APPL-AMZN Stoke Fear, Musk Takes TWTR

Once again, the major indices diverged at the open Thursday with SPY gapping a quarter of a percent higher, DIA gapping up 1% and QQQ gapping down a quarter of a percent. All three major indices then began a whipsaw that saw lows come the first 30 minutes, the highs come by 10:35 am, and then a roller coaster selloff kick in that had all 3 at new lows of the day before a bounce the last 3 minutes of the day. This action left us with divergent daily candles. The DIA looks like a Shooting Star, while the SPY looks like a Bearish Engulfing Spinning Top (Bear Engulfing candle with wicks on both ends), and the QQQ is giving us a strong gap-down black candle which may, just may, be trying to find support off the previous downtrend line.

On the day, half of the sectors are green and the other half red. Technology (-1.15%) is the lagging sector while Utilities (+0.96%) led the gains. The SPY lost 0.53%, the DIA gained 0.65%, and QQQ lost 1.82%. VXX was off almost 2% to 18.36 and T2122 came down a bit, but remains in the overbought territory at 87.59. 10-year bonds have dropped back below 4% to 3.913% and Oil (WTI) was up 1% to $88.74/barrel. So, from a 30,000-foot view, we had a very uneven and volatile day where Tech took the beating and safety havens (mega-caps and utilities) saw a flood of money moving that direction.

In economic news, September Durable Goods orders came in much worse than had been expected. The month-on-month number was -0.5% (when +0.2% had been forecasted). Meanwhile, the annualized number was +0.4% compared to the forecast of +0.6% and the previous month’s +0.2% number. Elsewhere, Q3 GDP came in stronger than was expected. The Q3 number was +2.6% while the forecast called for +2.4% (and the previous quarter has seen a contraction of 0.6%). The Q3 Price Index also came in far below forecast at +4.1% compared to forecast of +5.3% and the Q2 +9.1% number. Taken together, this data seemed to show a “goldilocks” scenario where the economy grew faster than expected while inflation seems to be waning. Finally, Weekly Initial Jobless Claims came in slightly better than expected at 217k (versus the 220k forecast and the 214k from the previous week).

SNAP Case Study | Actual Trade

In stock news, GOOGL’s “Google Play Store” is the target of a new EU antitrust investigation according to regulatory filings from the company. (For what it is worth, over the last 10 years, GOOGL has accrued $8.24 billion in EU antitrust fines following 3 previous investigations into company practices.) MO announced a new strategic partnership with JAPAF (Japan Tobacco) in an attempt to boost its “smoke-free” business unit. MO will hold a 75% ownership position in the new venture which will offer “heated tobacco stick” products. Elsewhere, a Federal jury in Detroit ordered F to pay $105 million in damages to a software company for breaching its 2004 license agreements and stealing trade secrets. The Wall Street Journal reported that the SEC has joined the US Dept. of Justice in investigating TSLA’s claims of “self-driving” cars via a system named “Autopilot.” In other TSLA news, the company recalled 24,000 cars due to a seat belt issue.

In miscellaneous news, the EU passed a ban on fossil-fuel cars starting in 2035. In China, it appears the government has quietly approved the BA 737 Max to resume flights in Chinese airspace as China Southern Airlines has scheduled a flight using that plane on Oct. 30. After the close, as part of their earnings report, INTC announced up to $10 billion in cost reductions over the next 3 years. The announcement did not mention layoffs, but this falls in line with previous Bloomberg reports that thousands of INTC layoffs are coming. Finally, Elon Musk takes over TWTR today and yesterday he told the company that all executives are immediately fired, he will become CEO, and that he is eliminating lifetime bans.

After the close, AAPL, GILD, PFG, RSG, EMN, WY, LPLA, VRTX, SWN, CSL, TEX, TXRH, PFSI, BIO, SKYW, DECK, DXCM, PINS, VICI, and MPWR all reported beats on the revenue and earnings lines. Meanwhile, AMZN, COF, MTX, RMD, NOV, ERIE, and SGEN all beat on revenue while missing on earnings. On the other side, INTC, X, HIG, PXD, MHK, AJG, ATR, COLM, ORI, TFII, INT, and HUBG all missed on revenue while beating on earnings. However, TMUS, LHX, EW, FSLR, and SSNC all missed on both the top and bottom lines. It is also worth noting that AMZN, INTC, EMN, EW, and SSNC all lowered their forward guidance. Meanwhile, TEX raised its guidance.

So far this morning CVX, SNY, BAH, JKS, CHD, AB, BLMN, and NVT have all posted beats on both the revenue and earnings lines. Meanwhile, XOM, EQNR, CL, AON, AVTR, and CRI all missed on revenue while beating on earnings. On the other side, oddly there are no tickers that beat on revenue while missing on earnings. However, CHTR, LYB, and DVA missed on both the top and bottom lines.

Overnight, Asian markets were mixed again but leaned to the red side as China led the decline. Hong Kong (-3.66%), Shenzhen (-3.24%), and Shanghai (-2.25%) paced the losses. Meanwhile, Singapore (+1.46%) led the gains while a trio of other smaller exchanges were positive by about one-quarter of a percent. In Europe, exchanges lean heavily to the downside at midday. The FTSE (-0.47%), DAX (-0.69%), and CAC (-0.18%) are typical of the region with only a few minor exchanges in the green in early afternoon trade. As of 7:30 am, US Futures are pointing toward a mixed, down start to the day. The DIA implies a -0.15% open, the SPY is implying a -0.64% open, and the QQQ implies a -1.08% open at this hour. 10-year bond yields are back to 4.006% and Oil (WTI) is down six-tenths of a percent to $88.58/barrel in early trading.

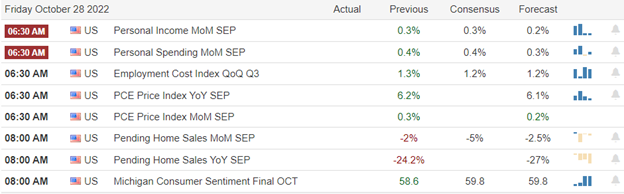

The major economic news events scheduled for Friday include Sept. PCE Price Index, Q3 Employment Cost Index, and Sept. Personal Spending (all at 8:30 am), as well as Michigan Consumer Sentiment and September Pending Home Sales (both at 10 am). The major earnings reports scheduled for the day include ABBV, AB, AVTR, BBVA, BSAC, BLMN, BAH, CHTR, CVX, CHD, CL, DVA, EQNR, XOM, FMX, FTS, GNTX, IMO, JKS, LYB, NWL, NMRK, NEE, NVT, SNY, and GWW before the open. There are no reports scheduled for after the close.

The earnings deluge continues, again with mostly positive results against lowered expectations. However, weak guidance from AMZN and an AAPL miss on iPhone sales (even amidst a quarterly beat) seems to have markets spooked about holiday spending and business activity. The rotation continues to be in play among sectors and asset classes (capitalization). With the Fed meeting again (futures say it will definitely be another 0.75% hike) next week and a weekend news cycle ahead, it would seem a likely place for bulls to take profits after the run-up from earlier in the week.

Premarket action is showing the large-caps are moving back toward their T-lines from above. However, the QQQ seems to be getting a bit extended to the downside of that 8ema. In either case, the overall market is still in an overbought condition according to T2122. Continue to show caution and be patient. Don’t chase gaps! With high volatility and several intraday reversals per day the norm, you either need to be able to handle the pain of all that whipsaw or this may be the time to pursue more cautious trading strategies (options spreads for example), including remaining hedged, quick, and/or small.

Don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is not a hobby. It’s a job. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service