The Week Ahead – 2/28/21

The bears became very feisty yesterday as sharply rising treasury yields shook investor confidence. Unfortunately significant technical damage occurred in the NASDAQ, with the index closing below its 50-day average. With bearish reversal patterns left behind in yesterday’s price action and the VIX, very elevated trades should prepare for a challenging day of price volatility. As we slide into the weekend, the buy the dip confidence may be a bit gun-shy to rush back into the turbulence.

Overnight Asian markets joined in on the selloff, with the NIKKEI dropping a whopping 3.99%. European markets trade red across the board this morning. The U.S. futures point to a missed open after a choppy overnight session. With potential market-moving reports on the economic calendar, anything is possible in the open. Expect considerable price volatility.

On the Friday earnings calendar, we get a little break with just 58 companies reporting quarterly results. Notable reports include AMCX, CNK, CRON, DKNG, SSP, FL, IEP, LAMR, LBDRA, & RHP.

Rising treasury yields brought out the bears yesterday, leaving behind concerning bearish engulfing candles in the indexes. The DIA finished the day above a critical price support level, but SPY and QQQ broke support levels. On the bright side, the SPY held above its 50-day average, but unfortunately, the QQQ significantly dropped through this significant psychological level. Tensions between the U.S. Iran reached a new level after Iranian-backed militia facilities in Syria as the U.S. carried out airstrikes. The attempt to include a mandatory $15 an hour minimum wage in the stimulus bill hit a roadblock. According to the House parliamentarian, it can’t be included in the 1.9 trillion dollar stimulus bill planned for passage today. However, Speaker Pelosi defiantly stated it would stay in the bill for today’s vote.

The confidently bullish market trend suffered considerable damage yesterday. With the VIX closing the day above 28 handles, traders should expect considerable price volatility today. Be prepared for gaps and challenging intraday whipsaws. As of late, any selloff has met with a strong surge of bullishness. I suspect a good deal of that extreme confidence was shaken to the core yesterday. However, with massive stimulus just around the corner, the bears will have their work cutout if they intend to defend price resistance levels. Buckle up it could be a rough day.

Trade Wisley,

Doug

The large-caps opened flat, but the bears were in control all day. It was the same story in the QQQ, but with a significant gap down to start the day. This left us with a Bearish Engulfing signal in the DIA, and ugly large-body black candles in the other two major indices. On the say DIA lost 1.74%, SPY lost 2.41%, and QQQ lost 3.49%. The VXX gained almost 16% to 16.79 and T2122 dropped all the way down to the edge of the oversold territory at 20.22. 10-year jumped again to 1.532% as inflation fears spooked markets all day. Oil (WTI) lost half a percent to $63.18/barrel.

After the close, the Senate Parliamentarian ruled that the Democratic minimum wage hike (to $15/hr.) must not be included in the relief bill since it is being passed under budgetary rules. On the surface, this seems like a win for the GOP, which has strongly opposed the increase. However, many Democrats had hoped for this ruling, as it makes it easier for the relief bill to pass the Senate and it removes the potential party split on this topic. In either case, this makes it much more likely for the President’s $1.9 trillion relief bill gets passed in the next couple of weeks. The House is scheduled to vote on the bill today.

Another story related to the idea of a trading tax idea (an idea that was quietly revived by Liberals during the Robinhood / Reddit / Short Squeeeze story) has popped up. The idea which is a favorite of populist politicians such as Senators Warren and Sanders (as a supposed way of reducing high-frequency trading by funds), is being adopted abroad as well. In this case, Hong Kong plans to implement the same type of tax. Overnight, the Hong Kong Finance Secretary (the counter-part to US Treasury Sec. Yellen) told CNBC Asia that the tax will not harm the competitiveness of the Hang Seng exchange. He went on to say it will bring in much-needed additional government revenue, helping fund the City’s $256 billion deficit for the pandemic year. CNBC did not follow-up on whether he knew something about the plans of other countries or why he specifically feels this increased cost per trade will not make the HSI exchange less attractive.

Related to the virus, US infections are starting to plateau at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 29,052,262 confirmed cases and deaths have now passed half a million at 520,785 deaths. As mentioned, the number of new cases is starting to level-out and uptick at an average of 71,412 new cases per day. Oddly, deaths, which have always lagged, seem to be preceding this plateau and rose back up to 2,082 per day. After the close Thursday President Biden celebrated the halfway point toward his promised 100 million vaccinations in 100 days. The 50million were actually accomplished in 5 weeks. In other good news, the FDA Advisory Panel will make its decision on the JNJ vaccine on today.

Globally, the numbers rose to 113,643,803 confirmed cases and the confirmed deaths are now at 2,521,185 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases has up-ticked slightly again to 382,500 per day. However, mortality ticked down again, now at 9,296 new deaths per day. In a real show of charity, India has shipped 36 million doses of vaccine to various developing countries. This is particularly impressive given that they have 1.4 billion people of their own to vaccinate. Elsewhere in Asian, South Korea has extended its Social Distancing measures through at least March 14 as vaccinations begin in that country.

Overnight, the few Asian markets were mostly strongly in the red, with only 2 smaller markets remaining green. Japan (-3.99%), Hong Kong (-3.64%) and Taiwan (-3.03%) led Asian markets lower. In Europe, we see red across the board so far today. The FTSE (-1.56%) and CAC (-1.03%) are leading stocks lower, but the DAX (-0.67%) is not exactly a bright spot. Inflation fears seem to be the culprit as was the case in the US on Thursday. However, another mid-day happening is the Bank of England’s Chief Economist warned that the “inflationary tiger has awoken” which will reinforce market fears over inflation. As of 7:30 am, US Futures are mixed and flat after a turbulent overnight session. The DIA is pointing to a -0.10% open, the SPY is implying a +0.10% open, and he QQQQ is implying a -0.07% open at this point.

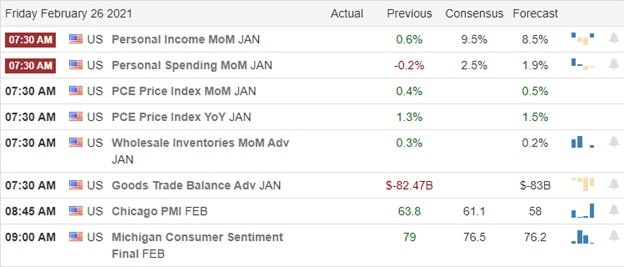

Major economic news for Friday includes Jan. PCE Price Index, Jan. Trade Balance, Jan. Personal Spending, and Jan. Retail Inventories (all at 8:30 am), Feb. Chicago PMI (9:45 am), Michigan Consumer Sentiment (10 am), and US Federal Budget (2 pm). Major earnings reports on the day include AMCX, BLDR, CRI, SSP, FLR, FL, LSXMA, and PEG before the open. Then after the close, COKE reports.

Inflation fears remain the “monster in the closet” for markets today. News out of Europe (contradicting Fed Chair Powell’s reassuring testimony about inflation earlier this week) is likely to reinforce the panic yesterday. It is also month-end, so there may be some balancing sales built into the market today after a strong February. So, have your downside protection at hand, but also be wary of the back-and-forth chop of this week.

The downtrend is obviously back in place for the major indices. If you are going to trade today, follow trend, respect support and resistance, and don’t chase those moves that you miss. However, remember that you don’t have to trade every day. Part of the trick to trading success is knowing when the market is too volatile to safely trade. Another trade will come along any minute. Achieve your ambitions in the long-run by taking short-term trade goals off the board as they are met, over and over again. Forget about predicting reversals or breakouts. Book your trade goals when you can and stick with your discipline.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas for Friday. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

In testimony to the Senate banking committee, Powell reiterated low-interest rates, and they plan to keep their foot on the gas with monetary operations. With a very dovish Fed and House planning to pass the 1.9 Trillion dollar stimulus bill, the bulls stampeded the Dow to new record highs. The Spy and the QQQ also enjoyed substantial rally though they still have overhead price resistance to clear. With a huge day of earnings and economic data coming our way, anything is possible. Buckle up for additional volatility.

Aian markets rallied strongly overnight, with the NIKKEI surging 1.67%. European markets trade mixed this morning with modest gains and losses after yesterday’s strong rally. U.S. future point to a mixed open with a massive day of data to digest.

We have a huge day on the Thursday earnings calendar with more than 230 companies reporting quarterly results. Notable reports include ADT, ABNB, ALRM, ABEV, AEP, AMT, BUD, ADSK, BBY, BYND, CZR, CWH, CM, CARS, CVNA, CNP, CLF, CUBE, DPZ, DASH, ETSY, STAY, FTCH, FSLR, FSR, GCI, GIL, HPQ, IHRT, SJM, KDP, KTOS, TREE, LYV, MAIN, MRNA, NTES, NLSN, NKLA, NCLH, PZZA, PCG, PLUG, RMAX, RKT, CRM, SEAS, SRE, SHAK, SHOO, STOR, RUN, TK, TD, VALE, SPCE, VMW, W, & ZS.

Uncle Powell reiterated in the Senate that the Fed would continue to hold rates low and keep their foot on the gas, pumping money out through continued operations. The dovish comments set a fire under the bulls lifting the Dow to new record highs as the so-called recovery stocks continued to extend. According to reports, the JNJ one-dose vaccine will soon help in the battle against the pandemic. Unfortunately, in a statement yesterday afternoon, the CDC director said the new Covid Variants could undermine all our efforts. Ugg! GameStop shares are once again surging as the Reddit crowd continues to play games with a company that is drawing attention to regulators. This week Congress proposed a 5% per trade tax, which will affect all traders. Charlie Munger, in an interview yesterday, explained that novice investors are being lured into a bubble. The 1.9 Trillion stimulus bills is expected to pass the House on Friday, and President Biden will extend the national emergency declaration.

Technically speaking, the DIA is once again showing tremendous bullishness, and through the SPY rallied strongly off of support, they still have overhead resistance to overcome. The T2122 indicator is again warning that markets are overextended but with an extremely dovish Fed and Congress ready to pump another 1.9 trillion into the economy, I’m not sure it matters. That said, be very careful overtrading and remember to take profits because if this market stumbles, the pullback could be very damaging to your accounts. With a huge day of earnings and several potential market-moving economic reports, price volatility could be very challenging.

Trade Wisely,

Doug

Markets gapped down again Wednesday, and sold off the first hour. However, as soon as Fed Chair Powell began to speak, the bulls stepped on the gas and rallied the rest of the day. This left us with strong bullish candles and the DIA even closed at another new all-time high. On the day, SPY gained 1.10%, DIA gained 1.31%, and QQQ lagged, but still gained 0.82%. The VXX fell 4% to 14.48 and T2122 jumped back into the overbought territory at 92.76. 10-year bond yield rose again to 1.383% and Oil (WTI) gained half a percent to $63.56/barrel.

Interestingly, Fed Chair Powell said that prices may rise in the coming months, but that does not mean inflation has come back. I’m not sure how that math works, especially in a time of Fed easy money policy. Still, markets took it as a sign of the Fed saying they were going to keep their foot on the gas regardless of inflation. In other Fed news, they reported a systems outage for four hours Wednesday. This means that millions of interbank transfers, payroll transactions, and even tax refunds could not be processed during that time. They reported this as a “operational error” and services were mostly restored by day end. However, the outage does raise questions about the robustness of American financial infrastructure.

VZ was the high bidder in Wednesday’s FCC’s 5G spectrum auction. The spent over $45 billion to secure over 3,500 licenses for the prime “mid-band” frequencies. T was the second highest bidder, spending over $23 billion to get 1,600 licenses. No other carrier purchased even 20% of what T bought and T bought less than half what VZ bought. This means VZ will be able to build out the largest 5G network in the country, by far.

Related to the virus and stimulus, US infections are starting to plateau at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 28,974,623 confirmed cases and deaths have now passed half a million at 518,363 deaths. As mentioned, the number of new cases is starting to level-out and uptick at an average of 70,678 new cases per day. Oddly, deaths, which have always lagged, seem to be preceding this plateau and rose back up to 2,131 per day. In more good news, NVAX said they expect to apply for FDA approval of their vaccine in Q2. As expected, House Speaker Pelosi has scheduled the vote to pass the $1.9 trillion relief bill in the House on Friday. The Senate will then consider the bill. One key issue that remains is that it will be the Senate Parliamentarian (a little know post) who decides if the $15/hr. minimum wage can be included in the bill. Democrats have told reporters privately that they hope the Parliamentarian strips that provision from the bill, because they doubt it will pass the Senate with than provision attached.

Globally, the numbers rose to 113,191,956 confirmed cases and the confirmed deaths are now at 2,510,807 deaths. The trends have been good, but we saw a significant uptick today. The world’s average of new cases has up-ticked slightly to 376,133 per day. Mortality also ticked up, now at 9,442 new deaths per day. PFE/BNTX and MRNA have both begun testing booster vaccines to fight the new UK and South African variants specifically. This would require a 3rd shot, but would extend protection, once the booster shot is proven in tests. In Europe, several of the smaller countries (like Austria) are now calling on the EU to create travel passports for those who have been vaccinated. Meanwhile Germany warned of a third wave if Europe does not reopen cautiously and France imposed a lockdown on another city (Dunkirk) due to outbreak.

Overnight, the few Asian markets were mostly in the green, with the lone exceptions of Shenzhen. South Korea (+3.50%), Japan (+1.67%), and Taiwan (+1.48%) led the way higher. In Europe, a similar story is taking shape today. Only the DAX (-0.17%) and Switzerland (-0.20%) are down, while the rest of the continent is at least above break-even. The FTSE (+0.40%) leads the way with the CAC (+0.12%) being more typical at this point of the day. As of 7:30 am, US Futures are mixed with the large-cap straddling the flat line and the QQQ pointing to a -0.76% open.

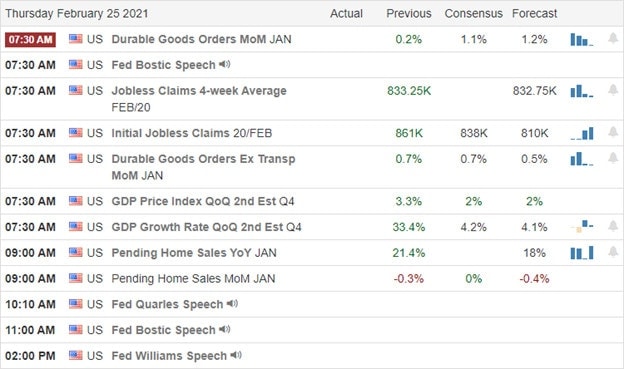

Major economic news for Thursday includes Jan. Durable Goods Orders, Q4 GDP, and Weekly Initial Jobless Claims (all at 8:30 am), Jan. Pending Home Sales (10 am), and a number of Fed speakers (Bostic at 8:30 am, Quarles at 11:10 am, Bostic again at noon, and Williams at 3 pm). Major earnings reports on the day include AES, AEP, AMT, BUD, BBY, CWH, CM, CNP, CLF, DPZ, DCI, EME, FCN, GIL, GTN, HSC, SJM, KDP, MLCO, NTES, NLSN, NOMD, PCG, PLTK, PWR, REZI, SAFM, SRCL, TD, TFX, VIPS, and W all before the open. Then after the close, ACHC, ADT, ABNB, ADSK, CZR, CVNA, FIX, CWK, DELL, DASH, EIX, ENDP, ERIE, FTCH, FND, HPQ, IHRT, LHCG, MTZ, MNST, QRTEA, REGI, RKT, CRM, SFM, TA, UHS, VALE, VMW, WDAY, and INT report.

Jobless Claims, the update on Q4 GDP, and earnings reports are likely to drive markets this morning. Markets were giddy Wednesday after Fed Chair Powell basically said “whatever it takes to get it done” to pump up the economy. However, regardless of Fed speak, rissing bond rates point to inflation and Mr. Market knows how the Fed reacts to inflation. So fear exists as well.

The downtrend is broken in the large-caps, but that question is still debatable in the QQQ as high-tech has lagged. Just follow the trend, respect support and resistance, and don’t chase those moves that you miss. Another trade will come along any minute. Remember, trading is a marathon, not a sprint. Achieve your ambitions in the long-run by hitting short-term goals over and over again. Forget about predicting reversals or breakouts. Book your trade goals when you can and stick with your discipline.

Ed

Swing Trade Ideas for your consideration and watchlist: FDX, XRT, ABBV, HON, LYFT, MU, F, TLRY. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Though a challenging and rough day of price action, Jerome Powell calmed market fears ensuring their accommodative policy will continue for the foreseeable future. The DIA roared back, holding onto the current bullish trend, but the SPY and QQQ still needs to clear overhead resistance and broken trends. With a big day of earings and another round of Powell testimony, anything is possible, and volatility is likely to remain high. However, with the House moving forward with the 1.9 trillion stimulus bill, it may be challenging the bears to garner the energy to defend market highs.

Overnight Asian markets sold-off strongly, with Hong Kong leading the way down nearly 3%. European markets are bouncing back this morning in response to the FED outlook, and U.S. futures point to modest gains ahead of a busy earnings calendar and petroleum status numbers. Keep a close eye on resistance levels just in case the bear attempt to mount a defense.

We have a big day on the earnings calendar with more than 170 companies fessing up to quarterly results. Notable reports include DDD, APA, BHC, BILI, BKNG, CSPR, LNG, EV, ELAN, ETR, EPR, EXC, FDP, GGB, LAND, GNL, HFC, HZNP, TWNK, IRM, KW, KL, LB, LOW, NTAP, NTNX, NVDA, OSTK, OMI, PBR, PSA, RDFN, RCII, RY, SIX, TDOC, TJX, UPLD, VER, & VIAC.

Jerome Powell calmed market fears saying that inflation is still soft and the Fed will stay on the gas with their current accommodation policies. The Chairman will offer more testimony today at 10 AM eastern, but we will unlikely learn anything new. Lowe’s earnings top estimates with store sale surging 28% but also warned that the trend of DIY’ers would likely fade. We have a big day on the earnings calendar, but other than the Powell testimony, a light day on the economic calendar with the Petroleum number at 10:30 AM Eastern.

After a rough day of price action, U.S. futures point to modestly bullish open when writing this report. However, with a slew of premarket earnings reports, anything is possible. The bullish trend in the DIA remains intact, but SPY and QQQ remain challenged by overhead price resistance. Will the bulls have the mettle recovering the trend, or do the bears have what it takes to defend the resistance? A question yet to be answered. As the House moving forward with the 1.9 trillion stimulus package moving lower could be difficult unless it’s already priced into the market. Stay vigilant as the price volatility adds challenge and uncertainty on the path forward.

Trade Wisley,

Doug

Markets gapped down and then put in a very volatile day as stocks rallied strong after Fed Chair Powell told us inflation was “still soft” and the Fed remains committed to the current “easy money” policies, including buying bonds. This left us with white-body indecisive candles that can be seen as Hammer candles (if you squint). On the day SPY gained 0.12%, DIA gained 0.05%, and QQQ lost 0.30%. The VXX fell 4% to 15.08 and T2122 also fell back to 72.05. The 10-year bond yields fell slightly to 1.353% and Oil (WTI) rose slightly to $61.88/barrel.

SQ bought $170 million in bitcoin Tuesday. Then overnight a 6th Chinese city launched their country’s Central Bank official digital currency ($6 million worth) as a test. Also last night, Bloomberg reported that Japan’s most expensive brokerage (Monex Group) has made a massive rally, up 136% this year, strictly on cryptocurrency bets. The story just goes to show that more and more of the world’s mainstream financial institutions and governments are starting to accept and invest in the crypto revolution. This all comes one day after Treasury Sec. Yellen warned that bitcoin was an “extremely inefficient” way to conduct monetary transactions…hinting at the need for the government to regulate those currencies and markets.

Mortgage demand plummeted 11% week-on-week on rate spikes, but may also be distorted by the winter storm impacts. In other business news, LOW announced a beat on earnings on 28% same-store sales growth. However, they warned that DIY trends could fade away as consumers return to a more normal life. OMI also beat on the topline, but unlike Lowes, OMI came in almost a percent light on revenue. Oil patch names like HFC also missed on both top and bottom lines. In the tech space, IRM missed badly on earnings (over 55%) on an almost 4% revenue miss.

Related to the virus, US infections are starting to plateau at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 28,897,718 confirmed cases and deaths have now passed half a million at 514,996 deaths. As mentioned, the number of new cases is starting to level-out and uptick at an average of 70,255 new cases per day. Oddly, deaths, which have always lagged, seem to be preceding this plateau and rose back up to 2,126 per day. With that backdrop, the White House said Tuesday that 2 million doses of the JNJ single-shot vaccine can be available next week, pending FDA approval. In addition, White House Press Sec. Psaki also said that states will now get 14.5 million doses/week (up from 8.6 million/week). President Biden also indicated that masks will be sent directly Americans.

Globally, the numbers rose to 112,739,376 confirmed cases and the confirmed deaths are now at 2,498,495 deaths. However, the trends have good until very recently. The world’s average of new cases has up-ticked slightly to 369,614 per day. Mortality also ticked up, now at 9,522 new deaths per day. In Europe, Ireland extended their lockdown through April 5. Meanwhile, Scotland is leaving lockdown and returning to a multi-tier system of restrictions, with the youngest children returning to in-person school next week. In Spain, the government said it will quadruple the number of available doses during Q2 relative to now. And in China, another Chinese vaccine maker has filed for Chinese approval after their tests show 65% efficacy (15% less effective than the first Chinese vaccine claimed).

Overnight, the few Asian markets were strongly in the red. Hong Kong (-2.99%), South Korea (-2.45%), and Shenzhen (-2.03%) led the way lower, but losses were broad and significant. However, in Europe, markets are almost all modestly green as of mid-day. The FTSE (+0.05%), and CAC (+0.13%) are flat while the DAX (+0.74%) is leading the way higher. As of 7:30 am, it appears the US is following Europe up this morning. The DIA is implying a +0.10% open, the SPY implying a +0.19% open, and the QQQ implying a +0.22% open at this hour.

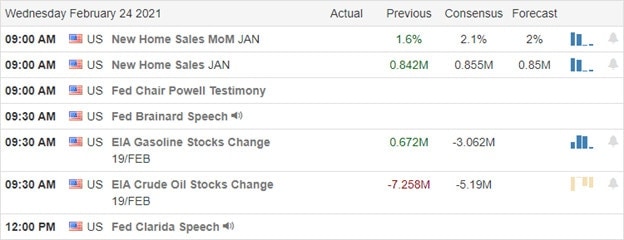

Major economic news for Wednesday includes Jan. New Home Sales (10 am), Crude Oil Inventories (10:30 am), and 3 Fed speakers (Chair Powell testifies at 10 am, Brainard at 10:30 am, and Clarida at 1 pm). Major earnings reports on the day include BHC, CQP, LNG, CLH, ELAN, ETR, EXC, HFC, HZNP, IRM, LOW, ODP, OSTK, OMI, PSN, PNW, PPD, RY, SBGI, SITE, TEN, TJX, and VRT before the open. Then after the close AMED, ANSS, APA, BKNG, BKD, CW, FNF, GEF, ICLR, LB, VAC, NTAP, NVDA, PARR, CNXN, RYI, SPTN, STN, FTI, TPC, UNVR, and VIAC report.

With little new data and Fed Chair Powell unlikely to say anything today that he didn’t say yesterday, it will be earnings reports that are likely to fill the minds of traders today. Meanwhile, the midwest (and TX in particular) are getting back to pandemic normal life as political and business fallout gathers steam. The chop and pullback of the last week were punctuated Tuesday with a high volume major intraday reversal. Is that the capitulation of bears on the pullback? I’m not sure, but it did signal the bulls are ready to jump back in at any time.

That said, the trend remains bearish on a daily level and we have to respect the trend until it is broken. Remember that knife-catching is not a long-term trading career path. Trading is a marathon, not a sprint. Achieve your ambitions in the long-run by hitting short-term goals over and over again. Forget about predicting reversals or breakouts. Just follow the trend, respect support and resistance, and don’t chase the moves you missed. Book your trade goals when you can and stick with your discipline. If you keep locking in your profits when you have them, you’ll never go bust.

Ed

Swing Trade Ideas for your consideration and watchlist: PENN, FCX, MLM, M, PINS, SNAP, APPS. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

A sad new world record was made yesterday as the U.S. topped 500,000 American Deaths due to the pandemic. However, the infection rates are declining, and there may be a light at the end of this very long and grim tunnel. Facebook struck a deal with Australia to restore service, but the tech sector remains a bit of concern after breaking the bullish trend. Jerome Powell will testify today, and it seems to have the market a bit on edge this morning, so it may be wise to keep an eye on price action as he speaks today.

Asian markets closed mixed but mostly higher overnight as HSBC topped earnings estimates. However, European markets are in decline this morning, lead by the DAX trading down over 1% this morning. The U.S. fluctuated dramatically overnight, but the premarket pump is trying to put on a brave face, currently suggesting a flat open ahead of earnings and the Powell testimony.

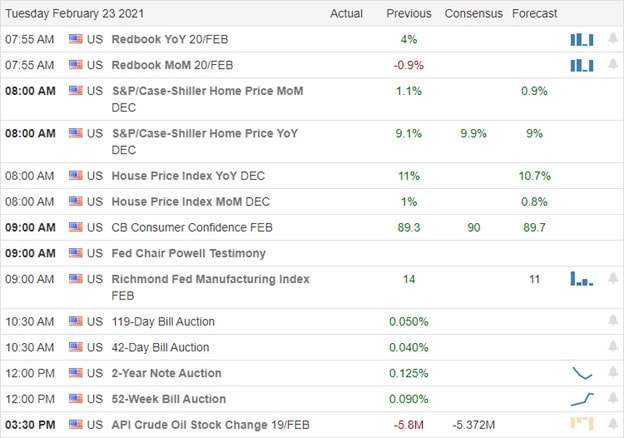

On the Tuesday earnings calendar, we have 60 companies reporting quarterly results. Notable reports include AAN, APLE, ARNC, AGR, BMO, BNS, BCO, COG, CHE, CLVS, CSGP, CBRL, DK, FLS, FI, HEI, HD, INTU, JAZZ, LDOS, M, MCFE, MDT, NXST, PXD, RRD, SPT, SQ, TRI, TOL, & UPWK.

Yesterday the U.S. hit a grim world record with more than 500,000 American deaths due to pandemic. The silver lining is that the rate of infections is declining, and vaccine availability is growing around the country. Facebook struck a deal with Australian news creators and will begin restoring the services it banded just last week. Apparently, the trending #deletefacebook struck a chord with the company leadership. Treasury Security Yellen sounded a warning yesterday about the ‘extremely inefficient way to conduct monetary transactions with bitcoin. She went on to say there remain important questions about the legitimacy and stability of the blockchain and cited dangers that it poses to investors. Home Depot tops earnings estimates this morning, reporting a 25% surge in sales. However, the stock is not seeing much price benefit from the report in the premarket.

Tech had a rough day yesterday, even as the DIA managed to squeak out a modest gain on the day. During the night, futures have fluctuated substantially between gains and losses, with the premarket pump once again lifting price off of overnight lows. We have a busy day earnings and some Jerome Powell testimony that seems to have the market a little on edge this morning. The House plans to pass the Biden Covid relief bill this week without a single bi-partisan vote in other political news setting up an interesting test for the newly formed Senate. Expect the Washington spin machine to shift into high gear in the days ahead. Technically speaking, the SPY and QQQ are beginning to raise some concerns after the selling yesterday. Stay focused and prepared for anything.

Trade Wisely,

Doug

Will the choppy price action continues this week? Rising treasury rates and jobless claims coupled with declining housing numbers added some uncertainty to the market condition. However, the indexes held onto bullish trends and price supports with the hope of big stimulus checks next month. The QQQ and SPY are the most concerning at the moment, leaving behind dark cloud cover candle patterns that suggest more lows are possible. A big week of earnings and economic data will keep us on our toes and likely continue price volatility.

Asia markets traded mostly lower overnight after China left the benchmark lending rate unchanged. European markets trade lower across the board this morning, and U.S. futures point to a bearish open as treasury yields continue to rally. Buckle up it could be a bumpy ride this morning.

We have 38 companies reporting quarterly results this Monday. Notable reports include AL, ACC, AWR, AU, BCC, CTB, CVI, FANG, DISCA, DISH, EXR, FIVN, DGOT, HTA, LSI, MRO, NHI, NLS, OXY, OKE, PANW, REAL, O, RSG, RCL, RIG, WMB, & ZI.

Every day last week started with a gap up open that immediately found sellers directly after. Overall there was little to no bearishness, just a week of a week choppy consolidating price action raising a little uncertainty. Higher jobless claims and a significant shift lower in housing as worries of rising rates battled with the expectation of more stimulus. With treasury yields climbing this morning, the bears show a bit of feistiness this morning, suggesting a lower open. Following a United Airlines engine failure, Boeing removed 24 777 aircraft from service as the FAA orders inspections. During the night, China keeps benchmark lending rates unchanged. After a brutally cold week, Texas residents are suffering once again with enormous energy bills.

Although trends remained bullish last week, choppy price action raised considerable uncertainty. The QQQ tested and held a key support area, but it looks as if it will gap below it this morning. Both the SPY and QQQ left behind dark cloud cover candle patterns raising some concern of a possible follow-through as we begin a new week. Today we have a very light economic calendar, but earnings reports will keep us on our toes. Though we have some bearishness showing this morning keep in mind with big stimulus checks expected next month, we can’t rule out the possibility of a buy the dip rally. Stay focused, avoid making rash decisions while waiting to see if the bears have the wherewithal to push on lower.

Trade Wisley,

Doug

Markets gapped up Friday, ground sideways the rest of the morning, sold off at lunchtime and then ground sideways the rest of the day. The left the 3 major indices with black candles on modest moves for the day. The SPY and QQQ printed Dark Cloud Cover type candles. On the day SPY was down 0.18%, DIA was down 0.20%, and QQQ was down 0.44%. The VXX fell over 3.5% to 15.10 and T2122 rose back into the overbought territory at 85.59. 10-year bond yields shot up again to 1.34% and Oil (WTI) fell 2.5% to $59.01/barrel.

Following on the GME hearings last week, on Friday Democratic Rep. Waters (who chairs the Financial Services Committee) said she is considering putting forward a tax on financial transactions in an effort to reduce transactions and curb high-frequency activity. The idea died on the vine a decade ago as major financial industry lobbies all opposed it. However, it has long been the dream idea of some liberals. During his campaign, President Biden said he supported the idea, but put forth no details or plans.

BA suffered another rough weekend as two US events impacted the same model plane. The 777-200 plane had cowling blow off during takeoff in one event and an engine blew up mid-flight (near Denver) in the other. The FAA has now ordered an inspection of all model 777-200 that have Pratt-Whitney engines to be inspected. The only US airline that flies that model is UAL and the airline took 24 planes out of service Sunday evening to facilitate the inspections. Separately, a BA 747-400 cargo plane also suffered an engine explosion shortly after takeoff that rained debris on a Dutch town on a flight bound for the US.

Related to the virus, US infections continue the recent trend of decreasing new cases. The totals have risen to 28,765,423 confirmed cases and deaths have now passed half a million at 511,133 deaths. However, the number of new cases continues to fall quickly and is back down to the October level as the average new cases are now 69,002 new cases per day. However, deaths remain at a stubbornly high level of 1,983 per day.

Globally, the numbers rose to 112,027,570 confirmed cases and the confirmed deaths are now at 2,479,313 deaths. However, the trends are good. The world’s average of new cases continues to fall quickly and is now down to 360,270 per day. Mortality lags but is also falling, now down to 9,398 new deaths per day. The number of new cases is rising slightly in Germany, which stands out because of the precipitous fall elsewhere. However, in the UK, PM Johnson announced a roadmap to reopening by removing restrictions step-by-step.

Overnight, the few Asian markets were mostly red. Shenzhen (-2.11%), India (-2.04%), and Shanghai (-1.45%) led the way lower. Japan (+0.46%) and Taiwain (+0.42%) were notable holdouts on the bullish side. The same is true so far today in Europe, where the only green at this point is Athens (+0.84%) and Norway (+0.77%). At mid-day, the FTSE (-0.63%), Dax (-0.58%), and CAC (-0.42%) are typical of the continent. As of 7:30am, it appears the US is following the rest of the world lower. The DIA is implying a -0.53% open, the SPY implying a -0.73% open, and the QQQ implying a -1.30% open at this hour.

There is no major economic news for Monday. Major earnings reports on the day include CTB, DISCA, DISH, KBR, and VTRS before the open. Then after the close, AL, CDNS, CVI, FANG, GFL. IR, MRO, OXY, OKE, PANW, PRIM, RSG, RIG, and WMB report.

With no data and not many major earnings reports to start the week, it looks like we will follow Europe and Asia lower. congress is bound to make some news this week as they dash to approve the Democratic or Biden Administration relief bill. Meanwhile, the midwest (and TX in particular) are trying to get back to pandemic normal life while repairing broken pipes, cleaning water damage, and in many cases dealing with electric bills in the thousands. (Many Texans pay based on power company market costs, and those skyrocketed in the last 10 days. This caused many to be without power while at the same time others had power but were paying exorbitant prices.) The sideways chop (consolidation) of the last 2 weeks has taken a toll on many in the market. However, in the longer view, bulls still have the upper hand and we remain less than a percent from all-time highs. So, beware of volatility (gap and fade we’ve seen recently), but stay on the right side of the trend until it is broken.

Remember that trading is a marathon, not a sprint. You don’t have to trade every day and don’t try to get rich quick. Do it in the long-run by hitting goals over and over again. Forget about predicting reversals or breakouts. Neither catching knives nor chasing trains is not a good career path. Just follow the trend, respect support and resistance, and don’t chase the moves you missed. Book your trade goals when you can and stick to your discipline. If you keep locking in your profits when you have them, you’ll never go bust.

Ed

Swing Trade Ideas for your consideration and watchlist: C, PFG, ADS, HCA, F, FB, CVS, HOME, URI, DFS, MGM, GE, ALLY. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service