Though this week’s uncertainty created some profit-taking in Friday’s market, the substantial earnings speculation continued despite the lowered expectations as the talking heads hyped the possibilities. Trader’s have one more day before the FOMC meeting begins; the fireworks show ignites with MSFT reporting after Tuesday’s bell. Plan for wild price gyrations and prepare for substantial morning gaps as the market reacts to the data. This week could be the make-or-break point for a bullish rally, so plan carefully and avoid overtrading due to the massive risks.

Asian markets closed mostly lower overnight as tech stocks slipped, and the China banking and real estate pressures created downgrades. However, European markets see nothing but green this morning as they wait on the big week of data. U.S. futures reversed early selling, pointing to a bullish gap open with high hopes of good giant tech earnings results and a less aggressive FOMC rate increase. Be careful to ingest too much hoipum while we wait!

Economic Calendar

Earnings Calendar

We have a very busy earnings week highlighted by market-moving tech giant reports. Notable reports include AGNC, BOH, BRO, CDNS, CVLG, CR, DX, WIRE, FFIV, PHG, NEM, NXPI, PKG, PETS, PCH, SMBK, SCCO, SQSP, SUI, & WHR.

News & Technicals’

According to a report published late Thursday, Goldman Sachs slashed its earnings outlook for the MSCI China stock index to zero growth for the year, down from 4%. China’s property market has come under renewed pressure in the last several weeks as many homebuyers stopped mortgage payments. The property market might take five years to recover from oversupply in China’s smaller cities, according to Henry Chin, head of research for Asia-Pacific at CBRE. China’s securities regulator told CNBC in a statement it has not researched a plan for a three-tiered system to help Chinese companies avoid U.S. delisting. The China Securities Regulatory Commission added that companies should comply with data security and listing rules, regardless of whether they were going public on the mainland or abroad. The regulator said other information about ongoing discussions with U.S. regulators should come from official announcements. For example, the WHO declared monkeypox a global health emergency. The rare designation means the WHO now views the outbreak as a significant enough threat to global health that a coordinated international response is needed. The WHO last issued a global health emergency in January 2020 in response to the Covid-19 outbreak. Europe is the epicenter of the outbreak. Right now, men who have sex with men are the community at the highest risk. The WHO chief said the global risk is moderate, but the threat is high in Europe. The WHO chief said that monkeypox is unlikely to disrupt international trade or travel right now. World leaders swiftly condemned Russian missile strikes on a Ukrainian port. The dramatic revelation comes from a U.N.-brokered deal that secured a sea corridor for grains and other foodstuff exports. The strike on Odesa, Ukraine’s largest port, illustrates yet another anxious turn in fruitless efforts to mitigate a mounting global food crisis. Treasury yields moved slightly higher in early Monday trading, with the 2-year trading at 2.99%, the 5-year at 2.88%, the 10-year at 2.80%, and the 30-year trading at 3.04%.

The miss on the PMI and the uncertainty of tech giant earnings ahead created some profit taking on Friday though substantial earnings speculation remained high. Overnight futures traded negative as Asian markets sold off, but the premarket pump recovered loss despite the uncertainty of all the market-moving data coming our way this week. However, today we have one more day for the talking heads, analysts, and traders to pontificate, predict, and gamble on what comes next. It all begins on Tuesday with the beginning of the FOMC meeting and the MSFT report after the bell. We should expect wild price volatility and the potential of significant morning gaps as the market gaps. Anything is possible, so plan your risk carefully and remember one of the primary jobs of a trader is to protect your capital!

Markets opened mixed on Friday, ran up the first 30 minutes, and then reversed into a strong selloff into 2:15 pm. The bulls then stepped back in to lead a small counter rally from 2:15 into the close. Eight of the 10 sectors are in the red with Technology leading the charge lower after Thursday night’s big miss by SNAP. Utilities were the only sector to manage to stay significantly green as traders sought safety. On the daily chart, the result was that all 3 major indices touched 6-week highs before retreating. This action is left us with a bearish Dark Cloud Cover candle in the SPY (and close to one in the DIA). Both also appear headed back down to retest their 50sma (which are now close below) as support. Meanwhile, the QQQ just printed a big, ugly black candle with larger wicks on both ends of the body.

Yet again, volume was very light on the day, far below the average for the SPY, DIA, and QQQ. On the day, SPY lost 0.93%, DIA lost 0.42%, and QQQ lost 1.75%. The VXX rose nearly 1% to 21.40 and T2122 fell but remains inside the overbought territory at 85.78. 10-year bond yields also plummeted for the same reason, running down to 2.73% before closing at 2.754% as markets bought up bonds. Oil (WTI) is down only 1.31% to $95.09/barrel. Friday’s move also saw us give back some of the gains for the week, creating Spinning Top type candles in all 3 major indices on a weekly chart.

In China news, Macau casinos (as well as many other businesses) reopened on a limited scale on Saturday. The reason for the slowed reopening is many restrictions remain in place. In the Chinese Real Estate sector, the CEO and CFO of defaulted property company Evergrande Group have resigned. Elsewhere, China continues to complain and warn about a potential trip by Speaker of the House Pelosi to Taiwan. The Washington Post reported that the Biden Administration is now worried about the trip and may do some horse-trading with China to get something in exchange for stopping Pelosi from making the trip. Finally, Sunday the Financial Times reports that major US-listed Chinese companies (including BABA, BIDU, and JD) have come up with a 3-tier data storage and audit strategy that they believe will allow them to remain listed in the US while complying with both Chinese and American regulations. The idea is that all data will be classified as non-sensitive, sensitive, or secretive data and different auditors would be allowed access to different tiers of data.

On the Russian invasion story, we have passed 150 days of war and are now working on the 6th month. Russia surprised markets Friday with a 150-basis-point rate cut (analysts had expected a 0.50% cut). This seems to indicate Russian concern over their economy. Related to grain, Ukraine and Russia did sign an agreement to allow the reopening of the Ukrainian Black Sea ports for grain shipments. This caused a major decrease in grain prices globally Friday. However, less than 24 hours after they signed the agreement, Russia launched multiple missile attacks on the port of Odesa. Meanwhile, Germany stepped in with a $15.3 billion bailout of German gas company Uniper on Friday afternoon. The deal also allows Uniper to start passing along some of the soaring gas price increases to end consumers (which were prohibited in the past). Meanwhile, the US has approved a 16th military assistance package for Ukraine. More importantly, the Pentagon also says the US is now ready to give/lease Ukraine jets in future packages, including the A-10 Warthog (tank buster made by NOC) and F-16 (a fighter from GD).

In business news, after the close Friday, UBER admitted to covering up a 2016 hack of their systems which affected 57 million passengers and drivers. This was part of a non-prosecution agreement with the FTC. On the other hand, TMUS agreed to pay $350 million plus spend another $150 million on security upgrades to settle litigation over a 2021 cyberattack affecting 76.6 million customers. (They are expected to take a $400 million Q2 charge over the matter.) A Hyundai subsidiary in Alabama has been accused of using child labor (including a 12-year-old boy, his 14-yeard old sister, and 15-year-old brother). The Hyundai subsidiary denied responsibility saying they relied on 3rd-party temporary work agencies to fill assembly plant jobs and expects them to remain in compliance with all labor laws. On Sunday, 2,500 workers at 3 BA (Defense division) plants rejected a contract (over the removal of a pension and funding level in 401K contributions) and announced they will strike on August 1.

So far this morning, INFY, NEM, and RPM have all reported beats on revenue while missing on earnings. RHG reported in line with expectations on both lines. DORM beat on both revenue and earnings, but also lowered forward guidance.

Overnight, Asian markets leaned heavily toward the downside, but on modest moves. Shenzhen (-0.83%), Japan (-0.77%), and Shanghai (-0.60%) paced the losses with only Thailand (+0.49%), South Korea (+0.44%), and Malaysia (+0.23%) in the green. In Europe, stocks are leaning the opposite way (again on modest moves) with only 4 showing red at mid-day. The FTSE (+0.10%), DAX (+0.46%), and CAC (+0.53%) are typical of the region with Norway (-0.77%) and Denmark (-0.91%) the only appreciable losers in early afternoon trading. As of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.55% open, the SPY is implying a +0.57% open, and the QQQ implies a +0.56% open at this hour. 10-year bond yields are back up to 2.814% and Oil (WTI) is up 1.25% to $95.90/barrel in early trading.

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for the day include INFY, and RPM before the open. Then after the close, ARE, BRO, CADE, CDNS, CLS, CR, WIRE, FFIV, KALU, LBRT, LOGI, NXPI, PKG, RRC, RNR, SSD, and WHR report.

In economic news coming later this week, on Tuesday we get Conf. Board Consumer Confidence, June New Home Sales, and the 5-year bond auction. Then Wednesday June Durable Goods Orders, June Trade Goods Balance, June Retail Inventories, June Pending Home Sales, Crude Oil Inventories, the Fed Interest Rate Decision, Fed Statement, and FOMC Press Conference are announced. Thursday brings Q2 GDP, and Weekly Initial jobless Claims. Finally, Friday we get the June PCE Price Index, Q2 Employment Cost Index, June Personal Spending, Chicago PMI, and Michigan Consumer Sentiment.

This data-heavy week (including a ton of major earnings reports) starts off slowly this morning. Ahead of the Fed and Q2 GDP, markets are drifting higher to start the week. The same may be true of food commodity prices as Russian attacks on Odesa (and for no apparent military reason Ukrainian wheat fields) has the world once again worried about food supplies. Don’t be surprised if/when we see more intraday whipsaw action. Yet on the daily chart, the bulls have the short-term trend on their side and are well up off the overnight lows. Still, if we look at a longer-term (perhaps weekly) chart, you can see that the downtrend has not been broken (or at least it is not clear it is broken and held) across the major indices. So, be careful taking anything but short-term trades ahead of the data and more importantly market reactions coming later in the week.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all our money!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: UPRO, SQ, ARKK, AFRM, CROX, NOK, BA, MRNA, DIS. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although the economic data was surprisingly bearish, the tech earnings speculation outweighed everything else, providing another good day for the relief rally. The T2122 indicator continues in a short-term overbought condition for the indexes, but the bulls appear more than willing to buy up risk ahead of the GDP report and FOMC rate increase betting big on tech giant earnings results next week. The miss and the nearly 30% decline indicated after the SNAP earnings disappointment was shaken off this morning as the premarket pump recovered early losses.

Asian markets traded mixed overnight as Japan continues to report rising inflation. European markets trade with modest gains across the board in a choppy session after the ECB rate increase. U.S. futures recovered much of the overnight losses pointing to a flat open as I write this report ahead of earnings results and PMI data. Plan your risk carefully, heading into next week’s significant market-moving reports.

Economic Calendar

Earnings Calendar

We have just over 20 confirmed reports this morning as we wind down this trading week. Notable reports include AXP, ALV, CLF, GNTS, HCA, NEE, NEP, RF, SLB, & VZ.

News & Technicals’

On Thursday, Amazon said it would buy primary-care provider One Medical for $3.9 billion. Amazon’s three most significant acquisitions are a grocery chain, a movie studio, and a health company. These deals show the company’s willingness to spend big to grow fast in new businesse areas identified as strategic growth opportunities. The office vacancy rate in San Francisco rose to 24.2% in the second quarter from 23.8% in the prior period, according to CBRE research. Big tech employers like Salesforce and Google are staying flexible when it comes to bringing people back. Small businesses that count on tech workers struggle to stay afloat if they haven’t already closed their doors. Convenience store chain 7-Eleven has slashed roughly 880 corporate jobs in the United States. The eliminations come roughly a year after it completed its $21 billion acquisition of rival C-store business Speedway. According to a spokesperson, the cuts were of certain jobs in the company’s Irving, Texas, and Enon, Ohio, support centers, as well as field support roles. The average price for a used car is $33,341, which is $172 below the peak in March, according to CoPilot research. Nearly new vehicles (1 to 3 years old) have an average listing price of $13,145 more than if typical depreciation had occurred over the past two years. A separate report shows that high used-car prices have pushed the average trade-in value above $10,000 for the first time. Snap missed on the top and bottom lines in its second-quarter earnings report. The company authorized a stock repurchasing program of up to $500 million. Snap said it plans to “substantially slow our hiring rate, as well as the rate of operating expense growth.” Treasury yields declined sharply in early Friday trading in response to ECB action. The 2-year declined to 3.03%, the 5-year dipped to 2.93%, the 10-year fell to 2.82%, and the 30-year dropped to 3.02%.

Despite the rise in jobless claims and the Philly Fed MFG Index’s substantial decline, the bulls had another good day on Friday, choosing to favor tech earnings speculation over economic data. The after-the-bell earnings miss from SNAP has the stock indicated to decline nearly 30% at the open, but as I write this report, the premarket pump has also shaken off that disapointment. Indexes remain in a short-term oversold condition, and volume remains noticeably low as the relief rally extends. Today we get the latest reading on the PMI Flash, and then we wait on next week’s GDP and FOMC rate decision, along with a hectic schedule of tech giant earnings. Though a pullback could occur at any time, the remarkable willingness to rush into risk ahead could keep the bulls in charge heading into the weekend.

Stocks opened basically flat on Thursday, but then sold off for the first hour. This saw the two large-cap indices to bounce up off their 50sma. For the rest of the day, we had a series of whipsaws, ending on bullish swing right into the close. In a broader context, it was another volatile, whipsaw day where the action ended up being bullish…again, on low volume. 7 of the 10 sectors were in the green with Healthcare and Technology leading the winners. However, Energy and Communication Services were the biggest movers and they were both losing sectors. The day saw the QQQ drag the large-caps higher on a standout post-earnings move by TSLA.

This all left us with white-bodied candles with longer lower wicks. So, at this point, all three major indices are above their 50sma and sit a bit extended from their T-line (8ema) as well as in terms of their 4-week New High/Low Ratios. On the day SPY gained 1.01%, DIA gained 0.52%, and QQQ gained 1.44%. The VXX fell 1.7% to 21.20 and T2122 remains deep in the overbought territory at 96.24. 10-year bond yields also fell sharply, dropping back below 3% to 2.889%, and Oil (WTI) dropped about 3.44% to $96.43/barrel (which was actually a rally up off the session lows).

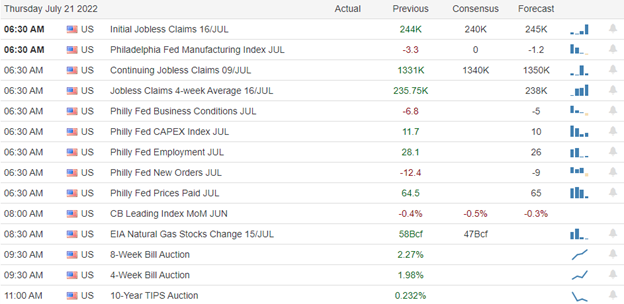

In economic news, Weekly Initial Jobless claims came in significantly higher than expected (251k vs 240k forecast). This was the highest level since mid-November. Meanwhile, the Philly Fed Mfg. Index fell to -12.3, down 9 points from the prior month and much worse than the expected 1.6 value. This was the lowest rating since May 2021. Elsewhere, the ECB raised rates by half a percent (but for perspective, only to zero now since they were negative rates). This was their first rate hike for 11 years and the largest hike since 2000. As a result, the Euro strengthened against the Dollar.

In business news, after the close, AMZN agreed to buy primary care provider One Medical for $3.49 billion as the e-commerce giant continues its push into the healthcare sector. Elsewhere, in a shock, Chinese chipmaker Semiconductor Manufacturing International (located in Shanghai) has advanced its chipmaking technology by more than 2 generations. They are now shipping 7-nanometer chips to Bitcoin miners. This essentially guts US sanctions. It could also make China a serious new competitor to western chipmakers like TSM, INTC, AMD, NVDA, QCOM, and SSNLF (import sanctions permitting). Finally, AXP raised its guidance on what it called resilient credit card usage.

On the Russian invasion story, Turkey announced that Ukraine and Russia will sign a deal today to reopen Ukraine’s Black Sea ports for grain exports. Meanwhile, Ukraine asked its creditors for a two-year freeze on bond payments (in order to use its diminished resources on war efforts). BLK is the largest holder of such bonds, holding $1.2 billion across its various funds. AB is the second largest Ukrainian bond holder with $580 million while Pimco and Eaton Vance both hold around $300 million of the bonds. Elsewhere, the EU announced another round of sanctions which included freezing the assets of Russia’s largest lender Sberbank.

After the close, MAT, UFPI, and WAL reported beats on both the top and bottom lines. Meanwhile, WRB, PPG, RHI, and THC, missed on revenue while beating on earnings. However, SNAP, STX, SIVB, SAM, and ISRG all missed on both lines.

Overnight, Asian markets were mixed again on modest moves. South Korea (-0.66%) and Shenzhen (-0.49%) were the only appreciable losers. On the other side, Malaysia (+1.07%), Singapore (+0.92%), and India (+0.69%) led the gainers. In Europe, stocks are mostly green on modest moves at mid-day. The FTSE (+0.22%), DAX (+0.32%), and CAC (+0.22%) are leading the region higher with only Belgium (-0.11%) and Finland (-1.22%) showing red at this point in early afternoon trading. As of 7:30 am, US Futures are pointing toward a mixed open that leans toward the red. The DIA implies a +0.10% open, the SPY is implying a -0.27% open, and the QQQ implies a -0.50% open at this hour. 10-year bonds are continuing that sharp fall at 2.809% and Oil (WTI) is off another 1.76% to $94.70/barrel in early trading.

The major economic news events scheduled for Friday are limited to Mfg. PMI and Services PMI (both at 9:45 am). The major earnings reports scheduled for the day include AXP, ALV, CLF, GNTX, HCA, NEE, NHYDY, RF, ROP, SLB, TWTR, and VZ before the open. There are no major reports after the close.

So far this morning, HCA, AXP, ALB, RF, and DNKEY all reported beats on both the revenue and earnings lines. Meanwhile, ALV, NEE, and ROP reported misses on the revenue line while beating on earnings. On the other side, CLF and VZ beat on revenue while missing on earnings.

Once again, earnings remain the primary focus of markets today. Last night’s terrible miss by SNAP on horrific ad sales has the high-tech QQQ spooked. So, despite generally good results, the 3 major indices are looking leery in the premarket. PMI numbers may have an impact after the market opens. However, as of now, we look to open flat to modestly bearish again. Don’t be surprised if the intraday whipsaw action continues. Still if we look at the daily chart, it is clear the bulls have the momentum in the short-term with part of a gap still left to fill to the upside in the large-cap indices.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all our money!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Disappointing home sales and mortgage data produced a bullish but choppy price action as the indexes remained in a short-term extended condition. Traders and investors will have to grapple with our most significant day of earnings so far this quarter, as well as Jobless Claims and the Philly Fed MFG data. We may also see a market reaction to the pending ECB rate decision as they begin fighting record inflation. Bullish earnings speculation remains strong but be careful not to overtrade and take some profits with the FOMC and GDP coming our way next week.

Asian markets traded mixed overnight as the Bank of Japan held trades steady. European markets trade mixed with muted results as they wait on the ECB rate decision. With a big day of market-moving data ahead, U.S. futures suggest a mixed open as I write this report but prepare for about anything as the market reacts to the results. Market emotion is high, so don’t rule out the possibility of some significant point swings.

Economic Calendar

Earnings Calendar

We have our most hectic day of the week on the earnings calendar, with more than 70 companies listed. Notable reports include ABB, ALK, AAL, T, AN, DHI, DHR, DPZ, DOV, FITB, ISRG, KB, NOK, NUE, PM, SAP, & TRV.

News & Technicals’

According to reports, the European Central Bank could go big on its first rate hike in 11 years. A new anti-fragmentation tool and a sizeable rate hike would come as the ECB deals with its primary mandate: price stability. The eurozone inflation print for June came in at 8.6%, up from 8.1% in May, and German producer prices in June were 32.7% higher than a year earlier. There had been concerns across the region that there could be a complete shutdown of gas supplies via the pipeline after it was closed earlier this month for maintenance. However, data on operator Nord Stream’s website showed that flows increased from zero to 29,284,591 kWh/h for 0600-0700 Central European Time Thursday. On July 10, the last day of operations before the maintenance work began, flows were roughly the same level, just above the 29,000,000 kWh/h. Speaking to Parliament, Draghi said he was going to speak to President Sergio Mattarella and inform him of his intentions after failing to unite his fragile coalition government. Last week, Mattarella rejected Draghi’s first resignation and asked him to lead more negotiations with lawmakers in the hope of avoiding snap elections. United Airlines on Wednesday notched a key profit milestone in its pandemic recovery. However, it said it will scale back its growth plans through 2023. Airlines have reported strong demand as well as high costs for fuel and other expenses. Microsoft eases hiring as economic concerns affect more of the tech industry but declined to specify which divisions will slow the hiring pace. The company lowered its quarterly earnings guidance in June but attributed the move to changing exchange rates. The Asian Development Bank has cut the growth forecast for China due to concerns over the country’s zero-Covid approach and strict lockdowns, which have also impacted its troubled property market. As a result, gross domestic product growth for the world’s second-largest economy is expected to be at 4% in 2022, down from an earlier estimate of 5%, ADB said in a report published Thursday. China’s continued “adherence to a zero-covid strategy in response to renewed outbreaks early in 2022 has triggered the reimposition of strict lockdowns,” the bank wrote in its report. Treasury yields rose slightly in early Thursday trading, with the 2-year inverted trading at 3.23%, the 5-year at 3.18%, the 10-year at 3.04%, and the 30-year at 3.17%.

The short-term extended condition of the market, disappointing housing data, and some mixed earnings results produced a choppy day of price action, but overall the bulls won the day. However, today will be our biggest day of earnings results so far this quarter which means anything is possible as traders react. We also face a pending ECB rate decision; Jobless Claims that have recently experienced a slow creep upward as well as Philly Fed MFG data. Unfortunately, the rising bond yields and 2/10 inversion continue to suggest a recession adding an element of uncertainty despite the hopeful bullishness of the recent relief rally. So continue to expect challenging price action with overnight gaps and reversals in the days and weeks ahead.

Markets opened flat on Wednesday and then ground sideways in a tight range for the first hour of the day. Then we saw a strong rally for a little over 30 minutes before resuming the sideways grind until about 12:45 pm. At that point, we saw a sharp selloff that also lasted about 30 minutes before bobbing along sideways for the next 1.5 hours. A slower rally took over at about 2:30 pm to take price back near the highs of the day only to fade the last 30 minutes. This left us with white-bodied candles with plenty of wick on each end. The DIA printed a Doji-type candle and the SPY a Spinning Top.

All 3 of the major indices have now broken through their 50sma and medium-term downtrend. Exactly half of the 10 sectors are green and half are down. With that said, Technology is by far the biggest mover, up nearly 2.5% on the day on big moves by NFLX, NVDA, AMD, META, and AMZN. Once again, all of this happened on below-average volume. On the day, SPY gained 0.65%, DIA gained 0.20%, and QQQ gained 1.59%. The VXX fell 1.28% to 21.57 and T2122 (the 4-week new High/Low ratio) is deep in the overbought territory at 96.60. 10-year bond yields climbed back above the key 3% level to 3.034% and Oil (WTI) fell just over 1.5% to $102.61/barrel.

In business news, Reuters reported that SHEL is looking to sell two of its US Gulf of Mexico oil and gas projects (fields), hoping to raise $1.5 billion. Then after the close, as part of its quarterly report, TSLA announced it sold 75% of its Bitcoin to raise $936 million in cash. Also after the close, F announced it will cut as many as 8,000 jobs in order to raise money for its electric vehicle investments. Then this morning F reassured markets that it already has secured 100% of the batteries it needs for its 2022 and 2023 plans.

On the Russian invasion story, natural gas flows resumed from Russia via the Nord Stream 1 pipeline. However, the flow resumed only at the reduced (60% of capacity) rate that Russia initiated in retaliation for sanctions. On the ground, Russian forces are getting closer to Ukraine’s second largest power plant (after having previously taken the largest). Elsewhere, US and European sources claim that Russia is taking the steps needed for their country to annex Eastern and Southern Ukraine by September. This news comes the same day that Deputy Chair of the Russian Security Council said that Ukraine could disappear from the map as a result of current events.

After the close, STLD, KMI, CSX, CCK, AA, CCI, KNX, and VMI all reported beats on both the top and bottom lines. Meanwhile, TSLA and EFX missed on revenue while beating on earnings. On the other side, UAL, LVS, and WTFC beat on revenue while missing on earnings. However, LSTR and SEIC reported misses on both the top and bottom lines.

So far this morning, T, PM, DOW, TRV, DHR, NOK, MMC, TSCO, IQV, DGX, IPG, KEY, ALK, SON, HBAN, SNA, and SNV have all reported beats on both the revenue and earnings lines. Meanwhile, SAP, AAL, FITB, DPZ, and HRI all reported beating on revenue while missing on earnings. On the other side, DHI, AN, BX, DOV, POOL, and TPH all missed on revenue while beating on earnings. However, ABB missed on both the top and bottom lines.

Overnight, Asian markets were mixed but leaned to the upside. Hong Kong (-1.51%), Shanghai (-0.99%), and Shenzhen (-0.94%) paced the losses as Real Estate market problems remained top of mind in China. Meanwhile, Taiwan (+1.39%), South Korea (+0.93%), and Malaysia (+0.93%) led the gainers in the region. In Europe, we see a similar story taking shape at mid-day. The FTSE (-0.47%), DAX (-0.45%), and CAC (+0.32%) are typical of the performance spread in the region. However, Russia (-1.03%) and a couple of other smaller exchanges are down more than a percent in early afternoon trading. As of 7:30 am, US Futures are pointing toward a mixed and mostly flat start to the day. The DIA implies a -0.19% open, the SPY is implying a -0.13% open, and the QQQ implies a +0.03% open at this hour. 10-year bond yields are up to 3.051% and Oil (WTI) remains extremely volatile, down 4.5% to $95.42/barrel in early trading.

The major economic news events scheduled for Thursday is limited to Philly Fed Mfg. Index and Weekly Jobless Claims (both at 8:30 am). The major earnings reports scheduled for the day include AIR, ABB, ALK, AAL, T, AN, BX, DHI, DHR, DPZ, DOV, DOW, FITB, FCX, HRI, HBAN, IPG, IQV, KEY, MMC, NOK, NUE, PM, POOL, DGX, SAP, SNA, SON, SNV, TSCO, TRV, TPH, UNP, and WBS before the opening bell. Then after the close, SAM, COF, ISRG, MAT, PPG, RHI, STX, SNAP, SIVB, THC, UFPI, VLRS, WRB, and WAL report.

In economic news coming later this week, on Friday Mfg. PMI and Services PMI are released.

In earnings reports later this week, on Friday we hear from AXP, ALV, CLF, GNTX, HCA, NEE, NHYDY, RF, ROP, SLB, and VZ.

Earnings remain the main focus for traders today. However, the Jobless Claims and to a lesser extent Philly Fed number coming at 8:30 may also drive markets. As of now, we look to open flat to modestly bearish. Still, there were a lot of strong earnings reports last night and so far this morning and the big tech names look to be trying to pull the rest of the market higher with them. So, don’t be surprised if the bulls find some energy…at least early. The QQQ shows a bullish trend, but the SPY and DIA are still just shy of getting that designation. With a gap to fill above in the large-cap indices, just keep in mind that the path of least resistance in the short term is upward.

Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Remember that trading is our job. So, do the work and follow the process. Always move your stops in your favor and remember the “Legend of the man in the green bathrobe“…it is NOT house money, it’s all our money! One way to put this is Buffett’s first rule of making big money in the market, which is to not lose big money in the market. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No tickers today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Price resistance levels cut like butter as the bulls had a really good day following through from the overnight reversal with the Dow more than 1700 points off the low just four trading days ago. There suddenly seems to be no concern that bond yields point toward a recession, and with the coming rate hike, the desire to hurry up and buy something is taking over. However, be careful not to chase or overtrade, with the T2122 indicator suggesting a short-term overbought condition.

Asia markets rallied strongly overnight in reaction to the U.S. buying surge, with the Nikkei leading the buying, up 2.67%. However, European markets have reversed early bullishness after their inflation hit a 40-year high of 9.4%, worrying that Russia will shut down energy supplies. U.S. futures have also reversed from early bullishness after mortgage demand dropped to a 22-year low as inflation-driven rate hikes damage home buying demand. That said, don’t rule out the power of earnings and the fear of missing out as the wild volatility in price action continues.

Economic Calendar

Earnings Calendar

The Wednesday calendar has about 30 confirmed earnings reports. Notable reports include ABT, ASML, BKR, BIIB, CMA, CCI, CSX, KMI, NDAQ, NTTRS, PACW, TSLA, & UAL.

News & Technicals’

Netflix lost nearly 1 million subscribers in the quarter after forecasting a dip of 2 million. The company forecast 1 million net adds for the third quarter, below Wall Street estimates of 1.8 million. Netflix is counting on changes, such as cracking down on password sharing and adding an advertising tier, to start in 2023. Bitcoin surged as high as $23,800 Wednesday, up 8% in 24 hours and trading at levels not seen since mid-June. Traders took comfort from the prospect of a rate hike from the Federal Reserve that is less aggressive than feared. Ether climbed above $1,500 amid optimism over a highly anticipated upgrade to its network known as the “Merge.” According to U.S. intelligence, Russia is laying the groundwork to annex parts of Ukraine. “We’re seeing ample evidence and intelligence and in the public domain that Russia intends to try to annex additional Ukrainian territory,” National Security Council spokesman John Kirby told reporters at the White House. Kirby that the U.S. observed a similar Russian playbook in 2014 ahead of the Kremlin’s annexation of Crimea, a Ukrainian peninsula on the Black Sea. Citing supply chain challenges due to Russia’s war in Ukraine, Gupta said the two countries capture a large part of the market share. Russia and Ukraine are the largest exporters of krypton — a gas used in chip production. Semiconductors are used in everything, from mobile phones and computers to cars and home appliances. Rising inflation and expectations of more monetary tightening are already causing a “consumer-led slowdown,” said Gupta. Last week, a spike in reported numbers of homebuyers halting mortgage payments prompted many banks to announce their low exposure to such loans. Across banks covered by Goldman Sachs, average exposure to property, including mortgages, was just 17%. If more homebuyers refuse to pay their mortgages, the poor sentiment would reduce demand — and theoretically, prices — in a vicious cycle. “It is critical for policymakers to restore confidence in the market quickly and to circuit-break a potential negative feedback loop,” Goldman Sachs chief China economist Hui Shan and a team said in a report Sunday. Treasury yields dipped slightly in early Wednesday trading, with the 2-year inverted at 3.13%, the 5-year at 3.11%, the 10-year at 2.98%, and the 30-year trading at 3.15%.

The bulls had a really good day on Tuesday, with the Dow closing up more than 1700 points from the low just four trading days ago. The buying party continued after the bell, with NFLX jumping more than 6% despite losing nearly 1 million subscribers and declining revenue. European inflation hit a 40-year high of 9.4%, with the risk of Russia shutting off the energy supply, yet the bulls push for a positive open fuelled by tremendous earnings speculation. The T2122 indicator suggests a short-term overbought condition, but that does not mean we can’t go higher, as the fear of missing out is a powerful motivator. That said, don’t allow greed to prevent you from taking some profits in case of a sudden reversal of sentiment comes into play.

Stocks gapped higher Tuesday and then slowly followed through to the upside until about 2:15 pm. At that point, we saw a sideways grind take shape that lasted until the bulls again stepped in the last half hour of the day. This left us with all 3 major indices forming something like a Fig Newton pattern on the daily chart and closing near their highs. It was also the best day in 3 weeks for US markets. The SPY and DIA are still fighting with their respective 50sma and longer-term downtrend resistance levels. However, QQQ has cleared both those levels and is trying to pull the large caps higher with it, on the strength of names like NVDA, AMD, META, GOOG, AMZN, and NFLX. All 10 sectors were in the green, with Industrials and Technology leading the way. On the day, SPY gained 2.70%, DIA gained 2.40%, and QQQ gained 3.08%. The VXX was flat at 21.85 and T2122 spiked deep into the overbought territory at 98.71. 10-year bond yields have popped back above 3% to 3.028% and Oil (WTI) closed 1.2% higher at $103.81/barrel. All-in-all, the day was a very nice move on below-average volume for the bulls.

In business news, AMZN sued thousands of Facebook group administrators who allegedly brokered false/fake AMZN product reviews. META shut down more than 10,000 such groups that AMZN reported for this behavior. Later in the day, a judge ruled that the trial over the lawsuit brought by TWTR against Elon Musk (seeking to force his $54.20/share purchase) will begin in October. Musk had sought to delay the trial until mid-2023. After the close ATVI announced that a second group of employees (this time Quality Assurance testers) have formed a union, just months before the company’s acquisition by MSFT closes. While this is a tiny group (20 people), it does represent a second department where either ATVI or MSFT will need to deal with the same union (Communications Workers of America).

In China news, the middle-class backlash against the housing sector is building steam. The real estate sector in China has a long history of starting huge housing projects, selling the units prior to completion, and then never finishing the development (often due to the developer defaulting on loans and going out of business). A now widespread boycott of paying mortgage payments on such projects has taken root and spread. Currently, Bloomberg reports more than 300 projects from 24 real estate developers spread across over 90 cities are now participating in the boycott. This is tripled in size from my first report on it a couple of weeks ago. This is huge news, because real estate makes up one-fifth of the Chinese economy and public protest of any kind is unheard of in that country. Elsewhere, SEC Chair Gensler again told reporters it was unclear whether Chinese authorities and American regulators will reach a deal to avoid delisting 200 Chinese companies from US stock exchanges. He went on to say he was not particularly confident.

On the Russian story, the Wall Street Journal reported that EU sources are currently expecting that Russia will restart the flow of natural gas through the Nord Stream 1 pipeline (as scheduled) when the planned maintenance period ends Thursday. The flow is expected to return to 60% of capacity (down 40% from prior levels). Elsewhere, the Ukrainian First Lady will speak to the US Congress today. She is expected to ask for more aid and condemn human rights abuses. In that vein, the US is preparing yet another shipment (the 16th) of military aid for Ukraine.

After the close, OMC, JBHT, CALM, and PNFP all reported beats on both the top and bottom lines. Meanwhile, IBKR beat on revenue while missing on earnings. On the other side, NFLX missed on revenue while beating on earnings. NFLX stock was up as much as 8.5% in after-hours trading as it lost fewer subscribers than analysts had expected (down just less than one million versus a loss of 2 million expected).

So far this morning, ABT, ASML, BIIB, TLSNY, NDAQ, CMA, and ELV all reported beating on both the top and bottom lines. Meanwhile, MTB missed on revenue while beating on earnings. On the other side, AKZOY, NTRS, and FHN beat on revenue but missed on earnings. Finally, BKR, WIT, and HCSG reported misses on both lines.

Overnight, Asian markets were green across the board. Japan (+2.67%) was an outlier to the upside as the Bank of Japan decided to remain accommodative in fear that economic growth is uncertain (they did not raise rates). Singapore (+1.68%), Australia (+1.65%), and Hong Kong (+1.11%) led the region higher. It is worth noting that Hong Kong ended its city-wide Covid isolation program. In Europe, stocks are mixed but lean to the red side at mid-day. The FTSE (-0.27%), DAX (-0.39%), and CAC (-0.26%) are leading the region lower. However, 7 of the smaller exchanges are in the green, led by Greece (+0.95%) and Russia (+0.80%). As of 7:30 am, US Futures are pointing toward a flat to modestly red start to the day. The DIA implies a -0.16% open, the SPY is implying a -0.13% open, and the QQQ implies a flat -0.03% open at this hour. 10-year bond yields as back down to 2.969% and Oil (WTI) is off almost 2% to $102.21/barrel in early trading.

The major economic news events scheduled for Wednesday are limited to June Existing Home Sales (10 am) and Crude Oil Inventories (10:30 am). The major earnings reports scheduled for the day include ABT, ASML, BKR, BIIB, CMA, ELV, LAD, MTB, NDAQ, NTRS, and WIT before the opening bell. Then after the close, AA, CCI, CCK, CSX, DFS, EFX, KMI, KNX, LSTR, LVS, SEIC, STLD, TSLA, UAL, VMI, and WTFC report.

In economic news coming later this week, on Thursday we get Philly Fed Mfg. Index and Weekly Jobless Claims. Finally, on Friday Mfg. PMI and Services PMI are released.

In earnings reports later this week, on Thursday we get reports from AIR, ABB, AAL, T, AN, BX, DHI, DHR, DPZ, DOV, DOW, FITB, FCX, HRI, HBAN, IPG, IQV, KEY, MMC, NOK, NUE, PM, POOL, DGX, SAP, SNA, SON, SNV, TSCO, TRV, TPH, UNP, WBS, SAM, COF, ISRG, MAT, PPG, RHI, STX, SNAP, SIVB, THC, UFPI and WRB. Finally, on Friday we hear from AXP, ALV, CLF, GNTX, HCA, NEE, NHYDY, RF, ROP, SLB, and VZ.

Earnings season remains the top story for markets. However, Mortgage demand dropped to its lowest point since 2000 last week as the average 30-year fixed-rate conforming loan rate rose to 5.82%. This comes as the overall demand fell another 6%, as new home purchase applications were down 7% week-on-week (down 19% versus the same week last year) and refinance applications fell 4% on the week. So, the housing market will also get some focus from traders.

Recession fears (including those stoked by Russia) will remain in the back of trader’s minds and eyes will also start drifting toward the Fed with a rate meeting next week. Futures are showing a very modestly bearish start to the day right now. However, there are more earnings reports coming before the open and overall the market is in a positive mood after yesterday’s strong showing. Remember that the SPY is still fighting with its mid-term downtrend line and 50sma. So, volatility remains a high probability. The only two things that we know for sure are that we are seeing very low volumes (which tells us there is not much conviction in either the bull or bear camps) and we also know the longer-term trend remains bearish, while we have been in a sideways to slightly bullish more for a few weeks.

Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Remember that trading is our job. So, do the work and follow the process. Always move your stops in your favor and remember the “Legend of the man in the green bathrobe“…it is NOT house money, it’s all our money! One way to put this is Buffett’s first rule of making big money in the market, which is to not lose big money in the market. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality. Lastly, remember it is Friday. So, be prepared for the weekend news cycle.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: HALO, INSG, AGNC, XBI, SWKS, INMD, RIVN, BMY, NFLX. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although we began the trading week with an exuberant gap up, the fade into a pop and drop pattern at price resistance on weak volume left more questions than answers. The price action left behind bearish engulfing and dark cloud cover candle patterns on the index charts but can the bear follow, or will the bull find the energy to defend? With increasing earnings reports and a reading on Housing Starts and Permits before the bell, prepare for just about anything with a dose of high price volatility to test technical and price resistance. Silly season is underway, so plan carefully and avoid trading as the drama unfolds.

Overnight Asian market seemed to struggle with direction closing the day with mixed results. European markets trade in the red across the board this morning seemly uncertain about the earnings results. However, U.S. futures again point to a gap up open ahead of possible market-moving data as the high earnings speculation continues. Expect another bumpy day of price action, and the bulls and bears duke it out at technical and price resistance levels.

Economic Calendar

Earnings Calendar

We have about 20 confirmed earnings reports to deal with on the Tuesday calendar. Notable reports include ALLY, CALM CFG, HAL, HAS, IBKR, JNJ, JBHT, LMT, MAN, NFLX, NVS, TFC, & UCBI.

News & Technicals’

The majority state-owned Gazprom said Monday that it is not in a position to comply with gas contracts with Europe due to unforeseeable circumstances. Germany’s energy firm Uniper confirmed to CNBC that Gazprom had claimed “force majeure” on its supplies. “We consider this unjustified and have formally rejected the force majeure claim,” Lucas Wintgens, spokesperson for Uniper, told CNBC’s Annette Weisbach. New data from blockchain analytics firm CryptoQuant shows that miners are rapidly exiting their bitcoin positions. 14,000 bitcoin, or more than $300 million at its current price, were transferred out of wallets belonging to miners in a single day — and in the last few weeks, miners have offloaded the largest amount of bitcoin since Jan. 2021. According to Treasury Department data released Monday, China’s portfolio of government debt in May dropped to $980.8 billion. It marked the first time since May 2010 that China’s holdings fell below the $1 trillion mark. Netflix announces its second-quarter earnings results on Tuesday. The company previously projected a loss of 2 million subscribers for the period. Netflix is adding an advertising tier and cracking down on password sharing to reinvigorate growth, but those maneuvers won’t kick in until later this year. Goldman Sachs has slowed its hiring and is looking to cut the fees it pays vendors as the investment bank prepares for tougher times. But New York-based Goldman has another tool in its arsenal to keep expenses under control: A potential return of year-end job cuts, according to a person with knowledge of the situation. No target exists yet for headcount reduction, according to the person, and the plans are dynamic and could change. Treasury yields ticked higher in early Tuesday trading, with the 2-year inverted over the 5,10 & 30-year bonds at 3.17%. The 5-year trades at 3.10%, 10-year at 2.99%, and the 30-year rose to 3.16%.

We kicked off the week with an exuberant gap up, but the early rally quickly faded into a pop and drop at price resistance leaving behind bearish engulfing candle patterns on the index charts. Indeed a concerning development if the bears can follow through to the downside today. However, if the bulls find the energy to defend, we may yet have a chance to break overhead price resistance levels finally. Today we face a growing number of earnings reports to keep the price volatility high with our first big tech NFLX, reporting after the bell. We will also get a read on the Housing Starts and Permits that consensus suggests moved up slightly over the last month. The rising bond prices and the sharp reversal in the dollar pushing commodities higher add some uncertainty, so stay focused on the price, continuing to respect resistance levels.

Markets gapped about 1% higher for the second straight time on Monday, following Europe and Asia. They even managed to follow-through for a few minutes. However, by 10 am, a long, slow selloff had taken over to more than fill the gap and drive to the lows of the day before rebounding the last 10 minutes of the day. This left us with gap-up, Bearish Engulfing Candles with an upper wick on all 3 major indices. Once again, all this action is taking place on very low volumes. Energy was far and away the biggest gaining sector, while Healthcare was by far the biggest losing sector of the session. Four of the 10 sectors were positive with the other six being negative. On the day, SPY lost 0.79%, DIA lost 0.64%, and QQQ lost 0.85%. The VXX gained 1.72% to 21.91 and T2122 was flat remaining in the overbought territory at 81.63. 10-year bond yields rose to 2.982% and Oil (WTI) spiked 4.64% to $102.12/barrel.

In economic news, despite the increase in bond yields, the curve remains inverted. The 5-year bond yields is higher than the 10-year bond yield and the 2-year yield is higher than the 5-year yield. So “2s vs 5s,” “5s vs 10s,” and “2s vs 10s” are all inverted, which are all potential indicators of a coming recession. Also related to bonds, it was announced that China’s holdings of US Bonds (debt) fell to $980 billion, below $1 trillion for the first time in 12 years (since May 2010). I am not sure if this is a reflection of the health of the Chinese economy, on Chinese perception of US debt risks, come combination of the two, or pure coincidence.

In business news, more companies are reporting belt-tightening. Early in the day Monday, GS announced it will slow hiring and reinstitute year-end performance reviews and staff reductions. Later, AAPL said they will slow hiring and reduce spending for some groups. This comes after MSFT reported over the weekend that they had laid off 1% of its staff and GOOGL said last week they will slow hiring and expected employees to work harder to avoid job cuts. It was also reported (but not announced) that META has told team managers to weed out poor performers to reduce staff sizes as its Ad business struggles.

On the Russian story, as many expected, state-owned Gazprom said that due to “unforeseen circumstances” it is not in a position to comply with gas contracts in Europe. This claim was made to not only cover future non-supply but also to cover the gas shipment reductions (40%) that Gazprom has put in place since June (as direct responses to Western sanctions). Germany has forcefully rejected the Gazprom “force majeure” claim. European economists are projecting scenarios where the cutoff of Russian gas would reduce the German GDP by at least 6% with major industries like chemicals being shut down nearly completely. So, in addition to people staying warm in winter, such a move would crush the European economy.

In Forex news, the dollar dropped early this morning on rumors that the ECB will raise rates by 50 basis points amidst a worsening inflation background. European bonds and stocks fell on the more hawkish outlook.

After the close, IBM reported beats on both the top and bottom lines. However, the company slightly reduced guidance for the year in terms of free cash flow (from $10.5 billion to $10 billion) as well as reporting that gross margins shrank from 55.2% (Q1) to 53.4% (Q2). So far this morning, JNJ, VLVLY, TFC, HAL, TELNY, CFG, and SBNY have all reported beats on both lines. Meanwhile, NVS, MAN, and HAS all missed on revenue while beating on earnings. However, ALLY reported a miss on both the top and bottom line.

Overnight, Asian markets were mixed but leaned heavily to the red side on modes moves. Japan (+0.65%) and India (+0.38%) were the only appreciable gainers. Meanwhile, Hong Kone (-0.89%), Thailand (-0.74%), and Australia (-0.56%) paced the losses. In Europe, stocks are also mixed on modest moves at mid-day. Russia (-1.92%) is by far the biggest loser. Meanwhile, the FTSE (+0.28%), DAX (+0.01%), and CAC (-0.12%) are typical of the region in early afternoon trading. As of 7:30 am, US Futures are pointing toward a gap higher to start the day. The DIA implies a +0.66% open, the SPY is implying a +0.83% open, and the QQQ implies a +0.88% open at this hour. 10-year bond yields remain flat at 2.98% and Oil (WTI) is down almost 2% to $100.57/barrel.

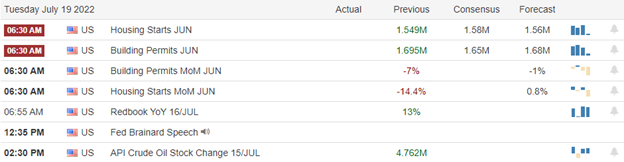

The major economic news events scheduled for Tuesday include June Building Permits and June Housing Starts (both at 8:30 am). The major earnings reports scheduled for the day include ALLY, CFG, HAL, HAS, JNJ, LMT, MAN, NVS, SBNY, and TFC before the opening bell. Then after the close, CALM, IBKR, JBHT, NFLX, and OMC report.

In economic news coming later this week, on Wednesday, June Existing Home Sales and Crude Oil Inventories are announced. On Thursday we get Philly Fed Mfg. Index and Weekly Jobless Claims. Finally, on Friday Mfg. PMI and Services PMI are released.

Again, earnings season and recession fears (including those stoked by Russia) are top of mind for most traders. There are smaller issues that pop up, such as rumors NCR is in talks to be acquired by a private equity firm or that individual companies are tightening belts to get ahead of a downturn. However, with the Fed still more than a week out, those two major themes dominate markets. Futures are showing that markets are in a positive mood this morning. However, expect more volatility and chop. The only two things that we know for sure are that we are seeing very low volumes (which tells us there is not much conviction in either the bull or bear camps) and we also know the trend remains bearish until it is broken and price proves it can hold the break.

Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Remember that trading is our job. So, do the work and follow the process. Always move your stops in your favor and remember the “Legend of the man in the green bathrobe“…it is NOT house money, it’s all our money! One way to put this is Buffett’s first rule of making big money in the market, which is to not lose big money in the market. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality. Lastly, remember it is Friday. So, be prepared for the weekend news cycle.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: MRVL, DKNG, C, SOFI, KWEB, CGC, WMT, AAPL, ARKK, NFLX, AFRM. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service