CPI Today, Some Expect Better Number

Markets gapped up through the downtrend lines in all 3 major indices. After that we saw some follow-through for an hour in the SPY, DIA, and QQQ for an hour. Prices then drifted back lower until shortly after noon, reaching the opening levels again. From that point on, price meandered between the open and the highs. This action left us with gap-up white candles with upper wicks (especially in the DIA).

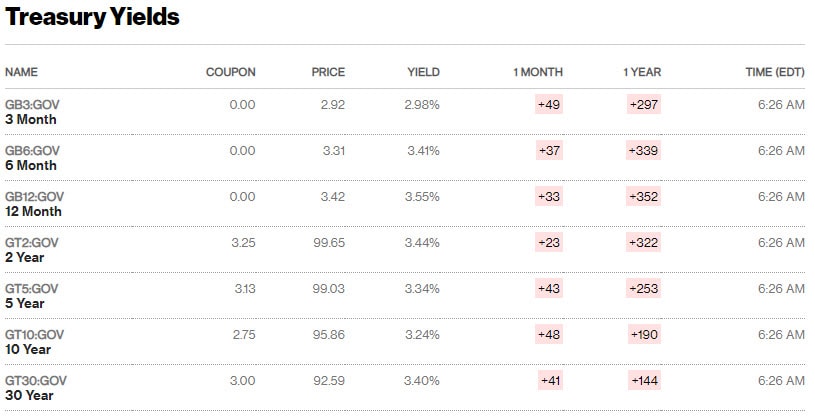

On the day, all 10 sectors are green with Consumer Cyclical (+1.61%) and Energy (+1.54%) leading the way higher. The SPY gained 1.07%, the DIA gained 0.71%, and the QQQ gained 1.19%. The VXX is off 1.73% to 18.15 and T2122 is up well into the overbought territory at 91.92. (The 3 major indices are also a tad extended above their respective T-lines.) 10-year bond yields have spiked back up to 3.356% (after being down in the 3.27% range early in the day) and Oil (WTI) is up 1.2% to $87.94/barrel. Overall, the bulls were in a good mood from the Ukraine news and their growing expectation that CPI will come in better than forecast tomorrow morning.

In business news, Monday afternoon, GS announced it will be cutting several hundred positions later this month. Then, after the close, PTON announced a major shakeup. Two of the PTON Co-founders (including the CEO and Chairman) as well as the Chief Commercial Officer are leaving. Elsewhere, after the close, TWTR shareholders voted to approve the sale to Elon Musk, despite his desire to back out of the deal). BAC was also fined $5 million by FINRA for failing to disclose 7.42 million options positions between 2009 and 2020. In addition, the SEC charged VMW with misleading investors starting in 2019. In addition, an industry group that represents US Defense Contractors (LM, BA, RTX, GD, NOC, HON, LHX, TXT, CAE, HII, etc.), issued a report to Congress saying the Pentagon will need an additional $42 billion in the next fiscal year budget to make up for inflation. Finally, SBUX will be holding an investor day today at 10:30 eastern. Their new CEO is expected to address guidance, unionization of their workforce (one store at a time), and his vision for the company.

SNAP Case Study | Actual Trade

In Economic news, the EU announced that member countries can use $227.5 billion in unused pandemic recovery funds for loans to offset the energy crisis brought on by Russia’s invasion of Ukraine. Meanwhile, in the US, the coal industry (BTU, ARCH, AMR, CEIX, etc.) is in panic mode ahead of what could be a potential Friday strike by rail workers. (Coal shipments would stop dead in the event of a rail strike.) Other industries that will be massively impacted include Lumber (BCC, UFPI, EVA, WFG, etc.), Metals and Minerals (FCX, VALE, AA, BHP, RIO, TECK, CCJ, etc.), and Steel (GGB, MT, RS, CMC, etc.). However, some industries have already shut down rail shipping (due to the nature of their products and the fear of shipments being stuck in rail cars during a strike). These include Fertilizers (MOS, NTR, CF, CTVA, FMC, SMG, etc.) and Chemicals (LIN, SHW, DOW, ALB, APD, LYB, ECL, DD, CE, etc.).

In a good sign for markets, a new survey by BAC finds that investors are fleeing the stock market searching for safety on recession fear. The survey found that 52% of investors are already underweight stocks with a record high 62% saying they are overweight cash. This matches up with Refinitiv-Lipper data that showed that last week saw the heaviest outflow of funds from equity funds seen in a quarter. Since most money piles in and out when it is too late, this could indicate the markets are past the worst of the pullback.

After the close, ORCL posted a miss on both the revenue and earnings lines. The company blamed foreign currency sales (versus the strong dollar) for the EPS miss. So far this morning, CNM slightly missed on revenue while beating on earnings. CNM also raised their forward guidance.

Overnight, Asian markets were mixed but leaned to the green side. South Korea (+2.74%) was an outlier to the upside. However, India (+0.75%), Australia (+0.65%), and Taiwan (+0.59%) led the region higher in modest trading. In Europe, stocks are nearly green across the board at mid-day, also on modest moves. Only Portugal (-0.48%) is preventing the clean sweep. The FTSE (+0.35%), DAX (+0.71%), and CAC (+0.68%) are typical and are leading the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward another green start to the day (though still well ahead of the morning data). The DIA implies a +0.67% open, the SPY is implying a +0.71% open, and the QQQ implies a +0.70% open at this hour. 10-year bond yields are down significantly to 3.316% and Oil (WTI) is up more than 1.5% to $89.18/barrel in early trading.

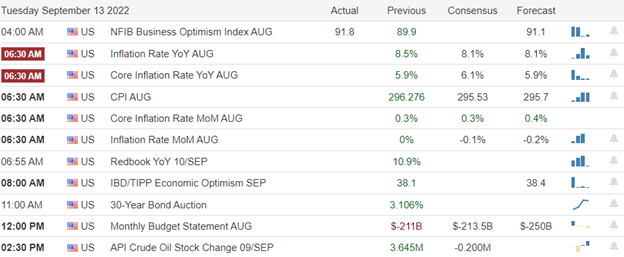

The major economic news events scheduled for Tuesday we get August CPI (the last major inflation data point prior to the Fed 9/20 meeting, at 8:30 am) and the August Federal Budget Balance (2 pm). The only major earnings report scheduled for the day is CNM before the open.

In economic news later this week, on Wednesday, August PPI and EIA Weekly Oil Inventories are reported. Then Thursday, we get August Import/Exports, Weekly Jobless Claims, NY Empire State Mfg. Index, Philly Fed Mfg. Index, August Retail Sales, August Industrial Production, July Business Inventories, and July Retail Inventories. Finally, on Friday, we get Michigan Consumer Sentiment. Friday is also Quadruple Witching

In terms of earnings later this week, on Wednesday, DOOO reports. Then Thursday ADBE reports. Finally, on Friday, there are no earnings reports scheduled.

The bulls continue their run this morning, as they have the momentum and (again ahead of the CPI data) are looking to gap us higher at the open. The schadenfreude of the Russian losses (men, material, and most importantly land) in Ukraine is also still a mood-lifting factor for traders as well. However, it is worth noting the resistance of the late August lows that will have to be dealt with after the opening bell. This CPI report may well be a large binary event, as some traders seem to have convinced themselves that a lower than forecast number will cause the Fed to hike only 0.50% instead of the 0.75% most expect. Make sure you are trading the reaction, not predicting the news. Either way, we know that zigs don’t last forever. So, there is a zag coming sometime in the not-too-distant future.

With that backdrop, we should note that all 3 major indices have broken their downtrends, but have yet to establish new uptrends (higher swing highs and higher swing lows). This is exactly the type of market that can become very choppy and volatile. So, while the bulls have control in the premarket, be prepared for a “gap and fail” or at least intraday reversals as the bulls and bears fight it out.

Remember that trading is our job, not a pastime or hobby. So, treat it that way. Do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: RIG, DVN, SQ, AMZN, NFLX, META, AAPL. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service