Strong Reports, Forecasts Buoy Bulls

Stocks gapped slightly higher on Tuesday and then ground sideways until about 3 pm, when a couple of Fed members (Bullard and Harker) told the press they DO NOT anticipate a half-point rate hike in March and that it would take another spike in inflation before they would support a half percent move. As a result, we saw a strong rally in the last hour of the day in all 3 major indices. This left us with Hammer-type white candles (longer lower wick) in all three. On the day, SPY gained 0.68%, DIA gained 0.77%, and QQQ gained 0.68%. The VXX fell another 7% to 19.86 and T2122 rose into the overbought territory at 84.69. 10-year bond yields rose to 1.796% and Oil (ETI) gained a third of a percent to $88.42/barrel.

After the close Tuesday, AMD, CB, EQR, OI, PKI, GOOG, and GOOGL all reported beats on both lines. Meanwhile, PYPL, SBUX, GILD, and AMCR beat on revenue but missed on earnings. On the other side, GM beat on earnings but missed on revenue. However, EA and MTCH missed on both lines.

In other earnings-related news, GM said they expect 2022 profits to be at record levels as the chip shortage ends (or at least eases). The stock was down slightly after hours. Meanwhile, AMD issued very strong revenue guidance for 2022, well ahead of analyst estimates (and following a 68% growth in sales during 2021). The stock soared 10% after reporting. It is also worth noting that GOOGL announced a 20-for-1 stock split effective in July. GOOGL was up 8% on the news.

So far this morning, TMO, WM, BSX, EMR, ROP, IDXX, ODFL, DHI, AVY, ABC, JCI, and MPC have all reported beats on both lines. At the same time, HUM and HWM have reported beats on earnings while coming in light on revenue.

Overnight, Asian markets were mostly green, to the extent that they were open (all Chinese markets are closed until Feb. 4th or 5th). Japan (+1.68%), India (+1.16%), and Australia (+1.17%) led the region higher. In Europe, stocks are nearly green across the board as of mid-day, with only Switzerland (-0.10%) showing any red. The FTSE (+0.89%), DAX (+0.40%), and CAC (+0.57%) are typical of the continent in early afternoon trading. As of 7:30 am, US Futures are pointing toward a green open…in particular in the tech-heavy NASDAQ. The QQQ implies a +1.72% open, the SPY is implying a +0.86% open, and the DIA implies a +0.13% open at this hour. 10-year bond yields are trading slightly lower (1.779%) and Oil (WTI) is flat in early trading.

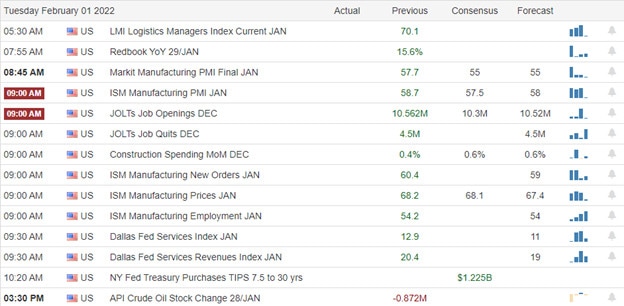

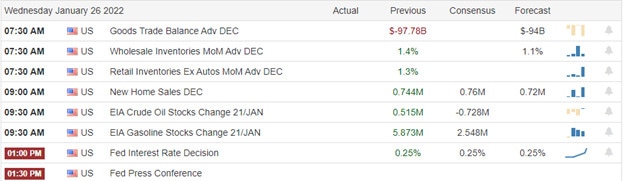

The only major economic news scheduled for release Wednesday are ADP Nonfarm Employment (8:15 am) and Crude Oil Inventories (10:30 am). Major earnings reports scheduled for before the market include ABBV, ATI, ABC, AVY, BSX, EAT, BIP, CHRW, CPRI, GIB, DHI, EMR, EVR, RACE, HWM, HUM, IDXX, JCI, MHO, MMP, MPC, MPLX, NYT, NVS, ODFL, ROP, SAIA, SBH, SR, SPR, TMO, WNC, and WM. Then after the close, AFL, ALGN, ALL, AVB, CENT, CCS, CHNG, CTSH, CTVA, DXC, FBHS, THG, HI, HOLX, LNC, MCK, FB, MET, MOD, MUSA, OMF, QRVO, QCOM, RRX, SKY, SPOT, SU, TMUS, TTEK, UGI, YELL report.

The (relief ?) rally continues and bulls are taking heart from the strong earnings news overnight. In particular, the QQQ is looking for a large gap higher on the strength of GOOG and AMD reports last night and broad-based great reports this morning. While the QQQ is gapping through its downtrend, remember that the large-cap indices have not yet reached that potential resistance. So, while the bulls have all the momentum in the short term, there is still a lot of work to do. Don’t get too “rally crazy” and start chasing.

Stick to your trading rules and manage the things that you can control. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Remember that the first rule of making money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. If you are wrong, just admit it and take your loss. (That’s why we set stops in the first place.) Trading is a marathon, not a sprint.

Ed

Swing Trade Ideas for your consideration and watchlist: VALE, BYND, PLUG, WFC, RIDE, HOOD, TSLA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service