical spas (online vendors) of products that claim to contain the main ingredient of its popular Zepbound weight-loss medicine. At the same time, investment advisor WisdomTree Asset Mgmt. agreed to pay $4 million to settle SEC charges of misleading marketing of three funds (greenwashing). Later, movie studio Alcon Entertainment sued TSLA and WBD, alleging the defendants used images from the file “Blade Runner 2049” in the promotion of TSLA’s new cycbercab. Meanwhile, a bipartisan group of dozens of Congressmen (52 in total) urged the White house to toughen the sanctions on Russia and specifically questioned sanction exceptions for oilfield services firm SLB.

In miscellaneous news, on Monday, South Korea and Ukrainian intelligence services confirmed North Korea has sent 10k troops to fight on behalf of Russia. This includes some North Korean special forces troops. Elsewhere, the disgraced ex-President continued to spread lies and long-debunked conspiracy claims about FEMA hurricane relief efforts at campaign events in NC on Monday. (Once again, FEMA and NC officials had to try to correct the serial-liar’s spew in hope people will not forgo (and as was recently seen) even hinder the recovery.) Meanwhile, his opponent, Vice President Harris, called for an unspecified increase to federal minimum wage levels in campaign events in PA, MI, and WI. The events held alongside several Republican supporters (like former Congresswoman Liz Cheney), who support Harris but did not comment on Harris’ minimum wage call. At the same time, the FTC rule banning fake online reviews went into effect Monday. (The rules allow the agency to issue penalties of up to $51,744 per violation for knowing violations of the rule.) Finally, Germany’s six-month trial with a four-day workweek has ended. However, Bloomberg reports that many of the 45 businesses that participated in the experiment will not go back. (73% of the participating companies said they were prepared to either extend the experiment or make the change permanent.)

In Middle East news, on Monday, Israel continued its attacks on both Gaza and Lebanon. In the latter, Israel said it had bombed 32 targets ranging from the North of the country to the South. However, the largest batch of Israeli bombing strikes was in Beirut where numerous buildings were collapsed. This included the headquarters of what Israel (and the US) called Hezbollah’s bank (Al-Qard Al-Hassan, which translates to “benevolent loan”) which Israel also designated as a “terrorist organization.” (It is worth noting that while the bank has links to Hezbollah, it also is involved in Lebanese government, NGO/charity, and civilian banking.) Meanwhile, US intelligence services said they were investigating online leaks of US surveillance data showing preparations for Israel’s retaliatory strike on Iran. (The leaked information included satellite images and written materials showing Israel is preparing long-range missiles and drone attacks. The information also said Israel would not use a nuclear weapon. The latter had not even been part of public discussion given there were no casualties and limited damage from Iran’s missiles and those were in response for Israeli bombings in Iran.)

Overnight, Asian markets were mostly in the red with just the three Chinese exchanges in the green. Japan (-1.39%), India (-1.25%), and Thailand (-1.24%) paced the losses. In Europe, with the lone exception of Oslo (+0.37%) we see red across the board at midday. The CAC (-0.76%), DAX (-0.35%), and FTSE (-0.75%) lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a second straight down open. The DIA implies a -0.44% open, the SPY is implying a -0.45% open, and the QQQ implies a -0.51% open at this hour. At the same time, 10-Year bond yields have hit 4.20% while Oil (WTI) popped another 0.94% to $71.22 per barrel in early trading.

The major economic news scheduled for Tuesday is limited to the API Weekly Crude Oil Stocks report (4:30 p.m.). We also hear from Fed member Harker (10 a.m.). Major earnings reports scheduled for before the open include MMM, AOS, DHR, FI, FCX, GE, GM, GPC, HRI, IPG, IVZ, KMB, LMT, MCO, NSC, PCAR, PNR, PM, PII, PHM, DGX, RTX, SHW, and VZ. Then, after the close, AGR, BKR, CNI, CSGP, EWBC, ENVA, MTDR, NBR, PKG, PFSI, RRC, RHI, STX, LRN, TXN, VMI, VLRS, and WFRD report.

In economic news later this week, on Wednesday, September Existing Home Sales, EIA Weekly Crude Oil Inventories, and the Fed Beige Book. We also hear from Fed Governor Bowman. On Thursday, we get September Building Permits, Weekly initial Jobless Claims, Weekly Continuing Jobless Claims, Preliminary Oct. S&P Global Mfg. PMI, Preliminary Oct. S&P Services PMI, Preliminary Oct. Composite PMI, Sept. New Home Sales, and the Fed Balance Sheet. Finally, on Friday, Preliminary Sept. Core Durable Goods Orders, Preliminary Sept. Durable Goods, Michigan Consumer Sentiment, Michigan Consumer Sentiment, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations are reported.

So far this morning, MMM, BKU, DHR, FI, GE, GM, IPG, IVZ, MCO, PNR, PHM, DGX, and RTX all reported beats on both the revenue and earnings lines. At the same time, AOS, KMB, PM, and VZ all missed on revenue while beating on earnings. On the other side, HRI beat on revenue while missing on earnings. However, GPC, PII, and SHW missed on both the top and bottom lines.

With that background, it looks like the Bears are in charge again early in all three major index ETFs. SPY and QQQ are again retesting their T-line (8ema) while DIA gapped down through its 8ema. All three are also mostly black body with a lower wick at this point. With that said, two of the three remain above their T-line with the third gapping below. So, the short-term trend remains modestly bullish. The mid-term and longer-term trends are obviously still strongly Bullish in all three. With regard to extension, none of the major index ETFs are too far extended from its T-line (8ema). In addition, the T2122 indicator is now back in the lower half of its mid-range. So, markets have room to run either direction if traders can find momentum, but the Bulls have just a little more slack to work with today. With regard to those 10 big dog tickers, nine of the 10 are in the red this morning. TSLA (-0.70%) leads on price move lower. The biggest dog, NVDA (+0.19%) is the only green member of the big dogs and has treaded 4.5 times as much dollar-volume as the next closest ticker so far this morning. (For what its worth, this has been typical of bullish days this year.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Friday, markets again diverged at the open, but then got back in-sync. SPY gapped up 0.30%, DIA opened 0.02% lower, and QQQ gapped up 0.52%. After that open, SPY and QQQ chopped along sideways above that opening level and closed in the green. Meanwhile, after the flat open, DIA immediately traded sharply lower for 25 minutes. At that point, it started a steady bullish trend that brought it back above the prior close by 12:30 p.m. before joining SPY and QQQ in a sideways chop just into positive territory. This action gave us indecisive, white-bodied, Doji or small-body Spinning Top candle in all three major index ETFs. SPY and QQQ were both Bullish Harami candles. DIA also printed a new all-time high and both SPY and DIA closed at new all-time high closes. This all happened on below-average volume in all three major index ETFs.

On the day, nine of the 10 sectors were in the green with Basic Materials (+0.84%) and Consumer Cyclical (+0.82%) out in front, leading the market higher. On the other side, Energy (-0.40%) was the only sector in the red. Meanwhile, SPY gained 0.38%, DIA gained 0.04%, and QQQ gained 0.66%. VXX fell 2.36% to close at 51.21 and T2122 climbed a bit further, but remains in the bottom half of its overbought territory to close at 83.90. At the same time, 10-Year bond yields fell to close at 4.079% while Oil (WTI) dropped 1.87% to close at $69.34 per barrel. So, the Bulls were in-charge pretty much all day on what was also an indecisive day. NFLX (+11.09%) was among the leaders of this charge after its blowout earnings Thursday evening. (For the week, SPY gained 0.86%, DIA gain 0.91%, and QQQ gained 0.22%. This was the sixth-straight week of gains for all three major index ETFs.)

The major economic news scheduled for Friday was limited to Preliminary September Building Permits came in lower than expected at 1.428 million (compared to a forecast of 1.450 million and the August 1.470 million value). At the same time, Preliminary September Housing Starts were a little better than predicted at 1.354 million (versus a forecast of 1.350 million but down from August’s 1.361 million reading). This was a decrease of 0.5% month-on-month.

In Fed news, on Friday, Atlanta Fed President Bostic made the case for the FOMC being patient in its rate reductions. Bostic said, “I’m not in a rush to get to neutral.” He continued, “I don’t want us to get to a place where inflation stalls out because we haven’t been restrictive for long enough, so I’m going to be patient.” Bostic went on to say, “If the economy continues to evolve as it does — if inflation continues to fall, labor markets remain robust, and we still see positive production — we will be able to continue on the path back to neutral.” He also said that he is expecting inflation (which is currently at 2.2% according to the Fed’s preferred measure) to get back to 2% by the end of 2025. That being his belief, he said “that should be sort of the timetable for when we should get to neutral.” All this said, Bostic said he expects the Fed to deliver two quarter point cuts in the last two FOMC meetings of the year. For what it’s worth, Bostic also said he has never expected a US recession, saying “I’ve always felt that there was enough momentum in this economy to absorb the restrictiveness of our policy and drive inflation back down to its 2% target. I’m grateful that that’s been playing out so well.”

In stock news, on Friday, the Wall Street Journal reported that activist investor Jana Partners (which has a 5% stake) is planning to pressure LW to explore a potential sale of the $10 billion French fry maker. At the same time, USM announced it has agreed to sell some specific spectrum licenses to VZ for $1 billion. Later, Reuters reported that the board of Japan’s Fuji Soft had agreed to continue to support a $3.72 billion buyout by KKR (despite having received a higher offer from BCSF). At the same time, CNBC reported that STLA will close and sell its large vehicle testing facility in AZ by the end of the year. (The 4,000-acre facility was bought from F for $35 million in 2007.) There are only 41 employees at the facility. At the same time, SPR announced it was furloughing 700 workers for 21 days due to the ongoing strike at BA, which has eaten up their cash reserves and space for storing inventory ready for delivery to BA.

Elsewhere, Reuters reported that SAVE reached an agreement with its credit card processor to extend its debt refinancing deadline two months to December 23. At the same time, Bloomberg reported that CI has resumed merger talks with rival HUM. (The companies had abandoned those discussions in late 2023.) Meanwhile, Reuters reported that the union representing striking BA workers said it is again engaged negotiations with the company, with Acting Labor Sec. Su performing as the intermediary. This is the first resumption of discussions since BA withdrew its last proposal and walked away from negotiations 10 days prior. Later, Reuters reported that T ratified agreements with the CWA union. The contracts cover 23k employees across the Southeast and West of the US. On Saturday, BA and the Machinists Union announced they had reached a tentative deal and the 33k striking union workers will vote on a package including a 35% raise over four years, a $7k signing bonus, and higher 401k company contributions.

In stock legal and governmental news, on Friday, Reuters reported that “Big Tobacco” (PM, BTI, and JAPAF) are close to a $23.6 billion settlement of a long-running lawsuit in Canada. (The suit, which the companies lost, alleged they had known of the cancer caused by smoking since the 1950s, but had hidden that fact and continued to market their products as safe.) If approved by the court, the mediator proposed settlement would be the largest of its kind outside the US. Later, the FDA placed a “partial hold” on a Phase 3 clinical trial of a BNTX lung cancer drug. (The hold was due to “varying results” between different populations in the trial.) At the same time, after consultation with the FDA, GILD announced it was voluntarily withdrawing its bladder cancer drug Trodelvy after the drug failed to meet the main goal of a trial. Later, the NHTSA verified news reports from Thursday, announcing it was investigating 2.4 million TSLA vehicles equipped with “Full Self-Driving” after four more reported collisions, including another fatality.

Elsewhere, the FAA announced it will open a new safety review into BA as the result of an in-flight emergency in January. (The probe is expected to take three months to complete.) Later, the US State Dept. approved the sale of $360 million of RTX-made tactical missiles to Japan. At the same time, a MA judge rejected a motion by META. He ruled that META must face a lawsuit alleging the company purposefully deployed features designed to addict children and deceived the public about the mental health dangers of its social media platform to teenagers. Later, a federal judge in CA granted GOOGL’s request to temporarily pause his order directing the company to overhaul its Android app store (Google Play Store) to give consumers more choice over how they download and pay for apps. The delay will allow time for the 9th US Circuit Court of Appeals to consider GOOGL’s request for appeal. At the same time, the SEC granted “accelerated approval” to 11 ETFs to list and trade options tied to the spot price of Bitcoin. The ETFs will trade on the NYSE. Meanwhile, a federal jury in Ca ruled WDC must pay $315.7 million for patent infringement to private company SPEX Technologies.

In miscellaneous news, on Friday, GS released a report indicating that last week saw hedge funds buying tech stocks (chips and chipmaking equipment) at the fastest pace in five months. (GS is privy to this data since its Prime brokerage service is a primary services provider to hedge funds.) GS said this was the third straight week hedge funds were net buyers of these stocks. Elsewhere, Chinese dronemaker DJI filed suit against the US Dept. of Defense, challenging its listing as a company working with the Chinese military (subject to import restrictions). Meanwhile, CNBC reported Friday that Port of Los Angeles (the country’s fifth-largest port) is now experiencing the largest rail delays in more than two years. (Rail delays means the railroads are unable to keep up with the volume of inbound containers. So, they containers stack up at the port.) The primary causes cited were increased volumes from shipping that was rerouted to LA when East Coast and Gulf Coast ports were expected to be striking, increased traffic from ships that had to avoid the Red Sea and Suez Canal, and increased volumes from holiday merchandise. As of now, containers are waiting an average of nine days to leave the port via rail after unloading from ships.

In Middle East news, on Friday, following an investigation, the UN accused Israeli settlers from killing civilians and cutting down Palestinian olive groves in the occupied West Bank. The Humanitarian Office of the UN called the 32 attacks “war-like” tactics. (Israel said it has suspended the officer in charge of the IDF in that area, pending its own internal investigation into allowing illegal settlers to commit violence under the protection of IDF forces.) On Saturday, Hezbollah fired 20 more rocket salvos into the north of Israel with IDF saying they were intercepted. Hezbollah also launched a single drone attack on PM Netanyahu’s “holiday home” (although the PM was not at that location). In retaliation, Israel pounded Beirut and Southern Lebanon as well as the Bekaa Valley (50 miles north of Beirut). This included bombings of the Lebanese Christian-majority town of Jounieh. Meanwhile, Israeli attacks in Gaza killed at least another 35 people and IDF forces laid siege to three Gaza hospitals. Israel also dropped leaflets saying Hamas would no longer be allowed to rule Gaza. On Sunday, Israel bombed a refugee building in Northern Gaza, kill another 100. Then Sunday night and early Monday, Israeli PM Netanyahu called a meeting of his top aides to discuss their next strike on Iran. For now, the oil markets still seem as much concerned with Chinese demand concerns more than disruption to Middle Eastern oil supplies. However, the preparations for Israel’s strike on Iran may change that balance.

Overnight, Asian markets were mixed with six green and six red exchanges. Shenzhen (+1.09%) led the gainers while Hong Kong (-1.57%) paced the losses. In Europe, the picture is much more or a red hue with 13 of the 14 bourses below break-even at midday. The CAC (-0.95%), DAX (-0.95%), and FTSE (-0.25%) lead the region lower in early afternoon trade. In the US, as of 7:40 a.m., Futures are pointing toward a down start to the week. The DIA implies a -0.22% open, the SPY is implying a -0.34% open, and the QQQ implies a -0.60% open at this hour. At the same time, 10-Year bond yields have spiked to 4.136% and Oil (WTI) is up 2.17% to $70.72 per barrel in early trading.

The major economic news scheduled for Monday is limited to September US Leading Economic Indicators Index (10 a.m.). We also hear from Fed members Kashkari (1 p.m.) and Daly (5:40 p.m.). The major earnings reports scheduled for before the open are limited to KSPI and LU. Then, after the close, ARE, BOKF, LOGI, MEDP, NUE, SAP, SIGI, TFII, WRB, WTFC, and ZION report.

In economic news later this week, on Tuesday we get API Weekly Cride Oil Stocks. We also hear from Fed member Harker. Then Wednesday, September Existing Home Sales, EIA Weekly Crude Oil Inventories, and the Fed Beige Book. We also hear from Fed Governor Bowman. On Thursday, we get September Building Permits, Weekly initial Jobless Claims, Weekly Continuing Jobless Claims, Preliminary Oct. S&P Global Mfg. PMI, Preliminary Oct. S&P Services PMI, Preliminary Oct. Composite PMI, Sept. New Home Sales, and the Fed Balance Sheet. Finally, on Friday, Preliminary Sept. Core Durable Goods Orders, Preliminary Sept. Durable Goods, Michigan Consumer Sentiment, Michigan Consumer Sentiment, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations are reported.

So far this morning, SDVKY beat on both the revenue and earnings lines. Meanwhile, LU missed on revenue while coming in in-line on earnings.

With that background, it looks like the Bears are in charge early in all three major index ETFs. QQQ gapped a bit lower while SPY and DIA opened roughly flat in the premarket. However, all three have sold off since that point and are printing larger black-body candles in the early session. QQQ is retesting its T-line (8ema) from above. Two of the three remain above their T-line (8ema) with the third testing a rising 8ema. So, the short-term trend remains modestly bullish. The mid-term and longer-term trends are also strongly Bullish in all three. With regard to extension, none of the major index ETFs are too far extended from its T-line (8ema). However, the T2122 indicator is still inside the lower edge of its overbought territory. So, markets have room to run either direction, but the Bears have more slack to work with again today. With regard to those 10 big dog tickers, all 10 are in the red this morning. TSLA (-1.23%) leads on price move lower. The biggest dog, NVDA (-0.64%) has traded a bit more than twice the next closest ticker in terms of dollar-volume traded.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets gapped and then ground on Thursday. SPY gapped 0.64% higher, DIA gapped up 0.41%, and QQQ gapped up 1.11% at the open. From there, SPY and QQQ sold off until just after 11 a.m., recross the opening gap in SPY and recrossing 85% of its gap by then. At that point, those two major index ETFs ground sideways inside the gap. For its part, DIA chopped sideways along its open all day. This action gave us gap-up, black-bodied candles in all three major index ETFs. The SPY and QQQ printed large, black, Marubozu candles that ended the day little-changed from Wednesday. Meanwhile, DIA gave us a gap-up, black-bodied, Doji type candle that also printed a new all-time high and closed at a new all-time high close. This all happened on below-average volume in the SPY and QQQ as well as slightly above-average volume in DIA.

On the day, five of the 10 sectors were in the green and the other half in the red with Utilities (-0.90%) well out in front leading the losers lower. At the same time, on the other side, Financial Services (+0.40%) led a more tightly-grouped pack of gainers. Meanwhile, SPY gained 0.01%, DIA gained 0.40%, and QQQ gained 0.07%. VXX fell 1.65% to close at 52.45 and T2122 dropped back to just inside the bottom edge of its overbought territory to close at 80.72. At the same time, 10-Year bond yields spiked again to close at 4.098% while Oil (WTI) gained 0.45% to close at $70.71 per barrel. So, the Bulls gapped markets higher on strong earnings and raised guidance from the world’s largest chipmaker, TSM (+9.77%), which had countered the previous day’s fear over that crucial sector sewn by ASML (+2.50%).

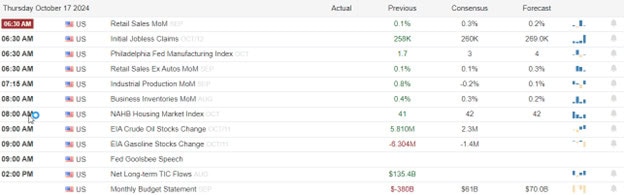

The major economic news scheduled for Thursday included Weekly Initial Jobless Claims, which were down as expected at 241k (compared to a 241k forecast and the prior week’s 260k number). In terms of on-going claims, Weekly Continuing Jobless Claims were up, but not as much as feared at 1,867k (versus a 1,870k forecast and the prior week’s 1,858k reading). At the same time, September Core Retail Sales were much stronger than expected at +0.5% (compared to a +0.1% forecast and August’s +0.2% value). On the manufacturing front, the Philly Fed Mfg. Index was also much stronger than predicted at 10.3 (versus a 4.2 forecast and well up from September’s 1.7 reading). This was done with less labor as the Philly Fed Mfg. Employment Index was down to -2.2 (compared to a September value of 10.7). At the same time, the September Retail Sales (month-on-month) were up to +0.4% (versus the +0.3% forecast and well above August’s +0.1% value). Later, September Industrial Production fell 0.3% (compared to a projected fall of 0.1% and well below August’s 0.3% climb). Later, August Business Inventories remained steady at 0.3% (versus a forecast and July reading of 0.3%). However, August Retail Inventories climbed a tick to 0.5% (compared to a forecast and July value of 0.4%). Later, the Weekly EIA Crude Oil Inventories showed a drawdown of 2.191 million barrels (versus a forecasted inventory build of 1.800 million barrels and the previous week’s 5.810-million-barrel build). At the close, the TIC Net Long-Term Transactions for August showed a decline to $111.40 billion (compared to the July $137.90 billion value). Then, after the close, the Fed Balance Sheet showed another reduction for the week at $7.039 trillion (versus last week’s $7.047 trillion).

In other news, on Thursday the Treasury Dept. released data that showed foreign holdings of US Treasury bonds surged to an all-time high in August after four straight months of increases. The Treasury reported that foreigners owned $8.503 trillion US bonds in August, up 11.5% from one year earlier. Japan remained the largest foreign holder of bonds at $1.129 trillion while China’s holdings fell to $774.6 billion.

After the close, OZK, CCK, ISRG, and NFLX all reported beats on both the revenue and earnings lines. Meanwhile, WAL beat on revenue while missing on earnings. However, WDFC missed on both the top and bottom lines.

In stock news, on Thursday SBGSY announced it had acquired controlling interest in private firm Motivair for $850 million. (Motivair makes liquid cooling technologies for data centers.) At the same time, the Financial Time reported that UBER has explored the idea of making a $20 billion offer to acquire EXPE. Later, NBRNF was acquired by private firm Bidco for $248.5 million. At the same time, META announced it partnered with private studio Blumhouse Productions to test its generative AI for video creation. At the same time, AMZN announced it was dipping a toe into the news market for Prime Video as it has hired NBC anchor Brian Williams to lead its coverage of the US election day. (This is noteworthy because Prime already offers a number of news channels such as CMCSA’s NBC, DIS’s ABC, and CNN.) Later, Reuters reported that BP is considering selling a minority stake in its offshore wind business. (This is reportedly another move by CEO Auchincloss to reduce the company’s renewables exposure as he was brought in to refocus on fossil fuels.)

Elsewhere, TSLA tried to rebound from the embarrassment of last week’s Optimus robot prototype show (which was later acknowledged to just be radio-controlled robots). Thursday, TSLA released a less than 90 second video (with numerous jump cuts) purporting to show an Optimus prototype navigating by itself on a simulated simplistic factory environment. Later, ZUO announced it had agreed to be acquired by the Singapore Wealth Fund and buyout form Silver Lake in a deal valued at $1.7 billion ($10/share). At the same time, PPG announced it will lay off 1,800 employees across the US and Europe as well as close some plants. PPG said this was part of reducing structural costs in Europe. Meanwhile, the Financial Times reported that META has fired around two dozen employees from its Los Angeles office for misusing their company meal allowances for items like laundry detergent and acne treatment pads.

In stock legal and governmental news, on Thursday the Federal Energy Regulatory Commission (FERC) issued an order allowing LNG to move liquified natural gas from its Corpus Christi storage facilities onto tankers. (Having cleared this key hurdle, LNG expects to have the plant producing export gas by year end.) Later, and somewhat oddly, GM announced it “fully supports” the Mexican government’s plans to strengthen supply chains by bringing production to Mexico rather than importing components. GM did not comment when asked to comment on speculation about its future plans in Mexico. At the same time, the FCC proposed a $147k fine for DIS’s ESPN network for violating broadcast rules by broadcasting emergency alert tones during promotional segments in the 2023-2024 NBA basketball season. Later, two consumer groups and two labor unions urged the FCC to block the acquisition of CTLC by NVO in a $16.5 billion deal. (The groups claim that deal would threaten competition in the weight loss drugs and cutting-edge gene therapies markets.)

Elsewhere, the US Dept. of Energy approved a total of nearly $3 billion in conditional loan guarantees for two sustainable aviation fuel projects from CLMT and GEVO. Later, Reuters reported exclusively that President Biden had directed the Commerce Dept., Dept. of Defense, and State Dept. will ease export restrictions on some satellite and spacecraft-related products to US allies. This includes technologies made by LMT, LHX, and BA. At the same time, a suit has been filed against ADM alleging the company failed to maintain and test safety systems on grain equipment for years, resulting in an explosion and the immolation of a worker last year. Later, the FTC has opened an investigation into DE over the company’s repair policies and restrictions the company puts on hardware and software to prevent customers from repairing their purchased products. (DE already faces antitrust lawsuits over the same issue in multiple states.)

In miscellaneous news, NOAA released an updated forecast calling for a warmer and drier-than-normal winter in the south and central Great Plains. This effect of La Nina is expected to worsen the drought across the plains, hitting the US’s top wheat-producing area and impacting wheat yields. (52% of US wheat-producing areas are currently in a drought condition, compared to 44% just two weeks ago.) However, a wetter than normal condition is forecast for the Great Lakes and Ohio River Valley regions this winter. Elsewhere, the CA state Dept. of Food and Ag reported that cattle are dying from bird flu as they are being stressed by heat (at least six days of 95-plus-degree temperatures so far in October). CA reported that herds are now seeing 15%-20% mortality rates (compared to 2% in other states).

In Middle East news, on Thursday, Israeli attacks in Gaza and Lebanon continued. The Israeli government also confirmed that it had, in fact, killed the Hamas military leader Yahya Sinwar on Wednesday. (An IDF unit was operating in Gaza when it stumbled into a 3-man Hamas ground unit. In the firefight that resulted, Israel killed the other two Hamas militants and seeing the severely injured Sinwar was still alive, fired another tank shell, which killed him. After the attack, they recognized Sinwar and collected his body for identification. He was identified by dental records, which Israel had because he had previously spent 23 years in Israeli prison before being released in a prisoner exchange in 2011.) Sinwar had been the subject or a ton of intelligence work and targeted attacks for over a year and had always been thought to be in tunnels hiding with hostages. However, it turns out he had actually been fighting as a regular Hamas fighter all along. While many hope this offers an opportunity to end the Israeli bombing and invasion of Gaza, Israeli PM Netanyahu said the fighting will continue. In addition, Hamas has already named a replacement for Sinwar. Elsewhere, the US confirmed B2 bombing of five weapon storage targets in areas controlled by Houthi rebels in Yemen.

Overnight, Asian markets were mostly green with just three of 12 exchanges below break-even. Shenzhen (+4.71%), Hong Kong (+3.61%), Shanghai (+2.91%), and Taiwan (+1.88%) paced the gains. Australian (-0.87%) and South Korea (-0.59%) led the losses. In Europe, we see a more mixed picture with five of 14 bourses in the red at midday. The CAC (+0.58%), DAX (+0.29%), and FTSE (-0.27%) lead the region and are typical of the early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mixed but generally green start to the day. The DIA implies a -0.05% open, the SPY is implying a +0.21% open, and the QQQ implies a +0.49% open at this hour. At the same time, 10-Year bond yields are up to 4.108% and Oil (WTI) is down four-tenths of a percent to $70.40 per barrel in early trading.

The major economic news scheduled for Friday is limited to Preliminary September Building Permits and Preliminary September Housing Starts (both at 8:30 a.m.). We also hear from Fed member Bostic (9:30 a.m.), Fed member Kashkari (10 a.m.), Fed Governor Waller (12:10 p.m.), and Fed member Bostic again (12:30 p.m.). The major earnings reports scheduled for before the open include ALLY, AXP, ALV, CMA, FITB, PG, RF, and SLB. Then, after the close, there are not reports scheduled.

So far this morning, VLVLY (Volvo), ALLY, CMA, FITB, and RF all reported beats on both the revenue and earnings lines. Meanwhile, AXP, PG, and SLB missed on revenue while beating on earnings. However, ALV missed on both the top and bottom lines.

In late-breaking news, GOOGL announced they had replaced the head of their search and ads unit leader (Raghaven) with longtime Google employee Nick Fox. GOOGL’s statement said that Raghaven will move to the role of Chief Technologist. (It was unclear if this was a new position or if he was replacing someone else.) Elsewhere, CVS replaced their CEO Lynch with longtime executive David Joyner, effective immediately. Meanwhile, the Chinese rally may be explained by its release of “better-than-expected” GDP growth of 4.6% year-on-year for Q3, where the consensus analyst estimate had been 4.5%. (Still, this was still the slowest growth in six quarters.) The tell may be that Beijing almost immediately announced new stimulus that propped up the Chinese markets.

With that background, it looks like the Bulls are in charge again in the SPY and QQQ as they both gapped higher to start the premarket and have followed-through with white-body candles. For its part, DIA is down a bit after opening the early session higher and then trading indecisively but lower. All three remain above their T-line (8ema). So, the short-term trend remains bullish. The mid-term and longer-term trends are also strongly Bullish in all three. With regard to extension, none of the major index ETFs are too far extended from its T-line (8ema). However, the T2122 indicator is still at the lower edge of its overbought territory. So, markets have room to run either direction, but the Bears have more slack to work with again today. With regard to those 10 big dog tickers, nine of the 10 are in the green this morning. NFLX (+6.74%) leads on price move after blow-out earnings last night. The biggest dog, NVDA (+0.93%) has traded a bit more than twice the next closest ticker in terms of dollar-volume traded. Finally, remember its Friday and options expiration Friday at that. So prepare your account for the day and weekend.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Wednesday markets diverged at the opening bell. SPY opened flat, DIA opened 0.06% lower, and QQQ opened 0.08% higher. From there, SPY and DIA rallied in a slow and steady manner all day. Meanwhile, QQQ sold off at the open, chopping sideways until noon and then began a slow, steady rally the rest of the day. All three modestly pulled back at the end of the session. This action printed a white-bodied, Bull Harami with small wicks on both ends in the SPY. At the same time, DIA gave us a Bull Engulfing candle that bounced up off its T-line (8ema). It should also be noted that DIA ended within 15 cents of another all-time high close. For its part, QQQ printed a Doji that retested its T-line and closed just a few pennies below that average. This all happened on below-average volume in the DIA and well-below-average volume in the SPY and QQQ.

On the day, all 10 sectors were in the green with Utilities (+2.01%) and Healthcare (+1.93%) way out in front leading the market higher. On the other side, Consumer Defensive (+0.03%) and Technology (+0.16%) lagged behind the other sectors. At the same time, SPY gained 0.42%, DIA gained 0.73%, and QQQ gained 0.01%. VXX fell 0.97% to close at 53.33 and T2122 spiked back up into the top end of the overbought territory to end the day at 95.22. At the same time, 10-Year bond yields fell again to 4.014% while Oil (WTI) was flat (-0.07%) to close at $70.53 per barrel. So, the Bulls partially bounced back from Tuesday’s down day in the SPY and DIA were in control all day Tuesday. QQQ was the laggard as Technology dragged on the market, but was held up by outlier NVDA (+3.13%) that traded 3.5 times more dollar-volume than any other QQQ ticker.

The major economic news scheduled for Wednesday included September Export Price Index, which came in lower than expected at -0.7% (compared to a forecast of -0.4% but not down as much as August’s -0.9%). At the same time, the September Import Index was a tick lower than predicted at -0.4% (versus a -0.3% forecast and down more than August’s -0.2% reading). Then, after the close, API Weekly Crude Stocks showed an unexpected drawdown of 1.580 million barrels (compared to a forecasted 3.200-million-barrel inventory build and far below the prior week’s 10.900-million-barrel drawdown).

In Fed news, on Wednesday, after the close, the Cleveland Fed issued a report saying that rent inflation will continue to put pressure on consumers for some time. The report said, “Our baseline forecast implies that (CPI) rent inflation will remain above its pre-pandemic norm of about 3.5% until mid-2026.” The report went on to cite a “notably wider” gap between new lease inflation and existing lease rollover increases. The report said, “Our estimated rent gap in September 2024 is just under 5.5%, suggesting that there remains a substantial amount of potential rent inflation to be passed through to continuing tenants.” (Prior to the pandemic, that gap stood at 1%.)

After the close, CCI, DFS, EFX, SNV, STLD, and UNB all reported beats on both revenue and earnings. At the same time, AA missed on revenue while beating on earnings. However, CSX, KMI, LBRT, and PPG missed on both the top and bottom lines.

In stock news, on Wednesday, AMZN announced its first color version of its Kindle e-reader after years of development. AMZN priced the device at $280, which is in the $149 – $330 range of similar devices from other manufacturers. At the same time, CZZ Chairman Ometto was quoted in a published interview saying that the company was not looking to sell its stake in VALE in the short-term. (This contradicts a Bloomberg report from late last month, which said the company was interested in selling its VALE stake.) Later, AMZN announced it signed three agreements with private companies for building small modular nuclear reactors to power the AMZN datacenters. (Under the deals, AMZN has the right to buy up to eight 80 MW reactors, which would be enough to power 770k homes.) At the same time, BTAFF announced a new line of synthetic nicotine pouches as a smoking alternative under the existing Velo product line. Later, GM announced it will contribute $625 million to a joint-venture with LAC with a goal of developing lithium mines in Thacker Pass, NV. (The goal is to reduce reliance on Chinese lithium sources.) GM will have 38% ownership of the venture.

Elsewhere, EADSY (Airbus) announced it will cut 2,500 jobs in its Defense and Space division after months of losses. (Negotiations with unions and countries throughout Europe are underway to determine which jobs will be cut and from what locations.) Later, BB told an investor conference that it was exploring options for its Cyclance unit. (Cyclance uses machine learning to preempt cybersecurity breaches.) At the same time, the Wall Street Journal reported that CMCSA-owned NBC Universal will add regional sports broadcasts to tie Peacock streaming service in early 2025. Later, AMX announced it plans to push the rollout of 5G service across Mexico and Latin America in 2025 as the main goal of its $7 billion capital expenditure forecast for the next year. After the close, LCID announced it now anticipates reporting a bigger-than-expected loss for Q3 when the report is released November 11. LCID simultaneously announced a 262 million pubic offering of new shares. In addition, Saudi Arabia’s Public Investment Fund said it would purchase 374.7 million shares, giving it 59% ownership of LCID.

In stock legal and governmental news, on Wednesday, the FDA placed a trial for NVAX’s experimental COVID-19 and influenza combination vaccine on hold. (The hold was due to a report of nerve damage in a patient in an earlier, mid-stage trial.) NVAX closed down 19.44% on the news. At the same time, the Dept. of Energy issued a conditional commitment for a loan of $670.6 million to ASPN for a plant to produce thermal barriers used in electric vehicle batteries. Later, the NHTSA announced that STLA is recalling 54k hybrid crossover SUVs due to a brake pedal that can disengage and stop working. (Just under half those vehicles were sold in North America.) At the same time, the FTC adopted its final rule requiring businesses to make it as easy to cancel subscriptions and memberships as it was to sign up.

Meanwhile, the US Dept. of Transportation tentatively awarded five new daily round-trip flights from Washington Reagan National to AAL, ALK, DAL, UAL, and LUV. The slots are subject to a two-week public comment period and one-week response period prior to the decision becoming final. After hours, Reuters reported that RTX has agreed to pay $959 million to resolve federal charges of defrauding the US Dept. of Defense and bribing a Qatrar official. The company entered into two deferred prosecution agreements (one in Boston and one in Brooklyn) to avoid criminal charges. At the same time, Reuters reported that the US Customs and Border Protection agency has halted the import of some DJI drones from China. (Reportedly, the halt came in response to the Uyghur Forced Labor Prevention Act.) Later, the US Supreme Court declined to put a hold on EPA rules targeting carbon pollution from coal-fired and gas-fired power plants. (The suit seeking to block the EPA rules had been brought by WV and 25, mostly GOP, states.) The suit can continue in lower courts, but the enforcement can proceed at least until that case is decided.

In Middle East news, on Wednesday, Israel defied calls for a cease-fire and pressure to allow humanitarian aid into Gaza and Lebanon by re-intensifying its bombing attacks on Beirut. In the process, the IDF took out a municipal building and aid distribution center killing the entirety of one suburb’s administration (Mayor, three key deputies, and several underlings) which had been meeting to plan the deliveries of a shipment of food aid. (That strike alone killed 16 people and wounded another 60.) This was part of more than 130 IDF attacks on Beirut and southern Lebanon on the day. For its part, the Israel said Hezbollah had fired 90 rockets at northern Israel, but there had been no casualties or significant damage. Meanwhile, and most importantly to markets, CNN reported that multiple sources now tell it that the Israeli response to Iran’s recent 180 missile barrage is ready. (It’s worth noting Iran’s missile attack on Israel did no real damage and caused no casualties.) CNN also says that US officials expect Israel to launch that retaliatory strike (to Iran’s own retaliation for Israeli bombings in Iran) prior to the US election. (This makes sense when you realize what Israeli PM Netanyahu prefers from the US election.)

Overnight, Asian markets were mixed with six exchanges in the green and six in the red. Shanghai (-1.05%), Hong Kong (-1.02%), and India (-0.89%) paced the losses while New Zealand (+1.01%), Singapore (+0.96%), and Australia (+0.86%) led the gainers. However, in Europe, we see green across the board at midday. The CAC (+1.19%), DAX (+0.80%), and FTSE (+0.42%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a move higher to start the day. The laggard DIA implies a +0.14% open, SPY is implying a +0.41% open, and QQQ implies a +0.80% open at this hour. At the same time, 10-Year bond yields are up to 4.036% and Oil (WTI) is up a quarter percent to $70.57 per barrel in early trading.

The major economic news scheduled for Thursday includes Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, September Core Retail Sales, Philly Fed Mfg. Index, Philly Fed Mfg. Employment, September Retail Control, and September Retail Sales (all at 8:30 a.m.), September Industrial Production (9:15 a.m.), August Business Inventories and August Retail Inventories (bot hat 10 a.m.), Weekly EIA Crude Oil Inventories (11 a.m.), and the Fed Balance Sheet (4:30 p.m.). The major earnings reports scheduled for before the open include BX, CMC, ELV, HBAN, INFY, KEY, MTB, MAN, MMC, SNA, TSM, TRV, TFC, WBS, and WIT. Then, after the close, CCK, ISRG, NFLX, WDFC, and WAL report.

In economic news later this week, on Friday, Preliminary September Building Permits and Preliminary September Housing Starts are reported. We also hear from Fed Governor Waller.

In terms of earnings reports later this week, on Friday, ALLY, AXP, ALV, CMA, FITB, PG, RF, and SLB report.

So far this morning, BX, CBSH, HBAN, INFY, KEY, MTB, MAN, TSM, TVBI, TRV, and TFC all reported beats on both revenue and earnings. (BX crushed on revenue growth by more than 44%. In addition, the worlds largest chipmaker, TSM, crushed with 36% revenue growth and 11.5% earnings growth. Regional bank TCBI reported a whopping 67% beat on earnings.) Meanwhile, MMC, NOK, and SNA missed on revenue while beating on earnings. On the other side, ELV beat on revenue but missed on earnings. However, CMC missed on both the top and bottom lines.

In late-breaking news, TSM crushed in its Q3 report and raised guidance. Since they are the world’s largest, and most cutting-edge chipmaker, this is reassuring markets that the tech market demand has not been hurt. (That dour outlook on chips and by extension tech came from Tuesday’s terrible ASML report.) It is worth noting that TSM’s largest customers are NVDA, AMD, AAPL (phone, tablet, and computer), INTC, and QCOM.

With that background, it looks like the Bulls are in charge again ahead of morning data. SPY and QQQ both gapped higher while DIA opened flat to start the premarket. From there, all three have printed white-body candles so far in the early session, with DIA the smallest of those bodies. SPY is now trading within pennies of another all-time high. All three remain above their T-line (8ema). So, the short-term trend remains bullish. The mid-term and longer-term trends are also strongly Bullish in all three. With regard to extension, none of the major index ETFs are too far extended from its T-line (8ema). However, the T2122 indicator is back in (the top of) its overbought territory. So, markets have room to run either direction, but the Bears have more slack to work with again today. With regard to those 10 big dog tickers, all 10 are in the green this morning. The biggest dog, NVDA (+3.03%) is back to leading that pack in terms of both price move and dollar-volume traded. (It is also worth noting that NVDA has traded 5.5 times as mush stock as the next-closest big dog, TSLA (+0.25%), on the strength of the TSM earnings.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

U.S. stock futures edged up slightly on Thursday as investors awaited the release of initial weekly jobless claims data and September retail sales figures at 8:30 a.m. ET. These reports are expected to provide insights into the health of the labor market and consumer spending in the U.S. Additionally, corporate earnings reports are set to continue, with Travelers, Blackstone, and Elevance Health among the major companies reporting Thursday morning. Regional banks, including KeyCorp, M&T Bank, and Truist Financial, are also scheduled to release their earnings, adding to the day’s financial data.

European markets saw an uptick on Thursday morning as traders anticipated the upcoming monetary policy decision from the European Central Bank (ECB). The banking sector led the charge, with the banking index rising nearly 1.3%, while telecom stocks saw a slight decline of 0.5%. The ECB is expected to announce its third interest rate cut of the year, responding to inflation risks in the European Union that are diminishing more rapidly than anticipated. In September, inflation in the euro area cooled to 1.8%, falling below the ECB’s 2% target.

Most Asia-Pacific markets experienced a downturn on Thursday following a lackluster briefing from China’s housing ministry, which failed to meet investor expectations and led to a significant drop in the country’s property stocks. In Japan, exports declined by 1.7% in September compared to the same month last year, while import growth for the same period was 2.1%, falling short of forecasts. Meanwhile, Australia reported a slight decrease in its unemployment rate for September, which came in at 4.1%, marginally lower than the figure predicted by a Reuters poll.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include BMI, BX, CMC, ELV, HBAN, IIIN, IRDM, KEY, MTB, MAN, MMC, SNA, TCBI, TRV, TFC, WBS, & WNS. After the bell reports include NFLX, OZK, CCK, ISRG, FNB, WDFC, & WAL.

News & Technicals’

TSMC reported a net income of 325.3 billion Taiwanese dollars ($10.1 billion) for the July-September quarter, exceeding the LSEG estimate of 300.2 billion Taiwanese dollars. The company’s net revenue for the third quarter reached $23.5 billion, marking a 36% increase year-on-year. As the world’s largest producer of advanced chips, TSMC continues to serve major clients like Apple and Nvidia, highlighting its pivotal role in the global semiconductor industry.

Novavax announced that the Food and Drug Administration has placed a hold on its application for a combination shot targeting both Covid-19 and influenza, as well as a stand-alone flu vaccine. This decision, which caused a sharp decline in the company’s shares, stems from a single report of nerve damage in a patient who received the combination shot during a phase two trial completed in July last year. This development represents a setback for Novavax, which is urgently working to introduce new products to the market amid declining global demand for its Covid-19 vaccine.

Shares of Lucid Group declined during after-hours trading following the announcement of a public offering of nearly 262.5 million shares of its common stock. The electric vehicle startup plans to use the proceeds from this offering for general corporate purposes, which may include capital expenditures and working capital. This move aims to bolster the company’s financial position as it continues to expand its operations and market presence.

The Biden administration announced the forgiveness of an additional $4.5 billion in student debt, benefiting over 60,000 borrowers. This latest round of relief stems from the U.S. Department of Education’s improvements to the Public Service Loan Forgiveness program, which has faced challenges in the past. Eligible borrowers can expect to receive notifications about their cancelled debt in the coming weeks, marking a significant step in the administration’s ongoing efforts to address student loan burdens.

With a big round of earnings and economic reports that begin with initial weekly jobless claims, expect some price volatility with the T2122 indicator flashing an overbought warning. We will also have to digest Retail Sales, Philly Fed Mfg., Industrial Production, Business Inventories, Housing Market Index, Natural Gas, Petroleum and more Fed talk from Goolsbee. So, buckle up it could be a wild and woolly day!

Markets diverged at the open Tuesday. SPY opened 0.06% higher, DIA gapped down 0.36%, and QQQ opened 0.08% higher. From there, SPY and QQQ ground sideways in a very tight range for 35 minutes before selling off sharply for 30 minutes and then moving sideways again until a little after 1 p.m. From there, those two broader index ETFs sold off again, just much more slowly, for the rest of the day. For its part, after its gap lower, DIA chopped sideways until 12:30 p.m. and then slowly sold off further all afternoon. This action gave us large black-bodied Bearish Engulfing candles in the SPY and QQQ. (QQQ also retested and crossed below its T-line, 8ema.) Meanwhile, DIA gave us a gap down, black-bodied candle with modest lower wick and a bit larger upper wick. This happened on average volume in the DIA, slightly-below-average volume in the QQQ, and below-average volume in the SPY.

On the day, six of the 10 sectors were in the red with Energy (-2.91%) way, way out in front leading the market lower as fears over an Israeli retaliatory strike on Iran faded temporarily. (The thinking is apparently that Israel would wait on a US THAAD missile system to be shipped, installed, and brought on-line by 100 US troops before attacking Iran.) On the other side, Communications Services (+0.60%) held up better than the other sectors. Meanwhile, SPY lost 0.78%, DIA lost 0.78%, and QQQ lost 1.34%. VXX gained 3.26% to close at 53.85 and T2122 fell out of its overbought territory to end in the top of its mid-range, closing at 74.65. At the same time, 10-Year bond yields fell quite a bit to 4.034% while Oil (WTI) plummeted 3.94% to close at $70.92 per barrel. So, the Bears were in control all day Tuesday. An accidental day early publication of earnings by ASML (-16.26%), which beat but missed on key segment growth and significantly lowered forward guidance, caused the stock to plummet. More importantly, that read through into NVDA (-4.69%), AMD (-5.22%), and INTC (-3.33%) among other chipmakers. (NVDA was the big hit to the overall market since it traded almost $50 billion in stock during the day.)

The major economic news scheduled for Tuesday was limited to NY Empire State Mfg. Index, which came in much lower than expected at -11.90 (compared to a +3.40 forecast and a September +11.50 value). Later, September NY Fed 1-Year Inflation Expectations were flat at 3.0% (versus the August 3.0% reading).

In Fed news, on Tuesday, San Francisco Fed President Daly said the FOMC remains on track for more rate cuts this year unless data is unlike than expected. She defended the September half point rate cut, saying that it was “right-sizing.” Daly described it as, “recognizing the progress we’ve made (on inflation) and loosening the policy reins a bit, but not letting go.” She went on, “even with this adjustment, policy remains restrictive, exerting additional downward pressure on inflation to ensure it reaches 2%.” Looking forward, Daly said, “I think one or two [rate cuts] this year would be a reasonable thing.” Regarding quantitative tightening, “Right now, today, I don’t have any signs this is something that needs to change right away.” She concluded saying, “The economy is clearly in a better place (regarding inflation),” … “the risks to our goals are now balanced.” Later, Atlanta Fed President Bostic told an event that he has penciled in just one more (quarter point) cut to rates in 2024 when he updated his “dot” at the September FOMC meeting. Bostic said, “The median was for … 50 basis points more, above and beyond the 50 basis points that was done in September. My dot was 25 basis points more.” However, Bostic said he is open to changing his view and it is not set in stone. Bostic said, “I am keeping my options open.”

After the close, FULT, HWC, and OMC reported beats on both the revenue and earnings lines. At the same time, JBHT and UAL missed on revenue while beating on earnings. On the other side, IBKR beat on revenue while missing on earnings.