Though slow and somewhat choppy Tuesday, the bears kept the pressure on the indexes with the high drama expected this Wednesday. Will the JPM and BLK report be healthy? Will the CPI come in hotter than expected due to supply chain issues, rising energy prices, and labor shortages? Will the FOMC minutes provide clues as to if or when taper could begin? As the drama unfolds, the one thing we can likely expect is challenging price action with elevated volatility. So plan your risk carefully as the answers roll out.

Asian markets traded mixed with modest gains and losses during the night, with HSI closed for a holiday. European markets also trade mixed as waiting for the key U.S. inflation data. However, keeping with the tradition, the premarket pump-up has the U.S. pointing toward modest gains across the board ahead of the data. So let’s get ready as the high drama unfolds.

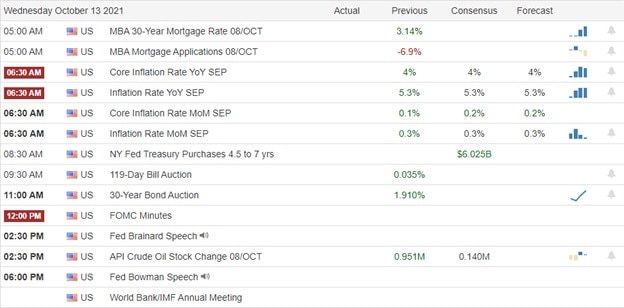

Economic Calendar

Earnings Calendar

Today we get the official kickoff of the 4th quarter earnings season with 11 companies listed but more than half unconfirmed. Notable reports include JPM, DAL, BLK, FRC, & INFY.

News & Technicals’

The good news for this earnings season is that business is good, and demand for most goods and services is relatively high. However, the bad news is the supply chain issues, labor shortages, and soaring energy prices could make it a challenging quarter for companies to produce high enough profits that support current stock prices. In addition, president Joe Biden will unveil a plan Wednesday to ease West Coast delays at the ports of Long Beach and Los Angeles by expanding round-the-clock operations. FedEx, UPS, Walmart, Home Depot, and others will also announce expanded hours operation plans during a virtual meeting Wednesday with Biden. That said, the administration will have to encourage the powerful International Longshore and Warehouse Union to get its members to work extra shifts at the ports. Today the consumer price index is expected to remain hot in September and could run hot for months to come. Economists say the recent surge in energy prices is one of the components of rising rents, making it possible that CPI could stay elevated. Treasury yields trade slightly lower this morning, with the 10-year easing to 1.566% and the 30-year declining to 2.073% in early morning trading.

On a somewhat choppy price action day, the bear kept downward pressure, waiting for the high drama of earnings and economic reports this Wednesday. We will kick off the day with big bank earnings from JPM and BLK, quickly followed by a read on inflation with the CPI report. Economists polled by Dow Jones expect the CPI rose 0.3% or 5.3% on a your-over-year basis. That said, there is a significant concern the number could come in hotter than expected due to rising energy prices, labor shortages, and supply chain impacts. Last but not least, we have the FOMC minutes this afternoon, where traders will be looking for clues regarding the taper of the easy money policies. So I think it’s fair to say anything is possible as today’s drama unfolds! The question is will it encourage the bulls or the bears? We can count on the fact that price action will remain challenging with considerable volatility for traders to battle.

Trade Wisely,

Doug

Comments are closed.