Assumed Hot June Payrolls Data On Deck

On Thursday, after an extremely hot ADP report, markets gapped down across the board with SPY opening down 0.84%, DIA opening down 0.79%, and QQQ opening down 1.05%). However, that was the end of clear direction for the day. Essentially all three major index ETFs drifted sideways with the QQQ having a slight bullish lean, and the two large-cap index ETFs continuing modestly lower until about 11 am and then trending modestly bullish. This action gave us gap-down (below the T-line or 8ema), indecisive candles in all three major index ETFs. Both SPY and QQQ printed white-bodied, Hammer-type candles while the DIA had a black-bodied, Spinning Top-type candle. The SPY got close, but only the QQQ was able to cross back above its T-line.

On the day, all 10 sectors were in the red with Energy (-2.11%) leading the way lower while Consumer Defensive (-0.75%) held up better than other sectors. At the same time, SPY lost 0.78%, DIA lost 1.04%, and QQQ lost 0.76%. The VXX jumped up 5.74% to close at 26.51 and T2122 dropped to the bottom end of the mid-range at 25.87. 10-year bond yields spiked up above four percent to 4.029% while Oil (WTI) ended flat at $71.85 per barrel. So, Thursday saw a gap lower but then mostly indecision as the rest of the day was a drift sideways with either a slightly bullish or slightly bearish lean. This all happened on average volume in the DIA and less-than-average volume in both the SPY and QQQ.

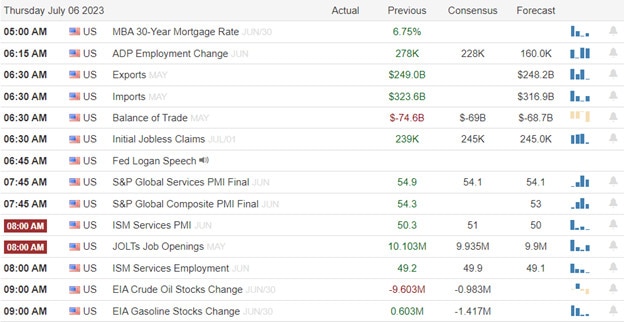

In major economic news Thursday, the June ADP Nonfarm Employment Change came in incredibly hot. The reported +497k was well more than double the forecasted +228k and almost double the May +267k reading. This was the news that spooked traders during the premarket. A little later, May Imports were reported lower than expected at $316.10 billion (versus an April reading of $326.60 billion). At the same time, May Exports also came in just a bit low at $247.10 billion (compared to an April value of $249.20 billion). Together those two led to a May Trade Balance of -$69.00 billion, which was exactly as forecasted and an improvement over the April -$74.40 balance). Meanwhile, Weekly Jobless Claims were a bit above anticipated at 248k (versus a forecast of 245k and higher than the prior week’s 236k). Later, June Service PMI was stronger than predicted at 54.4 (compared to a 54.1 forecast but lower than the May reading of 54.9). Simultaneously, the June S&P Global Composite PMI also was slightly better than expected at 53.2 (versus a forecast of 53.0 but also down from the April value of 54.3). Then, the June ISM Non-Mfg. PMI came in much better than expected at 53.9 (compared to a forecast of 51.0 and an April reading of 50.3). May JOLTs Job Openings were lower than had been forecasted at 9.824 million (versus a 9.935 million forecast and an April value of 10.320 million). Afterward, the EIA Weekly Crude Oil Inventories showed a 1.508-million-barrel drawdown (compared to a forecast calling for a 0.983-million-barrel draw but far less than the previous week’s 9.603-million-barrel drawdown. All-in-all, you could try to spin this some other way but the truth is that the economy remains strong, is weakening slowly to fight inflation, and, so far at least, it seems the Fed has threaded the needle and markets should take them at their word. They paused and there will be two more quarter-point hikes in the second half of the year.

SNAP Case Study | Actual Trade

In stock news, FIS agreed to sell a majority stake in its Worldpay merchant credit card processing services business to private equity firm GTCR. FIS will receive $11.7 billion and retain 45% ownership in Worldpay, which FIS had purchased for more than $30 billion). Later, F announced its quarterly auto sales rose 10% versus Q2 of 2022, including a 26% increase in truck sales. At the same time, STLA announced it has reached a preliminary 10-year deal to purchase rare earth minerals from NB, which plans to mine those minerals at its Nebraska mine. Elsewhere, PFE made a $25 million investment into CRBU, taking a minority stake in the biotech. In the afternoon, VLKAF (Volkswagen) announced it plans to launch autonomous vehicles for both ride-hailing and deliveries in Austin TX by 2026. By mid-afternoon, Reuters reported that CRON (which is backed by MO) is exploring options, including the potential sale of the company. The article mentions CURLF as a potential buyer of the Canadian pot producer. However, the biggest news of the day was META’s launch of its Twitter competitor Instagram Threads. The new app had 30 million user sign-ups for the service in the first 18 hours as it became the most-downloaded app in the Apple App Store. (Twitter does not release data anymore but reported 229 million active users back in May of 2022.) For its part, Twitter has threatened to sue META for “poaching of former employees” and theft of trade secrets and intellectual property. After the close, ABBV announced a cut in its full-year forecast. Citing higher R&D costs.

In stock legal and regulatory news, a federal judge ruled that RIVN must face a suit claiming it defrauded IPO investors. The suit claims RIVN concealed that it chose to underprice its electric vehicles initially, which led to price hikes that were very unpopular with consumers (that led to a 39% fall in stock price over just 10 days). At the same time, both UBER and DASH (as well as other app-based delivery services) filed suit against New York City over its law requiring companies to pay delivery workers a minimum of $17.96 per hour. Elsewhere, EU Antitrust Regulators warned that AMZN’s acquisition of IRBT may reduce competition and has opened a full-scale investigation into the deal. The decision is due by November 15. Meanwhile, the SEC announced they will vote next week on proposed changes to implement “swing pricing” to discourage hasty withdrawals from the money market and private asset funds during times of market stress. They will also vote on whether to require more disclosure from private asset managers (to detect a buildup of risk). Later, the CA state Air Resources Board along with truck and engine manufacturers such as CMI, GM, F, NAV, STLA, and VLVLY (Volvo) announced they had reached a deal. The agreement gives the manufacturers more flexibility in meeting the state’s emission rules and will give the companies no less than four years lead time before imposing new restrictions. After the close, the NRLB sued SBUX over the company’s treatment of workers which the company fired after union votes at Seattle-area stores. (SBUX claimed they were due to store reorganizations but the employees who had supported a union applied at other stores and were not rehired.) Also after the close, the FDA granted standard approval to BIIB’s new Alzheimer’s drug (which will mean wider insurance coverage for the treatment).

After the close, LEVI reported in line with forecasts on revenue and beat on earnings. However, it is worth noting that the company lowered its forward guidance.

Overnight, Asian markets leaned to the red side again. Australia (-1.69%), Japan (-1.17%), and South Korea (-1.16%) led the region lower. Meanwhile, in Europe, the bourses are mostly green at midday. The CAC (+0.57%), DAX (+0.55%), and lagging FTSE (-0.23%) are typical with 10 of the 15 exchanges in the green in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward an open just on the red side of flat. The DIA implies a -0.02% open, the SPY is implying a -0.07% open, and the QQQ implies a -0.16% open at this hour. At the same time, 10-year bond yields are rising again to 4.056% and Oil (WTI) is up a third of a percent to $72.06 per barrel in early trading.

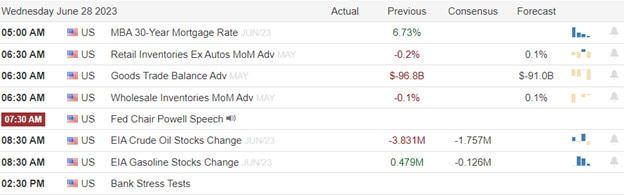

The major economic news events scheduled for Friday include June Nonfarm Payrolls, June Avg. Hourly Earnings, June Participation Rate, and June Unemployment Rate (all at 8:30 am). There are no major earnings reports scheduled for the day.

In miscellaneous news, the NY Fed released study data that indicates inflation may have slowed more than traditional headline numbers indicate. The May “multivariate core trend” said inflation stood at 3.5% (far below the May 4.6% PCE Price Index for the same period). This new report says there is actually a 68% chance inflation was really at 3% in May with the high-end of the readings being just below 4%. Fed staffers speculated the cause of the difference between PCE Price Index and the multivariate core trend is that the latter puts more weight on housing where rent increases have been moderating faster than the PCE Index components. Unfortunately, no word was given on what this might mean in terms of Fed action in July or beyond. So, it must be assumed this will not impact have a major impact on Fed rate decisions. In other Fed news, the central bank reported last night that banks again slightly decreased their borrowing from the Fed’s emergency lending programs. Fed data released Thursday showed borrowing fell to $270.09 billion last week down from $274.58 billion the previous week.

With that background, it looks like all three major index ETFs are waiting on June Payrolls data before placing any big bets this morning. As of now, we are looking at a slightly lower open and expectations are for a hot number from the June Jobs data. SPY and QQQ are both retesting the T-line (8ema) in the Premarket. At the same time, DIA is working on an inside day candle. It might be worth noting that all three of the major index ETFs are printing white-bodied candles and are currently at their highs of the early session. Overall, the pullback in an uptrend continues. However, we should note that DIA (laggard all year) is the weakest of the three and most recently printed a lower high. So, it is either acting as the canary in the coal mine or it is just the anchor that the leaders have to drag along with them. We are likely to see premarket volatility around 8:30 am, but I have a suspicion this will be another light-volume mostly drifting day as we head into the weekend again. As far as extension goes, none of the three major index ETFs is very far from their T-line and the T2122 indicator remains in the (bottom of) mid-range. So, if one side did find a reason to run today, there is slack (still buyers and sellers available). Beware of volatility and remember that its Payday. Take at least some profits if you have them, move stops, hedge, and prepare for the weekend news cycle.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service