Earnings results continued to fuel an unstoppable buying enthusiasm as the bulls pushed the indexes higher right into the weekend. Adverse economic data such as rising rates, a negative GDP, and a PCE number that continued to show inflationary pressure was no deterrent to the rally’s energy. But, with many of the big tech reports now in the rearview, can the upcoming reports push the indexes through the significant overhead resistance? Keep an eye on the PMI, ISM, and Construction spending reports later this morning.

Asian markets closed green across the board with modest gains after a private survey showed Chinese factory activity grew. European market trade cautiously bullish this morning with modest gains across most indexes. As we kick off August, trading U.S. futures recovered from overnight losses suggesting a flat open at the time of this report. Ride the bullish wave as long as it lasts but keep an eye on the overhead resistance for the possibility of entrenched bears.

Home price gains are cooling fast as demand wanes and supply builds. As a result, the annual rate of price appreciation fell two percentage points from 19.3% to 17.3%. However, price gains are still otherwise strong because of an imbalance between supply and demand. The housing market has had a severe shortage for years. Google CEO Sundar Pichai announced to employees Wednesday a new effort called “Simplicity Sprint,” which will solicit ideas from its more than 174,000 employees on where to focus and improve efficiency. Pichai said Google’s productivity as a company isn’t where it needs to be given the headcount it is and warned of a toughening economy. HR chief Fiona Cicconi also acknowledged industry-wide concerns about layoffs and said the company is “not currently looking to reduce Google’s overall workforce” but reiterated the need for greater efficiency and focus. Neel Kashkari, president of the Federal Reserve Bank of Minneapolis, told CBS’ “Face the Nation” that inflation poses a larger threat than a potential recession. “We’re going to do everything we can to avoid a recession, but we are committed to bringing inflation down, and we are going to do what we need to do,” Kashkari said. Chinese e-commerce giant Alibaba said it would comply with U.S. regulators and work to maintain its listings in New York and Hong Kong. “Alibaba will continue to monitor market developments, comply with applicable laws and regulations and strive to maintain its listing status on both the NYSE and the Hong Kong Stock Exchange,” it said in a statement to the Hong Kong bourse on Monday. Last week, supplies via Nord Stream 1 were reduced to 20%, with Gazprom citing technical issues. There are renewed price pressures every time Russia decreases its supplies to Europe, given how important the commodity is for several sectors. With supplies reduced and prices higher, the gas crisis is shaking Europe’s economic prospects. Treasury yields traded higher in early Monday trading, with the 2-year at 2.89%, the 5-year at 2.68%, the 10-year at 2.65%, and the 30-year holding at 3.02%.

Last week the buying enthusiasm was unstoppable as earnings beat lowered expectations. Rising interest rates, a negative GDP, and a rising PCE (the Fed’s preferred inflation indicator) could not deter the bulls hungry for risk. With the indexes not facing significant overhead resistance and a T2122 continuing to signal an over-extended condition, can the earnings supply enough bullish inspiration to keep the rally going? We now seem to have the ability to ignore adverse economic reports, so maybe the PMI, ISM, and Construction numbers won’t matter all that much, but it would be wise to keep an eye on them for a potential reaction. Ride the wave as long as it lasts but observe for clues from bears at or near overhead resistance levels.

Markets opened positive, if mixed, on Friday. The DIA opened flat, while the SPY and QQQ both gapped about a half of a percent higher at the open. All 3 major indices then followed through in a rally until about 10:45 am. At that point, all 3 sold off sharply for 45 minutes only to reverse again and start a long, strong, sustained rally for almost the entire rest of the day. With that said, in the last 10 minutes of the day, all 3 indices sold off as that dark pool volume crossed the tape. This left us with strong white candles with wicks on both ends across the major indices. Volume was closer, but still below, average on that month-end rebalancing.

Eight of the 10 sectors were in the green, with Energy up a whopping 3.08% and the worst of the losers was Healthcare (-0.59%). Over 70% of stocks closed about their 40sma and 29% closed above the 200sma. On the day, SPY gained 1.46%, DIA gained 1.01%, and QQQ gained 1.82%. The VXX climbed slightly to 20.94 and T2122 remains deep in the overbought territory at 96.46. 10-year bonds yields were down sharply as somebody bought up bonds, giving us a 2.66% yield and Oil (WTI) was up more than 2% to $98.43/barrel. This ended the best month since 2020 in all 3 major indices.

In economic news, June Personal Spending came in stronger than expected at +1.1% (versus +0.9% estimated and May’s +0.3%). The Q2 Employment Cost Index came in a bit higher than expected too at +1.3% (versus +1.2% forecast), but better than Q1’s +1.4% number. The Chicago PMI came in lower than expected at 52.1 (55.0 estimate). However, Michigan Consumer Sentiment came in better than expected at 51.5 (versus an estimate of 51.1 and last month’s 50.0). Taken together, this shows us the business is softening in anticipation of a downturn, but the consumer (driver of the economy) is holding up and has a little better outlook now that gas prices have been falling for 2 months.

In stock news, on Friday BABA was added to the SEC’s delisting watchlist (of more than 270 Chinese companies identified as at risk for delisting. The dispute is over non-compliance with US auditing standards. BABA was down more than 11% on the day. Elsewhere, AVYA fell 57% after the company posted terrible preliminary Q3 results and fired the company’s CEO. At the close Friday, AMD passed INTC in terms of market cap after INTC’s -8.56% day on poor earnings and outlook. On Saturday, BA workers cancelled their planned strike and will instead vote on a new contract proposal on Wednesday. Also on Saturday, USB was fined $37.5 million for the same practices that caused the uproar over WFC. USB had pressured employees to meet quotas by illegally accessing customer credit and personal data (for targeting) and then opening sham accounts in customer names.

In China news, real estate developer Evergrande said one of its subsidiaries had been ordered to pay a little over $1 billion to a guarantor, who had guaranteed loans in July 2021. Evergrande defaulted on the loans, the guarantor paid, and now Evergrande is obligated to pay the guarantor ahead of other creditors. In the same sector, a Chinese mortgage payment revolt (well over 100 developers have been hit with a loan payment boycott as projects were not completed by developers) has caused prospective new buyers to rethink. As a result, Chinese July home sales fell a staggering 40% (year on year) as new buyers no longer trust the developers will finish projects. Elsewhere, Speaker of the House Pelosi has left Sunday for her Asian trip with the itinerary, and the Speaker herself being silent on whether there will be a stop in Taiwan. This comes as China decried a potential visit from what would be the highest-ranking US official to visit Taiwan since 1997.

So far this morning, BLDR, J, GPN, AMG, CHKP, ARLP, and L have all reported beats on both the top and bottom lines. Meanwhile, HSBC missed on revenue while beating on earnings. On the other side, CNA and JELD both beat on revenue while missing on earnings. So far there have been no reports today that missed on both revenue and earnings.

Overnight, Asian markets leaned heavily to the green side on Monday. Shenzhen (+1.20%), Thailand (+1.07%), and India (+1.06%) led the gainers. Only Taiwan (-0.12%) showed any red on the day. In Europe, stocks are leaning to the upside, but show more red than in Asia at mid-day. The FTSE (+0.51%), DAX (+0.40%), and CAC (+0.46%) are leading the region higher while 5 exchanges head South, led by Russia (-0.67%) in early afternoon trading. As of 7:30 am, US Futures are pointing toward an open just on the red side of flat. The DIA implies a -0.02% open, the SPY is implying a -0.15% open, and the QQQ implies a -0.11% open at this hour. 10-year bond yields are falling, now at 2.649%, and Oil (WTI) is down more than 1.6% to $97.01/barrel in early trading.

The major economic news events scheduled for Monday are limited to Mfg. PMI (9:45 am) and ISM Mfg. PMI (10 am). The major earnings reports scheduled for the day include AJRD, AMG, ARLP, BLDR, CHKP, CAN, GPN, HSBC, J, JELD, K, and ON before the open. Then, after the close, ATVI, AFL, AMRC, ANET, CAR, CF, CVI, DVA, DVN, FANG, EHC, ENSG, NSP, KMPR, KMT, LEG, MATX, MOS, PINS, RRX, SANM, SBAC, SPG, STRL, TWI, RIG, TA, UNVR, WMB, and WWD report.

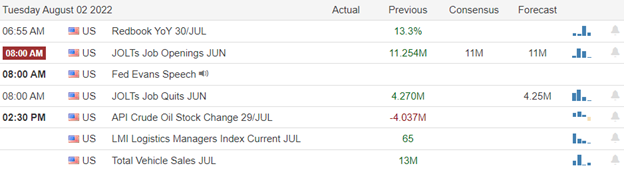

More than 20% of the S&P 500 report earnings this week. However, in economic news later this week, on Tuesday we get June JOLTS, API Weekly Crude Oil Stocks, and Fed voter Bullard speaks. Then on Wednesday the July Services PMI, June Factory Orders, July ISM Non-Mfg. PMI, and Crude Oil Inventories are announced. On Thursday we get Import/Exports, Weekly Initial Jobless Claims, June Trade Balance, and Fed voter Mester speaks. Finally, on Friday we get July Avg. Hourly Earnings, July Nonfarm Payrolls, July Participation Rate, and July Unemployment Rate.

As markets come off a very strong July, the dual fears of inflation and recession remain. However, for the most part, earnings reports continue to be strong…although many commpanies are issuing warnings and guiding lower. In short, we remain in a volatile market where major intraday reversals or many smaller whipsaws remain the norm. The trend remains bullish, but there is a lot of technical damage (resistance) to work through from the months of pullback. The one thing that continues to ring true is that volume shows that retail traders (and the big money) remain afraid to jump into this market yet. So, be cautious in believing that the recent trend truly shows market conviction.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all our money!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: BA, NIO, AMD, TSLA, MU, SQM, WMT, NVDA, MRVL, CVX, KMI. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Despite the GDP showing a technical recession is underway, markets opened with very minimal gaps (in both directions, QQQ down and large-caps up) on Thursday. All 3 major indices then sold off 1% or more over the first hour. However, at 10:30 am, they all reversed and rallied strongly until noon, more than making up for the selloff. After an hour of rest, the rally resumed, reaching the highs of the day late in the session and closing near the highs. This is leaving us with large white candles with significant lower wicks (and small upper wicks) in all 3 major indices.

All 10 sectors were green (with energy down only 0.05% with 30 minutes left in the day. 67% of stocks are now above their 40sma and 27% are above their 200sma. With that said, volume remains below average. We are also looking very overextended in all 3 major indices in relation to the T-line (8ema). On the day, SPY gained 1.25%, DIA gained 1.00%, and QQQ gained 0.98%. The VXX fell 2.3% to 20.82 and T2122 remains deep in the overbought territory at 96.31. 10-year bonds fell to 2.672% and Oil (WTI) was just on the downside of flat for the day at $97.18/barrel.

In economic news, regardless of what Fed Chair Powell, Treasury Sec. Yellen, and the White House said just the day before, GDP data Thursday morning showed we are, at least technically, in a recession. The Q2 GDP came in at -0.9%, far below the consensus estimate of +0.5%. However, that was slightly better than Q1’s -1.6% growth number. In the same vein, Weekly Initial Jobless Claims came in slightly higher than expected at 256k (versus 253k forecast). However, this too was better than the previous week’s 261k number. So, the time series shows improvements, but we’re still worst off on both measures than we thought we should be.

In business news, Thursday was the US House’s turn to pass the “Chips and Science” bill (again in a bipartisan vote) and the “law to be” is now headed for President Biden’s signature. The bill provides $52 billion in subsidies along with another $24 billion in tax credits for semiconductor manufacturing in the US. The House is expected to pass the revised bill later this week. The bill disproportionately benefits INTC, TXN, and MU. (INTC alone is expected to get $30 billion in subsidies.) However, chip designers like AMD, QCOM, and NVDA (regardless of the uproar over insider trading claiming they will benefit) are left out in the cold. This is because the latter group does not make chips. Instead, they contract out the production to TSM and to a lesser extent Global Foundries.

In energy news, as expected, we’ve seen record profits (if for some reason, not always revenue) across the major oil producers so far this quarter. However, a dispute is now in place as the US has officially complained about Mexico’s energy policy of tightening control over its oil and electricity markets. US energy companies see the actions to strengthen the Mexican state-run energy companies at the cost of private investors as a violation of the USMCA (formerly NAFTA) agreement. (And the Biden Administration has taken up the cause on behalf of those companies.) This may lead to a trade dispute, as Mexico is so far being defiant and asserting its national sovereignty. Elsewhere, Europe is scrambling to cut natural gas use, get coal-fired power plants back online, and today France’s President met with Saudi Crown Prince MBS in another bid to get OPEC+ to increase production quotas at their meeting next week. Examples of European gas-saving measures include the German city of Hanover switching off lighting at public fountains, the illuminations of buildings, cutting off hot water in public buildings, mandating 33% higher room temperatures (daycare excluded), and putting motion-detecting lighting in many public conveniences/buildings.

After the close, AAPL, LHX, EIX, EMN, CE, KLAC, AJG, TFII, CC, CLR, TBBK, TXRH, ATR, BIO, SKYW, FSLR, DXCM, UTCC, DECK, AUY, MERC, MTD, MTX, INT, and SGEN all reported beats on both the revenue and earnings lines. Meanwhile, HIG, MHK, OLN, EW, and BZH missed on revenue while beating on earnings. On the other side, AMZN, X, VFC, ERIE, and ULCC beat on revenue while beating on earnings. However, INTC, AVTR, DLR, and ROKU missed on both lines.

Overnight, Asian markets were mixed. Hong Kong (-2.26%) was an outlier while Shenzhen (-1.30%), Shanghai (-0.89%), and Singapore (-0.28%) paced the losses. Meanwhile, Thailand (+1.50%), New Zealand (+1.45%), and India (+1.35%) led the gainers. In Europe, stocks are almost green across the board at mid-day. Portugal (-0.51%) is the only red while the FTSE (+0.58%), DAX (+1.28%), and CAC (+1.42%) lead the region higher in early afternoon trading. As od 7:30 am, US Futures are pointing toward a green, if divergent, start to the day. The DIA implies a +0.21% open, the SPY is implying a +0.66% open, and the QQQ implies a +1.02% open at this hour. 10-year bond yields are back up to 2.701% and Oil (WTI) is back up to $98.60/barrel in early trading.

The major economic news events scheduled for Friday include June PCE Price Index, Q2 Employment Cost Index, and June Personal Spending (all at 8:30 am), Chicago PMI (9:45 am), and Michigan Consumer Sentiment (10 am). The major earnings reports scheduled for the day include ABBV, AB, AON, ARCB, AZN, BLMN, BAH, CRI, CBOE, CHTR, CVX, CHD, CNHI, CL, ENB, XOM, IMO, ITCB, LYB, MGA, NWL, NMRK, NVT, PSX, PG, GWW, and WY before the open. There are no major earnings scheduled for after the close.

So far this morning, CVX, BNPQY, CHTR, LYB, SMFG, AZN, TAK, MFG, CL, AFLYY, WY, BAH, CHT, BLMN, AB, ARCB, and NVT all reported beats on both the top and bottom lines. Meanwhile, XOM, PSX, KMTUY, AON, NWL, and CHD all missed on revenue while beating on earnings. On the other side, PG, MGA, FMS, and ES all beat on revenue while missing on earnings. So far this morning, there are no reports that missed on both revenue and earnings.

What is turning out to be another strong quarter of earnings (despite the lowering of forward guidance) has lifted market spirits. Today, it will be AMZN, AAPL (both from last night), CVX, and XOM that lead markets higher early. There is more economic data, but of late, Mr. Market doesn’t seem to care about economic data. With that said, expect more volatility as intraday reversals are the norm in recent weeks. We do have an uptrend in progress in all 3 major indices, but resistance is not too far overhead and we have a weekend news cycle starting after the close. Both of those urge caution on the Friday trader’s part. The only thing we know for sure is that low volumes for weeks indicate that the big money and John Q Public are not ready to believe the bottom is in just yet.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all our money!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: CLOV, VLO, V, GD, AAPL, NVDA, GE, NFLX, PYPL, CSCO, WMT, CLF. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Despite the rising rates and the U.S. officially entering a recession, earnings results continued to fuel a hurry up and buy something bullish exuberance. With the indexes showing a very extended short-term condition, can they keep it going into the weekend, or will we see some profit taking? As the indexes approach a substantial overhead resistance level, be careful with the urge to rush into already extended stocks. Though there is a lot of bullish energy, remember the Fed is actively working to slow the economy.

Asian markets had a rough session, with the Hang Seng falling 2.26% as tech came under selling pressure. However, European indexes see green across the board ahead of economic data fueled by earnings excitement. With the breakneck pace of earnings slowing a bit with pending economic data, U.S. futures continue the buying spree after AMZN and AAPL earnings results. As we head toward the weekend, it should be another wild day of price action.

Economic Calendar

Earnings Calendar

We have a little lighter day on the earnings calendar with under 100 companies listed. Notable reports include ABBV, AON, B, BLMN, BAH, CBOE, GTLS, CHTR, CVX, CHD, CL, XOM, IMGN, MTD, NWL, PSX, PG, GWW, & WY.

News & Technicals’

European officials have become increasingly concerned about the possibility of a shutdown of gas supplies. Gazprom, Russia’s majority state-owned energy giant, reduced gas supplies to Europe via the Nord Stream 1 pipeline to 20% of full capacity this week. A growing number of economists expect the eurozone to slide into a recession next year. Apple’s services business posted the lowest growth rate since the fourth quarter of 2015. A continuing slowdown could prompt investors to take a closer look at Apple’s valuation. The unit had a gross margin of 71.5% in the latest quarter, compared to Apple’s overall margin of 43.3%. Apple’s services business posted the lowest growth rate since the fourth quarter of 2015. A continuing slowdown could prompt investors to take a closer look at Apple’s valuation. The unit had a gross margin of 71.5% in the latest quarter, compared to Apple’s overall margin of 43.3%. Roku shares plummeted more than 25% in extended trading. The company missed on the top and bottom for its second quarter. Intel slashed its full-year guidance and turned in worse-than-expected quarterly results. The company launched new chips that compete with Nvidia’s graphics cards during the quarter. On Tuesday, the U.S. House approved legislation Intel requested that would subsidize microprocessor manufacturing in the country. McDonald’s said it had concluded the U.S. test of its McPlant burger as planned. Analyst research reported lackluster demand for the meatless burger made using Beyond Meat patties. McDonald’s sells the McPlant burger in several European markets but hasn’t announced a nationwide launch for the menu item in its home market. Amazon executives said consumer spending remains strong despite decades of high inflation. The optimistic commentary is a stark difference from warnings issued earlier in the week by Walmart and Best Buy. Rival retailers have cut their profit outlook after observing consumer spending shifts. Treasury yields moved slightly lower in early Friday trading, with the 2-year at 2.89%, the 5-year at 2.73%, the 10-year at 2.72%, and the 30-year at 3.08%.

Though the U.S. economy officially fell into recession with the GDP at -0.09%, the energy around big tech earnings keeps the bulls buying with a hurry up and buy something mentality. Could the party continue Friday? Of course! However, we could also see some profit taking heading into the weekend, with the T2122 showing a very extended condition. As the market rallies, so do energy and food prices, even as the U.S. dollar remains strong due to the rising interest rates. An interesting situation as we also enter a tax raising cycle on the biggest companies during a worldwide economic slowdown. Today we get the latest reading on Personal Incomes & Outlays, Employment Cost Index, Chicago PMI, and Consumer Sentiment. As we pump up the premarket, watch overhead resistance level and be careful chasing already extended stocks because a consolidation and rest could begin anytime.

The FOMC raised rates as expected and reiterated its commitment to a 2% inflation target, and the bulls partied hard as a result. However, Mike Wilson from Morgan Stanely warned the jump is a trap expecting more market pain on the way, and the T2122 indicator surged back into a short-term extended condition. Price action will likely remain very erratic with a massive day of earnings results that includes AAPL and AMZN with a GDP and Jobless Claims numbers to begin the day! Significant overhead resistance levels are near, so plan your risk carefully.

Asian markets closed mostly higher overnight with modest gains after a choppy session. European markets trade mixed with muted results after the Fed rate decision. As earnings roll out, U.S. futures currently point to modest declines ahead of the GDP report and the mega earnings results from AAPL and AMZN later today. Plan your risk carefully as overhead resistance approaches and the bulls try to keep the party going.

Economic Calendar

Earnings Calendar

Today is the busiest day on the earnings calendar so far, with about 225 companies listed. Notable reports include AAPL, AMZN, AOS, AGCO, MO, AMT, ARES, ABG, BAX, BZH, CPT, CE, CC, COHU, CLR, DECK, DXCM, DSX, DLR, EW, EGO, FHI, FSLR, FTS, BEN, GLPI, HOG, HIG, HSY, HTZ, INTC, KLAC, KDP, LH, MDC, MMP, MLM, MA, MRK, MHK, NOC, OLN, OSK, OSTK, PCG, BTU, PFE, PBI, ROKU, SGEN, SIRI, SO, LUV, SWK, TROW, X, VFC, VLO, VRSN, WFRD, WING, & ZEN.

News & Technicals’

Morgan Stanley’s Mike Wilson believes stocks are on a collision course with more pain due to the economic slowdown. The firm’s chief U.S. equity strategist and chief investment officer said on CNBC’s “Fast Money” that investors should resist putting their money to work in stocks despite the market’s post-Fed-decision jump. Meta missed on the top and bottom lines and gave a troubling forecast for the third quarter. As marketers pull back on ad spending, the shares have lost about half their value this year. The company said its guidance reflects the “continuation of the weak advertising demand environment.” The British bank reported a £1.071 billion ($1.30 billion) net profit attributable to shareholders for the second quarter — down 48% from the same period in 2021. The bank announced earlier this year that it had sold $15.2 billion more in U.S. investment products — known as structured notes — than it was permitted to. The related £1.3 billion in litigation and conduct charges booked in the second quarter were “substantially offset,” according to the bank, by a hedge that generated an income of £758 million. Ford reported second-quarter results that beat Wall Street’s estimates. The company’s adjusted operating income more than tripled from a year ago, when its production was hit hard by a global shortage of semiconductor chips. Ford reiterated its previous guidance for the full year and said it would raise its dividend but wouldn’t comment on reports that it’s planning layoffs. On Wednesday, Senate Majority Leader Chuck Schumer, D-N.Y., and Sen. Joe Manchin, D-W.V. unveiled a long-anticipated reconciliation package that would invest hundreds of billions of dollars to combat climate change and advance clean energy programs. The legislation, called the “Inflation Reduction Act of 2022,” provides $369 billion for climate and clean energy provisions, the most aggressive climate investment ever taken by Congress. The package would curb the country’s carbon emissions by roughly 40% by 2030, according to a summary of the deal.

The bulls partied hard after the FOMC rate decision as the committee reiterated its commitment to bring inflation back to its 2% target. However, Morgan Stanley’s Mike Wilson warned the market jump is a trap suggesting more pain is coming due to the economic slowdown. One thing for sure is that the T2122 indicator points to a short-term overbought condition after the rally, so chasing the move up may be unwise. Expect the price volatility to continue today with a reading on GDP, Jobless Claims, and the mega reports from AAPL and AMZN after the bell. Though the bulls remain in party mode, it would be wise to remember the significant overhead resistance and macroeconomic details that point to a slowing U.S. economy.

Stocks all gapped higher, but diverged in doing so yesterday with the traders seeming to bet that the Fed announcement would be positive for the market. The DIA gapped up four-tenths of a percent, the SPY gapped up nine-tenths of a percent, and the QQQ gapped up 1.6% higher. After a little follow-through, the first 30 minutes all 3 major indices traded flat (even through the Fed rate announcement) until after Fed Chair Presser started. However, the move at 2:40 pm was meteoric to the upside. We then saw the rally continue more-or-less into the close. This left us with a Bull Kicker in the QQQ and SPY, and just a gap-up strong white candle in the DIA.

Almost 62% of stocks are now above their 40sma and 23.54% of them are above their 200sma. So, all 3 major indices are also back above their T-lines (8 ema). The volume on the day was better than Tuesday, but still well below an average that continues to decline. All 10 sectors were green, with Technology far and away the big winner, up 4.37%. On the day, SPY gained 2.60%, DIA gained 1.41%, and QQQ gained 4.23%. The VXX fell 1.7% to 21.31 and T2122 climbed high into the overbought territory at 97.16. 10-year bond yields fell to 2.776% and Oil (WTI) spiked 3.3% to $98.12 (apparently on answers from Chair Powell that we are not in a recession).

As expected, the Fed (in a unanimous vote) raised rates 0.75%, which takes the rate to 2.25-2.50% on Wednesday. The hike itself was fully priced-in and markets had very little reaction on the hike news alone. However, Fed Chair Powell’s press conference set off a massive afternoon rally. In his presser, Powell said he did not think the US was in a recession yet (we’ll find out later this morning). He also said it would be appropriate at some point for the Fed to slow increases and assess how the overall policy was impacting both inflation and the economy. This left open the possibility for a lesser increase in Sept. which is what I think may have led to the presser-timed rally. He went on to point out the job growth remains robust and unemployment remains low.

In business news, the US Senate passed the “Chips and Science” bill in a bipartisan vote. This bill provides $52 billion in subsidies along with another $24 billion in tax credits for semiconductor manufacturing in the US. The House is expected to pass the revised bill later this week. The bill disproportionately benefits INTC, TXN, and MU. (INTC alone is expected to get $30 billion in subsidies.) However, chip designers like AMD, QCOM, and NVDA (regardless of the uproar over insider trading claiming they will benefit) are left out in the cold. This is because the latter group does not make chips. Instead, they contract out the production to TSM and to a lesser extent Global Foundries.

In stock news, after the close, SAVE canceled its negotiations with potential buyer ULCC after months of negotiations. SAVE’s talks with JBLU (another potential buyer) continue. (Then overnight JBLU agreed to buy SAVE for $3.8 billion.) However, any potential purchase may face monopoly scrutiny related to the Northeast corridor routes. Elsewhere, BBY lowered its forward guidance and is now expecting a drop of 13% in sales in Q3 and an 11% drop for the year. CS also announced they have replaced their CEO.

After the close, F, QCOM, MOH, CHRW, MUSA, LRCX, URI, FBHS, NCR, NOV, MTH, CSL, HOLX, GFL, CCS, ASGN, PLXS, MKSI, FIX, MYRG, CMPR, ACHC, AVB, QGEN, ETSY, GGG, TDOC, INVH, SLM, SNBR, MAA, FRWD, TYL, VICI, HP, and EQT all reported beats on both the top and bottom lines. Meanwhile, FLEX, WFG, RJF, FTI, OMF, KGC, and OII all beat on revenue while missing on earnings. On the other side, CTSH, RE, ACGL, EQIX, NOW, AWK, AEM, TROX, FLS, ICLR, ESI, COLM, AMED, CHE, and CHDN all missed on revenue while beating on earnings. However, META, ORLY, CYH, CINF, SSNC, MEOH, ALGN, LUNMF, CAKE, AR, JBT, and PTC all missed on both the revenue and earnings lines.

Overnight, Asian markets were almost green across the board. Only Hong Kong (-0.23%) and Taiwan (-0.20%) showed any red. Meanwhile, New Zealand (+1.74%), India (+1.73%), and Thailand (+1.50%) led the region higher. In Europe, stocks are showing a similar pattern at mid-day. It is the biggest exchanges that lag the rally with the FTSE (-0.15%), DAX (+0.01%), and CAC (+0.13%) following the rest of the continent in early afternoon trading. As of 7:30 am, US Futures are pointing toward a modestly down start to the day. The DIA implies a -0.14% open, the SPY is implying a -0.22% open, and the QQQ implies a -0.56% open at this hour. 10-year bond yields are up slightly to 2.785% and Oil (WTI) is up more than 2% to $99.24/barrel in early trading.

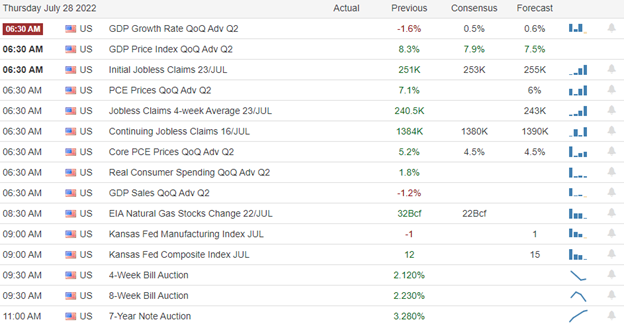

The major economic news events scheduled for Thursday are limited to Q2 GDP and Weekly Initial jobless Claims (both at 8:30 am). Treasury Sec. Yellen also speaks at 8:30 am. The major earnings reports scheduled for the day include AOS, AGCO, ALLE, MO, AMT, BUD, HOUS, MT, ARCH, ARES, ABG, BAX, BFH, BC, CP, CRS, CARR, CVE, CMS, CNX, CMCSA, DTE, EXP, EME, EEFT, FAF, FCNCA, FCFS, FMX, FTS, FTV, BEN, FCN, GTX, GOL, GVA, HOG, HSY, HTZ, HON, IP, JHG, KDP, KEX, LH, LAZ, LII, LECO, LIN, LKQ, MDC, MMP, HZO, MLM, MAS, MA, MRK, NOC, ORI, OSK, OSTK, PATK, PBF, BTU, PFE, PCG, BPOP, POR, RS, RCL, SNY, SNDR, SHEL, SIRI, SAH, SO, LUV, SWK, STM, TROW, TRP, TFX, TXT, TMO, TKR, TNL, VLO, VSTO, VC, WST, WEX, WTW, and XEL before the open. Then after the close, AMZN, AAPL, ATR, AJG, AVTR, BZH, BIO, CE, CC, CLR, DECK, DXCM, DLR, EMN, EIX, EW, ERIE, FSLR, HIG, INTC, KLAC, LHX, LBTYA, MTD, MTX, MHK, OLN, ROKU, SKYW, TXRH, TFII, UCTT, X, VALE, VFC, INT, and AUY report.

So far this morning, CMCSA, VLO, PFE, MRK, SNY, TMO, HON, CVE, LIN, MO, PBF, IP, CARR, SO, ASX, LUV, LH, RS, TXT, KDP, XEL, STM, ABG, AMT, HSY, BC, MDC, ARES, TKR, AOS, VSTO, ALLE, WST, EEFT, VC, KEX, VIRT, POR, EXP, WEX, VLY, TRTN, HEES, KIM, CBZ, and STNG all beat on both the top and bottom lines. At the same time, MT, BUD, NOC, LKQ, FAF, HOG, LAZ, TNL, TFX, HZO, FCFS, SHEL, and WTW all missed on revenue while beating on earnings. On the other side, DTE, SIRI, FTS, and ARCH beat on revenue while missing on earnings. However, SWK, SAH, DTE, BAX, MAS, OSK, TROW, GVA, GTX, OSTK, and JHG all missed on both the top and bottom lines.

In economic news coming later this week, Friday we get the June PCE Price Index, Q2 Employment Cost Index, June Personal Spending, Chicago PMI, and Michigan Consumer Sentiment.

As usual on Fed rate hikes, the market seems to have rethought the late afternoon rally from yesterday and is looking to open tepidly bearish…pending the GDP news, of course. Truthfully, the GDP print (and whether we are actually already in a recession) will drive trading today…especially if it says we are. Also, don’t discount the talking heads rehashing and reparsing every word Powell said yesterday. That may cause fluctuations across the market as every Tom, Dick, and Harry tells us what Powell “was really saying or implying.” Beyond that, we now have higher lows and higher highs in all 3 major indices, which is the very definition of an uptrend. However, don’t be surprised if/when we see more intraday whipsaw action.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all our money!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: ENVX, DOV, MRO, GE, F, BEAM, TXN, NFLX, NOK, PYPL. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Though the tech giants missed expectations, the market appears willing to forgive and continue to buy with high hopes the worst of the 2022 bear market is over. Unfortunately, we still have plenty of uncertainty today, considering the slew of earnings and economic reports culminating in an FOMC rate decision, keeping price action extremely challenging. We should continue to watch for the possibility of pop and drop this morning, so be careful rushing into risk at the open. We have a lot of data coming our way, and anything is possible as the details roll out. So, prepare for another wild day of hurry up and wait.

Asian markets traded mixed overnight as Hong Kong slipped 1.13% due to rising inflation in Australia. European markets trade cautiously higher this morning, focusing on the Fed decision ahead. Despite the mixed earnings results and pending economic reports, U.S. futures point to a bullish open, but a lot could change as data rolls out. The pop and drop is possible but be ready for just about anything as the market reacts.

Economic Calendar

Earnings Calendar

Again we ramp up the number of earnings reports today with more than 170 companies listed. Notable reports include META, ASGN, AEM, ALGN, AMED, AEP, AWK, ADP, AVY, BA, BOOT, BSX, BMY, BG< CHRW, CAKE, CHDN, CTSH, COLM, CYH, ETSY, EVR, FLEX, F, GD, GPC, HLT, KHC, LC, MHO, NSC, ORLY, ODFL, OC, PPC, QCOM, RJF, R, NOW, SHW, SHOP, SPOT, STAG, SHOO, TMUS, TDOC, URI, UPWK, VICI, WM, & WFG.

News & Technicals’

Alphabet reported earnings per share of $1.21 vs. $1.28 expected. The company also fell short of revenue expectations for advertising and Google Cloud. Alphabet shares have lost about a quarter of their value this year. Alphabet’s second quarter showed the slowest growth in YouTube ad revenue since the company first began reporting those numbers in the fourth quarter of 2019. Executives said a combination of tougher year-over-year comparisons and economic headwinds were primarily to blame. “Time will get us through the lapping,” CFO Ruth Porat said on the earnings call. Microsoft’s revenue and income fell short, as did the company’s revenue from Azure and other cloud services. Changing exchange rates and challenges in advertising and the PC markets brought down revenue in the quarter. Germany, the region’s largest economy and traditional growth driver, has a particular reason to worry. It’s largely reliant on Russian gas and is sliding toward a recession. The possibility of a recession in Europe now seems “clear-cut,” Citi economists and strategists said in a note Tuesday. “Time will get us through the lapping,” CFO Ruth Porat said on the earnings call. In a phone interview on Wednesday, such a drop would be worse than in 2008 when sales fell by roughly 20%, Esther Liu, director at S&P Global Ratings. She said the latest developments had delayed a recovery in China’s real estate sector to next year. Chipotle reported weaker-than-expected sales for its second quarter, although higher prices drove strong profit growth. Facing higher food, packaging, and labor costs, Chipotle also said it would hike prices again in August. “Fortunately for Chipotle, you know, most of our customers are a higher household income consumer,” CEO Brian Niccol said on the company’s earnings call. The Federal Reserve is expected to raise interest rates by three-quarters of a point Wednesday afternoon, its second hike in a row of that size. Investors will seek guidance from Fed Chairman Jerome Powell on what the central bank may do at its September meeting, but he is likely to be vague and leave options open. “I think they’re going to lean a little bit more hawkish on September,” said one strategist. “They’re just not seeing the progress on inflation.” Treasury yields traded nearly flat in early Wednesday trading as they wait on the FOMC decision. The 2-year priced at 3.05%, the 5-year is at 2.88%, the 10-year traded at 2.79%, and the 30-year slipped to 3.02%.

After a choppy of waiting, the tech giants MSFT and GOOGL reported a miss on expectations, but traders didn’t seem to care, buying up the stocks anyway, apparently thinking the worst of the bear 2022 bear market is over. However, the uncertainty is not over with Durable Goods, International Trade, Pending Home Sales, Petroleum Status, an FOMC rate decision, and a hectic day of earnings reports that includes META. With futures pointing to a bullish open, the T2122 indicator still elevated the pop, and drop remains a possibility considering all the uncertainty of the data ahead. That said, there seems to be an incredible willingness to buy up risk despite the weak economic data, so anything is possible over the short term. Personally, I think the market will see new lows in 2022 once the relief rally has run its course, and it may be the hawkishness of the FOMC that sets that in motion.

Markets gapped down between one and two-thirds of a percent at the open Tuesday. All 3 major indices then followed through by selling off until lows were hit about noon. From that point, DIA recovered a little with the SPY and QQQ continuing to bob along the lows. However, from 1:30 pm to 3 pm all 3 indices sold off again to drive to new lows before grinding sideways the last hour. 8 of the 10 sectors are in the red with Consumer Cyclical and Technology taking by far the worst hit. Healthcare and Utilities sectors managed to stay green. This action had all 3 major indices printing gap-down, black-bodied candles. QQQ has clearly given up the T-line as support while the SPY could be said to still be testing it and the DIA has yet to reach that much pullback. With that said, all 3 are holding just above their 50sma.

On the day, SPY lost 1.18%, DIA lost 0.76%, and QQQ lost 1.96%. The VXX rose almost 3.5% to 21.67 and T2122 fell to just outside the overbought territory at 76.34. 10-year bond yields climbed back to remain flat at 2.80% and Oil (WTI) fell 1.6% to $95.16/barrel. As has been the case for weeks, the volume was very light. So, overall, it looks like Mr. Market was betting on more downside ahead of Wednesday’s Fed announcement.

In business news, just before the open, SHOP announced it will lay off 10% of its workforce as the company struggles with slowing growth. After hours, TEVA announced it had reached a nationwide settlement of opioid lawsuits in the amount of $4.25 billion paid over 13 years. The NHTSA also announced it will be investigating a crash (which killed a motorcyclist) that involved a TSLA which was operating under Autopilot mode. Of note, both MDLZ and KO raised their full year guidance on strong demand. Finally, TWTR announced after hours that it will hold its shareholder vote on the Musk acquisition on September 13 (the court case takes place in October).

In energy news, after hours the American Petroleum Institute announced that US oil inventories fell by more than 4 million barrels last week (a drawdown of 1.21 million barrels was expected). The White House also announced that it does not plan to continue releasing oil from the Strategic Petroleum Reserve after the initial 6-month window. Elsewhere, the EU has agreed on cuts to natural gas usage. Each country agreed to cut their usage by 15% from August through March (versus the average use from 2017-2021). However, the agreement included exemptions for many industries. In related news, Germany announced it will cut electric car subsidies in 2023.

After the close, ASH, CB, MDLZ, V, TXN, AMP, CNI, FE, SKX, AGR, AXS, RUSHA, TNET, TER, BYD, CHX, BXP, EQR, CSGP, MTDR, ENPH, and NEX all reported beats on both the top and bottom lines. Meanwhile, CMG, and AXTA missed on revenue while beating on earnings. On the other side, JNPR, ZION, and HA beat on revenue while missing on earnings. However, GOOGL, GOOG, MSFT, and SYK all missed on both revenue and earnings.

So far this morning, BASFY, HUM, BMY, KHC, GPC, WM, TEVA, TEL, AEP, ADP, BSX, RCI, GIB, OC, AVY, TECK, CSTM, TMHC, ICL, HLT, GRMN, ODFL, EVR, IEX, SCL, SHOO, CHEF, TRN, and CCJ all posted beats on bot the top and bottom lines. Meanwhile, EQNR, GSK, GD, PAG, OTIS, GPI, ROK, CME, TPX, TDY, PRG, and TRN all missed on revenue while beating on earnings. On the other side, BG, DB, CS, SPOT, UMC, IVZ, EDU, and WNC beat on revenue while missing on earnings. However, BA, TMUS, and SHW missed on both the revenue and earnings lines.

Overnight, Asian markets were mixed but leaned to the upside. Hong Kong (-1.13%) was the only appreciable loser on the day. Meanwhile, Thailand (+1.50%), India (+0.96%), and Taiwan (+0.78%) led the gainers. In Europe, stocks are mostly green at mid-day. With only 3 minor exchanges showing very modest red, the FTSE (+0.57%), DAX (+0.26%), and CAC (+0.24%) are more typical of the region in early afternoon trading. As of 7:30 am US Futures are pointing toward a green start to the day ahead of data. The DIA implies a +0.37% open, the SPY is implying a +0.80% open, and the QQQ implies a +1.33% open at this hour. 10-year bond yields remain flat at 2.801% and Oil (WTI) is up 1.2% to $96.13/barrel in early trading.

The major economic news events scheduled for Wednesday include June Durable Goods Orders, June Trade Goods Balance, and June Retail Inventories (all at 8:30 am), June Pending Home Sales (10 am), Crude Oil Inventories (10:30 am), the Fed Interest Rate Decision and Fed Statement (both at 2 pm), and FOMC Chair Press Conference (2:30 pm). The major earnings reports scheduled for the day include AEP, APH, ADP, AVY, BA, BSX, BMY, BG, CAJ, GIB, CHEF, CME, CSTM, CS, CPG, DB, DRVN, EVR, FSV, GRMN, GD, GPC, GPI, HES, HLT, HUM, ICL, IVZ, KHC, LW, MHO, NSC, ODFL, OPCH, OTIS, OC, PAG, PRG, ROK, RCI, ROL, R, SAIA, SHW, SHOP, SLGN, SPOT, SCL, SHOO, TMUS, TMHC, TEL, TECK, TDY, TPX, TEVA, TRN, UMC, WNC, and WM before the open. Then after the close, ACHC, AEM, ALGN, AMED, AWK, NLY, AR, ACGL, ASGN, AVB, CHRW, CSL, CG, CCS, CAKE, CHE, CHDN, CMPR, CINF, CTSH, COLM, FIX, CYH, ESI, EQT, EQIX, ETSY, RE, FLEX, FLS, F, FBHS, FWRD, GFL, GGG, HP, HOLX, ICLR, INVH, JBT, LCRX, MTH, META, MEOH, MAA, MKSI, MOH, MUSA, MYRG, NCR, NOV, ORLY, OII, OMF, PPC, PLXS, PTC, QCOM, RJF, NOW, SNBR, SSNC, STC, FTI, TDOC, TROX, URI, VICI, WFRD, and WFG report.

In economic news coming later this week, Thursday brings Q2 GDP and Weekly Initial jobless Claims. Then Friday we get the June PCE Price Index, Q2 Employment Cost Index, June Personal Spending, Chicago PMI, and Michigan Consumer Sentiment.

With the Fed taking center stage today, the major indices seem a little bullish in premarket. And while there may be a pop to start the day, do not be surprised if we see a reversal or at least a dead market until the FOMC news finally breaks and we hear Fed Chair Powell’s tone in the presser. Futures have pegged it as an extremely high probability of a 0.75% rate hike. However, the outlook for September and beyond will be at least as important as the hike itself. The only exception to this would be if the Fed goes bigger to a 1% hike (which is a low probability according to futures). The point is the market is hanging on words and parsing sentences. So, don’t predict and get burned. Also, don’t be surprised if/when we see more intraday whipsaw action…especially after the 2 pm announcement. Still, the longer-term chart continues to show the downtrend hasn’t been broken (or at least it is not clear it is broken and held) across the major indices. So, be careful taking anything but very short-term trades. Also, remember that Q2 GDP comes out tomorrow and there are a flood of earnings still coming. Caution, hedged, small-and-nimble, or flat are the watchwords at the moment.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all our money!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

It would seem rather obvious that the next several days of this earnings silly season will be ruled by tremendous speculation and trepidation. Perhaps the market could do better with a psychological analyst than a technical analyst due to the emotional reactions we will likely see the rest of the week. Today we have housing data, consumer confidence numbers, and a large group of earnings reports that will reach a feared pitch when GOOGL and MSFT report after the bell. As the market reacts, expect very challenging price action with whipsaws and significant morning gaps.

Asia market finished the day with primarily bullish results, led by Hong Kong, up 1.67% at the close. Unfortunately, European markets look mostly lower this morning as they wait on earnings results and the FOMC decision Wednesday afternoon. Likewise, U.S. futures point lower this morning after some early disappointing earnings results, but anything is possible by the open as data continues to roll out. Experienced day traders will likely have the upper hand as the market reacts to the tech giant reports throughout the week.

Economic Calendar

Earnings Calendar

Tech Giant reports begin after the bell today with a busy morning to set the stage for volatility. Notable reports include GOOGL, MSFT, MMM, AGYS, ACI, ADM, BXP, BYD, CNC, CMG, CB, KO, GLW, ENPH, FE, FISV, GE, GM, IEX, JNPR, KMB, MSCI, MCD, MDLZ, NAVI, PCAR, PII, PHM, RTX, SSTK, SKK, SAVE, SYK, TER, TXN, TRU, UBS, UPS, V, VIST, WH, XRX, YNDX, & ZION.

News & Technicals’

A late Monday announcement from WMT, which cut quarterly and full-year profit estimates citing rising food inflation. WMT plunged nearly 9% in extended trading, dragging down other retail stocks, TGT fell 4,7%, AMZN dropped 3%, M & DG declined 4.3% & 3.3% respectively. CEO Doug McMillon said aggressive markdowns on items such as clothing are also hurting margins. General Motors reported second-quarter earnings that fell short of Wall Street’s estimates after supply chain issues led it to ship fewer vehicles than expected. GM also confirmed that it had secured the battery materials needed to build 1 million EVs annually by 2025. The company maintained its previous earnings guidance for the full year and expected to ramp up production in the second half. With second-quarter GDP data due Thursday, the question of whether the economy is in recession will be on everyone’s mind. The economy stands at least a fair chance of hitting the rule-of-thumb recession definition of two consecutive quarters with negative GDP readings. Should inflation stay at high levels, that will trigger the biggest recession catalyst, namely Federal Reserve interest rate hikes. Treasury Secretary Janet Yellen said “we just don’t have” conditions consistent with a recession. Major U.S. and European banks should be prosecuted for “committing war crimes” over their financing of the Russian regime, according to a top aide to Ukraine president Volodymyr Zelenskyy. Oleg Ustenko, an economic advisor to Zelenskyy, said the Ukrainian government believes banks, such as JPMorgan, HSBC, and Citi, are aiding the Kremlin’s war efforts in Ukraine. “Everybody who is financing these war criminals, who are doing these terrible things in Ukraine, are also committing war crimes in our logic,” he told CNBC’s Hadley Gamble on “Capital Connection” on Tuesday. UBS posted a net profit attributable to shareholders of $2.108 billion, below analyst expectations aggregated by the Swiss bank. As market declines accelerated across equity and fixed income in the second quarter, the bank’s wealth management division took a hit. However, CEO Ralph Hamers told CNBC that this had been largely offset by rising interest rates, with the U.S. Federal Reserve embarking on an aggressive hiking cycle to reel in inflation. Treasury yields moved slightly lower in early Tuesday trading, with the 2-year pricing at 3.00%, the 5-year at 2.84%, the 10-year at 2.75%, and the 30-year dipping to 2.98%.

The silly season will hit its stride today with tremendous speculation and trepidation as we wait on the tech giants GOOGL and MSFT to report after the bell today. Toss in the busy morning slate of earnings reports, a reading on Consumer Confidence and housing with Case-Shiller & New Home Sales, and we have the recipe for wild price action. Then, of course, the market will also have to deal with the anxiety of the pending FOMC rate decision Wednesday afternoon. I think it goes with saying that anything is possible, and even the best technical analysis likely won’t be of much use as the emotion spill out in reaction to the data. Protect your capital and prepare for intraday whipsaws and possible significant morning gaps the rest of the week.

Stocks opened flat to modestly higher on Monday. The two large-cap indices then proceeded to roller-coaster sideways until 1:30 pm – 2 pm, when a modest selloff took us to the lows of the day by 3 pm. Meanwhile, the QQQ sold off the first hour of the day and then roller-coastered sideways at a lower level until 1 pm, when its own selloff took hold taking it to the lows of the day also at 3 pm. However, a late rally took all 3 major indices up off the lows in a strong rally the last 30 minutes. On the daily chart, this left us with black-bodied candles with wicks on both ends (the longer one to the downside). The SPY and DIA printed indecisive Doji candles and the QQQ printed a Spinning Top. However, all 3 major indices do remain above their T-line in a rising short-term trend.

All of this happened on very low volume yet again (with only a dark pool surge taking the DIA barely above average volume. On the day, SPY gained 0.12%, DIA gained 0.28%, and QQQ lost 0.57%. The VXX fell a little over 1% to 21.15 and T2122 climbed deeper into the overbought territory at 91.22. 10-year bond yields rose to 2.805% and Oil (WTI) climbed more than 2% to $96.66/barrel. Despite this roller-coaster action in the indices, 8 of the 10 sectors were in the green, including Energy (which was far-and-away the biggest mover on the day) while Technology and Consumer Cyclicals were moderately lower.

In business news, after hours WMT warned about its profit forecast. This warning comes after the retailer cut its prices to get rid of excess inventory. This news sent shocks throughout the retail industry. WMT stock was down more than 10% in post-market trading. AMZN was off 4.5% and TGT was down almost 6% on the WMT news. Discount chains fared slightly better on that news. BIG, DLTR, DG, BJ, and OLLI were all down 4%, while COST was down 3%.

In energy news, during the day Russia’s Gazprom said it would further reduce the flow of gas to Europe from 40% of pipeline capacity to 20% of capacity. Gazprom said they were having equipment problems related to a turbine pump sent to Canada (Siemens) for repair, delayed in return due to sanctions, and now back in Russian hands. In related news, the IEA says that the US has eclipsed Russia to become the largest exporter of natural gas to Europe as of last month. Elsewhere, Reuters reports that a drop off in US demand, a glut of oil at trading hubs, and the expected coming exports from China and India (reshipping Russian oil) has refiners under pressure. The report says that refiners are now looking to reduce production in order to maintain higher profit margins. This comes as we now have had 6.5 consecutive weeks of falling gasoline prices.

After the close, UHS, PKG, CDNS, FFIV, ARE, WIRE, and CADE all reported beats on both the revenue and earnings lines. Meanwhile, WHR, and RNR both missed on revenue while beating on earnings. On the other side, NXPI, and SSD both beat on revenue while missing on earnings. However, KALU missed on both the top and bottom lines.

So far this morning, CNC, UPS, ADM, GE, KO, FISV, GPK, PNR, AAN, and ARCC all reported beats on both the top and bottom lines. Meanwhile, RTX, MMM, MCD, PHM, PII, XRX, AVNT, TRU, VNTR, and MSCI missed on revenue while beating on earnings. On the other side, UBS beat on revenue while missing on earnings. However, GM, MCO, and CEQP missed on both the revenue and earnings lines. It is worth noting that MMM also announced it will spin off its healthcare unit into a separate publicly trade company. That transaction is expected to complete at the end of 2023. In addition, GM cited supply chain problems for their misses and MCD touted price increases (increased margins) as the reason it beat on earnings even while missing on lower sales.

Overnight, Asian markets were mixed. Hong Kong (+1.67%), Shenzhen (+0.95%), and Shanghai (+0.83%) led the gainers. Meanwhile, India (-0.898%), Taiwan (-0.87%), and Thailand (-0.46%) paced the losses. In Europe, we see a similar picture taking shape at mid-day. The FTSE (+0.56%) points higher while the DAX (-0.92%) and CAC (-0.48%) point lower. Russia (+1.95%) is the biggest mover in early afternoon trading. As of 7:30 am, US Futures are pointing toward a down start to the day. The DIA implies a -0.43% open, the SPY is implying a -0.35% open, and the QQQ implies a -0.45% open at this hour. 10-year bond yields are falling at 2.758% and Oil (WTI) is up 1.8% to $98.48/barrel in early trading.

The major economic news events scheduled for Tuesday include Conf. Board Consumer Confidence and June New Home Sales (both at 10 am), and the 5-year bond auction (1 pm). The major earnings reports scheduled for the day include MMM, AAN, ACI, ADM, ARCC, AVNT, CNC, KO, GLW, CEQP, ECL, FISV, FELE, GE, GM, GPK, HUBB, IVZ, KMB, MCD, MCO, MSCI, PCAR, PNR, PII, PHM, RTX, ST, TRU, UBS, UPS, WSO, and XRX before the open. Then after the close, GOOGL, AMP, ASH, AGR, AXTA, AXS, BXP, BYD, CNI, CHX, CMG, CB, CSGP, ENPH, EQR, FE, GOOG, HA, JNPR, MTDR, MSFT, MDLZ, NEX, RUSHA, SKX, TER, TXN, V, and ZION report.

In economic news coming later this week, on Wednesday, June Durable Goods Orders, June Trade Goods Balance, June Retail Inventories, June Pending Home Sales, Crude Oil Inventories, the Fed Interest Rate Decision, Fed Statement, and FOMC Press Conference are announced. Thursday brings Q2 GDP, and Weekly Initial Jobless Claims. Finally, Friday we get the June PCE Price Index, Q2 Employment Cost Index, June Personal Spending, Chicago PMI, and Michigan Consumer Sentiment.

The WMT warning and big-name earnings misses have markets pulling back this morning. However, at least at this point, it looks like the T-line is holding as support and the daily chart continues to look like nothing more than a pullback in the recent week-long uptrend. These factors, plus the earnings calls, are likely to drive the market early today. As we get later in the day, positioning for tomorrow’s Fed announcement (which futures show a very high probability of being a 0.75% hike…but the wording and Q/A count!) and perhaps some waiting on that shoe to drop are likely to be the key factor across stocks, bonds, and even energy commodities. Don’t be surprised if/when we see more intraday whipsaw action. Still, if we look at a longer-term chart, you can see that the downtrend has not been broken (or at least it is not clear it is broken and held) across the major indices. So, be careful taking anything but short-term trades ahead of the data and more importantly market reactions coming later in the week.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all our money!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: BBY XRT, SBUX, COST, ETSY, TSLA, DKS, ROST, GES, PLNT, CHWY. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service