Holiday week trading is typically challenging due to the rapid decline in volume as traders shut down for travel. However, this week could be different with all the news hype about the beginning of a Santa Claus rally and an economic calendar full of market-moving data. Then don’t forget the possible market volatility that could happen should Biden change with the Fed Chair! With so much data coming our way, expect significant price volatility even as we pump the tech giants to new records and incredible P/E ratios. Remember to take some profits along the way.

Asian markets traded mixed overnight after the central bank kept loan rates steady. European markets trade mixed and flat this morning due to rising pandemic restrictions and protests that have erupted as a result. We don’t seem to have the same concerns with the U.S. futures, pointing to a bullish open that includes fresh new records as the tech giants continue to surge higher.

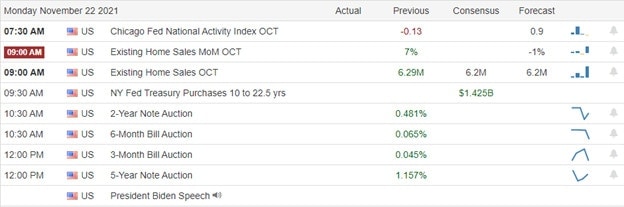

Economic Calendar

Earnings Calendar

We have 36 companies listed on the earnings calendar to kick off the shortened holiday week, with several unconfirmed. Notable reports include A, ARWR, IBEX, KEYS, NIU, URBN, & ZM.

News & Technicals’

The People’s Bank of China deleted several phrases in its latest monetary policy report, a move that economists say signals a shift toward easier policy. Despite signs of a growing slowdown in the economy, the phrases had signaled a level of restraint in central bank policy. However, the PBoC maintained a tough stance on the property market, which has struggled in the wake of Beijing’s crackdown on real estate developers’ high debt levels. In addition, Illinois legislators agreed to spend up to $694 million over the next five years to keep a handful of nuclear power plants open. The operator of the plants, Exelon, said they were losing hundreds of millions of dollars and that nuclear can’t compete with cheap natural gas and subsidized wind and solar. Critics say that Exelon had the state over a barrel and that longer-term solutions are necessary to make clean energy cheaper and more accessible. Protests against fresh Covid restrictions have continued to rock Europe over the weekend. There were demonstrations in Vienna, Brussels, and Amsterdam against new Covid rules. In addition, new coronavirus cases continue to surge across the continent. Treasury yields rose in early Monday trading, with the 10-year climbing to 1.5583% and the 30-year advancing to 1.9107% as we wait on the Biden Fed Chair appointment.

Holiday trading is always a hit-and-miss scenario when it comes to volume. That said, the news has laid it on thick over the weekend that we have the perfect setup for the so-called Santa Clause Rally to begin. Now toss in possible uncertainty with a Fed Chair appointment, inflation data, and Durable goods, GDP, and Personal incomes combined with likely declining volume throughout the shortened week, and anything is possible! However, the weekend hype seems to be working with the future, suggesting nothing but blue skies as we continue to extend the tech giants to phenomenal P/E ratios. So stay with the trend, but please remember to take some profits along the way just in case a scare or two comes along that engages the bears and price volatility.

Trade Wisely,

Doug

Comments are closed.