Stocks Face Second Gap Down But Now Oversold

Stocks gapped down over a percent on Wednesday as fear of Fed hawkishness and inconclusive news from major retailers on consumer spending led to uncertainty. The bad news for any bulls was that this led into a strong selloff that lasted the entire rest of the day in all 3 major indices. Only a bounce the last 5 minutes of the day prevented us from going out on the lows. This left us with big, ugly black gap-down candles in all 3 major indices and nearing the breakout of a Dreaded-h pattern in all 3. On the day, SPY lost 4.03% (worst day since June 2020), DIA lost 3.53%, and QQQ lost a whopping 4.91%. The VXX rose 5.24% to 26.09 and T2122 dropped back deep into the oversold territory at 5.08. 10-year bond yields dropped back to 2.884% and Oil (WTI) fell 2.8% to $109.25/barrel.

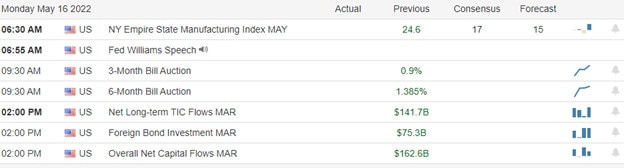

During the day, April Building Permits and Housing starts both came in below forecast. This falls in line with spiking mortgage rates that have seen declines in mortgage applications in recent weeks and may be a sign of the housing market bidding wars slowing. However, the big miss of the day was current crude oil inventories, which came in 4.7 million barrels lower than expected (-3.394 mil actual vs +1.383 mil est.). After hours, the CEO of UAA announced he will be stepping down as of June 1.

SNAP Case Study | Actual Trade

On the Russian invasion story, China is now in talks with Russia to buy a huge amount of Russian oil to fill their strategic oil reserves. Even at a steep discount to market price, this would be a huge financial boost to Russian coffers. However, Russian GDP growth missed expectations during Q1. Russian GDP came in at +3.5% (versus +3.7% that was forecast), down from the +4% during Q4. Since almost all of this drop-off came during the last month of the quarter, we can see the impacts of sanctions…even with soaring energy prices to boost numbers.

In addition to reporting earnings this morning, KSS also slashed forward guidance on both sales and profits. This came as the company said it expects to have received the last of the expected buyout offers in the next few weeks. There are known bids from FRG, another from SPG (who wants to combine KSS with former JCPenney), as well as a separate private equity group. It is unknown who the additional bidder(s) may be that the company is waiting for in the next few weeks.

Overnight, Asian markets were mostly in the red. Only Shenzhen (+0.38%) and Shanghai (+0.36%) managed gains while India (-2.65%), Hong Kong (-2.54%), and Japan (-1.89%) paced the losses. In Europe, we see red across the board at mid-day. The FTSE (-2.36%), DAX (-2.10%), and CAC (-1.75%) lead the way and are typical of the region in early afternoon trading. As of 7:30 am, US Futures are pointing toward a second straight significant gap lower. The DIA implies a -1.12% open, the SPY is implying a -1.15% open, and the QQQ implies a -1.23% open at this hour. 10-year bond yields are down strongly to 2.839% and Oil (WTI) is off 1.77% to $107.65/barrel in early trading.

The major economic news scheduled for release Thursday includes Weekly Jobless Claims and Philly Fed Mfg. Index (both at 8:30 am), and April Existing Home Sales (10 am). Major earnings reports scheduled for the day include WMS, BJ, KSS, and VIPS before the open. Then, after the close, AMAT, DECK, FLO, PANW, ROST, and VFC report.

So far this morning SQM, BJ, EXP, and MBT have reported beats on both lines. At the same time, KSS and WMS both reported beating the estimates on revenue but missing on the bottom line. On the other side, VIPS missed on revenue while beating on earnings. Finally, PLCE missed on both revenue and earnings.

After Wednesday’s rout in the market, fear has spread. The signal of this is bond yields dropping as investors stash money n bonds, bidding up their price (and thus push down yields). The bond market has also seen much more volatility in the last few days as skittishness has now infected bond markets as well. The proximate cause most talking heads point to is concern over economic slowdown (not inflation). Whether those analysts are right or not, when you add geopolitical risk to the mix, markets are just plain uncertain and nervous. So, continue to be very careful. The short and mid-term trends are bearish, the mid-term move is getting a bit long in the tooth. Plus in the short-term (as shown by T2122), we are oversold and have the potential support of a “bear market level” (down 20% from highs) in the area. So, remain nimble and hedged. Above all, don’t give in to FOMO and feel the need to chase a move or predict a reversal either way.

Trading is a job, not a lottery ticket. So, work the process. Stick with your trading rules and manage the things that you can control while trying not to worry about the things you have no control over at all. Trade with the trend, don’t chase, keep consistently taking profits when you have them, and move your stops in your favor. Also, remember that the first rule of making big money in the market is to not lose big money in the market. So, don’t be stubborn, and protect yourself from yourself. Keep in mind that nobody is right all the time. When you’re wrong, just admit it and take your loss. As they say, the best time to have taken a $500 loss is when you are now staring at a $1,500 loss.

Ed

Swing Trade Ideas for your consideration and watchlist: MO, ADM, MOS, SLB, NTR, RBLX, BTI, AMD. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service