As Jerome Powell took the notion of a 75 basis point increase off the table, the bull triggered a massive short squeeze rally as indexes surged to test price and technical resistance levels. However, I would be careful not to count the bear out if the overall downtrend remains intact. Unfortunately, the significant factors in the calculation of inflation, food, housing, and energy also surge higher on Wednesday. With a massive day of earnings, expect price volatility to remain challenging in the days ahead.

Asian markets closed mixed overnight in a choppy session after the Fed rate increase. However, European markets see only bullishness in reaction to the FOMC decision, and now the focus turns to the pending Bank of England decision. Ahead of a busy earning day, the U.S. futures point to a slightly bearish open as bond yields bounce higher in early trading.

Economic Calendar

Earnings Calendar

Thursday will be the busiest day of the week on the earnings calendar as we near 400 companies expected to report. Notable reports include ACIW, AL, APD, AMCX, BUD, APO, MT, AAWW, BLL, BDX, SQ, CAH, CHUY, CLNE, NET, COP, ED, CRSR, CROX, DDOG, DVA, D, DASH, DBX, EGLE, EOG, FND, FNKO, GCI, GOGO, GFI, GPRO, HAIN, HBI, HUBS, HII, ILMN, ICE, K, KTOS, TREE, LYV, LCID, MMP, MAIN, VAC, MCK, NWS, NKLA, NOG, NLOK, ZEUS, PZZA, PH, PENN, PBR, PBPB, PBYI, PWR, RSG, RCL, RPRX, SAIL, SEAS, SHAK, SHEL, SHOP, SWI, STLA, SPWR, SKT, TXRH, OLED, UNM, VRTX, SPCE, W, WPM, WWE, WW, YELP, Z & ZTS.

News & Technicals’

Shell’s results follow soaring profits seen across the oil and gas industry, even as many energy majors incur costly write-downs from exiting Russia. U.K. rival BP on Tuesday announced plans to boost share buybacks after first-quarter net profit jumped to its highest level in more than a decade. Shell reported a sharp upswing in full-year profit in 2021 on rebounding oil and gas prices, with CEO Ben van Beurden hailing it as a “momentous year” for the company. The Microsoft co-founder said at the Wall Street Journal’s CEO Summit Wednesday that it’s unclear how Elon Musk will change Twitter if he takes ownership. The tech billionaire’s comments come after Musk accused him of shorting Tesla stock last month. Musk also tweeted a crude joke about Gates. Facebook’s parent company sees challenges ahead because of Apple’s privacy changes, the war in Ukraine, and broad macroeconomic shifts. As a result, the company plans to stop or slow the pace of adding mid-level and senior people. CNBC’s Jim Cramer said Wednesday he’s still “drawn to owning stocks” despite concerns of a Fed-induced recession. The “Mad Money” host’s comments came after Wall Street rallied in response to Fed Chair Jerome Powell’s news conference. Cramer likes banks stocks and profitable tech companies like Advanced Micro Devices, given his economic outlook. Treasury yields are rising again this morning, with the 10-year rising five basis points to 2.97% and the 30- rising to 3.04%.

The bulls triggered a massive short squeeze after Jerome Powell suggested a 75 basis point increase is off the table for the next couple of months. The surge upward neared price resistance levels and tested 50-day moving averages as resistance but the overall downtrend in the indexes remains intact. Unfortuntually, the significant factors that affect inflation calculation also rose sharply after the rate increase. Higher rates and rising inflation may raise the concern of stagflation as more and more analysts suggest a recession is on the way. So, the big question for today can the bulls follow through with Wednesday’s rally facing a massive day of earnings events? Only time will tell, but I would not count out the bears yet while the overall downtrend still exists. Prepare for another day of wild volatility.

Swing Trade Ideas for your consideration and watchlist: BPT, STLD, AIZ, CAR, OXY, HAL, WRB, EPD, MRK, AAL, MOMO, HD, AMD, MMM. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

As traders and investors pondered the possible impacts on the economy of an aggressive Fed, the indexes struggled to pick a direction on Tuesday. Ultimately, we had our second day of relief with a last-minute surge as the indexes eked out a small gain out the close. Today, we have our busiest day of earnings events this quarter, with several economic reports likely to keep price action challenging as we head toward the FOMC rate decision and Powell’s press conference this afternoon. So, buckle up for a wild day where anything is possible!

Asian markets closed mostly lower overnight, with Hong Kong leading the selling, down 1.10%. Across the pond, European markets see red across the board as the EU proposes new oil sanctions with a Bank of England rate increase expected Thursday. Finally, ahead of a massive amount of potentially market-moving data, the U.S. put on a brave face pointing to bullish open but expect challenging price action throughout the day.

Economic Calendar

Earnings Calendar

We have a busy day with nearly 350 companies expected to report on the Wednesday earnings calendar. Notable reports include ADTN, ALB, ATI, ALL, ARMRN, ABC, ATO, GOLD, TECH, BKNG, BWA, EAT, CF, LNG, CIVI, CLH, CLVS, CXW, CTVA, CVS, DIN, EBAY, LOCO, EMR, ET, ETSY, FSLY, RACE, FSR, FTNT, FDP, GNRC, GIL, GBT, GDDY, GXO, HST, TWNK, IR, IRBT, JAZZ, JCI, LL, LITE, MRO, MAR, MET, MTG, MRNA, MUR< NBIX, NVO, NUS, OAS, PDCE, DOC, FXD, QRVO, QLYS, RYN, O, REGN, SBGI, SFM, STWD, STOR, RGR, SUN, RUN, TRIP, HEAR, TWLO, UBER, UTHR, VMC, WING & YUM.

News and Technicals’

Annual U.K. inflation hit a 30-year high of 7% in March as food and energy prices continued to soar. As a result, the Bank imposed its third hike in a row at its March meeting, taking the bank rate to 0.75%, and the market expects a 25 basis point increase to 1% when the MPC meets on Thursday. The tech billionaire, the CEO of Tesla and SpaceX, added that the social media platform will continue to be free for “casual users.” However, it’s unclear how much Musk would like to charge businesses and governments or whether certain groups such as non-profits and journalists would be exempt from any imposed fees. Twitter is already experimenting with a paid-for subscription service called Twitter Blue in the U.S., Canada, Australia, and New Zealand that offers additional features. AMD reported first-quarter earnings after the bell on Tuesday. AMD’s results on Tuesday suggest that the chipmaker is still growing fiercely, with 71% sales growth in the first quarter. Imposing measures that could reduce or entirely cut Russian energy supplies to the EU has been complicated for the bloc. Two anonymous officials said that both nations will have until the end of 2023 to halt Russian oil imports. The EU had moved last month to ban imports of Russian coal. It is now about to implement restrictions on oil purchases. And this is raising questions about whether the bloc will also stop its imports of natural gas. Lyft reported first-quarter 2022 earnings on Tuesday. Shares plunged on light guidance and continued driver incentives. Treasury yields rise ahead of the FOMC decision, with the 5-year rising to 3.00%, the 10-year ticking higher to 2.95%, and the 30-year price at 2.99%.

On Tuesday, indexes struggled to pick a direction as prices whipped between gains and losses to eke out small gains with a last-minute surge up at the close. However, the choppy price action was not a surprise as investors pondered the possible outcomes of the FOMC decision. At 2 PM eastern today, we will finally get their decision that will likely trigger an explosion of wild price action through the Powell press conference at 2.30 PM. If that’s not enough to keep traders and investors on edge, we have nearly 350 earnings reports ADP, International Trade, ISM Services, and Petroleum Statis numbers to deal with first. Expect a day jampacked with uncertainty and challenging price action where anything is possible!

On Tuesday markets opened basically flat again. All 3 major indices then road a roller-coaster the rest of the day, ending on an upswing on a very volatile day. This left us with indecisive Doji and Spinning Top candles. On the day, SPY gained 0.43%, DIA gained 0.15%, and QQQ gained 0.11%. The VXX fell 1.6% to 27.05 and T2122 rose out of the oversold territory to 39.29. 10-year bond yields rose slightly to 2.987% and Oil (WTI) fell 2.3% to $102.75/barrel.

After the close, AMD, ABNB, EXR, MTCH, SWKS, PKI, PEAK, JKHY, LFUS, ENLC, CRUS, CNR, DOOR, BXC, EIX, SCI, FNMA, and SABR all reported beats on both revenue and earnings. Meanwhile, PRU, PSA, CZR, AIZ, CNDT, BFAM, MCY, WERN, and GNW missed on revenue while beating on earnings. On the other side, SBUX, WCN, VRSK, OKE, AMCR, YUMC, LYFT, OSH, and CRK reported beating the estimates on revenue but missed on the bottom line. Finally, RNR, MCY, and AKAM reported misses on both lines.

Overnight, Chinese company DIDI fell more than 5% overnight as it was announced that the SEC is investigating the company related to its IPO. Since the company was already forced to delist from the US (US shareholders got Hong Kong shares), it is not quite clear what authority the SEC has or what legal liability the Chinese company or individuals might face. Nonetheless, the news spooked investors

On the Russian invasion story, the EU launched new sanctions to halt Russian oil sales by implementing a 6-month phase-out of Russian crude imports. Two EU countries will be given exemptions that will allow them to continue importing Russian oil until the end of 2023. Those are pro-Putin Hungary and Slovakia. The sanctions also include removing Sberbank (Russia’s largest bank by far) from the global SWIFT payment system. Lastly, a new ban prohibits European countries from offering any ships, services, or insurance to any entities for the transport of Russian oil. This could hurt Russian global oil exports, but China and India could also insure and provide ships for such shipments as well to at least some extent. These moves were largely expected but might still impact global oil prices. In other effects, CNN reported overnight that the US has now expended 35% of the US supply of Javelin missiles and 25% of the Stinger missile stockpile. While not threatening to US Defense, this will result in huge new orders to RTX, which is already working with the DoD to redesign and improve (at added cost) the Stinger.

Overnight, the never-ending saga of PR maven Elon Musk continued. He said that businesses, governments, and perhaps journalists need to start paying to access the TWTR platform. The vague statement did not address groups like non-profits, but he did say that “casual users” would continue to have access at no cost. Yet, TWTR has already begun rolling out a subscription service that adds new premium features like “undoing” tweets and adding bookmarks and folders.

Overnight, the Asian markets were mostly lower as mainland China was in it’s last day of holiday shutdown. India (-2.29%) and Hong Kong (-1.10%) were big outliers to the down side with most moves very modest in size. In Europe, stocks are nearly red across the board as the Bank of England is expected to announce a 4th-straight rate hike on Thursday. The FTSE (-0.62%), DAC (-0.08%), and CAC (-0.51%) are all lower in early afternoon trading. As of 7:30 am, US Futures are pointing toward a modest green start to the day. The DIA implies a +0.31% open, the SPY is implying a +0.34% open, and the QQQ implies a +0.26% open at this hour. 10-year bond yields are down a bit to 2.956% and Oil (WTI) is up almost 4% (on the EU-Russian oil news) to $106.19/barrel in early trading.

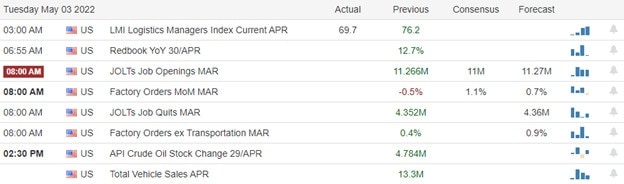

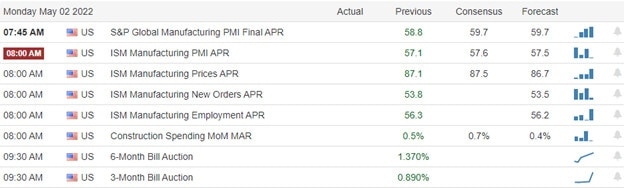

The major economic news scheduled for release on Wednesday includes ADP Apr. Nonfarm Payrolls (8:15 am), Imports/Exports and Mar. Trade Balance (both at 8:30 am), Apr. Services PMI (9:45 am), Apr. ISM Non-Mfg. PMI (10 am), Crude Oil Inventories (10:30 am), FOMC Statement and FOMC Rate Decision (both at 2 pm), and the FOMC Press Conference (2:30 pm). Major earnings reports scheduled for the day include ATI, ABC, AMRX, APG, ARKO, GOLD, BDC, BWA, BHG, EAT, BIP, BRKR, CDW, CRL, CQP, LNG, CLH, CVS, EMR, EXPI, RACE, FTS, FDP, GTES, GNRC, HZNP, IDXX, JHG, JCI, MAR, MRNA, MUR, NYT, NI, PSN, PNW, REGN, SBGI, SITE, SPR, SUN, TT, VNTR, VMC, XYL, and YUM before the open. Then after the close, ALB, ALGT, ALL, AEL, AFG, APA, ATO, BKH, BKNG, CPE, CENTA, CF, CHK, CIVI, CTSH, CLR, CTVA, CCRN, CW, DCP, CIOD, EBAY, ET, NVST, ETSY, FLEX, GFL, GIL, GDDY, GXO, HST, IR, JAZZ, LHCG, LNC, LUMN, MANT, MRO, MMS, MET, NUS, OPAD, OTEX, PTVE, PARR, PDCE, PXD, PAA, QRVO, QDEL, O, REGI, RCII, REV, RYI, SIGI, SAVE, SFM, SNEX, TTEK, TSE, TTEC, TTMI, TWLO, and UBER report.

So far this morning, REGN, AMKBY, ABC, GNRC, BWA, UTHR, SITE, PSN, GEL, VNTR, CVS, MRNA, CDW, TT, and FTS have all reported beats on both revenue and earnings. Meanwhile, VWAGY, VWAPY, GOLD, PDYPY, MUR, and FSNUY all missed on revenue while beating on earnings. On the other side, UBER, NI, FDP, BHG, and KD have reported beating the estimates on revenue but missed on the bottom line. Finally, IDXX, JHG, EAT, AMRX, and JCI reported misses on both lines.

This week we will see almost 1,500 earnings reports. On Thursday, we see APD, APO, BDX, COP, D, EOG, ILMN, ICE, MCK, MNST, MSI, PH, RSG, SRE, SQ, VRTX, WELL, and ZTS. Finally, on Friday we get CI.

All eyes are on the Fed today, even with other news and plenty of earnings on the calendar. There could be a bit of volatility in the morning, but I would not expect any definitive moves until after Fed Chair Powell’s presser (and maybe not until it is digested, which would mean Thursday). While it is very widely expected (98.5% chance per futures betting) that we will see a half percent rate increase, just as with earnings lately, the focus will be more on the forward guidance from Powell than the actual rate news (unless it is a major shock like a three-quarters of a percent move). With all this said, for now, all we know is that the trend is still very clearly bearish and that we’ve seen a very tepid relief bounce the last 2 days. Even so, “whipsaw” has been the keyword lately. So, caution is still the smart play. Don’t get caught chasing a gap only to be stuck in a reversal that you are not prepared to weather.

Remember that the first rule of making big money in the market is to not lose big money in the market. Staying hedged, nimble, and measured are good things…not bad. So, don’t be stubborn, and protect yourself from yourself. Nobody is right all the time. If you’re wrong, just admit it and take your loss. Just focus on your process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: CLX, XLE, SBUX, CVX, MOS, HAL, AR, FB, AMD, XOM, SLB. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Investors worry about an aggressive Fed and the real possibility of a recession, as a result, gave a rough start to May trading. However, in the last hour of the day, the bulls recovered the early selling leaving behind some hopeful bullish hammer patterns that still have some heavy resistance levels above. As the FOMC meeting begins, we have a deluge of earnings events and economic reports to keep traders guessing and price action challenging. Although we are overdue for a relief rally, be prepared for just about anything as the data rolls out, and we wait on the rate decision.

While we slept, Asian markets traded mixed in reaction to an Australian central bank rate increase. European markets trade with modest gains and losses waiting on the FOMC decision. U.S. futures are currently giving back overnight gains pointing to a slightly bearish open as earnings results roll out and the Fed meeting begins.

Economic Calendar

Earnings Calendar

Tuesday is a busy day with over 200 companies listed on the earnings calendar. Notable reports include AMD, PFE, AGCO, AKAM, AMCR, AIG, ANDE, ARNC, BTG, BGFV, BIIB, B.P., CZR, CWH, CNP, CPK, CRUS, LODE, CRK, CEIX, CMI, DENN, D.D., ETN, ETRN, E.L., AQUA, EXPD, EXR, BEN, I.T., GRBK, GPOR, THG, HRMY, HSIC, HLF, INCY, J, KKR, LEA, LOGI, LPX, LYFT, MPC, MLM, MTCH, MTOR, MSTR, TAP, MPLX, OKE, PRU, PSA, RDWR, QSR, ROK, SEE, SWKS, SMCI, TEVA, WAT, WLK, YUMC, & ZBRA.

News and Technicals’

On Wednesday, markets expect the Federal Reserve to announce a half-percentage point increase in its benchmark interest rate. However, fears are growing over how aggressive the central bank will have to be to tame inflation. “A recession at this stage is almost inevitable,” former Fed vice chair Roger Ferguson told CNBC. B.P.’s first-quarter underlying replacement cost profit, used as a proxy for net profit, came in at $6.2 billion. Analysts had expected B.P. to report a first-quarter profit of $4.5 billion, according to Refinitiv. The oil and gas giant also announced a further $2.5 billion share buyback. Instead, however, B.P. reported a headline loss for the quarter of $20.4 billion. This included pre-tax charges of $24 billion and $1.5 billion relating to the exit of its Rosneft stake in response to Moscow’s invasion of Ukraine. The Securities and Exchange Commission announced Tuesday that it would almost double its staff responsible for protecting investors in cryptocurrency markets. The regulator’s Crypto Assets and Cyber team, a unit of the SEC’s broader Enforcement division, will increase its headcount by 20 for 50 dedicated positions. The SEC said that the 20 additions would include investigative staff attorneys, trial lawyers, and fraud analysts. The Reserve Bank of Australia said 25 basis points would increase the cash rate to 0.35% — the first rate hike since November 2010. Analysts had widely expected the central bank to hike rates, given the rapid rise in inflation. In the last quarter, prices for food, petrol, and other consumer goods were all up. Lowe acknowledged in his statement that inflation had picked up more than expected, though it remains lower than in most other advanced economies. Treasury yields continue to inch higher in early Tuesday trading, with the 5-year up slightly to 3.02%, the 10-year trading at 2.98%, and the 30-year holding at 3.02%.

Monday got off to a rough start with investors worried about an aggressive Fed and the genuine possibility of a recession. However, the bulls finally found a surge of energy in the last hour of the day to reverse the early selling leaving behind some impressive hammer candle patterns. As we wait for the FOMC decision, the big question is, can the bulls follow through to confirm the pattern? Along with a busy earnings calendar, we will get readings on Motor Vehicle Sales, Factory Orders, and the Jobs Opening report adding to the already challenging price action. The T2122 indicator indicates we are overdue for a relief rally, but with so much uncertainty, anything is possible. So, continue to be on the lookout for intraday whipsaws and be prepared for total overnight reversals as this deluge of data rolls out.

Markets opened the week essentially flat Monday. Then an early rally lasted only the first hour before a reversal into a strong sustained selloff took us to the lows at about 3 pm. This gave way to another reversal with a strong rally in the last hour taking all 3 major indices out on or near the highs of the day. The QQQ led the afternoon rally and was the strongest of the three. This left us with indecisive candles in the large caps and a white candle with a long lower wick in the QQQ. On the day, SPY gained 0.64%, DIA gained 0.35%, and QQQ gained 1.67%. The VXX fell about three-quarters of a percent to 27.50 and T2122 rose but remains deeply oversold at 6.36. 10-year bond yields spiked up to 2.983% and Oil (WTI) rose over 1% to $105.70/barrel.

During the say, it was announced that the vote by a NY AMZN warehouse came down against unionizing by a huge margin. The warehouse, which is near the one that unionized earlier this year, voted 618 opposed to 380 for unionization. Elsewhere, AAPL was hit with another antitrust charge by the EU. This time the charge is over the “Apple Pay” monopoly where AAPL prevents competitors of Apple Pay from accessing the iPhone hardware required to implement “contactless payments” that AAPL itself enjoys.

Europe suffered its own “flash crash” Monday with many European exchanges momentarily dropping sharply. The worst-hit exchange was in Sweden, where the trouble started. The Swedish exchange dropped as much as 25% when a trader from C entered a “fat finger” trade that caused the crash and started a cascade of exchanges halting trade momentarily. There is no word as to whether this was a “spoofing” trade, which was the cause of the most recent US flash crash and is now outlawed in the US.

After the close, DVN, SANM, MGM, CC, CAR, FMC, FANG, LEG, CBT, ANET, KMT, TA, WEC, LOGI, and CACC all reported beats on both revenue and earnings. Meanwhile, WMB, CLX, and ARGO missed on revenue while beating on earnings. On the other side, NXPI, KMPR, CNO, OGS, and SEDG reported beating the estimates on revenue but missed on the bottom line. Finally, MOS, EXPE, FLS, WWD, and FN reported misses on both lines.

On the Russian invasion story, the EU has begun debating a ban on Russian oil. It appears that Hungary’s Pro-Putin regime may be a stumbling block. Analysts are expecting a specific exception for Hungary and perhaps Slovenia with the rest of the EU banning the import of Russian oil. The ban may be announced as part of the 6th round of sanctions as early as this week. C also announced it is in active discussions to sell its Russian operations (which have been closed since the start of the Russian invasion of Ukraine. Overnight, some US analysts began telling the press that they now expect Russian President Putin to actually declare war on Ukraine (so that he can institute a nationwide mobilization and draft more conscripts) very soon. Finally, it appears that Russia has dodged default again as at least some investors received dollar payments for their maturing bonds overnight in payments funneled through the London offices of C bank.

Overnight, the Asian markets were mostly in the red on modest moves with mainland Chinese exchanges still closed. New Zealand (-0.92%), Taiwan (-0.56%), and Australia (-0.42%) paced the losses. In Europe, stocks are mixed but leaning to the upside on modest moves at mid-day. The FTSE (-0.82%) lags while the DAX (unch.) and CAC (+0.13%) are typical with a few of the minor exchanges up as much as three-quarters of a percent in early afternoon trading. As of 7:30 am, US Futures point to a down start to the market day. The DIA implies a -0.45% open, the SPY is implying a -0.44% open, and the QQQ implies a -0.43% open at this hour. 10-year bond yields are down slightly to 2.967% and Oil (WTI) is off 1.5% to $103.66/barrel in early trading.

The major economic news scheduled for release on Tuesday is limited to Mar. Factory Orders and Mar. JOLTs Job Openings (both at 10 am). The FOMC Meeting also begins. Major earnings reports scheduled for the day include AGCO, AME, ARNC, BIIB, BP, BR, CTLT, CNP, CMS, CNHI, CIGI, CMI, DK, DD, ETN, EL, EXPD, FIS, BEN, IT, GEO, HSIC, HLT, HWM, ITW, INCY, ITT, J, KKR, LEA, LDOS, LGIH, LPX, MPC, MLM, MTOR, TAP, MPLX, PARA, PFE, PGR, PEG, QSR, ROK, SPGI, SMG, SEE, SGRY, TEVA, TRI, TWI, VSH, WAT, WLK, ZBRA, and ZBH before the open. Then after the close, ACHC, AMD, ABNB, AKAM, AMCR, AIG, ANDE, AIZ, BFAM, CZR, CWH, CDNT, EIX, THG, PEAK, KAR, LFUS, LYFT, DOOR, MTCH, MATX, MCY, MUSA, OSH, OKE, OMI, PKI, PRU, PSA, RNR, REZI, SCI, SWKS, SBUX, SMCI, VRSK, WCN, WERN, and YUMC report.

So far this morning, PFE, BNPQY, FIS, ETN, DPSGY, CHT, DD, AME, ZBH, IT, J, WLK, HWM, HSIC, SEE, ITT, MPLX, ZBRA, WAT, LPX and ATKR have all reported beats on both revenue and earnings. Meanwhile, BP, KKR, HLT, INCY, NHYDY, TEVA, TRTN, EL, BR, and LEA missed on revenue while beating on earnings. On the other side, BIIB, MLM, CNP, CTLT, PINC, WLKP, LDOS, and HLF have reported beating the estimates on revenue but missed on the bottom line. Finally, SPGI, ROK, ARNC, and ETRN reported misses on both lines.

This week we will see almost 1,500 earnings reports. The major reports coming later in the week include BKNG, CTSH, CTVA, CVS, EMR, FTNT, IDXX, JCI, MAR, MET, MRNA, PXD, O, REGN, and UBER on Wednesday. Then on Thursday, we see APD, APO, BDX, COP, D, EOG, ILMN, ICE, MCK, MNST, MSI, PH, RSG, SRE, SQ, VRTX, WELL, and ZTS. Finally, on Friday we get CI.

As the FOMC Meeting starts, most eyes are on that conference waiting for the outcome. While it is very widely expected that we will see a half percent rate increase from the Fed tomorrow, just as much focus will be placed on exactly what the statement says and how Chairman Powell responds to questions at the presser. So, tone matters to markets. With that said, we got a lot of mostly positive earnings last night and this morning. This might help the bulls a bit, but the premarkets have not shown this yet. Remember that the trend is still very clearly bearish, but that we have seen choppy moves (white candles, intraday reversals, and plenty of wicks in the bearish trend). Caution is still the smart play. Don’t get caught chasing a gap only to be caught in a whipsaw you are not prepared to weather.

Remember that the first rule of making big money in the market is to not lose big money in the market. Staying hedged, nimble, and measured are good things…not bad. So, don’t be stubborn, and protect yourself from yourself. Nobody is right all the time. If you’re wrong, just admit it and take your loss. Just focus on your process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: UPWK, CAR, ORCL, INTC, GT, GLW, QCOM, ROKU, FB, PINS, AA, PFE, FCX, CVE, MVIS, DOCU, EL. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Though traders hoped for another day of bullish relief on Friday, the bears roared into action, defending price resistance levels and reversing indexes to 2022 lows. As we begin a new trading week chalked full of earnings data, we also have to deal with an FOMC rate decision Wednesday afternoon. Though the market is overdue for a relief rally, the bulls will have their work cut out, so much overhead resistance and technical damage to repair in the index charts. Prepare for another week of challenging price action that could easily include wild intraday whipsaws and overnight reversals.

Asian markets traded mixed overnight as Chinese factory activity contracted in April. European markets trade mixed to mostly lower this morning after the weak China data with the U.K. market closed. With a big day of data and an FOMC decision Wednesday, the U.S. futures market point to a bullish open, hoping to spur a slight recovery after the punishing Friday selloff.

Economic Calendar

Earnings Calendar

We have a hectic week of earnings reports to keep traders guessing and high price volatility. Notable reports include AKR, AGNC, AMKR, AIRC, ANET, CAR, EXP, CBT, CHGG, CC, CLX, CVI, DVN, FANG, FN, GPN, GPRE, GPP, IPI, LEG, MGM, MCO, MOS, NE, NTR, NXPI, OHI, ON, OTTR, PK, SAIA, SIX, SEDG, TTI, RIG, & WMB.

News & Technicals’

Apple CFO Luca Maestri said supply constraints related to Covid-19 could hurt sales by between $4 billion and $8 billion. Nokia CEO Pekka Lundmark said that the Finnish telco would have grown faster in the last quarter had it not been for supply chain issues. The lockdowns in China add to short-term uncertainty, Lundmark said, about Nokia’s chip supply chain. During the Berkshire Hathaway shareholder event, Watten Buffett said inflation swindles almost everybody as he and Charlie Munger railed against bitcoin, a market mania that has turned it into a gambling parlor. Berkshire’s operating earnings were flat year over year at $7.04 billion. This comes amid a sharp drop in the company’s insurance underwriting business. The company’s net earnings came in at $5.46 billion, down more than 53% from $11.71 billion in the year-earlier period. The slowing U.S. economy impacted the flat operating results, which contracted in the first quarter for the first time since the onset of the Covid-19 pandemic. For many decades, the Nordic nation has shared an 808-mile land border with Russia and has carefully walked a foreign policy tightrope between Moscow and the West. During the Cold War, Finland adopted a neutrality policy, meaning it would avoid confrontation with Russia. But its long-standing neutrality, cherished by many Finns, could end due to Russia’s unprovoked invasion of Ukraine. Treasury yields start the week higher, with the 5-year rising to 2.95%, which remains slightly inverted over the 10-year pricing a 2.92%, and the 30-year rose to 2.99% in early trading.

The bears roared into action on Friday, triggering a brutal day of selling and quickly dashing hopes that the relief rally that began on Thursday could follow through a second day. Futures markets are trying to rebound slightly this morning, but the bulls will have their work cut out with so much technical damage to repair. Moreover, with a massive week of earnings and an economic calendar with an FOMC rate decision on Wednesday, traders should plan for another hectic week of challenging price action. To kick things off, we have PMI and ISM Mfg. reports along with Construction spending and three and six-month bond auctions. The T2122 indicator is back in an extreme short-term oversold condition. Still, with an aggressive Fed decision just around the corner, the bulls may find it challenging to overcome the bears, especially near resistance levels on the index charts. Watch for intraday whipsaws and overnight reversals this week with all uncertainty ahead.

On Friday, stocks gapped down after disappointing earnings from AMZN and even more scary guidance from INTC, AMZN, and others. After 30 minutes of finding their footing, the bears took firm control and drove markets on an all-day selloff that closed very near the lows in all 3 major indices. This left us with big, ugly, black candles in all 3 and took the QQQ to its low of the year with SPY only 0.30% above the February 24 low. On the day, SPY lost 3.58%, DIS lost 2.73%, and QQQ lost 4.38%. The VXX gained 6.4% to 27.71 and T2122 dropped deep into the oversold territory at 3.27. 10-year bond yields spiked to 2.926% and Oil (WTI) fell almost 0.9% to $104.45/barrel.

On Saturday, BRKB (Berkshire Hathaway) held its annual meeting. Among the topics discussed was the fact that BRKB bought back $51 billion worth of stock during Q1. The company also purchased 14% of OXY ($7 billion) over a 2-week period in March and significantly added to its CVX position during Q1. They also have bought 9.5% of ATVI (in a simple arbitrage bet for when the MSFT acquisition closes). Charlie Munger blasted BRKB investor CalPERS for having called for organizational changes including the replacement of Warren Buffett as Chairman. On other topics, Munger said the stock market is a “mania of speculation” and said that HOOD was “justly unraveling” for disgusting practices. He also warned people to avoid cryptocurrencies. For his part, Buffett as usual said he is having a lot of trouble finding anything worth buying and that he’s in a mode of “preparing BRKB for an economic stall” (hence the buying a big stake in non-cyclical oil companies).

Over the weekend, Bloomberg reported that China’s economy has slowed rapidly as its “Covid Zero” lockdowns are hurting deeply. The lockdowns have closed factories and other businesses, kept consumers from spending, and closed transportation systems like trucking and ports. Factory activity fell to the lowest level in 2 years with Mfg. PMI falling to 47.4 for the month. Meanwhile, Services PMI fell to 41.9 in April (the lowest level since Feb. 2020). China’s National Bureau of Statistics said that 19 of 21 sectors had seen a contraction over the month. This in itself tells you how bad it is since China is notorious for painting a rosy picture in official reports.

On the Russian invasion story, US House Speaker Pelosi led a small delegation of US lawmakers to Kyiv on Sunday for talks that included Ukrainian weapons needs. This comes in front of Congressional wrangling over President Biden’s new $33 billion aid request for Ukraine that was sent to Congress last week. In Russia, Sunday it was disclosed that $5 million worth of farm equipment (which Russians stole from a Ukrainian DE dealership since the invasion) has been remotely disabled. Dutch Dock Workers also refused to unload a tanker of Russian oil. More importantly, the German Econ. Minister Baerbock also announced that Germany would be free of dependence on Russian oil by this summer. That pulls forward the timeline for that independence by at least 3-6 months from previous estimates. This comes as the Financial Times reports Germany has now called for the EU to add a phased-in ban of Russian oil as part of a new round of sanctions on Moscow. Bloomberg also reports that Russian state-owned Gazprom reported that its gas exports fell 22% month-on-month in April. Despite this drop in supply, LNG prices have not spiked due to mild weather and increased supply from other sources, such as the LNG, SHEL, and TOT. Finally, as of Monday, Swedish Foreign Minister Linde said it is now all but certain that Sweden and Finland will both apply for NATO membership after weekend talks.

Bloomberg reported early this morning that Elon Musk sold another $4 Billion of TSLA stock in order to diversify and raise cash for his TWTR bid. Most of that selling was done on Tuesday, the day TSLA stock fell 12%. Bloomberg also says his pitch to bankers for funding for the TWTR takeover included job cuts, other cost-cutting, as well as the implementation of new ways to monetize the platform (recoup investment). However, in a bid to prevent TSLA from sliding further, Musk also added a comment to the SEC filing, saying that he has no more plans to sell TSLA stock.

Overnight, the Asian markets were lower on mostly modest moves as all the Chinese exchanges closed for a Labor Day holiday. Australia (-1.18%), New Zealand (-0.84%), and South Korea (-0.28%) paced the region Monday. In Europe, stocks are nearly red across the board at mid-day, with the sole exception of London. The FTSE (+0.47%), DAX (-0.60%), and CAC (-1.43%) are typical and lead the region as Europe digests bad Chinese data and the proposition of Energy sector sanctions on Russia. As of 7:30 am, US Futures are pointing toward a modestly green start to the day. The DIA implies a +0.40% open, the SPY is implying a +0.36% open, and the QQQ implies a +0.49% open at this hour. 10-year bond yields are down slightly from Friday to 2.912% and Oil (WTI) is off almost 3% to $101.64/barrel in early trading.

The major economic news scheduled for release on Monday is limited to Apr. Mfg. PMI (9:45 am), Apr. ISM Mfg. PMI (10 am). Major earnings reports scheduled for the day include AMG, ARLP, BRKB, CAN, EDP, FMX, GPN, GPRE, ITRI, JELD, MCO, ON, SAIA, TKR, and WEC before the open. Then after the close, ARGO, ANET, CAR, BGCP, BXP, CBT, CC, CLX, CNO, CTRA, CVI, DVN, FANG, EXPE, FN, FLS, FMC, KMPR, KMT, LEG, LOGI, MGM, MOS, NTR, NXPI, OGS, SANM, SEDG, RIG, TA, WMB, and WWD report.

So far this morning, BRKB (Saturday), EPD, WEC, GPN, TKR, SXC, and PK have all reported beats on both revenue and earnings. Meanwhile, AMG missed on revenue while beating on earnings. On the other side, CAN, and MCO have reported beating the estimates on revenue but missed on the bottom line. Finally, JELD and ARLP reported misses on both lines.

Economics news coming later this week includes Mar. Factory Orders and Mar. JOLTs Job Openings on Tuesday. Then on Wednesday, we see ADP Apr. Nonfarm Payrolls, Imports/Exports, Mar. Trade Balance, Apr. Service PMI, Apr. ISM Non-Mfg. PMI, Crude Oil Inventories, FOMC Statement, FOMC Rate Decision, FOMC Press Conference. On Thursday, we get Weekly Initial Jobless Claims, Q1 Nonfarm Productivity, and Q1 Labor Costs. Finally, on Friday we see Apr. Avg. Hourly Earnings, Apr. Nonfarm Payrolls, Apr. Participation Rate, and Apr. Unemployment Rate.

This week we will see almost 1,500 earnings reports. The major reports coming later in the week include AMD, AIG, DD, EL, FIS, HLT, ITW, KKR, MPC, PFE, PRU, PSA, SPGI, SBUX, and TRI on Tuesday. Then Wednesday we get BKNG, CTSH, CTVA, CVS, EMR, FTNT, IDXX, JCI, MAR, MET, MRNA, PXD, O, REGN, and UBER. On Thursday, we see APD, APO, BDX, COP, D, EOG, ILMN, ICE, MCK, MNST, MSI, PH, RSG, SRE, SQ, VRTX, WELL, and ZTS. Finally, on Friday we get CI.

So, another heavy week of earnings has kicked off. This morning those earnings are leaning green but are more mixed than earlier reports this quarter. As has been the case recently, it is the forward guidance that most traders are waiting to hear since the bad Q1 GDP Print last week has everyone fearing recession. With that said, remember that the trend is still very clearly bearish, but that we have seen choppy moves (white candles, intraday reversals, and plenty of wicks in the bearish trend). Caution is still the smart play. Don’t get caught chasing a gap only to be caught in a whipsaw you are not prepared to weather.

Remember that the first rule of making big money in the market is to not lose big money in the market. Staying hedged, nimble, and measured are good things…not bad. So, don’t be stubborn, and protect yourself from yourself. Nobody is right all the time. If you’re wrong, just admit it and take your loss. Just focus on your process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: HSY, UNG, MO, SQQQ, MMM, BAC, KO, LLY, KBH, GM, MSFT, AAPL, HD, BTU, SLB, HAL, AA, TSLA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although the bulls had a slow start, they finally overwhelmed the bears triggering a short squeeze relief rally. However, with a round of tech giant earnings after the bell that discontinued investors, the bulls will have their work cut out for them if they intend to follow through to the upside on Friday. As we slide into May with rate increases on the horizon, expect price action to remain challenging and an active group of bears heading into the summer.

Asian markets close green across the board overnight with the hope of more policy support from China as their economy continues to contract. European markets are green across the board this morning, boosted by earnings even as their inflation hits their 6th straight record inflation reading. Facing another round of earnings and economic data, U.S. futures point to a bearish open, with the Nasdaq leading the way.

Economic Calendar

Earnings Calendar

We have less drama on the Friday earnings calendar, with about 100 companies fessing up to results. Notable reports include ABBV, AON, AZN, B, BLMN, BMY, CBOE, CHTR, CVX, CL, COWN, XOM, HON, IMO, LHX, LYB, NWL, NMRK, PSX, SLCA, WPC, WY & WETF.

News & Technicals’

According to filings with the Securities and Exchange Commission, Elon Musk sold roughly $4 billion worth of Tesla shares in the days following his bid to take Twitter private. The bulk of the CEO’s sales were made on Tuesday, the filings showed. As a result, Tesla shares fell 12% that day but edged higher on Wednesday by less than one percentage point. As the filings became public Thursday evening, Musk wrote on Twitter, “No further TSLA sales planned after today.” Apple’s revenue grew nearly 9% year over year during the quarter ended in March. But shares fell nearly 4% in extended trading after Apple CFO Luca Maestri warned of challenges in the current quarter, including supply constraints that could hurt sales by up to $8 billion. In addition, the tech giant authorized $90 billion in share buybacks. Amazon on Thursday gave a revenue forecast that trailed analysts’ estimates. Growth rates are at their slowest since the dot-com bust in 2001. In addition, the company recorded a $7.6 billion loss on its investment in electric vehicle maker Rivian. Tensions between Russia and the West appear to have risen dramatically over the last week. In the last few days alone, Russia stopped gas supplies to two European countries and has warned the West several times that the risk of a nuclear war is very “real.” Russian President Vladimir Putin said that any foreign intervention in Ukraine would provoke what he called a “lightning-fast” response from Moscow. Treasury yields fell slightly in early Friday trading, with the 10-year dipping to 2.8386% and the 30-year slipping to 2.9145%.

The bulls had a slow start yesterday, but they ultimately overcame those feisty bears to trigger a short-covering relief rally. At the end of the day, the question on everyone’s mind is, can we get at least one more day of follow-through to the upside? Sadly after a round of disappointing big tech earnings, the bulls may find that very challenging on the last trading day of April. With the Fed planning rate increases beginning next month and the sharply contracting GDP to a negative 1.4, thoughts of a coming recession could make the bears very active this summer. Expect volatility to remain high in the weeks ahead as investors grapple with all the uncertainty.

On Thursday stocks gapped strongly higher at the open on positive earnings news. However, they immediately faded that gap, retesting the previous close, only to reverse again at 10:30 am to start a strong rally that lasted until 3:30 pm when they sold back off a bit the last 30 minutes. This left us with large white candles with large wicks at the bottom and smaller wicks at the top of the candle across all 3 major indices. (Too much wick to call any of the 3 a Morning Star pattern.) On the day, SPY gained 2.52%, DIA gained 1.88%, and QQQ gained 3.55%. However, that late-day selloff into the close gave back the T-line (8ema) in all three. The VXX lost 4.26% to 26.04 and T2122 climbed back out of the oversold territory to 31.79. 10-year bond yields were off to 2.83% and Oil (WTI) spiked 3.24% to $105.32/barrel.

Prior to the open Thursday, Q1 GDP came in much worse than expected. The number reported annualizes to a -1.4% GDP growth rate. This compares to 2021 final GDP number (+6.9%) and the analysts consensus forecast for Q1 of +1.1% (annualized). Of course, that bad number will be revised in the future. Economists also said that this print was exaggerated by temporary problems such as the Q1 supply chain bottlenecks at West Coast ports. However, despite the “don’t panic” spin, it was clearly a bad print. Nonetheless, markets ignored the bad news and gapped higher. In other economic news, the Weekly Initial Jobless Claims came in just as forecast at 180k for the week.

After the close, AAPL, INTC, GILD, WDC, SYK, MHK, AJG, OLN, KLAC, CE, AVTR, FBHS, COOP, DLR, SWN, CSL, AEM, HUBG, TEX, ATR, BIO, ENSG, TEAM, BZH, SKYW, WIRE, CENX, SM, ACA, MERC, and MATW all reported beating estimates on both revenue and earnings. Meanwhile, HIG, PFG, ATUS, CINF, LPLA, and WU missed on revenue while beating on earnings. On the other side, AMZN, EMN, SSNC, TKC, ROKU, DXCM, and ULCC beat on revenue while missing on earnings. However, RMD, DNZOY, LHX, HOOD, X, and CG missed on both lines.

In other after-hours earnings-related news, AAPL significantly beat on both lines and increased its buyback program to $90 billion for 2022. However, the company also warned of supply chain troubles (China Covid lockdowns) that could hurt Q2 numbers by between $4 billion and $8 billion. Elsewhere, AMZN lowered guidance which raises the fear that consumers are starting to be tapped out by inflated prices. They also took a $7.6 billion loss on their RIVN stake. In addition, INTC offered lower than expected guidance for Q2. Finally, HOOD reported it has fewer active users and shrinking revenue due to smaller order flow that they could sell. This is evidence that the meme stock craze and “day trading while working from home” have both decreased significantly over the last few months.

Bloomberg reported early this morning that Elon Musk sold another $4 Billion of TSLA stock in order to diversify and raise cash for his TWTR bid. Most of that selling was done on Tuesday, the day TSLA stock fell 12%. Bloomberg also say his pitch to bankers for funding for the TWTR takeover included job cuts, other cost-cutting, and implementing new ways to monetize the platform (recoup investment). However, in a bid to prevent TSLA from sliding further, Musk has added a comment to the SEC filing, saying that no more sales of TSLA stock are planned.

Overnight, the Asian markets were mostly very strongly green. Hong Kong (+4.01%), Shenzhen (+3.69%), and Shanghai (+2.41%) led the way higher. However, there were positive moves of over 1% in most exchanges. Only India (-0.83%) showed a significant loss. In Europe, stocks are mostly modestly green at mid-day. The FTSE (+0.07%) and CAC (+0.09%) lag, but the DAX (+0.68%) is typical of the region in early afternoon trading. As of 7:30 am, US Futures are pointing toward a gap down and red start to the day. The DIA implies a -0.44% open, the SPY is implying a -0.89% open, and the QQQ implies a -1.18% open at this hour. 10-year bond yields are trading up at 2.871% and Oil (WTI) is up over 1% to $106.61/barrel in early trading.

The major economic news scheduled for release on Friday includes Mar. PCE Price Index, Q1 Employment Cost, and Mar. Personal Spending (all at 8:30 am), Chicago PMI (9:45 am), and Mich. Consumer Sentiment (10 am). Major earnings reports scheduled for the day include ABBV, AB, AON, ARCB, AZN, BLMN, BMY, CRI, CBOE, CHTR, CVX, CL, XOM, HE, HON, IMO, LHX, LYB, MGA, NWL, NMRK, NVT, PSX, SYNH, TRP, and WY before the open. There are no major earnings reports scheduled for after the close.

So far this morning, AZN, BMY, HON, LYB, PSX, WY, CX, and CRI have all reported beats on both revenue and earnings. Meanwhile, CHTR, AON, SXT, and TAL all missed on revenue while beating on earnings. On the other side, XOM, CVX, CL, and CNX have reported beating the estimates on revenue but missed on the bottom line. Finally, CG, TIGO, and UOVEY reported misses on both lines.

The final flurry of earnings reports (in an earnings blizzard week) came last night and this morning. Again, the numbers were mostly positive, but not all were good and the devil is in the details. Also, the forward guidance (which has struck fear in many traders) has disappointed. With that said, remember that the trend is still very clearly bearish in the mid-term, despite a strong day Thursday. And whipsaw continues to be the norm recently. So, beware of a potential gap-and-reverse move after the open. Caution is still the smart play, especially with the weekend news cycle ahead. Don’t get caught chasing a gap only to be caught in a whipsaw you are not prepared to weather.

Remember that it’s Friday. So pay yourself. Also bear in mind that the first rule of making big money in the market is to not lose big money in the market. Staying hedged, nimble, and measured are good things…not bad. Also, don’t be stubborn, and protect yourself from yourself. Nobody is right all the time. So, if you’re wrong, just admit it and take your loss. Trading is not a sprint, it’s a marathon. Just focus on your process and enjoy yourself. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service