Traders Eyeing PPI Data and Jobless Claims

On Wednesday, July CPI numbers came in much better than expected and this led to the bulls gapping markets higher. The DIA gapped up 1.42%, the SPY gapped up 1.79%, and the QQQ gapped up a massive 2.39% at the open. This broke the market out of its pullback from the last couple of days. However, after the open, all the heavy partying was over, as the bulls failed to give us follow-through with prices chopping sideways with a slightly bullish trend most of the day. With that said, a rally at the end of the day took us out near the highs. This left us with gap-up, indecisive, Spinning Top or Hangman type candles in all 3 major indices.

All ten sectors were green with Technology and Consumer Cyclical up more than two and three-quarters percent. So, we definitely saw a risk-on day. With that said, all 3 major indices are also now fairly extended from their T-line (8ema). On the day, SPY closed up 2.04%, DIA was up 1.57%, and QQQ was up 2.79%. The VXX fell to 21.44 and T2122 (4-week New High/Low Ratio) is back up deep into the overbought territory at 95.18. Interestingly, 10-year bond yields were flat on the day at 2.785% and Oil (WTI) is back up 1.13% to $91.51/barrel on the session.

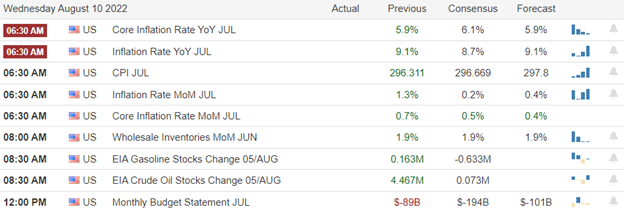

In economic news, as mentioned, July CPI came in a +8.5% annually. This was much better than the +8.7% expected and a lot better than June’s +9.1% annual reading. EIA Crude Oil Inventories followed Tuesday night’s API data came in dramatically higher than expected. The reading was +5.458 million barrels compared to a flat +0.073 mil barrels expected. The 10-year note auction came in at a lower than current 10-year yields (2.775% versus 2.785% open market) and significantly lower than the last auction (2.960%). Finally, the July Federal Budget Balance came in at 211 billion, which is down 30% from the same period in 2021.

SNAP Case Study | Actual Trade

In energy news, Russian oil deliveries to Hungary. Slovakia, and the Czech Republic after a Hungarian group agreed to pay Ukraine in dollars for the pipeline transit fees. This is a solution only for the month of August. Elsewhere, on Wednesday, LNT, WEC, NI, and PNM all announced that they are delaying the closure of coal-fired power plants in the US. This is seen as a political gesture in response to the climate provisions of the recently passed Inflation Reduction Act. All the companies cited delays or potential delays in the rollout of renewable energy projects when announcing the decision. In a follow-up to the EIA Crude report, they also announced a drawdown of 4.978 million barrels for the week. This indicates an increase in travel for the week.

After the close, DIS, AVT, and STN all reported beating on both the top and bottom lines. Meanwhile, CPNG, CACI, ENS, MFC, and VZIO all missed on revenue while beating on earnings. However, APP missed on both the revenue and earnings lines.

In stock news, APP made an all-cash offer to acquire U. This came the same day that U announced it has won a US government contract in partnership with CACI to provide simulation software. ACHR has received a $10 million pre-delivery payment from UAL in relation to UAL’s order for 100 of the ACHR electric vertical takeoff and landing aircraft. During its earnings reports, DIS announced that Disney+ subscriber growth was much higher than expected. Analysts had forecast 147 million, but DIS reported 152.1 million subscribers. Finally, JPM gold traders were found guilty of manipulating gold commodity prices by issuing bogus orders (canceled just before execution). They join traders from DB and BAC who were previously convicted for the same “order spoofing” crimes.

Overnight, Asian markets were almost green across the board. Only Japan (-0.65%) showed any red. Meanwhile, Hong Kong (+2.40%), Shenzhen (+2.05%), Taiwan (+1.73%), and South Korea (+1.73%) led the region higher. In Europe, most exchanges are on the green side, with the exception of the majors, at mid-day. The FTSE (-0.33%), DAX (-0.07%), and CAC (-0.19%) lag the rest of the region in early afternoon trade. As of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.42% open, the SPY is implying a +0.31% open, and the QQQ implies a +0.21% open at this hour. 10-year bond yields are back down to 2.772% and Oil (WTI) is up three-quarters of a percent in early trading this morning.

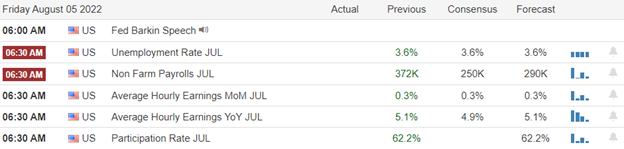

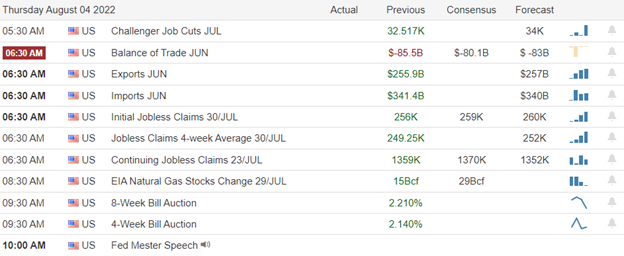

The major economic news events scheduled for Thursday include July PPI and Weekly Jobless Claims (both at 8:30 am). The major earnings reports scheduled for the day include AER, AIT, AZUL, BAM, CAH, DDS, HBI, KELYA, EYE, PRMW, SIX, and USFD before the open. Then, after the close, AQN, BAP, EDR, FLO, ILMN, OSCR, PFHC, RMD, RYAN, TOST, and VET report.

So far this morning, DTEGY, BAM, BFRS, USFD, DDS, AER, AIT, DDL, EYE, PRMW, and SLVM have all reported beats on both lines. Meanwhile, CAH, KELYA, and TAST all missed on earnings while beating on revenue. However, AEG, HBI, and SIX missed on both the top and bottom lines.

In economic news, later this week, on Friday the July Import/Export Price Index, Michigan Consumer Sentiment, and WASDE Ag Report are released.

After yesterday’s happy CPI news (if 8.5% inflation can be called happy news), traders are hoping for a similar story from PPI. (We know inflation is high, but we want to see Producer Prices coming in a bit to indicate that inflation has already peaked.) That sets up a binary even (similar to earnings, but in this case covering the entire market). If PPI comes in lower than expected, look for traders to gap stocks higher again. However, if PPI does not show the improvement we saw in CPI, I’d expect traders to believe they were overly optimistic yesterday and sell the market in a knee-jerk reaction. With that backdrop look for another low volume, volatile day. So, either look for longer horizons (loose stops and ability to ride fluctuations) or tighten up on the bat and take smaller, faster swings. Overall the trend remains bullish, but stocks are extended again relative to their T-lines and T2122.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: UAA, DIS, CVX, Z, BA, AMD, BAC, COF, GRWG, SBUX. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service