The Week Ahead – 2/21/21

Indexes briefly reacted negatively yesterday with jobless claims rising and housing starts declining, suggesting the so-called recovery is struggling. However, combat that Jannet Yellen came out with a go-big promotion for more stimulus and futures turned bullish this morning. Today we have a relatively light day on the earnings calendar with readings on PMI and Existing Home Sales after the open. Though the price action this week suggests some uncertainty, the overall trends remain bullish. With our next stimulus fix on the way, soon stay with the trend and ride the wave as long as it lasts.

Overnight Asian markets recovered early losses to close with modestly mixed results. European markets trade cautiously higher this morning, with a focus on earnings. U.Ss futures recovered from overnight lows, pointing to a modestly bullish open ahead of earnings and economic reports. Price action remains somewhat choppy, so plan your risk carefully as we slide into the weekend.

We have a lighter day on the Friday earnings calendar with just over 40 companies fessing up to quarterly results. Notable reports include AEE, DE, DTE, ERF, E, MGA, & MGI.

The indexes experienced a little selling yesterday, reacting to higher than expected joblessness and a substantial decline in housing starts. However, this morning futures are trying to shake off the weakening recovery after Janet Yellen pitches for the massive 1.9 trillion stimulus package. Facebook made the news again, banning thousands of Australian accounts after deciding to block publishers from sharing and viewing news content on its site. The #deletefacebook hashtag is trending across other social platforms.

Although the indexes price action has experienced a lot of chop this week, the overall bullish trends continue to hold. Without question, the economic data has raised some uncertainty. Still, with the market now addicted to newly printed money and the promise its next fix is just around the corner, the economy’s condition no longer seems to matter. I believe this will end badly in the long run, but for now, all we can do as traders stay with the trend. That said, we must remain disciplined, avoid overtrading with a fear of missing out and chasing already extended stock prices. An outsider looking at our index charts would have to assume that the pandemic was the best thing that’s ever happened to our economy! However, we all know that is not the case. Stay focused and flexible, sticking to your trading rules, and be prepared should the market stumble.

Trade Wisely,

Doug

Markets gapped down significantly, largely in reaction to an unexpectedly bad Weekly Initial Jobless Claims number and a week forecast during the WMT report. However, after the gap, all 3 major indices slowly ground back toward the prior candle. This left all three in white-bodied indecisive Doji or Spinning Top type candles. On the day, SPY lost 0.43%, DIA lost 0.33%, and QQQ lost 0.44%. The VXX was up slightly to 15.66 and T2122 fall back to mid-range at 56.00. 10-year bond yields gained slightly to 1.297% and Oil (WTI) fell almost 2% to $60.08/barrel.

The Congressional hearings Thursday made for a tough day for both Robinhood and Citadel who got blasted by House members on both sides of the political aisle. Citadel was left defending “payment for order flow” while Robinhood CEO Tenev had to defend that business model as well as not allowing customers to buy GME. However, Reddit and Reddit Trader Keith Gill (Roaring Kitty) received praise from both sides. There were also a couple of revelations, such as that over 50% of Robinhood’s revenue comes from payments for order flow (selling customer orders to the highest bidder). In addition, it was disclosed that Citadel is the broker’s largest counter-party, buying most of the orders that Robinhood sells. It also came out that on January 28, Robinhood was nearly out of business when the clearinghouse demanded $3 billion in posted capital and the company could not come up with that amount. (They stayed afloat by negotiating the clearinghouse down to $1.4 billion, which the company could raise from investors.)

The UK version of the Supreme Court has ruled unanimously that UBER drivers are employees, not independent contractors. UBER now has to go back to the country’s employment court to determine what back compensation their workers are due. The threat is that Europe and even US courts could take the same position in the future. However, this court ruling deals a blow to not only to UBER, but to all “gig economy” based companies that have been relying on contractors to reduce costs by transferring responsibilities to workers.

Related to the virus, US infections continue the recent trend of decreasing new cases. The totals have risen to 28,523,524 confirmed cases and deaths have now passed half a million at 505,309 deaths. However, the number of new cases continues to fall quickly and is back down to the October level as the average new cases are now 73,858 new cases per day. However, deaths remain at a stubbornly high level of 2,075 per day. Mid-day on Thursday, WMT’s CEO told CNBC that his customers need another round of stimulus checks and need it quickly. Then in the evening, Treasury Sec. Yellen made her push for a big package of relief, fast in interviews Thursday evening. Along those lines, House Democrats hope to pass their version of the $1.9 trillion relief package next week according to Speaker Pelosi. It appears they will be doing it without GOP support.

Globally, the numbers rose to 110,929,475 confirmed cases and the confirmed deaths are now at 2,454,516 deaths. However, the trends are good. The world’s average of new cases continues to fall quickly and is now down to 361,898 per day. Mortality lags but is also falling, now down to 9,976 new deaths per day. UK PM Johnson has called for the G7 Countries to work together as a coalition to be able to develop vaccines and treatments to pathogens (like the Covid variants) and test them within 100 days. This would be about 3 times faster than the first covid vaccines were rolled out. French President Macron then urged the G7 to donate 4%-5% of their available vaccine doses to developing countries.

Overnight, the few Asian markets were mixed. Australia (-1.34%) and Japan (-0.72%) led the losses, while Shenzhen (+0.75%) and South Korea (+0.68%) led the gains. In Europe, markets are also mostly green so far today. The FTSE (+0.10%) is just above flat, but the CAC (+0.63%) and DAX (+0.52%) are moderately green at mid-day. As of 7:30 am, US Futures are pointing toward a positive open. The DIA is implying a +0.26% open, the SPY implying +0.36%, and the QQQ implying a +0.53% open at this hour.

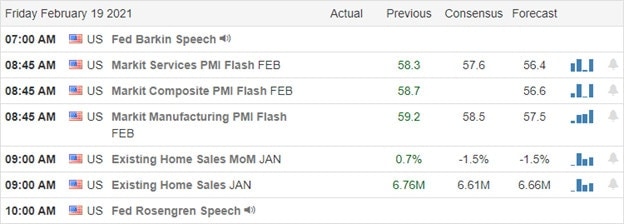

The major economic news for Friday is limited to Mfg. PMI and Services PMI (both at 9:45 am), Jan. Existing Home Sales (10 am) and a Fed speaker (Rosengren at 11 am). Major earnings reports on the day include DE, DTE, ITT, MGA, and POR before the open. There are no major earnings reports after the close.

With modest data, limited earnings reports, and Congress still not back in DC, the market does not have a clear driver for the day. It is Friday and with the winter storm projected to move into New York City today, we may see some of the big players head home early. The sideways and lower trading of this week has taken a toll. However, the bulls remain in control of the trend in a broader sense. So, beware of volatility (gap and fade we’ve seen recently) and get positioned for the weekend.

Forget about predicting. Knife-catching is not a good career path. Just follow the trend, respect support and resistance levels, and don’t chase the moves you missed. Book your trade goals when you can and stick to your discipline. If you keep locking in your profits when you have them, you’ll never go bust. Remember that trading is a marathon, not a sprint. You don’t have to trade every day and don’t try to get rich quick. Do it in the long-run by hitting goals over and over again. Also, remember it’s Friday, so don’t forget to pay yourself.

Ed

Swing Trade Ideas for your consideration and watchlist: DRI, SMAR, DOCU, H, MGM, KO, SAVE, CLSK, IQ, MU. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With a choppy mixed bag of results on Wednesday, the bullish momentum seems to have run into a bit of uncertainty. The DIA set a new all-time high as it defiantly rallied while SPY, QQQ, and IWM slipped modestly lower. Today, we have another big day of data coming our way, and although the futures currently point to lower open, anything is possible as the market reacts to the news. Keep an eye on the GameStop hearing in Congress as it could have market implications and news-related price reactions.

Overnight Asian markets traded mixed but mostly lower, and European markets flip-flop between modest gains and losses this morning. Ahead of a big day of data that includes Housing Starts, Jobless Claims, and the Philly Fed traders should prepare for just about anything even though futures currently suggest a cautiously lower open.

On the Thursday earnings calendar, we have more than 100 companies reporting quarterly results. Notable reports include WMT, BCS, GOLD, BLMN, APRN, COG, CBB, CVA, CS, DBX, FE, FVRR, FTDR, GLPI, GLOB, HL, HRL, HST, IDA, LTC, NEM, OPI, OPK, PLNT, PPL, RXT, SO, TXRH, TTD, TPH, TRIP, VTR, WM, & WST.

Futures point to a lower open the day after a choppy mixed bag of results on Wednesday. The DIA defiantly rallied to a new record high, with SPY, QQQ, and IWM indexes moving marginally lower. Today Congress will hold a hearing to investigate the short squeeze inspired by the Reddit community. Robinhood, Citadel, and Reddit CEO’s will testify as well as the Roaring Kitty the turn out hold a securities license and now faces fraud charges from the SEC. Interactive Brokers chair says the financial system came dangerously close to failure during the GameStop mania. Facebook has decided to block all news from Australia from being posted on the social platform even as Google reached a revenue-sharing agreement with news creators. Facebook has also decided it will debunk climate change myths and will be the sole judge of truth. Who else is getting tired of the truth filter of the all-knowing Facebook!

Though the choppy price action is raising some caution flags, index trends remain bullish. That said, we seem to have lost some momentum, and a bit of uncertainty has crept into the mix. Today we have another big day of earnings and economic data that includes Jobless claims. Currently, futures suggest a lower open, but with so much data coming our way before the bell, traders should prepare for just about anything.

Trade Wisely,

Doug

Markets gapped down about a third of a percent in the large-caps and about one percent in the QQQ on Wednesday. However, after a little morning vacillation, the bulls stepped in and tried to drive price back up. This left is with cap-down white candles across the board. Of the 3, only the QQQ printed a candle signal and that was an indecisive Spinning Top. On the day, SPY (+0.02%) was flat, DIA (+0.32%) was up and QQQ (-0.48%) was down. VXX fell 2% to 15.58 and T2122 fell out of the overbought territory down to 71.83. 10-year bond yields fell a bit to 1.282% and Oil (WTI) rose a dollar to $61.14/barrel on the back of the winter storm demand.

The Dow was buoyed by VZ and CV, which saw major moves on reports that BRKB had taken a major stake in Q4. (Everybody wants to follow Buffett.) The afternoon rally was helped by FOMC minutes that showed that an easy money policy will be in place for longer than many expected. The group’s focus was clearly on getting employment back to pre-pandemic levels regardless of the cost. Retail Sales in January also surged 5.3%, blowing away the consensus estimate of +1.2%. This seems to signal that people are spending their December stimulus checks and just the opposite of the FOMC, indicate a potential for inflation.

The key players in the recent “social media short squeeze” will be testifying today in front of the House Financial Services Committee. The CEOs of Reddit, Robinhood, Melvin Capital, Citadel and a key Reddit trade known as “Roaring Kitty” will all testify about GME stock price manipulation. Conspicuously absent from the list are major brokerages who also temporarily banned the shorting or trading of GME stock, such as SCHW, eTrade, Fidelity, IBKR, etc. So, perhaps they will have their turn in the barrel in a different hearing.

Related to the virus, US infections continue the recent trend of decreasing new cases. The totals have risen to 28,453,526 confirmed cases and deaths have now passed half a million at 502,544 deaths. However, the number of new cases continues to fall quickly and is back down to the October level as the average number of new cases are now 79,112 new cases per day. Unfortunately, deaths remain stubbornly high at a level of 2,145 per day. Related to this, the ports of Los Angeles and Long Beach (the two largest US ports) have begun diverting container ships to alternate ports because over 800 post workers are out sick with Covid. Unload times at these ports have risen from less than 3 days to more than 8 days as stretched staff have seen a major increase in traffic since last fall. This will add cost and likely delays to incoming freight.

Globally, the numbers rose to 110,520,588 confirmed cases and the confirmed deaths are now at 2,442,946 deaths. However, the trends are good. The world’s average of new cases continues to fall quickly and is now down to 367,784 per day. Mortality lags but is also falling, now down to 10,239 new deaths per day. In England, the government reported that new infections have dropped by two-thirds from the peak. However, in some “bad actor” news, Belgium reported that they have caught 184,000 violations of pandemic rules since last March (on a country of 11.5 million), but only 97,000 people were issued fines.

Overnight, the few Asian markets were mostly red. Hong Kong (-1.58%) and Malaysia (-1.22%) led the losses. However, there were a couple of holdouts with Shanghai (+0.55%) and Taiwan (+0.38%) closing higher. In Europe, markets are also mostly red so far today. The FTSE (-0.70%) and CAC (-0.22%) are down, but the DAX (+0.13%) is staying just above flat. As of 7:30 am, US Futures are pointing toward a lower open. The DIA is implying a -0.31% open, the SPY implying -0.40%, and the QQQ implying a -0.74% open at this hour.

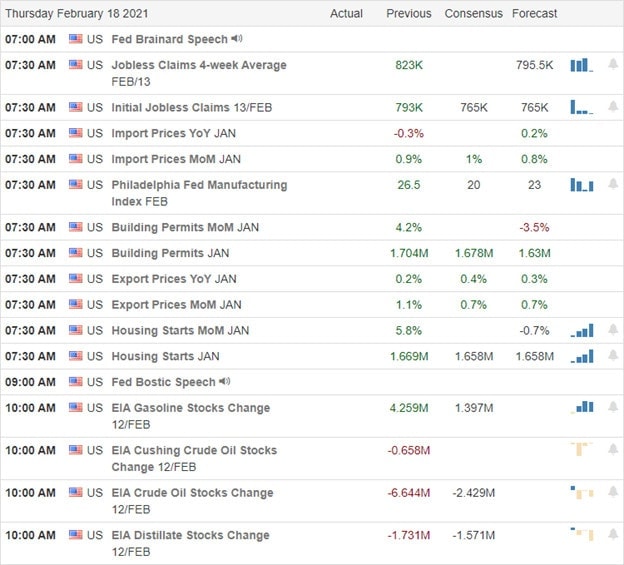

The major economic news for Thursday includes Philly Fed Mfg. Index, Jan. Building Permits, Jan. Import/Export Index, Jan. Housing Starts, and Weekly Initial Jobless Claims (all at 8:30 am), Crude Oil Inventories (11 am), and a couple Fed speakers (Brainard at 8 am and Bostic at 10 am). Major earnings reports on the day include AAWW, GOLD, BLMN, CFX, EPAM, FE, HRL, KELYA, LKQ, MAR, NEM, OMC, RS, SRE, SO, SYNH, TECK, TPH, VTR, VC, WAB, WMT, and WM before the open. Then after the close, COLD, AMN, AMAT, ATR, ANET, CNDT, ED, CPRT, EBS, KEYS, QDEL, RXT, ROKU, TDS, TXRH, and USM report.

With a lot of economic news out this morning, especially Jobless Claims and Housing data, markets do not seem optimistic. The winter storm also continues to weigh on sentiment in much of the country. However, the bulls remain in control of the trend as the bears have not been able to get enough traction for even a small pullback. Still, there may be market-related news out of the Congressional Hearing today that may shake things up again.

Forget about predicting. Knife-catching is not a good career path. Just follow the trend, respect support and resistance levels, and don’t chase the moves you missed. Book your trade goals when you can and stick to your discipline. If you keep locking in your profits when you have them, you’ll never go bust. Remember that trading is a marathon, not a sprint. Don’t try to get rich quick. Do it in the long-run by hitting goals over and over again.

Ed

Swing Trade Ideas for your consideration and watchlist: DXCM, AIG, PFE, CB, SNAP, PENN, C, KR, UNG. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Rising bond rates created a little uneasiness yesterday, robbing the bullish energy created in the morning gap to new highs. This morning the rapid decline in mortgage applications due to the rising interest rates may also contribute to futures taking a wait-and-see approach. We have a big day of earnings and economic reports with PPI and Retail Sales before the bell and the FOMC minutes later this afternoon. I think it’s fair to say anything is possible with that much data for the market to digest.

Asian markets traded mixed overnight, with Hong Kong surging more than 1%. European markets show modest declines across the board as they track rising Treasury yields. Ahead of a big day of data, the U.S. Futures point to flat but slightly lower open at the time of this report. However, with a significant day reports, anything is possible. Stay focused and flexible.

On the Wednesday earnings calendar, we have just short of 100 companies reporting quarterly results. Notable reports include SHOP, ALB, ADI, AXTA, BIDU, SAM, BCOV, FUN, CAKE, CHH, CDE, CONE, ET, EQT, FSLY, GRMN, GPC, GOOD, HVT, HLF, H, IAG, IQ, JACK, MIC, MANT, MRO, NI, OC, PAAS, SNBR, STMP, RGR, SPWR, SKT, TLRY, TWLO, WCN, WING, & WIX.

While the DIA made a new record high yesterday, it was not the kind of price action that provided a lot of confidence. I mentioned being careful of the possibility of a pop and drop pattern after the substantial gap up. Although we did pullback after the open, there was no technical damage in the price action; in fact, it could have been much worse with the concerns of rising bond yields. The bitter cold snap highlighted a significant deficiency in the U.S. power grid and exposed a massive deficiency in green energy efforts. The rolling blackouts affected a large portion of the county, with Texas being the hardest hit from the winter storm. According to reports, SpaceX raised another $850 million in funding, increasing the company valuation overnight. The European-based game developer Epic Games filed an antitrust complaint against Apple as the attack on big tech continues.

Trends remain very bullish, but with concerns of rising bond rates, U.S. Futures seem to be taking a wait-and-see approach this morning. Mortgage applications reported another decline in demand at the fastest pace in months as interest rates rise. We have a busy economic calendar with PPI and Retail Sales before the bell. The consensus expects an increase in retail numbers due to the last stimulus checks. Also, keep in mind the industrial production numbers and the FOMC minutes later this afternoon. If that’s not enough to create price volatility, toss in about 100 earings reports for the market to digest as well. Anything is possible, so stay focused on price action.

Trade Wisely,

Doug

Markets gapped up one-third to one-half of a percent Tuesday and then ground sideways to down in all 3 major indices. This left us with black-body candles that were flat for the session. For the day DIA led with a gain of 0.17% (another all-time high close) while the SPY (-0.09%) and QQQ (-0.27%) were on the red side of flat. VXX gained a little over a percent to 15.92 and T2122 fell back, but remains just inside the overbought territory at 82.87. 10-year bond yields spiked again to 1.311% (the highest in nearly a year) and Oil (WTI) rose 67 cents to close at $60.143/barrel.

The brutal winter storm continues to be the big news story. Rolling power blackouts (total blackouts in places like parts of TX) and treacherous driving conditions through the Midwest (TX to MN) are having impacts on business we well as people. Among the industries hit are Oil and Gas Fracking, which has halted throughout the Permian Basin due to the inability to ship product. As a result, Nat Gas prices spiked to $999/million BTU for next-day delivery in OK (versus $4.19/million last week). While this is the worst example, other contracts sold at $700, $620, $400, and $275/million at various hubs.

Bitcoin has set another all-time high this morning, almost touching $52,000 as major investment banks and other firms are starting to support the digital currency. Mortgage demand also fell over 5% last week as interest rates are increasing at the fastest pace in months. 30-year fixed rate mortgages now average 2.98%, with new purchase loan applications down 6% on the week.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 28,381,220 confirmed cases and 499,991 deaths. However, the number of new cases continues to fall quickly and is back down to the October level as the average new cases are now 82,841 new cases per day. However, deaths remain at a stubbornly high level of 2,270 per day. The University of Virginia has banned all in-person events after 117 new cases (including many of the UK variant) were reported on their campus yesterday. Even assuming FDA approval, JNJ will be delivering their one-shot vaccine much slower than the government had been led to believe. While 20-30 million doses by April had been expected, an apparent “miscommunication” now leads to an expectation that the number will be less than 10 million doses in that time. However, President Biden promised the country would have enough vaccine by the end of July to vaccinate every American (at least those that will take one).

Globally, the numbers rose to 110,115,976 confirmed cases and the confirmed deaths are now at 2,431,617 deaths. However, the trends are good. The world’s average of new cases continues to fall quickly and is now down to 374,515 per day. Mortality lags but is also falling, now down to 10,630 new deaths per day. South Africa has received its first shipment of the JNJ vaccine and discussions are underway as to whether to restart vaccinations (which were stopped when the MRNA vaccine was found to not work for the South African variant). And in better news, Sri Lanka has reopened their country for tourists without quarantine. However, they want no mingling between visitors and locals (and I have no idea how that would work).

Overnight, the few Asian markets that were open were mostly red. The dramatic outlier was Taiwan (+3.54%), mostly on the strength of TSM (+4.91%). In Europe, markets are mixed, but mostly red so far today. The FTSE (-0.22%), CAC (-0.03%), and DAX (-0.57%) are a typical spread with a few minor exchanges like Belgium and Portugal on the green side. As of 7:30 am, US Futures are pointing toward a flat open. The DIA is barely green (+0.03%), the SPY barely red (-0.02%) and the QQQ just red (-0.19%) at this hour.

The major economic news for Wednesday includes Jan. PPI and Jan. Retail Sales (both at 8:30 am), Jan. Industrial Production (9:15 am), Dec. Business Inventories (10 am), and Release of FOMC Jan. Minutes (2 pm). Major earnings reports on the day include ADI, ATH, CRL, COMM, ENCL, EQT, ES, GRMN, GPC, HSIC, HLT, NI, OC, SHOP, and SAH before the open. Then after the close, ALB, ALSN, AEL, AR, AXTA, BIDU, CF, CAKE, CYH, ET, HLF, IQ, MANT, MOS, NTR, OVV, PXD, RBC, SNBR, SUN, SNPS, TROX, UFPIVMI, and WCN report.

Again, with Congress gone for the week, earnings, economic news, and the winter storm are likely to drive the discussion. The bulls are still in charge of the trend, but it is the wall of worry (about overextension) that guides them, not an all-out bull charge. Be leery of any volatile moves at this point as it may signal exhaustion.

It’s all about achieving trade goals and sticking to your discipline. So, keep locking in your profits when you have them. Follow the trend, respect support and resistance levels, and don’t chase the moves you missed. Just stick with your plans, maintain discipline and work your process. Focus on getting rich slowly and not trying to hit the lottery.

Ed

Swing Trade Ideas for your consideration and watchlist: TRV, BA, SBUX, PENN, CCL, X, GOGO, CBAT, IPHI. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

While the severe cold is slowing down most of the country, the bulls remain undeterred, with the futures pointing more index records at the open. Although we have a short market week of trading, we have a week chalked full of earnings and economic reports for traders to digest. Expect price volatility to remain high as a result. Be careful chasing the morning record-setting gap with a fear of missing out. Please make sure we see follow-through buying and not the dreaded pop and drop that we can sometimes experience at market highs. Stay focused and flexible.

Overnight Asian markets rallied with lead by the HIS up nearly 2% on the day. However, European markets are trading nearly flat and have fluctuated throughout the morning, seemly concerned about the extending risk rally. The U.S. Futures don’t share that concern with the bulls charging forward, likely to set new records in the DIA, SPY, and QQQ at the open. Fasten your seatbelts as the buying frenzy continues.

As we begin a short market week, we have about 80 companies stepping up to report quarterly results. Notable reports include AAP, A, ALX, ACC, AIG, ANDE, AN, CAR, BYD, CLR, DENN, DVN, ECL, ES, EXAS, EXPD, GEO, INVH, LZB, LPX, OXY, PLTR, RNG, TRU, VNO, YNDX & ZTS.

As ugly cold snap grips, the country’s oil hits pandemic highs, with rolling blackouts due to the massive demand for power. However, the cold has not dampened the spirit of the bulls as they pushed sharply higher overnight. The 30-year Treasury yield is holding above 2%, a level not seen in nearly a year. Not satisfied with the Trump acquittal, Speaker Pelosi has announced an independent 9/11-style commission on the Capitol riot. According to reports, Australia will support the proposed media law on Facebook and Google. The new law would require the media giants to pay for the news created by other agencies. Google has threatened to turn off its search app in the country should it pass. Should other countries join in with this tactic, it would have far-reaching impacts on social media.

Though the market experienced a little price weakness last week, the futures are fired up this morning. If current prices hold until the open, the DIA, SPY, and QQQ will set new record highs a the open, with a sharp gap-up move. Trends are decidedly bullish, but I suspect the T2122 indicator will suggest a very extended condition at the open. Before chasing in with a fear of missing out, let’s make sure we see follow-through buying rather than getting caught in a classic pop a drop price pattern. We have a busy week of earnings and economic calendar news, so continue to expect wild price volatility while trying to price in the next round of government stimulus.

Trade Wisely,

Doug

Markets were dead most of the day Friday, but a strong rally on volume the last half hour took all 3 major indices on near the highs of the day. This created large-body Bullish Engulfing candles in the SPY and QQQ, while the DIA missed engulfing by 7 cents. On the day, SPY gained 0.51%, QQQ gained 0.56%, and DIA lagged at +0.11%. With that said, all 3 of the major averages closed at another all-time high close. The VXX fell over 3% to 15.74 and T2122 remains well into the overbought territory at 88.11. 10-year bond yields spiked to 1.205% and Oil (WTI) gained almost 2.5% to close at $59.66/barrel.

Also on Friday, ahead of their taking this week off, House Democrats pushed forward the parts of the relief plan that cover the $1,400 direct payments, payments to families with children (up to $3,600/child under age 6), and an extension of unemployment. These portions are out of committee and are still on track to be passed as a single “budget” bill to be reconciled with Senate versions by the end of the month. In unrelated news, President Biden called on Congress to pass “commonsense gun laws” on Sunday. The specifics called for are an elimination of immunity for gunmakers, universal background checks, and a ban on selling “assault-style” weapons and high-capacity magazines. This may well move gun stocks like RGR, SWBI, VSTO, etc.

Interesting news out of oil giant RDS. The Dutch company said on Monday that they believe the world hit “peak oil production” in 2019 with the Covid outbreak accelerating the move away from Oil. In fact, RDS said they main profit center will become liquified natural gas as time moves forward. With that said, the price of oil has hit a pandemic high this this last week, with WTI trading at $61.77 at one point, and is holding above $60 in the winter storm, which theoretically ought to stoke more production. Still, carmakers like GM are fast-tracking the move to electric vehicles with Chevy also adding 2 new electric models to their Bolt line on Monday.

Related to the virus itself, US infections continue to be of concern in the US. The totals have risen to 28,317,703 confirmed cases and 498,203 deaths. However, the number of new cases continues to fall quickly and is back down to the October level as the average new cases are now 87,603 new cases per day. However, deaths remain at a stubbornly high level of 2,481 per day. While new cases are down 62% this week, the CDC also announced Sunday that they have identified 7 new US-originated variants. Still, PFE and MRNA are contracted to deliver another 130 million doses over the next 6 weeks (versus the 70 million that have been delivered so far). So, we may be turning a corner.

Globally, the numbers rose to 109,747,785 confirmed cases and the confirmed deaths are now at 2,420,609 deaths. In good news, the world’s average of new cases is down again to 379,868 per day, but mortality remains high at 11,084 new deaths per day. NVAX announced Monday that the Phase 3 trials for its own COVID vaccine are now fully subscribed. This comes as some countries are easing social distancing measures despite warnings about relaxing too early. The latest to follow this trend are Hong Kong, Netherlands, and Israel.

Overnight, the few Asian markets that were open were mostly green. Japan (+1.28%) and South Korea (+0.52%) led the way. In Europe, markets are mostly modestly green so far today. The FTSE (+0.24%), CAC (+0.05%), and DAX (+0.03%) are a typical spread with a few minor exchanges like Portugal (+1.57%) standing out. As of 7:30 am, US Futures are pointing toward a green open. All 3 major indices are implying a moderate gap higher lower of about +0.55% on average at the opening bell.

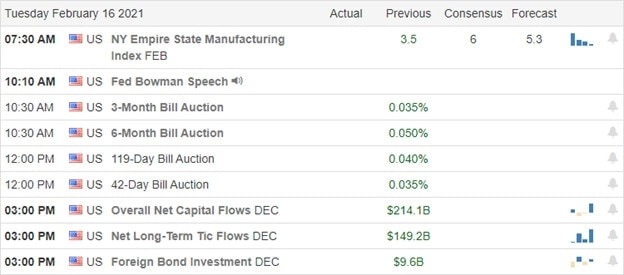

The major economic news for Tuesday is limited to NY Fed Empire State Mfg. Index (8:30 am) and a Fed speaker (Daly 3 pm). Major earnings reports on the day include AAP, ALLE, AN, BRKR, CVS, ECL, EXPD, JELD, LPX, TRU, USFD, VMC, and ZTS before the open. Then after the close, A, AIG, ANDE, CAR, BYD, CLR, DVN, MCY, and OXY report.

With Congress gone for the week and limited news today, it looks like the bulls are still in charge. The winter storm gripping most of the country is likely to dominate the news. Even earnings are limited today. So, over-extension seems to be the main thing that might slow the bulls stepping back in after the 3-day weekend.

Follow the trend, respect support and resistance levels, and don’t chase the moves you missed. It’s all about achieving trade goals and sticking to your discipline. So, keep locking in your profits when you have them. Stick with your plan, maintain discipline and work your process. Remember it’s Friday and we have a 3-day weekend coming. So, pay yourself and get your portfolio set for the long weekend.

Ed

Swing Trade Ideas for your consideration and watchlist: DAL, HYLN, UAL, VLO, WYNN, PENN, MRVL, ALLY, SOHU. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service