Good Earnings Continue on OpEx Day

Markets opened up mixed to get us started on Thursday. SPY gapped up 0.23%, DIA opened 0.01% lower, and QQQ gapped up 0.47%. From there, all three major index ETFs sold off for 30 minutes and then meandered sideways in waves until 1 p.m. At that point, SPY and QQQ diverged from DIA. SPY and QQQ made another leg lower for an hour, then rallied for an hour to get back to where they were at 1pm before selling off again the last hour. For its part, DIA just kept meandering sideways all day. This action gave us a Bearish Engulfing candle in the QQQ that gapped above and then failed its downtrend line, closing just above its T-line (8ema). The SPY gave us a Dark Cloud Cover that also gapped above and then failed its downtrend line, but remains above its T-line. Meanwhile, DIA printed a black-bodied Spinning Top Doji type candle.

On the day, eight of the 10 of the sectors were in the green with Utilities (+2.05%) way out in front leading the way higher. On the other side, Technology (-0.24%) and Consumer Cyclical (-0.23%) were the only sectors in the red and the laggards. At the same time, SPY fell 0.19%, DIA lost 0.26%, and QQQ dropped 0.70%. Meanwhile, VXX was just on the green side of flat at +0.16% to close at 43.62 while T2122 rose another 1.80%, closing at 87.56. On the bond side, 10-Year Bond yields dropped again to 4.615% and Oil (WTI) fell 1.69% to $78.69 per barrel. So, Thursday was an indecisive day that might have been signaling reversal of Wednesday’s pop. (Just remember that every candle signal needs confirmation.) This happened on well-below average volume in all three major index ETFs.

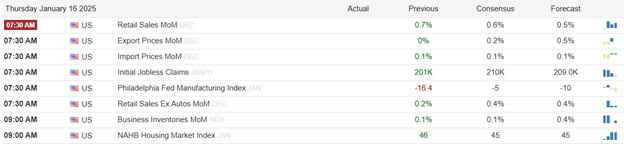

The major economic news Thursday included Weekly Initial Jobless Claims, which came in higher than expected at 217k (compared to a forecast of 210k and the prior week’s 203k). For ongoing, Weekly Continuing Jobless Claims were lower than was predicted at 1.859k (versus a 1,870k forecast and the previous week’s 1,877k value). At the same time, the December Export Price Index was higher anticipated at +0.3% (compared to the +0.2% forecast and November’s flat 0.0%). On the incoming side, the Dec. Import Price Index was +0.1% (versus a -0.1% forecast and in-line with November’s +0.1%). Meanwhile, the Philly Fed Mfg. Index was MUCH higher than expected at 43.3 (compared to a -5.0 forecast and December’s -10.9 reading). On the jobs side, Philly Fed Mfg. Employment was also stronger at 11.9 (versus December’s 4.8 value). At the same time, Dec. Core Retail Sales were up, but less that expected at +0.4% (compared to a forecast of +0.5% and November’s +0.2%). For the headline number, Dec. Retail Sales were lower than predicted at +0.4% (versus a forecast of +0.6% and November’s +0.8%). Later, November Business Inventories were up a tick as anticipated at +0.1% (compared to a +0.1% forecast and October’s flat 0.0% value). At the same time, Nov. Retail Inventories were up, but not as much as predicted at +0.5% (versus the +0.6% forecast, but up sharply from October’s +0.1% reading). Then, after the close, the Fed Balance Sheet showed a $20 billion decline from $6.854 trillion to $6.834 trillion.

In Fed news, on Thursday, Fed Governor Waller told CNBC that a rate cut cannot be ruled out for March. He said, “(Inflation) is getting close to what our 2% inflation target would be.” More broadly, Waller said, “If inflation data comes in as it has, I’d expect a cut in the first half of the year” … “If inflation is down and the labor market stays solid, you could think about restarting rate cuts several months from now…I don’t think March could be completely ruled out.” Later, Chicago Fed President Goolsbee told the Wall Street Journal, “I have over the last several months become more comfortable that this is a stabilization of the job market at a full-employment-like level, as opposed to something that was crashing through normal and turning into something worse.”

After the close, JBHT missed on both the revenue and earnings lines.

Overnight, Asian markets were mixed but leaned bullish with five exchanges in the red and seven in the green. New Zealand (+1.00%) led the gainers while Thailand (-0.88%) paced the losses. In Europe, the picture is greener with 13 of the 14 bourses above break-even at midday. The CAC (+1.04%), DAX (+0.98%), and FTSE (+1.29%) lead the region higher in early afternoon trade. Meanwhile, in the US, as of 7:40 a.m., Futures are pointing toward a modest move higher to start the day. The DIA implies a +0.38% open, SPY is implying a +0.34% open, and QQQ implies a +0.42% open at this hour. At the same time, 10-Year Bond yields are down to 4.582% and Oil (WTI) is just on the red side of flat at $78.61 per barrel in early trading.

The major economic news scheduled for Friday are limited to Dec. Building Permits and Dec. Housing Starts (both at 8:30 a.m.), Dec. Industrial Production (9:15 a.m.), and Nov. TIC Net Long-Term Transactions (4 p.m.). The major earnings reports scheduled for before the open include CFG, FAST, RF, SLB, STT, TFC, WBS, and WIT. Then, after the close, there are no reports scheduled.

So far this morning, CFG, RF, SLB, STT, TFC, and WBS have all reported beats on both the revenue and earnings lines. Meanwhile, WIT missed on revenue while coming in in-line on earnings. However, FAST missed on both the top and bottom lines.

With that background, the market tepidly bullish this morning. The three major index ETFs made a small gap higher to start the premarket. All three have managed to print small white body candles since the start of the early session, but there are no break-aways from the recent few days’ range. With that said, all three do remain above their T-line (8ema) and thus the short-term trend is bullish. It is worth noting that SPY has rejoined DIA (by virtue of the premarket gap higher) in being above their mid-term downtrend line which extends back to mid-December. So, the downtrends are broken in those two, but a new bullish trend (higher-highs and higher-lows) hasn’t been established. In the long-term all three are bullish. In terms of extension, none of the three are too extended above their T-line. For its part, T2122 is in its overbought range. So, both sides have room to work today, but the Bears have a bit more slack. In terms of the 10 Big Dogs, all 10 are in the green with NVDA (+0.85%) and AAPL (+0.82%) leading the way while INTC (+0.10%) lags. Related to volume, TSLA (+0.70%) is leading the way, having traded almost twice as much dollar-volume as NVDA, which has traded twice as much as AAPL. That said, it is a low-volume morning so far. (Remember this is Options Expiration day and Monday is a holiday.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Banks Clean Sweep and Jobless Claims Ahead

The big banks and especially CPI delivered for the Bulls on Wednesday. SPY gapped up 1.39%, DIA gapped up 1.48%, and QQQ gapped up 1.57%. From there, all three major index ETFs saw a follow-through rally for about 40-60 minutes, an hour of selloff, and then a rally that lasted the rest of the day. Only profit-taking the last 30 minutes prevented the market from going out on the highs. This action gave us gap-up, white-body candles in all three major index ETFs. SPY and QQQ had larger bodies, but all three were some form of a Spinning Top. All three are now above their T-line (8ema). However, it is worth noting that SPY and QQQ retested and back down from their Bear downtrend line that extends back to the all-time highs in mid-December.

On the day, all 10 of the sectors were in the green with Financial Services (+2.56%) and Technology (+2.26%) leading the way higher. On the other side, Consumer Defensive (+0.03%) was by far the laggard. At the same time, SPY gained 1.82%, DIA gained 1.67%, and QQQ gained 2.26%. Meanwhile, VXX plummeted 8.16% to close at 43.55 while T2122 popped up into its overbought range, closing at 86.01. On the bond side, 10-Year Bond yields plummeted to 4.653% and Oil (WTI) spiked 3.94% to $80.56 per barrel. So, after the strong gap higher Wednesday, the Bulls won the tug of war, but it was not decisive. In other words, there was plenty of wick on both ends of all three major index ETF candles. This happened on slightly above-average volume in the SPY, DIA, and QQQ.

The major economic news Wednesday included December Month-on-Month Core CPI, which came in a tick better than expected at +0.2% (compared to a +0.3% forecast and November value). On the annualized basis, December Year-on-Year Core CPI was also a tick better than expected at +3.2% (versus a +3.3% forecast and November reading). For the headline numbers, December Month-on-Month was up a tick as predicted at +0.4% (compared to a +0.4% forecast and a +0.3% November number). On an annualized basis, December Year-on-Year CPI was as anticipated at +2.9% (versus a +2.9% forecast but two ticks higher than November’s +2.7% value). At the same time, the NY Empire State Mfg. Index was way down to -12.60 (compared to a +2.70 forecast and a December +2.10 reading). Later, EIA Weekly Crude Oil Inventories showed a 1.962-million-barrel drawdown (less than the forecasted 3.500-million-barrel drawdown, but higher than the prior week’s 0.959-million-barrel draw.

In Fed news, on Wednesday, Richmond Fed President Barkin told reporters that the December CPI “continues the story we have been on, which is that inflation is coming down towards target.” Barkin continued, “The ‘economy weakening’ argument seems to be decaying … You keep seeing good numbers on retail sales, unemployment, and the like Demand, you are hearing, is good, solid, fine.” Separately, NY Fed President Williams said, “The process of disinflation remains in train.” He went on, “Monetary policy is well positioned to keep the risks to our goals in balance.” However, he also expressed caution based on indecision over the new administration’s policies. He said, “The economic outlook remains highly uncertain, especially around potential fiscal, trade, immigration, and regulatory policies. Therefore, our decisions on future monetary policy actions will continue to be based on the totality of the data, the evolution of the economic outlook, and the risks to achieving our dual mandate goals.” Elsewhere, Minneapolis Fed President Kashkari commented that “Tariffs themselves don’t cause inflation, but retaliation does and the whole issue is more complicated.” Finally, Chicago Fed President Goolsbee said he continues to see progress on inflation and that he is optimistic for a soft landing in 2025. However, he also said the CPI report was both somewhat encouraging and somewhat discouraging in equal measure. He continues to see continued progress on inflation, but he is also “wary of the seasonal pattern of inflation.”

After the close, CNXC and FUL both reported a miss on revenue while also beating on earnings. Later, SNV reported beats on both the top and bottom lines.

Overnight, Asian markets were mostly green with 10 of the 12 exchanges above break-even. Malaysia (-0.42%) was the only appreciable loser. Meanwhile, Taiwan (+2.27%), Australian (+1.38%), and South Korea and Hon Kong (both +1.23%) led the region higher. In Europe, we see a similar picture with 11 of 14 bourses showing green at midday. The CAC (+2.00%), DAX (+0.26%), and FTSE (+0.60%) lead the region higher in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a mixed start to the morning. DIA implies a -0.18% open, the SPY is implying a +0.15% open, and QQQ implies a +0.34% open at this hour. At the same time, 10-Year Bond yields are back up to 4.68% and Oil (WTI) has pulled back 0.94% to $79.28 per barrel in early trading.

The major economic news scheduled for Thursday includes Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. Export Price Index, Dec. Import Price Index, Philly Fed Mfg. Index, Philly Fed Mfg. Employment, Dec. Core Retail Sales, and Dec. Retail Sales (all at 8:30 a.m.), November Business Inventories and Nov. Retail Inventories (both at 10 a.m.), and the Fed Balance Sheet (4:30- p.m.). Fed member Williams also speaks again at 11 a.m. The major earnings reports scheduled for before the open include BAC, FHN, GS, INFY, MTB, MS, PNC, TSM, USB, and UNH. Then, after the close, JBHT reports.

In economic news later this week, on Friday, Dec. Building Permits, Dec. Housing Starts, Dec. Industrial Production, and Nov. TIC Net Long-Term Transactions are reported.

In terms of earnings reports later this week, Friday, CFG, FAST, RF, SLB, STT, TFC, WBS, and WIT report.

So far this morning, BAC, FHN, INFY, MTB, MS, PNC, TSM, and USB all reported beats on both the revenue and earnings lines. Meanwhile, UNH missed on revenue while beating on earnings.

With that background, the market seems undecided this morning. All three major index ETFs gapped higher to start the premarket. However, all three have also printed black-body candles since that point, with DIA being the only one with significant wicks (and the larges of those is to the upside). This indicates the market is uncertain that its gap up in the early session was warranted. With that said, all three do remain above their T-line (8ema) and thus the short-term trend is bullish. It is worth noting that SPY and QQQ joined DIA (by virtue of their premarket gap higher) in being above their mid-term downtrend line which extends back to mid-December. So, the downtrends are broken but a new bullish trend (higher-highs and higher-lows) hasn’t been established. In the long-term all three are bullish. In terms of extension, none of the three are too extended above their T-line, but they are starting to push things. For its part, T2122 is now in the overbought range. So, both sides have room to work today. In terms of the 10 Big Dogs, seven of the 10 are in the green with NFLX (+1.29%) leading the way while META (-1.54%) lags. Related to volume, NVDA (+0.92%) is leading TSLA (-0.96%) by about 25% with TSLA having traded five times as much as the next closest ticker.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Strong Bank Earnings

S&P 500 futures climbed on Thursday, following the benchmark index’s best performance since November, driven by a favorable inflation report and strong bank earnings. Investors are eagerly awaiting further economic insights, with the December retail sales report anticipated to show a 0.5% increase, slightly down from November’s 0.7% rise, according to Dow Jones estimates. Additionally, weekly jobless claims are expected to be released. Earnings reports from Morgan Stanley and Bank of America are also on the docket, concluding the earnings season for major banks.

European markets experienced a positive surge on Thursday, driven by impressive performances in the luxury and technology sectors. Luxury stocks soared, particularly those of Cartier, which reported strong results. This uplift was mirrored in the shares of France’s LVMH, Kering, and Christian Dior, all of which saw gains of around 8%. Retailers such as Moncler, Burberry, Swatch, and Hermes also performed well, clustering at the top of the Stoxx index. Technology stocks rose by 1.87%, with chip companies like ASM International and Be Semiconductor benefiting from better-than-expected earnings from Taiwan Semiconductor Manufacturing Company.

Asia-Pacific markets saw a positive trend on Thursday, with most indices recording gains. Korea’s central bank maintained its benchmark interest rate at 3%, defying expectations. This decision seemed to bolster investor confidence, as the Kospi rose by 1.23% and the Kosdaq by 1.77%. The Korean won, however, weakened slightly, trading at 1,456.91 against the US dollar. In Japan, the Nikkei 225 edged up by 0.33%, while the Topix dipped marginally by 0.09%. Hong Kong’s Hang Seng index climbed 1.08%, and China’s CSI 300 saw a modest increase of 0.11%. Meanwhile, Australia’s S&P/ASX 200 advanced by 1.38%, despite a slight uptick in the unemployment rate to 4% in December from 3.9% in November.

Economic Calendar

Earnings Calendar

Notable reports for Thursday before the bell include BAC, FHN, IIIN, MTB, MS, PNC, UNH, & USB. After the bell reports include OZK, & JBHT.

News & Technicals’

British oil major BP announced on Thursday its plan to cut thousands of jobs as part of a significant cost-cutting initiative. The company informed staff that approximately 4,700 roles would be impacted by the proposed changes, constituting a large portion of this year’s anticipated reductions. Additionally, BP plans to reduce its contractor numbers by 3,000. These measures aim to lower costs, following CEO Murray Auchincloss’s statement last year that BP intends to achieve at least $2 billion in cash savings by the end of 2026.

Target raised its fourth-quarter sales forecast on Thursday, attributing the increase to a surge in holiday shopping both in-store and online, especially during major discount days. The retailer now expects comparable sales to grow by about 1.5%, an improvement from its previous projection of flat growth. This metric includes sales from Target’s website and stores open for at least 13 months. Despite the positive sales outlook, Target did not revise its profit forecast, suggesting that the boost in sales was driven by promotional deals. The company anticipates fourth-quarter earnings per share to range between $1.85 and $2.45.

The Biden administration announced an executive order on cybersecurity on Thursday, introducing new standards for companies selling to the U.S. government and requiring greater transparency from software providers. This move follows several high-profile ransomware attacks on entities like Change Healthcare, Colonial Pipeline, and Ascension health care system. Additionally, Microsoft revealed in 2023 that Chinese attackers had breached U.S. government officials’ email accounts, leading to a critical federal report and subsequent changes at the company. Under the new order, software vendors must prove their development practices are secure, with evidence to be posted on a government website for the benefit of all software users, as stated by Neuberger.

Although we have seen some strong big bank earnings, the regional banks appear to be struggling a bit this morning. Continue to expect wild volatility and remember we have three day weekend just around the corner with the inauguration that could easily create some bumpiness due tot the big changes that are expected.

Trade Wisely,

Doug

Banks Start Earnings Season Strong, CPI on Deck

On Tuesday markets gapped higher on better-than-expected PPI numbers. The SPY gapped up 0.49%, DIA gapped up 0.49%, and QQQ gapped up 0.63%. From there, DIA meandered back-and-forth across its opening gap all day, ending up just above its open. For their part, SPY and QQQ gave us a similar motion, but did it with a slight bearish trend. This produced indecisive candles in all three major index ETFs. SPY printed a black-bodied Hammer-type candle that did not quite make it up to retest its T-line (8ema) from below. QQQ printed a larger-body, black-bodied Hammer-type candle that similarly did not quite make it up to retest the T-line. Meanwhile, DIA gave us a white-bodied Doji-type candle that retested and closed just above its T-line.

On the day Tuesday, nine of the 10 sectors were in the green with Financial Services (+1.59%), Industrials (+1.34%), and Basic Materials (+1.34%) leading the way higher. On the other side, Healthcare (-1.13%) was by far the laggard. At the same time, SPY gained 0.14%, DIA gained 0.52%, and QQQ lost 0.09%. At the same time, VXX fell another 2.27% to close at 47.42 while T2122 popped up to the top of its mid-range at 76.00. On the bond side, 10-Year Bond yields rose again to 4.792% and Oil (WTI) fell 1.09% to $77.96 per barrel. So, after the gap higher, Tuesday was a volatile day that sold off and rallied over and over. This choppy day really did nothing to change the trends and can be written off to noise within the downtrend. This happened on average volume in the SPY and QQQ but less-than-average volume in DIA.

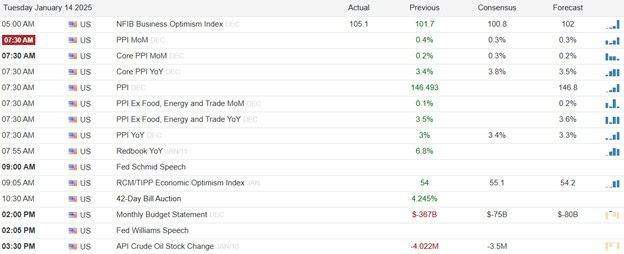

The major economic news Tuesday included Dec. Core PPI, which came in flat at 0.0% (compared to a forecast +0.3% and a November reading of +0.2%). On the headline side, December PPI was +0.2% (well below the forecast and November +0.4% value). Later, the December Federal Budget Balance came in at -$87.0 billion (compared to a forecasted -$80.0 billion but far better than November’s -$367.0 billion number). After the close, the API Weekly Crude Oil Stocks report showed a smaller than anticipated drawdown of 2.600 million barrels (versus a 3.500-million-barrel draw that was forecast and the previous week’s -4.022-million-barrel reading).

In Fed news, on Tuesday New York Fed President Williams told an audience that housing affordability was the main concern facing the NY Fed District. (He did not comment on Monetary Policy.) Meanwhile, Kansas City Fed President Schmid told a different audience that it is too early to tell what policies the new Trump administration will enact or how they will impact the US economy. Schmid went on to say he feels the economy is near the point where it doesn’t need either restrictive or expansionist Fed policy.

Overnight, Asian markets were mostly red. Taiwan (-1.24%) and Shenzhen (-1.03%) paced the losses while Thailand (+0.96%) was by far the leader among gainers. Yet in Europe we seen green across the board at midday. The CAC (+0.72%), DAX (+0.92%) and FTSE (+0.79%) lead the region higher in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a move higher to start the day. DIA implies a +0.53% open, SPY is implying a +0.33% open, and QQQ implies a +0.33% open at this hour. At the same time, 10-Year Bond Yields have fallen to 4.757% and Oil (WTI) is up half a percent to $77.89 per barrel in early trading.

The major economic news scheduled for Wednesday includes Dec. Core CPI, Dec. CPI, and NY Empire State Mfg. Index (all at 8:30 a.m.), EIA Weekly Crude Oil Inventories (10:30 a.m.), and Fed Beige Book (2 p.m.). We also hear from Fed members Kashkari (10 a.m.) and Williams (11 a.m.). The major earnings reports scheduled for before the open are limited to BK, BLK, C, GS, JPM, and WFC. Then, after the close, CNXC, FUL, and SNV report.

In economic news later this week, on Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. Export Price Index, Dec. Import Price Index, Philly Fed Mfg. Index, Philly Fed Mfg. Employment, Dec. Core Retail Sales, Dec. Retail Sales, Nov. Business Inventories, Nov. Retail Inventories, and the Fed Balance Sheet. Fed member Williams also speaks again. Finally, on Friday, Dec. Building Permits, Dec. Housing Starts, Dec. Industrial Production, and Nov. TIC Net Long-Term Transactions are reported.

In terms of earnings reports later this week, Thursday, we hear from BAC, FHN, GS, INFY, MTB, MS, PNC, TSM, USB, UNH, and JBHT. Finally, on Friday, CFG, FAST, RF, SLB, STT, TFC, WBS, and WIT report.

So far this morning, BK, BLK, GS, JPM, and WFC have all reported beats on both the revenue and earnings lines. (C does not report until 8 a.m.)

With that background, the market seems modestly bullish so far in the premarket. All three major index ETFs made a modest gap higher and have followed-through with small white-body candles that are mostly body (small wicks). It is worth noting that only DIA has stayed above its T-line (8ema), which is about where it closed Tuesday. So, two of the three remain below their T-line (8ema). This means the short-term trend remains bearish. The same is true in the mid-term where only DIA is challenging its downtrend line. However, in the long-term, all three are above their uptrend line (DIA just climbing back above). So, in the long-term the market remains Bullish. In terms of extension, all three of the major index ETFs are now back close to their T-line and, for its part, T2122 is at the top part of its mid-range. So, both sides have room to work but the Bears have slightly more slack to work with today. In terms of the 10 Big Dogs, all 10 are in the green with TSLA (+1.09%) leading the way while INTC (+0.05%) is the laggard. Related to volume, TSLA and NVDA (+0.36%) are neck-and-neck on what is a light-volume premarket session. The next closest ticker has traded 10 times less dollar-volume than those two.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

PPI on Deck as Musk in Talks to Buy TikTok

Markets gapped lower to start the week on Monday. SPY gapped down 0.82%, DIA opened 0.14% lower, and QQQ gapped down 1.18%. From that point, all three major index ETFs put in a choppy all-day rally. The only difference between the three was the size of the gap down they were trying to overcome. This action gave us gap down, large-body, white candles in all three. QQQ did not quite make it back up inside the body of Friday’s candle, but did close inside Friday’s lower wick. SYP made back up inside Friday’s candle body. However, DIA won the prize, printing a Bullish Piercing Arrow signal by closing more than half way up Friday’s candle body after gapping down below Friday’s low. This all happened on average volume in SPY and QQQ and below-average volume in DIA.

On the day Monday, eight of the 10 sectors were in the green with Energy (+1.25%) and Basic Materials (+1.18%) out front leading the market higher. On the other side, Technology -0.86%) and Utilities (-0.78%) were the laggards. At the same time, SPY gained 0.16%, DIA gained 0.87%, and QQQ lost 0.32%. At the same time, VXX fell 0.78% to close at 48.52 while T2122 popped up out of its oversold territory to the lower half of its mid-range at 31.38. On the bond side, 10-Year Bond yields rose again to 4.788% and Oil (WTI) jumped another 2.76% to $78.68 per barrel. So, after the gap down, Monday was really the Bulls’ day. It was choppy, but the trend was bullish from the open, and it was just a quested of whether the gap could be overcome.

The major economic news Monday was limited to December NY Fed 1-Year Consumer Inflation Expectations, which came in flat at +3.0% (compared to November’s +3.0% reading).

After the close, KBH reported beats on both the revenue and earnings lines.

Overnight, Asian markets were mixed, but leaned toward the green side. Shenzhen (+3.77%), Shanghai (+2.54%), and Hong Kong (+1.83%) led the gains perhaps on the release of Chinese Trade data or follow-up on the US’s all-day rally following its gap down from Monday. Regardless, Japan (-1.83%) was the big loser on the day in that region. In Europe, the market is decidedly bullish at midday with 13 of 14 exchanges showing green. The CAC (+0.84%), DAX (+0.65%), and laggard FTSE (-0.11%) lead the region in early afternoon trade. Meanwhile, in the US, as of 7:30 a.m., Futures are pointing toward a modest green start to the day. The DIA implies a +0.13%) open, the SPY is implying a +0.14% open, and the QQQ implies a +0.15% open at this hour. At the same time, 10-Year Bond yields sit at 4.79% and Oil (WTI) is down four-tenths of a percent to $78.50 per barrel in early trading.

The major economic news scheduled for Tuesday includes Dec. Core PPI and Dec. PPI (both at 8:30 a.m.), Dec. Federal Budget Balance (2 p.m.), and API Weekly Crude Oil Stocks (4:30 p.m.). Fed member Williams also speaks at 3:05 p.m. There are no major earnings reports scheduled for either before the open or after the close on Tuesday.

In economic news later this week, on Wednesday, Dec. Core CPI, Dec. CPI, NY Empire State Mfg. Index, EIA Weekly Crude Oil Inventories, and Fed Beige Book are reported. We also hear from Fed members Kashkari and Williams. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. Export Price Index, Dec. Import Price Index, Philly Fed Mfg. Index, Philly Fed Mfg. Employment, Dec. Core Retail Sales, Dec. Retail Sales, Nov. Business Inventories, Nov. Retail Inventories, and the Fed Balance Sheet. Fed member Williams also speaks again. Finally, on Friday, Dec. Building Permits, Dec. Housing Starts, Dec. Industrial Production, and Nov. TIC Net Long-Term Transactions are reported.

In terms of earnings reports later this week, Wednesday, BK, BLK, C, JPM, WFC, CNXC, FUL, and SNV report. Then Thursday, we hear from BAC, FHN, GS, INFY, MTB, MS, PNC, TSM, USB, UNH, and JBHT. Finally, on Friday, CFG, FAST, RF, SLB, STT, TFC, WBS, and WIT report.

With that background, the market seems undecided early. All three major index ETFs gapped up to start the premarket, but have shown indecision. DIA has printed a black body, tiny hammer that gapped up to its T-line and has, so far, backed off, but is also up off its premarket lows. SPY has given us a tiny black-body, Spinning Top after its gap higher in the early session. Meanwhile, QQQ gapped higher, but has printed a black candle since then which is just now up off its lows. All three remain below their T-line (8ema). So, the short-term trend is bearish. The same is true in the mid-term. However, in the long-term, only DIA has broken its uptrend line. So, on balance, long-term the market remains Bullish. In terms of extension, all three of the major index ETFs are now back closer to their T-line given the premarket gap. For its part, T2122 is in the lower half of its mid-range. So, both sides have room to work but the Bulls have slightly more slack to work with today. In terms of the 10 Big Dogs, nine of the 10 are in the green with TSLA +1.41%) leading the way while META (-0.55%) is the laggard. Related to volume, TSLA is back as the early leader, having traded about $600 million so far, which is 1.5 times as much as NVDA (+1.10%) and NVDA has traded 6.5 times as much as the next most liquid stock.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Key Inflation Reports

US Stock futures rose as investors prepared for the first of two, key inflation reports this week. The producer price index (PPI), which tracks wholesale inflation, is scheduled for release at 8:30 a.m. ET. Economists surveyed by Dow Jones expect the headline PPI to have increased by 0.4%, with the core PPI, excluding food and energy, anticipated to rise by 0.3%. In the earnings arena, major banks are set to kick off the fourth-quarter earnings season. JPMorgan Chase, Citigroup, Goldman Sachs, and Wells Fargo will report their results on Wednesday, followed by Morgan Stanley and Bank of America on Thursday.

European markets traded higher, reversing the recent negative sentiment in the region. However, investors remain cautious, closely monitoring borrowing costs for core European economies as bond yields stay elevated. The oil and gas sectors led the losses, declining by 0.7% after BP announced that its fourth-quarter profit would be impacted by up to $300 million due to weakening refinery margins. Retail stocks also faced challenges, with JD Sports plummeting to the bottom of the Stoxx 600 after lowering its profit guidance.

Asia-Pacific markets experienced a general upward trend, with notable gains in several key indices. Hong Kong’s Hang Seng index surged by 1.9%, and mainland China’s CSI 300 saw an impressive rise of 2.63%. In contrast, Japan’s markets were the exception, as the Nikkei 225 fell by 1.83% and the Topix decreased by 1.16%. South Korea’s Kospi closed with a modest increase of 0.31%, while the small-cap Kosdaq performed better, adding 1.39%. Australia’s S&P/ASX 200 also ended the day positively, up by 0.48%. Meanwhile, investors are keeping a close eye on India’s rupee, which has weakened to a record low against the U.S. dollar.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include PGR. After the bell reports include APLD, & CVGW.

News & Technicals’

According to a report by Bloomberg News on Monday, the Chinese government is considering a plan for Elon Musk to acquire TikTok’s U.S. operations to prevent the app from being effectively banned. This contingency plan is one of several options China is exploring as the U.S. Supreme Court deliberates on whether to uphold a law requiring ByteDance, TikTok’s China-based parent company, to divest its U.S. business by January 19. If the deadline passes without compliance, third-party Internet service providers would face penalties for supporting TikTok’s operations in the U.S. Under the proposed plan, Musk would manage both X, which he currently owns, and TikTok’s U.S. business. However, Chinese officials have not yet made a final decision on whether to proceed with this plan.

Two Robinhood broker-dealers, Robinhood Securities LLC and Robinhood Financial LLC, have agreed to pay a combined $45 million in penalties to settle administrative charges by the Securities and Exchange Commission (SEC). The SEC found that the firms violated over ten securities law provisions related to their brokerage operations. These violations included failing to report suspicious trading promptly, not implementing adequate identity theft protections, and inadequately addressing unauthorized access to their computer systems. Additionally, Robinhood Securities was cited for failing to provide complete and accurate securities trading information, known as blue sheet data, to the SEC for more than five years.

A global sell-off in bond markets is intensifying, raising concerns about government finances and the potential for higher borrowing costs for consumers and businesses worldwide. Bond yields have been climbing globally, with the U.S. 10-year Treasury yield reaching a new 14-month high of 4.799% on Monday. In the UK, 30-year gilt yields are at their highest since 1998, and the 10-year yield has hit levels not seen since 2008. Japan, which has been working to normalize its monetary policy after ending its negative interest rates regime last year, saw its 10-year government bond yield rise above 1%, the highest in 13 years, on Tuesday. In the Asia-Pacific region, India’s 10-year bond yields rose the most in over a month on Monday, nearing two-month highs at 6.846%. Similarly, yields on New Zealand and Australia’s 10-year benchmark government bonds are also near two-month highs. Meanwhile, China’s 10-year bond yield dropped to a record low this month, leading the central bank to suspend its government bond purchases last Friday.

On Tuesday, Los Angeles firefighters prepared for intense winds that could exacerbate two massive wildfires, which have already claimed two dozen lives, destroyed entire neighborhoods, and burned an area equivalent to the size of Washington, D.C. Meteorologist David Roth from the National Weather Service’s Weather Prediction Center warned of potential hurricane-force winds reaching 75 mph (120 kph) from early Tuesday, with gusts between 50-70 mph expected through Wednesday. Over 8,500 firefighters battled the blazes from both the air and ground, successfully preventing the fires from spreading overnight. Los Angeles City Fire Chief Kristin Crowley cautioned residents, stating, “This setup is about as bad as it gets. We are not in the clear.”

With the beginning of earnings season tomorrow and the combined influence of the key inflation reports, PPI today and CPI plan for significant price volatility. Today also keep a close eye on the bond yields as they provide some strong clues to overall market direction.

Trade Wisely,

Doug

CPI, PPI, and Earnings Ahead This Week

The major index ETFs gapped lower at the open in response to December Payrolls. SPY gapped down 0.61%, DIA gapped down 0.43%, and QQQ gapped down 0.74%. From there, it was a volatile roller-coaster ride in all three with morning follow-through selloff into noon, a rally back toward the opening level until 2 pm. and the another sell cycle into the close. This action gave us gap-down, black-body candles in all three major index ETFs. SPY seemed to bounce up off its trendline dating back to October 2023. DIA broke out of its recent consolidation dating back to December. This took place on roughly average volume in all three.

On the day, Friday, nine of the 10 sectors were in the red with Financial Services (-2.50%) was out front leading the market lower. On the other side, Energy (+0.25%) was the only sector in the green and 1.20% stronger than the rest of the sectors. At the same time, SPY lost 1.53%, DIA lost 1.60%, and QQQ lost 1.57%. At the same time, VXX jumped 6.71% higher to 49.45 while T2122 fell back to the lower half of its oversold territory to 8.86. On the bond side, 10-Year Bond yields popped to 4.763% and Oil (WTI) jumped 3.64% to $76.61 per barrel. So, Friday was the Bears Day. The December Payroll Data set the tone and the Bulls never really had an answer.

On the day Wednesday, six of the 10 sectors were in the green as Basic Materials (+0.32%) and Industrials (+0.22%) led the gainers. On the other side, Technology (-0.37%) and Utilities (-0.32%) paced the losses. Meanwhile, SPY gained 0.15%, DIA gained 0.19%, and QQQ gained 0.02%. At the same time, VXX was on the red side of flat at 46.34 while T2122 rose, but remained in the oversold territory at 18.91. On the bond side, 10-Year Bond yields were at 4.693% and Oil (WTI) fell 1.24% to $73.33 per barrel. So, Wednesday was an indecisive day. Markets all opened flat and then went back-and-forth from green to red and back to green all day long.

The major economic news Friday included December Month-on-Month Average Hourly Earnings, which came in as expected at +0.3% (compared to a +0.3% forecast, but down a tick from November’s +0.4%). On an annualized basis, December Year-on-Year Average Hourly Earnings were down to +3.9% (versus a forecast and November value of +4.0%). At the same time, Dec. Nonfarm Payrolls were MUCH stronger than expected at +256k (compared to a +164k forecast and a November reading of +212k). On the private side, Dec. Private Nonfarm Payrolls were also MCU stronger than was predicted at +223k (versus a +135k forecast and a +182k November value). We also had a Dec. Participation Rate that remained stable at 62.5%. Altogether, this gave us a Dec. Unemployment Rate that was down a tick to 4.1% (compared to a forecast and November reading of 4.2%). Later, Michigan Consumer Sentiment came in below the predicted number at 73.2 (versus a 74.0 forecast and December value). Looking ahead Michigan Consumer Expectations fell to 70.2 (compared to a 73.3 December reading). On the inflation side, Michigan 1-Year Inflation Expectations popped to 3.3% (versus a 2.8% forecast and Dec. value). Further out, Michigan 5-Year Inflation Expectations were also 3.3% (compared to a 3.0% forecast and December reading). Then, after the close, the Fed’s Balance Sheet showed a $2 billion increase to $6.854 trillion.

After the close, WDFC reported a huge miss on revenue while also beating significantly on earnings.

Overnight, Asian markets were red across the board. Taiwan (-2.28%) was by far the biggest loser, followed by India (-1.47%) and Australia (-1.23%). However, losses were wide and significant. In Europe, a very similar picture is taking shape at midday with just one of the 14 bourses above break-even. The CAC (-0.71%), DAX (-0.59%), and FTSE (-0.30%) lead the region lower. Meanwhile, in the US, Futures are pointing toward a gap down to start the day. The DIA implies a -0.20% open, SPY is implying a -0.70% open, and QQQ implies a -1.06% open at this hour. At the same time, 10-Year Bond Yields are up at 4.766% while Oil (WTI) is spiking another 2.22% to $78.26 per barrel in early trading.

The major economic news scheduled for Monday is limited to December NY Fed 1-Year Consumer Inflation Expectations (11 a.m.) and Dec. Federal Budget Balance (2 p.m.). There are no major earnings reports scheduled before the open. However, after the market close, KBH reports.

In economic news later this week, on Tuesday, we get Dec. Core PPI, Dec. PPI, and API Weekly Crude Oil Stocks. Fed member Williams speaks at 3:05 p.m. Then Wednesday, Dec. Core CPI, Dec. CPI, NY Empire State Mfg. Index, EIA Weekly Crude Oil Inventories, and Fed Beige Book are reported. We also hear from Fed members Kashkari and Williams. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, Dec. Export Price Index, Dec. Import Price Index, Philly Fed Mfg. Index, Philly Fed Mfg. Employment, Dec. Core Retail Sales, Dec. Retail Sales, Nov. Business Inventories, Nov. Retail Inventories, and the Fed Balance Sheet. Fed member Williams also speaks again. Finally, on Friday, Dec. Building Permits, Dec. Housing Starts, Dec. Industrial Production, and Nov. TIC Net Long-Term Transactions are reported.

In terms of earnings reports later this week, there are no earnings reported scheduled for Tuesday. On Wednesday, BK, BLK, C, JPM, WFC, CNXC, FUL, and SNV report. Then Thursday, we hear from BAC, FHN, GS, INFY, MTB, MS, PNC, TSM, USB, UNH, and JBHT. Finally, on Friday, CFG, FAST, RF, SLB, STT, TFC, WBS, and WIT report.

With that background, the Bears gapped all three major index ETFs lower to start the premarket. SPY and QQQ followed-through to the downside before joining DIA in a rebound rally. This leaves the SPY as a black Hammer, QQQ as a white Hammer, and DIA as a white large-body, small-wick candle. However, all three are well below Friday’s close. All three remain well below their T-line (8ema). So, the short-term trend is strongly bearish. The same is true in the mid-term. However, in the long-term, only DIA has broken its uptrend line. So, on balance, long-term the market remains Bullish. In terms of extension, all three of the major index ETFs are now extended too far below their T-line and T2122 sits in the lower half of its oversold area. So, the Bulls have room to run and the market is in need of at least a relief rally. (Still, that does not mean it will come before traders go broke betting on a reversal too soon.) In terms of the 10 Big Dogs, all 10 are in the red with TSLA (-2.96%) being the worst off and META (-0.39%) holding up best. For a fourth-straight day, NVDA (-2.73%) leads in dollar-volume traded by about 35% over TSLA (which itself has traded nine times as much as the next most liquid stock).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stock Futures Declined

US stock futures declined on Monday as investors continued to offload shares of key technology companies that have been driving the recent bull market. This sell-off has been fueled by a surge in bond yields, particularly the 10-year Treasury yield, which reached its highest level since late 2023. Investors are anticipating the start of the fourth-quarter earnings season, hoping it will bring some stability to the volatile markets. Several major banks, including Citigroup, Goldman Sachs, and JPMorgan Chase, are scheduled to report their earnings on Wednesday, while Morgan Stanley and Bank of America will release their results on Thursday.

The pan-European Stoxx 600 index traded lower this morning, with most sectors experiencing declines. Investors in the region are closely monitoring eurozone and U.K. government bond yields, which climbed to fresh multi-month highs last week. Market focus will also shift to the U.S. December consumer price index release on Wednesday morning, following the release of the December producer price index report on Tuesday. These key economic data points will provide further insights into the trajectory of inflation and potential monetary policy decisions.

Asia-Pacific markets experienced a downturn on Monday. Mainland China’s CSI 300 index declined by 0.27%, likely influenced by a record low for China’s 10-year bond yield this month. Hong Kong’s Hang Seng Index also saw a decrease of 0.73%. In India, the Nifty 50 and BSE Sensex indices fell by 0.95% and 0.80%, respectively, ahead of the anticipated release of inflation data later in the day. South Korea’s Kospi and Kosdaq indices closed lower, with losses of 1.04% and 1.35%, respectively. Australia’s S&P/ASX 200 index also experienced a decline of 1.23%. Japan’s markets were closed for a holiday.

Economic Calendar

Earnings Calendar

Notable reports for Monday before the bell we have no noteworthy reports. After the bell reports include KBH.

News & Technicals’

U.S. Treasury yields climbed higher on Monday as investors braced for key inflation data releases. The 10-year Treasury yield, which had surged to its highest level since November 2023 following a stronger-than-expected jobs report on Friday, continued to rise by one basis point to 4.784%. Similarly, the 2-year Treasury yield saw an increase of three basis points, reaching 4.421%. This upward trend in U.S. Treasury yields aligns with a broader global rise in bond yields, reflecting a growing expectation among traders that interest rate cuts will occur at a slower pace this year. This cautious outlook is primarily driven by the anticipation that the U.S. Federal Reserve will proceed carefully, navigating a complex economic landscape characterized by both potential economic strength and lingering uncertainties.

The U.S. government announced new restrictions on the export of artificial intelligence chips and technology, aiming to maintain American dominance in AI by controlling its global spread. These regulations will limit AI chip exports to most countries while granting unrestricted access to U.S. AI technology for close allies. The measures, designed to prevent China, Russia, Iran, and North Korea from accessing advanced computing power, will also cap the number of AI chips that can be exported to other nations. This move reflects a broader strategy to concentrate advanced AI development within the U.S. and its allies.

In a recent podcast interview, Meta CEO Mark Zuckerberg criticized Apple for its perceived lack of innovation and the imposition of “random rules” on its platform. While acknowledging the iPhone’s significant impact in making smartphones ubiquitous, Zuckerberg expressed frustration with Apple’s current approach. He argued that Apple has not introduced any groundbreaking innovations since the iPhone’s initial release, essentially “sitting on it” for two decades. Furthermore, Zuckerberg criticized Apple for implementing arbitrary rules that hinder competition and innovation within the tech ecosystem

Blue Origin was forced to abort the inaugural launch of its New Glenn rocket on Monday due to a last-minute technical issue with the vehicle. This setback significantly impacts Blue Origin’s efforts to compete with SpaceX in the satellite launch market. The company decided to stand down the launch attempt to address the identified subsystem issue, which would have exceeded the available launch window. Blue Origin is now evaluating potential dates for the next launch attempt. The ambitious mission aimed to achieve a significant milestone by landing the first-stage booster on the offshore ship Jacklyn in the Atlantic Ocean for future reuse while propelling the second stage into orbit.

Although stock futures declined this morning, we are looking at a substantial oversold situation in the short term. Start watching for clues of a modest relief rally but keep in mind all the uncertainty we face in the days ahead that anything is possible. Expect significant volatility throughout the week.

Trade Wisely,

Doug

December Payrolls Data and Michigan Surveys

Markets opened flat Wednesday and then spent the day meandering back-and-forth across the opening level. SPY opened 0.02% higher, DIA opened dead flat, and QQQ opened down 0.01%. As mentioned, all three major index ETFs rode a roller coaster all day with peaks in the late morning and mid-afternoon as well as troughs during the first 90 minutes and early afternoon. This action gave us white-bodied, indecisive, Doji or small-body Spinning Top candles in all three. SPY may have just retested its T-line (8ema) from below (failing that test) while the DIA and QQQ did not quite retest that level. This happened on below-average volume in all three major index ETFs (and well below average volume in the DIA).

The major economic news Wednesday included ADP December Nonfarm Employment Change, which showed much slower growth than expected at +122k (compared to a +139k forecast and a November +146k number). Later, Weekly Initial Jobless Claims were fewer than was predicted at 201k (versus a 214k forecast and a 211k prior week value). At the same time, Weekly Continuing Jobless Claims were 1,867k (less than the 1,870k forecast but up from the previous week’s 1,834k). Later, EIA Weekly Crude Oil Inventories showed a smaller-than-anticipated drawdown of 0.959 million barrels (compared to a -1.800-million-barrel forecast and the prior week’s 1.178-million-barrel reading). Finally, Nov. Consumer Credit came in much lower than anticipated at $7.49 billion (versus a $10.30 billion forecast and massively lower than October’s $17.32 billion number).

On the day Wednesday, six of the 10 sectors were in the green as Basic Materials (+0.32%) and Industrials (+0.22%) led the gainers. On the other side, Technology (-0.37%) and Utilities (-0.32%) paced the losses. Meanwhile, SPY gained 0.15%, DIA gained 0.19%, and QQQ gained 0.02%. At the same time, VXX was on the red side of flat at 46.34 while T2122 rose, but remained in the oversold territory at 18.91. On the bond side, 10-Year Bond yields were at 4.693% and Oil (WTI) fell 1.24% to $73.33 per barrel. So, Wednesday was an indecisive day. Markets all opened flat and then went back-and-forth from green to red and back to green all day long.

The December FOMC Minutes also came out Wednesday. Those minutes indicated that Fed members are concerned about the unknown impacts of Trump’s threatened policies. (With at least four mentioned about the impacts of changes in immigration and trade policies on the economy.) The minutes also said, “The committee would likely slow the pace of further adjustments to the stance of monetary policy” and that the decision to make another cut in December was a close call. Specifically, the Dec. minutes said “judgments about this meeting’s appropriate policy action had been finely balanced.” The notes also said, “Almost all participants judged that upside risks to the inflation outlook had increased.” … “As reasons for this judgment, participants cited recent stronger-than-expected readings on inflation and the likely effects of potential changes in trade and immigration policy.”

After the close Wednesday, GBX and JEF reported beats on both the revenue and earnings lines. However, PSMT missed on both the top and bottom lines.

On Thursday, markets were closed for President Carter’s funeral. However, Philly Fed President Harker spoke, saying, “I still see us on a downward policy rate path.” He continued, “It’s appropriate for us to take a bit of a pause right now and see how things shake out … We’re not talking about a long pause potentially, but let’s see how things shake out. There’s a lot of uncertainty.” He went on, “Looking at everything before me now, I am not about to walk off this path or turn around.” Later, Boston Fed President also seemed to signal a pause, saying, “With an economy that is in a good place overall and policy already closer to a more neutral stance, I view the current nature of uncertainty as calling for a gradual and patient approach to policymaking.” Elsewhere, Kansas City Fed President Schmid indicated a reluctance to cut rates again, saying, “We are currently pretty close to meeting our dual mandate of price stability and full employment and, with inflation close to target and growth showing continued momentum, I believe we are near the point where the economy needs neither restriction nor support and that policy should be neutral.”

Finally, Fed Gov. Bowman (the most hawkish FOMC member) said December’s rate cut should be the last for this cycle. She said that she continues to feel that inflation is “uncomfortably above” the Fed’s 2% goal while she also thinks the current Fed policy rate is near “neutral.” Beyond that, Bowman seemed to be lobbying for Trump’s favor or perhaps endorsement as new Vice Chair for Bank Supervision. She said, “We (Fed) should also refrain from prejudging the incoming administration’s future policies.” She went on to say, “Bank regulation and supervision need not be an adversarial system, with banks and regulators acting in opposition. Rather, banks and regulators often have the shared goal of a banking system that is safe, sound, and effective, with each serving an important role in furthering these objectives.”

Overnight, Asian markets were mostly in the red. Shenzhen (-1.80%), Singapore (-1.58%), and Japan (-1.05%) led the losses. In Europe, the bourses are more mixed at midday with seven gainers and seven losers. The CAC (+0.22%), DAX (+0.34%), and FTSE (-0.40%) lead the region in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a down start to the day ahead of data. The DIA implies a -0.14% open, the SPY is implying a -0.28% open, and the QQQ implies a -0.35% open at this hour. At the same time, 10-Year Bond yields are at 4.687% and Oil (WTI) is spiking, now up 3.11% to $76.21 per barrel in early trading.

The major economic news scheduled for Friday, we get Dec. Average Hourly Earnings, Dec. Nonfarm Payrolls, Dec. Private Nonfarm Payrolls, Dec. Participation Rate, Dec. Unemployment Rate, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-Year Inflation Expectations, and Michigan 5-Year Inflation Expectations. The major earnings reports scheduled before the open are limited to STZ, DAL, SNX, and WBA. Then after the market close, WDFC reports.

So far this morning, DAL, and WBA have reported beats on both the revenue and earnings lines.

With that background, it looks like the market is undecided ahead of Jobs Data this morning. All three major index ETFs are on the red side of flat, but have given us Doji type candles so far in the premarket. All three remain below their T-line (8ema) (although DIA did retest briefly in the early session). That being the case, the short-term trend is bearish. If we look further out, SPY and QQQ are below their downtrend lines, meaning the mid-term trend is also bearish. (DIA is to the right of is downtrend but still printing lower highs and lower lows.) However, in the long-term, looking at higher-timeframe charts, the market remains in a strong bull trend. In terms of extension, none of the three are extended from their T-line. However, T2122 sits in the top of its oversold area. So, the market has room to run either direction, but the Bulls have more slack to work with again today. In terms of the 10 Big Dogs, nine of the 10 are in the red with AMD (-2.03%) being the worst off by more than half a percent. On the other side, TSLA (+0.27%) is by far the strongest of that group and only one in the green. For a third-straight day, NVDA leads in dollar-volume traded by about 25% over TSLA (which itself has traded six times as much as the next most liquid stock). Don’t forget that it’s Friday. So prepare for the weekend news cycle.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service