Clearly, we still have a lot of challenges ahead for the economy, but last week I believe we experienced a substantial shift in institutional sentiment. Volume has grown in this relief rally, unlike the head-fake of the July/August surge upward with declining volume. However, the extreme point swings will continue to make this market very dangerous as we still face worldwide economic challenges and substantial geopolitical pressures. Perhaps a mix of long and short positions may be appropriate to hedge the uncertainty path forward.

Asian markets closed the day mixed but mostly lower, with a very volatile session in Hong Kong tech names. This morning, European markets trade with modest bullishness as bond yields and currencies continue to fluctuate. U.S. futures suggest a little rest for the bulls after the last week’s wild run-up that could trigger a bit of profit-taking to begin the week. Nevertheless, traders should continue planning for challenging price volatility as the bulls and bears duke out near substantial overhead resistance levels.

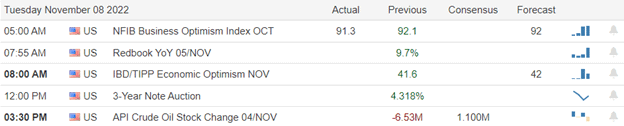

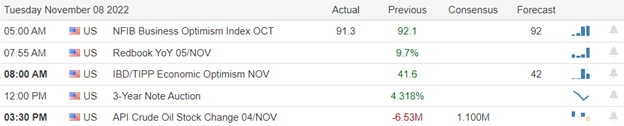

Economic Calendar

Earnings Calendar

Although we have a lot of companies listed on the Monday earnings calendar, many are unconfirmed or tiny small-cap names. Notable stocks include ACM, LI, JJSF, OTLY, TSEM, TSN, VVV, & WEBR.

News & Technicals’

Germany is open to strengthening ties with China but is not “stupid,” according to the country’s Economy Minister and Vice-Chancellor. The comments come after German Chancellor Olaf Scholz made a controversial solo trip to China to meet President Xi Jinping. A stronger dollar over the year has weighed heavily on many emerging market currencies. CNBC spotlights the performance of Ghana’s cedi, the Cuban peso, the Zimbabwean dollar, and more. The Zimbabwean dollar has lost a staggering 76.74% of its value against the dollar since January.

The investment cases for America’s largest automakers are increasingly diverging around electric and autonomous vehicles. For example, GM is diversifying as much as possible around its emerging battery and self-driving vehicle businesses while expanding to offer electric vehicles by 2035. Ford recently disbanded its autonomous vehicle business to concentrate on nearer-term technologies and EVs.

According to a source, Alameda Research, a trading firm founded by Sam Bankman-Fried, was trading billions of dollars from FTX accounts and leveraging the exchange’s native token as collateral. The source says that many employees and outside auditors were unaware that FTX did not have enough money to match customer withdrawals. Three sources familiar with the company told CNBC that FTX’s missteps blindsided them and that only a small cohort knew about the potential misuse of customer deposits.

Though we still have many challenges ahead for the economy, we experienced a substantial shift in sentiment to the buy side last week. The July/August rally suffered from a lack of volume, but this time volume continues to grow to suggest a promising institutional change. That said, we still have a lot of work to do, and the price action volatility will continue to make swing trading challenging as we face layoffs, worldwide recessionary economic impacts, and geopolitical tensions. As a result, a mix of long and short positions may be appropriate but plan carefully for sudden large point swings that will challenge even the most experienced trader.

Markets opened flat on Friday. At that point, we saw a wave of volatility until 11:30 am. This was volatility to the upside on the SPY and QQQ and to the downside on the DIA. Then the 3 major indices got into lock-step and steadily rallied in the afternoon until we saw a small pullback at 3 pm. However, the day ended on a run back up near the high of the day. The QQQ broke out of its “W pattern” resistance level during the day. This action gave us white-bodied candles with wicks at both ends in the SPY and QQQ. At the same time, the DIA printed a Dragonfly Doji candle.

On the day, eight of the ten sectors were in the green with the Consumer Cyclical sector (+2.95%) leading the way higher while the Utility sector (-0.97%) lagged behind. Meanwhile, the SPY gained 0.97%, the DIA gained 0.16%, and the QQQ gained 1.84%. The VXX was down 1.34% to 16.98 and T2122 remained deep in the overbought territory at 96.26. 10-year bond yields remained lower at 3.811% and Oil (WTI) spiked 2.76% to $88.86 per barrel. So, all-in-all, Friday saw modest follow-through to Thursday’s CPI rally everywhere other than the DIA where we got a pause.

In miscellaneous news, Friday evening, Reuters reported that EL was close to a deal to buy luxury brand Tom Ford for $2.8 billion and details may be announced as soon as today. On Sunday, TSLA said it will assist Chinese police in investigating another fatal crash (2 dead, 3 injured) of a Model Y car on November 5. TSLA has faced claims of brake failure in the past in China and a witness to this crash (a family member of the driver) said the driver was having problems with the brake pedal, but video of the crash showed no brake lights. In various buyback announcements, ASML authorized $12.43 billion in additional buybacks, PSX approved a $5 billion increase in its buyback plan, TMO authorized $4 billion in buybacks, and STLD added another $1.5 billion to its existing share buyback plans.

In cryptocurrency news, the crypto world continued to be rocked by the implosion (and Friday bankruptcy) of crypto exchange FTX. Over the weekend, it was reported that, in addition to the company’s financial woes, FTX was hacked with over $400 million in coins missing. Even more troubling, recently FTX’s former CEO (Sam Bankman-Fried) moved $10 billion of customer funds from the FTX exchange to his own trading company (Alameda Research). From there, as much as $1.7 billion has gone “missing” in the last couple of weeks. Meanwhile, in the same space, Crypto.com says it has now recovered $400 million of Ether coins days after that money had been “misplaced” when Crypto.com mistakenly sent 320k Ether coins to a cold wallet owned by Gate.io. All of this turmoil has caused billions of dollars of withdrawals from crypto exchanges and untold loss of capital in the panic selling of the last week. This has led many leading analysts in the crypto world to call for strong government regulation to re-establish trust before the entire crypto space implodes.

In energy news, Natural Gas prices plunged (5.5%) Friday as traders were trying to figure out how to interpret a blizzard of tweets that have since been called false and disinformation by the target of the tweets. Essentially, the original tweet said that the major natural gas terminal (Freeport LNG) would remain offline for at least months due to “cracked pipes” that resulted from a fire back in June. (Markets had been counting on this major terminal coming back online to reduce inventory.) If true, this would mean that US export of natural gas would be severely curtailed and US inventories of natural gas would skyrocket, lowering US prices for months. However, Freeport has now said that tweet was false, the information did not come from them (even though the original tweet was made to look like a company announcement). Meanwhile, in Congress, Coal-backed Senator Manchin has now said he does not intend to hold a re-confirmation hearing for President Biden’s Energy Secretary. This is his petty response to Biden calling for the “end of dirty energy” in the last ten days prior to last week’s election. Nonetheless, it could leave the Energy Dept. without a head for the foreseeable future.

In dividend news, these were the largest dividend increases for last week. ADP hiked its dividend by 20.2% to $1.25/share ($5 annualized) to be paid on January 1 for the holders of record on December 8. MAR raised its dividend by 33.3% to $0.40 ($1.60 annualized) per share payable December 30 for holders as of November 22. AAON hiked its semi-regular dividend by 26% to $0.24 ($0.48 annualized) payable December 16 for holders of record on November 28. PFSW declared a special $4.50 dividend payable on December 15 for holders as of November 30. ROP bumped its dividend by 10.1% to $0.6825 per share ($2.73 annualized) payable Jan. 23 for owners as of January 6.

So far this morning, MT, BAM, AZN, USFD, RWEOY, BDX, NIO, DDS, TDG, KELYA, SBH, SLVM, and NICE all posted beats on both the revenue and earnings lines. At the same time, AEG, WRK, TPR, EPC, and EYE all missed on revenue while beating on the earnings line. On the other side, PRMW beat on revenue while missing on earnings. Unfortunately, WE and SIX missed on both the top and bottom lines. It is worth noting that USFD and PRMW raised their forward guidance. However, BDX, NIO, TPR, SBH, WE, and YETI all lowered their forward guidance.

Overnight, Asian markets were mixed. Hong Kong (+1.70%), Taiwan (+1.19%), and Singapore (+1.01%) were the gainers. Meanwhile, Japan (-1.065) Thailand (-0.85%), and South Korea (-0.34%) paced the rest of the region lower into losses. In Europe, we see a similarly mixed picture at midday. The FTSE (+0.26%), DAX (+0.37%), and CAC (+0.27%) are leading the region modestly higher, while 4-5 smaller exchanges are showing red in early afternoon trade. As of 7:30 am, US Futures are pointing toward a down start to the day. The DIA implies a -0.24% open, the SPY is implying a -0.38% open, and the QQQ implies a -0.62% open at this hour. 10-year bond yields are rising again at 3.899% and Oil (WTI) is off 1.34$ to $87.77/barrel in early trading.

There are no major economic news events scheduled for Monday. However, there are two Fed speakers scheduled (Brainard at 11:30 am and Williams at 6:30 pm). The major earnings reports scheduled for the day are QFIN, ACM, XRAY, and VNTR before the open. Then, after the close, NU reports.

In economic news later this week, on Tuesday, we get October PPI, NY Empire State Mfg. Index, and API Weekly Crude Oil Stocks report. Then Wednesday, October Retail Sales, October Import/Export Price Indexes, October Industrial Production, September Business Inventories, EIA Weekly Crude Oil Inventories, and a Fed speaker (Williams) report. On Thursday, we get October Building Permits, October Housing Starts, Weekly Initial Jobless Claims, and Philly Fed Mfg. Index. Finally, on Friday, October Existing Home Sales are reported.

In earnings reports later this week, on Tuesday we hear from ARMK, BERY, ENR, AQUA, HD, SE, TME, VVV, WMT, AAP, and GSM. Wednesday, ARCO, LOW, TGT, TCEHY, TJX, ZIM, BBWI, CSCO, CPA, HP, HI, NVDA, and SONO report. Then on Thursday, we hear from BABA, BJ, BV, DOLE, KSS, M, NTES, WB, AMAT, FTCH, GPS, KEYS, PANW, POST, ROST, WSM, and WWD report. Finally, on Friday, we hear from FL, JD, and SPB.

Over the weekend, it became clear that Democrats will retain control of the Senate, with a chance to expand their margin depending on the December Georgia runoff. In addition, control of the House still remains up in the air. (The expected “red wave” we were supposed to see last week, simply wasn’t a wave at all and while it looks more likely the GOP will control the House, it will be by razor-thin margins at best with 10 more races not decided.) Also, as mentioned above, the cryptocurrency implosion (and massive volatility) also became more clear, with allegations that the CEO of FTX had moved and used $10 billion in customer funds to his own trading company prior to the Friday default. (Criminal investigations are now ensuing.) Then, overnight at the G20 summit, President Biden met with Chinese President Xi in a bid to cool tensions between the two largest economies in the world. In not unrelated news, China announced a 16-point plan to boost its real estate sector on Monday.

With that background, premarkets now look modestly red and are very extended (especially the QQQ). So, do some serious thinking before you chase any bullish moves. We know that price moves in a lightning bolt, zig-zag pattern. And, once again, at the moment, our zig is sorely in need of a zag if this is going to be a sustained move higher. Finally, remember that we get another read on the US consumer this week as the big retail names all report. Markets may wait on that news and give outsized importance to individual retail reports this week. So, beware of volatility.

So, continue to be deliberate and disciplined…but don’t be stubborn. Remember it’s 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to remember the “Legend of the man in the green bathrobe“…in that situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! And there is absolutely no reason to keep raising your bet (risk) just because you’ve had a win. Finally, keep in mind that trading is not a hobby. It’s a job. The money is real. So, you have to treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: VZ, PFE, FDX, INTC, ANET, NFLX, PLUG, PM. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

After a pleasant surprise, stocks ripped higher in the pre-market and gapped massively higher at the open. (SPY gapped up 3.75%, DIA gapped up 2.75%, and QQQ gapped up 4.95%.) At that point, we saw a sideways rollercoaster that led to gains of another 0.3% (DIA) to 1.1% (QQQ) by noon. From that point, stocks sold off modestly for an hour and recovered for another hour, bringing us back to the highs of the day at about 2 pm. At that point we saw another wave higher the rest of the afternoon. This action gave us a huge gap-up, followed by strong white candles with lower wicks in the DIA, SPY, and QQQ. All three indices are now extended well above their T-line (8ema) and the SPY and DIA have broken out of their recent high resistance level. DIA is also testing its long-term downtrend line (going back to the start of the year). Meanwhile, the QQQ is testing its 50sma.

On the day, all ten sectors were in the green with Technology (up a whopping +8.42%) and Consumer Cyclical (+7.06%) leading the way higher while the Energy sector (+2.22%) “lagged” behind. Meanwhile, the SPY gained 5.49%, DIA gained 3.66%, and QQQ gained 7.31%. The VXX was down 5.49% to 17.21 and T2122 spiked back up deep into the overbought territory at 97.69. 10-year bond yields continue to be very volatile and plunged back down to 3.824% and Oil (WTI) went up 0.56% to $86.31 per barrel. So, all-in-all, Thursday was all about the huge gap with a modest morning and then an even larger afternoon follow-through that took us out near the highs.

In economic news, as mentioned above, the October CPI gave us a great surprise by coming in at 7.7% (compared to a forecast of 8.0% and September’s reading of 8.2%). That 0.5% month-on-month drop led traders to think that inflation is coming under control and the Fed may start easing up on its rate hikes. As a result, pre-markets rocketed higher and the bulls never looked back. The Weekly Initial Jobless Claims came in slightly worse than expected at 225k (compared to the forecast of 220k and last week’s reading of 218k). That too reinforced the idea that the economy was now slowing and that should lead the Fed to ease up soon. Finally, in the afternoon, the October Federal Budget Balance also came in better than expected at a $88 billion deficit (compared to the expected $90 billion deficit).

In miscellaneous news, the US Dollar fell sharply on Thursday after the CPI data. This gave the Japanese Yen its largest gain since 2008 while the British Pound had its best day since 1985. Meanwhile, in China, the country’s normal annual surge in exports is now in doubt after it reported October exports fell unexpectedly due to falling global demand and covid lockdowns. Back in the US, Fed speakers on Thursday seemed to embrace more gradual rate hikes at this point. San Francisco Fed President Daly told a virtual conference that she “supports a more gradual approach.” At the same time, Kansas City Fed President George said “A more measured approach to rate increases may be particularly useful…” At a separate event, Philly Fed President Harker said he believes the Fed ought to pause once rates get above 4.6% and that the Fed can always start tightening again if needed, based on data.

In stock news, GOOGL’s Waymo announced it has opened up its autonomous taxi service in Phoenix AZ after months of test runs. Meanwhile, AZN announced it has withdrawn its application for US approval of its Covid-19 vaccine. AZN cited declining demand that is already being served by existing shots. Elsewhere, AMD released new server market CPU products Thursday that analysts say are far faster, larger (many more cores and I/O lanes), and much more power efficient than rival INTC offerings. In CEO news, BIIB announced that the former CEO of SNY will take over the reins as BIIB on November 14. The CEO of KDP also resigned after a violation of the company code of conduct. However, the CEO of AIG was given a 5-year contract extension after hours. Finally, after hours, the state of CA sued MMM and DD (and other smaller companies) in an effort to recoup the costs of clean-up of toxic and cancer-causing substances known as “forever chemicals.” The state is alleging the two firms marketed products containing these chemicals in the state for decades despite knowing their toxicity.

After the close, FLO, BZH, STN, and TOST reported beating on both the revenue and earnings lines. Meanwhile, EDR missed on revenue while beating on earnings. On the other side, COMP beat on revenue while missing on earnings. It is worth noting that TOST raised its forward guidance. However, COMP and EDR both lowered their forward guidance.

So far this morning, MT, BAM, AZN, USFD, RWEOY, BDX, NIO, DDS, TDG, KELYA, SBH, SLVM, and NICE all posted beats on both the revenue and earnings lines. At the same time, AEG, WRK, TPR, EPC, and EYE all missed on revenue while beating on the earnings line. On the other side, PRMW beat on revenue while missing on earnings. Unfortunately, WE and SIX missed on both the top and bottom lines. It is worth noting that USFD and PRMW raised their forward guidance. However, BDX, NIO, TPR, SBH, WE, and YETI all lowered their forward guidance.

Overnight, Asian markets were strongly green across the board. Following the cue from the US, Hong Kong (+7.74%), Taiwan (+3.73%), and South Korea (+3.37%) led the region higher. In Europe, we see a more mixed picture, but still leaning toward the upside at midday. The FTSE (-0.47%), DAX (+0.38%), and CAC (+0.27%) are leading a region that is mixed and showing modest moves in early afternoon trade. Denmark (-1.24%) is an outlier in the region. As of 7:30 am, US Futures are pointing toward a modestly green start to the day. The DIA implies a +0.35% open, the SPY is implying a +0.35% open, and the QQQ implies a +0.39% open at this hour. 10-year bond yields are down again to 3.811% and Oil (WTI) is spiking more than 3% to $89.21/barrel in early trading.

The major economic news events scheduled for Friday is limited to Michigan Cons. Sentiment (10 am). The major earnings reports scheduled for the day are limited to AQN before the open. There are no major earnings reports scheduled for after the close.

So far this morning, AQN beat on the revenue line while missing on the earnings line. However, DDL had massive misses on both the top and bottom lines. It is worth noting that AQN also lowered their forward guidance.

After a massive rally on Thursday, US markets (both stock and bonds) seem to have declared victory over the inflation enemy and will now EXPECT the Fed to act accordingly. This just means the risk has shifted to the downside, where Fed words (and especially the December meeting) could crush those raised expectations of the bulls. Be careful buying into that line of thinking. Yes, inflation came down half of a percent, but it’s still at 7.7% and that is a far cry from the Fed’s 2% target. Even more salient is the fact that this is a single data point. All of the Fed members have been talking about tightening and staying tight until inflation has shown clear evidence of SUSTAINED progress toward the target. I’m just a country boy, but to me, one data point does not equal sustained. Either way, all we can do is focus on what the market actually does, not on what we expect the Fed will/should do.

With that background, premarkets look green, but we are very extended and coming into resistance areas in the DIA and QQQ. So, think long and hard about chasing and if you decide to do so, stop and think again. We know that price moves in a lightning bolt, zig-zag pattern. And at the moment, our zig is sorely in need of a zag if this is going to be a sustained move higher. This is born out in the distance from the T-line and the extension in the T2122 indicator. Also remember that control of the House and Senate are still up in the air. While it is a very high probability that the GOP will take the House, we will not know about the Senate for another month due to the GA runoff.

So, continue to be deliberate and disciplined…but don’t be stubborn. Remember it’s 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to remember the “Legend of the man in the green bathrobe“…in that situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! And there is absolutely no reason to keep raising your bet (risk) just because you’ve had a win. Finally, keep in mind that trading is not a hobby. It’s a job. The money is real. So, you have to treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: no trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Midterm uncertainty and rising layoffs brought the bears back to work on Wednesday ahead of today’s CPI reading. Unfortunately, failures of 50-day moving averages and lower highs in the SPY, QQQ, and IWM raise additional concerns technically. That said, the damage could quickly reverse or worsen this morning depending on the reaction to the CPI and Jobless numbers coming out before the bell. Plan for another opening gap and considerable price volatility as the market reacts.

Asian markets traded lower across the board overnight as Chinese producer prices declined. European markets trade flat in a choppy cautious morning session as they wait on U.S. inflation data. However, in the usual fashion of late, U.S. futures try to pump up a positive open ahead of the CPI despite the uncertainty of what it may reveal about the path forward. So, buckle up for another wild morning where anything is possible.

Economic Calendar

Earnings Calendar

Our most hectic day of the week on the earnings calendar, with nearly 200 verified companies reporting quarterly results; however, many of them are little small-cap names. Notable reports include MT, AXN, BZH, BDX, BAM, COMP, DDS, FLO, HNST, IAA, LZ, MTTR, NIO, POSH, RL, RYAN, SBH, SIX, SSYS, SWHC, TRP, TOST, UTZ, WRBY, WB, WRK, WE, & YETI.

News & Technicals’

Binance is backing out of its plans to acquire FTX, the company said Wednesday. “The issues are beyond our control or ability to help,” Binance said in a tweet. FTX, valued at $32 billion earlier this year, is now in jeopardy of collapsing. As possibilities of bankruptcy loom, venture capital firm Sequoia Capital will mark down to zero its investment of over $210 million in the cryptocurrency exchange FTX. “Based on our understanding, we are marking our investment down to $0,” the Silicon Valley-based firm said Wednesday.

New York-based Citigroup let go of roughly 50 trading personnel this week, according to people with knowledge of the moves who declined to be identified speaking about layoffs. Bloomberg reported Tuesday that the firm also cut dozens of banking roles amid a slump in deal-making activity. In addition, London-based Barclays cut about 200 positions across its banking and trading desks this week, according to a person with knowledge of the decision. Underperformers may also be at risk at JPMorgan Chase, which will use selective end-of-year cuts, attrition, and smaller bonuses to rein in expenses, according to a person with knowledge of the bank’s plans.

According to filings published Tuesday, Elon Musk sold nearly $4 billion of Tesla shares. That follows his sale of billions of dollars in stock last year and earlier this year. Tesla’s stock price has been sinking for much of 2022 due to economic concerns and Musk’s purchase of Twitter, which closed in late October. In addition, rocket Lab delivered quarterly results on Wednesday that boasted record revenue, with the space company tacking on additional contract wins across its business. The company reported third-quarter revenue of $63.1 million, up 14% from the second quarter. The spacecraft and components business also won several contracts during the third quarter.

The bears showed their teeth on Wednesday due to midterm uncertainty and rising layoff announcements. Technically, the DIA suffered no damage from its extended condition, but the lower highs in the SPY, QQQ, and IWM raise some concerns of more trouble ahead. In addition, the SPY and IWM dipping below their 50-day averages may signal that the earnings rally has run its course. Of course, today’s reading on CPI has the potential to reverse or confirm those concerns quickly. As a result, we should prepare for another market gap at the open and expect considerable price volatility as the market reacts.

Stocks gapped lower on Wednesday (0.50% in the SPY, 0.60% in the DIA, and 0.70% in the QQQ) at the open. From there we saw a sideways roller coaster ride in all 3 major indices until noon. At that point, the bears stepped in to lead a steady 45-degree selloff for the remainder of the day. All three of the major indices closed very close to their lows for the day. This action gave us big, ugly black candles that complete Evening Star-type patterns for the DIA, SPY, and QQQ. (Not picture perfect, but show exactly the same sentiment change that an Evening Star shows.) The DIA is sitting right at a retest of its T-line (8ema), while the SPY and QQQ gave up the T-line levels during the day. Meanwhile, the SPY also fell back through its 50sma after having climbed above it just a day before. Once again, only the DIA managed to reach their average volume for the day.

On the day, all ten sectors were in the red with Energy (-4.25%) leading the way lower and Utilities (-0.92%) holding up the best. Meanwhile, the SPY lost 2.05%, DIA lost 1.92%, and QQQ lost 2.31%. The VXX was up 3.11% to 18.21 and T2122 fell out of the overbought territory and back toward the bottom of the mid-range at 27.27. 10-year bond yields continue to be very volatile and fell back to 4.084% and Oil (WTI) plunged 3.72% to $85.60/barrel. So, overall, it was a gap down and then fail to hold the level type of day. Perhaps, most traders were waiting on today’s CPI print before making any serious moves. However, traders continue to seek safety in the mega-cap DIA as it tries to hold the rest of the market up.

In economic news, early Wednesday morning (3 am), NY Fed President Williams told a Swiss audience that relatively stable longer-term inflation expectations are correct. Still, he also expressed concern that some in the US are expecting short-term declines in price pressures, which is a bad expectation according to Williams. Then at mid-morning, the EIA Weekly Crude Oil Inventories showed a 3.925-million-barrel build of inventory (three times the size of the expected build of 1.360 million barrels). Later in the day, the WASDE report increased both US corn and soybean production forecasts (corn was raised by 35 million bushels, and beans were raised by 33 million bushels). However, the US corn crop is still expected to be at a three-year low.

In stock news, MSFT faces a new European antitrust complaint from technology trade group CISPE over its cloud computing (Azure) practices. In related news, EU antitrust regulators are now drawing up charges against META over its use of customer data. If META loses the case, the EU would impose fines of up to 10% of the company’s global turnover (but appeals would drag this case out for years). Elsewhere, in another “do we really need this and is it safe” decision, ZOOM and TSLA announced they will be bringing video conferencing to TSLA vehicles. On the legal front, a lawsuit filed in Seattle Wednesday claims that AAPL and AMZN have colluded to drive up iPhone and iPad prices, by allowing only 7 of the previous 600 resellers to stay on the AMZN platform. (20% discounts used to be common on Amazon prior to the removal of the vast majority of AAPL product resellers.) In addition, LLY was ordered to pay TEVA $176.5 million after losing a trial over patent infringement related to a migraine drug. Meanwhile, COP announced it is cutting 1,100 jobs on Wednesday and expects to save up to $500 million (after taking charges for the separation costs).

In miscellaneous news, at the close on Wednesday, Binance backed out of its rescue buyout of peer exchange FTX. This leaves the FTX exchange and its native token FTT on the brink of collapse. That fear spread all across the crypto space as Bitcoin dropped 13%, Ethereum plunged more than 15%, and BNB-USD plummeted over 16%. On the supply chain front, railroad unions and companies have extended the strike deadline to December 4. The previously agreed cooling-off period was previously set to expire on November 19. Finally, in China, the number of new Covid cases in Beijing jumped to the highest in five months this week. Most alarming to the Health Ministry was that a large number of those were outside the city’s quarantine zone. This raises the specter of even wider quarantines.

After the close, G, WYNN, JAZZ, ENS, ATO, TTEC, RNG, RXT, TTEK, CRGY, JXN, and RIVN all reported beats on both the revenue and earnings lines. Meanwhile, CPNG, and RDFN both missed on revenue while beating on earnings. On the other side, LNW beat on revenue while missing on earnings. Unfortunately, STE, APP, VET, BGS, CANO, KGC, RBT, ADV, and NGL all missed on both the top and bottom lines.

So far this morning, MT, BAM, AZN, USFD, RWEOY, BDX, NIO, DDS, TDG, KELYA, SBH, SLVM, and NICE all posted beats on both the revenue and earnings lines. At the same time, AEG, WRK, TPR, EPC, and EYE all missed on revenue while beating on the earnings line. On the other side, PRMW beat on revenue while missing on earnings. Unfortunately, WE and SIX missed on both the top and bottom lines. It is worth noting that USFD and PRMW raised their forward guidance. However, BDX, NIO, TPR, SBH, WE, and YETI all lowered their forward guidance.

Overnight, Asian markets were mostly down. Singapore (+0.24%) and Malaysia (+0.252%) were the only green in the region. Meanwhile, Hong Kong (-1.70%), Shenzhen (-1.33%), Taiwan (-0.99%), and Japan (-0.98%) led the rest of the area’s exchanges lower. In Europe, stocks are slightly more mixed, but still lean to the red side at midday. The FTSE (-0.03%), DAX (+0.04%), and CAC (-0.40%) lead the region on volume with Russia (+1.33%) being an outlier in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modestly higher start to the day. The DIA implies a +0.17% open, the SPY is implying a +0.27% open, and the QQQ implies a +0.50% open at this hour. 10-year bond yields are up slightly to 4.09% and Oil (WTI) is off four-tenths of a percent to $85.47/barrel in early trading.

The major economic news events scheduled for Thursday include October CPI and Weekly Initial Jobless Claims (both at 8:30 am), and October Federal Budget Balance (2 pm). We also hear from 4 Fed speakers (Waller at 2 am, Mester at 12:30 pm, George at 1:30 pm, and Williams at 6:35 pm). The major earnings reports scheduled for the day include AZN, AZUL, BDX, BAM, CAE, CEPU, EPC, GBTG, KELYA, EYE, NICE, PRMW, RL, SBH, SIX, TPR, TDG, USFD, WRK, WE, and YPF before the open. Then, after the close, BZH, COMP, EDR, FLO, ITUB, STN, and TOST report.

In economic news later this week, on Friday, we get Michigan Consumer Sentiment. In terms of Friday earnings reports, AQN reports before the open.

With crypto markets in mayhem (the FTX exchange may file for bankruptcy today), and control of Congress still an unknown (it looks like the GOP will win the House and the Dems may just barely hang on to the Senate with their VP tie-breaker, but neither is decided yet as races remain uncalled and/or in need of a runoff election), all eyes are on the October CPI data to come out at 8:30 am. The consensus is expecting an annual rate of 8.0%, which seems like a big ask to me since last month’s number was 8.2%. So, I think the risk is to the upside. If we do get a hotter-than-expected number, markets may shoot lower as traders realize that would likely mean the Fed needs to keep up its aggressive rate hikes. If the consensus number is hit (or even beaten), look for the bulls to run (under the expectation that would mean the Fed will ease up in December). In either case, we should know how the market will react well before the open.

With that background and before that data, it looks like the markets are set to open with a modestly green “inside day” type of price as of now. Extension is no issue at all, either from the T-line or in terms of the T2122 indicator. Bear in mind that divergence between the mega-cap DIA (which has been pulling markets higher pretty much single-handedly as of late) remains a very real factor as traders have been seeking the haven of the big, stodgy names. So, beware of the knee-jerk reaction to the CPI number as well as any surprises from election decisions or sore loser challenges in various “election denying” spots around the country. Those could cause a market blip. However, the key thing to keep in mind is that you are no The Amazing Carnac” and you can’t predict reversals. So, just follow the trend and manage your risk. Slow and steady wins the race.

Be deliberate and disciplined, but don’t be stubborn. Remember that it is 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take the loss before it gets out of hand. And when price does move in your direction, always move your stops in your favor and take a little profit off the table. (You have to remember the “Legend of the man in the green bathrobe“…in that situation, it is NOT HOUSE MONEY you’re betting, it’s all OUR MONEY!). Finally, trading is not your hobby. It’s a job. The money is real. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. I know the Powerball is huge right now, but give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: no trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets opened with a modest gap higher in the 3 major indices Tuesday (up 0.3% in the SPY and DIA and up 0.6% in the QQQ). After immediately recrossing that gap the bulls stepped in to rally prices for 2 hours in all 3 of those indices. Then we traded sideways in a VERY tight range for about 2 hours. At 1:15 pm, we started a very strong selloff that crossed back down to the lows of the day and lasted until 2:30 pm. At that point, markets reversed yet again and strongly rallied back across the morning gap and about three-quarters of the way back to the highs of the day, only for another selloff to take us back down the last 30 minutes. This action gave us very indecisive Spinning Top candles in all 3 indices. The body of these candles is right at the T-line (8ema) in the QQQ, just above the T-line in the SPY, and just above the breakout of the J-hook pattern in the DIA.

It is worth noting that the DIA action happened on heavier than average volume, while the SPY and QQQ failed to reach their average volume levels. On the day, nine of the ten sectors are in the green with only the Energy (-0.16%) in the red while the Basic Materials (+2.05%) sector was far out front and Technology (+0.81%) led the pack of sectors higher. Meanwhile, SPY gained 0.52%, DIA gained 1.00%, and QQQ gained 0.71%. The VXX is up 2.91% to 17.66 and T2122 has remained just in the overbought territory at 83.53. 10-year bond yields continue to be very volatile and fell back to 4.134% and Oil (WTI) was down 2.77% to $89.25/barrel. So, overall, it was a very indecisive and whipsaw day punctuated by a strong morning rally, a mid-day drift, and then an afternoon selloff and rebound. It’s also clear money was chasing the safety of the mega-cap DIA.

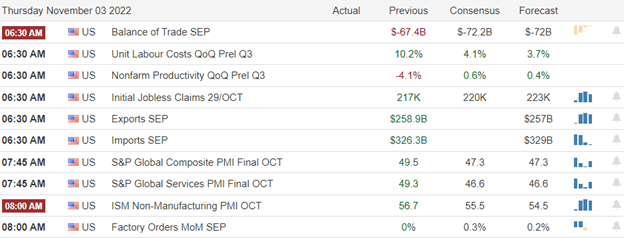

In economic / energy news, the EIA Short-Term Energy Outlook came out Tuesday. It said the US Q4 and Q1 natural gas prices are expected to be a whopping 17% lower than the EIA had forecast in October. This is based on a huge increase in natural gas storage as winter approaches. The report also said it expects natural gas and coal-fueled electricity generation to fall in 2023 from 24% (2022) to 22% (2023). Finally, the group expects Russian oil output to decrease 14% in 2023, down to 9.3 million barrels per day. Elsewhere, after the close, the API Weekly Crude Oil Stocks report showed a large unexpected build in oil inventories. The API report shows a build of 5.618 million barrels over the week compared to a forecast of a 1.100-million-barrel increase and last week’s 6.530-million-barrel drawdown.

In stock news, GFI ended its bid to acquire AUY after a joint bid of $4.8 billion was made by AEM and PAAS. (The GFI bid back on May 31 had been $6.7 billion, but that offer has declined to $4 billion as GFI stock declined since the end of Spring.) Across the pond, STLA won its appeal of an EU order to pay $30 million in back taxes to Luxembourg. This was a blow to EU rulings that are intended to stop sweetheart tax deals between EU countries and companies. Meanwhile, Airbus announced that it delivered 60 jets in October, up from 55 in September. This contrasts with BA, which delivered 35 jets in October down from 51 in September after a fuselage flaw caused delays in the production and delivery of 737 Max planes. After the close, space company ASTR announced it is laying off 16% of its workforce as the faces rocket delays. Finally, META began laying off 11,000 employees at 6 am today.

In international news, there is an opposite side of the economic harm caused by Russia’s war of aggression in Ukraine. The country of Georgia says it has received more than 100,000 Russian immigrants, most of which are college educated and many of whom brought significant money with them. As a result, Georgia anticipates its 2023 GDP will be close to 10% compared to pre-Russian-draft forecasts of 2.5% GSP growth. (Of course, one assumes those people will return home someday.) In China, the government has expanded a financing program aimed at shoring up troubled real estate developers amid that country’s growing loan defaults from that sector. The plan will offer $34.5 billion of bond financing to private firms that are at risk of defaulting on loans.

After the close, SFM, AKAM, GO, AMC, MRC, JKHY, MASI, ARRY, NOG, GXO, OVV, NLOK, and VVX all reported beats on both the revenue and earnings lines. Meanwhile, OXY, DAR, and OSCR reported beats on revenue while missing on earnings. On the other side, DOX, PRI, AMRK, and ANGI missed on revenue while beating on earnings. Regrettably, DIS, NWS, NWSA, FNF, IAC, VSAT, and NVAX all missed on both the top and bottom lines.

So far this morning, PFGC, SPTN, ICL, CPRI, HGV, CLMT, NOMD, and CRBG all reported beats on both the top and bottom lines. Meanwhile, GIB, HBI, BHG, WEN, and COHR all missed on revenue while beating on earnings. Unfortunately, DHI, RCI, MIDD, WWW, and SEAS all missed on both the revenue and earnings lines. It is worth noting that HBI, BHG, and WWW all also lowered their forward guidance.

Overnight, Asian markets were mixed. Taiwan (+2.18%), South Korea (+1.06%), and Singapore (+0.63%) led the gains while Hong Kong (-.120%), Shenzhen (-0.79%), and Thailand (-0.62%) paced the losses. In Europe, markets are leaning to the downside at midday. The FTSE (-0.27%), DAX (-0.56%), and CAC (-0.35%) are typical of the early afternoon trade. However, there are three small exchanges that are barely green and three smaller exchanges that are down more than one percent at this point. As of 7:30 am, US Futures are pointing toward a down open as the market reacts to GOP gains in mid-term elections with cautious pessimism. The DIA implies a -0.36% open, the SPY is implying a -0.31% open, and the QQQ implies a -0.32% open at this hour. 10-year bond yields are down slightly to 4.126% and Oil (WTI) is off 0.84% to $88.15/barrel in early trading.

The major economic news events scheduled for Wednesday, we get EIA Crude Oil Inventories (10:30 am), the WASDE Ag Report (noon), and another Fed speaker (Williams at 3 am). The major earnings reports scheduled for the day include BHG, CLMT, CPRI, GIB, COHR, CRBG, DHI, GGB, HBI, HGV, ICL, LTH, MIDD, NOMD, PFGC, RBLX, RCI, SEAS, SWX, SPTN, TRP, TGNA, WEN, and WWW before the open. Then, after the close, ADV, ATO, BGS, BRFS, CANO, CPNG, CRGY, ENS, FSM, G, JXN, JAZZ, KGC, LNW, MFC, RBT, NGL, RXT, RDFN, RNG, RIVN, STE, TTEK, TTEC, VET, and WYNN report.

In economic news later this week, on Thursday, October CPI, Weekly Initial Jobless Claims, October Federal Budget Balance, and 2 Fed speakers (Mester at 1:30 pm and George at 2:30 pm) report. Finally, on Friday, we get Michigan Consumer Sentiment.

It is a bit lighter week of earnings reports as, on Thursday, we hear from AZN, AZUL, BDX, BAM, CAE, CEPU, EPC, GBTG, KELYA, EYE, NICE, PRMW, RL, SBH, SIX, TPR, TDG, USFD, WRK, WE, YPF, BZH, COMP, EDR, FLO, ITUB, STN, and TOST. Finally, on Friday, AQN reports.

As the mid-term results settle, it appears GOP gains were less than expected, picking up control of the House, but with the Senate likely to once again come down to a runoff race in GA. Meanwhile, in the crypto world, yesterday the exchange Binance saved its competitor FTX buy buying out that company to prevent its failure. This comes after several billions of dollars were withdrawn from FTX in 72 hours as its own coin crashed. Bitcoin fell 3% overnight on the reaction. At this point, all eyes move on from elections toward Thursday’s inflation number.

With that background, it looks like the markets are set to open with a down, but “inside day” type of price. At this point, extension from the T-line is not an issue and T2122 is just barely into the overbought territory. The divergence between the mega-cap DIA (which has been pulling markets higher pretty much single-handedly as of late and the other two indices is the elephant in the room. “How long can those few stodgy mega-caps hold up the entire market” is the question. With all this said, remember that the reality of the economy and the direction of the economy has not been changed one bit by the election. It is all about perception and reaction today. So, beware of the knee-jerk reaction as well as follow-on tremors if/when sore losers start challenging the legitimacy of elections in various spots around the country. The bottom line is that we should be cautious and sustained in our actions. Don’t jump “all in” and “all out.” Slow and steady wins the race.

Be deliberate and disciplined, but don’t be stubborn. Remember that it is 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take the loss before it gets out of hand. And when price does move in your direction, always move your stops in your favor and take a little profit off the table. (You have to remember the “Legend of the man in the green bathrobe“…in that situation, it is NOT HOUSE MONEY you’re betting, it’s all OUR MONEY!). Finally, trading is not your hobby. It’s a job. The money is real. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. I know the Powerball is huge right now, but give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: TXG, VZ, XLP, BAC. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With some steady low-volume buying, the Dow 30 eventually pulled the other indexes out of their intraday consolidation as the dollar fell and bond yield inversion continued to extend. The Dow closed more than 1000 points off the low in just three trading days making for a high-risk situation if a pullback were to occur. The QQQ lags way behind as the most vulnerable index while the DIA continues to extend. With a big day of earnings data and the midterm results just around the corner, anything is possible Wednesday morning, so plan carefully.

While we slept, Asian markets finished the day mixed and cautious, waiting on the U.S. election results. Likewise, European markets trade flat to modestly bullish in a choppy session as the midterm results raise investor caution. However, in the norm of late, U.S. futures are pumping up the premarket, suggesting a bullish open with a deluge of earnings data on the horizon. Watch the significant overhead resistance levels, price volatility, and intraday whipsaws as the day unfolds.

Economic Calendar

Earnings Calendar

Election day will be busy with earnings results, with over 160 companies confirmed to report results. Notable reports include DIS, DDD, AFRM, AKAM, BIRD, AMC, BLNK, BLDR, CEG, COTY, DD, ELAN, EXPD, GFS, GDRX, GO, GXO, HAIN, HALO, IAC, LMND, RIDE, LCID, LITE, MNKD, NEO, NWSA, NCLH, NVAX, OXY, OPK, PLNT, PLUG, SRG, SFM, SPWR, UPST, & WYNN.

News and Technicals’

Take-Two stock dropped more than 15% in extended trading on Monday after the company said its outlook in the current quarter and early 2023 would be significantly lower than expected. In addition, shares of Palantir fell Monday after the company released third-quarter earnings before the bell that missed analyst estimates for earnings but beat on revenue. Palantir’s revenue for the quarter increased 22% year over year, and its US commercial revenue grew 53%.

The German Port of Bremerhaven, Europe’s fourth largest auto hub, is seeing so much congestion due to driver shortages and overall trade volume that cars are piling up on land and at sea. As a result, Tesla, Chrysler, and Jeep parent companies Stellantis, Renault, BMW, and Volvo are all impacted. Leading vehicle carrier Wallenius Wilhelmsen has refused auto exports for October, November, and possibly into December.

Steady low-volume buying in the Dow eventually lifted the SPY and QQQ out of an intraday consolidation producing a bullish Monday even as bond yields continued to rise. Commodities had a good day, with oil and precious metals rallying as the dollar’s value declined. The SPY peaked above its 50-day average, but the QQQ lags significantly behind. The T2122 indicator is once again nearing an overbought condition, with the DIA the most extended with significant overhead resistance showing in all indexes. Today we will be subject to midterm election news and a blizzard of earnings data with a tranquil day on the economic calendar. Plan your risk carefully as election results are revealed this evening; anything is possible Wednesday morning in reaction.

Stocks gapped modestly higher (by 0.30% to 0.40% across the 3 major indices) at the open Monday. Then from 9:30 am to 2 pm, the SPY and QQQ indices rode a roller coaster back and forth the across that gap. Over that same span, the DIA rode its own roller-coaster with a modest bullish trend. However, at 2 pm, all 3 indices started a bit stronger bullish trend. These afternoon rallies have lasted to the highs of the day at 3:30 pm and closed near the highs. This action gave us a white-bodied hammer or hanging man candles in the SPY and QQQ, while the DIA prints a large-bodied white candle with a smaller lower wick. The SPY and DIA are back above their T-line (8ema), but none are above the longer-term downtrend. It’s also worth noting the DIA has greater than average volume and both the other major indices were below average.

On the day, nine of the ten sectors are in the green with only the Utilities (-1.64%) in the red while the Energy (+1.13%) and Technology (+1.20%) sectors led the market higher. Meanwhile, SPY gained 0.96%, DIA gained 1.32%, and QQQ gained 1.10%. The VXX is down 1.1% to 17.16 and T2122 has edged up into the overbought territory at 82.87. 10-year bond yields were very volatile again and spiked to 4.216% and Oil (WTI) was down 0.82% to $91.85/barrel. So, overall, it was an indecisive morning in the market, followed by a bullish afternoon, with the mega-cap DIA leading the way all day long.

In stock news, OUST and VLDR announced they have reached a deal to merge. The deal is expected to close in the first half of 2023. Elsewhere, VillageMD (which is backed by WBA) announced it is buying Summit Health for $9 billion to expand its footprint in the healthcare business (to compete with AMZN which acquired ONEM in July, and CVS which is planning to buy Signify Health). WBA will invest $3.5 billion to support the acquisition. In other WBA news, the company cut its stake in ABC by $1.6 billion (10 million shares). WBA owned almost 53 million shares of ABC as of August 2. In legal news, it was announced Monday afternoon that the CFO of TSN (also the son of the CEO and great-grandson of the founder) was arrested Sunday for trespassing and public intoxication. In Texas, LCID filed suit against the state for blocking it from selling direct to customers in the state (as opposed to having dealerships). Meanwhile, HD workers in Philadelphia voted against forming a union the NRLB reported. It was reported by Bloomberg that D is considering selling its multi-billion dollar, 50% stake in the Cove Point LNG facility located in MD. The facility is run by BRKB (which has 25% ownership) and partly owned by BAM (25% stake). Finally, RIDE announced it is getting another $170 million in funding from Taiwan contract manufacturer Foxconn (which most notably makes iPhones for AAPL). Foxconn already owns a stake in RIDE and last summer bought the namesake RIDE plant in Lordstown Ohio.

In miscellaneous news, the US Supreme Court conservative majority appeared to be inclined to challenge the regulatory power of the FTC and SEC on Monday (based on their questioning and statements during two hours of oral arguments in cases involving both agencies). If they rule as the questioning made it appear, it will be easier for companies to appeal regulatory rulings of the Federal government. Elsewhere, the UK is set to announce a major new deal with the US (after the COP27 Climate Summit) for the US to supply Britain with LNG. Finally, Bloomberg reported after hours that US Consumer borrowing rose less than expected in September. Total credit increased by $25 billion compared to August, but the average forecast was for a $30 billion increase. This $25 included the smallest credit card borrowing increase in four months ($8.3 billion). This falls in line with V and MA both saying that consumer spending had recently slowed.

After the close, IFF, ATVI, SANM, PTVE, WELL, CBT, LYFT, DOOR, FN, QGEN, PRIM, ACCO, PAM, CLOV, OSH, and ICUI all reported beats on both the revenue and earnings lines. Meanwhile, FANG, BKD, and SEDG all beat on revenue while missing on earnings. On the other side, ASTL, CENX, AEL, DIOD, TWI, and MTW all missed on revenue while beating on earnings. Unfortunately, MOS, BHF, ARKO, VRM, TTWO, and BWXT all missed on both the top and bottom lines. It is worth noting that SANM, TPVE, ASH, FN, QGEN, and OSH all raised their forward guidance. However, IFF, WELL, CBT, JHX, LYFT, TTWO, and BWXT all lowered their forward guidance.

So far this morning, DD, BLDR, CNHI, GFS, CG, COTY, and IGT have all reported beats on both the top and bottom lines. Meanwhile, PKI, NXST, ELAN, REYN, RPRX, HAIN, and CLVT have all missed on revenue while beating on earnings. On the other side, CEG, AHCO, PLTK, CCO, and NFE all beat on revenue while missing on the earnings line. Unfortunately, PRGO, DBD, TAC, PRTY, RCM, and VTNR missed on both the revenue and earnings lines. It is worth noting that GFS and CCO raised their forward guidance while ELAN, PRGO, REYN, and RCM all lowered their own forward guidance.

Overnight, Asian markets were mostly green. Shenzhen (-0.58%), Shanghai (-0.43%), and Hong Kong (-0.23%) were the only real red in the region. Meanwhile, Japan (+1.25%), South Korea (+1.15%), and Taiwan (+0.94%) led the region higher. In Europe, the board is more mixed on modest moves at midday. The FTSE (-0.15%), DAX (+0.34%), and CAC (-0.05%) are typical of the region in early afternoon trade. However, Copenhagen (+1.09%) is an outlier and larger mover. As of 7:30 am, US Futures are pointing toward a green start to the morning. The DIA implies a +0.29% open, the SPY is implying a +0.30% open, and the QQQ implies a +0.53% open at this hour. 10-year bond yields are up slightly to 4.22% and Oil (WTI) is down two-thirds of a percent to $91.17/barrel in early trading.

The major economic news events scheduled for Tuesday is limited to the EIA Short-Term Energy Outlook (noon). The major earnings reports scheduled for the day include AHCO, BLDR, CG, CLVT, CCO, CNHI, CEG, COTY, DBD, DD, SSP, ELAN, EXPD, GFS, IGT, LITE, NFE, NXST, PRTY, PKI, PRGO, RCM, RPRX, REYN, SCSC, SSRM, SGRY, TAC, and VTNR before the open. Then, after the close, AMKR, AKAM, AMC, DOX, ANGI, DAR, FNF, GO, GXO, IAC, JKHY, MASI, MRC, NLOK, NVAX, OXY, OSCR, OVV, PRI, SFM, VSAT, and DIS report.

In economic news later this week, on Wednesday, we get EIA Crude Oil Inventories, the WASDE Ag Report, and another Fed speaker (Williams at 3 am). Then Thursday, October CPI, Weekly Initial Jobless Claims, October Federal Budget Balance, and 2 Fed speakers (Mester at 1:30 pm and George at 2:30 pm) report. Finally, on Friday, we get Michigan Consumer Sentiment.

It is a bit lighter week of earnings reports as, on Wednesday, BHG, CLMT, CPRI, GIB, COHR, CRBG, DHI, GGB, HBI, HGV, ICL, LTH, MIDD, NOMD, PFGC, RBLX, RCI, SEAS, SWX, SPTN, TRP, TGNA, WEN, WWW, ADV, ATO, BGS, BRFS, CANO, CPNG, CRGY, ENS, FSM, G, JXN, JAZZ, KGC, LNW, MFC, RBT, NGL, RXT, RDFN, RNG, RIVN, STE, TTEK, TTEC, VET, and WYNN report. On Thursday, we hear from AZN, AZUL, BDX, BAM, CAE, CEPU, EPC, GBTG, KELYA, EYE, NICE, PRMW, RL, SBH, SIX, TPR, TDG, USFD, WRK, WE, YPF, BZH, COMP, EDR, FLO, ITUB, STN, and TOST. Finally, on Friday, AQN reports.

All eyes are on the US mid-term elections today. However, crypto markets are all tumbling overnight as major crypto exchange Binance sold off all of its remaining FTT tokens ( the token of FTX, another crypto exchange). With that said, as mentioned above, there are some earnings in the news this morning. Chief among these was the DD report which beat on both the top and bottom lines.

With that background, it looks like the bulls want to retest the T-line in the QQQ today (at least going by premarket action). Meanwhile, the DIA looks to test the breakout level of its J-hook pattern and the SPY is testing its 50sma. The divergence between the mega-cap DIA and the other two main indices tells us that the market is still seeking the safety of the stodgy, traditionally less volatile Dow 30. Take that to heart. While the reality of the economy will not change tonight, Mr. Market is likely to knee-jerk stocks (for no good reason) in one direction or the other based on surprises (or non-surprises) in the results. So, don’t be in a hurry. Unless you are a volatility trader (scalper) there isn’t a lot of reason to jump in before the dust settles. Keep firm hold of your FOMO and your fear in general.

Be deliberate and disciplined, but don’t be stubborn. Remember that it is 100 times more important to avoid big mistakes than it is to pick big winners. If you have a loss, admit you were wrong and take the loss before it gets out of hand. And when price does move in your direction, always move your stops in your favor and take a little profit off the table. (You have to remember the “Legend of the man in the green bathrobe“…in that situation, it is NOT HOUSE MONEY you’re betting, it’s all OUR MONEY!). Finally, trading is not your hobby. It’s a job. The money is real. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. I know the Powerball is huge right now, but give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: EGHT, PTON, F, OUST, ACB. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Is it too much to ask for just one week of stable price action devoid of the enormous intraday whipsaws and the institutionally generated daily market gaps? Unfortunately, I would not expect it to calm down with a massive week of earnings, midterm elections, worldwide economic uncertainty, and a pending inflation report. Nevertheless, expectations for a holiday rally could undoubtedly happen as earnings help to drive high speculation despite the declining economic conditions. Therefore, expect the big price swings and challenging price action to continue in the week ahead.

Even though there was an annual drop in Chain’s exports, Asian markets were green across the board, with Hong Kong leading the buying up 2.69%. European though a bit more cautious, are also primarily bullish this morning. With midterm elections beginning Tuesday, a massive week of earnings, and a CPI read on Thursday, U.S. futures point to a gap-up open to being the week. Plan for the wild volatility to continue as the week unfolds.

Economic Calendar

Earnings Calendar

We have another crazy week of earnings with more than 700 companies on the calendar. Notable reports include ATVI, ADTN, ASH, BNTX, CHH, FANG, FN, GRPN, LYFT, MOS, NRG, PLTR, SEDG, TTWO, TRIP, VECO, & WELL.

News & Technicals’

Lidar makers Ouster and Velodyne have agreed to merge, combining roughly $400 million in market value. Under the deal, signed on Friday, Velodyne shareholders will receive 0.8204 shares of Ouster for each Velodyne share they hold – a premium of about 7.8% based on Friday’s market close. Intense investor interest in the potential of self-driving vehicles led many lidar startups to go public over the last few years. But valuations are now a fraction of what they were. According to a report from the Wall Street Journal, meta could begin to carry out large-scale layoffs as soon as Wednesday. The layoffs are expected to impact thousands of employees, the report said.

Berkshire’s operating earnings totaled $7.761 billion in the third quarter, up 20% from the year-earlier period. In addition, the conglomerate spent $1.05 billion in share repurchases, bringing the nine-month total to $5.25 billion. However, the Omaha-based company suffered a $10.1 billion loss on its investments during the third quarter’s market turmoil. China’s exports and imports fell in October in U.S.-dollar terms, according to customs data released Monday. That decline missed Reuter’s expectations for growth in both categories. China’s exports to the U.S. fell in October for a third-straight month. iPhone 14 production has been temporarily reduced because of Covid-19 restrictions at its primary iPhone 14 Pro and iPhone 14 Pro Max assembly plant in Zhengzhou, China. The factory, operated by Foxconn, is operating at “significantly reduced capacity,” Apple said. “The actual reopening is still months away as elderly vaccination rates remain low and case fatality rates appear high among those unvaccinated based on Hong Kong official data,” Goldman Sachs said in a note. The firm estimates that a full reopening could bring a 20% rally in the Chinese equity market, a separate note said.

It would sure be nice to have a week of stable price action, but with another crazy week of earnings and a CPI report later in the week, the challenging volatility will likely continue. Toss in the uncertainty of the midterm elections, and traders should be ready for just about anything! China’s annual exports declined for the first time since 2020, and with more pandemic lockdowns underway, Apple is warn’s of production losses. While next year does not look promising, we can not rule out the possibility of a holiday rally, especially with all the earnings enthusiasm generated this quarter. However, as worldwide economic activity continues to decline, plan for big intraday whipsaws and overnight reversals.

Friday was a very volatile bull trap across all 3 major indices. SPY gapped up 1.6%, DIA gapped 1.15% higher, and QQQ gapped 2% higher at the open. However, this was met with an immediate selloff that recrossed the gap in the QQQ, crossed back half the gap in the DIA, and crossed back down two-thirds of the gap in the SPY. However, then it was the bull’s turn to trap the bears as a strong rally in the second half hour took us to new highs, more than crossing up out of the gap, in all 3 major indices. At that point, the whipsaw kicked in once again as a very strong selloff ensued for the next 75 minutes. This process completely recrossed the opening gap again, down to new lows on the day at noon. From there we saw a smaller sideways rollercoaster centered on the Thursday closing price in the SPY, DIA, and QQQ. That left us bobbing back and forth between small green and small red moves for the day up until 2:15 pm when the bulls began a strong rally that is driving us back up the rest of the day in all 3 indices. It left the QQQ about three-fourths of the way back up to the opening price, the SPY 90% of the way back up to the opening price, and the DIA back just above the opening price at the close.

This action is giving us gap-up, indecisive, Spinning Top candles with wick on both ends, but considerably more wick to the downside. On the day, all ten sectors were in the green with Healthcare (+0.42%) lagging and Basic Materials (+5.26%) by far (like by 3% far) the largest gaining sector. Meanwhile, SPY gained 1.45%, DIA gained 1.35%, and QQQ gained 1.61%. The VXX was down 1.25% to 17.35 and T2122 was up but remains in the mid-range at 73.62. 10-year bond yields pulled back from early highs to 4.169% and Oil (WTI) gained 5% to $92.54 per barrel. So, overall, was a very volatile and indecisive day inside a very bearish and gap-filled week.

In economic news, October Average Hourly Earnings came in exactly as forecast at +4.7% year-on-year (compared to the expected +4.7% and well below the September value of +5.0%). This would tend to point toward a lessening of inflationary pressure. However, October Nonfarm Payrolls came in hot at +261k (versus the forecast +200k, but far below the September value of +315k). Again, this tends to show we are moving in the right direction…just not as fast as forecast. The same was true for October Private Nonfarm Payrolls which came in at +233k versus the forecast of +200k, but again far below the September value of +319k. The October Unemployment Rate was up more than expected to 3.7% (versus a forecast of 3.6% and September’s value of 3.5%). And finally, the October Participation Rate fell to 62.2% versus the September value of 62.3%. So, all this data seems to lean toward Fed actions working, inflation pressures starting to lessen, and progress being made…just not as much as we would have hoped/forecast. This is why markets gapped so strongly higher (the expectation that the FOMC will have cover to lessen hikes soon).

In stock news, Reuters reported that the US Auditors’ onsite inspection of US-listed Chinese companies has now ended. The article’s sources said it was too early to tell if the audits met US expectations. The FAA has approved JBLU’s request to waive the minimum flight requirement. This allows JBLU to keep the right to keep their gates and runway slots at NY’s JFK and NJ’s Newark airports, even though it does not use them at least 80% of the time. A state of WA court has blocked ACI from paying out the $4 billion dividend to shareholders prior to the closing of the proposed deal to be acquired by KR. In related news, the unions representing workers at both KR and ACI, as well as 26 organizations (purported antitrust experts) have urged the FTC to block that merger. The US Supreme Court has agreed to hear AMGN’s appeal to revive their patents on the cholesterol drug Repatha that were invalidated by legal challenges from REGN and SNY in 2019.

In miscellaneous news, Friday afternoon Bloomberg reported that US commercial property prices have plunged 13% from their peak in May (but only 8% over the last 12 months). Then Saturday, BRKB reported operating income up 20% year-on-year for Q3, but still managed to post a $2.69 billion net loss for the quarter, mostly from insurance losses (compared to a $10.1 billion gain in Q3 of 2121). BRKB also spent $1.05 billion on stock buybacks during the quarter (bringing the YTD total to over $5.25 billion of stock repurchased). Elsewhere, interestingly, the CFTC said after the close Friday that currency speculators have reduced their bets on a strong dollar, with the smallest net long position at the end of October for more than a year. There was $3.08 billion in net long dollar contracts compared to $10.21 billion net long the week before. This may have contributed to the Dollar’s pullback versus the Euro and Yen on Friday. Finally, on Saturday, China’s Health Ministry told a press conference that (contrary to recent rumors) China will continue its Zero Covid policy.

So far this morning, BRK.B, BNTX, HE, AMG, and FOUR have all reported beats on both the top and bottom lines. Meanwhile, NRG, NI, and PLTR beat on revenue while missing on the earnings line. On the other side, VTRS, and THS both missed on the revenue line while beating on earnings. However, AMR missed on both the revenue and earnings lines. It is worth noting that BTNX has raised its forward guidance.

Overnight, Asian markets leaned heavily to the upside. Thailand (-0.17%) was the only exchange in the red. At the same time, Hong Kong (+2.69%), Taiwan (+1.51%), and Japan (+1.21%) led the region higher. In Europe, we see a similar picture taking shape at midday. The FTSE (-0.22%) is the worst off of the only 2 exchanges showing any red. Meanwhile, the DAX (+0.84%) and CAC (+0.13%) lead the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.54% open, the SPY is implying a +0.48% open, and the QQQ implies a +0.42% open at this hour. The volatile 10-year bond yields are back down to 4.125% and Oil (WTI) is off more than 1% to $91.65/barrel in early trading.

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for the day include AMG, AMR, BNTX, CGAU, DK, FNV, DINO, KOS, NI, NRG, THS, and VTRS before the open. Then, after the close, ACCO, ATVI, ASTL, AEL, ARKO, ASH, BHF, BKD, BWXT, CBT, CENX, CLOV, CAPL, FANG, DIOD, FN, ICUI, IFF, JHX, LYFT, MTW, DOOR, MOS, OSH, PTVE, PRIM, SEDG, TTWO, TWI, VRM, and WELL report.

In economic news later this week, on Tuesday we have a Fed speaker (Mester at 4:40 am). On Wednesday, we get EIA Crude Oil Inventories, the WASDE Ag Report, and another Fed speaker (Williams at 4 am). Then Thursday, October CPI, Weekly Initial Jobless Claims, October Federal Budget Balance, and 2 Fed speakers (Mester at 1:30 pm and George at 2:30 pm) report. Finally, on Friday, we get Michigan Consumer Sentiment.

It is a bit lighter week of earnings reports as, on Tuesday, we hear from AHCO, BLDR, CG, CLVT, CCO, CNHI, CEG, COTY, DBD, DD, SSP, ELAN, EXPD, GFS, IGT, LITE, NFE, NXST, PRTY, PKI, PRGO, RCM, RPRX, REYN, SCSC, SSRM, SGRY, TAC, VTNR, AMKR, AKAM, AMC, DOX, ANGI, DAR, FNF, GO, GXO, IAC, JKHY, MASI, MRC, NLOK, NVAX, OXY, OSCR, OVV, PRI, SFM, VSAT, and DIS. Then on Wednesday, BHG, CLMT, CPRI, GIB, COHR, CRBG, DHI, GGB, HBI, HGV, ICL, LTH, MIDD, NOMD, PFGC, RBLX, RCI, SEAS, SWX, SPTN, TRP, TGNA, WEN, WWW, ADV, ATO, BGS, BRFS, CANO, CPNG, CRGY, ENS, FSM, G, JXN, JAZZ, KGC, LNW, MFC, RBT, NGL, RXT, RDFN, RNG, RIVN, STE, TTEK, TTEC, VET, and WYNN report. On Thursday, we hear from AZN, AZUL, BDX, BAM, CAE, CEPU, EPC, GBTG, KELYA, EYE, NICE, PRMW, RL, SBH, SIX, TPR, TDG, USFD, WRK, WE, YPF, BZH, COMP, EDR, FLO, ITUB, STN, and TOST. Finally, on Friday, AQN reports.

As mentioned above, there is no scheduled economic news today. However, overnight Bloomberg reported that AAPL is now expecting to make 3 million fewer iPhone 14s than originally anticipated. So, the woes in tech land continue. Probably more importantly, over the weekend, China announced that, despite rumors to the contrary, the second-largest economy in the world is sticking to its strict “Zero Covid” policy. The one olive branch from that press conference was that Chinese officials will discourage “local over-reactions.” (Still, you have to wonder whether a local official whose livelihood and maybe life depend on lowering covid case numbers is going to worry too much about the Health Ministry thinking he “overreacted”). So, it looks like we can expect more lockdowns, Chinese markets, and supply chain disruptions this winter as the covid season kicks into higher gear again.