MSFT Buyback and Industrial Production

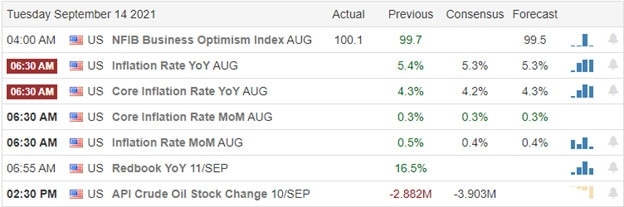

On Tuesday, CPI came in better than expected (core CPI much better) and markets gave us another little bull trap. A gap up of about a third of a percent was met with immediate strong selling that lasted for an hour. Then, after a small late-morning rally, the bears stepped in again all afternoon. This left us with big, ugly black candles in all 3 major indices, including a Bearish Engulfing of a Doji in the DIA. On the day, SPY lost 0.54%, DIA lost 0.81%, and QQQ lost 0.28%. The VXX rose to 26.46 and T2122 fell into the oversold territory at 15.81. 10-year bond yields fell to 1.284% and Oil (WTI) rose to $70.77/barrel.

During the day the Senate grilled SEC Chair Gensler on various items. Several called on him to set tighter rules on cryptocurrencies. He told them the SEC is working overtime to create a set of rules to oversee the crypto markets. He also said the SEC is working on several approaches on how to handle brokers’ conflict of interest when they take payments for order flow. In other political-related news, Senator Warren sent a letter to the Fed calling for them to break up WFC over their various improprieties over the years that have been fraudulent and anti-consumer.

During the afternoon, AAPL held its annual product announcement event. Among the products put out this year are a new iPhone 13 (in 4 models from $699 to $1,099), a new iPad and iPad mini, and a new Apple Watch. The main new features of the flagship phones are a bigger battery (1.5-2.5 longer battery life) and an improved camera. In other tech news, early this morning MSFT announced a dividend increase and a new $60 billion share buyback program.

New mortgage demand spiked 7% last week (week-on-week), even as rate for a 30-year fixed-rate loan remained unchanged. While a definite change in trend for demand, this is still 11% lower than a year ago. At the same time, applications for loan refinancing fell 3% week-on-week and remain just below where they were a year ago.

Overnight, Asian markets were mostly red after China’s retail sales came in much slower than expected for August. (Chinese retail sales grew 2.5% for the month versus an expected 7% growth.) Hong Kong (-1.84%) was far-and-away the biggest loser, but losses were widespread at a more moderate pace. India (+0.80%) was an outlier among the 3 exchanges that managed green numbers. In Europe, stocks are also mostly in the red at mid-day. The FTSE (+0.06%), DAX (-0.18%), and CAC (-0.54%) are typical of the region, with only Norway (+0.52%) more than barely green in early afternoon trading. As of 7:30 am, US Futures are pointing toward a mixed, flat open. The DIA is implying a dead flat open, the SPY implying a +0.10% open, and the QQQ implying a +0.21% open. The Dollar is down, as are 10-year bond yields, with Oil (WTI) up 1.33% (as are most commodities in reaction to the dollar) in early trading.

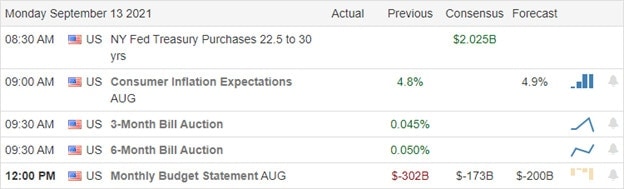

The major economic news scheduled for release on Wednesday includes the August Import/Export Price Index and NY Fed Empire State Mfg. Index (both at 8:30 am), August Industrial Production (9:15 am), and Crude Oil Inventories (110:30 am). Major earnings reports scheduled for release are limited to JKS and WEBR before the open. There are no earnings announcements scheduled for after the close.

After the bears sprung another bull trap at the open yesterday, they remained in control of the short-term trend. However, the longer-term trend remains bullish and markets are just a bit extended to the downside at the moment. However, before predicting that means a reversal, remember the market can remain wrong longer than you can stay solvent being right too early. As of now, less than 40% of stocks are above their 40-day moving average and only 43% are above their 200sma. This could be maintained, even in a rally, given the huge cap weightings of the massive Tech names. However, it is not a recipe for long-term market growth. So, the short-term outlook remains bearish and we need to keep an eye out for signs of a broader pullback.

Remember you don’t have to trade every day and that the Trend is your friend. Manage your existing trades before you chase any new ones. Focus on the process and on managing the things you can control. Don’t worry about the things you can’t control. Discipline and good trading rules are what separates trading success from failure over the long run. Above all, consistently take profits when you have them. A good trader refuses to let greed turn their winners into losers.

Ed

Swing Trade Ideas for your consideration and watchlist: No tickers today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service