We closed Friday with the indexes near the flatline with investors in a wait-and-see mode with pending inflation data coming Wednesday this week. Adding to the uncertainty the slowing Chinese and European economies as well as the rising U.S. bond yields and energy price impacts on an already stressed consumer. We begin the week with a light day of earnings and economic reports as we ponder what comes next with the pending CPI and PPI reports. Expect choppy price conditions as we hurry up and wait.

Overnight Asian markets began the week by closing mixed as they wait on key data later this week from Chain and India. However, European markets see modest bullishness across the board as they work to relive some of last week’s selling. U.S. futures also point to a modestly bullish open hoping to keep the relief rally alive with the inflation data uncertainty just around the corner.

Economic Calendar

Earnings Calendar

Notable reports for Monday include ORCL, CASY, and FCEL.

News & Technicals’

Europe’s largest economy, Germany, is facing a bleak outlook for 2023 as the COVID-19 pandemic continues to weigh on its recovery. According to the European Commission, Germany is expected to shrink by 0.4% this year, a downward revision of 0.6 percentage points from its previous forecast in May. This would make Germany the only major European economy to contract this year, as its peers are projected to grow by an average of 4.7%. The main reasons for Germany’s poor performance are the prolonged lockdowns, the slow vaccination rollout, and the supply chain disruptions that have affected its export-oriented manufacturing sector. The Commission also warned that Germany faces significant downside risks from the spread of new variants, the uncertainty over fiscal policy, and the potential spillovers from other countries.

Some people who take drugs for diabetes and weight loss have reported an unexpected side effect: they have less desire for addictive substances and behaviors. These drugs, known as GLP-1s, include Ozempic and Wegovy, which have been shown to help people lose weight by suppressing appetite and increasing metabolism. However, some patients also claim that these drugs have reduced their cravings for alcohol, nicotine, opioids, and some compulsive behaviors, such as online shopping and gambling. These anecdotal reports suggest that GLP-1s may have a role in treating addiction, a chronic brain disorder that affects millions of people worldwide. Several studies in animals support this idea, showing that GLP-1s can modulate the reward system in the brain and decrease the reinforcing effects of drugs. However, more research is needed to confirm these findings in humans and to understand the mechanisms and optimal doses of GLP-1s for addiction treatment.

The 10-year U.S. Treasury yield, which reflects the market’s expectations for future interest rates, rose on Monday as investors awaited key economic data due this week. The yield climbed to 1.62%, up from 1.57% on Friday, as bond prices fell. Investors are looking for clues about the strength of the U.S. recovery and the inflation outlook, which could influence the Federal Reserve’s monetary policy decisions. Some of the data releases that could move the market this week are the consumer price index (CPI) on Tuesday, the producer price index (PPI) on Wednesday, and the retail sales and consumer sentiment on Friday. Higher-than-expected inflation or growth figures could fuel expectations that the Fed will taper its bond-buying program or raise interest rates sooner than anticipated, which could put upward pressure on yields. Conversely, lower-than-expected data could ease those expectations and lower yields.

Equity markets closed near the flatline on Friday lacking momentum as pending inflation left investors in a wait-and-see mode. Chain’s ban on iPhone use for government employees weighed heavily on the tech sector which struggled for direction throughout the week. The slowing economic numbers out of China and Europe added to the uncertainty while rising bond yields and energy prices piled on keeping traders cautious heading into the weekend. Monday begins with a very light day of earnings and economic reports likely to keep price action choppy and volume low, as wait on the Wednesday CPI data. The big question is, will it inspire the bulls or will it bring out the bears? Only time will tell so get ready for a choppy couple of days as we hurry up and wait.

Friday was a “much ado about nothing” day in the market. All three major index ETFs opened flat. Then they rallied to the highs of the day by mid-morning and slowly sold off, reaching the lows of the day at about 3:30 p.m. Finally, the SPY, DIA, and QQQ all rallied modestly in the last 30 minutes. This action gave us white-bodied, indecisive candles in all three major index ETFs. The SPY and QQQ printed high-wick, Inverted Hammer type candles while the DIA printed more of a white-bodied Spinning Top candle. All three retested their T-lines from below…and failed that test, with DIA closing right at its T-line (8ema) while the other two closed below theirs. The SPY and QQQ also retested their 50smas from below, with QQQ managing to close about a dime above its 50sma while the SPY filed its test.

On the day, five of the 10 sectors were in the green with Energy (+0.91%) out in front leading the way higher and Industrials (-0.45%) by far the biggest loser among the sectors. At the same time, the SPY gained 0.15%, DIA gained 0.24%, and QQQ gained 0.14%. VXX fell a bit over two percent to close at 21.27 and T2122 climbed up out of the oversold territory to the lower end of the mid-range at 29.33. 10-year bond yields were up slightly to close at 4.258% while Oil (WTI) gained another half of a percent to close at $87.33 per barrel. This all happened on far-below-average volume in all three of the major index ETFs. So, on balance, the bulls won the day. However, there was not a lot to feel good about for the Bulls with those upper wicks and failures to clearly break through moving averages.

For the week, all three major index ETFs printed black, Bearish Harami candles. The DIA also fell through its weekly T-line (8ema). However, both the SPY and QQQ retested their own weekly T-lines and passed that test, remaining above. All three major index ETFs remain well above their weekly 50sma, with the SPY and QQQ far above. Those latter two remain in a weekly PBO (potential J-hook in formation) pattern of a strong bullish uptrend. DIA is in the same weekly pattern, but is in a much weaker (and possibly breaking or being challenged uptrend…depending on how you draw it).

There was no major economic news reported Friday. However, to summarize Fed speakers during the week, we repeatedly heard something like there is no hurry to move and it may well be worth not hiking in September…but we are not declaring victory over inflation and it is very possible we may need to hike or otherwise tighten later. This included Dallas Fed President Logan (normally more hawkish) saying late Thursday “Another skip could be appropriate … this month but my base case, though, is that there is work left to do.” Another usually hawkish member, Fed Governor Waller came right out and said it earlier, “We can just sit (to see if inflation keeps trending in a downward direction).” Meanwhile, other Fed speakers tended to tow the “let’s wait to see what more data says” line in their comments during the week. For example, NY Fed President Williams said “It’s still an open question as we go forward. Have we got sufficiently restrictive to achieve that (a 2% Fed inflation goal)?” While this went on, as of the Friday close, Fed futures indicated that the market has priced in a 93% chance of no rate hike at the September FOMC meeting. (That probability is up 7% from one month prior.)

The US dollar completed an eight-straight week of gains against its peers on Friday. Elsewhere, a Fed report Friday showed that US household wealth jumped to a record in Q2, increasing 3.7% to $154.3 trillion. This included a $2.6 trillion increase in US household equity holdings, while the value of their real estate rose just $2.5 billion in the quarter. Of course, the wealth gap continues to widen with most of than wealth concentrated in the top 10 percent of American households. (Which, in part, helps explain the “woe is us” reports of credit card debt climbing and people living paycheck-to-paycheck at the same time wealth is at record levels.)

In stock news, late Thursday night, an independent research group announced they had found a security flaw in AAPL iPhones that had allowed Israeli firm NSO to plant spyware on iPhones. Then on Friday, ABG said it was buying private firm Jim Koons Automotive for $1.2 billion in order to expand its presence in the Mid-Atlantic region. Later, Bloomberg reported that BABA has decided to temporarily shelve its plans to IPO its Freshippo grocery chain due to poor performance in the consumer stock sector recently. (BABA was hoping for a $6 billion – $10 billion valuation, but investment houses were advising roughly $4 billion would be achieved now.) At the same time, Chinese auto market analyst CPCA announced that TSLA had more than doubled its Chinese market share in August thanks to significant discounts and tax breaks. This allowed TSLA to return to unit sales growth for the month. Later, Reuters reported plastics and chemical maker COVTY has entered into discussions with suitor Abu Dhabi National Oil Company. (In August, ADNOC had offered $12.4 billion for COVTY.) Elsewhere, the Financial Times reported that the ARM IPO is already oversubscribed by five times (Reuters reported the number was more than six times oversubscribed) in the widely-watched tech IPO. Later, SLTA announced it is expanding its battery production capacity by 60% globally. No specific timetable was provided, but the company already has six battery plants under construction around the world and said there are more to come. At the same time, GNL shareholders approved a planned merger with RTL in an all-stock deal. After the close, NKLA announced that one of its electric semi-trucks caught fire near company headquarters and that this was the second such incident in the last week. Also after the close, GT announced they would cut 1,200 jobs in Europe, Africa, and the Middle East.

In stock government, legal, and regulatory news, KR announced it will sell 400 stores to private firm C&S Wholesale Grocers for $1.9 billion in an effort to gain approval for its $25 billion acquisition of ACI. Elsewhere, in Congress, the House announced it will be holding more AI hearings this week including testimony from the President of MSFT and the Chief Scientist of NVDA. On the Senate side, on Tuesday they will also hold an AI hearing. Separately, on Wednesday, Senate Majority Leader Schumer is hosting a forum (non-hearing) intended to allow Senators and Congressmen to become more informed on AI matters. These will consist of various industry presentations and Q&A sessions including one by META CEO Zuckerberg and TSLA CEO Musk. At the same time, an FTC Administrative Judge ruled against INTU on Friday. The ruling found that INTU engaged in deceptive advertising and deceived at least 4.4 million customers with ads claiming they were offering “free” tax products and services. The ruling issued a “cease and desist” order, but no financial penalty. Later KR announced they had agreed to a $1.4 billion settlement (paid over 11 years) to resolve thousands (most) of outstanding lawsuits by US states and local governments over opioid distribution. This included $1.2 billion going to states, $177 million in attorney fees, and $36 million to Native American tribes. In the afternoon, a US federal judge ruled META must face a lawsuit claiming it violated the medical privacy of patients who used medical facility websites that included a META Pixel tracking tool. The judge ruled against META’s motions to dismiss the case. In the afternoon, the FDIC released a report saying the agency should have been more aggressive in its policing of the risk management of FRCB prior to its failure in May. (It said it was unclear if this could have saved the bank given the speed at which depositors pulled their money out of the bank. However, it should have done more and sooner.) After the close, the NHTSA cited inadequate inspections as the cause of a UAL 2021 jet engine failure. Soon after the failure, the FAA ordered immediate inspections of all BA jets with RTX-made Pratt & Whitney 4000 engines.

In Autoworker contract talks or strike news, on Friday, STLA offered the UAW a 14.5% wage increase over four years. This is far short of the UAW’s desired 46% increase and a reduction to a 32-hour work week. Previously, GM offered a 10% immediate raise, followed by two other 3% increases over the four years. The week before, F had offered 9% increase over four years along with a 6% lump-sum one-time payment. The UAW contract with all of the “Big 3” automakers ends Thursday night at midnight.

Overnight, Asian markets were mixed but leaned toward the green side. Shenzhen (+0.98%), India (+0.89%), and Shanghai (+0.84%) paced the gains. Meanwhile, Taiwan (-0.86%), Hong Kong (-0.58%), and Japan (-0.43%) paced the 5 (or 12) down exchanges. However, in Europe, we see nearly green across the board at midday. Only Russia (-0.82%) is in the red while the CAC (+0.42%), DAX (+0.34%), and FTSE (+0.06%) lead the 15 green exchanges higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a green start to the day. The DIA implies a +0.19% open, the SPY is implying a +0.41% open, and the QQQ implies a +0.61% open at this hour. At the same time, 10-year bond yields are up a bit to 4.294% and Oil (WTI) is off by three-quarters of a percent to $86.89 per barrel in early trading.

There is no major economic news scheduled for Monday. There are also no major earnings reports scheduled for before the opening bell. However, after the close, CASY and ORCL report.

In economic news later this week, on Tuesday we get the EIA Short-Term Energy Outlook, WASDE Ag Report, August Federal Budget Balance, and API Weekly Crude Oil Stock report. Then Wednesday, August Year-on-Year CPI, August Month-on-Month CPI, and EIA Weekly Crude Oil Inventories are reported. On Thursday, we get August Month-on-Month PPI, Weekly Initial Jobless Claims, August Retail Sales, July Business Inventories, July Retail Inventories, and the Fed Balance Sheet. Then Friday, August Export Price Index, August Import Price Index, NY Empire State Mfg. Index, August Year-on-Year Industrial Production, August Month-on-Month Industrial Production, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Consumer 12-month Inflation Expectation, and Michigan Consumer 5-Year Inflation Expectations are reported.

In terms of earnings reports later this week, on Tuesday there are no major reported scheduled. Then Wednesday, CBRL reports. On Thursday, we hear from ADBE, CPRT, and LEN. Finally, on Friday, there are no major earnings reports scheduled again.

In miscellaneous news, on Friday, the SEC approved a NASDAQ request to allow a new AI-driven order type. The new M-ELO order type would use AI to speed up the matching of orders at the midpoint of the bid-ask spread. The new order type, first proposed in 2018, would allow investors to trade with 10-millisecond waiting periods. (This means these orders would fill about 20% faster, greatly reduce non-fills, and reduce required holding times by more than 11%.) It was not mentioned, but this certainly seems aimed at high-frequency traders and the benefit of brokers. Elsewhere, the state of AK filed suit against the US Dept. of Agriculture, seeking to block the decision announced Wednesday that President Biden was reversing a Trump-era ruling allowing large swaths (9.37 million acres) of the Tongass National Forest to be opened for logging, mining, and oil exploration and production. Biden’s order canceled dozens of oil and gas leases issued in the last days of the Trump administration. Finally, on Sunday, the now-former CEO of BABA resigned. (It was not long ago that he was “relieved” of CEO and Chairman duties to focus on the new BABA Cloud business.) The unexpected move riles BABA shares in China.

In late-breaking geopolitical news, over the weekend, President Biden and Indian PM Modi announced a new international transportation network project meant to rival China’s “Belt and Road” initiative at the G20 Summit. The idea is to invest in infrastructure connecting Asia, the Middle East, and Europe. Not only will US-based multinationals benefit, but it will make the US and India an alternative funding source (competitor) to help limit the increase in Chinese influence in the world (achieved through financing and then takeover). In a separate initiative, on Sunday it was announced the Biden Administration and Saudi Arabia have jointly entered into talks with multiple African nations to secure ownership of various mining operations (mostly rare earth mines). Under the joint deals being offered, the Saudis would buy the mines and the US would be guaranteed the right to buy percentages of those mine’s production. (Implied, but unstated, is that US force would be there to ensure the security of the mines should anything of an Islamic or Wagnerian nature threaten them.) Finally, there was a major 6.8 earthquake in Morocco Friday. (This was made “more major” because the region was not built or prepared for such a disaster.) So far, 2,400 are known dead and 300k are homeless.

With that background, it looks like the Bulls are trying to make another move this morning. All three major index ETFs are back above their T-line (8ema) in the early session. The SPY and QQQ are also back above their 50sma. However, with its black premarket candle, the DIA has, so far, failed a retest of its 50sma. This leaves the SPY, QQQ, and DIA all on the green side of flat at least at this point. The very short-term and mid-term trends are now bullish, but only just so in the short-term. (The previous short-term downtrend has been broken, but we have not yet proven we can hold. So, it is really a presumed resumption of the mid-term uptrend.) As far as extension goes, none of the major index ETFs are far from their T-line and the T2122 indicator is sitting in the lower-end of its mid-range. So, there is plenty of slack for either the bulls or the bears to make a move…again, if they can find the buyers or sellers.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Thursday gave us another schizophrenic day with a gap in one direction and the market then trading in the opposite direction all day. In this case, we gapped down 1.21% in the QQQ, 0.69% in the SPY, down just 0.11% in the DIA. All three major index ETFs then traded sideways for an hour. However, at that point, the Bulls stepped in to drive a slow, modest rally that lasted the entire rest of the day. The SPY and QQQ climbed back up into the opening gap while DIA crossed its much smaller gap to close a little to the positive side. This gave us white-bodied candles in all three index ETFs that could all be seen as larger-bodied Spinning top-type candles in the SPY, QQQ, and DIA. QQQ ended the day testing its 50sma from below and DIA was just below its T-line (8ema) at the high of the day.

On the day, eight of the 10 sectors were in the red with only Utilities (+0.93%) by far the strongest while Technology (-1.13%) and Basic Materials (-0.97%) led the way lower. At the same time, the SPY lost 0.31%, DIA gained 0.20%, and QQQ lost 0.72%. VXX was essentially flat at 21.71 and T2122 climbed but remained inside of the edge of oversold territory at 17.25. 10-year bond yields fell to close at 4.254% while Oil (WTI) dropped 0.81% to close at $86.83 per barrel. (That was Oil’s first drop in 10 days.) This all happened on lower-than-average volume in all three of the major index ETFs. So, the Bears had control at the open, but once they got their footing, the bulls were in charge of a tepid rally the rest of the way.

The major economic news reported Thursday included Weekly Initial Jobless Claims which came in well below expectations at 216k (compared to a forecast of 234k and the prior week’s 229k). At the same time, Q2 Nonfarm Quarter-on-Quarter Productivity came in at +3.5% (a bit below the +3.7% forecast but far better than the Q1 -2.1%). In addition, Q2 Quarter-on-Quarter Unit Labor Costs rose 2.2% (far outstripping the +1.6% forecast but also dramatically lower than the Q1 +4.2%). Later, the EIA Weekly Crude Oil Inventories followed Wednesday evening’s API data by showing a much larger-than-expected drawdown of 6.307 million barrels (versus a forecast calling for a 2.064-million-barrel draw but still far lower than the prior week’s 10.584-million-barrel drawdown). Finally, after the close, the Fed reported that they reduced their Balance Sheet by another $20 billion from $8.121 trillion to $8.101 trillion.

In Fed and regulator news, on Thursday, the FDIC reported that US bank profits and deposits were broadly steady in Q2. This suggested that the turmoil in the sector in Q1 had passed. The report said industry profits in Q2 fell 11.3% year-on-year from 2022 to $70.8 billion. (If the SIVB and SBNY failures were stripped out of the report, the rest of the sector increased profits by 5.7% in Q2 versus 2022.) However, deposits declined for the fifth quarter in a row, down 0.5% quarter-on-quarter. Elsewhere, the Senate confirmed the last open Fed Governor seat, approving Adriana Kugler (who is a labor market expert). Later, NY Fed President Williams told Bloomberg “We’ve got policy in a good place, but we’re going to need to continue to be data dependent.” He went on to say that it was an “open question” whether monetary policy is restrictive enough to bring the economy back into the proper balance of inflation and full employment. After the close, Dallas Fed President Logan said that while it could be appropriate to skip an interest rate hike in September, more policy tightening may be needed before we reach the 2% goal. She said, “Another skip could be appropriate when we meet later this month, … but skipping does not imply stopping.”

In stock news, on Tuesday, SUM announced they have agreed to buy Columbian cement producer Cemento Argos for $3.2 billion in cash and stock. (That deal would make SUM the largest cement maker in the US.) Elsewhere, NWSA said it’s engaged in various negotiations with artificial intelligence companies over the use of content produced by AI. At the same time, MGA (electric vehicle components maker) told an investors conference that it expects to roughly double its sales this year and double again by 2025. Later, the CEO of CHTR said it was urgent to resolve its contract dispute with DIS. (DIS has blocked CHTR customers from accessing DIS content, including ESPN during the highest-rated football season and CHTR is hemorrhaging subscribers as a result.) In cost-cutting news, WMT announced changes to its entry-level store compensation plans to make cashiers, stockers, self-checkout helpers, department associates, and personal shoppers all receive the same hourly wage. The move was meant to take advantage of a slowing job market (which I must have missed happening). WMT did not specify the amount it expects the move to save. Meanwhile, the CFO of BA said the company still expects to hit its annual 737 deliveries goal, despite a new production problem that has slowed deliveries of its bestselling 737 MAX. However, he also said BA will be on the low end of its 400-450 jet target. In other BA news, SPR told an investor conference Thursday that it has asked BA to absorb more of the financial pain caused by inflation and parts shortages. The CEO told the conference that their contracts with BA are “not sustainable.” (BA did not reply to Reuters requests for comment.) At the same time, the CFO of RIVN told a GS conference that the company expects a significant decrease in the cost of battery materials during 2024, and will even see some of those effects in Q4 of 2023.

In stock government, legal, and regulatory news, AAPL suffered a second-straight terrible day after China banned the use of iPhones by government officials. (This move by China is widely seen as both a signal to AAPL, which has recently been moving operations out of China and into places like India, and to the US government that it could ban iPhones altogether if trade wars continue.) a three-judge federal appeals court panel revived a lawsuit against GM from a black safety supervisor. The suit accused GM of racism and sexism that created a hostile work environment over complaints of workers displaying nooses and Confederate flags as well as using racial and sexist slurs toward herself and other black employees for a prolonged period without company sanctions. At the same time, MSFT announced it would pay the legal damages that its customers might suffer if they are sued for copyright infringement for using the output of MSFT AI products. The potentially legally risky plan could also be a marketing boon for its co-pilot assistant products. At nearly the same time, MSFT also announced that it suspects Chinese-controlled social media accounts are already using AI to influence voters as the US prepares to enter the heart of the 2024 election cycle. MSFT said they have made the US Dept. of Justice aware of its research findings. (Screenshots of META’s Facebook and X, formerly Twitter were provided.) After the close, Reuters reported that ZM has been in talks with the US FTC and EU, UK, and German competition regulators, outlining anti-competitive behavior by MSFT related to chat and video apps and bundling with MSFT’s dominant Office suite.

In Autoworker contract talks or strike news, GM offered a 10% immediate wage hike and two additional 3% increases over four years. The offer also included a $5,500 ratification bonus (immediate) as well as $5,000 in potential bonuses over the life of the contract. The UAW President quickly called it “an insulting proposal that doesn’t come close to an equitable agreement.” He continued by implying the threat of a strike as of midnight on September 14. Elsewhere, the UAW said it plans to deliver a counter-proposal to STLA Friday. Meanwhile, F is taking a different tact, by giving 8,000 UAW hourly workers a $4.33/hour ($9,000/year) raise effective immediately (a week ahead of the expiration of the current contract and before a new contract has been agreed. For what it is worth, analysts say a strike against STLA is the most likely thing to happen with a strike against GM and F held as negotiating escalation tools by the UAW.

Overnight, Asian markets were nearly red across the board on a modest move day. Only India (+0.47%) was in the green, while Japan (-1.16%), New Zealand (-0.72%), and Singapore (-0.58%) led the region lower. In Europe, we see a similar picture taking shape at midday. Three of the 15 bourses are in the green. However, the CAC (-0.09%), DAX (-0.41%), and FTSE (-0.09%) lead the way lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a modestly red start to the day. The DIA implies a -0.19% open, the SPY is implying a -0.22% open, and the QQQ implies a -0.30% open at this hour. At the same time, 10-year bond yields are flat at 4.254% and Oil (WTI) is up two-thirds of a percent to $87.48 per barrel in early trading.

There is no major economic news scheduled for Friday. The only major earnings report on the day is KR before the opening bell. There are no reports scheduled for after the close.

After the close, DOCU and RH reported beats on both the revenue and earnings lines. It is worth noting that DOCU raised its forward guidance. This morning, KR was supposed to report at 7:15 a.m. However, for some reason, they are delayed and have not posted results yet as of 7:45 a.m. (Late, KR reported a miss on revenue and a beat on earnings. It has not posted any change to guidance yet.)

In miscellaneous news, traffic on the ChatGPT website fell for the third month in a row. Since they are widely accepted as the leader in the AI space, this begs the question as to whether “AI mania” is subsiding or if this is just the result of numerous competitors diluting the ChatGPT market leadership. Elsewhere, the Financial Times reports that GS will begin following the “Jack Welch at GE” plan, meaning they now have plans to fire 1%-5% of the GS workforce annually, based on performance evaluations. This “culling of the deadwood” would lead to 450 to 2,500 firings (and presumably replacement hires) each year. Meanwhile, CNBC did an analysis of just how much impact “shrinkage and theft” are really impacting retailer profits. (The topic has been a major talking point among right-wing media and has even been cited as an excuse by some retailers to explain poor results.) CNBC analyzed seven big retailers (TGT, M, DKS, LOW, FL, ULTA, DLTR, TJX, and WMT) balance sheets. Contrary to the general narrative of the right, they found that inventory losses were only a small fraction of the retailer’s sales and “pale in comparison to other factors squeezing margins.” (Those factors include “excessive” discounting and promotions.) In fact, CNBC found that shrink is in line with the industry-standard losses over the last decade (1% – 1.5% of sales). This suggests that despite individual well-publicized cases that are aided by ever-present video, “organized theft rings” and “people just feeling entitled to take ransack or take what they want” is not really more of a problem than it was a decade or two ago. It just seems that way because companies are looking for excuses and one side of the political aisle wants to push the narrative that things are terrible. (To be fair, this is certainly not exclusively a tactic of the right. It has been said that there are only two themes to politics. “Things have gone to hell, throw the bum out” and “You’ve never had it this good, give me another term.”) The point is, that theft was mostly just a convenient excuse, taking advantage of one part of society that wanted to push a certain narrative, being used by companies to justify poor performance.

In geopolitical news, Bloomberg reports that India is currently studying its potential responses to a Chinese invasion of Taiwan. The report says this comes after the US made discreet inquiries about how India might contribute in the event of war, which would result when the US steps in to defend Taiwan. While this made news and is being reported as a “new study commissioned by India’s top military commander,” I have serious doubts whether that is entirely true. Frankly, both Indian and the US military and political leadership would need to be completely incompetent if such a scenario had not been extensively studied and various responses discussed, over and over again. The topic is probably revisited at least annually in each country. In fact, I would bet that the subject has been discussed between the militaries and between the political leaders of the two countries repeatedly over many years. (At least ever since India started to think of itself as an emerging power in Asia.) So, I suspect this is just a story leak meant to make news and apply a bit of pressure on China as the G-20 meeting gets going. Still, it made Bloomberg’s top headlines.

With that background, it looks like the Bulls tried to make a move in the premarket, but have sold off since that point. All three major index ETFs started the early session at or very near their T-line (8ema), but have since sold down to create black-bodied premarket candles. (QQQ has also done the same with its 50sma this morning.) This leaves the SPY, QQQ, and DIA just on the red side of flat as we get nearer to the open. The short and mid-term trends remain bearish with the long-term trend remaining bullish across all three major index ETFs. As far as extension goes, none of the major index ETFs are far from their T-line and the T2122 indicator is sitting just inside the top edge of the oversold territory. So, both sides have room to run, if they can gain the momentum to do so. Finally, don’t forget it’s Friday. Pay yourself and prepare your account for the weekend news cycle. Hedge, lighten up, or get some insurance (options) to mitigate risk as you see appropriate.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Indexes closed with losses on a light day of data here in the U.S., while Asian and European economic news started the day off with a little bearish sentiment. The pressure continued to grow as oil rose to a 10-month high adding worries to its potential inflation impact and helping bond yields to surge higher on the day. To find inspiration today we have Mortgage, Trade, PMI, ISM, Beige Book, Fed speak, and just a few notable earnings events for the bulls and bears to wrangle over. Plan for price action to remain challenging as the bulls look for anything to resume the relief rally and the bears look for some inspiration to resume selling.

While we slept Asian markets traded mixed even as Country Garden made payments allowing China real estate stocks to surge. However, European markets trade bearishly across the board as surging energy prices add additional challenges to an already struggling economy. U.S. futures also suggest a modestly bearish open ahead of earnings and economic data worried about the inflationary and economic impacts of rising energy prices.

Economic Calendar

Earnings Calendar

Notable reports for Wednesday include AEO, AI, CNM, GME, PLAB, PLAY, SPWH, PATH, & VRNT.

News & Technicals’

The European Commission, the executive branch of the European Union, has announced that it has identified six tech giants as “gatekeepers” under its new Digital Markets Act (DMA) — a landmark law that aims to curb the power of the dominant digital platforms. The six gatekeepers are Alphabet, Amazon, Apple, ByteDance, Meta, and Microsoft. These are large digital companies that provide core platform services, such as online search engines, app stores, social networks, and messaging services. The DMA imposes a set of obligations and prohibitions on these gatekeepers to prevent them from abusing their market position and harming competition and consumers. The DMA is one of the first regulatory tools to comprehensively regulate the gatekeeper power of the largest digital companies. The DMA complements but does not change EU competition rules, which continue to apply fully. The European Commission is the sole enforcer of the DMA and will monitor the compliance of the gatekeepers with the law.

The U.S. government is facing the risk of a shutdown at the end of September unless Congress passes a spending bill to fund its operations. The White House and the leaders of both chambers of Congress have agreed to support a stopgap measure, also known as a continuing resolution, that would keep the government running until December 3. However, the stopgap measure still needs to be approved by both the House and the Senate, which could face some challenges from lawmakers who oppose certain provisions or demand additional funding for their priorities. A government shutdown would have negative consequences for the economy, public services, and federal employees. The last government shutdown occurred in 2018-2019 and lasted for 35 days, the longest in U.S. history.

Country Garden, a Chinese property developer, has seen its shares rise after it narrowly avoided defaulting on its bond payments. The company reportedly paid $22.5 million in bond coupon payments on Tuesday, just hours before a 30-day grace period expired. The bond payments were originally due in August, but Country Garden had requested an extension due to liquidity problems. The company has been facing financial difficulties amid the tightening regulations and slowing demand in China’s real estate sector. The successful payment of the bond coupons has eased some of the market concerns and boosted the confidence of the investors. Country Garden’s shares rose by 4.6% on Wednesday, outperforming the broader market.

Tuesday, the stock market closed with losses, while the bond market and the dollar gained. There was no major news that moved the market, but some weak economic data from abroad caught some attention. The services sector in China grew slower than expected in August, showing that the stimulus measures have not boosted consumption yet. Similarly, the final numbers for the services sector in the eurozone were lower than the initial estimates, indicating some slowdown in growth. The energy sector was the best performer today, as oil prices rose after Saudi Arabia announced that it would keep its voluntary production cuts until the end of the year. Oil prices reached a ten-month high of $87 per barrel. Today investors will have Mortgage Applications, International Trade, PMI, ISM, Beige Book, and some Fed speak along with a handful of notable earnings to find bullish or bearish inspiration.

Tuesday gave us a modest gap lower at the open (down 0.10% in the SPY, up 0.01% in the DIA, and down 0.23% in the QQQ). At that point, we saw a little follow-through by the Bears that bottomed out at about 10:40 a.m. Then the Bull stepped in to rally us until shortly after 11 a.m. From there, the Bears led a long, slow, wavy decline right into the close on the SPY and DIA. Meanwhile, the QQQ ran back and forth between the late morning high and the Friday closing level. This action gave us black-bodied candles with very little wick in the SPY and DIA (with the DIA crossing back just below its T-line and 50sma). Meanwhile, the QQQ printed a white-bodied Spinning Top candle.

On the day, nine of the 10 sectors were in the red with only Energy (+0.10%) hanging onto green territory while Basic Materials (-0.1.93%) and Industrials (-1.74%) led the way lower. At the same time, the SPY lost 0.43%, DIA lost 0.55%, and QQQ gained 0.13%. VXX gained two-thirds of a percent to close at 21.35 and T2122 plummeted back down to the other side of the mid-range to just outside the edge of oversold territory at 21.48. 10-year bond yields shot up to close at 4.266% while Oil (WTI) gained another 1.39% to close at $86.74 per barrel. This all happened on extremely low volume (not much more than half of the 50-day average) in all three of the major index ETFs. So, the Bears had control on the day, but it sure felt like just a tepid pullback after last week’s pre-holiday rally.

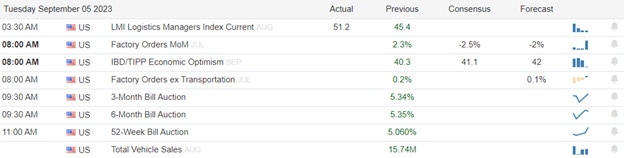

The major economic news reported Tuesday was limited to July Factory Orders, which came in down but better than expected at -2.1% (compared to a forecast of -2.5% but much worse than the June reading of +2.3%).

In Fed news, Fed Governor Waller said Tuesday that the latest economic data was giving the FOMC space to wait and see whether it needs to raise rates again. He went on to note that he currently sees nothing that would force the Fed to raise the cost of short-term borrowing again. Waller said, “we have to wait and see if this inflation trend is continuing … I want see a couple of months continuing along this trajectory before I say we’re done doing anything.” (For what it’s worth, the market is pricing in only an 8% chance of a rate hike in just over two weeks at the September meeting and just over a 40% chance of a hike at any of the three remaining scheduled 2023 meetings.) Later in the day, the NY Fed said that it believes the neutral rate (neither restrictive or stimulative), known as R-star had fallen in Q2. The Fed analysis pegged 0.57% as the R-star for Q2, down from 0.68% in Q1. It is worth noting that analysts add the Fed target of 2% inflation to that R-star. In this case, it would mean a 2.57% rate would be neutral for the economy. Since the Fed currently has rates at 5.25% to 5.50%, that means the Fed is being very restrictive.

In stock news, on Tuesday, WBD announced that the Hollywood writer’s strike will hit the company’s 2023 profits. The company expects the impact to be $300 million – $500 million for 2023 reducing earnings to $10.5-$11 billion. Elsewhere, STLA said that its testing shows that 24 of the company’s existing internal combustion engines work, without modification, on new e-fuels. (E-fuels are synthetic fuels that blend existing standard fuels with carbon that has been captured and hydrogen created from sustainable electric sources like wind, solar, and nuclear.) At the same time, UAL announced that it had resumed flight departures after a computer issue had forced them to have the FAA ground all non-departed flights earlier in the day. By midday, MA denied reports that the company is planning to increase the fees charged merchants when a credit card is processed. This came after the Wall Street Journal reported it had obtained documents and sources claiming that both MA and V have plans to raise those fees in October and April respectively. After the close, Reuters reported that the head of GM manufacturing said that current UAW demands “have significant costs attached that would threaten our ability to maintain our manufacturing momentum.” Also after the close, ENB announced they had agreed to acquire 3 utilities from D for a total purchase price of $14 billion ($9.4 billion in cash and $4.6 billion in assumed debt). In the early evening, AAPL announced it had extended its deal with soon-to-IPO ARM in a deal that extends until 2040. (AAPL uses ARM chips in all of its phones, tablets, and computers. During the evening, COIN announced it would be launching a new lending platform aimed at large institutional investors. (A regulatory filing shows that COIN has raised $57 million to fund the development and launch of this new platform.)

In stock legal and regulatory news, TSLA filed suit in China against Chinese chip designer Bingling, claiming the company violated its intellectual property rights. (Bingling specializes in chip design related to battery efficiency optimization.) Later, the NHTSA announced a decision that 52 million airbag inflators should be recalled. (The agency had first called for the recall in May, but the maker, Arc Automotive, refused.) This would impact 12 automakers, including GM, F, STLA, TSLA, TM, HYMTF, MBGAF, BMWYY, VLKAF, and models from 2000 through early 2018. The next step will be a public hearing in October to compel the recall. After the close, the Wall Street Journal reported that the FTC is planning to file an antitrust suit against AMZN later this month after the e-commerce giant refused to offer concessions related to its pricing and rules requiring third-party sellers to use “Fulfillment by Amazon” to avoid fees.

On Monday evening, ZS posted beats on both the revenue and earnings lines. The company also raised its forward guidance. So far this morning, CNM reported in-line revenue but missed on the earnings line by a penny. At the same time, EXPR missed on both the top and bottom lines.

US mortgage demand fell last week to a 27-year low, even as interest rates fell slightly. Total applications for new home purchase loans fell two percent for the week (and were 28% lower than one year prior). Meanwhile, refinancing applications were down five percent week-on-week (and were 30% lower than the same week in 2022). This all took place while the average rate for a 30-year, fixed-rate, conforming loan dropped from 7.31% to 7.21% (with closing points also decreasing from 0.73 to 0.69).

Overnight, Asian markets were mixed but leaned toward the downside. Japan (+0.62%) was, by far, the biggest gainer. Meanwhile, Australia (-0.78%) and South Korea (-0.73%) were by far the biggest losers on the session. In Europe, things are more dicey at midday with only Belgium (+0.09%) hanging onto green territory. On the other side, the CAC (-0.71%), DAX (-0.40%), and FTSE (-0.66%) lead the rest of the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing to a modestly red start to the day. The DIA implies a -0.19% open, the SPY is implying a -0.22% open, and the QQQ implies a -0.27% open at this hour. At the same time, 10-year bond yields are back down to 4.244% while Oil (WTI) is off a third of a percent to $86.38 per barrel in early trading.

The major economic news scheduled for Wednesday includes July Imports, July Exports, and July Trade Balance (all at 8:30 a.m.), August S&P Global Composite PMI and August S&P Global Services PMI (both at 9:45 a.m.), August ISM Non-Mfg. Employment, August ISM Non-Mfg. PMI, and August ISM Non-Mfg. Price Index (all at 10 a.m.), Fed Beige Book (2 p.m.), and API Weekly Crude Oil Stock Report (4:30 p.m.). The major earnings reports scheduled for before the open are limited to CNM. However, after the close, AEO, PLAY, and GME report.

In economic news later this week, on Thursday, Weekly Initial Jobless Claims, Q2 Nonfarm Productivity, Q2 Unit Labor Costs, EIA Crude Oil Inventories, and Fed Balance Sheet are reported. We also have 3 Fed speakers (Harker at 10 am, Williams at 3:30 pm, and Bowman at 4:55 pm). Finally, on Friday there are no major economic news reports.

In terms of earnings reports later this week, on Thursday, we hear from ABM, DOOO, DBI, KFY, SAIC, TTC, DOCU, and RH. On Friday, KR reports.

In China news, last week, while US Commerce Sec. Raimondo was visiting, China unveiled the latest Huawei smartphone. A Canadian analyst firm acquired and tore one down. What they found was that China has made a massive leap in capability. The Huawei phone uses a Chinese-made 7nm chip that was created using UEV (extreme ultraviolet lithography). Prior to this, the most advanced chip China was known to create was 14nm and even the top Western companies only began using UEV lithography in 2019. 7nm still only yields 50% (half the chips made are bad), but this all means China is only one generation behind the West (TSM and INTC for example) rather than previous expectations that China was 3-4 generations behind. It also means that the sanctions dating back to 2020, and greatly expanded by President Biden, have either been circumvented or made irrelevant by Chinese internal development. Elsewhere, overnight China announced it will increase its support of the property sector. This caused Chinese property developer stocks to spike higher with Evergrande up 83% and Sunac China Holdings up 68%.

In miscellaneous news, Oil settled at a 10-month high on Tuesday after both Russia and Saudi Arabia announced they are extending their voluntary supply cuts through the end of the year. (Markets had expected another 1-month extension…not the 3-month extension announced.) The continued strength of the US Dollar also helped oil, as bond rates rose again Tuesday (on a post-holiday flood of investment-grade corporate bonds that took away Treasury buyers and thus drove up bond yields). Elsewhere, Turkey’s President Erdogan ended his talks with Russia’s Putin with any public progress on resuming the “Grain deal.” Still, Erdogan said it would soon be possible to revive the deal and get Ukrainian grain to market.

With that background, it looks like the Bears are looking to start the shortened week with a move lower. DIA even retested its T-line (8ema) in the premarket. However, it has the strongest early session candle bouncing up off the level while the other two major indices are giving us indecisive gap-down candles so far. The trend remains bullish with all three major index ETFs above a rising T-line, 17ema, and 50sma. As far as extension goes, none of the major index ETFs are too far extended from their T-line and the T2122 indicator is sitting right at the upper edge of the midrange (or just outside of overbought territory if you prefer). So, both sides have the room to run, if they can muster the momentum.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Conflicting jobs data, rising bond yields, and Fed member hawkish speeches have not stopped the market and the talking heads from predicting the Fed’s actions pushed stocks higher last week with high hopes they will be right this time. China and European economies continue to raise uncertainties as does the changing habits of U.S. consumers as energy, food, & housing prices continue to rise. We have a light week of earnings and economic reports this week so expect anything in price action with a sensitivity to the news cycle.

Asian markets mostly declined overnight as Australia held interest rates with health care and real estate dragged markets down. European markets trade mixed this morning as the eurozone PMI figures were revised lower changing investor early sentiment. U.S. futures chop around the flatline facing a light week of data as worldwide economic uncertainty mutes last week’s relief rally follow-through.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday include AVAV, CRMT, BRC, GTLB, & ZS.

News & Technicals’

Baidu, the Chinese tech giant and the leader in artificial intelligence (AI), has announced some of its latest achievements and products based on generative AI at an event on Tuesday. Generative AI is a type of AI that can create new content or data from existing ones, such as images, text, audio, or video. One of the products that Baidu showcased was an AI-powered tool that is integrated with its cloud service, which is similar to Google Drive. This tool can help users generate various types of documents, such as resumes, contracts, reports, and summaries, based on their needs and preferences. Baidu said that more than 6 million users have used this tool so far. Another product that Baidu demonstrated was a generative AI-based system that can assist with different scenarios, such as traffic management, financial research, and coal mine logistics. For example, the system can generate optimal traffic plans, financial reports, and coal transportation schedules based on the input data and the objectives. Baidu also mentioned that ChatGPT, a generative AI-powered chatbot developed by OpenAI, a research organization backed by Microsoft, is not officially available in China, where Google and Facebook are banned. ChatGPT is a chatbot that can produce humanlike responses to any input and has gained popularity and controversy around the world.

Mercedes and BMW, two of the most renowned German automakers, have unveiled their new electric vehicle (EV) concepts at the IAA auto show in Munich. The Mercedes-Benz Concept CLA Class and the BMW Vision Neue Klasse are the latest models that showcase the future of EV design and technology from the two brands. These cars are built on entirely new platforms that will support both their EV offerings for the coming years. This is a sign of the most aggressive push into the EV market from Mercedes and BMW, as they aim to compete with Tesla, the current leader in the EV industry. The Mercedes-Benz Concept CLA Class is a sleek and sporty four-door coupe that features a minimalist interior, a large touchscreen, and a high-performance battery. The BMW Vision Neue Klasse is a compact and elegant sedan that combines a spacious cabin, a digital dashboard, and an efficient drivetrain. Both cars are expected to go into production by 2025.

North Korea and Russia are strengthening their military and political ties, as Moscow seeks to acquire more weapons amid the ongoing war in Ukraine. According to the data I found, North Korea and Russia have recently held several meetings and joint exercises, signaling their closer cooperation and mutual support. For example, in August 2023, North Korea’s leader Kim Jong-un met with Russia’s President Vladimir Putin in Vladivostok, where they discussed regional security issues and economic cooperation. In September 2023, North Korea and Russia conducted a joint naval drill in the Sea of Japan, where they practiced anti-submarine warfare and missile defense. These moves indicate that North Korea and Russia are trying to counter the influence and pressure of the United States and its allies in the region, as well as to boost their defense capabilities. North Korea is also hoping to get more economic and humanitarian aid from Russia, as it faces severe sanctions and food shortages. Russia, on the other hand, is looking to expand its arms market and access to North Korea’s natural resources. The growing alliance between North Korea and Russia poses a challenge and a threat to the stability and security of Northeast Asia and beyond.

Stock markets ended slightly higher on Friday, continuing the positive mood of the week that was driven by optimism about the economy and the Fed’s actions. Interest rates also went up, with the 10-year Treasury yield near 4.2%. However, the bond market this week saw a decline in rates from last week’s 2023 highs, as the market expected fewer rate hikes from the Fed. Oil and gold prices rose, while sectors, such as energy, materials, financials, and industrials, led gains. To kick off a short trading week light day of earnings and economic reports with bond yields rising as economic uncertainty weighs on investors. Expect price volatility to continue as traders and investors continue trying to guess the Fed’s next actions despite their year-long poor track record in doing so.

On Friday, markets opened higher, gapping up 0.62% in the SPY, up 0.62% in the DIA, and up 0.67% in the QQQ. However, that was the last we saw of the Bulls with all three major index ETFs selling off until about noon. (QQQ had faded its morning gap by 10:35 am while SPY and DIA faded their own gaps by 11:50 am.) From that low of the day at noon, the SPY and DIA drifted slowly and slightly higher the rest of the day (closing back inside the opening gap area) as QQQ rode waves sideways and did not quite reach the Thursday close level at the end of the day. This action gave us a gap-up, inside day, black-body Spinning Top in the DIA. At the same time, we got a gap-up, black-bodied candle in the SPY. Meanwhile, the QQQ printed a gap-up, Dark Cloud Cover signal. All three remain above their T-line (8ema) and did not even retest those levels. The same goes for the DIA not retesting its 50sma, but to be fair, DIA is not far above either average.

On the day, seven of the 10 sectors were in the green with Energy (+1.96%) far out front leading the way higher while Communications Services (-0.88%) lagged behind the other sectors. At the same time, the SPY gained 0.19%, DIA gained 0.34%, and QQQ lost 0.11%. VXX dropped 1.35% to 21.21 and T2122 climbed back up to the edge of the overbought territory at 76.92. 10-year bond yields pulled back slightly to close at 4.18% while Oil (WTI) gained 2.89% to close at $86.05 per barrel. This happened on modestly below-average volume in all three of the major index ETFs. So, the bullish trend of the week continued but it felt tepid with a strong gap in one direction and then trading the rest of the day that went back the other way.

The major economic news reported Friday included August Average Hourly Earnings which rose a bit less than expected at +4.3% (year-on-year), compared to a forecast of +4.4% and the July reading of +4.4%. It is worth noting that the month-on-month Avg. Hourly Earnings also came in a bit below forecast at +0.2% versus both a forecast of +0.3% and the July value of +0.3%. At the same time, August Nonfarm Payrolls grew more than predicted at +187k (compared to a forecast of +170k and the July reading of +157k). Meanwhile, August Private Nonfarm Payrolls were reported much stronger than anticipated at +179k (versus a forecast of +150k and a July value of +155k). The August Participation Rate increased to 62.8% (compared to the forecast and July numbers which were both 62.6%). This drove a jump in the August Unemployment Rate to 3.8% (from the forecast and July readings which were both 3.5%). Later the August S&P US Mfg. PMI came in at 47.9 (better than the 47.0 forecasted but lower than the July 49.0 value). Then the August ISM Mfg. PMI was better than expected at 47.6 (versus a forecast of 47.0 and a July reading of 46.4). At the same time, the August ISM Mfg. Price Index was reported well above predicted at 48.4 (compared to a 43.9 forecast and a 42.6 July reading). So, to summarize, wages grew by slightly less than expected and jobs were also up much more than expected. However, a pop in participation led to a pop in the unemployment rate. Bloomberg characterized this as a “controlled cooling.” Meanwhile, manufacturing was better than anticipated but still contracting both in the US and globally.

In stock news, on Friday, the Wall Street Journal reported that Saudi Aramco is now strongly considering issuing a $50 billion secondary before the end of the year. If done, this would essentially double the world’s largest oil company’s outstanding shares. This seems a bit odd since the company just increased dividend payouts by $10 billion in August. However, the $50 billion will be used to bolster the Saudi sovereign wealth fund (which is a major investor in US markets). Later, HOOD announced it would buy a block of stock formerly owned by Sam Banman-Fried (disgraced “wunderkind” indicted on crypto fraud and conspiracy charges). The block was seized by the US government in November and is now held by the US Marshal Service. The sale will be for $605.7 million or $10.96/share. Elsewhere, entertainment stocks took a hit Friday as a major contract dispute between DIS and CHTR (second-largest cable TV provider) over the television distribution fees of their deal. Later, TSLA announced a new, restyled Model 3 in China with a higher price. At the same time, TSLA slashed the price of its premium vehicles, which include the “Full Self-Driving” software, by 14%-21%. After the close, the New York Times reported that META may allow Facebook and Instagram users in Europe to pay in order to avoid getting advertisements on its platform.

In stock legal and regulatory news, on Friday, the NHTSA announced that F will recall 169k vehicles to replace rearview cameras, update software on some cameras left in place, and will take a $270 million charge as a result. Later, the FTC approved the AMGN $27.8 billion acquisition of HZNP. This comes after the FTC ended its lawsuit to block the deal. To obtain the agreement, AMGN agreed not to bundle its own drugs with those from HZNP. Elsewhere, HUM joined the list of big pharma companies who are suing the US government. In this case, HUM does not want Medicare to claw back billions of dollars of overcharges after audits found prescriptions for medications for conditions that are not even listed in the patient’s medical records. HUM claims the rule allowing the clawbacks is “arbitrary and capricious.” The Biden Administration says the clawbacks will save $4.7 billion over 10 years. At the end of the day, NVS also sued the Dept. of Health and Human Services, hoping to prevent Medicare from negotiating drug prices for its 66 million enrollees. One of NVS’s top-selling drugs (Enestro) was on the list of 10 drugs Medicare announced it would be negotiating prices on (as opposed to just accepting whatever the drug maker wants as it is now). After the close, the US government sued EIX for negligence that led to a 2020 fire near Los Angeles, which burned 180 square miles.

In major IPO news, ARM revised its filing and is now pricing the much-anticipated chip stock between $47 and $51 per share. Although this IPO is expected to raise around $5 billion, with SoftBank retaining 90.6% of the stock. (The IPO underwriters do have the option to up to an additional $735 million of the stock, which would reduce SoftBank’s stake to 89.9%.) FWIW, ARM is the architecture AAPL chose when it replace INTC chips with so-called AAPL-designed chips and ARM is the only real competitor to the x86 chip architecture used by the industry leaders INTC and AMD.

Overnight, Asian markets were mostly in the red. Japan (+0.30%), India (+0.24%), and Taiwan (+0.01%) managed to hold onto green while Hong Kong (-2.06%), Shanghai (-0.71%), and Shenzhen (-0.67%) led the region lower. In Europe, we see a similar picture taking shape with only four of the 15 bourses in the green at midday. The CAC (-0.39%), DAX (-0.24%), and FTSE (+0.09%) are typical of the region in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a red start to the day. The DIA implies a -0.09% open, the SPY is implying a -0.22% open, and the QQQ implies a -0.42% open at this hour. At the same time, 10-year bond yields are up briskly to 4.23% and Oil (WTI) is off by a third of a percent to $85.27 per barrel.

The only major economic news scheduled for Tuesday is July Factory Orders (10 a.m.). There are no major earnings reports scheduled for before the open. Then, after the close, the only earnings report that might be considered major is ZS.

In economic news later this week, on Wednesday we get July Imports, July Exports, July Trade Balance, August S&P Global Composite PMI, August S&P Global Services PMI, August ISM Non-Mfg. Employment, August ISM Non-Mfg. PMI, August ISM Non-Mfg. Price Index, Fed Beige Book, and API Weekly Crude Oil Stock Report. Then Thursday, Weekly Initial Jobless Claims, Q2 Nonfarm Productivity, Q2 Unit Labor Costs, EIA Crude Oil Inventories, and Fed Balance Sheet are reported. We also have 3 Fed speakers (Harker at 10 am, Williams at 3:30 pm, and Bowman at 4:55 pm). Finally, on Friday there are no major economic news reports.

In terms of earnings reports later this week, on Wednesday, CNM, AEO, PLAY, and GME report. Then Thursday, we hear from ABM, DOOO, DBI, KFY, SAIC, TTC, DOCU, and RH. On Friday, KR reports.

In miscellaneous news, the National Federation of Retailers said that their surveys lead them to predict there will be record back-to-school spending of $135 billion this year. That is up $24 billion (a 21.8% increase over 2022). Elsewhere, the industry group that represents large private hedge funds filed suit against the SEC on Friday, claiming the agency went too far in requiring them to disclose their expenses and preventing them from giving different investors different deals (sweetheart deals). Oddly, the group filed suit in New Orleans, so there was probably some judge shopping going on there. Finally, a reminder that we have 9 days until the current UAW contracts with F, GM, and STLA expire. Given the nature of brinksmanship, expect a lot of stories on this topic and the possibility of a major strike over those 9 days.

In world economic news, Bloomberg reported Friday that US corporate profits are on the rise again for the second straight quarter. Profits rose 4.5% in Q2 according to data from the Bureau of Economic Analysis. Their report showed US corporate profits grew from 13.8 percent to 14.3 percent of GDP in the second quarter. So, in the US we are seeing what may be a “controlled cooling” with an extremely strong job market, and corporate profits on the rise. (It is worth noting that GS has now lowered the probability of a US recession to 15%, down from 20% and far below the cycle-high probability of 60%.) However, in Europe, things are not as rosy. Inflation there is much worse than in the US and is remaining higher (stickier) due primarily to energy prices. At the same time, EU economic growth continues to be very weak leading many to start talking about potnetial “stagflation” in Europe. Meanwhile, in China, the picture is grim. The Chinese are now experiencing a banking sector that is under siege from a real estate crisis, and is also seeing widespread unemployment (especially among youth).

With that background, it looks like the Bears are looking to start the shortened week with a move lower. DIA even retested its T-line (8ema) in the premarket. However, it has the strongest early session candle bouncing up off the level while the other two major indices are giving us indecisive gap-down candles so far. The trend remains bullish with all three major index ETFs above a rising T-line, 17ema, and 50sma. As far as extension goes, none of the major index ETFs are too far extended from their T-line and the T2122 indicator is sitting right at the upper edge of the midrange (or just outside of overbought territory if you prefer). So, both sides have the room to run, if they can muster the momentum.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service