Stock futures climbed on Monday as Wall Street prepared for a bustling week of tech giant earnings and economic data releases. The recent slowdown in the tech sector has weighed on broader market indexes, but the resurgence in small-cap stocks has provided a positive counterbalance. This week’s earnings reports, particularly from tech giants like Microsoft, Meta Platforms, Apple, and Amazon, will be crucial in determining if tech stocks can rebound. Investors are keenly watching these developments to gauge the market’s direction and overall economic health.

European markets started the week on a positive note, buoyed by investor reactions to recent U.S. inflation data. As market participants digest these figures, they are also gearing up for a busy week filled with earnings reports and crucial central bank meetings. The upcoming policy meetings of the Federal Reserve and the Bank of England are particularly in focus, as investors seek clues on the future direction of interest rates.

The upcoming week is set to be pivotal for major Asian economies, with a series of significant economic data releases on the horizon. Japan, China, and South Korea will be in the spotlight, starting with the Bank of Japan’s anticipated rate hike at its July 30 meeting, as forecasted by a Reuters poll of economists. Additionally, China’s July Purchasing Managers’ Index (PMI) will provide insights into the country’s manufacturing and service sectors. Meanwhile, Australia is poised to release its latest inflation figures, which will be closely scrutinized ahead of the Reserve Bank of Australia’s monetary policy meeting on August 6.

Economic Calendar

Earnings Calendar

Notable reports for Monday before the bell include, AMG, CTRI, CAN, HOPE, IART, MCD, OIS, ON, & RVTY. After the bell include, AMKR, BYON, CHK, CNO, CDP, CORT, CR, CWK, CVI, PLOW, ESI, EQR, FFIV, FLS, HLIT, HOLX, KFRC, LSCC, LTC, NEO, PCH, SAFE, SANM, SBAC, ST, SFM, TLRY, TRNS, VRNS, WELL, & WWD.

News & Technicals’

President Biden has introduced a series of reform proposals aimed at overhauling the Supreme Court, which include implementing term limits for justices and establishing a more stringent ethics code. In response to the Supreme Court’s recent ruling that granted Donald Trump immunity for “official acts” committed during his presidency, Biden is also advocating for a constitutional amendment to ensure that presidents are not immune from criminal prosecution for any crimes committed while in office. With less than six months remaining in his presidency, Biden emphasized that overhauling the Supreme Court will be a key priority.

Shares of Philips surged in early trading on Monday following the company’s announcement of better-than-expected second-quarter earnings. The Dutch device maker reported a 2% increase in comparable group sales, reaching 4.5 billion euros ($4.88 billion), driven by robust demand in North America. However, sales in China declined, which the company attributed to Beijing’s push for self-sufficiency in critical technologies, including healthcare. Despite the dip in China, the strong performance in other regions helped boost investor confidence.

During his keynote speech at the 2024 Bitcoin Conference, Donald Trump refrained from committing to the establishment of an official U.S. bitcoin strategic reserve currency. Instead, he pledged to maintain the current level of bitcoin holdings that the U.S. has accumulated through the seizure of assets from financial criminals. Trump’s stance was notably more conservative compared to RFK Jr.’s proposal, which advocates creating a 4 million bitcoin strategic reserve to parallel the government’s existing gold reserves.

A range of fast-food chains, including McDonald’s and Taco Bell, have introduced $5 meal deals to lure back customers who have been deterred by rising menu prices. These discounts are aimed at attracting low-income consumers who have been particularly affected by the price hikes. However, investors remain cautious, questioning whether these value meals can significantly boost sales without negatively impacting profit margins. The success of this strategy will depend on balancing customer appeal with financial sustainability.

Traders should plan for a wild week of price action with tech giant earnings reports, central bank decisions around the world including an FOMC decision Wednesday as well as several jobs reports that will culminate with Friday employment situation report. Emotional price gaps are likely and traders should watch for whipsaws as these highly anticipated report results are revealed.

Markets were volatile Thursday, giving us great whiplash moves. SPY opened flat at +0.02%, DIA opened down 0.03%, and QQQ opened 0.05% higher. At that point, SPY and QQQ sold off sharply until 10:15 a.m. when they hit the lows of the day. Then they both reversed and rallied hard back across the open to the highs of the day at 1:15 p.m. However, then they both reversed again selling off hard again trying to reach the lows again, but coming up just a little short. Meanwhile, DIA just rallied after its open, also reaching the highs of the day at 1:15 p.m. Then it too sold off, but not quite as strongly as the other two major index ETFs. This action gave us a black-bodied, large-bodied Spinning Top candle in QQQ, a black-bodied, large Inverted Hammer in the SPY, and a white-bodied Inverted Hammer in the DIA.

On the day, six of the 10 sectors were in the green with Industrials (+1.09%) out front leading the gaining sectors higher. On the other side, Technology (-0.76%) was again the worst-performing sector. At the same time, SPY fell 0.52%, DIA gained 0.21%, and QQQ fell 1.10%. VXX climber just a bit to 49.59. Meanwhile, T2122 spiked back up into the upper half of its mid-range at 59.11. On the bond front, 10-year bond yields fell to close at 4.246% and Oil (WTI) gained 0.68% to close at $78.12 per barrel. This happened on above-average volume in the QQQ and average volume in the SPY and DIA. So, Thursday saw a continuation of the sharp selloff in SPY and QQQ. However, DIA held its ground after the rough week or so. If there was any upside for Bulls, it would be that the QQQ closed on its long-term uptrend line dating back to October.

The major economic news scheduled for Thursday included Weekly Initial Jobless Claims, which came in just below predictions at 235k (compared to a forecast of 237k and the prior week’s 245k). For the ongoing side, Weekly Continuing Jobless Claims were also better than expected at 1,851k (versus a forecast of 1,860k, which was also the prior week’s value). At the same time, June Core Durable Goods Orders showed a jump of +0.5% (compared to a forecasted +0.2% and the far better than May’s -0.1%). On the headline number, June Durable Goods Orders showed a large and unexpected decline of -6.6% (versus a forecast calling for +0.3% and May’s +0.1% reading). I’ve got no idea how the core and headline numbers on that work together. In terms of Preliminary Q2 PCE Prices, they were up 2.90% (compared to a +2.70% forecast but down from June version’s +3.70%). At the same time, Preliminary Q2 GDP was much stronger than anticipated at +2.80% (versus a +2.0% forecast and a June value of +1.4%). In terms of prices, the Preliminary Q2 GDP Price Index was not as high as was expected at +2.3% (compared to the +2.6% forecast and well down from the June +3.1% reading). Finally, after the close, the Fed Balance Sheet showed a modest decline of $3 billion for the week, down to $7.205 trillion from the prior week’s $7.208 trillion value.

After the close, ALSN, AJG, ASB, BKR, BYD, CINF, COLB, FIX, DECK, EIX, ENIC, ENSG, ERIE, FIBK, HIG, LHX, LPLA, DOC, SKYW, SSNC, TXRH, UCTT, and VLTO all reported beats on both the revenue and earnings lines. Meanwhile, ATR, COLM, DXCM, DLR, EMN, EGO, FBIN, MTX, MHK, NSC, and TFII missed on revenue while beating on earnings. On the other side, TBBK, SAM, and PFG beat on revenue while missing on earnings. However, BTE, JNPR, OLN, SKX, WY, and WKC missed on both the top and bottom lines.

In stock news, on Thursday, WBD stock fell 5.67% after it failed to renew its NBA broadcast rights contract (on its TNT channel). (WBD indicated it intended to sue after the league rejected its offer to match the bid from AMZN.) At the same time, Reuters reported that iPhone sales in China during Q2 fell 6.7% while Chinese rival Huawei saw its China phone sale surge by 10%. Later, AAL lowered its annual revenue forecast, citing a poor sales strategy. At the same time, INST announced it had agreed to be acquired by KKR for $23.60 per share or $4.8 billion. Later, VLO announced it plans to run its refineries at 92% of capacity in Q3. This is down from the 94% VLO operated at during Q2 and well below its previously-announced plan to operate at more than 95% of capacity.

Meanwhile, Reuters reported that TSLA CEO Musk intends to ask the board of TSLA to make a $5 billion investment into his xAI startup company. Later, BAC announced its payments app had handled a record $500 billion in payments by mid-year. At the same time, in Canada, WMT announced it will invest $53 million to increase the wages of 40,000 Canadian workers. Later, Bloomberg reported that GM intends to begin charging for Cruise robotaxi rides in early 2025. At the same time, LUV announced it will end its long-standing “open seating” policy as the airline seeks to improve earnings by instituting seating price tiers. Later, OpenAI announced it is now testing a direct competitor to GOOGL and to a much lesser extent MSFT (which is a also ran in the market in question) search engines called SearchGPT.

In stock legal and governmental news, on Thursday, Reuters reported multiple sources tell it META will be hit with its first EU antitrust fines within a few weeks. The fines are for META tying classified advertisements service Marketplace with its Facebook social network. (The fine could be as much as $13.4 billion, which is 10% of its 2023 global revenue.) At the same time, in the UK, COIN was fined $4.5 million for breaching the British financial crimes requirements. Later, the US Dept. of justice announced that it and BA had finalized the company’s guilty plea. BA will pay at least $243.6 million in fines for breaching its 2021 agreement that allowed it to avoid charges then. At the same time, Russia reduced the speed of GOOGL’s YouTube service by 40% in order (with a threat to reduce it further to down 70%) next week) to pressure the company to reinstate blocked Russian YouTube channels.

Elsewhere, the KR $25 billion acquisition of ACI has been halted until after a trial in CO that is scheduled to start in September. At the same time, the CA Supreme Court rejected a union lawsuit, upholding the recent ballot measure that called for treating UBER and LYFT drivers as independent contractors instead of employees. Later, BAYRY (Bayer) announced a settlement where it will pay $160 million to resolve Seattle’s PCB contamination lawsuit against the company’s Monsanto unit. At the same time, a shareholder has filed suit to block the long and troubled merger (acquisition) of PARA by Skydance Media. The suit alleges the deal would cost non-voting shareholders $1.65 billion.

Overnight, Asian markets were mixed but leaned toward the green. India (+1.76%), Shenzhen (+1.45%), and Thailand (+1.10%) led the seven gainers. Meanwhile, Taiwan (-3.29%) was an outlier as it resumed trading after being closed due to typhoon for two days. That outlier was nearly 3% worse than any of the other four red exchanges. In Europe, markets lean heavily toward the green at midday with only two of the 15 bourses in the red. The CAC (+0.90%), DAX (+0.31%), and FTSE (+0.68%) lead the region higher in early afternoon trade. In the US, as of 7:00 a.m., Futures are pointing toward a strongly green open early (before PCE data). The DIA implies a +0.60% open, the SPY is implying a +0.75% open, and the QQQ implies a +0.99% open at this hour. At the same time, 10-Year bond yields are down to 4.244% and Oil (WTI) is off 0.42% to $77.95 per barrel in early trading.

The major economic news scheduled for Friday, June Core PCE Price Index, June PCE Price Index, and June Personal Spending (all at 8:30 a.m.), Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Consumer 1-Year Inflation Expectations, and Michigan Consumer 5-Year Inflation Expectations (all at 10 a.m.) are reported. The major earnings reports before the open include MMM, AB, AON, AVTR, BAH, BMY, CNC, CHTR, CL, BEN, GNTX, NWL, POR, SAIA, and TROW. There are no major earnings reports scheduled for after the close.

In miscellaneous news, on Thursday, the Pentagon announced it had found another $2 billion accounting error that had caused the value of munitions sent to Ukraine to be overvalued. (They had used replacement cost rather than depreciated value to place a price on the goods.) This effectively increases the amount the US can send Ukraine by another $2 billion. Elsewhere, attacks on French railways are causing travel chaos in Paris as the city preps for today’s opening ceremony of the Olympics. About 250k passengers will be disrupted today and more than 800k disrupted over the weekend. At the same time, a French-Swiss airport (Basel-Mulhouse) was evacuated and closed for safety reasons. Finally, in overnight news, Reuters reported that HMC plans to close a factory in China as well as temporarily halting production at another plant. The halt is part of a retooling to start producing more electric vehicles amidst heavy competition from Chinese EV rivals.

So far this morning, MMM, AFLYY, AB, BASFY, BMY, CHTR, CL, POR, TROW, and VLOWY all reported beats on both the revenue and earnings lines. Meanwhile, AVTR and CRI missed on revenue while beating on earnings. On the other side, AON, BAH, and CNC beat on revenue while missing on earnings.

With that background, it looks as if the Bulls are looking to start Friday with a significant gap higher. All three major index ETFs began the premarket with a gap up and have followed through with white-bodied candles. Only QQQ has wicks on its early session candle, indicating less indecision among the DIA and SPY early. DIS is even retesting its T-line (8ema) from below having crossed above in the premarket. However, with all that said, we are still an hour away from the PCE Inflation data that could rock the boat (which just don’t know in what direction). So, after a rough four days in the market, it appears the Bulls have some momentum very early on a Friday. The short-term trend remains Bearish. Meanwhile, in the mid-term and longer-term, there is no way to look at markets except to say they remain very bullish and still not all that far from all-time highs. In terms of extension, even considering the premarket move higher, QQQ is stretched below its T-line. At the same time, the T2122 indicator is now in its mid-range. Therefore, overall, this means the market still has room to run in either direction if the market can find momentum. With regard to those 10 big dog tickers, all 10 are solidly or strongly in the green in the early session with AMD (+2.39%) and NVDA (+2.31%) leading the group higher on strong moves and good volume. Meanwhile, GOOGL (+0.41%) is the laggard, having moved less than half as much as the next lowest performer MSFT (+0.87%).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

U.S. will release key data on gross domestic product and initial jobless claims, which are highly anticipated by market watchers. Economic concerns intensified on Wednesday when former New York Fed President William Dudley advocated for lower borrowing costs, ideally at the upcoming meeting. Analysts have expressed worry that such a move might signal a sense of urgency among officials to stave off a potential recession.

European markets experienced a downturn amid a wave of corporate earnings reports. Notably, results from Nestle SA and Gucci owner Kering SA indicated a reduction in consumer spending across various sectors, from essential food items to luxury handbags. This trend reflects growing economic caution among consumers. Additionally, upcoming data releases on German consumer confidence and business activity in the euro zone and the U.K. are anticipated.

China’s central bank recently reduced the medium-term facility lending rate from 2.5% to 2.3%, following a prior cut in loan prime rates earlier in the week. This move aims to stimulate economic activity amid ongoing challenges. Meanwhile, South Korea’s GDP grew by 2.3% year-on-year, falling short of the 2.5% growth anticipated by economists polled by Reuters. On a quarterly basis, South Korea’s economy contracted by 0.2%, contrary to the expected 0.1% increase.

Unilever shares surged on Thursday morning following the company’s announcement of an increased full-year margin guidance. Additionally, Unilever confirmed that the spinoff of its ice cream business remains on schedule for completion by the end of 2025. The company reported underlying price growth of 1% in the second quarter of this year, a significant decrease from the 8.2% growth recorded in the same period of 2023. This update reflects Unilever’s strategic adjustments and market performance amid evolving economic conditions.

Ford Motor fell short of Wall Street’s second-quarter earnings expectations, despite surpassing revenue forecasts. The shortfall was primarily due to persistent warranty costs that have troubled the automaker for several years. In response, Ford raised its target for free cash flow but chose to maintain its 2024 earnings guidance. This decision left some investors disappointed, as they had anticipated an upward revision in earnings projections.

Auto giant Stellantis reported a first-half net profit of 5.6 billion euros ($6.07 billion), marking a significant 48% decline compared to the same period in 2023. Stellantis CEO Carlos Tavares attributed the disappointing performance to a challenging industry environment and internal operational issues. He acknowledged that the company’s results for the first half of 2024 fell short of expectations, underscoring the difficulties faced by the automotive sector in navigating current economic conditions.

Chipotle Mexican Grill reaffirmed its full-year outlook for same-store sales growth, signaling confidence in its ongoing performance. The restaurant chain exceeded Wall Street’s expectations for both quarterly earnings and revenue, showcasing its robust financial health. Additionally, Chipotle reported an impressive 8.7% increase in restaurant traffic during the second quarter, highlighting the brand’s continued popularity and effective customer engagement strategies.

The release of key data such as Durable Goods, GDP, International Trade and Jobless Claims will likely set the tenor of the morning. With the data give the bulls what’s needed to inspire a relief rally, or will the bears gain energy to follow-through with yesterday’s attack? We will soon find out but traders should plan for whipsaws and possible big point moves so plan your risk accordingly.

Tuesday saw similar movement across all three major index ETFs, but with different magnitudes. SPY opened down 0.02%, DIA opened up 0.04%, and QQQ opened down 0.17%. From there, all three meandered back-and-forth around the “gaps” with SPY and DIA moving in a 0.50% range while QQQ moved in a 0.85% range. This was only interrupted by a selloff the last 10 minutes across all three major index ETFs. This action gave us black-bodied, inverted Hammer type candles in the SPY, DIA, and QQQ. SPY and QQQ both retested their T-line (8ema) from below and failed the test during the day. Meanwhile, DIA retested its own T-line from above and fell through by just four cents. (So, it’s still a test in progress.)

On the day, six of the 10 sectors were in the red with Energy (-1.26%) way out front leading the market lower. On the other side, Financial Services (+0.31%) held up better than the other sectors. At the same time, SPY fell 0.16%, DIA fell 0.16%, and QQQ fell 0.35%. VXX fell 0.82% to close at a very low at 10.83. T2122 fell a bit, climbed just a bit further into its overbought range at 85.97. On the bond front, 10-year bond yields closed at 4.253% and Oil (WTI) continued to fall, down another 1.19% to close at $77.47 per barrel. This all happened on far below-average volume in the SPY, DIA and QQQ. So, Tuesday saw a pause after Monday’s gains. continuation of the pullback from all-time highs with QQQ leading, SPY in the middle, and DIA following (just as it did on the way up).

The major economic news scheduled for Tuesday included June Existing Home Sales, which came in light at 3.89 million (compared to a forecast of 3.99 million and the May reading of 4.11 million). Then, after the close, API Weekly Crude Oil Stocks showed a much larger drawdown than expected at -3.900 million barrels (versus a forecasted build of 0.700 million barrels but less of a drawdown that the prior week’s -4.440 million barrels).

After the close, GOOGL, AGR, CALM, CB, EWBC, ENVA, GOOG, MTDR, PKG, RRR, STX, and TXN all reported beats on both the revenue and earnings lines. Meanwhile, CSGP, EQT, MAT, RRC, and V missed on the revenue line while beating on earnings. On the other side, NBR and TSLA beat on revenue while missing on earnings. However, CNI, COF, and WFRD missed on both the top and bottom lines.

In stock news, on Tuesday, KMB, KO, PM, SHW, HCA, GM, LMT, and even UPS (despite reporting its Q2 miss) raised their annual guidance. Later, tech industry magazine Information reported that AAPL is working on a foldable iPhone with a planned release date in 2026. At the same time, GM announced it has delayed plans for a self-driving version of the Chevrolet Bolt without a steering wheel. (In 2022, GM have petitioned the NHTSA to allow deployment of 2,500 self-driving vehicles without human controls.) Later, META released a new version of its Llama AI model, the biggest (largest training data set) model it has released to date. At the same time, IEX announced it will buy private firm Mott Corp for $1 billion in cash. (The move would improve IEX’s presence in the medical technologies industry.) Later, cybersecurity startup Wiz ended talks with GOOGL related to the tech giant’s $23 billion deal to acquire the Israeli firm. Meanwhile, German private firm Robert Bosch announced it had agreed to buy JCI’s residential ventilation business for $8 billion. After the close, BA announced it has resumed deliveries of 737 MAX jets to China.

In stock legal and governmental news, on Tuesday, AMZN unit Whole Foods reported it had reached a settlement in a lawsuit filed against it alleging the company fired an employee over refusing to remove a Black Lives Matter facemask. Terms of the deal were not disclosed. At the same time, the NHTSA announced that STLA has recalled 19,516 hybrid mini-vans in the US over fire potential from a battery pack, advising any customers to park the vehicles outside until they are repaired. Later, Italy seized $131 million from the Italian unit of AMZN over alleged tax fraud and illegal labor practices. At the same time, the US FTC has launched an investigation into individual pricing based on previous purchase history, consumer location data, and other personal data. The FTC has asked MA, JPM, and six other companies to provide information on their “targeted pricing” practices. The FTC is also seeking information from software providers and consultancies involved in implementing such systems.

Elsewhere, the FAA launched a safety review of LUV after a series of near-misses involving their planes. At the same time, the US Dept. of Transportation announced it has opened a probe into DAL related to the more than 5,000 flights the carrier has canceled due to the global cyber outage last Friday. (DAL had canceled 30% of its flights Friday through Monday and 13% of its flights Tuesday, while other airlines recovered much more quickly.) Among the complaints from stranded passengers was phone agent wait times of well over 12 hours for those trying to reroute. After the close, the state of CO announced it has ramped up its response to bird flu and now requires dairies to test their milk every week following outbreaks and many cases of bird to cow transmission in the state. (CO found 47 cattle herds that have been infected so far, with 60% of those coming in the last month. This comes after 3.1 million chickens were culled or died of the disease in that state.)

Overnight, Asian markets were mostly red. Only Taiwan (+2.76%), the region’s biggest mover and New Zealand (+0.85%) were in the green. Meanwhile, Shenzhen (-1.32%), Japan (-1.11%), and Hong Kong (-0.91%) led the rest of the region lower. In Europe, we see a similar picture taking shape with only three of the 15 bourses in the green at midday. The CAC (-1.00%), DAX (-0.71%), and FTSE (-0.19%) lead the region lower in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a gap lower to start the day. The DIA implies a -0.45% open, the SPY is implying a -0.78% open, and the QQQ implies a -1.15% open after TSLA’s fourth consecutive quarterly miss. At the same time, 10-Year bond yields are just on the green side of flat at 4.24% and Oil (WTI) is up nearly one percent to $77.71 per barrel in early trading.

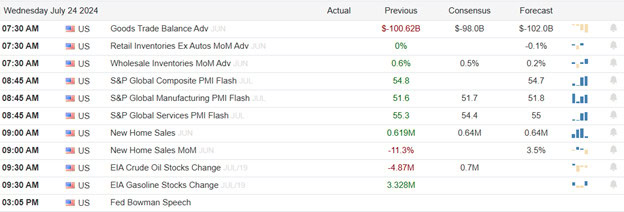

The major economic news scheduled for Wednesday includes, Building Permits, June Goods Trade Balance, and June Retail Inventories (all at 8:30 a.m.), S&P Global Mfg. PMI, S&P Global Services PMI, S&P Global Composite PMI, and June New Home Sales (all at 10 a.m.), and EIA Weekly Crude Inventories (10:30 a.m.). Fed Governor Bowman also speaks at 4:05 p.m. The major earnings reports before the open include Wednesday, we hear from, ALLE, APH, T, BSX, CHKP, CME, EQNR, EVR, FI, FLEX, FMX, FTV, GEV, GD, GPI, IP, IPG, KBR, LW, LII, NEE, ODFL, ORAN, OTIS, BPOP, PRG, RCI, ROP, TMHC, TEL, TECK, TDY, THC, TMO, TNL, VRT, and WAB. Then after the close, ALGN, AMP, ASGN, CSL, CLS, CCS, CHE, CMG, CHDN, CYH, EW, FAF, F, GL, GGG, ICLR, IBM, INVH, KALU, KLAC, KNX, LVS, MTH, MOH, NEM, ORLY, OII, PTEN, PLXS, RJF, RNR, RSG, ROL, NOW, TER, TYL, URI, UHS, VMI, WCN, WFG, WHR, WM, and WH report.

In economic news later this week, on Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, June Core Durable Goods Orders, June Durable Goods Orders, Preliminary Q2 PCE Prices, Preliminary Q2 GDP, Preliminary Q2 GDP Price Index, Preliminary Goods Trade Balance, Preliminary Retail Inventories, and the Fed Balance Sheet. Finally, on Friday, June Core PCE Price Index, June PCE Price Index, June Personal Spending, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Consumer 1-Year Inflation Expectations, and Michigan Consumer 5-Year Inflation Expectations are reported.

So far this morning, ALLE, BXMT, BSX, CHKP, CME, EVR, FI, IPG, NAVI, BPOP. SF, TMHC, THC, TMO, TNL, VRT, WNC, and WAB all reported beats on both the revenue and earning lines. Meanwhile, EQNR, GEV, GPI, IP, KBR, LII, ODFL, OTIS, RCI, ROP, TEL, TECK, and TDY all missed on revenue while beating on earnings. On the other side, GD beat on revenue while missing on earnings. However, T missed on both the top and bottom lines.

In miscellaneous news, a US District Judge in Philadelphia rejected a lawsuit seeking to block the FTC rule which prohibits “non-compete agreements” as a condition of employment. Elsewhere, the Equip. Leasing and Finance Assn. (ELFA) said Tuesday that companies borrow 4% less to finance equipment in June. (This came after double-digit growth in the borrowing the two prior months.) Later, Bloomberg reported that an Pentagon technology services provider owned by LMT was recently hacked, resulting in internal documents being stolen. (In addition to the Dept. of Defense, the Dept. of Homeland Security, NASA and numerous other agencies and foreign entities were among the customers of that LMT unit.) Meanwhile, KHC suffered a little blow when its iconic “Wienermobile” hit another car and flipped on a Chicago highway Tuesday. (Fortunately for hot dog fans, KHC has several Wienermobiles it can roll out to fill the void.)

With that background, it looks as if the Bears are in control early in the premarket. All three major index ETFs gapped down significantly to start the early session. However, they have printed small, indecisive candles since that gap lower. So, there is no unanimity of feeling among traders. All three major index ETFs are below their T-line (8ema), meaning the DIA lost its test from above as of the Tuesday close. So, the premarket looks solidly Bearish and the short-term is likewise pointing down. Meanwhile, in the mid-term and longer-term, there is no way to look at markets except to say they remain very bullish and still not far from all-time highs. In terms of extension, QQQ is getting a little stretched below its T-line by the morning gap down. At the same time, the T2122 indicator remains in the overbought area. Therefore, those mixed signals mean the market has room to run in either direction if the market can find momentum. With regard to those 10 big dog tickers, all 10 are strongly red in the early session with TSLA (-8.37%) leading by a wide margin in terms of move and dollar-volume traded early. AAPL (-0.12%) and NFLX (-0.52%) are holding up better than the other big dogs.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

U.S. futures indicated a lower opening on Wednesday as investors reacted to disappointing reports from major tech companies Alphabet and Tesla. Shares of Alphabet, Google’s parent company, dropped by 3.4%, while Tesla’s stock saw a more significant decline of over 7% due to results that fell short of expectations. This underperformance from two of the market’s leading tech giants contributed to the overall negative sentiment among investors.

European markets experienced a downturn as the earnings season intensified. Major indexes across the region, along with nearly all sectors, saw declines. Household goods stocks were particularly affected, dropping by 1.55%. In contrast, the travel and leisure sector was the only one to buck the trend, posting a modest gain of 0.62%. Additionally, flash purchasing managers’ index (PMI) data revealed that business activity in the euro zone had stalled in July.

Asia-Pacific markets experienced a downturn as traders evaluated the latest business activity data from Japan and Australia. The technology and electric vehicle (EV) sectors were notably impacted, with stocks in these areas seeing significant declines. In Australia, the private sector’s growth decelerated in July, as indicated by the composite purchasing managers index (PMI) which fell to 50.2 from 50.7 in June, according to Juno Bank.

Shares in LVMH declined on Wednesday following the release of the luxury group’s earnings for the first half of 2024. The company reported quarterly sales of 20.98 billion euros ($22.7 billion) for the second quarter, which fell short of analysts’ expectations as surveyed by LSEG. Additionally, LVMH disclosed that sales in Asia, excluding Japan, dropped by 14% in the second quarter compared to the same period last year. This underperformance in a key market contributed to the overall negative reaction from investors.

Tesla CEO Elon Musk recently posted an informal poll on social network X, inquiring whether his publicly traded automaker should invest $5 billion into his latest startup, xAI. Established in March 2023 and first publicly discussed in July 2023, xAI focuses on developing large language models and AI products designed to compete with offerings from Google, Microsoft, and OpenAI. Musk’s companies have a history of collaboration and financial interactions, making this potential investment a continuation of his integrated business strategy.

In a Tuesday interview with CNBC’s Jim Cramer, Mattel CEO Ynon Kreiz expressed optimism about the Barbie maker’s success as an independent company. Meanwhile, a Reuters report revealed that private equity firm L Catterton, backed by luxury goods giant LVMH, has approached Mattel with a potential deal. This development highlights the ongoing interest in Mattel’s business and confidence in its prospects.

The ride-hailing company announced that Sverchek’s departure is not due to any disagreements within the company, its board of directors, or management, nor is it related to Lyft’s operations or policies. Despite the exit, Sverchek will receive severance benefits, including a cash payment of $650,000. This clarification aims to reassure stakeholders that the departure is amicable and unrelated to any internal conflicts or operational issues.

Anticipation may have become a little concern after disappointing reports from GOOG and TSLA roused the bears this morning. With a huge number of earnings reports today and tomorrow expect volatility to remain high. Add in the heavy hitting economic reports on the horizon and the stage it set for very challenging market conditions.

U.S. Equity Futures showed mixed trading as market participants shifted their attention from political developments to the ramp up earnings and beginning of big tech reports. Notably, tech giants Tesla Inc. and Alphabet Inc. are set to release their earnings reports later Tuesday, which could significantly influence market sentiment. Additionally, traders are keeping a close eye on economic indicators, with key data on nonmanufacturing activities and existing home sales expected to be released on Tuesday morning.

Europe’s Stoxx 600 Index experienced fluctuations as gains in technology and travel company shares were counterbalanced by declines in the chemicals and mining sectors. Investors are also anticipating Hungary’s latest interest rate decision, which could influence market dynamics. Additionally, upcoming data releases on Dutch and Irish consumer confidence.

China’s CSI 300 Index led declines in Asia amid mixed trading across the region. Market participants are also closely watching India, which is set to unveil its first budget under Prime Minister Narendra Modi’s third five-year term, a significant event that could shape economic policies and investor sentiment. Meanwhile, Singapore’s consumer price index for June rose by 2.4% year-on-year, surpassing Reuters’ expectations of a 2.7% increase, indicating a slightly slower pace of inflation than anticipated.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include AOS, ACI, AVY, BANC, KO, CBU, CSTM, DHR, FDP, FELE, FCX, GATX, GE, GM, GPC, HCA, HRI, IVZ, KMB, LMT, MCO, MSCI, NWBI, ONB, PCAR, PNR, PM, PII, PHM, DGX, SHW, SPOT, UPS, & WBS. After the bell include APHM, BDN, CALM, CNI, AOF, CB, CSGP, EWBC, EGP, ENVA, ENPH, EQT, FCF, GOOGL, MTDR, MAT, NBR, PKG, PFSI, RRC, RRR, RNST, ROIC, STX, TSLA, TXN, TRMK, VBTX, VIXR, V, & WFG.

News & Technicals’

Wiz has decided to walk away from a $23 billion acquisition deal with Google, which would have marked the search giant’s largest-ever acquisition. Instead, Wiz informed its employees that it will proceed with its initial plan to pursue an IPO. A person familiar with the company’s decision-making process cited concerns over antitrust issues and investor apprehensions as key factors in abandoning the potential deal. This move highlights the growing scrutiny of large tech acquisitions, and the strategic considerations companies must weigh in such high-stakes decisions.

Six senators have urged the Justice Department and the Federal Communications Commission to challenge a deal that would permit T-Mobile to utilize part of U.S. Cellular wireless spectrum. In a new letter, the lawmakers expressed concerns that such a deal could lead to higher costs for consumers, as it might result in the combination of lower-priced carriers with higher-priced ones, potentially charging consumers billions more. Additionally, the senators have requested that the Justice Department consider unwinding the merger between T-Mobile and Sprint, highlighting ongoing apprehensions about market competition and consumer pricing.

Best Buy unveiled a comprehensive strategy on Tuesday aimed at reigniting sales growth. This plan includes dedicating staff to key areas within its stores, producing more engaging videos to spark customer interest, and launching a new marketing campaign. The consumer electronics retailer is looking to capitalize on the anticipated replacement cycle of pandemic-era purchases and a surge of new innovations. In an interview with CNBC, CEO Corie Barry emphasized the company’s focus on reintroducing fresh and exciting products to attract customers and drive sales.

Shares in automaker Porsche declined on Tuesday following the company’s announcement of a reduced outlook for 2024. Porsche attributed this adjustment to a shortage of special aluminum alloys affecting several of its suppliers. This shortage is expected to impact production, potentially leading to shutdowns for certain Porsche vehicle series. The company’s revised forecast has raised concerns among investors about the potential disruptions in its manufacturing processes.

Traders will temporarily set aside political uncertainty to focus earnings, specifically the big tech reports from GOOG and TSLA coming after the bell today. Plan on high drama with these massively anticipated reports and be prepared for wild price gyrations and big morning gaps to challenge even the most experienced trader. Plan your risk carefully.

Friday saw markets open down to varying degrees. SPY opened 0.06% lower, DIA gapped down 0.31%, and QQQ opened 0.08% lower. At that point, all three major index ETFs chopped sideways for 30 minutes. However, from there, all three sold off until 2:45 p.m. and then meandered along the bottom the rest of the day. This action gave us black-bodied, large-ish candles with wicks on both ends in all three major index ETFs. DIA crossed back below its T-line (8ema) while QQQ pulled fairly far below its own T-line. SPY sits in about midway between DIA and QQQ in terms of its distance below its T-line.

On the day, eight of the 10 sectors were in the red with Technology (-0.97%) out front leading the market lower. On the other side, Healthcare (+0.24%) held up much better than the other sectors. At the same time, SPY fell 0.68%, DIA fell 0.93%, and QQQ fell 0.89%. VXX shot up 4.25% to close at a still low at 11.53. T2122 fell a bit, but remains in the center of its mid-range at 40.26. On the bond front, 10-year bond yields popped again to 4.24% and Oil (WTI) plummeted 3.08% to close at $80.29 per barrel. This all happened on average volume in the SPY, DIA and QQQ. So, again on Friday saw a continuation of the pullback from all-time highs with QQQ leading, SPY in the middle, and DIA following (just as it did on the way up).

There was no major economic news scheduled for Friday.

In economic speak news, on NY Fed President Williams said Friday that the FOMC is “getting closer” to the point where it can start cutting rates. Williams said, “I feel like the past three months—and I would include in June, based on what we’ve seen — seems to be getting us closer to a disinflationary trend that we’re looking for.” He continued, “I would like to see more data to gain further confidence inflation is moving sustainably towards our 2% goal. We’ve got a few good months now.” Later, Atlanta Fed President Bostic said that he now only expects one rate cut this year. Bostic told reporters, “The economy continues to deliver surprises and it continues to be more resilient and more energized than I had forecast, … And as a consequence, I’ve sort of re-calibrated when I think it’s appropriate to move.” Bostic continued, “We will have to see how the data comes in over the next several weeks.”

In stock news, on Friday, SERV shares spiked and closed up 187% (after being up more than 241% during the day) after NVDA disclosed it had taken a 10% stake in the company. Later, Reuters reported that OXY is in talks with Columbia’s Ecopetrol over the sale of a 30% stake in shale oil producer CrownRock by OXY for $3.6 billion. At the same time, AAL announced it had reached a tentative contract deal with the union representing 28k flight attendants after three years of negotiations. Later, Bloomberg reported that UL has begun discussions with buyout firms about the possible sale of its ice cream unit, which includes the “Ben & Jerry’s” brand. (BX is among to top firms on the potential buyer side.)

In stock legal and governmental news, on Friday, LLY announced that it had received approval for its weight loss drug tirzepatide from Chinese regulators. (NVO’s Wegovy, a competing GLP-1 weight loss drug had already been approved.) At the same time, a US District Court ruled that BKNG violated the Computer Fraud and Abuse Act by scraping data from the RYAAY website. Later, Bloomberg reported HE had reached a tentative settlement of more than $4 billion, which would resolve hundreds of lawsuits stemming from the 2023 wildfires on Maui. At the same time, Reuters reported that the EU is set to impose provisional tariffs on Chinese biodiesel due to unfairly low pricing (government subsidized). Meanwhile, ORCL agreed to pay $115 million to settle a suit alleging the company violated CA consumer privacy by collecting and selling personal data without permission.

Elsewhere on Friday, a court filing by class action law firms accused BRKB of colluding with three other law firms to convince fire victims to reach lowball settlements on suits filed against BRKB’s PacifiCorp. At the same time, the NHTSA disclosed that STLA paid $190.7 million in US fuel economy penalties for the years 2019 and 2020. In addition. STLA still owes another $459.7 million in outstanding penalties for the same infractions prior to 2021. (In 2023, STLA paid $235.5 million for the same thing covering 2018 and $156.6 million covering 2016-2017.) Later, the Fed fined GDOT $44 million for “unfair and deceptive” practices in its “prepaid debit card” services. At the close, Bloomberg reported that the FTC has opened an investigations into OXY, HES, and FANG over their communications with OPEC officials.

Overnight, Asian markets were red across the board wit the lone exception of Hong Kong (+1.25%). Taiwan (-2.68%), Japan (-1.16%), and South Korea (-1.14%) seem to have reacted poorly to Biden dropping out of the US Presidential race just hours before the Asian opens. This idea was bolstered as China made a surprise interest rate cuts in both short-term and long-term rates. (Unlike the US, China cut 7-day, one-year, and 5-year PBOC (China’s Central Bank) rates by a tenth of a percent each. However, in Europe, we see very strong green across the board at midday. The CAC (+1.33%), DAX (+1.35%), and FTSE (+0.73%) lead very broad gains of more than a percent on an initial positive reaction to Biden’s Sunday move. In the US, as of 7:30 a.m., Futures are pointing toward a strong start to the morning. The DIA implies just a +0.16% open, but the SPY implies a +0.50% open, and the QQQ implies a +0.82% open at this hour. At the same time, 10-Year bond yields are down to 4.22% and Oil (WTI) is off by half a percent to $79.72 per barrel.

There is no major economic news scheduled for Monday. The major earnings reports before the open include are limited to IQV, KSPI, TFC, and VZ. Then, after the close, ARE, BOKF, BRO, CDNS, CLF, CCK, LOGI, MEDP, NUE, NXPI, SAP, VLRS, WRB, and ZION report.

In economic news later this week, on Tuesday, we get June Existing Home Sales and API Weekly Crude Oil Stocks report. Then Wednesday, Building Permits, June Goods Trade Balance, June Retail Inventories, S&P Global Mfg. PMI, S&P Global Services PMI, S&P Global Composite PMI, June New Home Sales, and EIA Weekly Crude Inventories are reported. Fed Governor Bowman also speaks. On Thursday, we get Weekly Initial Jobless Claims, Weekly Continuing Jobless Claims, June Core Durable Goods Orders, June Durable Goods Orders, Preliminary Q2 PCE Prices, Preliminary Q2 GDP, Preliminary Q2 GDP Price Index, Preliminary Goods Trade Balance, Preliminary Retail Inventories, and the Fed Balance Sheet. Finally, on Friday, June Core PCE Price Index, June PCE Price Index, June Personal Spending, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan Consumer 1-Year Inflation Expectations, and Michigan Consumer 5-Year Inflation Expectations are reported.

So far this morning, IQV and TFC reported beats on both the revenue and earnings lines. Meanwhile, VZ missed on revenue while beating on earnings.

In miscellaneous news, after the close Thursday, a federal appeals court blocked the Biden Administration from continuing to implement a new student debt relief plan at the request of seven GOP-led states. (The Dept. of Education said it had already granted $5.5 billion in debt relief to 414k borrowers under that “SAVE” plan.) At the same time, the IMF said the US should raise taxes to reduce the US federal debt and put off any rate cut until at least late 2024. Meanwhile, mortgage finance agency Freddie Mac told Reuters Thursday that the US 30-year fixed-rate mortgages fell to the lowest rate since mid-March, with the national average down to 6.77% from the prior week’s 6.89%. Finally, Reuters reported that the state of CA reported that TSLA car registrations fell in Q2. TSLA’s 52,211 new registrations for Q2 was down and a third consecutive quarter of falling new registrations.

With that background, it looks as if the markets are enjoying the Sunday and overnight news. All three major index ETFs gapped up to start the premarket session. Since that point, SPY and QQQ have followed through with good-sized white-body candles showing no wick at this point. For its part, DIA gapped less and has given a smaller white-body candle as it retests its T-line (8ema) from below. So, the premarket looks strongly Bullish, but the short-term trend is Bearish. Meanwhile, in the mid-term and longer-term, there is no way to look at markets except to say they remain very bullish and not far from all-time highs. In terms of extension, QQQ is the most extended to the downside, but the early session action has relieve the worst of its over-done issue. At the same time, the T2122 indicator remains in the center of its mid-range. Therefore, the market has room to run in either direction if the Bulls or Bears can find momentum. With regard to those 10 big dog tickers, all 10 are strongly green in the early session with the biggest dog (NVDA, +2.06%) leading that way again both in terms of move and volume. However, the least of the big dog movers is NFLX (+0.40%).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Traders enter a new week with more election uncertainty as Biden is pushed out and Harris gets the nod with just four months to make her case. Although markets hate uncertainty S&P 500 futures saw a modest increase of 0.5%, following a challenging week where the index experienced its steepest losses since April. The shift came as investors moved away from Mega-cap technology stocks, opting instead for smaller-cap names. Meanwhile, futures for the Dow Jones Industrial Average and Nasdaq-100 also showed gains, rising by 0.2% and 0.7%, respectively. This movement indicates a cautious optimism among investors, despite recent market volatility.

On Monday, European stocks experienced an upward trend, with the pan-European Stoxx 600 index rising by 1.06% as of 11:29 a.m. London time. This positive movement was broad-based, with most sectors showing gains. However, the travel and leisure sectors were an exception, declining by 1.73%, making it the only sector in negative territory. This divergence highlights the varying performance across different industries within the European market.

Asia-Pacific markets experienced a downturn, influenced by unexpected monetary policy changes from China’s central bank. The People’s Bank of China reduced the short-term 7-day reverse repurchase rate from 1.8% to 1.7%. Additionally, the one-year and five-year loan prime rates were both lowered by 10 basis points, now standing at 3.35% and 3.85%, respectively. These rate cuts, aimed at stimulating economic activity, reflect ongoing concerns about China’s economic growth, which in turn impacted market sentiment across the region.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday before the bell include BOH, IQV, TFC, & VZ. After the bell include AGYS, AGNC, ARE, BOKF, BRO, CADE, CDNS, CALX, CATY, CLF, CCK, ELS, HSTM, MEDP, NUE, NXPI, RLI, SSD, WRB, & ZION.

News & Technicals’

On Sunday, the Atlanta-based airline faced significant operational challenges, canceling over 600 mainline flights, which accounted for approximately 17% of its schedule. This disruption was more extensive than any other U.S. airline. While most other carriers have managed to recover from similar issues, Delta continues to experience persistent disruptions, highlighting ongoing challenges within its operations.

On Monday, Ryanair shares plummeted by 12.2% as of 8:57 a.m. London time, following the company’s announcement of a 46% drop in quarterly profit after tax for the three months ending in June. The budget airline also projected lower-than-expected fares in the upcoming months, contributing to the negative market reaction. This downturn in Ryanair’s shares had a ripple effect on other European airlines, with EasyJet losing over 6%, Jet2 falling by 4%, and Hungarian airline Wizz Air sliding by more than 6%. The widespread decline underscores the broader concerns within the airline industry.

Bank of Japan officials are facing a challenging decision regarding potential interest rate hikes at their upcoming policy meeting, due to observed weaknesses in consumer spending. According to sources familiar with the matter, some officials believe that raising rates could send an overly hawkish signal, which they are keen to avoid. This internal debate highlights the delicate balance the BOJ must strike between supporting economic growth and managing inflation expectations.

In a seven-day period we had an attempted presidential candidate assassination attempt and the sitting president bow out of the run highlighting the extreme election uncertainty we face this November. Toss in the earnings season and we have the makings for very turbulent price action. GOOG will kick of the big tech reports on Tuesday with a looking GDP Thursday followed by the CORE PCE numbers Friday. Fasten your seatbelt it may prove to be a bumpy ride.

Markets gave us divergent gaps to start the day. However, by mid-morning the three major index ETFs had gotten their direction synchronized again. SPY gapped up 0.29%, DIA gapped down 0.26%, and QQQ gapped up 0.77%. However, after the gap up and bobbing around for 45 minutes, SPY sold off sharply until 12:30, bounced for an hour, and then started another leg lower. It ended the day on a modest bounce. At the same time, after its open, DIA followed-through to the upside for an hour. Then, it too also sold off sharply until 12:30, ground sideways for 75 minutes, and then started its own second leg lower, ending the day on a small 30-minute bounce. Meanwhile, after the large gap higher, QQQ immediately sold off sharply until noon, bounced significantly for 75 minutes, and then started another leg back toward the noon lows. Still, QQQ bounced more sharply than its peer EFTs over the final 40-minutes. This action gave us large-body, black candles in all three major index ETFs. SPY had wicks at both ends, failing a retest of the T-line (8ema) from below. QQQ had a wick only at the lower end and it was a larger wick than the other two had. However, DIA printed a new all-time high, leaving a large upper wick but did not even approach its own T-line from above.

On the day, all 10 sectors were in the red with Healthcare (-2.22%) way out front (by almost 0.75%) leading the market lower. On the other side, Energy (-0.06%) held up much better than the other sectors. At the same time, SPY fell 0.77%, DIA fell 1.26%, and QQQ fell 0.47%. VXX gained another 2.88% to close above 11 at a still very low at 11.06. T2122 dropped out of its overbought territory, all the way down to the center of its mid-range at 46.34. On the bond front, 10-year bond yields popped to 4.197% and Oil (WTI) fell 0.78% to close at $82.20 per barrel. This happened on heavy volume in DIA, above-average volume in QQQ, and average volume in the SPY. So, again on Thursday we saw a head fake move higher at the open. However, the Bears were in command all day after the open.

The major economic news scheduled for Thursday included Weekly Initial Jobless Claims, which came in higher than expected at 243k (compared to a forecast of 229k and the prior week’s 223k). On the ongoing side, Weekly Continuing Jobless Claims were also up and above predictions at 1,867k (versus the 1,860k forecast and the prior week’s 1,847k reading). At the same time, the Philly Fed Mfg. Index was up to 15.2 (compared to the June -2.5 value). Later, the June US Leading Economic Indicators Index was up and a tick better than anticipate at -0.2% (compared to a -0.3% forecast and May’s -0.4%). Then, after the close, the Fed’s Weekly Balance Sheet showed a $16 billion reduction, from $7.224 trillion to $7.208 trillion.

In economic speak news, on Thursday, Dallas Fed President Logan lauded progress made by the Fed in making sure that banks can tap Fed emergency liquidity if needed. Logan said, “(The Fed Discount Window) has been effective in supporting the stability of the banking and financial systems and, in turn, the flow of credit to households and businesses.” She continued, “A critical element of ensuring the safety of the banking system is making sure banks are prepared to use the discount window if circumstances call for it.” Logan said more than 5,000 deposit-taking banks have completed the paperwork to be able to access the Discount Window in a crisis. In addition, those banks have increased the pool of collateral available to back loans through the window from $1 trillion in 2023 to $3 trillion now.

After the close, DIT, ISRG, NFLX, and WAL all reported beats on both the revenue and earnings lines. Meanwhile, AIR and PPG reported misses on revenue while beating on earnings. However, SCHL missed on both the top and bottom lines.

In stock news, on Thursday, the Financial Times reported that WBD is discussing the potential to break up the company to boost stock valuations. At the same time, F laid out plans to rework a Canadian plant that had been intended to build a future electric vehicle (starting in 2025) to instead build larger, gasoline-powered F-series pickup trucks. Later, the Financial Times reported that META is in talks to purchase a 5% stake in eyewear maker ESLOF (EssilorLuxottica, which makes Ray-Ban). At the same time, Adobe Analytics said that AMZN Prime Day boosted US online retail shopping to a record $14.2 billion. This was up 11% from the event in 2023. Later, Bloomberg reported that AAPL is in talks to license more Hollywood films, in order to boost its streaming content portfolio. Elsewhere, NFLX announced it is discontinuing its cheapest “$11.99 Basic Plan” (the lowest ad-free plan). NFLX had stopped taking new Basic Plan subscriptions in January.

Meanwhile, SPWR plummeted 40% after it informed clients that it was pausing some operations. The cessations include ending some leases and power purchase agreements as well as halting new product shipping. Elsewhere, SMAR share spiked (but ended only 5.45% higher) after Reuters reported the company is considering buyout offers from private equity firms. After the close, Reuters reported that OpenAI has begun talks with AVGO over the development of a new AI chip, in an effort to overcome shortages of AI chips from NVDA and AMD. (Earlier this year, OpenAI CEO Altman made news when he announced plans to raise billions to be used to set up AI chip manufacturing plants in partnership with TSM, INTC, and Korean Samsung.)

In stock legal and governmental news, on Thursday, the NHTSA announces that HYMTF (Hyundai) will recall 67k vehicles over fuel pump issues that can cause a loss of power during operation. Later, C announced it had reached a settlement with a Montreal exchange to resolve claims the bank had failed to report options trades over the exchange’s reporting threshold. The amount of the settlement was about $150k. At the same time, the highest court in Trinidad and Tobago reaffirmed a decision that recognizes COP’s $1.33 billion arbitration claim against the country of Venezuela. The decision will enable COP to begin legal action to seize Venezuelan assets in that country to satisfy the claim. Later, the NHTSA announced that STLA will recall 24k Chrysler hybrid minivans over fire risk.

Overnight, Asian markets were mostly down with only three of the 12 exchanges hanging onto green territory. Taiwan (-2.26%) and Hong Kong (-2.03%) were the worst performers (by a percent), but losses were widespread. In Europe, we see a similar picture taking shape as only three of 15 bourses are in the green at midday. Russia (+1.39%) is a notable outlier. However, the CAC (-0.56%), DAX (-0.70%), and FTSE (-0.54%) lead the region lower in early afternoon trade. In the US, as of 7:15 a.m., Futures are pointing toward a modestly lower start to the day. The DIA implies a -0.16% open, the SPY is implying a -0.06% open, and the QQQ implies a -0.15% open at this hour. At the same time, 10-Year bond yields are rising again to 4.203% and Oil WTI) is off 0.39% to $82.50 per barrel in early trading.

There is no major economic news scheduled for Friday. However, Fed members Williams (10:40 a.m.) and Bostic (12:45 p.m.) speak. The major earnings reports before the open include AXP, ALV, CMA, EEFT, FITB, HAL, HBAN, RF, SDVKY, SLB, TRV, and WIT. There are no major reports scheduled for after the close.

So far this morning, CMA, FITB, HBAN, RF, and SLB all reported beats on both the revenue and earnings lines. (Apparently, the hand-wringing over regional banks and loans is misplaced so far.) Meanwhile, AXP, EEFT, HAL, SDVKY, and TRV all missed on revenue while beating on earnings. However, ALV missed on both the top and bottom lines.

In miscellaneous news, after the close Thursday, a federal appeals court blocked the Biden Administration from continuing to implement a new student debt relief plan at the request of seven GOP-led states. (The Dept. of Education said it had already granted $5.5 billion in debt relief to 414k borrowers under that “SAVE” plan.) At the same time, the IMF said the US should raise taxes to reduce the US federal debt and put off any rate cut until at least late 2024. Meanwhile, mortgage finance agency Freddie Mac told Reuters Thursday that the US 30-year fixed-rate mortgages fell to the lowest rate since mid-March, with the national average down to 6.77% from the prior week’s 6.89%. Finally, Reuters reported that the state of CA reported that TSLA car registrations fell in Q2. TSLA’s 52,211 new registrations for Q2 was down and a third consecutive quarter of falling new registrations.

In overnight news, computer systems around the world failed Friday. This took firms from banking, to stock exchanges, to airlines offline. So far, there seem to be two unrelated causes. The first was a MSFT Windows crashing due to a conflict between that system and CRWD’s security software. Separately, MSFT reported outages of its Azure and Office 365 cloud systems. Combined, this caused an unprecedented and widespread computer outage globally. The exact causes are unknown, but it is likely to be related to a software update, possibly by MSFT since it had two separate set of issues.

With that background, it looks as if the markets are indecisive again this morning. SPY and QQQ gapped higher while DIA gapped a bit lower to start the premarket. All three major index ETFs have put in mostly wick since that point as the Bulls and Bears remain uncertain who has the strength in the early session. Overall, the short-term trend is Bearish. The rotation out of tech and into small-caps and the traditional mega-cap names also took a break (or stopped) on Thursday. However, for the mid-term and longer-term, there is no way to look at markets except to say they remain very bullish. In terms of extension, none of the three major index ETFs are stretched away from their T-line (8ema). Meanwhile, the T2122 indicator is back down into the center of its mid-range. Therefore, the market has room to run in either direction if the Bulls or Bears can find momentum. With regard to those 10 big dog tickers, eight of the 10 are in the green this morning. AAPL (+0.83%) and GOOGL (+0.74%) lead the way. Obviously, due to the overnight issues, MSFT (-1.38%) lags far behind and leads the morning dollar-volume traded. Lastly, don’t forget that it is Friday, Pay Day, and there is a weekend news cycle ahead. So, prepare your account for that situation.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the Man in the Green Bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby, it’s a job. The gains are real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service