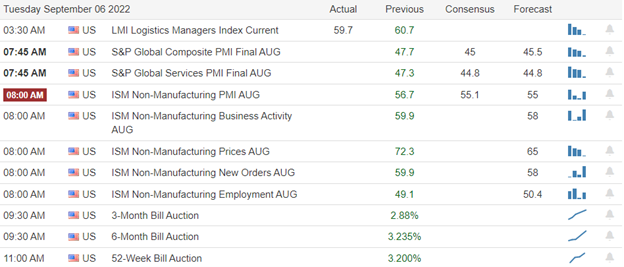

Hot employment data continues to worry the market about aggressive Fed rate hikes. Though the bulls triggered hopes of a relief rally yesterday, we have the Employment Situation to deal with this morning. Analysts suggest the number could come in hot but will the bulls continue to defend yesterday’s low, or will it inspire the bears? Traders could be thinking about an early getaway to extend the 3-day weekend, so don’t be surprised if volume quickly drops off after the data-driven volatility of the open.

Asian markets traded mostly lower as we slept with worries about the FOMC’s next decision. However, European markets trade decidedly bullish with cautious eyes on the U.S. jobs report. With no earnings inspiration this morning, U.S. futures suggest a flat to slightly lower open, pensively waiting on the Employment Situation number before switching gears and heading into the long holiday weekend. Consequently, it could be a wild morning session followed by light and choppy price action as traders get away early and extend their weekend plans.

Economic Calendar

Earnings Calendar

Although we have about 20 companies listed on the Friday earnings calendar, only one report confirmed from GB that’s not particularly notable.

News & Technicals’

Stocks have been selling off, and bond yields have risen ahead of Friday’s August employment report, providing a critical reading of the labor market. It is a particularly important report because it is expected to be one of the last big economic reports the Federal Reserve will consider before it raises rates at its late September meeting. According to Dow Jones, economists expect 318,000 jobs added in August, and the unemployment rate held steady at 3.5%. In addition, on Thursday, a National Labor Relations Board official recommended that Amazon’s objections to a historic union election in New York be rejected. In April, workers at Amazon’s JFK8 warehouse voted to form its first U.S. union. Amazon has until Sept. 16 to appeal the NLRB official’s recommendations. Starbucks on Thursday named Laxman Narasimhan as its next chief executive officer. Narasimhan most recently served as CEO of health and hygiene company Reckitt. He’ll join Starbucks in October, learning about the company and its reinvention plan, before assuming the top job in April. Morgan Stanley analysts laid out an economic scenario for China if authorities do not provide enough funding and other support to stabilize the real estate market. The analysts said Chinese stocks would plunge, GDP would slow, and unemployment would rise. However, they said spillover from real estate to the rest of China’s economy “remains manageable so far.” Between April 2020 and June 2021, solar panels at Amazon fulfillment centers caught fire or experienced electrical explosions at least six times. “The rate of dangerous incidents is unacceptable and above industry averages,” an Amazon employee wrote in an internal report viewed by CNBC. Rooftop solar is part of Amazon’s overall plan to zero emissions by 2040.

Thursday again saw the bears dominate early trading as hot employment data continues to worry investors about aggressive rate hikes from the Fed. However, the bulls finally staged a bit of a comeback at the end of the day, raising hopes of a relief rally. Unfortunately, we have the Employment Situation number before the bell this morning that analysts suggest could also come in hot. So, I guess the question is will it inspire the bears, or will the bulls stand their ground supporting yesterday’s lows? After we pass the data-driven morning volatility, traders will begin thinking about the long weekend ahead and the uncertainty it may provide. I don’t think we can rule out the possibility of light choppy price action or pile-on selling to reduce risk as we slide into the 3-day weekend.

Markets gapped lower at the open on Wednesday on fears raised by the closing of yet another major (21 million population) Chinese City due to a covid outbreak. (The gaps were between half of a percent and nine-tenths of a percent.) We then saw some follow-through with the 3 major indices reaching the lows of the day by 11 am. At that point, markets ground sideways for a couple of hours. The day then ended with a slow protracted 3-hour rally that filled the opening gap and closed very near the highs of the day. This action gave us white-bodied Hammer-type candles in all 3 major indices. It is worth noting that Thursday saw slightly above average volume in all 3 major indices (and that was the first time that has happened on a green day since August 16).

On the day, seven of the 10 sectors were in the red, with Basic Materials and Energy both down more than 2%. Healthcare (+0.91%) and Utilities (+0.82%) were by far the leading sectors Wednesday. Despite the sectors leaning red, the SPY gained 0.31%, DIA gained 0.45%, and QQQ gained 0.04%. The VXX rose 1% to 19.44 and T2122 remains deeply oversold at 3.57. 10-year bond yields spiked higher to 3.257% and Oil (WTI) plummeted another 3.5% to $86.44/barrel. Overall, this was a small attempt by the bulls to find their footing (support) after reeling since last Friday’s Jackson Hole inspired bloodbath.

In economic news, Weekly Initial Jobless Claims came in better than expected (232k actual versus 248k forecast and 237k previous week). Q2 Nonfarm Productivity also came in better than expected, but still down. The actual was -4.1% while -4.5% was the consensus forecast and last quarter we saw -4.6%. August Mfg. PMI and August ISM Mfg. PMI also both came in stronger than expected (PMI 51.5 actual vs 51.3 forecast and ISM PMI at 52.8 actual versus 52.0 forecast). All of these things would indicate the economy is at least slightly stronger than expected…therefore giving the Fed cover for a larger September rate hike. However, on the other side, Q2 Unit Labor Costs came in lower than expected. They showed a +10.2% actual versus a +10.7% consensus forecast and last quarter’s +10.8%. This would tend to indicate that there is less inflationary pressure on labor costs than expected, which would speak against a heavy hand by the Fed.

In stock news, US military veterans sued MMM to prevent the company from spinning off its healthcare business. The lawsuit calls the move by MMM a blatant attempt to transfer liability over defective earplugs to another company after a judge had ruled MMM could not use bankruptcy to avoid the damages. Elsewhere, the UK Antitrust Regulator has ruled that the MSFT acquisition of ATVI (for $69 billion) could harm competition. This is not likely to derail the deal but should force MSFT to give broader assurances around the not ordering platform exclusivity of games to block rivals SONY and Nintendo from having access to ATVI games.

In energy news, XOM and RDS.A agreed to sell their California oil joint venture operations to German asset manager IKAV for $4 billion. Elsewhere, the US Dollar reached yet another 20-year high Thursday, providing an additional headwind for oil prices (which are denominated in dollars). In nuclear news, the California legislature approved a bill to extend the life of the state’s only atomic power plant by 5 years on Thursday. This reversed the 2016 decision to retire the PCG Diablo Canyon plant by 2025. The bill also provided PCG with a $1.4 billion loan to keep the plant operational until 2030.

After the close AVGO and LULU both reported beats on the revenue and earnings lines. Both companies also raised forward guidance. However, JOAN beat on revenue while missing on earnings. The company left guidance as-is.

This morning, META and QCOM announced an agreement to jointly develop and produce a chipset META’s Quest virtual reality devices. The chipset will be based on QCOM’s Snapdragon chip line which is already widely used in Android phones. This partnership comes just weeks ahead of META launching a new virtual reality headset (set for October). However, losses have continued to widen in META’s “Reality Labs” division since the company bet its future on virtual reality by rebranding in 2021.

Overnight, Asian markets leaned heavily to the red side on modest moves. Taiwan (-0.87%), Hong Kong (-0.74%), and Singapore (-0.57%) led the region lower. In Europe, stocks lean heavily to the upside at midday. The FTSE (+0.62%), DAX (+1.31%), and CAC (+0.44%) are leading the region higher with only 3 smaller exchanges showing red in early afternoon trade. As of 7:30 am, US Futures are pointing toward a slightly red start to the session (granted, well ahead of critical data). The DIA implies a -0.13% open, the SPY is implying a -0.18% open, and the QQQ implies a -0.36% open at this hour. 10-year bond yields are up just slightly to 3.258% and Oil (WTI) is up almost 2% to $88.29/barrel in early trading.

The major economic news events scheduled for Friday include Aug. Avg. Hourly Earnings, Aug. Nonfarm Payrolls, Aug. Participation Rate, and Aug. Unemployment Rate (all at 8:30 am), July Factory Orders (10 am). There are no major earnings reports scheduled for the day.

Today brings a slew of data before the open, most importantly August Payrolls data. This is widely expected to come in hotter than the consensus forecast (+300k) and most analysts think this will cause the bears to roar (as traders then expect another 0.75% hike later this month). However, US futures are already pricing in an 80% probability of a 0.75% rate hike. So, to me, the risk seems to be to the upside if somehow the Payroll data comes in a bit soft. With that said, the premarket is essentially flat (just on the red side) already while we wait on the data.

Expect volatility at the open as markets react to Payrolls, Unemployment Rate, and Participation. However, with a 3-day weekend ahead, it is very likely we see light volume in the afternoon (perhaps all day) as the big traders head for a long weekend in the Hamptons. So, be careful about initiating any new positions that you might not be able to get out of later in the day. The short-term trend remains strongly bearish, but we did put in candles that suggest the bulls tried to find support Thursday. If nothing else, we are due a pause just to relieve bearish overextension. The bottom line is that we are in a downtrend, but the bulls are trying to hold this level and the bears may have gotten ahead of themselves.

Again, remember it is Friday and we have a 3-day weekend ahead. Prepare yourself by taking profit, hedging, and/or getting smaller in your risk positions. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Remember that trading is our job. So, do the work and follow the process. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today, Rick is on vacation visiting a gandbaby. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stocks gapped higher Wednesday between 0.2% (DIA) and 0.95% (QQQ). However, once again this was a bull trap. After about 25 minutes of meandering higher from the open, the bears stepped in and took all 3 major indices on a slow, protracted selloff that lasted the rest of the day and closed on the lows. This action gave us black-bodied candles with small upper wicks and no lower wick across all those indices. It could be seen as the completion of the second half of the Bearish Doji Continuation which was started last Friday.

On the day, all 10 sectors were in the red with Basic Materials and Communications Services leading the way lower. The SPY lost 0.79%, the DIA lost 0.75%, and QQQ lost 0.58% during the session. The VXX fell another 1.23% to 19.24 and T2122 (4-week New High/Low Ratio) remains deeply oversold at 3.00. 10-year bond yields surged higher to 3.178% and Oil (WTI) fell more than 3% to $88.86/barrel. All-in-all, it was a slow, methodical, bear day in the market.

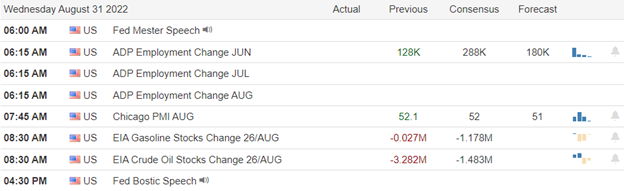

In economic news, the Aug. ADP Nonfarm Payrolls added far fewer jobs than was expected or was added in July (+132k vs. +300k forecast and +268k in July). This indicates a slowing economy. However, the Aug. Chicago PMI came in slightly better than expected at 52.2 (versus 52.0 forecast and July’s 52.1 number). Elsewhere, the EIA Weekly Crude Oil Inventories diverged from Tuesday night’s API number. EIA showed a drawdown of 3.326 million barrels for the week, which was more than twice the expected drawdown (1.483 million barrels) and slightly worse than the prior week’s drawdown of 3.282 million barrels.

In stock news, after the close, BBBY confirmed what it had leaked. The retail chain will close 150 stores, cut about 20% of its jobs (roughly 6,400), and change its merchandising strategy by cutting private label lines in favor of national third-party brands. BBBY also confirmed that it has secured a $500 million loan (to get it through the holiday season) and it now forecasts a 26% drop in sales for Q2. BBBY stock was down 21% on Wednesday. Also, after the close, COST reported that its “Same Store Sales” grew 10.1% in July and 15.3% over the same period last year. Elsewhere, Arm (owned by SFTBY) filed a lawsuit against QCOM. At issue was that QCOM acquired Nuvia (a chip design firm) last year and neither company informed or gained consent from Arm as required by Arm’s license agreement. Finally, late last night, NVDA reported that the US government has ordered them to stop selling chips to Russia and China. The company had previously gotten export exemptions to continue selling to China, but now doubts that exemption will be extended again. NVDA said it expects to lose $400 million in sales this quarter due to the restriction.

In energy news, on Wednesday, US Gasoline futures fell back below the price they were at when Russia invaded Ukraine in February ($2.59/gallon). Elsewhere, OPEC+ put out a statement Wednesday that failed to mention production cuts (as had been threatened by Saudi Arabia last week). Instead, the release hyped up global demand for oil, which analysts read as meaning cuts were the last thing on the minds of OPEC+ members. In related news, the White House said President Biden has informed Israel about the revival of the 2015 JCPOA nuclear deal with Iran. (This deal reportedly will allow Iran to ship oil, significantly increasing global supplies.) In addition, after the close, the White House announced the G7 will be discussing the Biden Administration’s proposal to put a price cap on Russian oil when the group meets Friday.

After the close GEF, PSTG, and VEEV all reported beats on both the revenue and earnings lines. However, COO beat on revenue while missing on earnings. FIVE missed on both the top and bottom lines. GEF and PSTG raised their guidance while COO and FIVE lowered forward guidance.

So far this morning, CPB, SAIC, SIG, GMS, and WB have all reported beats on both the top and bottom lines. Meanwhile, HRL beat on revenue while missing on earnings. HRL also lowered its forward guidance. On the other side, GCO missed on revenue while beating on earnings. However, PDCO, CIEN, FLWS, and OLLI all reported misses on both lines. FLWS and GCO also both lowered forward guidance.

Overnight, Asian markets leaned heavily to the downside. South Korea (-2.28%), Australia (-2.02%), and Taiwan (-1.94%) led the region lower with only two smaller exchanges managing to stay on the green side of flat. In Europe, stocks are red across the board at mid-day. The FTSE (-1.38%), DAX (-1.40%), and CAC (-1.25%) are leading the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a gap lower to start the day. The DIA implies a -0.48% open, the SPY is implying a -0.50% open, and the QQQ implies a -0.68% open at this hour. 10-year bond yields are surging again, now at 3.20%, and Oil (WTI) is down another 2% to $87.81/barrel in early trading.

The major economic news events scheduled for Thursday include Weekly Initial Jobless Claims, Q2 Nonfarm Productivity, and Q2 Unit Labor Costs (all at 8:30 am), PMI Mfg. (9:45 am), and ISM Mfg. PMI (10 am). There is also another Fed Speaker (Bostic at 3:30 pm). The major earnings reports scheduled for the day include FLWS, CPB, CIEN, GCO, GMS, MOMO, HRL, HOV, OLLI, PDCO, SAIC, SIG, TTC, and WB before the open. Then after the close, AVGO, JOAN, and LULU report.

In economic news later this week, on Friday we get Aug Avg. Hourly Earnings, Aug. Nonfarm Payrolls, Aug. Participation Rate, Aug. Unemployment Rate, July Factory Orders. In terms of earnings, there are no major reports scheduled for Friday.

September looks to be coming in like a bear as the bulls just have not been able to find their footing this week. We remain very extended to the downside at this point (both in terms of the T-line and T2122). However, the futures are not giving the bulls much hope, except that prices have recovered from the overnight lows. Be very careful of chasing any gaps or early moves. Remember that the last two days started with “gap traps” and we want to learn from those examples. The short-term trend remains strongly bearish, the mid-term bullish trend has been broken, and the long-term bearish trend is also broken. Volatility is a high probability and if nothing else we still need a pause to ease overextension. The bottom line is that we are in a downtrend, but the bears may have gotten ahead of themselves with support not far below.

Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Remember that trading is our job. So, do the work and follow the process. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today, Rick is on vacation visiting a gandbaby. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Early bullishness faded quickly on Tuesday after the JOLTS report came in hot, re-engaging the bears with the expectation of an aggressively hawkish Fed. Yesterday added to the technical damage of index charts with the DIA, SPY, and QQQ closing the day below their 50-day moving averages. Sadly the 9.1% inflation report out of Europe is piling on to the bearish attitude this morning and could make it difficult for the bulls to begin an overdue relief rally. We face a lot of economic data the rest of the week as we slide toward the uncertainty of a 3-day weekend.

Ason markets closed mixed overnight, with China’s declining factory activity adding to the worry of their slowing economy. European markets see red across the board as they struggle with rate tightening fears after hearing their inflation rate hit 9.1%. U.S. futures have seesawed in pre-market trading, wanting a relief rally despite the piling on of adverse economic data from here and around the world. Expect the volatile and challenging price action to continue with earnings and economic reports just around the corner.

Economic Calendar

Earnings Calendar

The mid-week earnings calendar has a few more companies listed than Tuesday, with around 20 confirmed. Notable reports include BF.B, COO, DBI, FIVE, MDB, OKTA, PSTG, SMTC, VEEV, & VRA.

New & Technicals’

Eurozone inflation hit a new record high in August at 9.1%. The rate was above expectations, with a Reuters poll of economists anticipating a rate of 9%. It is expected that gas flows via Nord Stream 1, which runs from Russia to Germany via the Baltic Sea, will be suspended from Aug. 31 through to Sept. 3. The temporary supply halt reflects a deepening gas dispute between Russia and the European Union. It underscores both the risk of a recession and a winter shortage. “Europe is in full bunkering mode and taking no chances with Russian supplies heading into the winter,” said Wei Xiong, senior analyst at energy consultancy Rystad Energy. In addition, analysts told CNBC that Iraq’s political turmoil could bring about a considerable risk to global oil markets. “While Iraqi production is usually fairly resilient to unrest, the current political environment is extraordinarily toxic and poses a considerable risk to the oil sector,” said Fernando Ferreira, a director at Rapidan Energy Group. Those concerns come on the heels of escalated protests in Iraq on Tuesday after powerful Shiite Muslim cleric Muqtada al-Sadr announced his resignation from politics. EV maker BYD falls more than 12%, dragging down Hang Seng Index on Wednesday. According to a filing, Warren Buffett’s Berkshire Hathaway trimmed its stake from 19.92% to 20.04%. Yang Liu of Atlantis Investment says this is a “common trend,” warning “maybe we’ll see more” of such trims. Treasury yields tick higher in early Wednesday trading, with the 12-month at 3.42%, the 2-year at 3.48%, the 5-year at 3.30%, the 10-year at 3.14%, and the 30-at 3.25%.

Futures began the morning pushing for some gains, but after the jobs-opening report came in hot, the bears returned to work expecting an aggressive hawkish Fed. Unfortunately, the selling created more technical damage in the index charts closing the DIA, SPY, and QQQ below their 50-day averages. If there is a silver lining in the clouds, it would be that the T2122 indicator suggests a short-term oversold condition, and a relief rally could begin at any time. However, the bearish data is beginning to pile on as world economies slow and inflation remains persistent. Though I will be watching for clues of an oversold rally, the 9.1% inflation reading out of Europe has reversed early bullishness and could keep the bears engaged. We have a lot of economic reports coming our way the rest of the week, so plan carefully and remember we also face the uncertainty of a 3-day weekend.

Markets gapped higher between a third and a half of a percent on Tuesday. However, this was a bull trap as all 3 major indices sold off hard the first 90 minutes of the day. From that point, we saw a sideways grind in a small range (relatively speaking) for the rest of the day. This action is giving us a Bearish Engulfing candle of a Doji / Spinning Top (or if you prefer the start of the completion of a Bearish Doji Continuation or Doji Sandwich signal). This made for the third straight down day for all 3 major indices and all this happened on average volume.

On the day, all 10 sectors are down sharply, with the Energy Sector (down 4%) leading the way lower. The SPY lost 1.05%, DIA lost 0.95%, and QQQ lost 1.11%. The VXX was also down a percent to 19.48 and T2122 is extremely oversold to 3.35. 10-year bond yields have rebounded from early lows and are back up to 3.112% while Oil (WTI) is down 5% to $92.16/barrel on news out of a Pro-Iran UK television station saying Iran has agreed to a deal with the United States to revive the Trump-killed JCPOA nuclear deal and allow Iran to sell oil. All-in-all, it’s looking like it will end up a blah, bull trap, one plus percent down day.

In economic news, the Conference Board Consumer Confidence came in a 103.2, well above the consensus forecast (97.9) s well as July’s reading (95.3). At the same time, July JOLTS (Job Openings) came in higher than expected at 11.293 million (versus a consensus forecast of 10.475 million and a June reading of 11.04 million). Then, after the close, API reported Weekly Oil Stocks surprised with a modest build (0.593 million barrels) while a modest drawdown (-0.633 million barrels) was expected. However, this was still much better than the prior week’s 5.632-million-barrel drawdown.

In Forex / Fed news, the Dollar hit a 20-year high for the second day in a row Tuesday. This came after the JOLTs report suggested a stronger than expected economy. In addition to the forex impacts, traders have upped their bets for a 75-basis-point hike in September. US Futures now have now priced in a 74.5% probability of that 0.75% hike. After the close, NY Fed President Williams told the Wall Street Journal that he expects rate hikes and balance sheet reduction (quantitative tightening) to continue into 2023. Specifically, he pushed back against the idea of a rate cut in 2023 (while the futures market still expects a cut in the fall of 2023). This all just focuses eyes on the August Payrolls report Friday.

In stock news, it was reported Tuesday that SNAP is planning to reduce staffing by 20%. Elsewhere, after its earnings report, BBY told the earnings call that they are now forecasting that consumers will resume the old pattern by doing most of their holiday shopping late. (In 2021, consumers did the majority of their holiday shopping early.) In TWTR news, Elon Musk has asked the judge to postpone the trial over his purchase of TWTR until November (from October 17). In the filing, Musk cited his subpoena of the newly announced TWTR whistleblower as the reason.

After the close CRWD reported beats on both the top and bottom lines. The company also raised guidance. Meanwhile, HPE, HPQ, AMRK, CHWY, and PVH all reported misses on revenue while beating on earnings. In addition, HPQ, PVH, and CHWY all lowered their forward guidance. So far this morning, DBI, DCI, and CHS have all reported beats on both the revenue and earnings lines. Meanwhile, EXPR missed on revenue while beating on earnings.

Overnight, Asian markets were mixed. Shenzhen (-1.29%), Shanghai (-0.78%), and Singapore (-0.55%) led the way lower on weak PMI data out of China (which actually slightly beat expectations but still came in at only 49.4 for Mfg. while Services PMI was at 52.6). Meanwhile, India (+2.58%) Taiwan (+0.95%), and South Korea (+0.86%) paced the gainers. In Europe, markets are mostly in the red at midday with the notable exception of Russia (+3.63%). The FTSE (-1.08%), DAX (-0.36%), and CAC (-0.48%) are typical for most of the continent with a few smaller exchanges just holding on to the green side of flat in early afternoon trade. As of 7:30 am, US Futures are pointing toward a flat to modestly green start to the day. The DIA implies a +0.08% open, the SPY is implying a +0.22% open, and the QQQ implies a +0.58% open at this hour. 10-year bond yields are higher to 3.142% and Oil (WTI) is off 2.68% to $89.17/barrel in early trading.

The major economic news events scheduled for Wednesday include ADP Nonfarm Payrolls (8:15 am), Chicago PMI (9:45 am), EIA Crude Oil Inventories (10:30 am), and a couple of more Fed speakers (Mester at 8 am and Bostic at 6:30 pm). The major earnings reports scheduled for the day include BF.A/B, CHS, DBI, DCI, and EXPR before the open. Then after the close, FIVE, PSTG, and VEEV report.

In economic news later this week, on Thursday Weekly Initial Jobless Claims, Q2 Nonfarm Productivity, Q2 Unit Labor Costs, PMI Mfg., and ISM Mfg. PMI are reported. Finally, on Friday we get Aug Avg. Hourly Earnings, Aug. Nonfarm Payrolls, Aug. Participation Rate, Aug. Unemployment Rate, July Factory Orders.

In earnings later this week, on Thursday, FLWS, CPB, CIEN, GCO, GMS, MOMO, HRL, OLLI, PDCO, SAIC, SIG, TTC, WB, AVGO, JOAN, and LULU report. Finally, Friday there are no major reports.

Markets are limping into the last day of August, coming off 3 straight down days. We remain very extended to the downside at this point and futures are giving us a very modest and indecisively bullish indication. Be very careful of chasing any gaps or early moves (especially to the downside). While the short-term trend is bearish, the mid-term bullish trend is broken, and the long-term bearish trend is also broken, volatility and if nothing else a pause to ease extension is a high probability. The bottom line is that we are in a volatile downtrend, but the bears may have gotten ahead of themselves with support not far below.

Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Remember that trading is our job. So, do the work and follow the process. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: BABA, Z, SNOW, CAH, UUP, BIG, WEAT, UEC, SQQQ. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Stocks gapped down between three-quarters and a full percent on Monday in what the bears hoped was the start of follow-through on Friday’s big move down. However, after some early volatility, the bulls stepped in to fill the gap in a protracted rally from 11 am to 2 pm. Then prices remained near those highs for the next 1.5 hours. However, late in the day, the bulls took their profits, and all 3 major indices sold off hard in the last 15 minutes. This action is giving us indecisive, Spinning Top type candles (long wicks on both ends of the candle) that are resulting in modest bearish moves overall. This sets up either a Bearish Doji Continuation (Sandwich) or a Bullish Morning Star Signal in all 3 indices.

Seven of the 10 sectors were red, with Energy being far-and-away the biggest gainer and Technology being far-and-away the biggest losing sector. On the day, SPY lost 0.67%, DIA lost 0.57%, and QQQ lost 0.99%. The VXX fell more than 2% to 19.71 and T2122 remains deep in the oversold territory at 10.25. 10-year bond yields are up significantly to 3.11% and Oil (WTI) has surged more than 4% to $96.96/barrel.

There was no major economic news on Monday. However, there was a LendingClub survey reported by CNBC that claimed there was a slight decline in the percentage of Americans who are living paycheck to paycheck. The study found that 59% of Americans fall into that category, down from 61% in June, but also above the 54% number from June. In somewhat related news, in the face of nine weeks of declining gasoline prices, US oil refiners have recently been really pushing exports of refined products in order to limit domestic supply and increase their recently-record profits. It has gotten to the point where on Monday Energy Sec. Granholm was basically begging oil refiners to stop increasing those recent record-level distillate and fuel exports.

In stock and miscellaneous news, MSFT announced it will amend cloud licensing deals as of Oct. 1 in order to stave off round another EU antitrust penalties. The changes will make it easier for rivals (GOOGL, AMZN, and BABA) to compete with MSFT in Europe. Elsewhere, TSLA was hit with a class action lawsuit over sudden “phantom braking” by the company’s Model 3 when using the “Driver Assist” (Autopilot) mode. Related to inflation, we’ve received some news lately tending to indicate that inflation has already peaked (especially gas prices). However, the Zumper National Rent Index came out yesterday afternoon and shows that landlords don’t buy that story. The national average rent for a 1-bedroom apartment rose to a record $1,500 in July, up 2% from June and more than 12% from one year ago.

In Russian invasion news, on the ground, Ukraine launched its long-awaited counter-offensive in the Southern Kherson region. More than six months into the war, Monday, Ukraine recaptured 4 villages in that region and breached the first of 3 Russian defense lines. Ukraine also initiated a much smaller offensive in the Eastern Izium region. Elsewhere, Monday evening, EU Commissioner von Der Leyen announced that the EU is planning an “emergency intervention” in the region’s power market. This plan clearly breaks with the EU’s prior “let the market handle the situation” stance. Details are lacking, but EU countries have already been granted permission to cap natural gas prices and many are now calling for the same power on electricity prices. (EU wholesale electricity prices are more than 800% higher than one year ago.) Finally, a team of UN inspectors has left to visit the Russian-occupied Zaporizhzhia nuclear power plant (the largest in Europe) amidst fear over Russian shelling near the plant and Russia’s cutting the plant off from the electric grid. (The plant produces more than 20% of all electricity generated in Ukraine.)

After the close HEI reported a beat on revenue, but missed on earnings. So far this morning, AMWD, BMO, and BBY all reported beats on both the top and bottom lines. Meanwhile, BIDU, BIG, and FUTU missed on revenue while also beating on earnings. However, IQ beat on revenue and came in in line with earnings (a loss of $0.04/share).

Overnight, Asian markets were mixed but leaned to the upside. India (+2.58%), New Zealand (+1.23%), and Japan (+1.14%) led the gains while mainland China showed the only red in the region. In Europe, we see mostly green at midday. The FTSE (+0.12%), DAX (+1.84%), and CAC (+1.11%) are leading the region higher in early afternoon trade. However, Norway (-1.03%) is showing the only appreciable red in the region. In the US, as of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.69% open, the SPY is implying a +0.83% open, and the QQQ implies a +1.12% open at this hour. 10-year bond yields are back down to 3.058% and Oil (WTI) is starting the day down more than 2.77% to $94.32/barrel.

The major economic news events scheduled for Tuesday include Conf. Board Consumer Confidence and July JOLTs (both at 10 am), API Weekly Crude Oil Stocks (4:30 pm), and a Fed speaker (Williams at 11 am). The major earnings reports scheduled for the day include AMWD, BIDU, BMO, BBY, BIG, FUTU, and IQ before the open. Then after the close, AMRK, CHWY, CRWD, HPE, HPQ, and PVH report.

In economic news later this week, on Wednesday we see ADP Nonfarm Payrolls, Chicago PMI, EIA Crude Oil Inventories, and another Fed speaker (Mester). On Thursday Weekly Initial Jobless Claims, Q2 Nonfarm Productivity, Q2 Unit Labor Costs, PMI Mfg., and ISM Mfg. PMI are reported. Finally, on Friday we get Aug Avg. Hourly Earnings, Aug. Nonfarm Payrolls, Aug. Participation Rate, Aug. Unemployment Rate, July Factory Orders.

In earnings later this week, Wednesday we get reports from BF.A/B, CHS, DBI, DCI, and EXPR. On Thursday, FLWS, CPB, CIEN, GCO, GMS, MOMO, HRL, OLLI, PDCO, SAIC, SIG, TTC, WB, AVGO, JOAN, and LULU report. Finally, Friday there are no major reports.

Coming off a second straight day of losses, futures seem to indicate the bulls are ready to make a stand. The question is whether this is a true reversal, just an over-extension bounce, or even a bull trap. BAC warned this morning that the flow of funds from its account holders has gotten decidedly defensive since Friday. So, given the strength of the selloff the last 15 minutes Monday, we should be very cautious about chasing any gaps or rallies. We were very extended and at this point, the futures move does not look like a major reversal of market sentiment to me. The short-term trend is bearish, the mid-term bullish trend is broken, and the long-term bearish trend is also broken. The bottom line is that we are in a volatile, undecided market.

Demonstrate patience and wait for confirmation. Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: CGC, MCK, META, UEC, KSS, ADM, CAH, X, DBC, WEAT, Z, SPXU, QID, UVXY. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Friday was a day of reckoning for markets are all 3 major indices opened flat and traded that way until Fed Chair Powell began to speak. However, when he did begin to speak, it was immediately apparent that Powell was not going to tell the Bulls what they had hoped to hear (that inflation was coming down and the Fed could ease up on the tightening). So, we saw massive volatility in the 10 minutes after Powell started speaking and then a brutal selloff the rest of the day (especially from 10am -11am) from that point. This gave us a huge Bearish Engulfing signal in the DIA and just big, ugly black candles in the SPY and QQQ. Obviously, all 3 major indices failed their T-lines (8ema) during the day, but all 3 are also now extended well below those 8ema levels.

All 10 sectors are well into the red with Technology, Consumer Cyclical, and Industrials leading the way lower on a risk-off day. On the day, SPY lost 3.38%, DIA lost 3.07%, and QQQ lost 4.10%. The VXX has gained over 2.25% to pop back up to 20.15 and T2122 has fallen all the way from overbought to well oversold at 7.87. 10-year bond yields pulled back to be slightly down (after rising overnight) at 3.028% and Oil (WTI) was down 0.5% to $92.99/ barrel. Basically, the Bulls wanted Powell to tell them that the Fed can take its foot off the gas on tightening, but instead he was adamant that the rate increases will continue, and higher rates will persist “for some time.” In fact, he told us to expect some pain ahead with higher interest rates, slower growth, and softer labor markets all required to bring down inflation. Basically, that was a gut punch for the traders who have been chasing growth.

In China stock news, Beijing and Washington reached a preliminary deal that will allow SEC officials to review the audit documentation of 163 businesses that the SEC identified at high risk of US trading prohibition. This is a good first step in avoiding the delisting of those companies from the NYSE and NASDAQ exchanges. Some of those major tickers potentially saved include BABA, JD, BIDU, PDD, NIO, YUMC, PTR, EDU, etc.

In food/agriculture/consumer news, a new forecast revision released Friday shows that drought and heatwaves have slashed US corn yield expectations for the fall. The revisions are now expecting more than a 4% yield reduction versus last year, taking the crop total down to 2019 levels. This does not sound like a huge issue, but add to that some very similar climate change problems in Europe and China, as well as the Russian invasion taking 20% of Ukrainian cropland out of production. The end result will be shortages and higher food prices expected toward year-end. Corn, Soybeans, and Wheat are the primarily-impacted grains with Beef, Hog, and Chicken meats impacted in turn (all are heavily grain fed). This will have a big impact on consumer defensive input prices and consumer inflation this year. However, the problem may well be made worse in 2023 because the Russian aggression has also cut natural gas supplies, lowering global fertilizer production (as much as 50% for Nitrogen-based fertilizer). This is expected to lower next year’s crop yields globally an unspecified, but very significant amount as well. (Global crop yields have dramatically increased ever since the early 1970s. This has kept food expenses a low percentage of the consumer’s budget, and freed up money for all sorts of previously unfeasible consumer spending (especially in North America and Europe). This all happened on the back of very cheap and widely-available nitrogen-based fertilizers. If that paradigm changes, you can bet consumer spending habits will also need to change…therefore reshaping stock market leadership. (All grain using tickers and as a result, the consumer spending on non-essentials will be hit significantly.)

In legal news, on Friday, a judge rules that MMM cannot use bankruptcy to avoid liability over selling defective earplugs to the US military. MMM was down 12% on the news. On Saturday, META agreed in principle to an undisclosed settlement of a lawsuit in US Federal Court seeking damages for allowing third parties (such as the infamous Cambridge Analytica) to access uses private data. Finally, also on Saturday, the USDOT temporarily waived truck driver hours of service restrictions. This came after a fire took an Indiana BP refinery offline Wednesday causing the need for much more fuel trucking in the Midwest.

In market trends, Bloomberg reports that “meme stocks” are here to stay. In a weekend survey of 522 investors, two-thirds expect the speculative meme stock phenomenon to be here to stay (based on easy/rapid internet communications). Elsewhere, Reuters reports that funds are heeding Powell’s Friday message and sticking to the old “Don’t fight the Fed” mantra. At this point, traders have amassed the largest short position on 3-month Fed Rate Futures, having doubled in the last month and gained 100,000 contracts Friday. (Traders are betting short-term bonds will fall in value as yields and interest rates rise.) In short, markets believed Chair Powell and expect more bear market pain.

So far this morning, PDD reported beats on both the top and bottom lines. Meanwhile, CTLT missed on revenue while beating on earnings. CTLT also lowered its forward guidance when it reported.

Overnight, Asian markets were deeply in the red. Japan (-2.66%), Taiwan (-2.31%), and South Korea (-2.18%) led the region lower as Asia played catch-up to the North American route from Friday. In Europe, we see the same story (with the lone exception of a green Russia +0.67%) at mid-day. The FTSE (-0.70%), DAX (-1.24%), and CAC (-1.90%) are leading the wave of red across that region in early afternoon trade. As of 7:30 am, US Futures are pointing toward a significant gap lower to start the week. The DIA implies a -0.87% open, the SPY is implying a -0.94% open, and the QQQ implies a -1.13% open at this hour. In addition, 10-year bond yields are up sharply to 3.11% and Oil (WTI) is up a half of a percent in early trading.

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for the day include CTLT, HTHT, and PDD before the open. Then, after the close, HRI and YY report.

In economic news later this week, on Tuesday we get Conf. Board Consumer Confidence, July JOLTs, and a Fed speaker (Williams). Then Wednesday we see ADP Nonfarm Payrolls, Chicago PMI, EIA Crude Oil Inventories, and another Fed speaker (Mester). On Thursday Weekly Initial Jobless Claims, Q2 Nonfarm Productivity, Q2 Unit Labor Costs, PMI Mfg., and ISM Mfg. PMI are reported. Finally, on Friday we get Aug Avg. Hourly Earnings, Aug. Nonfarm Payrolls, Aug. Participation Rate, Aug. Unemployment Rate, July Factory Orders.

In earnings later this week, Tuesday we hear from BIDU, BMO, BBY, BIG, FUTU, IQ, AMRK, CHWY, CRWD, HPE, HPQ, and PVH. Then Wednesday we get reports from BF.A/B, CHS, DBI, DCI, and EXPR. On Thursday, FLWS, CPB, CIEN, GCO, GMS, MOMO, HRL, OLLI, PDCO, SAIC, SIG, TTC, WB, AVGO, JOAN, and LULU report. Finally, Friday there are no major reports.

Friday is a prime example of what happens when the market really wants to hear something. Mr. Market can really throw a tantrum when he doesn’t get what he wants/expects. However, we need to remember that the base case of markets is that they overreact, overreact to the overreaction, and then react again. That is what causes the unmistakable stairstep, zig-zag, or wave movements of price. So, at this point, we are back in a bear market…but we are over-extended to the downside in the short term. That doesn’t mean we have to rest or relief rally today…but it raises the probabilities. Just be wary of chasing gaps and run-away to the downside. Volatility is still high and traders have had a weekend to gather their wits and nerve since the unexpected bad news.

Demonstrate patience and wait for confirmation. Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: UXVY, SQQQ, SPXU, QID, PSQ, SNAP, MRVL, SNOW. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Though Thursday brought us another negative GDP, sharply rising bond yields, and declining corporate profit figures, the bulls said I don’t care, get out of my way so I can buy something. Their effort held index price support levels, and the VIX indicated fear continues to diminish. Although the number of earnings declines sharply today, inspiration will come in from economic reports and the Jerome Powell speech from Jackson Hole at 10 AM Eastern. With the Chairman expected to deliver a hawkish tone, how the market might react is anyone’s guess, so plan carefully and expect some wild price volatility.

Asian market mostly rises, with only Shanghai seeing a little red to close the week. However, European markets see mostly red in a choppy session as they cautiously wait for Powell’s comments. Likewise, U.S. futures point to a bearish open with pending economic data and all eyes on the Jackson Hole speech from the Chairman and what it might mean for the future market direction! So, buckle up the show is about to begin!

Economic Calendar

Earnings Calendar

The number of earings drop off shrply today with only 13 listed and just 5 confrimed. Notable reports include JKS, & SNP.

News and Technicals’

Fed Chairman Jerome Powell speaks Friday at 10 AM. ET in a much-anticipated appearance at the Federal Reserve’s annual Jackson Hole, Wyoming, symposium. Fed watchers do not expect a new message from the Fed chairman, just a tougher version of the central bank’s promise to slow inflation by raising interest rates. Powell is likely to emphasize that the Fed is unlikely to quickly reverse course after it reaches an end rate, as the futures market has been expecting. “I think we only need 100 basis points more,” Wharton business school professor Jeremy Siegel told CNBC’s “Squawk Box Asia.” “The market thinks it’s going to be a little more — 125, 130 basis points more. My feeling is we won’t need that much because of what I see as a slowdown.” “If you want to do it all at once, or you want to do it over a period of two to three meetings — it won’t make that much of a difference,” he said. U.S. Federal Reserve Chair Jerome Powell is slated to speak at Jackson Hole later on Friday, where he’s likely to emphasize that the Fed will use all the firepower it needs to snuff out inflation. U.K. energy bills to rise by 80%! The new cap will be in effect from October 1 to the end of the year, which is expected to rise further. The government is under pressure to announce greater support for households and a wide-ranging plan to oversee the energy supply industry through a crisis. However, the candidates to be the new prime minister have said a comprehensive strategy needs to wait until the leadership election on Sept. 5. A Chipotle Mexican Grill restaurant in Lansing, Michigan, became the chain’s first location to vote to unionize. Workers at the store voted 11 to three in favor of unionizing under the International Brotherhood of Teamsters. The win for Chipotle organizers in Michigan comes on the heels of more than 200 Starbucks cafes in the U.S. voting to unionize in the last ten months. Treasury yields ticked moved higher in early Friday trading, with the 12-month at 3.26%, the 2-year at 3.38%, the 5-year at 3.20%, the 10-year at 3.07%, and the 30-year at 3.28%.

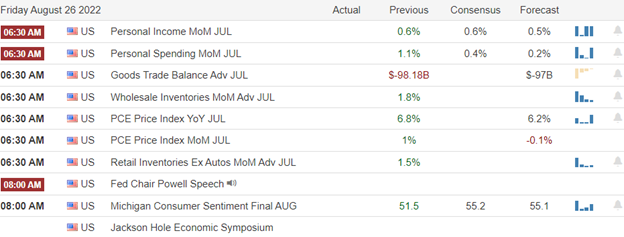

With a negative reading on the GDP, declining corporate profits, and mixed earnings results, the bulls said don’t care, get out of my way so I can buy something, as they defended the index chart price supports. Can they keep up that enthusiasm while likely facing a hawkish Jerome Powell speech from Jackson Hole? We should also remember that on Sept. 1st, the Fed will tighten the money supply by rolling off 90 billion from their balance sheet. So far this week, the market has largely ignored the weakening economic reports, so how they react to today’s International Trade figures, Personal Income and Outlay, Inventory data, and Consumer Sentiment is anyone’s guess. I would, however, suggest we could see substantial price volatility around the Chairman’s speech at 10:00 AM Eastern so plan carefully.

On Thursday, the SPY and QQQ gapped higher while the DIA opened flat. From there, all 3 major indices made a morning rally to the highs of the day at about 11 am. However, once again the whipsaw kicked in and a selloff took all 3 indices back down to the open value or below in just 30 minutes before grinding sideways for a couple of hours. At that point, the bulls rallied us back up to within shouting distance of the highs (or to new Highs in the DIA) again by 2:30 pm. Finally, a very strong rally in the last 45 minutes tool all 3 major indices out on their highs. This action is giving us white-bodied candles in the SPY, DIA, and QQQ. The QQQ and SPY both crossed back above their T-line (8ema) and the DIA is right at that level at the close.

All 10 sectors are green with Basic Materials, Technology, and Consumer Cyclical leading the way higher. On the day, SPY gained 1.41%, DIA gained 1.00%, and QQQ gained 1.77%. The VXX is down 0.51% to 19.70 and T2122 crossed back up into the overbought territory at 83.95. 10-year bond yields fell back to 3.03% and Oil (WTI) fell 2.09% to $92.91/barrel. Once again, this all took place on below-average volume.

In economic news, Q2 GDP came in a -0.6% which was better than the -0.8% forecast as well as Q1’s -0.9% print. Weekly Initial Jobless Claims also came in better than was expected at 243k (versus 253k consensus forecast) as well as slightly better than last week’s 245k number. In the afternoon, Fed Hawk Bullard told CNBC that he expects high inflation to persist and that interest rates are not yet high enough to begin curbing price increases. He went on to say he favors front-loading rate hikes and hopes to convince peers to vote for a benchmark rate of between 3.75% to 4.00% by year-end. Other Fed voters at Jackson Hole said that whether there will be a 0.75% or 0.50% hike in September is not decided yet and will depend on the 2 additional inflation and multiple jobs reports before the meeting. However, rates still need to rise to fight inflation.

On Thursday, AMZN announced they had struck a deal with hydrogen fuel cell maker PLUG to supply power to forklifts, long-haul trucks, and building operations starting in 2025. Part of the deal included PLUG giving AMZN a warrant to buy up to 16 million shares of PLUG with an exercise price of $22.98. (PLUG closed the day at $30.00.) AMZN also agreed to spend at least $2.1 billion on PLUG products over the 7-year contract. Later in the day, the California Air Resources Board voted to require all new cars sold in the state to be electric or electric hybrid by 2035. However, these regulations must still be approved by the US EPA.

In energy news, Reuters reported Thursday evening that ERCOT (the Texas Power Grid operator) has spent an additional $1 billion to avoid blackouts this summer. This comes in the form of rewards for industrial customers to cut usage, paying power generators a premium to maintain higher reserves (production capacity). The state set 11 demand records so far this summer. Elsewhere, OPEC+ is seeing more support for Saudi Arabia’s stated plan to curb oil supplies to “stabilize world oil markets.” Iraq, Algeria, Bahrain, Kuwait, Venezuela, Equatorial Guinea, Congo, Azerbaijan, and Libya all endorsed the plan to cut OPEC+ production. (Clarity on the move should be seen on this plan on September 5 when the group meets again.) Overnight, the UK Energy Regulator announced that they expect Britons to pay as much as three times last year’s price to heat their homes this coming winter (including an 80% hike in October). Meanwhile, Germany is looking at restricting companies able to benefit from higher natural gas prices amidst public outcry over record energy company profits and soaring consumer costs.

In miscellaneous market news, Texas accused BLK, CS, UBS and other European-listed financial companies of boycotting the state’s huge fossil fuel industry. (This is part of the state’s anti-ESG investing campaign.) The state claims it may divest billions of dollars in state pension funds from those companies and their funds. This may have big market price impacts on those stocks. For example, the Texas School Teach Retirement fund currently owns large positions in BLK. In unrelated news, after the close Thursday, the CBOE announced that it is in talks with IBKR, HOOD, VIRT and others about taking equity stakes in the recently purchased ErisX crypto exchange (to be renamed CBOE Digital). In telecom news, late last night, Elon Musk (SpaceX) and TMUS announced a joint venture aimed at eliminating cellular dead zones. This backup network will only be available to TMUS customers and initially will only cover SMS messages. However, the (at least initially) no-cost backup service will later be upgraded to cover voice calls and video streaming.

After the close Thursday, GPS, VMW, ULTA, and FTCH all reported beats on both the top and bottom lines. Meanwhile, DELL and MRVL both missed on revenue while also beating on earnings. On the other side, WDAY beat on revenue while missing on earnings.

Overnight, Asian markets were mixed but leaned to the upside on mostly modest moves. Shenzhen (-0.37%), Shanghai (-0.31%), and New Zealand (-0.16%) were the losing exchanges. Meanwhile, Hong Kong (+1.01%), Australia (+0.79%), and Japan (+0.57%) paced the remaining, gaining exchanges in the region. In Europe, stocks are mixed, but leaning red at mid-day, but again on mostly modest moves. Denmark (-1.30%) is an outlier. However, the FTSE (+0.04%), DAX (-0.41%), and CAC (-0.33%) are leading the region in a modest move lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a lower start to the day. The DIA implies a -0.29% open, the SPY is implying a -0.42% open, and the QQQ implies a -0.57% open at this hour. 10-year bond yields are back up to 3.071% and Oil (WTI) is up 1.3% to $93.74 in early trading.

The major economic news events scheduled for Friday include July PCE Price Index, July Personal Spending, July Trade Goods Balance, and July Retail Inventories (all at 8:30 am), Michigan Consumer Sentiment (10 am), and the Jackson Hole Central Banker Symposium continues with Fed Chair Powell Speaking (at 10 am). The major earnings reports scheduled for the day are limited to JKS before the open. There are no reports after the close.

Markets will have their eyes focused on Fed Chair Powell’s speech this morning. While he is very unlikely to tell the bulls what they want to hear, the bears are also not going to get everything they want. Expect him to say some version of “it will depend on coming data” when he addresses September Fed actions. Premarket action is looking like a battle around the T-line in all 3 major indices as traders wake up to a modestly down “wait and see” market. The pullback was broken (at least temporarily) on Thursday. However, the new short-term bullish trend is not running rampant yet. So, caution is in order, volatility is expected, and even if we get a good clue from Powell…it is Friday with a long weekend news cycle ahead.

Demonstrate patience and wait for confirmation. Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls squeaked out a win on Wednesday, defending index price support levels in an otherwise mostly choppy day despite the declining Durable Goods and Pending Home Sales. This morning’s uncertainty will be the latest reading on GDP and Jobless Claims before the talking heads at Jackson Hole circulate a lot of hot air. So, expect some volatility as they put their particular spin on the market and the overall economic conditions. We also have our most important day of earnings this week to keep us on our toes and provide inspiration to the bulls or bears. Let’s get ready to rumble!

Asian markets rebounded while we slept, with the Hang Seng surging a whopping 3.63% by the close, even with expectations of a Hawkish Fed statement at Jackson Hole. Likewise, European markets trade cautiously in a choppy morning session with eyes on Jackson Hole. Nevertheless, futures point to a bullish open with a full day of talking head spin, a busy earnings calendar, and pending market-moving economic reports before the bell. However, anything is possible by the open depending on the pre-market data’s reaction.

Economic Calendar

Earnings Calendar

We have a more hectic day on the Thursday earnings calendar with about 60 companies listed but less than 30 confirmed. Notable reports include ANF, AFRM, BURL, COTY, DELL, DG, DLTR, FTCH, GPS, HAIN, HIBB, MRVL, OLLI, PTON, SAFM, TITN, TD, ULTA, VMW, & WDAY.

News and Technicals’

According to an internal memo on Wednesday, Amazon is shuttering its telehealth service, known as Amazon Care. Amazon Care launched in 2019 as a pilot program for employees in and around the company’s Seattle headquarters. However, it’s unclear how much traction Amazon Care had gained. Sony on Thursday raised the recommended retail price of its PlayStation 5 games console in several international markets citing the global economic environment, including high inflation. The Japanese gaming giant said that the price hikes are effective immediately except in Japan, where they will begin on Sep. 15th. Sony is not raising the price of the PS5 in the U.S. Energy consultancy Auxilione estimates the price cap, currently at £1,971 a year, could climb to as high as £6,089 next April as Britain’s cost-of-living crisis worsens. Around one in seven working adults in the U.K. worked from home between April 28th and May 8th. However, that number could decrease as bills surge, according to Sarah Coles, the senior personal finance analyst at Hargreaves Lansdown. Nvidia reported second-quarter earnings that missed Wall Street expectations for revenue and earnings per share. The disappointing report aligned with Nvidia’s preliminary earnings two weeks ago. Nvidia said that the miss was because of lower sales of its gaming products, primarily graphics cards for PCs facing “challenging market conditions.” Salesforce beat quarterly expectations but came short on guidance for the current quarter and the full fiscal year. The enterprise software maker is raising prices on Slack after acquiring the team communications app last year. Salesforce said its board approved $10 billion on the company’s first buyback program. Treasury yields dip slightly ahead of Fed comments at Jackson Hole, with the 12-month at 3.26%, the 2-year at 3.37%, the 5-year at 3.19%, the 10-year at 3.09%, and the 30-year at 3.30%.

Despite declining Durable Goods and Pending Home Sales., the bulls won another mostly choppy day Volume remained noticeably anemic as the bulls worked to hold price support levels in the index charts. Although NVDA and CRM disappointed after the bell, names like ADSK and NTAP jumped higher on a mixed afternoon of earnings results. Today begins the Jackson Hole Symposium, so expect a glut of talking heads hitting the news cycle to put their particular spin on the market and economic condition. However, before all that hot air gets circulated, we will get a reading on GDP and Jobless Claims to add a dose of uncertainty before the open. As you plan forward, remember we have the Fed’s favorite measure of inflation, the PCE, coming out Friday morning before the Jerome Powel comments at 10 AM Eastern.