Premarket Bounce and More Fed Speakers

Markets gapped down significantly Tuesday and the bears piled on to follow-through into the early afternoon. Then after a short, mid-afternoon rally, we sold off again the last hour to end the day near the lows. This left us with big, ugly black candles in all 3 major indices that printed an Evening Star failing the 50sma in the DIA and a Dreaded-h pattern in the SPY and QQQ. Tech stocks took the worst of the beating with TWTR down 4.47%, GOOG down 3.76%, FB down 3.66%, and MSFT down 3.62%. On the day SPY lost 1.97%, DIA lost 1.63%, and QQQ lost 2.77%. The VXX rose 10% to 27.37 and T2122 fell hard to just inside the oversold territory at 17.25. The 10-year bond yields rose sharply, closing a 1544% and Oil (WTI) fell 0.85% to $74.81/barrel.

During the day, it was reported that the progressive faction of the House Democrats will defy Speaker Pelosi and oppose the $1 trillion bipartisan Infrastructure bill deal unless they get a vote at the same time on the more liberal portions of President Biden’s economic agenda. Meanwhile, in the Senate, Republican members blocked another Democratic attempt to raise the debt ceiling (the second time in two days). This comes after the Treasury Dept. announced the actual date the government will no longer be able to avoid a default on US debt (without a prior debt ceiling increase) is October 18. While many pundits claimed these impasses were the cause of Tuesday’s selloff and even with no deal is in sight, it still seems unlikely the US will default. A temporary shutdown of the government is quite possible, but default really serves no party’s interests, and certainly not the country’s interest, in the long run. However, analysts say that is what the market is fearing most and could be the proximate cause of a deeper pullback.

Interest rates rose last week, with a 30-year fixed-rate mortgage averaging 3.10% (up from 3.03% the week prior). This led total mortgage applications to fall 1.1% week on week. Interestingly, the rate-sensitive refinance application number was also only 1% lower than the prior week.

In miscellaneous news, last night TSLA CEO Elon Musk told an industry conference that the US Government should avoid regulating crypto. Cryptocurrency markets took heart from this, but it is quite unlikely even a billionaire like Musk has much sway with the Feds. Bloomberg reported this morning that the FDA will approve booster shots of the MRNA vaccine (in the same way it recently approved PFE booster shots). The huge tech names that led the beating are all showing a bounce (dead cat?) in premarket action. TWTR, TSLA, NFLX, MSFT, FB, and AAPL all up over three-quarters of a percent at 7:30 am.

Overnight, Asian markets were mostly in the red. Japan (-2.12%), Taiwan (-1.90%), Shanghai (-1.83%), and Shenzhen (-1.64%) led the region lower. Hong Kong (+0.67%) and Indonesia (+0.81%) bucked the trend. In Europe, markets are strongly in the green so far today. The FTSE (+0.85%), DAX (+0.95%), and CAC (+1.21%) are typical and leading the region higher at mid-day. As of 7:30 am, US Futures are pointing to a modest gap higher. The DIA is implying a +0.46% open, the SPY implying a +0.54% open, and the QQQ implying a +0.65% open at this hour. 10-year bond yields are down to 1.51% and Oil (WTI) is trading two-thirds of a percent lower in early trading.

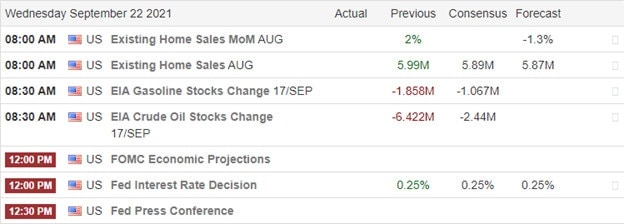

The major economic news scheduled for release on Wednesday is limited to August Home Sales (10 am), Crude Oil Inventories (10:30 am), and a trio of Fed speakers (Chair Powell at 11:45 am), Bostic at 1 pm, and Williams at 5 pm. The major earnings reports scheduled for the day include CTAS, JBL, and WOR before the open. Then after the close, MLHR reports.

After such an ugly Tuesday, traditionally we would see a rebound (at least early) as traders anticipate that the prior day’s candle was an overreaction. This seems to be taking shape in premarkets. However, whether this modest gap-up is a true reversal is a completely different question. Beware massive volatility as the fear factors, whether they be a government shutdown, US debt default (as JPM CEO Dimon started to warn yesterday), the Delta variant, or just markets in need of a correction after such a long time without one all remain in place.

Remember you don’t have to trade every day. Cash is a perfectly valid position. Nobody has ever consistently predicted reversals. So, don’t think you can either. Consider waiting if you want to be long and stay nimble if you trade short as bear moves end faster than bull moves. Focus on the process and on managing the things you can control. It’s discipline and good trading rules that separate trading success from failure over the long run. Above all, consistently take profits when you have them. A good trader refuses to let greed turn their winners into losers.

Ed

Swing Trade Ideas for your consideration and watchlist: MMAT, FLR, WRK, PLUG, TSN, DOG, SPXU, SQQQ, UVXY. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service