***Sorry everyone the YouTube is being very slow this morning and I don’t know when or/if the daily video will be active for viewing. Its out of my control! 🤬

Yesterday’s price action may have hinted at a slowing in the current rally; the bulls are clearly in control, and traders have zero concern about the 8.5% inflation and a hawkish Fed. However, with significant overhead resistance and slowing housing and manufacturing sectors as a persistent bond inversion continues, there are still willing buyers that could keep the rally going through the rest of the week. Inspiration for buyers or sellers will come from potentially market-moving economic reports and a handful of notable earnings.

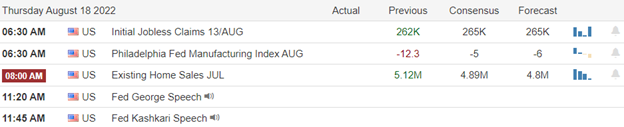

During the night, Asian markets closed in the red across the board, with Goldman and Nomura again cutting China’s GDP outlook. European markets traded with choppy caution after a 50 basis point increase from the bank of Finland. U.S. futures trade cautiously bullish ahead of jobless claims, manufacturing, and housing data. Will the data inspire the bulls or the bears? We will soon get the answer.

Economic Calendar

Earnings Calendar

We have just over 40 companies listed on the Thursday earnings calendar, with around 20 confirmed reports. Notable reports include AMAT, BILI, BJ, CSIQ, EL, KSS, MLCO, NTES, NIO, ROST, TPR, and WB.

News & Technicals’

According to the July minutes, the Fed sees interest rate hikes continuing until inflation eases substantially but did not provide specific guidance. Tensions between the U.S. and China are not helping President Joe Biden’s efforts to control inflation; economist Jeffrey Sachs told CNBC’s “Street Signs Asia.” He said inflationary pressures would likely persist for the foreseeable future. Norway’s central bank hikes rates by 50 basis points in a fight to control surging inflation. The increase takes the Norges Bank’s sight deposit rate to 1.75% from 1.25%, exceeding its prior forecast in June. Norwegian inflation hit an annual 4.5% in July, up from 3.6% in June and well ahead of consensus projections for 3.8%. CNBC’s Jim Cramer on Wednesday said the market could continue to stall out after Wednesday’s slump and urged investors to trim some of their positions. “Things can still go right. I don’t want to freak you out. I think stocks need a cooling-off period after this miraculous run, and we’re getting one for certain,” he said. Iranian negotiating team adviser Mohammad Marandi said on Monday that “we’re closer than we’ve been before” to securing a deal and that the “remaining issues are not very difficult to resolve.” The Biden administration says it’s ready to sign a deal quickly if Iran accepts it. Three major sticking points remain, however. According to Oxford Economics ‘ lead economist, Tommy Wu, developer cash flows through July are down 24% year-on-year on an annualized basis. The data showed a sharp slowdown from growth for nearly every year since at least 2009. In addition, recent homebuyers’ refusal to pay mortgages has worsened real estate developers’ funding situation. Despite multiple reports of government plans to keep developers funded, the central government has yet to announce broader support for real estate officially. Goldman Sachs downgrades its 2022 forecast for China to 3% from 3.3%. Nomura cuts its full-year growth outlook to 2.8% from 3.3%. Both cite weak demand, uncertainties over China’s zero-Covid policy, property woes, and an energy supply crunch. Cisco gave better-than-expected guidance for its full 2023 fiscal year. Management touted strong demand despite a volatile backdrop. Treasury yields ticked slightly lower in early Thursday trading, with the 2-year at 3.27%, the 5-year at 3.04%, the 10-year at 2.88%, and the 30-year at 3.13%.

Though yesterday’s selling may hint at slowing the current bull run, the 8.5% inflation and hawkish Fed seem to be of zero concern to traders willing to buy near overhead resistance. Moreover, index chart technicals and trends remain bullish though housing and manufacturing are slowing. Finally, rising bond yields point to a troubling and deepening recession possibility as the rate inversion persists, but the overall market seems unconcerned. Thursday brings a busy economic calendar of potential market-moving reports with a handful of notable earnings to inspire. Of course, we will soon find out if all the data inspires the bulls or bears, so buckle up and plan your risk carefully.

Trade Wisely,

Doug

Comments are closed.