The bulls lifted the Dow above 32,000 for the first time in history as the market celebrates the passage of one of the biggest spending bills of all time. Treasury yields also softened after a successful 10-bond auction sending industrial and consumer defensive stocks soaring as big tech continued to suffer. With more than 150 earings reports, Jobless Claims, JOLTS, and a 30-year bond auction ahead, the bulls push for another gap up open to keep the party going. Be careful not to chase such an extended rally because a significant pullback could begin at any time but until then, enjoy the ride!

Asian markets advanced overnight, led by the Hong Kong surging 1.65% at the close of the session. European markets traded mixed this morning as they chop cautiously around the flatline waiting for the next move of the ECB. U.S. Futures want the bullish party to continue pointing to a gap up open ahead of earnings and jobs data.

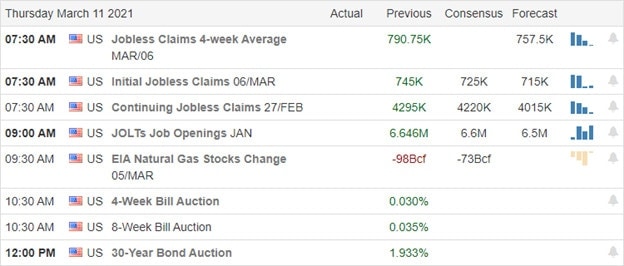

Economic Calendar

Earnings Calendar

As usual, Thursday is the busiest day of the week on the earnings calendar, with more than 150 companies reporting quarterly results. Notable reports include DOCU, LOCO, XONE, GCO, GOGO, GRDX, J.D., PRTY, PBPB, STNE, TTSH, TLYS, ULTA, MTN, WPM, & ZUMZ.

News & Technicals’

The passage of the stimulus bill lit a fire under the bulls pushing Dow above 32,000 for the first time in history. It is one of the biggest spending packages in history and the first legislative win for President Biden. Simultaneously, the President is under heavy pressure with more than 150,000 illegal border crossings in February, setting new records. The 10-year treasury yield softened slightly after a quick and successful auction yesterday afternoon. Today there will be a 30-year auction that to keep an eye on at 1 PM eastern. Denmark suspends using the AstraZeneca Covid vaccine after severe cases of blood clots reported in those vaccinated. President Biden will speak to the nation in a prime-time address on Thursday where he plans to announce the “next phase” of his pandemic response.

When it comes to the chart technicals, there is no question that bulls are large and in charge in the Dow, cementing new records prices. Although the NASDAQ has also enjoyed a nice relief rally, big tech continues to struggle with price resistance levels closing the day well below its 50-day average. Industrial and consumer defensive sectors continue to see substantial rallies as the massive rotation of the pandemic high flyers hits a fevered pitch. Be very cautious not to chase overextended stocks. With such a massive point rally in just a few days as a substantial pullback would not be out of the question and could begin at any time. Until then, enjoy the ride as the market celebrates the creation of deficit spending.

Markets gapped up about two-thirds of a percent higher in the large-caps and above 1.4% in the QQQ. After the gap-up, large caps ground sideways, while the QQQ sold off before starting its sideways grind about 11am. This left us with a Gap-up Doji in the SPY, a large white bullish candle in the DIA (which closed at an all-time high close), and a large ugly black candle in the QQQ. On the day, DIA gained 1.48%, Spy gained 0.58%, and QQQ lost 0.29%. The VXX fell over a percent to 14.60 and T2122 rose deep into the overbought territory at 96.05. 10-year bond yields fell slightly to 1.521% and Oil (WTI) rose a percent and a quarter to $64.80/barrel.

The economic news on the day was that there was enough demand for 10-year bonds at the government auction that yields pulled back slightly (higher bond prices mean lower bond yields). However, the demand was not enough to drive bond yields down strongly. All-in-all, this is an indication the bond market thinks inflation is in check for now. In addition, the House passed the $1.9 trillion relief bill as expected. So, we can expect consumers to have an injection to start spending as soon as the end of the month.

Related to the virus, US infections are starting to plateau at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 29,862,124 confirmed cases and deaths have now passed half a million at 542,191 deaths. As mentioned, the number of new cases fell again to an average of 57,621 new cases per day. Deaths, which have always lagged, was flat at 1,477 per day. President Biden directed the DHS to purchase 100 million more doses of the JNJ vaccine on Wednesday. In addition, more states eased restrictions on the day. MD is allowing “high traffic” businesses like restaurants, gyms, and retail to open without restrictions. CA announced they will be opening theme parks and outdoor stadiums as of April 1, although at reduced capacities.

Globally, the numbers rose to 118,739,789 confirmed cases and the confirmed deaths are now at 2,634,166 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases have up-ticked again slightly to 408,286 per day. Mortality, which lags continued to tick down slowly, now at 8,517 new deaths per day. In Central and Eastern Europe, the pandemic is picking up steam again. Among the countries seeing a “third wave” are Poland, Czechia, Ukraine, Romania, Serbia, Bulgaria, and Hungary. Meanwhile Denmark has suspended use of the AZN vaccine after reports that a number of patients have developed blood clots after vaccination. In Brazil, for the 2nd straight day, that country reported a new record number of covid deaths, this time almost 2,300.

Overnight, Asian markets were strongly in the green. China led the gainers with Shanghai and Shenzhen both posting +2.36%, Hong Kong up +1.65%, and Taiwan up +1.68%. In Europe, markets are mixed, but leaning to the green side so far today on modest moves. The FTSE (-0.27%) and DAX (-0.08%) are slightly lower, while the CAC (+0.16%) is slightly higher. The smaller exchanges are leading to the upside such as Portugal (+1.44%) and Denmark (+1.20%) at this point in their day. As of 7:30 am, US futures are pointing to a gap higher. The DIA is implying a +0.31% open, the SPY implying a +0.67% open, and the QQQ implying a major gap up of +1.75% open.

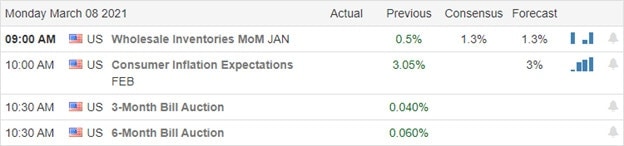

The only major economic news on Thursday are Weekly Initial Jobless Claims (8:30 am) and Jan JOLTS (10 am). Major earnings reports before the open include GCO, JB, OPCH, PAE, PRTY, and REV. Then after the close, ULTA and MTN both report.

It looks like traders are reversing the recent rotation into value names this morning. The Tech sector, which has been beaten up in the recent pullback, is looking to roar back on broad pre-market moves. There may also be general market optimism as leaks from the White House suggest President Biden will lay out a “path to normalization” in his speech tonight. Regardless of the reason, it looks like the bulls are chasing back toward new all-time highs across the board.

With that said, don’t blindly chase the gaps you miss. Make sure you are not buying into a volatility move or fade of that gap. Follow the trend, respect support and resistance, and remember another trade will be along any minute. So, control your FOMO. However, also do not try to predict reversals, just follow the market. Most importantly, keep taking your trade goals (profits) off the table when you can and stick to your discipline. Consistency is the key, not occasional home runs.

Ed

Swing Trade Ideas for your consideration and watchlist: HON, VZ, HAL, KR, JPM, ATKR, K. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls went back to work in the NASDAQ yesterday, lifting the index 3.69%, with the Dow briefly touching a new record high. However, the bulls still have a lot of ground to recover, with the QQQ, SPY, and IWM still challenged by overhead resistance. I think the big question the market has to grapple with is the bullishness of another 1.9 Trillion in stimulus and the possible bearishness that could create in interest rates and inflation. The success of the 10-year bond auction at 1 PM eastern today could be telling.

Asian markets closed mixed after a choppy session that saw selling into the close of the day. European markets seesaw this morning with modest gains and losses as the rally momentum seems to have faded. Ahead of earnings and a reading on the CPI, U.S. futures trade mixed in the premarket as inflation worries linger.

Economic Calendar

Earnings Calendar

On the Wednesday earnings calendar, we have just short of 100 companies fessing up to quarterly results. Notable reports include AMC, ASAN, BLDP, BBW, CPB, CLDR, EXPR, FOSL, FNV, LC, NGMS, SUMO, tup, UNFI, & VRA.

News & Technicals’

The bulls went back to work on Tuesday, pushing the Dow to a new high, but afternoon selling closed short of a record high close. The SPY and QQQ rallied sharply, testing resistance levels of price and downtrend, with big tech leading the gains. The U.S. House plans to pass the Senate revised stimulus bill today, and the President says he will sign it as soon as it hits his desk, adding 1.9 trillion in deficit spending. At 1:00 PM Eastern today, there will be a bond auction of the 10-year Treasuries. The last 10-year auction triggered a sharp rise in rates raising significant concerns of inflation. I may be wise to keep an eye on today’s auction if it energizes the bears for another attack. Representative Suzan DelBene is reintroducing a bill aimed at creating a national standard for digital privacy rights allowing states to build on the protections of the federal standard.

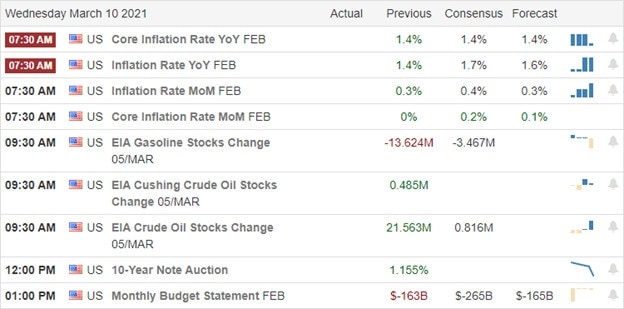

A look at the index charts, and it’s pretty easy to see the DIA is leading the way in printing a new record high before the profit-taking heading into the close. IWM is also in good condition though still challenged by some overhead resistance. Both the SPY and QQQ rallied sharply but still must address the downtrend as well as price resistance levels above. Keep in mind that that the QQQ remains the weakest of the indexes needing to recover more than 10 points to challenge its 50-day average as resistance. Before the bell, we will get the latest reading on CPI, and later today, it may be wise to keep an eye on the 10-year bond auction.

Bond yields pulled back overnight, leading to a gap strong gap higher by markets on Tuesday. After this, markets rallied all morning (strongly in the QQQ and more slowly in the large-caps). The afternoon saw more sideways action across all 3 major indices until a selloff the last 30 minutes of the day. This left us with gains, but large high-side wicks, especially the large-caps. On the day, QQQ +3.94% led the way higher, with SPY +1.40%, and DIA +0.11% flat on the day. The VXX fell 4% to 14.77 and T2122 fell a bit, but remains in over-bought territory at 85.11. 10-year bond yields fell sharply, but remain elevated at 1.537% and Oil (WTI) fell almost 2% to $63.83/barrel. It’s worth noting that after a brutal week or so, TSLA led the way in the Nasdaq at +19.64%.

Bloomberg reported an interesting fact on Tuesday afternoon. Bear in mind, it’s quite possible to drown in a river that is “on average” half an inch deep. In the article and story Bloomberg reported that analysts have looked at the S&P500 during periods of interest rate increases of at least 1.5%. That had happened 13 times since 1962 and 10 of those 13 times the S&P500 also rose. The average across all 13 instances was an S&P gain of 15%. While rates have not currently risen 1.5%, they are headed that direction with many traders eyeing inflation with fear. It’s worth considering.

The OECD released its economic forecast for 2021. They are predicting global economic growth of 5.6% on the year, with +6.5% in the US, +7.8% in China, +12.6% in India, and +3.9% in the EU compared to last year. In other economic news, US mortgage refinancing demand is down 43% from a year ago even as home purchase loan demand rose 75 for the week. This comes as average loan rates rose three basis points on the week. In addition, the $1.9 trillion covid relief bill is expected to pass today and head to the President’s desk for signing.

Related to the virus, US infections are starting to plateau at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 29,801,506 confirmed cases and deaths have now passed half a million at 540,574 deaths. As mentioned, the number of new cases fell again to an average of 58,564 new cases per day. Deaths, which have always lagged, was flat at 1,640 per day.

Globally, the numbers rose to 118,257,673 confirmed cases and the confirmed deaths are now at 2,624,252 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases have up-ticked again slightly to 404,475 per day. Mortality, which lags continued to tick down slowly, now at 8,649 new deaths per day. Mexico announced it should see results of the NVAX vaccine phase 3 trials in April. Meanwhile, Brazil reported its highest daily death total of almost 2,000.

Overnight, Asian markets were mixed again on more modest moves. Australia (-0.84%) led the losses while smaller country exchanges led the gains. China and Japan were flat on the day. In Europe, so far today markets are mostly green. The FTSE (-0.18%) is down, but the DAX (+0.36%) and CAC (+0.68%) are more typical of the continent as of mid-day. As of 7:45 am, US Futures are mixed and flat. The QQQ is pointing to a -0.13% open, the SPY to a +0.11% open and the DIA to a +0.35% open.

The major economic news on Wednesday includes Feb. CPI (8:30 am), Crude Oil Inventories (10:30 am), and Feb. Federal Budget Balance (2 pm). Major earnings reports before the open include CPB and UNFI. Then after the close, BEST and ORCL both report. However, there is a US bond auction today and given the focus that has been placed on rising bond rates recently, this auction may be a larger driver of markets than a typical auction.

With the relief bill and reopening of the economy now priced into markets, inflation has been a key focus of traders. The handicapping seems to be that if rates rise too fast, even at low levels, markets fear the Fed going to a more hawkish stance. On the contrarian side, as I pointed out above, analysis shows that most of the time, as rates rise the market goes up. Either way, that seems to be the backdrop of market direction now. As always, it’s not the news, but how the market reacts to the news this time that matters.

Follow the trend, respect support and resistance, and don’t chase those moves that you miss. Another trade will come along any minute. Don’t try to predict reversals, just follow the market. Keep taking your trade goals (profits) off the table when you can and stick to your discipline. Consistency is the key, not ocassinoal home runs.

Ed

Swing Trade Ideas for your consideration and watchlist: SNDL, MSFT, MOMO, BCRX, AA, FTNT. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday’s price action was exciting but left behind an uncertain mixed bag of results. While industrials and consumer defensive stocks enjoyed a bullish stampede, the bears had their way in the NASDAQ pushing it into the correction zone. Adding more confusion, we have 1.9 trillion in stimulus on the way, coupled with rising concerns about inflation and a plethora of shooting star patterns left behind at or near resistance levels tossed in for an extra dose of uncertainty. With the Dow up more than 1200 points in just 3-trading days, the futures are once again pumping the fear of missing out and trying to encourage traders to chase. Plan your risk very carefully.

Asian markets closed mixed but mostly higher as SHANGHAI struggled to find buyers. European markets trade green across the board this morning, keeping a close eye on bond rates. U.S. futures once again surge higher with the House planning to pass the massive stimulus bill within the next 48 hours. Be careful chasing already extended stocks and keep an eye on bond rates with a 10-year auction scheduled for Wednesday afternoon.

Economic Calendar

Earnings Calendar

We have about 70 companies reporting quarterly results this Tuesday. Notable reports include AVAV, BNED, PLCE, DQ, DKS, HRB, NAV, & THO.

News & Technicals’

Yesterday was a rather odd day in the market with the bulls stampeding into industrials and consumer defensive sector stocks while the Nasdaq suffered significant losses. The bulls seem focused on the pending 1.9 trillion dollar stimulus bill, with the House planning to complete its work in the next 24 hours. Unfortuntually, the 10-year treasury yields continue to raise inflation concerns with all newly printed money about to enter circulation. It may be wise to watch the 10-year note auction scheduled for Wednesday afternoon, keeping your fingers crossed that it goes much better than the prior. The CDC announced yesterday that people fully vaccinated against Covid could return to meeting indoors without masks, but the government continues to caution about removing mask requirements too soon.

Technically we have an uncertain mixed bag in the indexes. The DIA reached out to a new record high yesterday but lost more than half of its gains, with sellers taking profits into the close. Simultaneously, the QQQ remained under significant selling pressure dipping a full 10% from its recent highs. Toss in the shooting star patterns at or near resistance levels left behind in the SPY and IWM, and the path forward becomes even more uncertain. However, once again, the premarket pump tries to encourage traders to chase, dredging up the fear of missing out emotion. Be very careful remembering that the Dow is already more than 1200 points above its low in just 3-days of trading. With long-bonds holding at higher rates, there is a lot of risk should the bears decide to defend resistance. Plan carefully, avoid over-trading, and chasing already extended stocks.

Markets gapped slightly higher Monday, but then diverged. The DIA surged higher and then pulled back while being able to hold onto a white candle, leaving a high upper wick that could be seen as a shooting star if you squint. This came largely on a pop by DIS on reports that their Disneyland resort is expected to reopen April 1. At the same time, the SPY and especially the QQQ sold off hard to put in ugly black candles. On the day, DIA was up 0.95%, SPY was down 0.50%, and QQQ was down a whopping 2.83% (closing down 11% from the Feb. 12 record high). The VXX rose a little under 2% to 15.39 and T2122 drove higher, well into the overbought territory at 90.44. 10-year bond yields spiked again to 1.601% and oil (WTI) sold off over 2% to $64.74/barrel.

It was announced Monday that over the last week the US has averaged more than 1 million airline passengers per day. This is the first time in a year the US has reached that level of travel. This announcement came the same day that the CDC said it was okay for fully-vaccinated people (at least 2 weeks post-vaccination) to meet indoors without masks. Small steps, but signs of progress as the country is vaccinating more than 2 million people per day.

Related to the virus, US infections are starting to plateau at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 29,744,652 confirmed cases and deaths have now passed half a million at 538,628 deaths. The number of new cases fell again to an average of 58,798 new cases per day. Deaths, which have always lagged, also fell again to 1,623 per day. The Houston Health Dept. found a fairly large amount of the UK variant in their wastewater testing. The House now plans to vote (pass) on the Covid Relief Bill on Wednesday since the Senate has not yet delivered the bill as passed in their chamber. In good news, lab studies are hinting that the PFE-BTNX vaccine can give protection against the Brazilian mutation.

Overnight, Asian markets were mixed. China led the losses again as Shenzhen (-2.84%) and Shanghai (-1.82%) were down sharply. However, Japan (+0.99%). Hong Kong (+0.81%), and India (+0.95%) led to the upside. In Europe, markets are mostly green, with a couple smaller exchanges being just on the red side of flat so far today. The FTSE (+0.67%), DAX (+0.32%), and CAC (+0.36%) are all positive, with a few of the smaller exchanges being major outliers to the upside, like Denmark (+2.39%) and Portugal (+2.32%). As of 7:30 am, US Futures are strongly higher across the board as bond yields pulled back (but remains above 1.5%) overnight. The DIA is implying a +0.50% open, the SPY implying a +0.99% open, and the QQQ implying a +2.19% open.

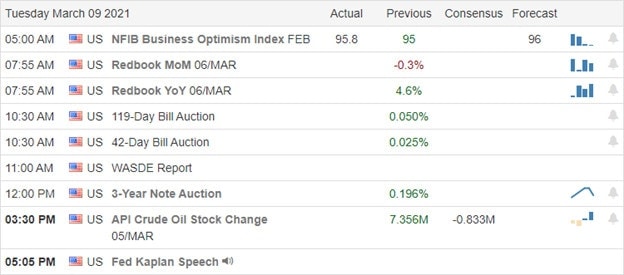

The only major economic news on Tuesday is a Fed speaker (Kaplan at 6:05 pm). Major earnings reports before the open include DKS, NAV, and THO. Then after the close, ABM reports.

Softening bond yields overnight seem to be giving the bulls energy this morning. With no planned economic news and no real major earnings, that may be enough to help them run on the day. However, there is a lot of technical damage to overcome. So, while a “V reversal” could happen, it is more likely we will see some chop as bulls become more sure of the footing before running wild. So, be prepared for volatility and one-day directional moves.

Follow the trend, respect support and resistance, and don’t chase those moves that you miss. Another trade will come along any minute. Don’t try to predict reversals, just follow the market. Keep taking your trade goals (profits) off the table when you can and stick to your discipline. Consistency is the key, not ocassinoal home runs.

Ed

Swing Trade Ideas for your consideration and watchlist: WBA, JETS, PM, JWN, UAL, DIS. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Friday brought a welcome relief raising hopes and leaving behind bullish engulfing patterns all over the place. Remember, hammer patterns must be validated with follow-through bullish price action. Soon money will begin to flow from the 1.9 trillion stimulus bill. Still, the question to be answered is can all the newly printed money overcome the consequences of rising inflation concerns as bond yields surge upward. Keep in mind the VIX remains elevated, so expect challenging price action so plan carefully.

Asian markets had a rough overnight session, with the HIS leading the declines closing down 1.92%. Across the pond, European markets trade modestly higher this morning, and the U.S. point to a flat open as investors monitor rising bond rates. Plan for choppy price action as the bulls and bears battle for control.

Economic Calendar

Earnings Calendar

On the Monday earnings calendar, we have 65 companies stepping up to report quarterly results. Notable reports include BNFT, CASY, TACO, NCMI, NIU, PVAC & SFIX.

News & Technicals’

Over the weekend, the Senate pass the 1.9 Trillion stimulus bills, and after another vote from the House, the money will begin to flow. While one would expect the market to celebrate, the newly printed money futures seem to be struggling a bit this morning. It turns out the massive printing continues to worry the market about inflation, with the 10-year Treasury yield topping 1.6%. Yemen’s Houthis attacked Saudi oil facilities this weekend, once again raising tensions in the region and pushing crude prices above $70 per barrel. The defense department stated the U.S. would hold accountable those responsible for the rocket attacks against the Iraqi base that hosts American troops.

On the technical front, last Friday’s relief rally left behind a lot of bullish hammer patterns lifting hopes that a market recovery had begun. Although buying the dip has been a good strategy in the past, I’m not sure it will work this time. Keep in mind a hammer pattern requires the price to follow-though to be valid. With rising bond rates spooking investors, can all the government stimulus still overcome the concerns of if it just made it worse? Then we still have the challenge of downtrends as well as overhead price resistance levels yet to overcome. With the VIX still elevated, I expect price action to remain challenging in the week ahead. Watch for overnight reversal and intraday whipsaws as the bulls and bears battle for control. Keep an eye on bonds, as I suspect it will be difficult for the tech sector to bounce back should they continue to rise.

Markets gapped up a percent Friday on a major beat by the Feb. Nonfarm Payrolls (379k vs 182k est.) while unemployment dipped to 6.2%. However, that gap was met with an immediate 2% selloff as fears of inflation resurfaced. Then about 11:30am, the bulls stepped in to defend the lows as bond yields lessened a touch from their highs. This led to a rally that lasted the rest of the day. This left all 3 major indices with long-wicked White-bodied Hammer type candles. On the day, the SPY gained 1.84%, the DIA gained 1.83%, and the QQQ gained 1.51%. The VXX fell 7% to 15.12 and T2122 rose back up to just outside the overbought territory at 77.18. 10-year bond yields spiked again to 1.577% and Oil (WTI) rose almost 4% to $66.28.

The Democratic relief bill hit a few snags on Friday. First, the President had to agree to a reduction from $400/week extended unemployment to $300/week. Then a WV Senator held the bill hostage for several hours related to various unemployment aspects. In the end, the Senate passed the bill Saturday in a 50-49 party-lines vote (one Republican was absent). The bill is now expected to be passed (as amended by the Senate) in the House on Tuesday before being signed by President Biden. The bill gives $1,400 direct checks to those making less than $80,000, extends unemployment at $300/week through September 6 and makes the first $10,200 of unemployment tax free for households making less than $150,000. Even with Senate passage, futures are pointing lower. So, apparently Mr. Market has already baked-in the stimulus and has moved on to other concerns.

After the close Friday, the SEC charged T and 3 of its executives with selectively sharing non-public information about the company’s investments to certain stock analysts. In return, those analysts lowered their earnings estimates to just below the level the company then reported. In other words, the SEC is claiming that T bought an “earnings beat” by giving insider data to certain specific analysts. In other market news, Pot stocks slumped for the second straight week last week. This comes as the partisan nature of Washington is being seen by industry analysts as making it much harder to get national legalization (which many had expected from a Biden administration). And in commodity news, OPEC+ members unexpectedly agreed to keep output restrictions in place. This triggered another rally in oil which now has the price of oil above the balanced-budget required price of three large producing countries. This includes Saudi Arabia, Bahrain, and Oman, with UAE and Kuwait only about $3/barrel from their own break-even prices. This was before Brent topped $70/barrel over the weekend on the OPEC+ restriction extension news.

Related to the virus, US infections are starting to plateau at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 29,696,250 confirmed cases and deaths have now passed half a million at 537,838 deaths. As mentioned, the number of new cases fell again to an average of 59,777 new cases per day. Deaths, which have always lagged, also fell again to 1,725 per day. In good news, the US has now hit the milestone of doing over 2 million vaccinations per day. However, Health officials again warned over the weekend that it is too soon to ease social distancing and especially mask mandates.

Globally, the numbers rose to 117,509,784 confirmed cases and the confirmed deaths are now at 2,606,789 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases have up-ticked again by 10,000 over the weekend to 399,523 per day. Mortality, which lags continued to tick down slowly, now at 8,715 new deaths per day. Among the places seeing a surge is Brazil, which reports it highest daily increase in new cases in over 2 months.

Overnight, Asian markets were mixed, but mostly red Monday. Shenzhen (-3.24%), Shanghai (-2.30%), and Hong Kong (-1.92%) led the move lower as China bore more most of the brunt of rising oil prices. However, Singapore (+1.90%) gained on that news. In Europe, stocks are green across the board so far today. The DAX (+1.38%) and CAC (+0.88%) are typical of the continent, but the FTSE (+0.21%) lags. As of 7:30 am, US Futures are mixed but generally down. The QQQ is implying a -1.32% open, the SPY implying a -0.49% open, but the DIA remains flat, implying a -0.01% open.

There is no major economic news on Monday. There are also no major earnings reports before the open. However, after the close, CASY and WISH report.

Inflation fears continue to grip Wall Street. Even clearing another major hurdle toward the $1.9 trillion stimulus bill has not helped the weekend mood. It looks as though Friday’s strong day is being answered by the bears pushing back today. The trend remains to the downside, but remember the bulls have recently defended a level not far below. So, volatility is to be expected.

As always, don’t try to predict, just follow the market. It’s the big money that makes the market move and we just need to tag along for the swings. Follow the trend, respect support and resistance, and don’t chase those moves that you miss. Another trade will come along any minute. Keep booking your trade goals when you can and stick with your discipline.

Ed

Swing Trade Ideas for your consideration and watchlist: DFS, DIS, F. XRT, MO, PFE, WMT, LUMN, NLSN, IVZ, MA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Jerome Powell stepped on a landmine with his inflation comments that raised some uncertainty about future interest rates. Long-term bond yields surged bring out the bears and creating substantial technical damage to the SPY and QQQ index charts. Although it was painful, the DIA and IWM holding at their 50-day averages could be a silver lining, not to mention the massive stimulus bill that’s moving through the Senate. Expect price volatility to continue as we face potential market-moving reports before the bell.

Asian markets had a rough night of volatility but ended the session only modestly lower. European market trade cautiously this morning as they monitor the inflation-sensitive long bonds. U.S. futures recovered from overnight losses, currently pointing to a flat or ever so slight bullish open ahead of the Employment Situation report. With the VIX elevated cinch up your big boy pants for another day of volatility.

Economic Calendar

Earnings Calendar

As we slide toward the weekend, we have a lighter day on the Friday earnings calendar with just 24 companies reporting. Notable reports include BIG, HIBB, & RUTH.

News & Technicals’

Reacting to Jerome Powells inflation comments where he stated the committee would ‘probably’ not raise interest rates, the market plunged sharply. The bears also gained energy as the longer-term treasuries rallied sharply as worried investors ran for the doors. The Senate cleared a hurdle yesterday, paving the way for the next round of stimulus. The hope is to have it completed by mid-March. Before the bell today, we will get the latest reading on the Employment Situation. Economists expect 210,000 jobs were created in February, up from the 49,000 last month but warn we have a long way to go before seeing a substantial employment recovery.

There is no doubt that yesterday’s price action was painful as it reacted to the Powell inflation comments. The majority of the technical damage focused on the tech sector, while the DIA and IWM managed to hold their 50-day averages. With the SPY so heavily weighted with tech giants, it also suffered substantial technical damage closing below its 50-average that now become overhead price resistance. With the VIX closing above 28 handles and turbulent overnight futures trading, expect another rough day price action. Keep an eye on the 10, 20, & 30-year treasury bonds. Should they continue to rise, the bears will likely remain in control. With market-moving economic news before the open, futures are trying to put on a positive face but stay on your toes and be ready for just about anything. Have a wonderful weekend, everyone!