Bulls Look to Follow-Up Dimon Reversal

Monday was certainly a wild ride. Markets gapped down (0.8% in the SPY, 0.36% in the DIA, and 1.4% in the QQQ) and proceeded to follow through, selling off to the lows by 11 am. However, from that point, stocks rallied hard in a wildly whipsaw-like rally that ended the day on the highs. This left us a white hammer in the SPY, a black hammer in the DIA, and a large-body white candle with a long lower wick in the QQQ. On the day, SPY lost 0.12%, DIA lost 0.45%, and QQQ gained 0.07%. It should be noted that the QQQ was down nearly 3% before its torrid intraday rally. The VXX was down almost 2% to 18.47 and T2122 fell to 38.15 (still in the mid-range). 10-year bond yields fell just a bit to 1.759% and Oil (WTI) was down two-thirds of a percent to $778.40/barrel.

During the day, two different major banks came out saying they expect at least 4 rate hikes by the Fed this year. Before the bell, GS said they are now forecasting 4 rate hikes in 2022. Later in the day, Jamie Dimon of JPM said he expects “the best growth in decades,” a “soft landing” on inflation, and is very bullish. (Whether coincidence or not, this is when the market started its intraday rally.) However, he also said he would not be surprised if the Fed went further than 4 hikes. In fact, he said he would be surprised if it was only 4 rates hikes in 2022. Of course, we have to temper his words by the fact the Fed has projected that it will do 3 rate hikes this year…and big banks do best during periods of rising interest rates (so he could be “talking his book”).

After the close Monday, Fed Vice-Chair Richard Clarida announced he will be stepping down as of this Friday. The surprise move comes with his term expiring in a few weeks on January 31. The move seems to stem from scrutiny over Clarida’s trading done in February 2020 just as the Fed was preparing to roll out its unprecedented array of rate cuts, QE, and lending facilities that caused markets to go on one of the strongest rallies in history starting in late March 2020. Clarida has always maintained that the trades were part of a “long-planned portfolio rebalancing” and were not related in any way to Fed plans.

In what is likely to be a global trend, China has taken the next step with its digital currency (e-CNY). The country has already gotten all leading Chinese mobile payment and e-commerce companies like BABA, TME, WeChat, and Alipay onboard. However, now the regional tests (10 major cities) have now been rolled out nationally. The PBOC (Central Bank) announced Monday that it will also be pushing the “digital Yuan” at this year’s Olympics in an effort to gauge global interest and speed broader adoption. While the US and other countries are far behind China in the move toward a block-chain digital currency (complete government visibility of all transactions), the trend is clear around the world, including the US

Overnight, Asian markets were mixed again. Shenzhen (-1.27%), Japan (-0.90%), and Australia (-0.77%) paced the losses. Meanwhile, Malaysia (+0.91%), Thailand (+0.61%), and Singapore (+0.60%) led the gainers. In Europe, markets are green across the board at mid-day. The FTSE (+0.67%), DAX (+1.12%), and CAC (+1.33%) are fairly typical of the spread across the region. As of 7:30 am, US Futures are pointing toward a mixed green open. The DIA implies a +0.17% open, the SPY is implying a +0.31% open, and the QQQ implies a +0.49% open at this hour as rotation back toward tech (growth) seems to be back in play. 10-year bond yields are down a bit to 1.762% and Oil (WTI) is up almost 1.5%.

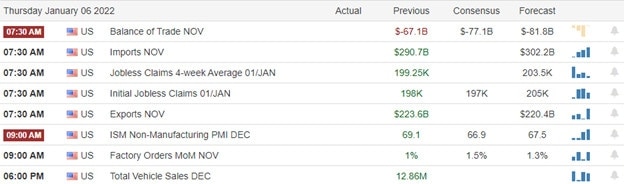

There is no major economic news scheduled for release Tuesday. However, there are 3 Fed speakers (Mester at 9 am, George at 9:30 am, and Chair Powell faces his re-nomination testimony at 10 am). The major earnings reports scheduled for before the market is limited to ACI and SNX. There are no major reports scheduled for after the close.

The market seems to be trying to follow through this morning on what may have been a “Dimon’s outlook rally” yesterday. However, keep in mind that all 3 major indices are still in a downtrend and none of them have tested (let alone broken through) their T-lines yet. So, be careful of getting caught in the “buy the dip” rush. The bears still have the trend and overall momentum. Also, remember that intraday whipsaw (like Monday’s massive reversal) has been the norm lately.

Remember that the first rule of making a lot of money in the market is to not lose a lot of money in the market. So, don’t be stubborn. When you’re wrong, just admit it and take your loss. (That’s why we set stops.) Stick to your trading rules and on managing the things you can control. Don’t chase, trade with the trend, keep consistently taking profits when you have them, and move your stops in your favor.

Ed

Swing Trade Ideas for your consideration and watchlist: TREE, ABBV, DVN, TRIP, GSK, BMY, CVS. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service