With more Federal stimulus on the way, the bulls continue the drive higher yesterday after news that the Senate may allow a reduced unemployment bonus payment of $100 per week. Today we have our biggest round of earnings this week and will also get the latest reading on unemployment. So far, the market has shrugged off the rising tensions between the US and China though many are warning that impacts could have significant market impacts. For now, the bulls are large and in charge, with no signs of slowing down in the charts.

Asian markets closed mixed but mostly lower overnight as US/China tensions grow. However, European markets are decidedly bullish, seeing green across the board. US Futures point to another gap up open focused on more stimulus, earnings reports.

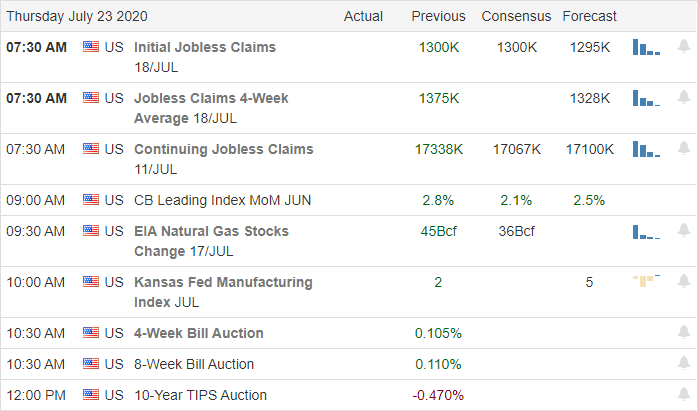

Economic Calendar

Earnings Calendar

Today we have our biggest day of earnings this week with 110 companies reporting. Notable reports include APD, ALK, AB, T, AN, BX, SAM, CTAS, CTXS, DHR, DWO, EW, EXPE, FCX, HSY, HBAN, INTC, KMB, MTB, MAT, NUE, PNR, PBCT, PHM, SWKS, LUV, TSCO, TRV, TWTR, UNP, VRSN, & GWW.

News and Technical’s

Focused on hopeful earnings reports, the indexes continued the rally with a strong late-day surge. The bulls shrugged off rising tensions between the US, and China and the markets remain unconcerned about the protest violence around the country and or the rising pandemic death toll. After the bell, yesterday MSFT reported as expected but sold off about 2%, and TSLA reported is 4th straight profit seeing a rally in aftermarket trading. The Senate reportedly reached a tentative $1 trillion agreement on the next round of federal stimulus. We are still waiting on the retaliation that Beijing has vowed on the closure of the Houston consulate. Some have started to mention the tensions as the next cold war and concerns are growing as to far the two countries will go and how deep the possible market impacts could become in the near future.

Technically speaking, the indexes are in bullish patterns, and the bulls are pushing yet another gap up open this morning. Today we have our biggest day of earnings this week and will get the latest reading on unemployment which is expecting about 1.3 million new filings. About 20 million Americans remain unemployed, which is far higher than during the depths of the 2008 financial crisis. It would seem as long as the central banks and government stimulus continues to deficit spend employment is no longer a factor considered for economic health. I suspect we can expect more of the same as the presidential election nears. Buckle up for a bumpy ride.

We saw a gap down in the large caps and a small gap up in the QQQ on Wednesday. However, most of the day was a rollercoaster until a late-afternoon rally closed markets near their highs. This gave us a Bull Engulfing candle in the SPY and DIA as well as a Bullish Doji Harami in the QQQ. On the day SPY gained 0.56%, DIA gained 0.63%, and QQQ gained 0.35%. VXX was down a tad to 29.16 and the T2122 4-week High/Low Ratio remained deep in over-bought territory at 94.80. 10-year bond yields fell slightly to 0.599% and Oil (WTI) was flat, closing at $41.89.

The GOP continued to haggle over what their own proposal for the next stimulus bill will be, but they appear to be making progress. Among the key areas of disagreement is whether (and how) to extend “enhanced unemployment insurance.” There are GOP camps fighting for $400/week, $200/week, and $100/week as well as some who want to drop it altogether. Still, the Senate Republicans announced overnight that they have reached a “fundamental agreement” on the basics on their side of the table. (Reportedly a $1 Trillion bill proposal.) So, now negotiations with the Democrats (whose own $3.5 Trillion proposal has been in place since May) can now actually get in gear. (As mentioned yesterday, Congress is not going to want to hang around DC long since most of them want to go home for politicking.)

In the US, the virus numbers show we have 4,101,308 confirmed cases and 146,192 deaths. The country saw just under 72,000 new cases and a little over 1,200 new virus deaths on Wednesday. CA also surpassed NY for the dubious honor of becoming the state with the most confirmed cases to date. IN, MN, OH, and Washington DC all joined the group of states ordering a statewide mask mandate in lieu of a Federal mandate. The head of FEMA also told CNBC that the Federal Government still does not have enough PPE gear and his agency as well as the states are still aggressively trying to buy more. He said that due to logistics issues and overall short supply, it is possible that virus hot-spots could run out on a temporary basis, but the continue to work on it.

Globally, the number of cases has reached 15,405,069 confirmed cases and 631,015 deaths. Brazil reported a record of almost 68,000 new cases Wednesday, days after the WHO had said new cases had reached a plateau. India’s exponential growth curve for new cases continues. In Tokyo, they also saw a new record-high number of cases today, although the Japanese number is hardly worth mentioning in comparison to Brazil or the US. South Korea also announced Thursday that it has fallen into a technical recession as of Q2 due to the virus. Australia had said overnight that the virus had shrunk its GDP by 5%.

Overnight, Asian markets were mixed and showed a move of less than a percent both directions. China, Japan, and Korea were down while Hong Kong and Australia were up. In Europe, markets are mixed, but also broadly “modestly green” with just a few stragglers so far today. In the US, as of 7:30 am futures are pointing to a modest gap higher of about a third of a percent with the exception of the QQQ which is looking at three-quarters of a percent gap higher.

The only major economic news for Thursday is Weekly Initial Jobless Claims (8:30 am). However, once again there are a massive number of major earnings reports, including AAL, AB, ADP, ADS, ALK, ALLE, AN, BX, CVE, CTAS, CTXS, DGX, DHR, DOW, FAF, FITB, FCX, GWW, HBAN, HSY, KMB, MTB, MTRN, NUE, ORI, PHM, PNR, POOL, RS, T, TECK, TSCO, TRV, TWTR, UNP, and WSO. Then after the close ETFC, EW, FE, INTC, RHI, SKX, SWKS, and SIVB report.

Wednesday’s rollercoaster and late-day rally did nothing to break the bullish trend. We should expect volatility to continue as virus news remains bad (but bulls will see only the rosy scenario) and stimulus negotiations are now beginning. However, earnings news continued to be generally good as of last night (against extremely reduced expectations) and there will be more of that this in morning’s reports. US-China relations remain the wild-card since the ball is in China’s court at the moment.

In this sort of environment, all we can do is watch the short-term chart and follow the trend. Remember to keep an eye on those FAANG stocks as our “canary in the coalmine.” Remain focused on your trades and don’t chase, don’t predict, and always take profits as you go. Also remember that in earnings season, we should be wary of both reactions and re-reactions.

Ed

The Daily Swing Trade Ideas for today: AMD, NVAX, GDOT, WU, ABT, COF, MA, XRT, ALGN, CVX. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The State Department orders the Chinese Houston consulate to close after charging two Chinese nationals in vaccine hacking attacks against American companies. Beijing, of course, vows retaliation as the tensions continue to grow and adding another layer of uncertainty for the market to deal with as earnings season ramps up. Pressure is also increasing on the economic recovery as the US death toll tops 1100 for the first time since April with the President stating its likely to get worse before getting better.

Asian markets closed the day mixed, but mostly lower and European indexes trade in the bearish territory this morning, reacting to the rising tensions between the US and China. US futures have rallied off overnight lows ahead of Housing Data, and a big round of earning that includes MSFT after the bell today.

Economic Calendar

Earnings Calendar

On the hump day earnings calendar, we have 47 companies reporting quarterly results. Notable reports include MSFT, TSLA, ABB, ALGN, BKR, BIIB, CP, CMG, CSX, DFS, DOV, EFX, HCA, KEY, KMI, NDAQ, RCI, SLG, SAVE, UAL, & WHR.

News & Technical’s

With tensions growing between the US and China, the State Dept. orders China to close the Houston consulate as Beijing vows retaliation. The decision come after the US charges two Chinese nationals in vaccine hacking attacks. The President, in his first coronavirus briefing in several weeks, said we should expect the pandemic to get worse before it gets better and encourages Americans to wear masks to help prevent the spread. The briefing came on the heels of the largest daily death toll spike since April topping 1100. United Airlines posts a 1.5 billion dollar loss in pandemic impacts that sadly continue to grow daily. During the night, the Alaska Peninsula experience a powerful 7.8 earthquake. Worries of a possible tsunami sent residents fleeing to higher ground, but that threat has now passed. Gold is soaring this morning after Europe delivers another 2 trillion in virus stimulus. Here in the US, Congress continues to haggle over their next stimulus package that may happen as soon as next week.

Yesterday’s gap up open tested but ultimately failed the breach of the resistance of the Island reversal pattern created in early June price action. However, the SPY not only breached the resistance but yesterday broke above its island pattern and, although found some profit-taking by the end of the day, managed to hold onto the new level as support. After attempting a push to new record highs, the QQQ seemed to run out steam leaving behind a contradictory dark cloud pattern while still in a bullish trend. In an interesting turn of events, IWM finished the day strong with the aid of a financial rally. With tensions rising with China, futures were a bit bearish during the night, but as is the norm lately, the morning pump has begun ahead of housing numbers and a big wave of earnings reports. Expect price volatility to remain high.

Markets gapped strongly higher at the open Tuesday on the EU recovery deal, general recovery optimism, and good earnings. However, the huge tech names sold off immediately, and the rest of the market could not fight that wave, finally following suit in the afternoon. The QQQ closed down 1.04%, but the large-caps eked out gains as SPY closed up 0.18% and DIA closed up 0.57%. The VXX was flat at 29.48 and T2122 climbed all the way to the top of overbought territory at 96.49. 10-year bond yields fell slightly to 0.604% and Oil (WTI) climbed 2% to $41.76/barrel.

Republicans met and began cobbling together their proposal for the next stimulus bill, a necessary precursor for the start of negotiations with Democrats (whose plan has been passed and, on the table, since May). As of Tuesday, the GOP has agreed amongst themselves that businesses need more PPP loans, other grants, and liability protection at a minimum. They also will ask for $105 billion for schools. However, the Payroll Tax Cut that the President demanded didn’t appear to make the list since it is being opposed by even some Republicans. Later, House Minority Leader McCarthy told CNBC he does not expect a final deal to be negotiated and passed until August. Still, Congress will want to adjourn again and get back home to begin their reelection campaigns. So, early August is probably as late as it will be allowed to go.

The other major storyline overnight is the ratcheting up of trade tensions with China. This may be a legitimate confrontation about the activity or something that would always be legitimate but is done now for unrelated purposes. In any event, the US charged (in absentia) 2 Chinese men for hacking and attempted (but unsuccessful) theft of medical data. The US also abruptly forced the closure of the Chinese Consulate located in Houston. The Chinese have vowed retaliation for both through their state-run media. Regardless of the true reasons behind these moves or their validity, it does stir up fear of another round of trade war.

In a one-off story snuck out overnight, Citadel Securities announced it has agreed to be was fined by FINRA for front-running client orders in a settlement agreed July 16, but announced in a Tuesday press release. The fine was a paltry $700,000. However, this case had been dragged out so long that the activity covered dates from way back in 2012-2014. So, apparently it pays to hire top FINRA and SEC officials as your General Counsel as Citadel had done.

In the US, the virus numbers show we have 4,028,733 confirmed cases and 144,958 deaths. This includes 67,000 new cases Tuesday. TX and FL continue to report record-high 7-day average new deaths. However, at least for the first time in over a week, FL reported under 10,000 new cases with 9,400). LA Governor Edwards announced Tuesday the state will remain in phase 2 of reopening for at least another 2 weeks (rather than move to phase 3 on Friday as previously scheduled). On the business side there was good news as BBY announced that sales are returning (up about 2.5% in Q2) and they have brought back about half of the employees furloughed in April.

Globally, the number of cases has reached 15,120,686 confirmed cases and 620,263 deaths. Asia is again becoming a hot spot. For example, India continues to see a surge as they reported over 39,000 new cases on the day in their very underwhelming testing program (given their huge population). The outbreak in Australia also continues, especially in its two largest states. Japan also is back near their record-high in cases although the last 2 examples are tiny relative to US numbers, due to the tiny Australian population and Japan’s overwhelming acceptance of mask-wearing. Closer to home, Mexico surpassed 40,000 deaths as their 7-day average of new cases also sits at an all-time high.

Overnight, Asian markets were in the red with the exception of China and Taiwan, which were mildly green. These moves came mostly in response to trade fears. The same is true in Europe, with only Russia above break-even (barely) at this point in their day. In the US, as of 7:30 am futures are pointing to a modest gap lower of about a quarter percent.

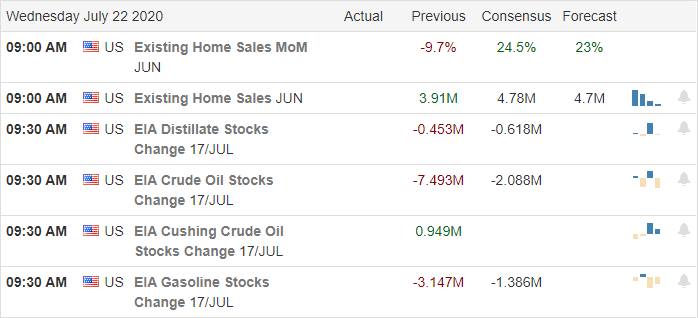

The major economic news for Wednesday is limited to June Existing Home Sales (10 am) and Crude Oil Inventories (10:30 am). The major earnings reports on the day include ABB, APH, BIIB, BKR, CP, CSTM, DOV, HCA, IQV, KEY, KNX, LAD, NQAD, NTRS, NVR, RCI, SLGN, and TMO before the open. Then after the close, CMG, CSX, EFX, KMI, LSTR, LVS, MSFT, MTH, PLXS, RJF, RUSHA, SU, TRN, TSLA, UFPI, and WHR.

Tuesday’s fading of the gap higher did nothing to break trend. We simply printed a black candle in an uptrend. The sentiment drivers are likely to be earnings (since we are in silly season), stimulus bill negotiations, and US-China relations. Remember to watch those FAANG stocks as they proved again yesterday that it’s very hard for the market to buck any move they make as a group. Remain focused on short-term charts and don’t chase, don’t predict, and always take profits as you go. In earnings season, be wary of both reactions and re-reactions.

Ed

The Daily Swing Trade Ideas for today: NBL, CWH, WDC, PENN, OIH, AIG, XOP, WFC, DKNG, X, MRO, SLB. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

New of more government stimulus provides the bullish energy to set new NASDAQ records amid rising infections, hospitalizations, and deaths. Europe leaders reach a deal to provide another $858 billion (US Value) in stimulus, and reports suggest Congress is aiming at a total that will top 1 trillion. There seems to no lack of desire to buy up stocks at any price as many issues hit new record highs yesterday ahead of earnings their earnings reports. With a light day of economic news, earnings and stimulus news will take front and center as futures push for another record high open today.

Asian markets traded higher overnight, supported by hopeful vaccine news. European markets are decidedly bullish in reaction to the stimulus deal, and the US futures all point to a bullish gap-up open fueled by more government deficit spending. Continue to ride the wave as long as it lasts.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have 43 companies stepping up to report results today. Notable reports include CNI, COF, KO, CMA, IBKR, ISRG, IRBT, LMT, LOGI, NAVI, NVS, PM, PLD, SNAP, SYF, TER, TXN, & UBS.

News & Technical’s

Hopeful vaccine news and lots of talk about government stimulus big tech led Monday’s rally that inked another all-time high close for the NASDAQ. At the same time, virtual infections, hospitalizations, and deaths rose. According to reports, EU leaders reached a deal of fiscal stimulus that totals $858 billion, and the US is shooting for a plan that will add at least another trillion in US stimulus. A new study from New York suggests that as many of 1/3 of businesses will never reopen due to pandemic impacts, but as of now, the market seems utterly unconcerned about unemployment. UBS reported an 11% fall in second-quarter profits early this morning and warned of continued credit losses, but the stock is gapping up this morning. KO reported a 33% decline in earnings; however, it sees demand improving as lockdowns ease, pushing the shares higher this morning. Chicago took steps to increase COVID restrictions yesterday, and according to reports, LA County is on the cusp of another shut-down in the battle against the virus.

DIA, SPY & IWM setup yesterday with bullish patterns with the big-5 tech giants doing the majority of the lifting. The QQQ hit new record highs, and the US futures point to more records at the open as the race to buy stocks at all-time highs continues. With a very light day on the economic calendar, earnings reports and government stimulus news will take front and center. Somehow COVID, unemployment, and year over year, declining company revenues no longer matter. Stay with the bullish trend but remain focused and flexible because this sensitive news market has proven several times how quickly it can reverse.

Markets opened flat Monday and after a few minutes of pullback, the bulls stepped in and rallied all day long. The big tech stocks led the way as TSLA was up 9.47% and AMZN was up 7.93%. Initial vaccine test news out of the UK also led to optimism. The DIA was the outlier, printing another indecisive Doji. However, QQQ and SPY both printed strong Bullish candles coming off last week’s consolidation. At the close, SPY was up 0.81%, DIA was up 0.03%, and QQQ was up 2.84% (a new all-time high close). The VXX fell back below 30 to 29.23 and T2122 fell out of overbought territory to 70.18. 10-year bond yields fell slightly to 0.613% and Oil (WTI) was flat, closing at $40.69/barrel.

The EU finally reached a deal on a recovery plan last night. The $860 billion plan includes 52% of the money distributed as grants to the 27 member countries and the remaining 48% will be given out as loans. They will fund the plan through EU-backed bonds that will stop being printed in 2026 and will be paid off by 2058. They also announced that they will need additional taxes to repay those bonds. The new taxes will include a carbon tax and a non-recyclable waste tax. Quite a contrast to US governance.

Several businesses announced layoffs or buyouts. Among them are LinkedIn, who will cut 6% of their workforce. LUV also announced that 17,000 employees had volunteered for early retirement or contract buyouts.

In the US, the virus numbers show we have 3,961,805 confirmed cases and 143,864 deaths. The good news is that daily new cases fell below 63,000 Monday for the first time in over a week. The bad news is that deaths ticked up on the day, but still below the 7-day average. So far, only 28 states have listened to experts and instituted state-wide mask mandates. However, several others have partial mandates or municipal-level mask orders in place. The rest can’t bear the idea of government mandates, even if they believe wearing a mask is in the public good. (I’m unsure whether the freer states also have looser laws on public nudity or driving without a seatbelt. lol) However, for traders the impactful issue is that in the absence of mandates it becomes retailers and restaurants that must enforce a mask rule and that will continue to generate bad press or at least hurt feelings among some former/potential customers.

Globally, the number of cases has reached 14,881,625 confirmed cases and 613,996 deaths. In Spain, a new outbreak has occurred in a traditional summer holiday region (including Barcelona). No new lockdown has been ordered, but the public has been “urged to stay home.” Meanwhile, the UK reported a 4.5% drop in real wages for Q2. This was the largest drop since the 1970s oil crisis according to a report from Resolution Foundation in London. Real Wages or Standard of Living is a measure of disposable income and the drop considers lost wages as well as price inflation.

Overnight, Asian markets were green across the board. The strongest showing was made in Hong Kong and Australia, but the rally was broad-based. The same is true in Europe, where the recovery plan deal (after 5 days of heated negotiation) lifted market expectations. In the US, as of 7:45am futures are pointing to a gap higher of 0.7%-0.9% on Monday evening’s IBM beat and Tuesday Morning’s KO beat.

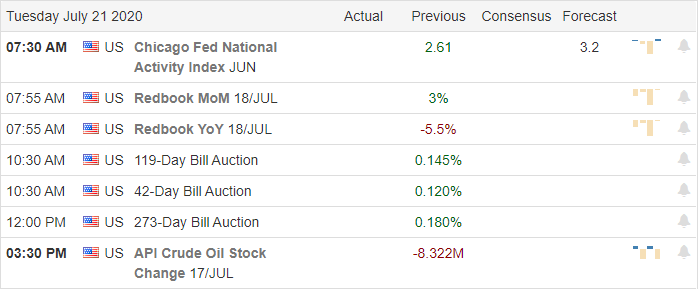

There is no major economic news for Tuesday. The major earnings reports on the day include CIT, CMA, GPK, KO, LMT, MUSA, NVS, PCAR, PLD, PM, SNV, SYF, and UBS all before the open. Then after the close AGR, AMTD, COF, CNI, CSL, IBKR, ISRG, NAVI, SUM, TER, TXN, UAL, and WRB all report.

Monday’s rally has bulls off and running this week. However, it is possible we drift until a deal is reached on the next US stimulus (recovery) bill being negotiated this week. Keep an eye on those FAANG stocks that have been the market’s “canary in the coalmine.” They clearly signaled yesterday’s rally and it would be very hard for the market to fight them if they all go one direction. Remain focused on short-term charts and don’t chase, don’t predict, and always take profits as you go. Remember we are in earnings season now, so some surprises are likely to happen…plus usually every initial reaction is met with an “on second thought” re-reaction. So be nimble.

Ed

The Daily Swing Trade Ideas for today: MS, NIO, FVRR, ROKU, PINS, KR, SNAP, ETSY, UBER, MU. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

As we begin a new week, an economic uncertainty continues to grow as the fast-spreading virus threatens shutdowns and fills hospitals ICU units to capacity. However, the market seems relatively undeterred with visions of enormous government stimulus spending hopes on the horizon in Europe and the United States. The big question yet to be answered is, can we deficit spend enough to cover the business impacts of the pandemic? With a light economic calendar, a busy earnings calendar, and pandemic uncertainty rising expect price action to remain volatile and challenging.

Asian markets closed the overnight mixed but mostly higher as the SHANGHAI rallied more than 3%. European markets trade mixed with EU leaders deadlocked on a massive stimulus coronavirus recovery fund. US futures have rallied off overnight lows ahead of earnings reports indicating a flat to slightly bearish open with NASDAQ futures bank in the green. Buckle-up and stay focused and flexible.

Economic Calendar

Earnings Calendar

On the Monday earnings calendar, we have 22 companies reporting quarterly results. Notable reports include PEP, HAL, MAN, PETS, CCK, IBM, LOGI & STLD.

News and Technical’s

Concern is rising as US infection rates top 3.7 million with a death toll moving over 140,000 this weekend. Florida has reported more than 10,000 new infections in the last 5-days as space in ICU units in several hot spot states are reportedly at capacity. As the healthcare system strains to keep up, the market seems transfixed on hopes of massive government stimulus in the pipeline in Europe and the United States. I guess the question yet to be answered is, can the government actually buy our way out of this pandemic without a massive debt crisis as the after effect? I guess only time will tell. I think one of the most honest answers I’ve heard came from Jamie Dimon’s warning for the US economy this weekend, “nobody knows what comes next.”

Technically the indexes continue in bullish trends even with the palpable uncertainty that lies ahead. This week we have a relatively light economic calendar, but traders will have to navigate a minefield of earnings reports the could create some significant price volatility. Futures opened on a positive note last night but quickly slipped negative, suggesting that Florida may have to shut down once again. However, in the normal fashion of late, the morning pump has rallied the futures well of the lows currently indicating a flat to everso slight bearish open as we wait on morning earnings. Stay flexible with an ear to the news that could quickly create reversals both up and down.

Markets gave us the epitome of “the summer blahs” Friday, essentially treading water in an indecisive day of trading. The SPY and QQQ gave us small gaps higher and the DIA a small gap lower at the open. The SPY and QQQ then printed Doji candles while the DIA printed a small Bearish Engulfing of a Doji. At the close, SPY was up 0.29%, DIA down 0.27%, and QQQ up 0.12%. The VXX fell to 30.62 and T2122 (4-week New High/Low Ratio) fell a bit to 94.00, which is still deep into the over-bought territory. 10-year bond yield rose slightly to 0.623% and Oil (WTI) closed down a tad to $40.57/barrel.

Treasury Sec. Mnuchin told Congress Friday they should forgive all small business PPP loans (regardless how the money was used), though he did acknowledge some measure of fraud prevention would be needed. He didn’t specify how he defines “small business” and as of his testimony, there were still over $132 billion of PPP funds approved that had not been requested. Nonetheless, Mnuchin also recommended a second round of PPP loans (companies allowed to take a second loan). In separate testimony, former Fed Chair Yellen told Congress she is extremely worried that if extended unemployment was not renewed, it could be a catastrophe for the economy. Sunday White House Chief of Staff Meadows said that real negotiation of the next virus stimulus bill will begin Monday.

After the close Friday, the US Bureau of Labor Statistics reported that Q2 saw the greatest jump in average weekly earnings in the country’s history (a 10% increase in one quarter). While this seems like good news, experts say it is actually misleading. They say this was bad news, because it reflects that high salary workers were being retained while a much larger percentage of the hourly workforce and low-level salaried employees were let go. It’s unclear to me how this is different than any other point in time as the supposed high-value employees are always first hired, last fired while by definition the lower-cost workers are often an after-thought to businesses. So, I don’t know if I agree with analysts. You decide.

In the US, the virus numbers show we have 3,898,639 confirmed cases and 143,289 deaths. The 7-day average of new cases is almost 68,000 and the 7-day average of virus deaths is just under 800 as of Sunday. And while 38 states have 7-day average new cases that increased by at least 10% week-on-week during most of last week, as of Sunday we are down to 32 rising at least that much, with 10 states now neither rising nor falling by at least 10% and 2 states are down more than 10%. Also, so far at least, hospitalizations have not yet exceeded the April peak. The only caveat with that good news is that hospitalizations tend to lag infections by 3 weeks and deaths tend to lag another 1-2 weeks.

Globally, the number of cases has reached 14,668,298 confirmed cases and 609,511 deaths. The UK reported that their economy recovered much less than was expected in May as their easing got underway. The UK GDP grew 1.8% for the month versus a consensus expectation of 5.5% growth. In China, supply chain issues (such as filling orders for PPE gear) are being caused by massive flooding across their nation. The flooding has exacerbated already jammed transportation infrastructure (such as ports) that have yet to recover from the backlogs caused by Feb.-Mar. shutdowns. In the EU, 3 days of negotiation over a stimulus package details and a 5-year budget have yet to produce a deal. In fact, negotiations are heated with multiple “table pounding” arguments reported. (That makes an interesting dichotomy with the US. The supposedly socialist Europeans are fighting tooth-and-nail over taxing and spending $850 billion (with a population of 450 million people), while the supposedly capitalist US has had no trouble at all spending trillions and trillions of dollars (so far) with 330 million people.)

Overnight, Asian markets were mixed, with China up strongly, India up modestly, Japan and South Korea flat and the rest of the region in the red. Europe is also mixed, but leans toward the green and is also little-moved so far. The FTSE is down 0.54%, DAX up 0.31%, and CAC down 0.21% at mid-day. The rest of the continent is mixed, but leaning green. In the US, as of 7:30am futures are flat, just on either side of break-even.

There is no major economic news for Monday. The major earnings reports on the day include CALM, HAL, LII, and MAN before the open as well as CCK, CDNS, IBM, LOGI, STLD, and ZION after the close.

Friday’s candles were indecisive for the third day in a row with neither the bulls nor the bears gaining traction. Expect more volatility as virus news helps the bears, vaccine hope/speculation helps the bulls, and stimulus negotiations could go either way. Keep an eye on those FAANG stocks that have been the market’s “canary in the coalmine.” Remain focused on short-term charts and don’t chase, don’t predict, and always take profits as you go. Remember we are in earnings season now, so some surprises are likely to happen…plus usually every initial reaction is met with an “on second thought” re-reaction. So be nimble.

Ed

The Daily Swing Trade Ideas for today: CSCO, HD, GLD, AZN, OSTK, GPN, INTC, SLV, IAG. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday a slow and grinding day of price action with a little profit-taking after a mixed bag of earnings reports and higher than expected jobless numbers. That said, the indexes suffered little to no technical damage with the bulls fighting hard to defend against any attempt by the bears to start a selloff. The tech sector may experience some pressure today after NFLX disappointed investors after the bell yesterday. Infection numbers continue to set new records, but the market is unconcerned as they wait for the next round of stimulus spending.

Asian markets closed the trading week mixed but mostly higher amidst rising US-China tensions. European markets trade mixed this morning with an ever so slight advantage to the bulls. Here in the US, after smashing the new infection record and disappointing NFLX report, futures point to modestly bullish open ahead of earnings and economic data.

Economic Calendar

Earnings Calendar

On the Friday Earnings Calendar, we have 28 companies fessing up to their quarterly results. Notable reports include ALLY, BLK, CFG, KSU, FR, & STT.

News and Technical’s

Indexes found a few profit-takers yesterday after a mixed bag of earnings reports and Jobless Claims numbers higher than expected. The market was also dealing with a new record high in pandemic infections, but just one day later, that record was smashed with the number topping 77,000 yesterday. According to reports, the next congressional stimulus bill will cost 1.3 Trillion as written with several elected officials suggesting it needs to be substantially more. Netflix reported a miss after the bell yesterday with and expectation that subscribers will decline in the coming quarter. Share of Netflix fell as much as 10% in extended trading, which may add some pressure today on the high flying tech sector. This morning analysts expect a significant increase in housing starts as the 30-year mortgage fell briefly below 3% for the first time in history yesterday. We will also get a reading on Consumer Sentiment as well as several notable earnings reports that could move the market.

Yesterday mild round of profit-taking made for a slow grinding day of price action but little to no technical damage to the index charts. The tech sector has seen a bit of weakness this week, and it will be interesting to see if the miss from Netflix yesterday will continue that pressure today. There has been a notable increase in the consumer defensive and consumer staples stocks in the last few days. It would seem we are witnessing a rotation into better value dividend-paying issues as the interest in the high flying tech sector wains. There may be some concern that some of the current market leaders will have a difficult time supporting these high prices in their upcoming earnings reports. As we approach the weekend, consider carefully consider the risk as the pandemic infections surge and an uncertain earnings season ramps up to a fevered pitch.

Markets gapped down Thursday, maybe on virus fears, US-China worries or less than expected reduction in new jobless claims. After the gap, prices took a rollercoaster ride that ended up not far from where they opened. This gave us white-body candles that had faded the gap down but also had longer wicks (especially the DIA and QQQ), indicating a lot of indecision. There was also the beginnings of a rotation out of the massive tech names that have led for months with cyclical and staples names leading for the second straight day. The SPY closed down 0.31%, DIA down 0.51%, and QQQ down 0.68%. VXX also fell a bit to 31.72 and the T2122 4-week High/Low Ratio eased just a bit (but stayed deep in the overbought territory) to 94.97. 10-year bond yields also fell to 0.617% and Oil (WTI) pulled back slightly to $40.73/barrel.

After-hours the CDC extended the ban on cruises. The ban was scheduled to expire July 24 but has now been extended at least through September. NCLH, RCL, and CCL stock were hammered in post-market trading on the news.

The European Court of Justice canceled a US-EU data-sharing deal Thursday over fears that the US government will snoop on personal data. This means that either the US changes their data surveillance laws or US businesses will be forced to change their business operations and costs. For example, both tech giants and 2300 small businesses will now have to prevent all European data from flowing onto servers or networks located in the US. This would include communications on FB, TWTR, and GOOG. MSFT announced they would not be affected because they already use EU-written contracts guaranteeing privacy rather than contracts based on the US-EU Privacy Shield agreement which was annulled.

In a follow-on to the US-China relations story, Attorney Gen. Barr accused American tech giants of being pawns for China. In another example of “everyone’s out to get us,” his list of alleged conspirators against America included GOOG, MSFT, AAPL, CSCO, DIS, all of Hollywood, and the media. No sanctions or even threats of sanction was announced. However, the implication was that they have an investigative target on their back for their supposed transgressions. On another front, the US announced a travel ban for all Chinese Communist Party members and their families.

In the US, the virus numbers show we have 3,696,141 confirmed cases and 141,130 deaths. This includes 73,000 new cases nationally on the day. More states also joined the mask mandate bandwagon including AR, CO, and OH (partially). However, GA Governor Kemp decided to go the other way, by voiding all local mask mandates in his state and suing the Mayor of Atlanta for her mask mandate. At the same time, GA reported almost 3,500 new cases, which was trumped only by CA (4,600), TX (7,500), and FL (almost 14,000) new cases. Both TX and FL also recorded another record number of virus deaths Thursday.

Globally, the number of cases has reached 13,979,223 confirmed cases and 593,450 deaths. Brazil reported over 44,000 new cases and the largest number of deaths in a single day that they have had. India reported 36,000 new cases, also their largest daily total. In Europe, Spain reported the highest number of new cases since May 10th so they have retightened some restrictions. They are also slaughtering some 100,000 minks after dozens tested positive for Covid-19. In the UK, PM Johnson announced further easing as well as an additional $4 billion for their NHS in preparation for a second wave of infections.

Overnight, Asian markets were mixed, but mostly modestly green. In Europe, markets are also mixed and not far from break-even on either side. This is seen as largely due to the EU leaders meeting to negotiate on a stimulus measures, with some leaders saying they think there is less than a 50% chance of agreement on a plan. In the US, as of 7:30am futures are varied, but on the green side. The SPY and DIA are looking at modestly higher opens, However, the QQQ is pointing toward a gap-up of almost 1%.

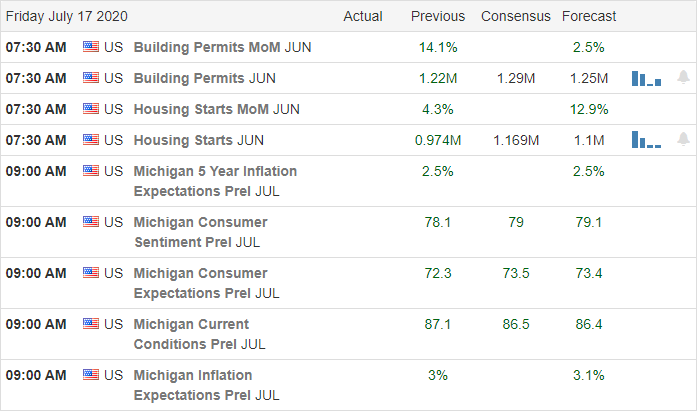

The major economic news for Friday includes June Building Permits and June Housing Starts (both at 8:30 am) and Michigan Consumer Sentiment (10 am). The major earnings reports on the day include ALLY, ALV, BLK, CFG, ERIC, HON, KSU, RF, STT, and VFC all before the open.

Thursday’s candles were indecisive if a bit on the red side of flat. It remains unclear whether the bulls or bears have the momentum coming out of yesterday’s session. Expect more volatility today and keep watching those FAANG stocks that are a good “canary in the coalmine” for the markets. Remain focused on short-term charts and don’t chase, don’t predict, and always take profits as you go. Remember we are in earnings season now, so some surprises are likely to happen…plus usually every initial reaction is met with a “on second thought” re-reaction. Also, don’t forget today is Friday. So don’t forget to take a paycheck in front of the weekend news cycle.

Ed

The Daily Swing Trade Ideas for today: BUD, VALE, HD, ABBV, KSS, JNJ, NVAX, AMGN, AZN. Trade your plan, take profits along the way, and smart. Also, don’t forget to check for upcoming earnings. Finally, remember that the stocks/ETFs we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service